Europe Insulated Concrete Form Market Size, Share, Trends & Growth Forecast Report By Material Type, Application, End User, and By Country (Germany, France, United Kingdom, Sweden, Italy, Spain & Rest of Europe) – Industry Analysis and Forecast, 2026 to 2034

Europe Insulated Concrete Form (ICF) Market Summary

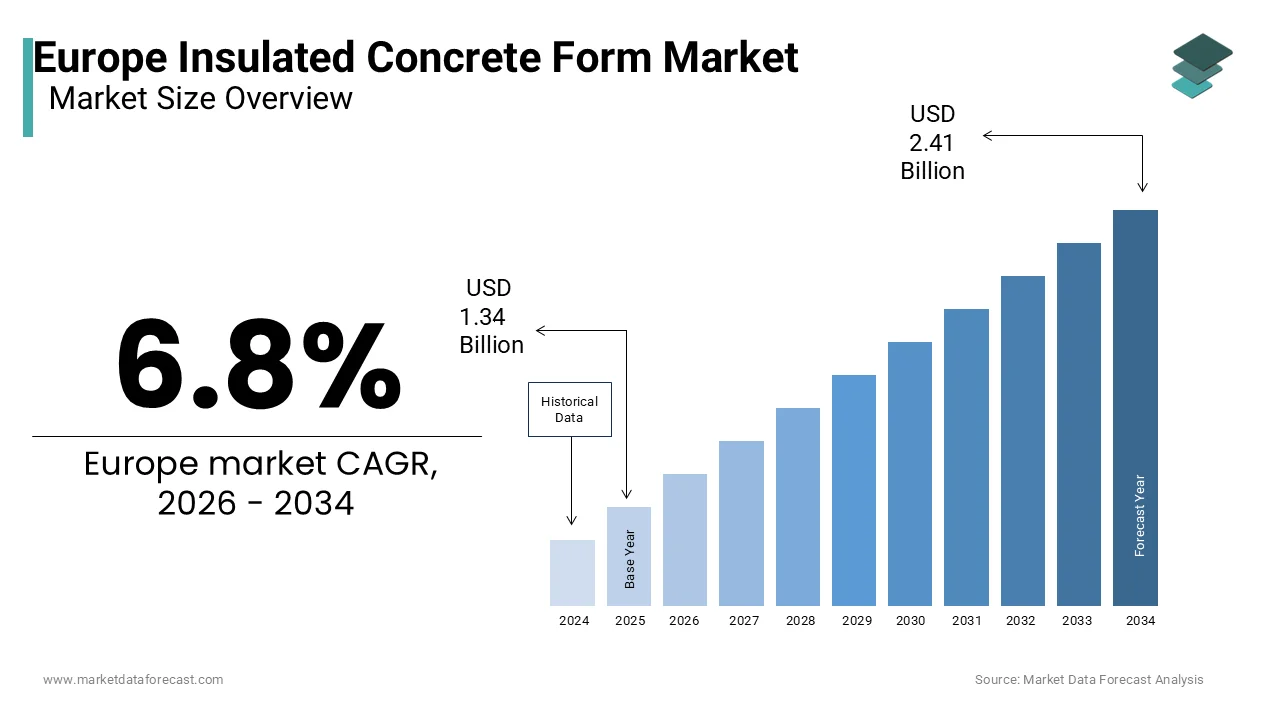

The europe insulated concrete form (ICF) market, valued at USD 1.34 billion in 2025, is projected to reach USD 2.41 billion by 2034, expanding at a CAGR of 6.8% driven by EU zero-emission building mandates, renovation wave programs, and rising adoption of high-performance wall systems.

Key Market Insights

- 2025 Market Size: USD 1.34 billion

- 2026 Estimate: USD 1.43 billion

- 2034 Forecast: USD 2.41 billion

- CAGR (2026–2034): 6.8%

- Base Year: 2025

- Forecast Period: 2026–2034

Quick Growth Drivers

- EU Energy Performance of Buildings Directive (EPBD) mandating zero-emission buildings

- Strong push from the European Green Deal Renovation Wave

- Rising adoption of passive house and low-carbon construction

- Severe construction labor shortages favoring faster wall systems

- Demand for multi-hazard resilient structures (fire, flood, seismic)

Principal Restraints

- Higher upfront costs compared to traditional masonry

- Limited ICF-trained installer base in Southern and Eastern Europe

- Fragmented access to financial incentives and subsidies

- Resistance from cost-driven public housing procurement

High-Value Opportunities

- Deep energy retrofits of pre-1970 urban buildings

- Integration into modular and prefabricated construction

- Rising use in institutional buildings (schools, hospitals, public offices)

- Structural + thermal upgrades in seismic-risk regions

Key Market Challenges

- Inconsistent fire-safety interpretations across EU member states

- Limited EPS recycling infrastructure, affecting circularity scores

- Fragmented national certification and approval pathways

- Low awareness among traditional contractors and developers

Fastest-Growing Segments

- Polyurethane Foam ICFs: 11.3% CAGR — thinner walls, urban efficiency

- Institutional Buildings: 9.7% CAGR — lifecycle cost prioritization

- Prefabricated & Modular Housing: rapid off-site assembly

Regional Leadership & Dynamics

- Germany (22.4%) — passive house leadership, strong subsidy framework

- France (18.6%) — RE2020 lifecycle carbon accounting

- United Kingdom — Future Homes Standard and deep retrofit demand

- Nordics (Sweden, Finland) — cold-climate performance and modular adoption

- Italy & Southern Europe — seismic safety and reconstruction-driven growth

What Wins Commercially

- Proven compliance with EPBD, passive house, and ZEB standards

- Integrated structure + insulation + air barrier systems

- Strong installer training and certification networks

- Compatibility with BIM, modular, and off-site workflows

Top Strategic Ask for Executives

Scale installer training, strengthen regulatory harmonization, and align ICF systems with retrofit and modular construction programs to unlock mass adoption across Europe’s zero-emission building transition.

Leading Players

Some of the companies that are playing a dominating role in the Europe insulated concrete form market include:

- Nudura Corporation

- Logix Insulated Concrete Forms

- Amvic Inc.

- Quad-Lock Building Systems

- BuildBlock Building Systems

- BASF SE

- Durisol

- RPM International

Europe Insulated Concrete Form Market Size

The europe insulated concrete form (ICF) market was valued at USD 1.34 billion in 2025, is estimated to reach USD 1.43 billion in 2026, and is projected to reach USD 2.41 billion by 2034, growing at a CAGR of 6.8% from 2026 to 2034.

Insulated Concrete Forms (ICF) are a high-performance building system using hollow, lightweight Expanded Polystyrene (EPS) foam blocks or panels that lock together like Lego bricks to create structural, cast-in-place concrete walls. These systems deliver high energy efficiency, structural resilience, and rapid construction timelines, aligning with Europe’s stringent building performance mandates. According to research, the majority of the European Union’s building stock was constructed before modern energy standards were implemented, resulting in high energy consumption for heating and cooling. The European Union requires all new construction projects to meet high energy-efficiency standards, commonly known as nearly zero-energy, which promotes the adoption of superior insulating building components. High-performance wall systems, including insulated concrete forms, are being utilized to significantly reduce thermal transmittance and enhance building efficiency. Besides, the European Green Deal’s Renovation Wave seeks to increase the pace of building retrofits, driving demand for innovative solutions that improve the thermal envelope of existing structures. National building codes in Germany, France, and the Nordic countries now explicitly recognize insulated concrete forms as compliant with passive house and low-carbon certification schemes. This confluence of regulatory stringency, climate ambition, and construction modernization positions insulated concrete forms as a critical enabler of Europe’s decarbonized built environment.

MARKET DRIVERS

Stringent EU Building Energy Efficiency Regulations Drive Adoption of High-Performance Envelopes

European Union policy frameworks have systematically elevated thermal performance from a design option to a legal requirement, which acts as a key driver of the European insulated concrete foam market. This shift has accelerated the deployment of ICFs across the region. The Energy Performance of Buildings Directive (recast 2024) mandates that all new buildings achieve zero-emission status (ZEB) by 2030 (public buildings by 2028), with primary energy demand thresholds varying by climate zone. As per European best practices, top-tier standards often translate to wall U-values of 0.15 W/m²K or lower levels readily achieved by insulated concrete forms (ICF) with standard 6-to-10-inch foam panels. In Germany, the GEG regulations strongly favor high-efficiency envelopes, making insulated concrete forms a strong choice for Passive House projects, which are part of a growing market for low-energy construction. Similarly, France’s RE2020 thermal regulation imposes dynamic carbon accounting over a building’s lifecycle, favoring materials with low embodied energy and high operational savings criteria where insulated concrete forms are increasingly used as an alternative to traditional masonry. National incentives further reinforce compliance, with various EU countries offering subsidies and low-interest loans for homes achieving the highest energy efficiency labels through advanced envelope systems. This regulatory architecture transforms insulated concrete forms from a niche product into a mainstream compliance tool across Europe’s new construction landscape.

Accelerated Construction Timelines Address Labor Shortages and Project Cost Pressures

The region’s construction sector faces chronic labor scarcity and rising wage costs, which make speed and simplicity critical selection criteria for building systems, and thereby fuel the expansion of the European insulated concrete foam market. Several European regions within the construction sector are facing a noticeable shortage of specialized workers for tasks such as masonry and concrete placement. Insulated concrete forms are being adopted as a method to address this labor scarcity by streamlining the wall construction process, potentially leading to faster assembly times for building envelopes with reduced reliance on highly skilled labor. This acceleration reduces crane rental, scaffold, ng aon-siteite labor costs while minimizing weather-related delays. In Sweden, where winter construction windows are narrow, a notable portion of modular housing developers specify insulated concrete forms to maintain year-round building schedules, as per sources. The system’s integration of structure insulation and air barrier in a single step further eliminates coordination between trades, thereby compressing project timelines and enhancing predictability in an increasingly volatile construction economy.

MARKET RESTRAINTS

High Initial Material Costs Deter Widespread Adoption inPrice-Sensitivee Segments.

The upfront cost of ICFs, despite lifecycle savings, remains a significant barrier to the European insulated concrete foam market. This is particularly true in publicly funded and low-margin housing projects across Southern and Eastern Europe. The initial investment for certain wall systems is consistently higher compared to traditional brick and block methods. In regions with restricted public construction budgets, these higher upfront costs can limit the consideration of alternative, energy-efficient building methods during the bidding process. Budgetary limitations for public residential projects frequently prioritize lower initial capital expenditures over long-term, lifecycle-oriented energy benefits. Traditional masonry continues to be the dominant choice for social housing, largely driven by constraints in upfront funding rather than a comparative analysis of long-term performance. Even in wealthier mmarkets contractors face client resistance when presenting higher initial quotes without immediate operational savings. National incentives for green buildings exist but are frequently hard to navigate, fragmented, or insufficient to cover actual cost differences. This financial friction prevents insulated concrete forms from achieving scale in volume housing segments where policy mandates are weak or enforcemis inconsistentiste,nt thereby limiting market penetration to premium or self-financed projects.

Limited Skilled Installer Base Restricts Execution Quality and Scalability

The successful implementation of ICFs requires specialized knowledge in bracing alignment, concrete pour sequencing, and thermal bridge detailing, which is not yet widespread among European construction crews, and this consequently impedes the expansion of the European insulated concrete foam market. Contractors in Southern European nations face significant challenges in securing qualified installers for specialized energy-efficient wall systems, driven by broader labour shortages in the construction industry. Improper installation, such as inadequate bracing during concrete placement or poor foam panel sealing, compromises structural integrity and thermal performance, leading to callbacks and reputational damage. Assessments of insulated concrete form structures in France have highlighted that improper installation techniques can lead to noticeable thermal weak points and gaps within the wall assembly. Training programs exist through manufacturers and industry associations b, but lack standardization across borders therebys limiting workforce mobility. Unlike conventional masonry walls, hich benefits from centuries of craft transmission, insulated concrete forms remain a relatively new system in many regions with fragmented certification pathways. Despite the technology's inherent technical merits, its reliability and scalability will remain restricted until installation competence is formally integrated into vocational curricula or mandatory certification programs.

MARKET OPPORTUNITIES

Retrofit Integration in Historic Urban Renovation Unlocks New Application Volumes

The region’s vast stock of aging urban buildings presents a significant opportunity for ICFs in deep energy retrofits, which is expected to propel the growth of theEuropeane insulated concrete foam market. This is especially true where structural upgrading and thermal enhancement are pursued simultaneously. According to sources, millions of buildings constructed before 1970 require comprehensive renovation under the Renovation Wave Strategy, with many exhibitinadequate load-bearingngng capacity for external insulation. Insulated concrete forms offer a solution by enabling internal wall lining that adds both thermal resistance and structural reinforcement without altering historic facades. Regional authorities have begun approving the use of insulated concrete form infill to enhance the energy performance of mid-century residential buildings while reinforcing aging masonry components. In areas susceptible to seismic activity, heritage oversight bodies are increasingly permitting these retrofits to improve the structural ductility and resilience of older properties. National financial frameworks for building efficiency have expanded their scope to recognize these systems as viable methods for simultaneous thermal and structural upgrades. This dual benefit of energy and structural upgrade positions insulated concrete forms as a strategic tool for Europe’s complex urban renewal agenda.

Modular and Prefabricated Construction Trends Favor Integrated Envelope Systems

The region’s shift toward off-site and industrialized construction creates ideal conditions for ICF adoption due to their compatibility with factory production rapid-sitetete assembly, which paves the way for fresh expansion possibilities in the European insulated concrete foam market. According to European housing market trends, the adoption of modular construction for new residential buildings has increased significantly as a solution to supply shortages and sustainability goals. Insulated concrete form panels are easily pre-cut, labelled, and shipped askits enabling precise factory coordination and minimal waste. Prefabricated housing manufacturers in Denmark are increasingly integrating insulated concrete forms into volumetric modules, allowing for nearly completed structures to be delivered to sites, which drastically lowers on-site labor requirements. The system’s monolithic concrete core also provides acoustic separation and fire resistance critifor multi-unitnitt developments. Finland’s environmental and building authorities support the use of highly insulated, concrete-based modular units to meet strict Nordic cold-climate standards, speeding up the adoption of these methods in social housing developments. This synergy between industrialized construction and high-performance envelopes positions insulated concrete forms as a foundational technology for Europe’s scalable low-carbon housing future.

MARKET CHALLENGES

Inconsistent Fire Safety Classification Across Member States Creates Regulatory Uncertainty

Many European countries impose additional national fire requirements, despite meeting Euroclass B s1 d0 ratings under EN 13501, that restrict or complicate ICF use in multi-story buildings, and therefore challenge the growth of the European insulated concrete foam market. Regulations in the United Kingdom regarding external walls on tall buildings have created ambiguity, leading to inconsistent interpretations of how insulated concrete forms are classified. Authorities in the United Kingdom have shown discrepancies in accepting certain insulated concrete forms for high-rise residential construction. Building codes in Austria require additional, specific fire safety measures for foam-based insulation systems, whicimpact thehe complexity and cost of construction. This regulatory fragmentation forces manufacturers to maintain multiple product variants and technical dossiers, increasing compliance overhead. This uncertainty discourages investment in multifamily insulated concrete form projects, particularly in dense urban markets where approval delays can derail financing.

Recycling Infrastructure Gaps Undermine Circular Economy Credentials

The end-of-life management of expanded polystyrene used in ICFs continues to be a significant environmental challenge to the European insulated concrete foam market. This is owing to lthe imited collection and reprocessing capacity across the region. Contamination with concrete, wood, or adhesives often renders construction-site polystyrene unsuitable for standard recycling processes, despite its theoretical recyclability. Post-construction polystyrene often experiences low recovery rates, with a significant portion of materials directed toward incineration or landfill. Select European countries have launched pilot programs for clean material streams, but a nationwide infrastructure is not yet fully in place. "Despite being recognized as a priority material within European construction waste management, Polystyrene (PS) recovery rates often fall short of established targets. This gap contradicts the EU Taxonomy’s requirement for sustainable construction products to demonstrate circularity. Manufacturers are investing in chemical recycling and ttake-backschemes but thremain small-scalelele. The lack of mature recycling markets and reverse logistics limits the use of insulated concrete forms in eco-conscious public works, even though they are highly energy-efficient during use.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Material Type, Application, End User, and Region. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, Rest of Europe |

| Market Leaders Profiled | Amvic Inc., BuildBlock Building Systems LLC, Fox Blocks (Owens Corning), Logix Insulated Concrete Forms Ltd, RPM International Inc., BASF SE, Airlite Plastics Company, Quad-Lock Building Systems Ltd, Nudura Corporation, LiteForm Technologies, Polycrete International, Durisol, SuperForm Products, Rastra, ConForm Global, KORE Insulated Forms, Sunbloc, Beco Products Ltd, Mikey Block Co.

|

SEGMENTAL ANALYSIS

By Material Type Insights

In 2025, the polystyrene foam segment held the majority share of Europe insulated concrete form market. The supremacy of the polystyrene foam segment is attributed to its ccost-effectivenessthermal performan,ce and established supply chain. Expanded polystyrene provides a combination of thermal insulation properties and material cost efficiency. This material allows manufacturers of insulated concrete forms to produce wall systems with high thermal resistance for cost-sensitive housing projects. A significant majority of insulated concrete form projects in Germany utilize polystyrene cores, benefiting from predictable performance and ease of processing in automated production systems. The material’s dimensional stability under load and moisture resistance further ensure long term insulation integrity without degradation. National energy certification schemes such as France’s CEPC and Sweden’s Miljöbyggnad recognize polystyrene-based systems as compliant with passive house standards without requiring supplementary insulation layers. This combination of economic accessibility, regulatory alignment, and field reliability solidifies polystyrene as the backbone of Europe’s insulated concrete form market. Polystyrene benefits from decades of use in construction and packaging, creating mature supply and processing ecosystems across Europe. Numerous specialized facilities within the European Union possess the technical capacity to manufacture precision insulation panels with high material efficiency. Clean production scrap is frequently reintegrated into the manufacturing process, which helps to decrease the reliance on raw materials. Initiatives in the Netherlands demonstrate that EPS waste from construction sites can be successfully recovered and reprocessed into new products. Despite persistent obstacles in the comprehensive recycling of post-consumer waste, targeted, local efforts are strengthening the recovery of polystyrAdditionallytiona,,lly major chemical suppliers like BASF and INEOS maintain regional pro duct,, ion hubs ensuring consistent quality and logistics responsiveness. This industrial maturity allows insulated concrete form producers to scale rapidly without material bottlenecks, a critical advantage over newer or less standardized alternatives in a market driven by project timelines and cost predictability.

The polyurethane foam segment is predicted to witness the highest CAGR of 11.3% during the forecast period, owing to superior performance in compact applications. Polyurethane foam provides superior thermal conductivity compared to polystyrene, allowing for thinner wall construction while maintaining necessary insulation performance. This thinner profile is advantageous in dense urban areas where maximizing floor area directly affects the value of a property. Shrinking plot sizes in major metropolitan areas are driving increased demand for building solutions that enhance space efficiency. In regions with strict regulations on building footprints, there is a noted preference for utilizing polyurethane cores in insulation projects to optimize interior space. Architects also favor the material’s smooth surface finish hichch reduces plaster thickness and improves aesthetic outcomes. This spatial efficiency transforms polyurethane from a premium option into a strategic design enahigh-density urbanityurban contexts. Polyurethane foam adheres more aggressively to concrete during pour creatingeating a monolithic composite wall with superior shear resistance and reduced risk of delamination. Research indicates that polyurethane-based insulated concrete forms demonstrate superior interfacial strength following long-term thermal cycling simulations compared to polystyrene alternatives. The material’s closed-cell structure helps reduce water vapor diffusion, which may minimize risks related to internal condensation in humid climates. Building regulations in certain regions, which require a long design life for new structures, have led to increased adoption of polyurethane-insulated concrete forms for below-grade applications. The performance characteristics of these materials are often considered for applications where structural integrity and moisture resistance are critical, particularly in premium construction segments. The use of these materials is experiencing growth in specific European markets.

By Application Insights

The residential segment dominated thEuropeanpe insulated concrete form market by accounting for a significant share in 2025. The leading position of the residential segment is driven by alignment and homeowner demand for energy autonomy. The European Union’s Energy Performance of Buildings Directive mandates that all new residential buildings transition from nearly zero energy consumption to a zero-emission standard, requiring extremely low energy consumption largely met by renewable sources, with specific, higher-efficiency requirements set by individual Member States tailored to their local climate conditions. Insulated concrete forms readily meet these thresholds through continuous insulation and airtight construction without requiring complex mechanical systems. Insulated concrete forms are increasingly utilized in certified high-efficiency single-family home construction within Germany. New environmental regulations in France emphasize lifecycle carbon assessment, whicemphasizessze the operational energy efficiency of concrete construction. Energy efficiency standards in the Netherlands encourage the use of building envelopes that promote high-performance energy ratings. Various European nations are employing regulatory and financial incentives to encourage the adoption of energy-efficient building metho..ds This regulatory architecture makes insulated concrete forms not optional but essential for compliance in the residential new build sector across Europe. European homeowners increasingly prioritize lifetime cost over price rice particularly as energy prices remain volatile. Prospective homebuyers are increasingly prioritizing the energy performance of residential properties. Buildings constructed with materials that offer high thermal mass are associated with higher valuation in specific European markets. Structures utilizing insulated concrete forms help maintain consistent indoor temperatures, reducing the need for active heating and cooling. The capacity for stable indoor environments is becoming a significant factor during periods of extremAdditionally,nally the monolithic concrete core offers superior sound insulation aresistanceistanceire res,istance enhancing livability and safety. In rural regions of Ireland, self-build is common, and insulated concrete form kits are favored for DIY compatibility and rapid enclosure. This blend of economic comfort and resilience ensures sustained residential demand beyond regulatory compulsion.

The institutional segment is estimated to register the fastest CAGR of 9.7% from 2026 to 2034 due to decarbonization mandates and lifecycle budgeting. European governments are legally bound to achieve carbon neutrality by with with0 w,, ith public buildings required to lead by example. Public procurement policies in Europe are increasingly prioritizing long-term operational efficiency over initial expenditures, encouraging the adoption of systems with low energy consumption. Educational authorities in the UK are incorporating specific structural systems for school construction to achieve reduced maintenance needs and enhanced environmental conditions within buildings. Health services in Sweden are approving particular building methods for medical facilities to leverage benefits in sound reduction and hygienic, solid wall construction. Administrative building projects in France are heavily utilizing specific envelope systems to meet higher environmental and energy performance certifications. This institutional shift toward whole life value rather than first cost creates a stable and growing pipelhigh-performance insulatednsulated concrete form applications. In regions prone to extreme weather or activity a ctivi,, ty insulated concrete forms offer structural advantages critical for public safety. Public infrastructure rebuilding efforts in Slovenia following recent flooding have incorporated insulated concrete forms, emphasizing the material's structural resistance to water damage and mold, aligning with updated reconstruction strategies. New municipal building construction in the Emilia Romagna region of Italy has adopted insulated concrete forms, driven by guidelines focused on enhancing structural ductility and improving resistance to collapse during seismic events. The use of insulated concrete forms in these European regions reflects a trend toward prioritizing materials that offer enhanced durability against specific, localized environmental risks. These construction choices indicate a shift in regional approaches to public facility development, prioritizing long-term resilience against natural hazards like flooding and earthquakes. The system’s rapid assembly also supports emergency housing needs with the Swiss Federal Office for Civil Protection deploying insulated form-based temporary clinics during alpine disaster responses. These functional imperatives, beyond energy, position insulated concrete forms as multi-hazardrd resilient solution for Europe’s evolving public building portfolio.

COUNTRY LEVEL ANALYSIS

Germany Insulated Concrete Form Market Analysis

Germany's European insulated concrete form market is expected to hold a 22.4% share in 2025. The dominance of the German market is propelled by its regulatory leadership and construction innovation. Stringent national energy regulations for new residential construction have driven a shift toward building methods that prioritize high thermal efficiency, such as insulated concrete forms. A significant portion of Europe's certified passive house structures are located in this region, with a high concentration of single-family projects utilizing insulated concrete forms. Large-scale housing entities are increasingly adopting insulated concrete forms for multi-family projects as a strategy to meet energy efficiency and cost targets. The widespread availability of specialized contractors helps ensure technical proficiency and quality in the execution of these building systems. Government-backed financial initiatives and loan programs help facilitate the adoption of these energy-efficient construction methods. This ecosystem of reglfancefinance,, finan,,ce and craftsmanship sustains Germany’s position as Europe’s most advanced and highest volume insulated concrete form market.

France Insulated Concrete Form Market Analysis

France was the second largest country in tEuropeanope insulated concrete foam market by capturing a 18.6% in 2025. The expansion of the French market is supported by dynamic carbon accounting and social housing modernization. Moreover, the French thermal regulation evaluates building projects based on both operational energy efficiency and embodied carbon impact over a building's lifespan. Also, the regulation's standards have influenced the adoption of specific building methods, such as insulated concrete forms, for various residential projects, including social housing initiatives. The insulated concrete form method is utilized for its combined characteristics of reduced operational energy demand and durable constructi..on Governmental financial support frameworks have been adapted to include incentives for new building projects that meet specific energy and carbon certifications. Prefabricated construction developers are integrating insulated concrete form systems into their portfolios, which affects construction time. Additionally, al l oftio, ally France’s seismic zones in the southeast mandate robust wall systems where insulated concrete forms provide both thermal and structural resilience,, public privatetion domains,ensurings France’s strong and expanding role in the market.

United Kingdom Insulated Concrete Form Market Analysis

The United Kingdom holds a significant position in thEuropeanpe insulated concrete foam market due to future homes standards and retrofit innovation. It is accelerating under the Future Homes S tanda, rd which will require new homes to produce less CO₂ than current levels. Insulated concrete forms are a primary compliance pathway due to inherent airtightness and thermal performance. The UK government continues to explore various methods and technologies for low-carbon new-build housing, with a focus on improving the energy efficiency of the overall housing stock, though progress in decarbonization has been insufficient to meet future targets. The system is also gaining traction in deep retrofits of post warestatesestatesing esta,tes where internal insulated concrete form linings upgrade both energy and structural performance without altering street facades. Driven by a commitment to improving housing quality and energy performance, Scotland continues to implement stringent energy standards aimed at achieving higher energy efficiency ratings for social housing stock in the coming years. Despite post-Grenfescrutinyiscr technolog,y non-combustible concrete core has secured technical approvals from the British Board of Agréofnt, enabling continued growth multi-storyory applications.

Sweden Insulated Concrete Form Market Analysis

Sweden held a promising share of the European insulated concrete foam market owing to extreme climate demands and industrialized construction. Sweden’s harsh winters and stringent energy codes make insulated concrete forms a natural fit for residential and public buildings. The material’s thermal mass stabilizes indoor temperatures during longcold periodss reducingng peak heating loads. Timber remains the primary construction material for new detached housing in Sweden, while energy-efficient concrete methods are adopted for specific, high-performance projects. The country’s leadership in modular construction further amplifies adoption, with firms like BoKlok integrating insulated concrete form,factory-built volumetric units. Additionally, Sweden’s national fossil-free construction prioritizes systems with low operational energy, even if embodied carbon is moderate. Insulated concrete forms are recognized as a compliant building material contributing to high-performance energy efficiency within the Swedish Green Building Council's comprehensive certification system. This climatic necessity, ty combined with industrialized building culture,ture ensures Sweden’s robust and growing insulated concrete form market.

Italy Insulated Concrete Form Market Analysis

Italy is predicted to register a notable CAGR in the European insulated concrete foam market over the forecast period due to seismic safety mandates and post disaster reconstruction. Its market is uniquely shaped by its high seismic risk, with a portion of the national territory classified as earthquake-prone. The National Technical Code for Construction explicitly recognizes insulated concrete forms as ductile wall systems that enhance building resilience, a critical factor after the 2016 Central Italy earthquakes. The reconstruction efforts in specific Italian regions have increasingly utilized insulated concrete forms for rebuilding public structures. This construction method has been implemented within a government-supported incentive program designed to facilitate renovations. The rise in energy poverty across the country has intensified the demand for residential buildings that offer improved heating efficiency. Houses constructed with these insulated forms are observed to significantly reduce energyconsumption duringe the uring winter months. Manufacturers like Tecnocreto have developed locally optimized systems with enhanced acoustic performance for dense urban settings. This dual imperative of safety and affordability positions Italy as a dynamic and policy-responsive market in Southern Europe.

COMPETITIVE LANDSCAPE

The European insulated concrete form market features a competitive landscape defined by technological differentiation, regulatory expertise,se and regional specialization rather than price alone. Competition centers on system perperformance structural robustness,, ess fire safety,y and ease of installation across varied climatic and seismic conditions. While global players like Nudura and Logix leverage standardized foam-based systems, sts such as Durisol and local manufacturers compete through alternative materials cement-bondedocement-bondeded composites that align with circular economy principles. The market is highly fragmented by national regulations requiring customized technical dossiers and testing protocols, which favors companies with strong local partnerships and certification agility. Public sector projects increasingly demand whole life carbon assessment,s giving an edge to firms with environmental product declarations and transparent supply chains. Innovation in digital integration, on BIM compatibility, and installer support further differentiates leaders from commodity suppliers. Despite modest overall size, ze the strategic importance of insulated concrete forms in achieving EU climate targets ensures intense focus on quality compliance and sustainability among participants across Europe.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the global europe insulated concrete form market include

- Amvic Inc.

- BuildBlock Building Systems LLC

- Fox Blocks (Owens Corning)

- Logix Insulated Concrete Forms Ltd

- RPM International Inc.

- BASF SE

- Airlite Plastics Company

- Quad-Lock Building Systems Ltd

- Nudura Corporation

- LiteForm Technologies

- Polycrete International

- Durisol

- SuperForm Products

- Rastra

- ConForm Global

- KORE Insulated Forms

- Sunbloc

- Beco Products Ltd

- Mikey Block Co.

TOP LEADING PLAYERS IN THE MARKET

- Nudura Corporation is a globally recognized innovator in insulated concrete form technology with a strong footprint across Europe through partnerships with local distributors and construction firms. The company specializes in expandable polystyrene-based interlocking formsbracing integrate braci, ng isult, insulation, and concrete placement into a single system. Nudura actively contributes to global building code development and sustainability certifications by providing extensive thermal and structural testing data. Its initiative strengthens its position as a solutions provider rather than just a material supplier in Europe’high-performancece construction landscape.

- Logix Insulated Concrete Forms Ltd, headquartered in Canada, da maintains a significant presence in Europeanrope market through its robust product portfolio and emphasis on fire and acoustic performance. The company’s forms are engineered to meet stringent European standards, ds including Euroclass fire ratings and passive house thermal requirements. Logix collaborates with European testing laboratories to validate system performance under regional climate and load conditions. The firm also enhanced its installer certification program across Southern Europe to ensure consistent quality and compliance with national building codes, es thereby reinforcing trust among contractors and public agencies.

- Durisol UK Ltd represents a distinct European approach by utilizing cement-bonded wood fiber blocks instead ofoam-baseded syste, ms offeringbio-basedsed alternative with excellent fire resistance and vapor permeability. The company supplies projects across the United Kingdom, Ireland, om Irela, nd and Benelux with a focus on sustainable pubbuildings,, gs schools alow-carbonbon housing. Durisol’s products are certified under leading European environmental labels, bels including Cradle to Cradle and BREEAM. This project exemplifies its strategy of aligning with institutional decarbonization mandates while promoting circular material use through locally sourced recycled wood fibers.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Key players in the European insulated concrete form market invest heavily in technical certification to comply with diverse national building codes and energy standards across member states. They develop digital design and estimation tools to integrate seamlessly into architects’ BIM workflows and accelerate specification. Companies prioritize installer training and certification programs to ensure consistent on-site quality and mitigate execution risks. Strategic partnerships with public housing agencies and modular construction firms secure long-term project pipelines. Additionally, manufacturers pursue material innovation such as bbio-basedcomposites or enhanced polystyrene formulations to address fire safety and circularity concerns while maintaining thermal performance.

MARKET SEGMENTATION

This research report on the europe insulated concrete form market is segmented and sub-segmented into the following categories.

By Material Type

- Polystyrene Foam

- Polyurethane Foam

By Application

- Residential

- Institutional

- Commercial

- Industrial

By End User

- Homeowners

- Government & Public Authorities

- Commercial Developers

- Industrial Facility Owners

By Country

- Germany

- France

- United Kingdom

- Sweden

- Italy

- Spain

- Rest of Europe

Frequently Asked Questions

1. Which segment dominates the Europe Insulated Concrete Form Market?

The residential segment leads the Europe Insulated Concrete Form Market, driven by building codes prioritizing energy efficiency and homeowner demand for cost savings. ICFs offer quick assembly and long-term insulation benefits. Commercial and institutional follow as sustainability pushes broader adoption in the Europe Insulated Concrete Form Market.

2. What are key drivers in the Europe Insulated Concrete Form Market?

Key drivers include EU Energy Performance of Buildings Directive (EPBD), NZEB mandates, and consumer focus on low-carbon homes in the Europe Insulated Concrete Form Market. Heat pump integration and renovation booms amplify demand. Climate resilience against extremes further propels growth.

3. What challenges face the Europe Insulated Concrete Form Market?

Challenges in the Europe Insulated Concrete Form Market involve higher initial costs versus traditional methods and need for skilled labor. Supply chain issues for foams persist. However, long-term savings and incentives mitigate these in the maturing Europe Insulated Concrete Form Market.

4. Who are major players in the Europe Insulated Concrete Form Market?

Leading players in the Europe Insulated Concrete Form Market include ICF Tech Ltd, Airlite Plastics (Fox Blocks), JACKON Insulation GmbH, IntegraSpec, and HIRSCH Servo AG. They innovate in foam tech and modular systems. Competition drives efficiency in the Europe Insulated Concrete Form Market.

5. How does Germany influence the Europe Insulated Concrete Form Market?

Germany spearheads the Europe Insulated Concrete Form Market with strict environmental rules and passive house popularity. Its manufacturing base and subsidies boost ICF for emissions reduction. This leadership inspires wider European adoption.

6. What benefits do ICFs offer in the Europe Insulated Concrete Form Market?

ICFs in the Europe Insulated Concrete Form Market deliver top thermal insulation, cutting energy bills by up to 50%, plus strength against earthquakes and storms. Faster builds reduce labor costs. Soundproofing suits urban areas.

7. What materials are used in the Europe Insulated Concrete Form Market?

Common materials in the Europe Insulated Concrete Form Market are polystyrene foam, polyurethane foam, cement-bonded wood fiber, and polystyrene beads. These provide durability and eco-friendliness. Innovations enhance recyclability.

8. How do regulations impact the Europe Insulated Concrete Form Market?

EU Green Deal and EPBD drive the Europe Insulated Concrete Form Market by mandating low-energy buildings. National policies in France and UK reward ICF use. Compliance boosts market penetration.

9. What is the forecast for the Europe Insulated Concrete Form Market to 2030?

The Europe Insulated Concrete Form Market eyes USD 2.6 billion by 2032, growing via sustainability trends. Edge computing and smart integrations expand uses. Steady CAGR persists.

10. Why is residential key in the Europe Insulated Concrete Form Market?

Residential rules on efficiency spike ICF demand in the Europe Insulated Concrete Form Market. Homeowners seek durable, low-maintenance walls. Sales forecasts show 7% yearly rises.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com