Europe Insect Protein Market Size, Share, Trends & Growth Forecast Report - Segmented By Insect Type (Crickets, Black Soldier Fly Larvae (BSFL), Mealworms, Grasshoppers, Ants, Silkworms, Others), Form, Application, Source, End Use Industry, And Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic & Rest of Europe) - Industry Analysis (2026 to 2034)

Market Size, 2025

$0.19 BnMarket Estimate, 2026

$0.27 BnMarket Forecast, 2034

$5.39 BnCAGR, 2026–2034

44.80%Europe Insect Protein Market Size

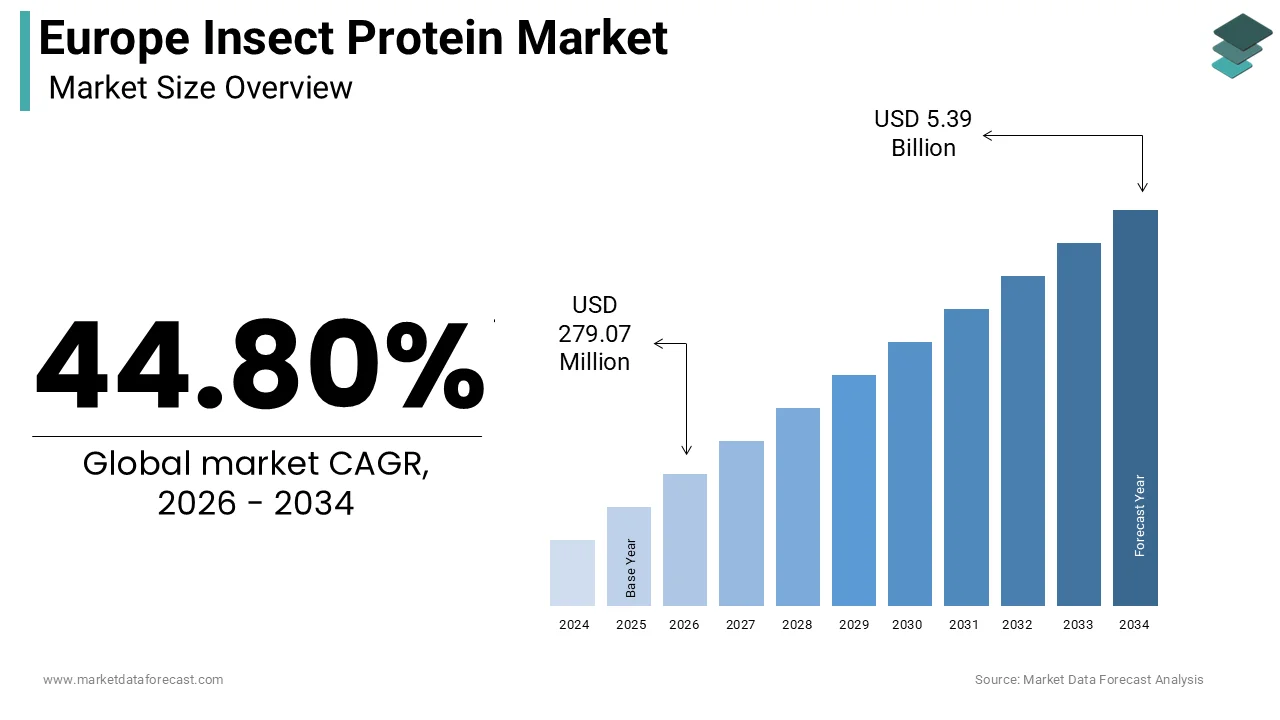

The insect protein market size in Europe was valued at USD 192.73 million in 2025. The European market is expected to grow at a CAGR of 44.80% from 2026 to 2034 and be valued at USD 5.39 billion by 2034 from USD 279.07 million in 2026.

The insect protein is an alternative protein focused on the production and utilization of protein derived from insects such as black soldier fly, mealworm, and crickets for animal feed, pet food, and increasingly human nutrition applications. Insect farming offers a low land use, high feed conversion efficiency, and significant greenhouse gas reduction compared to conventional livestock. The European Commission authorized the use of processed insect protein in poultry and pig feed in 2021 and in aquaculture feed as early as 2017, marking a regulatory turning point.

MARKET DRIVERS

Regulatory Approvals for Insect-Derived Feed in Livestock and Aquaculture Drive Commercial Adoption

The progressive authorization of insect protein in animal feed by European regulatory bodies is propelling the growth of the Europe insect protein market. As per the European Feed Manufacturers Federation, over 85 % of compound feed producers in Western Europe now include insect meal in at least one formulation for monogastric animals. The EU’s Farm to Fork Strategy explicitly encourages alternative proteins to reduce reliance on imported soy, which accounts for nearly 70 % of the bloc’s protein feed needs, as documented by the European Parliament Research Service.

Growing Demand for Sustainable Pet Food Ingredients Fuels Niche Market Penetration

The premium pet food is increasingly embracing insect protein as a novel hypoallergenic and environmentally sustainable ingredient with the shifting consumer preferences and brand innovation, which is bolstering the growth of the Europe insect protein market. According to the European Pet Food Industry Federation, over 85 million households in the European Union owned a pet in 2023, with premium and super premium pet food categories growing at 6.8% annually. Brands such as Yora in the United Kingdom and Greenspace in the Netherlands have launched dog and cat foods where black soldier fly meal replaces traditional poultry or beef protein, reducing the carbon paw print by up to 70 % as verified by life cycle assessments conducted by Wageningen University and Research Center. Regulatory clarity further supports this trend as the European Commission included insect protein in the updated Catalogue of Feed Materials in 2022, enabling transparent labeling.

MARKET RESTRAINTS

Consumer Skepticism and Cultural Aversion Limit Human Food Applications

The deep-rooted cultural aversion and consumer awareness are hampering the growth of the Europe insect protein market. According to a 2023 pan-European survey by the European Commission’s Joint Research Center, only 28% of respondents indicated willingness to consume food products containing insect ingredients even when assured of safety and nutritional equivalence. This reluctance is particularly pronounced in Southern and Eastern European countries, where entomophagy has no historical precedent. Furthermore, the inconsistent labeling practices and lack of standardized communication about processing methods exacerbate mistrust.

High Production Costs and Energy Intensity Undermine Price Competitiveness

The production costs and significant energy demands associated with controlled rearing environments are restricting the growth of the Europe insect protein market. According to a 2023 techno-economic analysis by the Technical University of Berlin, the average cost of producing one kilogram of black soldier fly meal in the European Union ranges from 3.80 to 5.20 euros, compared to 1.10 euros for soybean meal and 1.60 euros for fishmeal, as reported by the International Feed Industry Federation. Additionally, the lack of standardized automated harvesting and processing equipment increases labor dependency and reduces economies of scale.

MARKET OPPORTUNITIES

Integration into Circular Agri Food Systems Creates High Value Synergies

The alignment of insect farming with Europe’s circular economy objectives by converting low-value organic waste streams into high-quality protein and fertilizer is creating new opportunities for the growth of Europe's insect protein market. According to the European Environment Agency, the European Union generates over 88 million metric tons of food waste annually, with 30% originating from food processing and retail sectors. Companies like Ÿnsect in France and Protix in the Netherlands have established closed-loop facilities that source pre-consumer waste from supermarkets and breweries, then return frass, nutrient-rich excrement as organic fertilizer to local farms.

Expansion into Functional Ingredients and Nutraceuticals Opens Premium Revenue Streams

The extraction of functional bioactive compounds such as chitosan antimicrobial peptides and lauric acid for use in nutraceuticals, cosmetics, and pharmaceuticals is positively impacting the growth of the Europe insect protein market. According to the European Cosmetics Association insect insect-derived chitosan is gaining traction as a natural, biodegradable alternative to synthetic polymers in skincare formulations due to its film-forming and moisture retention properties. Companies like Entocube in Finland and NextProtein in France have developed proprietary extraction protocols to isolate these compounds at pharmaceutical-grade purity.

MARKET CHALLENGES

Fragmented Regulatory Framework Across Member States Delays Market Harmonization

The regulations for insect farming create significant disparities in national implementation, creating operational cross-border scalability, which is likely to challenge the growth of the Europe insect protein market. While Regulation EU 2017 893 permits the use of processed animal protein from insects in feed, he approval of input substrates such as catering waste or manure remains under the jurisdiction of individual member states. This fragmentation forces producers to maintain multiple production protocols and limits access to optimal low-cost feedstocks.

Limited Access to Specialized Feedstock and Supply Chain Infrastructure Constricts Scalability

The supply chain is hampered by inadequate infrastructure for consistent sourcing of approved organic substrates and distribution of finished products, which also hinders the growth of the Euthe rope insect protein market. According to Eurostat, less than 18% of post-harvest food processing waste in the European Union is segregated and made available for bioconversion as of 2023. Insect farms often compete with biogas plants and composting facilities for the same waste streams, driving up input costs. Additionally, there is a lack of standardized logistics networks for transporting live larvae or processed meal under temperature-controlled and hygienic conditions across regions.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 44.80% |

| Segments Covered | By Insect Type, Form, Source, End Use Industry, and Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, anthe d the Czech Republic |

| Market Leaders Profiled | InnovaFeed, HEXAFLY, Protix, Ynsect NL Nutrition & Health B.V., Jimini’s, Swarm Nutrition GmbH, AgriProtein Holdings Ltd, And Next Protein Inc. |

SEGMENTAL ANALYSIS

By Insect Type Insights

The black soldier fly larvae segment accounted holding 58.3% of the Europe insect protein market share in 2025. Black Soldier Fly Larvae dominated the European insect protein market due to their exceptional bioconversion efficiency, rapid life cycle, and regulatory approval for use in multiple feed applications. According to the European Food Safety Authority, BSFL can convert two kilograms of organic waste into one kilogram of biomass within 14 days under controlled conditions, making them a resource-efficient insect species for industrial rearing. Furthermore, BSFL, a frass, byproduct of rearing, is recognized as an organic fertilizer under EU Regulation 2019 1009, enhancing circularity. Companies like Ÿnsect in France and Protix in the Netherlands operate fully automated BSFL facilities producing over 20000 metric tons annually.

The mealworms segment is likely to grow with an expected CAGR of 18.3 % during the forecast period, with their approval for human consumption and versatility in food applications. The European Food Safety Authority authorized dried yellow mealworm as a novel food in January 2021, enabling its incorporation into bakery snacks and protein bars. Mealworms contain 54% crude protein and all nine essential amino acids, as verified by Wageningen University and Research Center, making them nutritionally comparable to beef. Startups such as Jimini’s in France and Bugfoundation in Germany have launched retail products featuring mealworm flour, capturing premium shelf space in organic supermarkets. Additionally, mealworm farming requires less vertical space than BSFL systems, allowing modular urban installations.

By Form Insights

The powdered segment held a dominant share of the Europe insect protein market in 2025. Powdered insect protein is the prevailing form in Europe owing to its functional adaptability on shelf li, and compatibility with existing manufacturing processes. In the food sector, powdered mealworm and cricket flour can be seamlessly incorporated into extrusion baking and blending operations without requiring capital retooling, as confirmed by the European Food Information Council. Furthermore, powdered form facilitates accurate dosing in pet food formulations where insect inclusion levels typically range from 5 to 15 % as documented by the European Pet Food Industry Federation.

The insect oil segment is expected to witness a CAGR of 21.6 % throughout the forecast period, due to the high concentration of lauric acid in Black Soldier Fly oil, which exhibits potent antimicrobial and anti-inflammatory properties. The European Cosmetics Association notes that over 35 new skincare products containing insect-derived oil were launched in the EU in 2023, targeting the natural and clean beauty segments. The oil extraction process also yields defatted protein meal, enhancing overall resource efficiency.

By Source Insights

The farmed insects segment was the largest and held a significant share of the Europe insect protein market in 2025. Farmed insects exclusively dominate the European market due to stringent biosecurity,ity hygiene, and traceability regulations that prohibit the commercial use of wild-harvested insects in food and feed. Regulation EU 2017 893 explicitly requires that insects used for protein production be reared under controlled conditions with documented feed inputs and health monitoring. Farmed systems ensure consistent protein content, moisture level,s nd absence of environmental contaminants such as heavy metals or pesticides, which are common in wild populations as documented by the Joint Research Center.

The farmed insects segment is lucratively growing with an anticipated CAGR of 16.8 % throughout the forecast period, with continuous technological advancements in vertical farming automation and waste integration. Innovations such as asAI-drivenn larval monitoring, robotic harvesting, and renewable energy-powered drying have reduced production costs by 22 % since 2020, as reported by the Technical University of Berlin. National policies further accelerate adoption with France’s Bioeconomy Strategy and the Netherlands’ Protein Delta initiative, providing grants for farmed insect infrastructure.

By End Use Industry Insights

The animal feed segment is lucratively to grow with a prominent share of the Europe insect protein market in 2025. The animal Feed segment is growing with the early regulatory approvals, strong economic rationale, and integration into existing supply chains. Major integrators like Hendrix Genetics and Skretting have signed multi-year offtake agreements with insect producers, ensuring stable demand. Furthermore, the EU’s Common Agricultural Policy incentivizes the use of locally produced alternative proteins through eco-scheme payments.

The Food and Beverage segment is expected to register a CAGR of 24.3% during the forecast period, with the novel food approvals for mealworms and crickets, and rising consumer interest in sustainable protein sources. Startups like Bugfoundation in Germany and Jimini’s in France have launched protein bars, pasta, and burger patties, achieving distribution in over 2000 organic and specialty stores across Western Europe, as per IRI retail tracking data.

REGIONAL ANALYSIS

France Market Analysis

France was the top performer of the Europe insect protein market with 26.3% of the share in 2025, with a proactive national policy, strong scientific infrastructure, and an early mover advantage in industrial scale production. France also leads in regulatory engagement, having submitted the first dossiers for mealworm and cricket novel food approval to the European Food Safety Authority. Over 45 licensed insect farms are operational across the country as per the French Agency for Environment and Occupational Health and Safety, reflecting a mature ecosystem.

Germany Market Analysis

Germany's insect protein market growth is likely to be driven by a robust industrial base, strong consumer awareness of sustainability, and active academic research. The Federal Ministry of Food and Agriculture reported that 28 insect production facilities were operational in 2023 with clusters in B,, Berlin, Varia, and North Rhine-Westphalia. Germany leads food-grade applications, with companies like Bug Foundation and Essento launching insect-based retail products available in major chains such as Edeka and dm dm drogerie. ss

United Kingdom Market Analysis

The United Kingdom insect protein market held 12.3% of the share in 2025. The Biotechnology and Biological Sciences Research Council has funded 12 insect protein projects since 2020, totaling 8.5 million pounds to advance strain selection and waste conversion efficiency. Although no longer bound by EU novel food regulations, the UK Food Standards Agency has maintained alignment by approving mealworms and crickets under its own framework, working to ensure market continuity. Startups benefit from incubators like the Center for Process Innovation, which provides support.

COMPETITION OVERVIEW

The Europe insect protein market features dynamic competition characterized by a blend of industrial-scale producers and agile technology startups vying for dominance through innovation, regulatory foresight, and circular integration. Large players like Ÿnsect and Protix dominate through capital-intensive facilities and established offtake agreements, while smaller firms differentiate via modular systems, niche applications, or regional waste valorization models. Competition is further shaped by the race to secure approvals for novel food uses and expand into high-margin segments such as cosmetics and nutraceuticals. The absence of standardized production protocols creates both opportunity and fragmentation as companies develop proprietary rearing and processing methods.

KEY MARKET PLAYERS

A few of the dominating players in the Europe insect protein market include

- InnovaFeed

- HEXAFLY

- Protix

- Ynsect NL Nutrition & Health B.V.

- Jimini’s

- Swarm Nutrition GmbH

- AgriProtein Holdings Ltd

- Next Protein Inc.

Top Strategies Used by the Key Market Participants

Key players in the Europe insect protein market pursue several strategic imperatives to enhance competitiveness and drive sector growth. Vertical integration from waste sourcing to protein and oil refining ensures cost control and supply chain resilience. Strategic partnerships with feed manufacturers, food bran, ds, and municipal waste operators secured long-term offtake agreements and feedstock access. Continuous investment in automation and AI-driven monitoring systems improves yield consistency and reduces labor dependency. Regulatory engagement through early dossier submissions to the European Food Safety Authority accelerates market entry for novel applications.

LEADING PLAYERS IN THE MARKET

Ynsect

Ynsect is a France-based global leader in insect protein production, specializing in Black Soldier Fly Larvae for animal feed and fertilizer applications. The company operates one of the world’s largest vertical insect farms in Amiens and supplies sustainable protein to aquaculture and pet food manufacturers across Europe and Asia. Ynsect has pioneered automated rearing systems that integrate artificial intelligence for climate and feeding control, enhancing efficiency and scalability. In 2023, the company secured regulatory approval for its frass as an organic fertilizer under EU standards and expanded its R and D collaboration with INRAE to optimize waste conversion ratios.

Protix

Protix, headquartered in the Netherlands, is a pioneer in insect bioconversion technology, transforming organic residue into high-quality proteins and lipids. The company’s flagship facility in Bergen op Zoom serves as a blueprint for circular production by sourcing pre-consumer waste and returning nutrient-rich frass to local agriculture. Protix supplies insect meal to major feed integrators, including Skrett, Ing, and has developed proprietary processing techniques to ensure consistent protein quality and safety. In 2023, Protix launched a dedicated pet food ingredient line and partnered with Rabobank to create a financing model for insect farming startups.

Entocube

Entocube, based in Finland, focuses on modular and scalable insect farming solutions with an emphasis on urban and decentralized production. The company provides turnkey insect rearing units to farms, restaurants, and municipalities, enabling on-site conversion of organic waste into protein and fertilizer. Entocube’s technology is designed for cold climates and integrates renewable energy sources to reduce operational costs. In 2023, it deployed pilot systems in Stockholm and Helsinki in collaboration with municipal waste authorities and launched a B2B platform for insect protein traceability.

MARKET SEGMENTATION

This research report on the European insect protein market has been segmented and sub-segmented based on the following categories.

By Insect Type

- Crickets

- Black Soldier Fly Larvae (BSFL)

- Mealworms

- Grasshoppers

- Ants

- Silkworms

- Others

By Form

- Powdered

- Oil

- Paste

- Others

By Application

- Animal Feed

- Aquaculture Feed

- Pet Food

- Poultry Feed

- Livestock Feed

- Human Consumption

- Food Ingredients

- Dietary Supplements

- Snacks and Bars

- Others

By Source

- Farmed Insects

- Wild Insects

By End-Use Industry

- Food & Beverage

- Animal Feed

- Pharmaceuticals

- Cosmetics

- Others

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

1. What is driving the growth of the Europe insect protein market?

Key drivers include increasing demand for sustainable protein, rising environmental concerns, the high nutritional value of insects, and growing adoption in animal feed and human food products.

2. Why is insect protein considered sustainable?

Insect farming requires less land, water, and feed compared to traditional livestock and produces lower greenhouse gas emissions, making it an eco-friendly protein source.

3. What are the main applications of insect protein in Europe?

It is widely used in animal feed (especially aquaculture and poultry), pet food, human food products, fertilizers, and even pharmaceuticals.

4. Which insect types are commonly used for protein?

Common insects include mealworms, crickets, black soldier flies, and locusts, which are rich in protein and essential nutrients.

5. Which insect species are approved in the EU?

Approved species include yellow mealworm, house cricket, migratory locust, and lesser mealworm, among others

6. What are the challenges in the Europe insect protein market?

Major challenges include consumer acceptance issues, regulatory complexities, high initial production costs, and limited large-scale processing infrastructure.

7. How fast is the Europe insect protein market growing?

The market is expected to grow at a CAGR of around 30–45% during the forecast period, indicating rapid expansion.

8. What role does regulation play in this market?

Regulation is critical, as insect-based products must pass safety assessments by authorities like EFSA before entering the market.

9. What is the future outlook of the Europe insect protein market?

The market is expected to grow rapidly due to rising investments, technological advancements, and increasing acceptance of alternative proteins.

10. What trends are shaping the Europe insect protein market?

Key trends include expansion into human food products, innovation in protein extraction technologies, partnerships between startups and food companies, and increasing use in pet food and aquaculture.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com