Europe Lipase Market Segmented By Source (Microbial Lipases, Plant Lipases, Animal Lipases), Application (Animal Feed, Dairy, Bakery, Confectionery, Others), Functions (Frozen Food And Beverage Additives And Food And Beverage Texturants), And Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic and Rest of Europe) – Size, Share, Trends, Growth, Forecast (2026 to 2034)

Market Size, 2025

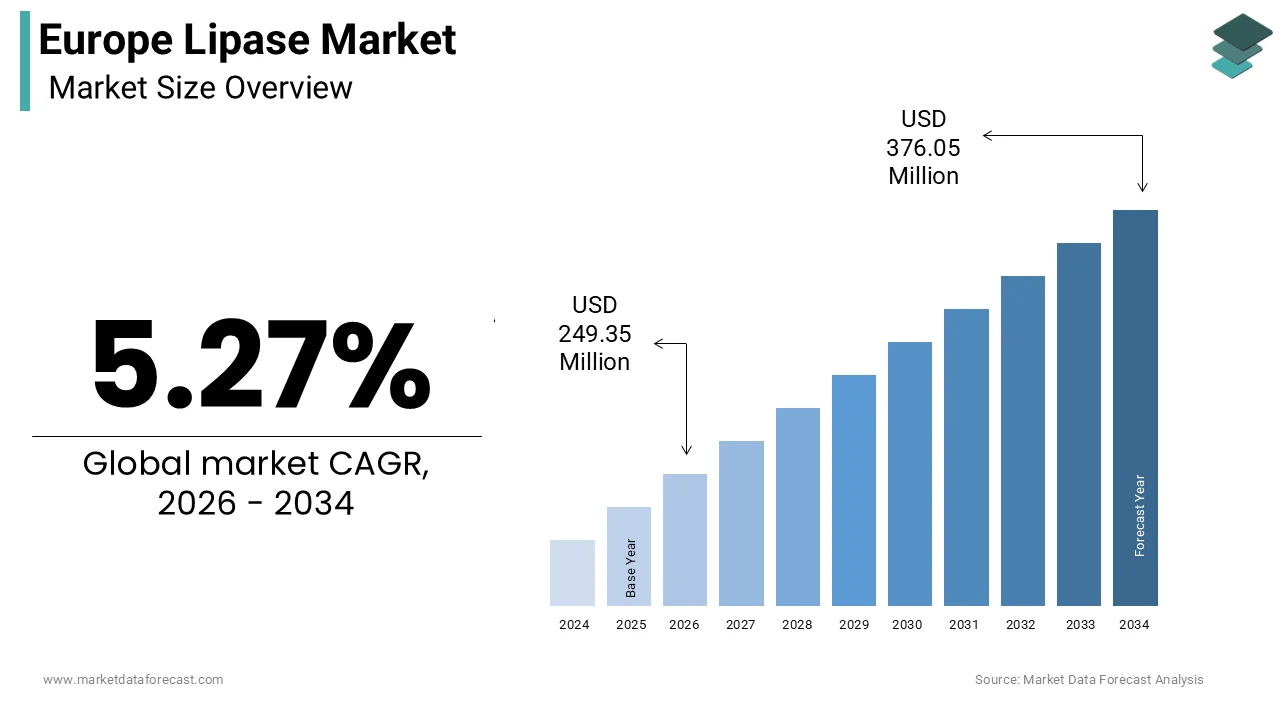

$236.87 MnMarket Estimate, 2026

$249.35 MnMarket Forecast, 2034

$376.05 MnCAGR, 2026–2034

5.27%Europe Lipase Market Size

The Europe Lipase Market size was calculated to be USD 236.87 million in 2025 and is anticipated to be worth USD 376.05 million by 2034, from USD 249.35 million in 2026, growing at a CAGR of 5.27% during the forecast period.

Lipase is a digestive enzyme that catalyzes the hydrolysis of dietary fats into glycerol and free fatty acids, playing an indispensable role in both physiological digestion and industrial bioprocessing. In Europe, lipase finds extensive application across food processing, animal feed, pharmaceuticals, and biofuel sectors, driven by its specificity, efficiency, and biodegradability. The enzyme is primarily sourced from microbial fermentation using strains of Aspergillus, Rhizopus, and Candida, with recombinant technologies enhancing yield and stability. The European Food Safety Authority recognizes and regulates numerous lipase enzyme preparations, affirming their safe use across diverse food processing applications in the European Union. As per Eurostat, the European Union is a leading producer of cheese, with the manufacturing process relying heavily on lipase for flavor development in specific varieties like Romano and Provolone. Additionally, the European Commission recognizes exocrine pancreatic insufficiency as a condition requiring prescription pancreatic enzyme replacement therapy, with lipase acting as the primary component for treatment. These intersecting health and industrial demands underpin the strategic relevance of lipase in Europe’s bioeconomy.

MARKET DRIVERS

Rising Prevalence of Pancreatic and Digestive Disorders

The growing burden of exocrine pancreatic insufficiency and related gastrointestinal disorders across the region is a primary clinical driver for the Europe lipase market. Exocrine pancreatic insufficiency is a significant health concern across the European Union, driven by conditions that impair the body's ability to produce necessary enzymes. Cystic fibrosis, which is a major cause of this insufficiency in Europe, often results in a need for lifelong enzyme replacement therapy for the majority of those affected. The management of this condition typically involves the consumption of high doses of lipase units with each meal. Concentrated therapeutic demand exists in specific European nations where the incidence of cystic fibrosis is higher. The prevalence of chronic pancreatitis has been increasing, which is often associated with factors such as lifestyle and metabolic conditions. These epidemiological trends necessitate consistent access to high-purity pharmaceutical-grade lipase, reinforcing its role as a non-discretionary therapeutic agent within European healthcare systems.

Expansion of Functional and Fermented Dairy Production

The region’s robust dairy industry increasingly leverages lipase to enhance flavor complexity and accelerate ripening in specialty cheese varieties, which creates sustained industrial demand and fuels the expansion of the Europe lipase market. The European Union produces millions of metric tons of cheese annually, with Italy, France, and Germany accounting for a notable share of output. Traditional cheeses such as Pecorino Romano, Provolone, and Parmigiano Reggiano rely on lipase derived from calf or microbial sources to generate short-chain fatty acids that impart sharp, piquant notes during aging. Exogenous lipase is increasingly used in the production of hard and semi-hard cheeses to standardize flavor and reduce maturation time. There is a trend towards adopting microbial and recombinant enzymes, largely driven by demand for plant-based, kosher, and halal products, indicating a broader industry shift toward sustainability and efficiency. This confluence of tradition, regulation, and consumer preference solidifies lipase’s industrial indispensability.

MARKET RESTRAINTS

Stringent Regulatory Approval Processes for Enzyme Use

The European Union imposes rigorous safety and efficacy evaluations for all enzymes used in food and pharmaceutical applications, which creates significant entry and expansion barriers for lipase producers, and thereby limits the growth of the Europe lipase market. The regulatory framework mandates that food enzymes undergo a thorough risk assessment by the relevant European safety authority before being included on the permitted list. The approval process for new microbial lipases typically involves a multi-year timeline with extensive evaluation of relevant data. According to industry association information, the authorization of new food enzymes, including specific lipase variants, has been limited over the past several years. Lipase-containing products in the pharmaceutical sector must adhere to specific pharmacopoeia standards and undergo comprehensive marketing authorization procedures. This complexity discourages small biotech firms from pursuing novel lipase formulations. Moreover, post approval, manufacturers must maintain full traceability of fermentation strains and production batches, increasing compliance costs. These regulatory hurdles slow innovation cycles and limit the diversity of commercially available lipase products, ultimately constraining market responsiveness to emerging applications.

Price Volatility and Supply Chain Constraints for Raw Materials

The production of microbial lipase in the region is highly sensitive to fluctuations in fermentation substrate costs and energy availability, which directly impacts manufacturing economics and the expansion of the Europe lipase market. Agricultural raw materials used in fermentation processes have seen upward price volatility. Simultaneously, energy costs for industrial fermentation and downstream processing have significantly increased. These combined costs represent a major portion of total production expenses, with recent trends impacting operational viability. Geopolitical disruptions further exacerbate instability. The war in Ukraine reduced sunflower oil and wheat availability, key components in some fermentation media, leading to reformulation delays. Additionally, Europe imports a portion of its specialty microbial strains from non-EU countries, exposing supply chains to customs delays and biosafety regulations under the Nagoya Protocol. These structural vulnerabilities increase production risk and discourage long term capacity investment, particularly among mid-sized enzyme manufacturers.

MARKET OPPORTUNITIES

Growing Demand for Enzyme-Based Detergents in Eco-Friendly Cleaning

The European household and industrial cleaning sector is increasingly adopting lipase as a biodegradable alternative to petrochemical surfactants, which provides new opportunities for the growth of the Europe lipase market. This trend aligns with the EU’s Green Deal objectives. Lipase effectively breaks down lipid-based stains such as oils, greases, and food residues at low temperatures, reducing energy consumption during washing. A significant majority of liquid laundry detergents sold in the EU contain at least one type of cleaning enzyme to enhance performance, particularly in colder washes. Lipase is commonly incorporated into many premium liquid detergent formulations within the EU to target specific fat-based stains. Germany leads consumption, where eco-labeling standards such as the Blue Angel certification require minimum biodegradability thresholds that favor enzymatic ingredients. The use of lipase in cleaning products is a growing trend driven by the demand for more effective and sustainable cleaning solutions. Moreover, industrial applications in food processing plant sanitation are expanding. Lipase-based cleaners are increasingly used in industrial settings, including dairy and meat processing facilities in the Netherlands, for effective effluent treatment. This green chemistry transition positions lipase as a strategic enabler of circular economy goals.

Advancements in Recombinant DNA Technology for High-Yield Strains

Recent breakthroughs in synthetic biology and metabolic engineering are enabling the development of high-efficiency microbial strains that dramatically increase lipase yield and stability, and thereby offer fresh prospects for the Europe lipase market expansion. European research institutions have pioneered CRISPR Cas9-mediated optimization of Aspergillus niger and Yarrowia lipolytica genomes to enhance secretion capacity and thermostability. Engineered microbial strains are demonstrating higher lipase production levels during submerged fermentation processes compared to traditional strains. The improved efficiency of these developed strains correlates with shorter fermentation times, and pilot studies indicate that using these specialized strains can lead to lower costs in the downstream purification phase. Research initiatives are focusing on enzyme engineering, with a particular emphasis on lipase due to its versatility across different sectors. Additionally, engineered lipases now exhibit activity in non-aqueous environments, unlocking applications in biodiesel production where they catalyze the transesterification of waste cooking oil. As per sources, enzyme-based biodiesel processes reduce wastewater generation compared to chemical catalysis. These innovations are transforming lipase from a commodity enzyme into a platform for sustainable industrial transformation.

MARKET CHALLENGES

Sensitivity of Enzyme Activity to Process Conditions

Lipase performance is highly dependent on pH, temperature, and ionic environment, which challenges the growth of the Europe lipase market. This creates formulation and application challenges across diverse industrial settings. Many microbial lipases often function best in neutral to slightly alkaline environments and moderate temperatures, which can reduce their effectiveness in acidic or high-heat industrial applications. Thermal processing steps, such as spray drying, can cause a significant reduction in lipase activity due to heat-induced denaturation. Variations in raw milk composition, which are influenced by seasonal factors, affect calcium levels and subsequently influence the functionality and flavor-producing capability of lipases in dairy production. The source of milk, such as differences between grass-fed and grain-fed livestock, can impact the activity level of specific microbial lipases, leading to challenges in production consistency. Furthermore, in pharmaceutical formulations, gastric acidity can degrade unprotected lipase before it reaches the duodenum, necessitating enteric coating that adds manufacturing complexity. These biochemical constraints require costly stabilization strategies such as immobilization, protein engineering, or microencapsulation, increasing product development cycles and limiting adoption in cost-sensitive segments.

Limited Consumer and Industrial Awareness of Enzyme Benefits

Lipase's underutilization in several potential European applications, despite its functional advantages, is a major barrier to the European lipase market. This is due to insufficient technical understanding among end users and formulators. Many small and medium-sized food processors in certain European regions demonstrate limited awareness of lipase's functional roles in flavor enhancement and dough processing. Adoption of lipase in animal feed production in specific Eastern European countries remains low, despite potential benefits for improving fat digestibility. Concerns about financial risk and a lack of local trial data appear to constrain lipase use in regional broiler diets. Enzyme-based biodiesel production is technically feasible but constitutes a small fraction of total output, partly due to the need for more training in biocatalysis for engineers. This knowledge gap impedes demand generation and slows the translation of laboratory innovations into commercial practice, particularly outside Western Europe’s innovation hubs.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 5.27% |

| Segments Covered | By Source, Application, Function, And Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, and the Czech Republic |

| Market Leaders Profiled | E I Du Pont De Nemours and Company, Associated British Foods PLC, Amano Enzymes Inc, Novozymes A/S, Renco New Zealand, Koninklijke DSM N.V, Chr. Hansen Holdings A/S and Clerici-Sacco Group |

SEGMENTAL ANALYSIS

By Source Insights

The microbial lipases segment dominated the Europe lipase market by accounting for a substantial share in 2025. The dominance of the microbial lipases segment is attributed to its superior catalytic efficiency, broad substrate specificity, and compatibility with industrial-scale fermentation processes. Unlike animal and plant sources, microbial lipases can be produced year-round in controlled bioreactors using non-animal substrates, aligning with EU regulations on animal welfare and food safety. Recently approved food enzyme dossiers predominantly feature products derived from microbial sources. This trend aligns with a regulatory preference for enzymes sourced microbially, attributed to the enhanced consistency and traceability they offer. Industrial fermentation, particularly in specific Northern European regions, supports large-scale enzyme production. Advanced fermentation techniques at these facilities utilize optimized microbial strains to achieve high enzyme yields, including lipases. Additionally, microbial lipases exhibit greater stability in alkaline conditions, making them ideal for detergent and biodiesel applications. As per research, a significant share of enzyme-based laundry formulations in Western Europe use microbial lipases due to their performance at low wash temperatures. This convergence of technical, ethical, and regulatory advantages solidifies microbial lipases as the backbone of Europe’s enzyme economy.

The microbial lipases segment is also estimated to register the fastest CAGR of 7.9% from 2026 to 2034 due to advances in synthetic biology that enable the design of tailored lipase variants for niche applications. Researchers are using gene-editing techniques to engineer yeast strains with improved protein secretion and higher heat tolerance for industrial applications. Public policy initiatives in Europe are encouraging the incorporation of enzymes into animal nutrition to improve environmental sustainability. Scientific studies indicate that specific microbial lipases can enhance the digestibility of dietary fats in poultry. Regulatory frameworks within the European Union have streamlined compliance for certain microbial products, facilitating their adoption in the feed industry. Observations in the European market show an increasing trend in the use of microbial enzymes within compound feed. These scientific, policy, and sustainability tailwinds ensure microbial lipases will sustain their dual status as market leader and fastest expanding category.

By Application Insights

The dairy application segment held the majority share of 38.1% of the Europe lipase market in 2025. The supremacy of the dairy application segment is credited to Europe’s deep cultural and industrial commitment to artisanal and semi-hard cheese production, where lipase is indispensable for flavor development. Italy alone produces significant metric tons of lipase-dependent cheeses such as Pecorino Romano and Provolone annually, as per sources. Lipase accelerates lipolysis during aging, releasing short-chain fatty acids that impart sharp piquant notes, reducing maturation time without compromising sensory quality. Many hard cheese producers in southern regions utilize added enzymes, such as those derived from microbes, to achieve consistent flavor profiles regardless of changes in raw milk composition. The demand for non-animal-derived lipases has increased due to the growing market for vegetarian and halal-compliant products. Microbial lipase variants are increasingly favored for use in new product development within specific European cheese-producing regions. The adoption of these enzymes assists manufacturers in overcoming challenges related to seasonal variations in milk. This fusion of tradition, regulation, and consumer ethics anchors dairy as the cornerstone of lipase utilization in Europe.

The animal feed segment is anticipated to witness the fastest CAGR of 8.3% during the forecast period, owing to tightening environmental regulations and the need to enhance nutrient utilization in monogastric livestock. The European Union’s 2023 update to the Industrial Emissions Directive mandates reduced nitrogen and phosphorus discharge from intensive farming, incentivizing enzyme supplementation to improve feed efficiency. Observations indicate that lipase supplementation in broiler and piglet diets may enhance fat utilization and increase the metabolizable energy values of dietary fats. This improvement is frequently noted in younger animals or with diets having lower fat digestibility, suggesting a trend of increased adoption of lipases in major European pork-producing regions, particularly in starter feeds. Additionally, the EU ban on in-feed antibiotics has elevated enzymes as alternatives for gut health support. Lipase reduces undigested fat accumulation that can foster pathogenic bacteria. These regulatory and nutritional imperatives position animal feed as lipase’s most dynamic growth frontier.

By Function Insights

The food and beverage texturants segment led the Europe lipase market by holding a 62.7% share in 2025. Lipase modifies lipid structures to influence mouthfeel, emulsification, and dough rheology across multiple categories. In bakery applications, lipase replaces chemical emulsifiers like DATEM by strengthening gluten networks through the generation of lysophospholipids, improving volume and crumb structure in bread. Industrial bread manufacturers in Germany and the Netherlands increasingly rely on enzyme-based dough conditioners, with lipase serving as a key component to enhance product quality and achieve clean-label standards. Similarly, in chocolate and confectionery, lipase controls cocoa butter crystallization, preventing bloom and enhancing snap. The European confectionery industry has seen a steady rise in the adoption of lipase enzymes to refine flavor development and improve the texture of specialty chocolate products. Regulatory momentum further supports this trend. The EU’s Clean Label Initiative discourages synthetic additives, driving formulators toward enzymatic solutions. Recent safety evaluations by European food safety regulators have affirmed that microbial lipases are safe for human consumption, supporting their expanded use across diverse baking and food processing categories. These functional, regulatory, and consumer drivers cement texturants as lipase’s primary functional domain.

The frozen food and beverage additives segment is likely to experience the fastest CAGR of 9.1% from 2026 to 2034. The swift expansion of the frozen food and beverage additives segment is fuelled by the expanding demand for convenient yet high-quality frozen meals and the unique ability of lipase to maintain lipid integrity during freeze-thaw cycles. Lipase prevents rancidity by hydrolyzing free fatty acids that catalyze oxidation, extending shelf life without synthetic antioxidants. The European market for frozen food shows a consistent upward trend in consumption, primarily driven by strong demand for prepared meals and bakery items. Enzymatic solutions like lipase are increasingly used in frozen dough applications to improve product structure and volume after thawing. The expansion of plant-based frozen products is creating new opportunities for functional ingredients that enhance texture and mimic fat in vegan items. Major manufacturers are actively updating their product lines to include advanced stabilization methods for improved quality control. These innovations and consumption trends position frozen food additives as lipase’s most rapidly evolving functional segment.

REGIONAL ANALYSIS

Germany Lipase Market Analysis

Germany was the top performer in the Europe lipase market by accounting for a 24.1% share in 2025. The dominance of the German market is driven by its integrated enzyme manufacturing base, advanced food processing sector, and stringent environmental policies driving feed enzyme adoption. Germany hosts production facilities for global leaders, including BASF and Evonik, which leverage high-density fermentation to supply microbial lipase across the continent. Industrialized baking operations are widely adopting enzymatic agents to enhance dough handling, consistency, and product quality. The livestock sector is increasingly utilizing enzyme additives to improve nutritional efficiency and adhere to environmental management standards. Regulatory bodies are actively approving new enzyme-based, specialized feed additives to facilitate these improvements in animal production. The overall trend shows a shift toward utilizing specific functional enzymes to meet, rather than hinder, industrial production goals and compliance requirements. Combined with strong R&D investment, the country remains Europe’s undisputed epicenter of lipase innovation and consumption.

Italy Lipase Market Analysis

Italy followed closely in the Europe lipase market by holding a 16.5% share in 2025. The growth of the Italian market is fuelled by its world-renowned cheese industry, which relies on lipase for flavor development in traditional hard cheeses. The production of certain Italian cheeses relies significantly on added enzymes for flavor development. A shift towards non-animal-derived enzymes is evident, partly influenced by consumer demand for vegetarian products and labeling regulations. Southern regions, known for their artisanal dairies, are major consumers of dairy enzymes. Furthermore, growth in the baked goods export market has led to increased use of enzymes in dough to improve texture. Regulatory alignment with EU clean label standards and strong domestic enzyme distribution networks further sustain demand. Italy’s unique fusion of heritage food production and modern enzymology secures its pivotal role in the European lipase landscape.

France Lipase Market Analysis

France maintains a noteworthy position in the European lipase market. The country’s demand is diversified across dairy, animal feed, and functional baking, supported by robust agricultural output and progressive food policy. France maintains high-volume cheese production, where lipolytic enzymes are frequently employed in the manufacturing process of specific, traditional varieties to enhance texture and flavor profiles. Simultaneously, the French poultry sector is navigating a shift towards increased enzyme inclusion in starter feeds to align with broader efficiency targets and sustainability goals. The utilization of lipase in both the dairy and poultry sectors highlights a pattern of enzyme application to optimize resource efficiency, improving cheese characteristics in the dairy industry and enhancing feed digestibility in the poultry sector. This pattern points to a continued integration of enzymatic tools to meet production and efficiency goals in both sectors. France is also a leader in enzyme research. This balance of traditional food craftsmanship and sustainability-driven innovation underpins France’s steady market influence.

The Netherlands Lipase Market Analysis

The Netherlands is moving ahead steadfastly in the Europe lipase market. Despite its small size, the country exerts an outsized influence through its concentration of enzyme innovators, agri-food exporters, and port-based distribution hubs. The Netherlands is home to DSM and Chr Hansen, which develop and export specialized lipase strains across global markets. The domestic dairy sector generates a significant volume of milk, supporting a specialized industry for producing cheese and butter that utilizes enzymes for flavor development. The Dutch poultry and pig sectors, recognized for high efficiency, incorporate lipase to improve the conversion ratios of feed. A substantial portion of compound feed in this region includes enzyme fortification. The Port of Rotterdam facilitates rapid enzyme import and re-export, making the Netherlands a key logistics node. National policies promoting circular bioeconomy principles further catalyze enzyme adoption. This synergy of science, logistics, and policy cements the Netherlands as a critical market enabler.

Spain Lipase Market Analysis

Spain is anticipated to grow in the Europe lipase market from 2026 to 2034 due to its expansive dairy and meat processing industries, both undergoing modernization to meet EU sustainability standards. Spanish cheese production continues to be a significant economic driver, with producers adapting traditional, protected-origin products to meet modern dietary preferences. There is a visible shift toward using alternative enzymes in the manufacture of traditional cheeses, allowing for vegetarian-friendly labeling. The livestock sector is increasingly incorporating enzymatic feed additives to address environmental sustainability goals, aligning with national nutrient management objectives. The export of frozen bakery goods is a growing sector, with manufacturers employing technical additives to enhance product stability for long-distance transport. Additionally, public research institutions such as CSIC have partnered with enzyme suppliers to develop thermostable lipase variants for high-temperature baking. These industrial adaptations, aligned with EU regulatory currents, position Spain as a key growth market in Southern Europe’s evolving enzyme ecosystem.

COMPETITION OVERVIEW

The Europe Lipase Market features a concentrated yet dynamic competitive landscape dominated by multinational biotechnology and chemical firms with deep R&D capabilities. Novozymes, DSM-Firmenich, and BASF lead through integrated enzyme platforms that span food, feed, and industrial applications. Competition is less about price and more about technical differentiation, formulation expertise, and regulatory readiness. Companies compete to demonstrate measurable benefits such as improved fat digestibility in animal feed, reduced maturation time in cheese, or enhanced dough stability in frozen bakery products. The EU’s strict regulatory regime for food enzymes creates high entry barriers, favoring incumbents with established safety dossiers and fermentation infrastructure. Innovation cycles are accelerating as firms leverage CRISPR and AI-driven protein design to develop next-generation lipases with tailored pH, temperature, and substrate profiles. Regional partnerships with dairy cooperatives, feed mills, and detergent brands are critical for market access. As sustainability imperatives intensify, competition increasingly centers on enzymes that support circular economy goals and reduce environmental footprints across the agri-food value chain.

KEY MARKET PLAYERS

A few major players of the Europe lipase market include

- E I Du Pont De Nemours and Company

- Associated British Foods PLC

- Amano Enzymes Inc

- Novozymes A/S

- Renco New Zealand

- Koninklijke DSM N.V

- Chr. Hansen Holdings A/S

- Clerici-Sacco Group

Top Strategies Used by the Key Market Participants

Key players in the Europe Lipase Market focus on advanced strain development through synthetic biology to enhance enzyme stability and activity under industrial conditions. They pursue strategic collaborations with food and feed manufacturers to co-develop application-specific formulations that meet clean label and sustainability criteria. Companies invest in regional production and formulation hubs to ensure supply chain resilience and regulatory compliance with EU food and feed safety standards. They actively engage with European policy frameworks such as the Green Deal and Farm to Fork Strategy to position lipase as a tool for environmental and nutritional efficiency. Additionally, they expand into emerging applications such as plant-based dairy and frozen food stabilization to diversify revenue streams beyond traditional segments.

Leading Players in the Market

- Novozymes A/S, headquartered in Denmark, is a global leader in industrial enzymes with a strong footprint in the European lipase market. The company supplies microbial lipases for dairy, animal feed, and detergents, leveraging its proprietary fermentation and protein engineering platforms. It also deepened its partnership with the European Feed Manufacturers Federation to promote enzyme-based solutions for sustainable livestock production. Novozymes strengthens its position as a key technology provider globally and in Europe by consistently investing in R&D and aligning with the EU's green agenda, enabling innovation across industries like energy, agriculture, and chemicals for a sustainable future.

- DSM-Firmenich AG, formed through the merger of DSM and Firmenich, plays a pivotal role in the European lipase landscape through its Food & Beverage and Animal Nutrition divisions. The company offers tailored lipase solutions that enhance flavor development in cheese and improve fat digestibility in poultry and swine feed. It also integrated lipase into its sustainable feed additive platform launched under the EU’s Green Deal framework. DSM-Firmenich drives cross-segment relevance and global innovation leadership by marrying sensory science with nutritional efficiency.

- BASF SE, the German chemical and biotechnology giant, contributes significantly to the Europe lipase market through its industrial biotechnology and feed enzyme portfolios. BASF produces high-purity microbial lipases via advanced submerged fermentation at its facilities in Ludwigshafen and invests heavily in strain optimization using synthetic biology tools. It also expanded clinical trials for a novel lipase formulation in pancreatic enzyme replacement therapy in partnership with European gastroenterology centers. These strategic moves demonstrate BASF’s commitment to diversifying lipase applications across consumer, industrial, and pharmaceutical domains.

MARKET SEGMENTATION

This research report on the Europe lipase market has been segmented and sub-segmented based on source, application, function, and region.

By Source

- Microbial lipases

- Animal lipases

- Plant lipases

By Application

- Animal Feed

- Dairy

- Bakery Confectionary

- Others

By Function

- Frozen food and beverage additives

- Food and beverage texturants

By Region

- UK

- France

- Spain

- Germany

- Italy

- Russi

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com