Europe Intelligent Building Market Size, Share, Trends, COVID-19 Impact & Growth Forecast Research Report, Segmented By Component, Type, End-User, and Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic and Rest of Europe), Industry Analysis From (2026 to 2034)

Market Size, 2025

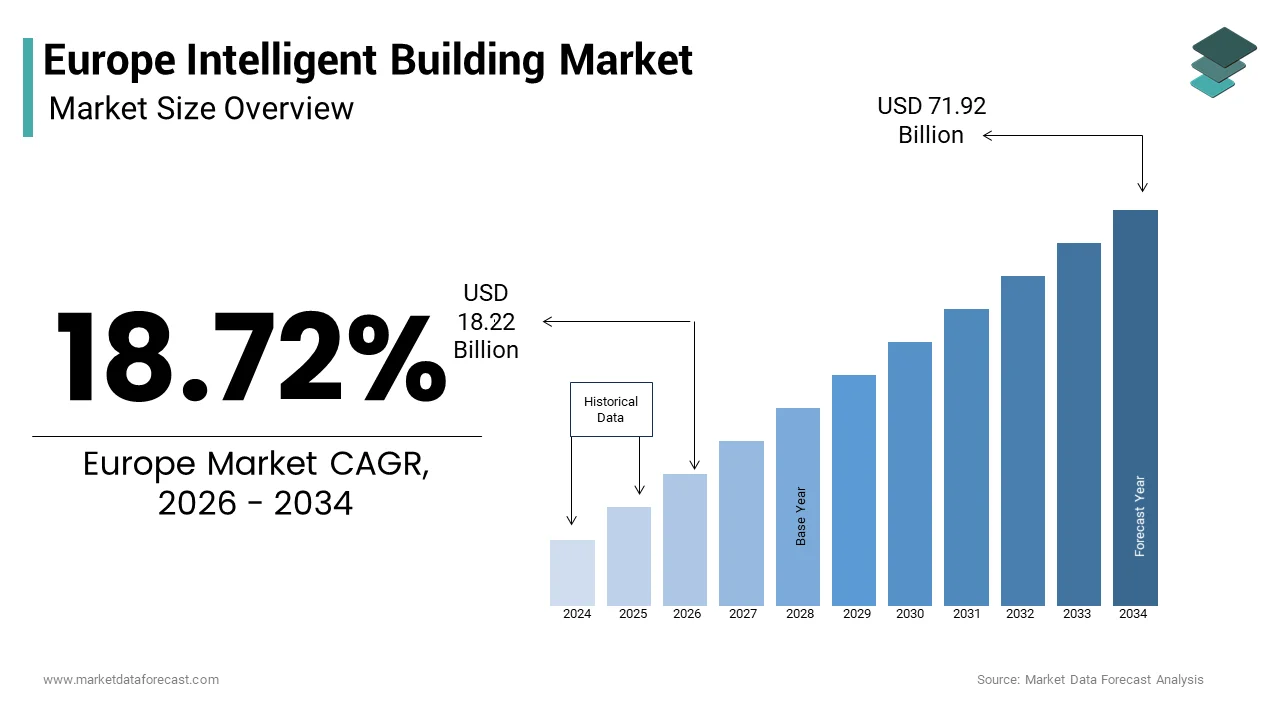

$15.35 BnMarket Estimate, 2026

$18.22 BnMarket Forecast, 2034

$71.92 BnCAGR, 2026–2034

18.72%Europe Intelligent Building Market Size

The Europe Intelligent Building Market size will reach USD 15.35 billion in 2025 and is anticipated to reach USD 18.22 billion by 2026 to reach USD 71.92 billion by 2034, growing at a CAGR of 18.72% during the forecast period from 2026 to 2034.

Current Market Definition and Operational Landscape

The intelligent building is an integrated advanced automation systems, Internet of Things sensors, and data analytics platforms to optimize operational efficiency, occupant comfort, and energy performance. These facilities utilize interconnected subsystems for heating, ventilation, air conditioning, lighting, security, and fire safety to create responsive environments that adapt to real time conditions. As per the European Commission, buildings account for 40% of total energy consumption and 36% of greenhouse gas emissions in the European Union, establishing the critical imperative for digital retrofitting. According to Eurostat, the renovation rate of existing building stock currently stands at approximately 1% annually, highlighting the vast potential for technological upgrades to meet the 2050 climate neutrality goals. The Energy Performance of Buildings Directive mandates that all new public buildings must be nearly zero energy buildings, driving the incorporation of smart management systems from the design phase. As per the International Energy Agency, digitalization in buildings could reduce global energy demand by 10% by 2040, a target that European policymakers actively pursue through regulatory frameworks. The European Green Deal aims to renovate 35 million buildings by 2030, creating a massive addressable market for intelligent infrastructure solutions. These contextual factors define the operational environment where intelligent building technologies serve as the primary mechanism for decarbonizing the built environment across the region.

MARKET DRIVERS

Regulatory Mandates for Energy Efficiency Accelerate Smart System Adoption

The regulatory mandates to adopt smart systems due to the stringent legal requirements imposed on property owners is solely accelerating the growth of Europe intelligent building market. The revised Energy Performance of Buildings Directive requires all member states to establish national building renovation plans that prioritize deep renovations supported by smart readiness indicators. According to the European Commission, the Smart Readiness Indicator framework evaluates the capacity of buildings to use information and communication technologies to adapt to occupant needs and optimize energy consumption, effectively making intelligence a compliance metric. As per national implementation data, countries like France and Germany have introduced penalties for non-compliant properties, forcing landlords to invest in automated building management systems to avoid financial sanctions. The EU Taxonomy for sustainable activities classifies building renovations that improve energy performance by at least 30% as sustainable investments, unlocking access to green financing instruments. Many commercial real estate owners in major European cities are accelerating retrofit projects to align with these regulatory timelines before enforcement deadlines arrive. The requirement for real time energy monitoring and reporting under new carbon disclosure regulations necessitates the deployment of granular sensor networks and analytics platforms. As per strategic assessments, the alignment of national building codes with EU level climate targets creates a uniform demand signal that transcends local market variations by ensuring sustained growth for vendors providing compliance oriented intelligent building solutions.

Corporate Sustainability Goals Drive Demand for Occupant Centric Technologies

The corporate sustainability goals, as multinational corporations and large enterprises seek to reduce their carbon footprints and enhance employee well-being is additionally gearing up the growth of Europe intelligent building market. Major tenants in the European commercial real estate sector increasingly demand LEED or BREEAM certified spaces that utilize smart systems to verify and report environmental performance metrics accurately. According to the World Green Building Council, net zero carbon buildings must be highly efficient and fully electrified, relying on intelligent controls to balance renewable energy generation with consumption patterns. The integration of occupancy sensors and air quality monitors allows facility managers to optimize space utilization and ensure healthy indoor environments, directly supporting post pandemic return to office strategies. According to research, buildings with certified smart features command rental premiums of up to 7% compared to conventional structures, providing a clear financial incentive for investment. The rise of Environmental Social and Governance criteria in investment decisions means that asset managers prioritize properties with demonstrable digital capabilities for tracking sustainability progress. As per research, the ability of intelligent systems to provide auditable data on energy savings and carbon reduction makes them indispensable for organizations striving to meet publicly announced climate pledges and satisfy shareholder expectations.

MARKET RESTRAINTS

High Initial Capital Expenditure Limits Retrofitting Feasibility

The high initial capital expenditure, as the cost of comprehensive system upgrades often exceeds the immediate budgetary capacity of property owners is limiting the growth of Europe intelligent building market. The installation of extensive sensor networks, upgraded controllers, and centralized management software requires substantial upfront investment that can deter owners of older building stock from initiating modernization projects. According to a study, a full scale intelligent building retrofit can cost between 15% and 25% of the total asset value by creating a significant financial barrier for small and medium sized enterprise landlords. As per economic assessments, the fragmentation of ownership in multi-tenant residential and commercial buildings complicates the decision making process, as individual stakeholders may be unwilling to contribute to shared infrastructure improvements without guaranteed returns. The long payback periods associated with energy efficiency projects, often ranging from 7 to 10 years, conflict with the shorter investment horizons preferred by many real estate funds and private equity firms. According to financial surveys, access to favorable financing remains limited for retrofit projects due to perceived risks regarding technology obsolescence and performance uncertainty. The complexity of integrating new smart systems with legacy mechanical and electrical infrastructure further inflates installation costs due to the need for specialized labor and custom engineering solutions.

Interoperability Fragmentation Hinders Seamless System Integration

The interoperability fragmentation with the widespread adoption of intelligent building solutions due to the proliferation of proprietary protocols and incompatible devices is attributed in degrading the growth of Europe intelligent building market. The lack of universal standards, forcing facility managers to navigate a complex sector of competing communication languages that prevent different subsystems from exchanging data effectively. As per a study, the reliance on vendor specific ecosystems locks building owners into single supplier relationships, reducing flexibility and increasing long term maintenance costs while stifling innovation. According to some reports, the difficulty in integrating legacy equipment with modern Internet of Things devices forces many owners to undertake costly rip and replace strategies instead of incremental upgrades. The emergence of new wireless standards adds another layer of complexity, as building managers struggle to determine, which technologies will remain viable over the 20 year lifespan typical of building infrastructure. As per expert opinions, this fragmentation increases the risk of project failure and reduces the realized value of intelligent building investments by causing hesitation among potential adopters who fear being stranded with obsolete or isolated systems that cannot evolve with future technological advancements.

MARKET OPPORTUNITIES

Digital Twins Enable Predictive Maintenance and Lifecycle Optimization

The digital twins by creating virtual replicas of physical assets that enable predictive maintenance and lifecycle optimization is substantially creating new opportunities for the growth of Europe intelligent building market. These dynamic models utilize real time data from sensors to simulate building performance under various scenarios, allowing facility managers to identify potential failures before they occur and optimize energy usage patterns proactively. According to research, the implementation of digital twin technology can reduce maintenance costs by up to 25% and extend the lifespan of critical building equipment by 10% through data driven intervention strategies. As per technological assessments, the ability to test retrofit scenarios in a virtual environment before physical implementation minimizes disruption to occupants and ensures that investment decisions are based on accurate performance projections. The European construction sector is increasingly adopting Building Information Modeling standards that facilitate the creation of high fidelity digital twins from the design phase through to operation. The integration of artificial intelligence with digital twins enables autonomous adjustment of building systems to maximize comfort and efficiency without human intervention.

Grid Interactive Efficient Buildings Unlock New Revenue Streams

The grid interactive efficient buildings by transforming static consumers into active participants in the energy ecosystem through demand response capabilities is additional factor to level up the growth of Europe intelligent building market. These smart structures utilize advanced automation to adjust their energy consumption in real time based on grid signals, electricity prices, and renewable energy availability, thereby generating revenue through flexibility services. The buildings equipped with smart thermostats, battery storage, and controllable loads can reduce peak demand charges by 20%, while earning incentives from utility providers for load shifting. The increasing penetration of intermittent renewable energy sources necessitates flexible demand to maintain grid stability, positioning intelligent buildings as infrastructure for the energy transition. According to pilot project results, commercial buildings participating in demand response programs in countries like Denmark and Germany have achieved return on investment periods of less than 5 years solely through energy arbitrage and grid services. The integration of electric vehicle charging infrastructure within intelligent buildings further enhances their grid interaction potential by managing charging loads to align with surplus solar or wind generation.

MARKET CHALLENGES

Cybersecurity Vulnerabilities Threaten Operational Integrity

The cybersecurity vulnerabilities, as the emergence of operational technology and information technology expands the attack surface for malicious actors is one of the major challenges for the growth of Europe intelligent building market. The proliferation of connected devices and remote access capabilities in smart buildings creates numerous entry points for cyberattacks that can compromise occupant safety, data privacy, and critical infrastructure operations. According to security research, the average number of connected devices per intelligent building has surpassed 1000, with many lacking basic security features such as encryption or secure authentication mechanisms. As per reports, ransomware attacks targeting building management systems have increased by 40% in the last two years, disrupting heating and cooling operations and holding sensitive tenant data hostage. The legacy nature of many building automation protocols means they were designed without security considerations by making them inherently susceptible to exploitation when exposed to internet connected networks. According to regulatory guidance, the NIS2 Directive imposes strict cybersecurity obligations on essential entities including large building operators, requiring comprehensive risk management measures that many facility managers are ill equipped to implement. The shortage of professionals skilled in both building operations and cybersecurity exacerbates the problem, leaving many intelligent buildings inadequately defended against sophisticated threats. As per industry warnings, a successful cyberattack on a critical building system could result in physical harm or significant financial loss by creating liability concerns that may slow the adoption of highly connected intelligent solutions until robust security standards are universally enforced and verified.

Data Privacy Concerns Complicate Occupant Monitoring Deployment

Data privacy concerns, as the deployment of granular sensors raises ethical and legal questions regarding occupant surveillance and data usage is another factor hampering the growth of Europe intelligent building market. The collection of detailed information on movement patterns, room occupancy, and even biometric data to optimize building performance conflicts with the strict privacy protections enshrined in the General Data Protection Regulation. The building operators must navigate complex consent requirements to legally process personal data captured by smart cameras and presence detectors that often limiting the scope of data available for optimization algorithms. The requirement for data minimization under GDPR forces vendors to design systems that collect only strictly necessary information by potentially reducing the effectiveness of advanced analytics that thrive on large datasets. The ambiguity surrounding the classification of certain building data as personal or anonymous creates legal uncertainty that hinders innovation and investment in monitoring technologies. The need for transparent data governance frameworks and robust anonymization techniques adds complexity and cost to intelligent building deployments.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 18.72% |

| Segments Covered | By Component, Type, End-user, and Country |

| Various Analyses Covered | Global, Regional, and Country Level Analysis, Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities. |

| Regions Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, and the Rest of Europe |

| Market Leaders Profiled | Abb Ltd., Siemens Ag, Cisco Systems, Inc., Honeywell International Inc., Legrand, Johnson Controls, United Technologies Corporation, Delta Controls, Schneider Electric, Intel Corporation |

SEGMENTAL ANALYSIS

By Component Insights

The hardware segment was the largest by holding a prominent share of the Europe intelligent building market in 2025 owing to the fundamental necessity of physical infrastructure to enable any form of digital intelligence within a structure. The deployment of sensors, actuators, controllers, and smart meters constitutes the foundational layer upon which all software and service capabilities rely. According to the International Energy Agency, the installation of over 500 million smart sensors across European commercial buildings is required by 2030 to meet basic energy efficiency targets, creating massive volume demand for hardware components. As per Eurostat data, the renovation wave initiative mandates the replacement of legacy heating and cooling controls with smart thermostats and variable frequency drives in millions of existing units, directly fueling hardware sales. The physical nature of these upgrades means that every intelligent building project begins with substantial capital expenditure on devices before software licensing or maintenance contracts become relevant. The shift toward wireless sensor networks reduces installation complexity but increases the unit count of devices required per square meter, sustaining high hardware volumes.

The software segment is likely to witness a fastest CAGR of 16.4% throughout the forecast period owing to the increasing reliance on data analytics, artificial intelligence, and cloud based management platforms to extract value from the installed hardware base. According to McKinsey, advanced building management software can reduce energy consumption by an additional 15% beyond what hardware automation alone achieves, driving strong demand for intelligent algorithms. The integration of digital twin technology requires sophisticated simulation software that continuously updates based on real time sensor data, a capability that is becoming standard in new constructions. According to the European Commission, the Smart Readiness Indicator framework encourages the adoption of software capable of self-learning and adaptive control, pushing owners to upgrade their digital stacks regularly. The need for cybersecurity patches and compliance updates under the NIS2 Directive forces continuous software evolution by ensuring sustained spending cycles. As per industry reports, the ability of software to integrate disparate subsystems into a unified dashboard addresses the critical pain point of fragmentation, making it a high priority investment for facility managers. This shift from static control to dynamic optimization positions software as the primary engine of future market expansion.

By Type Insights

The Building Energy Management System segment was the largest by capturing 35.4% of the Europe intelligent building market share in 2025 with the urgent regulatory and economic imperative to reduce energy consumption and carbon emissions in the built environment. The Energy Performance of Buildings Directive mandates strict energy efficiency standards that can only be met through sophisticated monitoring and control of heating, ventilation, air conditioning, and lighting loads. According to the European Commission, buildings are responsible for 40% of energy consumption in the EU, making energy management the primary focus of any intelligent building strategy. As per data, the implementation of advanced energy management systems can yield energy savings of up to 30% in commercial properties by providing a clear and rapid return on investment that drives adoption. The volatility of electricity prices in Europe following recent geopolitical events has heightened the focus on demand response and load shifting capabilities inherent in these systems. According to strategic assessments, the requirement for real time carbon reporting under the Corporate Sustainability Reporting Directive necessitates granular energy data collection that only specialized management platforms can provide. The integration of renewable energy sources such as solar photovoltaics and battery storage further complicates building operations, requiring intelligent software to balance generation and consumption dynamically.

The intelligent security system segment is projected to register a fastest CAGR of 17.2% from 2026 to 2034. The emergence of physical security and cyber security needs, alongside the demand for integrated safety solutions that leverage artificial intelligence and video analytics. The adoption of AI powered video surveillance capable of detecting anomalies, unauthorized access, and potential safety hazards in real time is surging across European corporate campuses and public facilities. As per regulatory developments, the updated NIS2 Directive classifies large commercial buildings as essential entities requiring robust security postures, compelling owners to upgrade from passive monitoring to active intelligent defense systems. The integration of biometric access control and facial recognition technologies, while subject to privacy debates, is gaining traction in high security zones due to their superior accuracy and convenience. The ability of modern security systems to integrate with fire detection and emergency evacuation protocols creates a holistic safety ecosystem that appeals to risk conscious facility managers. The rise of remote work and hybrid office models has increased the need for flexible access management solutions that can be controlled digitally from anywhere.

By End User Insights

The commercial segment held 55.4% of the Europe intelligent building market share in 2025 owing to the intense pressure on office buildings, retail spaces, and hospitality venues to optimize operational costs and enhance tenant experiences in a competitive real estate landscape. According to the European Real Estate Society, commercial property owners face increasing demands from institutional investors to demonstrate Environmental Social and Governance compliance, which heavily relies on intelligent building certifications. The multinational corporations in Europe, now require their leased offices to have smart building capabilities to support their own net zero commitments, driving landlords to invest aggressively in automation. The high density of occupants in commercial structures maximizes the value proposition of intelligent systems for space utilization, air quality monitoring, and energy management. The potential for operational expense reduction in commercial buildings through smart technologies can reach 20% annually, a significant margin that justifies substantial upfront capital expenditure, as per research. The complexity of managing diverse systems in large shopping malls and skyscrapers necessitates centralized intelligent platforms that can coordinate thousands of devices simultaneously. The rise of "Building as a Service" models in the commercial sector allows owners to monetize data and flexibility services by creating new revenue streams that are only accessible through advanced intelligent infrastructure.

The residential segment is esteemed to witness a fastest CAGR of 18.5% throughout the forecast period owing to the rising consumer awareness of energy costs, the proliferation of affordable smart home devices, and supportive government policies for residential retrofitting. According to Eurostat, household energy prices in Europe have seen significant volatility, prompting homeowners to adopt smart thermostats, intelligent lighting, and automated shading systems to manage consumption actively. As per the European Green Deal, specific funding mechanisms and subsidies are being directed toward individual households to encourage the installation of smart energy management solutions as part of the renovation wave. The integration of electric vehicle charging stations within private homes requires intelligent load management software to prevent grid overload, further stimulating market growth. According to the survey, the price of smart speakers and connected hubs has dropped below 50 euros, which is making entry level intelligent home ecosystems accessible to the mass market. The growing preference for remote monitoring of home security and elderly care applications among the aging European population adds another layer of demand. The development of interoperable standards like Matter is reducing compatibility fears, encouraging consumers to mix and match devices from different vendors.

COUNTRY ANALYSIS

Germany Intelligent Building Market Analysis

Germany was the top performer of the Europe intelligent building market by holding 24.3% of share in 2025 due to its robust manufacturing base and stringent energy regulations. The country's market status is defined by a strong emphasis on industrial grade building automation and deep energy retrofits driven by the Building Energy Act. According to the German Federal Ministry for Economic Affairs and Climate Action, the sector is mandated to reduce primary energy consumption in buildings by 65% by 2030, creating a massive pipeline for intelligent control systems. As per industry data, Germany hosts the highest concentration of smart factory and logistics center projects in the region, which require sophisticated infrastructure management systems to operate efficiently. The presence of leading global automation vendors headquartered in Germany fosters a local ecosystem of innovation and early adoption of cutting-edge technologies. According to study, the "Efficiency House" certification program provides low interest loans for residential projects that integrate smart monitoring, accelerating uptake in the housing sector. The country's strong engineering culture ensures that intelligent building deployments prioritize reliability and technical depth over mere aesthetic features.

United Kingdom Intelligent Building Market Analysis

The United Kingdom intelligent building market was positioned second by holding 19.3% of share in 2025 with the smart city initiatives and advanced service integration. According to the UK Green Building Council, the commitment to achieve net zero carbon buildings by 2030 has spurred a wave of retrofits focusing on digital twins and predictive maintenance tools. As per government data, the "Smart Places" program funds pilot projects that integrate intelligent building data with wider urban infrastructure by creating unique opportunities for system interoperability. The financial services sector in London demands premium smart office environments to attract top talent, which is driving investment in occupant experience technologies like app based access and personalized climate control. According to research, the UK leads Europe in the deployment of cybersecurity measures for building systems, reflecting heightened awareness of digital risks. The strong presence of proptech startups in cities like Manchester and Bristol introduces disruptive business models that challenge traditional incumbents.

France Intelligent Building Market Analysis

France intelligent building market growth is steadily growing at a fastest CAGR in coming years with the aggressive state led renovation programs and a focus on social housing modernization. The market status is defined by the "MaPrimeRénov" scheme, which provides substantial grants for homeowners to install smart heating controls and energy monitoring systems. According to the French Ministry of Ecological Transition, the goal to renovate 700000 homes annually includes specific bonuses for installing connected thermostats and smart vents, directly boosting the residential segment. The large stock of social housing managed by public entities is undergoing systematic digital upgrades to reduce energy bills for tenants and meet national climate targets. The centralization of energy policy in France allows for rapid scaling of standardized intelligent solutions across vast portfolios of public buildings.

Italy Intelligent Building Market Analysis

Italy intelligent building market growth is likely to grow with the opportunity of integrating intelligent technologies into historic and heritage buildings. The growing trend, where smart systems are used to preserve architectural integrity, while improving energy performance in centuries old structures. According to the Italian National Agency for New Technologies, Energy and Sustainable Economic Development, specific guidelines have been developed for non-invasive installation of sensors and wireless controls in protected monuments, opening a niche market segment. The seismic activity in certain regions drives demand for intelligent structural health monitoring systems that can detect building stress in real time. The "Superbonus 110%" tax incentive, although modified, initially sparked a massive wave of building upgrades including smart automation, the effects of which continue to ripple through the market. The fragmented nature of property ownership in Italy, favors wireless and battery operated intelligent solutions that require minimal construction work.

Netherlands Intelligent Building Market Analysis

The Netherlands intelligent building market growth is likely to be driven by its role as a testing ground for circular economy principles and highly sustainable intelligent building concepts. The market status is defined by the widespread adoption of "cradle to cradle" certified buildings that rely on intelligent systems to track material flows and energy loops. According to the Dutch Green Building Council, the country aims to have a fully circular economy by 2050, driving demand for smart meters and tracking software that monitor resource usage with extreme precision. As per urban planning data, cities like Amsterdam and Rotterdam are implementing district level energy management systems where multiple buildings share resources via intelligent grids. The high density of the Dutch population and limited land availability encourage the construction of multi-functional smart complexes that require advanced infrastructure management to operate efficiently. The Netherlands leads Europe in the integration of smart water management systems within buildings to handle flood risks and optimize rainwater harvesting. The strong digital literacy of the Dutch population accelerates the acceptance of user facing smart home interfaces and community energy trading platforms. The collaborative culture in the Dutch construction sector fosters open standards and data sharing, reducing fragmentation and speeding up innovation cycles.

COMPETITIVE LANDSCAPE

The competition in the Europe intelligent building market is characterized by intense rivalry between established industrial conglomerates and agile technology startups specializing in niche software solutions. Incumbent giants leverage their broad hardware portfolios and deep installation networks to offer integrated end to end systems that appeal to large scale developers and government entities. Meanwhile specialized software firms differentiate themselves through superior user experience and advanced artificial intelligence algorithms that deliver precise energy savings and predictive maintenance capabilities. Regulatory complexity acts as a significant barrier to entry favoring vendors with proven track records in navigating stringent European energy and data privacy laws. Customer switching costs remain high due to the critical nature of building infrastructure yet the push for decarbonization drives carriers to evaluate modern cloud alternatives aggressively. This dynamic environment fosters continuous innovation as competitors strive to deliver measurable sustainability gains and enhanced occupant experiences to secure long term contracts in a rapidly maturing digital landscape.

KEY MARKET PLAYERS

A Few of the market players that are dominating the Europe intelligent building market are

- Abb Ltd.

- Siemens Ag

- Cisco Systems, Inc.

- Honeywell International Inc.

- Legrand

- Johnson Controls

- United Technologies Corporation

- Delta Controls

- Schneider Electric

- Intel Corporation

Top Players In The Market

- Siemens AG stands as a global leader in building technologies, providing comprehensive solutions that integrate heating, ventilation, air conditioning, and security systems into unified intelligent platforms. Siemens, recently launched enhanced artificial intelligence capabilities within its building operating system to predict maintenance needs and automate energy savings dynamically. Their commitment to open standards facilitates interoperability with third party devices by addressing a critical industry pain point. Globally the firm leverages its extensive industrial automation expertise to scale smart building solutions for major metropolitan projects. These strategic initiatives reinforce their position as a primary enabler of sustainable and efficient urban environments worldwide.

- Schneider Electric delivers innovative energy management and automation solutions that empower buildings to achieve net zero carbon goals through advanced digital services. The company dominates the European landscape with its EcoStruxure Building platform which connects disparate subsystems to provide real time visibility and control over energy consumption. Schneider Electric recently expanded its software portfolio by acquiring specialized analytics firms to enhance predictive maintenance and occupant comfort features. Their global contribution includes setting industry benchmarks for sustainability through circular economy principles applied to product design and lifecycle management. The firm actively collaborates with utility providers to enable demand response programs that turn buildings into flexible grid assets. These continuous innovations and strategic partnerships solidify their role as a pivotal partner for owners seeking to future proof their real estate assets against evolving environmental regulations.

- Honeywell International offers a robust suite of intelligent building technologies that optimize operational efficiency, safety, and productivity for commercial and industrial facilities across Europe. The company utilizes its Forge digital platform to aggregate data from building systems and apply advanced analytics for actionable insights into energy usage and space utilization. Honeywell recently introduced new generative artificial intelligence tools designed to simplify facility management tasks and improve decision making speeds for operators. Their global impact is evident in the widespread deployment of their connected safety solutions which protect occupants while ensuring regulatory compliance. The firm strengthens its market position by forming strategic alliances with major construction companies to embed smart technologies during the initial design phase of new developments. These efforts ensure they remain at the forefront of the transition toward autonomous and sustainable building operations globally.

Top Strategies Used By Key Market Participants

Key players in the Europe intelligent building market primarily utilize strategic acquisitions to rapidly acquire specialized technologies such as artificial intelligence analytics and cybersecurity capabilities. Companies frequently form extensive partnerships with cloud infrastructure providers to ensure scalable and secure data hosting for their building management platforms. Another dominant strategy involves heavy investment in research and development to create open architecture systems that guarantee interoperability among diverse devices and protocols. Vendors actively pursue certifications for sustainability and energy efficiency to align their products with strict European regulatory frameworks and attract environmentally conscious clients. Product localization remains crucial as firms adapt their software interfaces and compliance modules to meet specific national laws and language requirements across the region. Additionally, companies focus on developing subscription based service models to generate recurring revenue streams and deepen long term customer relationships. These combined approaches enable market leaders to maintain competitive advantages and effectively address the complex evolving needs of European building owners and operators.

MARKET SEGMENTATION

This research report on the Europe intelligent building market is segmented and sub-segmented into the following categories.

By Component

- Hardware

- Software

- Services

By Type

- Intelligent Security System

- Building Energy Management System

- Infrastructure Management System

- Network Management System

By End-User

- Commercial

- Industrial

- Residential

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

How do intelligent building systems improve building operations?

They integrate automation technologies to manage lighting, security, energy, and climate control more efficiently.

What factors are driving the growth of the intelligent building market in Europe?

Rising focus on energy efficiency, smart infrastructure, and sustainable construction is accelerating market growth.

Which technologies are commonly used in intelligent buildings?

Technologies such as IoT sensors, building management systems, and automated energy control platforms are widely used.

Why are intelligent buildings becoming important in modern urban development?

They help optimize resource usage, reduce operational costs, and improve occupant comfort.

Which sectors are adopting intelligent building solutions in Europe?

Commercial offices, residential complexes, healthcare facilities, and educational institutions are key adopters.

How do intelligent buildings support energy management?

They monitor and control energy consumption through automated systems that adjust usage based on real-time needs.

What challenges affect the intelligent building market in Europe?

High initial installation costs and system integration complexity can slow adoption.

How is digital transformation influencing intelligent building technologies?

Advancements in connectivity and data analytics are enabling smarter and more responsive building systems.

Which European countries are leading the adoption of intelligent building solutions?

Germany, the United Kingdom, France, and the Netherlands are major markets due to their advanced infrastructure projects.

What future trend is expected in the Europe intelligent building market?

Increasing integration of AI-driven building management and smart city initiatives is expected to drive future growth.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com