- Product Description Description

- Table of Contents TOC

- List of Table & Figure LOT

- Get Free Sample PDF Sample PDF

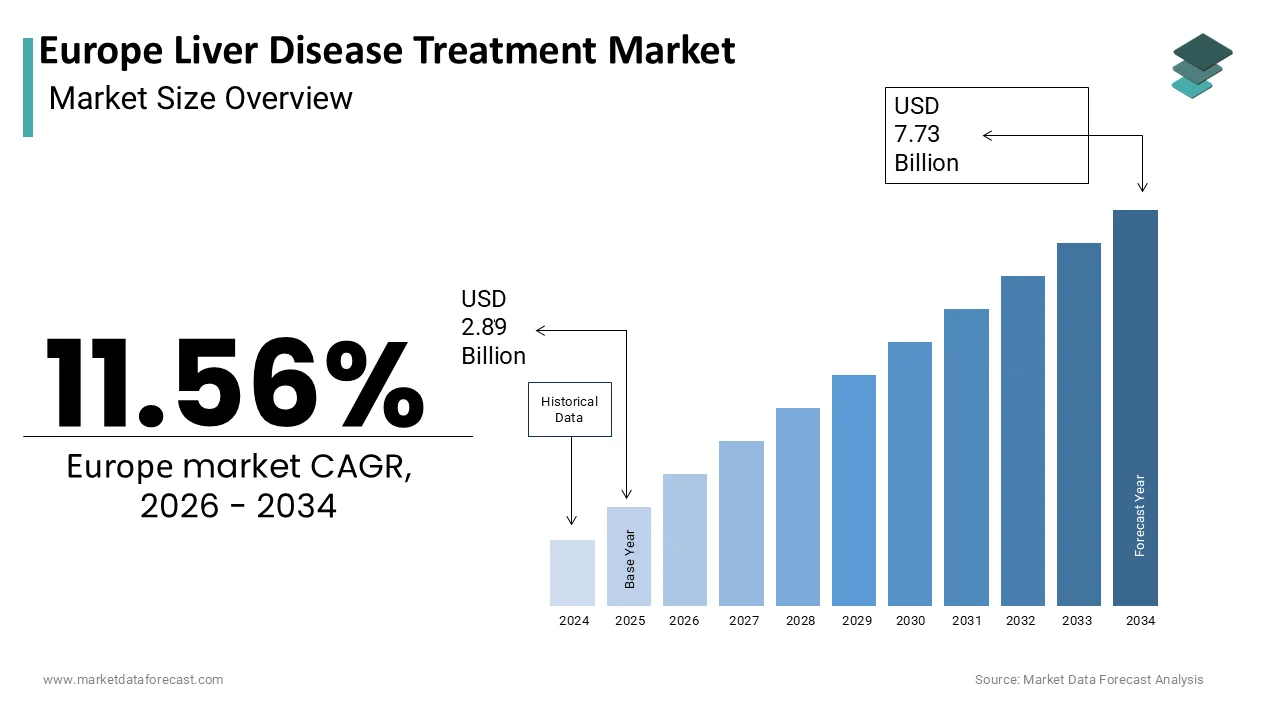

Market Size, 2025

$2.89 BnMarket Estimate, 2026

$3.22 BnMarket Forecast, 2034

$7.73 BnCAGR, 2026–2034

11.56%Europe Liver Disease Treatment Market Summary

Market Size & Growth

- The Europe Liver Disease Treatment Market was valued at USD 2.89 billion in 2025.

- Expected to reach USD 7.73 billion by 2034, growing at a CAGR of 11.56% from 2026 to 2034.

- Germany held the leading country share at 23.6% in 2025; the liver cancer segment is the fastest-growing disease type at a CAGR of 11.2% from 2026 to 2034.

Key Market Segments

- By Treatment Modality: Antiviral Therapies (leading, 48.1% share in 2025), Immunosuppressive Agents (fastest-growing, CAGR of 9.4%), Vaccines, Chemotherapy, Corticosteroids.

- By Disease Type: NAFLD/MASLD (leading, 39.7% share in 2025), Hepatitis, Alcohol-Induced Liver Disease, Liver Cancer (fastest-growing).

- By Country: Germany (23.6% share in 2025), United Kingdom (18.3% share in 2025), France, Italy, Spain, Russia, Sweden, Denmark, Switzerland, Netherlands, Rest of Europe.

Key Drivers

- Rising prevalence of Metabolic dysfunction-associated Steatotic Liver Disease (MASLD), formerly NAFLD, linked to obesity and type 2 diabetes across Germany, France, and the UK — now the leading indication for liver transplantation in several Western European countries.

- Persistently high alcohol-related liver disease burden; Europe accounts for a disproportionately high share of global alcohol consumption, with alcohol-related liver conditions contributing to tens of thousands of EU deaths annually.

- Expansion of non-invasive diagnostics such as transient elastography and FibroScan enabling earlier intervention and a larger addressable patient pool for antifibrotic and metabolic therapies.

- Advancement of precision medicine and gene-based therapeutic pipelines, including CRISPR-Cas9 and mRNA therapies; EMA has granted PRIME designation to agents targeting alpha-1 antitrypsin deficiency, Wilson disease, and primary biliary cholangitis.

Key Restraints

- Severe donor shortages for liver transplantation; waiting times in Germany, Netherlands, and Belgium often exceed one year.

- High cost and protracted health technology assessment (HTA) processes delay reimbursement for novel therapeutics, particularly in Eastern European member states.

Key Players

Gilead Sciences Inc. (U.S.), Pfizer Inc. (U.S.), Merck and Co. (U.S.), Johnson and Johnson (U.S.), Novartis (Switzerland), Roche (Switzerland), Sanofi-Aventis (France), Abbott Laboratories (U.S.), Bayer Schering AG (Germany), AstraZeneca (United Kingdom), AbbVie Inc., Bristol Myers Squibb.

Europe Liver Disease Treatment Market Size

The Europe Liver Disease Treatment Market is projected to grow from USD 2.89 billion in 2025 to USD 3.22 billion in 2026 and reach USD 7.73 billion by 2034, registering a CAGR of 11.56% during the forecast period from 2026 to 2034.

Liver disease treatment refers to the pharmaceuticals, procedures, and lifestyle interventions designed to manage and cure diverse hepatic conditions such as hepatitis, NAFLD/MASLD, cirrhosis, cancer, and genetic issues, utilizing methods like antiviral drugs, chemotherapy, immunosuppressants, diet changes, surgery, and gene therapies. The region’s aging population, rising obesity rate, and persistent alcohol consumption patterns have intensified disease prevalence, driving demand for advanced diagnostics and therapeutics. According to the European Association for the Study of the Liver, Chronic liver conditions are prevalent across the European Union, with steatotic liver disease, now termed metabolic dysfunction-associated steatotic liver disease (MASLD), representing a significant and growing health concern linked to obesity and unhealthy lifestyles. Liver cirrhosis accounts for ove170,00000 deaths annually across Europe, according to the World Health Organization Regional Office for Europe, making it a leading cause of premature mortality. National health strategies in countries like the UK and Germany now prioritize early detection through fibrosis screening programs, while the European Medicines Agency has fast-tracked approvals for novel antifibrotic and antiviral agents. European Union research initiatives, such as the Horizon Europe program, acknowledge the burden of liver disease and fund a variety of research and innovation projects aimed at prevention, diagnosis, and treatment. These demographic, clinical, and institutional forces collectively shape a complex yet increasingly responsive treatment landscape across the continent.

MARKET DRIVERS

Escalating Prevalence of Metabolically Dysfunctional Associated Steatotic Liver Disease

Metabolically-dysfunctional associated steatotic liver disease, formerly known as non-alcoholic fatty liver disease, has emerged as the dominant driver of the European liver disease treatment market. This is due to its tight linkage with obesity and type 2 diabetes. A significant majority of the adult population in the European region carries excess weight. In several major European countries like Germany, France, and the UK, a substantial portion of adults are affected by metabolic liver issues. A concerning percentage of these liver cases progress to a more serious inflammatory condition. The condition is now the leading indication for liver transplantation in several Western European countries, surpassing viral hepatitis. National health systems are responding with systematic screening. A health service in the UK has initiated a large-scale program focused on detecting early signs of liver damage within the type 2 diabetes population. This proactive identification is generating unprecedented demand for pharmacotherapies and monitoring tools. With no approved pharmacological treatment yet widely available, the pipeline for metabolic liver disease therapies—including FXR agonists and THR beta modulators—is accelerating, positioning this segment as the primary growth engine in Europe’s liver disease treatment market.

Sustained High Burden of Alcohol Related Liver Disorders

Alcohol-related liver disease remains an important and persistent driver of therapeutic demand across the region, which further boosts the expansion of the European liver disease treatment market. This trend reflects the region's historically high per capita alcohol consumption. Europe accounts for a significant portion of global alcohol consumption relative to its population. Alcohol consumption is considered a primary contributor to health issues such as cirrhosis in several European countries, with alcohol-related liver conditions contributing to tens of thousands of deaths each year across the European Union. Age-standardized mortality rates from alcoholic cirrhosis in some Central and Eastern European areas are significantly higher than the general global averages. Despite public health campaigns, alcohol consumption patterns have rebounded post-pandemic. This sustained burden necessitates continuous investment in hepatoprotective agents, corticosteroids, ds, and transplant services. Hospitals in France and Spain now dedicate specialized liver intensive care units to manage acute alcoholic hepatitis, further amplifying treatment infrastructure and pharmaceutical demand.

MARKET RESTRAINTS

Limited Access to Liver Transplantation Due to Donor Shortages

The severe and persistent shortage of viable organ donors restricts curative options for end-stage liver disease and negatively impacts the growth of the European liver disease treatment market. The waiting time for a liver transplant in several European countries, including Germany, the Netherlands, and Belgium, often extends beyond a year, which can result in a significant percentage of patients becoming too ill for surgery or passing away while awaiting an organ. The general rate of deceased organ donors across the European Union is below the level needed to satisfy current demand for transplants. Cultural and legal barriers further exacerbate the gap. In certain countries, such as Italy and Poland, more than a third of families refuse to authorize organ donation, even when an opt-out system is in place. This scarcity forces healthcare systems to rely on bridging pharmacotherapies and palliative interventions rather than definitive cures. Consequently, patients with hepatocellular carcinoma or decompensated cirrhosis often receive suboptimal care, limiting the clinical and commercial potential of advanced therapies that assume transplant eligibility. The pace of therapeutic innovation is currently capped by limitations in donor infrastructure and public consent mechanisms.

High Cost and Reimbursement Delays for Novel Therapeutics

Protracted health technology assessment processes and inconsistent reimbursement policies across member states also slow down the expansion of the European liver disease treatment market. This affects the commercialization of next-generation liver disease treatments in the region. The high cost of some new therapeutic agents for liver diseases prompts close examination of their value for money. Significant delays in securing public funding for new liver therapies are observed in some regions, which can affect both patient access to treatment and commercial interest in bringing products to market. Limited public health budgets in certain Eastern European countries impact the extent to which new, approved medicines for liver conditions are publicly funded. Even in wealthier nations, payers impose strict criteria. These fragmented and cautious reimbursement landscapes discourage rapid market entry and limit the scalability of innovative treatments. The inability to recoup high development costs, due to a lack of pan-European pricing agreement or adaptive payment systems, is stalling pipeline progress.

MARKET OPPORTUNITIES

Advancement of Non-Invasive Diagnostics to Enable Early Intervention

The integration of non-invasive fibrosis assessment tools introduces a key opportunity for the European liver disease treatment market. This is facilitated by enabling early diagnosis and timely therapeutic intervention. Technologies such as transient elastography, FibroSca,,n and serum biomarker panels like ELF and FibroTest have largely replaced liver biopsy in routine clinical practice across Western Europe. National screening programs are leveraging these tools. Early detection allows treatment initiation before irreversible cirrhosis develops, expanding the addressable patient pool for antifibrotic and metabolic therapies. Diagnostic innovation is becoming a critical enabler of therapeutic market growth, driven by the EU’s Beating Cancer Plan's emphasis on liver cancer prevention through fibrosis screening.

Expansion of Precision Medicine and Gene-Based Therapeutic Pipelines

The region is emerging as a global leader in the development of precision and gene-based therapies for inherited and advanced liver diseases, which offers fresh prospects for the expansion of the European liver disease treatment market. This opens new therapeutic avenues beyond conventional management. The European Medicines Agency has granted PRIME designation to several investigational agents targeting alpha 1 antitrypsin deficiency, Wilson disease, and primary biliary cholangitis, accelerating their clinical pathways. In addition, A biotech company initiated an initial human trial of an mRNA therapy designed to restore functional protein expression in certain metabolic liver disorders. Besides, gene editing platforms like CRISPR Cas9 are being evaluated in European academic centers for hepatitis B functional cure strategies. Protocols for gene and cell therapy targeting liver conditions are a significant part of current clinical trial activity in the European region. These innovations address previously untreatable monogenic conditions and offer potential cures rather than chronic management. Europe is set to lead the next wave of liver therapeutics, transitioning the market emphasis from managing symptoms to modifying the disease itself, driven by adaptable regulatory frameworks and increased manufacturing capacity.

MARKET CHALLENGES

Fragmented Disease Awareness Leading to Late Stage Diagnosis

The pervasive lack of public and primary care awareness results in widespread late-stage diagnosis, which challenges the growth of the European liver disease treatment market. Liver disease is often asymptomatic until advanced fibrosis or decompensation occurs, yet only a portion of European adults can identify common risk factors such as metabolic syndrome or silent hepatitis infection. Primary care physicians in countries like Greece and Portugal report insufficient training in liver risk stratification, leading to missed opportunities for early referral. The diagnostic delay not only increases mortality but also shifts treatment toward palliative and high-intensity care, reducing the impact of emerging early intervention therapies. Europe’s therapeutic advances cannot reach their full potential without coordinated public health campaigns and robust primary care education, as systemic underdetection will otherwise persist.

Regional Disparities in Healthcare Infrastructure and Specialist Access

Significant inequities in hepatology care infrastructure across the region impede uniform access to advanced liver disease treatments, particularly in Southern and Eastern regions, which ultimately constrains the expansion of the European liver disease treatment market. A variation in the number of liver specialists is apparent across different European regions. The scarcity limits the availability of fibrosis assessment, transplant evaluation, and novel therapy administration. Furthermore implementation of country-specific plans addressing liver health challenges is not universal across all member states. Individuals living in less populated areas sometimes face significant travel distances when seeking specialized liver care, which may impact how quickly they receive a diagnosis and maintain treatment. These infrastructural gaps mean that even when innovative therapies are approved and reimbursed, their real-world impact is diluted by delivery bottlenecks. Bridging this geographic and specialist divide is essential to ensuring equitable therapeutic outcomes across the European population.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Treatment Modality, Disease Type, Resolution, and Region. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, Rest of Europe |

| Market Leaders Profiled | Gilead Science Inc. (U.S.), Pfizer Inc. (U.S.), Merck & Co. (U.S.), Johnson & Johnson (U.S.), Novartis (Switzerland), Roche (Switzerland), Sanofi-Aventis (France), Abbott Laboratories (U.S.), Bayer Schering AG (Germany), and AstraZeneca (United Kingdom). |

SEGMENTAL ANALYSIS

By Treatment Modality Insights

The antiviral therapies segment captured the leading share of 48.1% of the European liver disease treatment market in 2025. The dominance of the antiviral therapies segment is driven by the continued need to manage chronic hepatitis B and C, despite significant progress in hepatitis C cure rates. Several people in the EU remain chronically infected with hepatitis B, generally requiring long-term antiviral therapy to manage the condition and prevent complications. There is a higher prevalence of hepatitis B in some Eastern European countries. The high prevalence of hepatitis B in certain regions contributes to a sustained demand for antiviral treatments. Antiviral treatments have successfully treated many individuals with hepatitis C. The continued occurrence of reinfection and previously undiagnosed cases maintains an ongoing need for antiviral regimens for hepatitis C. National elimination programs in Germany and France include annual screening and immediate treatment protocols, ensuring consistent prescription volumes. The European Medicines Agency continues to approve next-generation antivirals with a higher barrier to resistance, reinforcing this modality’s central role in viral liver disease management.

The immunosuppressive agents segment is predicted to witness the highest CAGR of 9.4% from 2025 to 2033. The swift growth of this segment is primarily fueled by the rising incidence of autoimmune liver disorders, particularly autoimmune hepatitis and primary biliary cholangitis, which affect a large number of patients in the EU. Newer agents like mycophenolate mofetil and tacrolimus with improved safety profiles are replacing older regimens, driving prescription upgrades. National protocols mandate personalized immunosuppression based on pharmacogenomic testing, enhancing efficacy and reducing side effects. As awareness of autoimmune liver conditions improves and transplant volumes grow, immunosuppressive therapy is transitioning from niche to mainstream, underpinning its accelerated adoption.

By Disease Type Insights

The Non alcoholic fatty liver disease (NAFLD) segment led the European liver disease treatment market by holding a share of 39.7% in 2025. The supremacy of the NAFLD segment is credited to its epidemic scale, driven by rising obesity and metabolic syndrome across the continent. A significant number of adults in the EU have non-alcoholic fatty liver disease (NAFLD), with a notable proportion developing non-alcoholic steatohepatitis. The prevalence of NAFLD is elevated in several European countries among adults in older age groups. The absence of approved pharmacotherapies has intensified demand for off-label use of antidiabetics such as pioglitazone and GLP-1 agonists, which are increasingly prescribed by hepatologists for metabolic liver disease. National health systems are investing in fibrosis screening. Some regions are implementing health strategies to improve the detection of liver conditions in primary care settings. This proactive identification expands the treated patient pool and anchors NAFLD as the largest disease segment.

The liver cancer segment is estimated to register the fastest CAGR of 11.2% during the forecast period. The acceleration of the liver cancer segment is propelled by the rising incidence of hepatocellular carcinoma secondary to undiagnosed NAFLD and persistent hepatitis B in migrant populations. Europe observes tens of thousands of new liver cancer cases each year. The occurrence of new cases has been increasing. The approval of novel systemic therapies, including immune checkpoint inhibitors like atezolizumab plus bevacizumab as first-line treatment, has transformed clinical management and extended survival. Multiple new regimens for liver cancer treatment have recently been approved within Europe. National cancer plans in some countries in the region mandate multidisciplinary liver tumor boards, ensuring timely access to advanced therapies. So, liver cancer’s clinical and therapeutic footprint will continue to expand rapidly.

COUNTRY LEVEL ANALYSIS

Germany Liver Disease Treatment Market Analysis

Germany outperformed other countries in the European liver disease treatment market by occupying a 23.6% share in 2025. The growth of liver disease treatment in Germany is attributed to its dense network of specialized hepatology centers, universal health coverage, and robust pipeline integration. Germany operates numerous liver transplant units and performs a notable number of transplants annually. The statutory health insurance system covers all EMA-approved liver therapies without prior authorization for advanced fibrosis, ensuring rapid access. Additionally, Germany hosts leading academic institutions. This combination of clinical excellence, policy support, rt, nd real-world data infrastructure solidifies Germany’s central role in Europe’s therapeutic landscape.

United Kingdom Liver Disease Treatment Market Analysis

The United Kingdom held the second position in the European liver disease treatment market by capturing an 18.3% share in 2025. The prominence of the UK market is due to systematic public health interventions and evidence-based reimbursement frameworks. A significant health initiative is in progress to screen adults with diabetes or obesity for liver fibrosis. This screening effort has led to the identification of hundreds of thousands of new liver disease cases. The National Institute for Health and Care Excellence maintains detailed liver disease guidelines that standardize treatment pathways across England, ensuring consistent adoption of antivirals, immunosuppressants, and emerging NAFLD therapies. The UK also leads in liver cancer innovation. Furthermore, New liver therapies are being made available faster in the UK through a rapid access pathway. This integration of screening policy and clinical guidance makes the UK a model for proactive liver disease management.

France Liver Disease Treatment Market Analysis

France continues to be a significant player in the European liver disease treatment market owing to the high burden of metabolic and alcohol related liver disease and a coordinated national response. A notable proportion of adults in France has non-alcoholic fatty liver disease (NAFLD). Alcohol consumption levels in the region are comparatively high. A plan has been initiated to address liver health concerns. Efforts focus on improved early identification of liver conditions. Programs include specialist education. Digital health monitoring tools are part of the initiative. The plan includes mandatory fibrosis assessment for all patients with type 2 diabetes, generating sustained demand for diagnostics and therapeutics. French hospitals perform a considerable number of liver transplants yearly, with full reimbursement for immunosuppressive regimens. Additionally, France leads EU clinical trials for antifibrotic agents, hosting many active studies. This policy-driven ecosystem ensures France remains a high-volume and high-innovation market.

Italy Liver Disease Treatment Market Analysis

Italy witnessed consistent growth in the European liver disease treatment market. Its significance derives from the confluence of high hepatitis B prevalence in migrant communities and Europe’s second-largest liver transplant program. A significant number of Italians live with chronic hepatitis B, with incidence rates in Southern regions exceeding those among foreign-born populations. Italy performs a notable number of liver transplants annually. The national health service provides universal access to antivirals and post-transplant immunosuppressants, with no cost sharing for chronic liver conditions. Italy faces a complex challenge due to its significant elderly population and increasing rates of NAFLD, creating a persistent need for diverse liver disease treatments.

Spain Liver Disease Treatment Market Analysis

Spain is expected to be an attractive region in the European liver disease treatment market from 2025 to 2033 due to a high prevalence of alcohol induced liver disease and systemic delays in diagnosis. Alcohol consumption in Spain is considerable compared to some other European regions. Heavy alcohol consumption is associated with alcoholic cirrhosis, a significant factor in liver-related hospitalizations. Liver cancer is often identified at later stages. Early detection of liver cancer may be affected by the availability of primary care screening programs. Despite these challenges, Spain is rapidly modernizing its response. Spain also participates in the EU’s Be Hepa initiative to eliminate viral hepatitis, expanding antiviral access. So, Spain represents a high need market transitioning toward proactive management through policy and infrastructure investment.

TOP LEADING PLAYERS IN THE MARKET

- Gilead Sciences Inc. maintains a prominent position in the European liver disease treatment market through its leadership in antiviral therapies for hepatitis B and C. The company’s direct-acting antivirals have cured over one million patients across Europe since their introduction, significantly advancing regional elimination goals. Gilead continues to innovate with next-generation tenofovir prodrugs offering improved renal and bone safety profiles for chronic hepatitis B management. Gilead also collaborates with the European Association for the Study of the Liver on real-world evidence initiatives tracking long-term outcomes in viral hepatitis. Through sustained scientific investment and inclusive access strategies, Gilead reinforces its global contribution to viral liver disease eradication while strengthening its therapeutic footprint in Europe.

- AbbVie Inc. plays a critical role in the European liver disease treatment market with its portfolio of antiviral and immunomodulatory therapies. The company’s hepatitis C regimens remain widely used in retreatment and complex cases across Southern and Eastern Europe. Beyond virology, AbbVie is advancing its presence in autoimmune and metabolic liver diseases through pipeline candidates targeting primary biliary cholangitis and non alcoholic steatohepatitis. The company also funds hepatology fellowships across France and Spain to build specialist capacity. By diversifying its liver disease portfolio and embedding support services within public health systems, AbbVie extends its impact beyond pharmaceutical supply to holistic disease management.

- Bristol Myers Squibb significantly influences the European liver disease treatment market through its oncology leadership and emerging metabolic liver pipeline. The company’s immune oncology combination of nivolumab and ipilimumab is approved for advanced hepatocellular carcinoma, offering a critical option for patients ineligible for surgery. Bristol Myers Squibb is also advancing fibroblast growth factor receptor inhibitors for cholangiocarcinoma and THR beta agonists for non alcoholic fatty liver disease through late-stage European trials. Additionally, it supports the European Reference Network on Hepatological Diseases with data analytics for rare liver cancers. Through oncology innovation and metabolic pipeline development, Bristol Myers Squibb addresses both prevalent and orphan liver conditions across the continent.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Key players in the European liver disease treatment market focus on expanding therapeutic indications through robust clinical development, particularly in non alcoholic fatty liver disease and liver cancer. They engage in strategic partnerships with national health systems to facilitate early diagnosis and treatment access through screening programs and digital health tools. Companies invest in real-world evidence generation to demonstrate long-term outcomes and support reimbursement submissions across diverse payer environments. Geographic tailoring of access programs addresses disparities in Eastern and Southern Europe, including migrant and underserved populations. Portfolio diversification beyond antivirals into immunology, oncology, and metabolic disease reduces dependency on mature hepatitis segments. Additionally, many firms support hepatology education and specialist training to build treatment capacity. These integrated strategies enhance both clinical impact and commercial sustainability in Europe’s complex liver disease landscape.

COMPETITIVE LANDSCAPE

The European liver disease treatment market features intense yet differentiated competition among multinational pharmaceutical companies and emerging biotech firms. While antiviral therapies for hepatitis are dominated by established players with mature products, newer segments like non alcoholic fatty liver disease and liver cancer are attracting agile innovators with novel mechanisms of action. Competition is not primarily price-based but hinges on clinical differentiation, timing, and health technology assessment success. Large firms leverage integrated pipelines and global trial networks to accelerate European approvals, while smaller biotechs focus on niche indications such as rare cholestatic diseases. Reimbursement variability across member states creates asymmetric market entry dynamics, favoring companies with strong local health economics teams. Collaborative models with academic centers and patient organizations are increasingly vital for real-world validation and advocacy. Overall, the market rewards scientific innovation, health system integration, and equitable access over conventional marketing approaches.

KEY MARKET PLAYERS

Companies playing a vital role in the europe liver disease treatment market profiled in the report are

- Gilead Science Inc. (U.S.)

- Pfizer Inc. (U.S.)

- Merck & Co. (U.S.)

- Johnson & Johnson (U.S.)

- Novartis (Switzerland)

- Roche (Switzerland)

- Sanofi-Aventis (France)

- Abbott Laboratories (U.S.)

- Bayer Schering AG (Germany)

- AstraZeneca (United Kingdom)

MARKET SEGMENTATION

This research report on the europe liver disease treatment market has been segmented and sub-segmented into the following categories.

By Treatment Modality

- Antiviral

- Vaccines

- Chemotherapy

- Immunosuppressive Agents

- Corticosteroids

By Disease Type

- Hepatitis

- Non-Alcoholic Fatty Liver Disease

- Alcohol-Induced

- Liver Cancer

By Country

- United Kingdom

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Rest of Europe