Europe Livestock Monitoring System Market Size, Share, Trends & Growth Forecast Report, Segmented By Offering, Application, Species, And By Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic & Rest of Europe), Industry Analysis From 2026 to 2034

Market Size, 2025

$545.11 MnMarket Estimate, 2026

$643.23 MnMarket Forecast, 2034

$2417.81 MnCAGR, 2026–2034

18%Europe Livestock Monitoring System Market Size

The Europe livestock monitoring system market size was valued at USD 545.11 million in 2025 and is anticipated to reach USD 643.23 million in 2026 from USD 2417.81 million by 2034, growing at a CAGR of 18% from 2026 to 2034.

Current Introduction of the Europe Livestock Monitoring System Market Report

A Livestock Monitoring System is an integrated technology solution, often powered by the Internet of Things (IoT) and Artificial Intelligence (AI), designed to track and manage the health, behavior, and location of farm animals in real-time. These systems utilize wearable sensors smart ear tags boluses accelerometers and environmental monitors linked to cloud based analytics platforms to enable data driven decision making. Their deployment aligns with the European Union’s strategic emphasis on precision livestock farming animal welfare and sustainable agricultural practices. According to a 2025 European Commission study, approximately 83 percent of surveyed livestock farmers in the EU reported using at least one livestock-specific digital tool, reflecting an optimistic trend toward on-farm digitalization. Under initiatives like Horizon Europe and the Digital Europe Programme, the EU supports on-farm digitalization. Specifically, the "Digital and data technologies for livestock tracking" program provides up to €5 million in funding to enhance sustainable production and supply chain transparency. Furthermore, Regulation (EU) 2019/6 and the EMA Strategy on Antimicrobials 2021–2025 mandate enhanced surveillance and data collection on antimicrobial use to promote responsible treatment and reduce the risk of resistance in livestock. This regulatory and technological convergence positions livestock monitoring systems not as optional innovations but as essential components of modern compliant and competitive European animal production.

MARKET DRIVERS

EU Regulatory Pressure to Reduce Antibiotic Use Drives Adoption of Health Monitoring Technologies

The European Union’s stringent policies targeting antimicrobial resistance have made proactive health monitoring indispensable for compliant livestock production, which contributes to the growth of the Europe livestock monitoring system market. According to the European Medicines Agency (EMA), sales of antibiotics for food-producing animals in the EU dropped by over 50% between 2011 and 2022, reaching the lowest level ever reported. Further reductions are mandated under the Farm to Fork Strategy, aiming for a 50% reduction in sales by 2030 compared to 2018 levels. To meet these goals farmers increasingly deploy monitoring systems that detect early signs of illness such as reduced rumination elevated body temperature or altered activity patterns. As per joint reports from the European Food Safety Authority (EFSA) and the EMA, continuous monitoring and targeted interventions have contributed to a significant reduction in antibiotic use, with overall sales of veterinary antimicrobials decreasing by 44% between 2014 and 2021. National action plans in Sweden and the Netherlands now incentivize farms that implement digital health surveillance with Denmark’s “Antibiotic Free Pork” certification requiring documented use of monitoring technologies. Research by Wageningen University & Research has shown that sensor-based management in automatic milking systems can improve the detection of subclinical and clinical mastitis, allowing for faster intervention and potential reduction in antibiotic treatments. These regulatory financial and clinical drivers collectively transform livestock monitoring systems into critical tools for sustainable and legally compliant animal husbandry across Europe.

Labor Shortages and Rising Operational Costs Accelerate Automation in Animal Management

Persistent agricultural labor shortages across the region are compelling livestock producers to adopt monitoring systems as force multipliers, which further boosts the expansion of the Europe livestock monitoring system market. These systems enhance productivity with fewer personnel. The EU agricultural sector faces a significant labor shortage driven by rapid aging of the workforce and rural population decline, increasing reliance on automation. Livestock farms in Western Europe are experiencing increased labor recruitment difficulties, contributing to the adoption of automated herd management technologies. Monitoring systems address this by automating routine tasks such as heat detection lameness scoring feeding alerts and calving prediction. The adoption of automated estrus detection systems in dairy farming significantly increases accuracy in detecting heat, leading to better reproductive outcomes and improved labor efficiency compared to traditional visual monitoring. In the Netherlands where the average dairy farm manages over 100 cows per worker such technologies are now considered essential infrastructure. Wages are rising and labor availability is contracting across European livestock sectors. Consequently, digital monitoring is shifting from a productivity enhancer to an operational necessity. This shift is vital for maintaining competitiveness and high animal care standards.

MARKET RESTRAINTS

High Initial Investment and Fragmented Connectivity Infrastructure Limit Small Farm Adoption

Significant upfront costs and inconsistent rural digital infrastructure across the region impede the growth of the Europe livestock monitoring system market. This affects the widespread deployment of livestock monitoring systems, despite clear benefits. The cost of specialized digital monitoring technologies is becoming a significant, and sometimes prohibitive, investment for medium-sized dairy operations, often requiring specialized financing or subsidy support. Financial and administrative constraints remain major obstacles for smaller European farms looking to adopt new digital technology, often resulting in lower adoption rates compared to larger, more specialized agricultural enterprises. Besides, rural broadband and mobile connectivity, while improving, remain fragmented in several Southern and Eastern European areas, hindering the real-time data transmission needed for precision farming technologies. A significant portion of farmers, particularly in specific Southern European regions, cite poor digital infrastructure and high costs as primary reasons for neglecting or abandoning investments in digital agriculture tools. EU digital agriculture funds exist, however, they often require co-financing and complex applications. These barriers deter smaller operators. Costs must decrease and connectivity gaps must close for digital tools to be widely adopted in livestock farming. Currently, the benefits of these technologies remain concentrated among larger commercial farms. This inequality is deepening the digital divide in European agriculture.

Lack of Interoperability and Data Standardization Hinders System Integration

A fragmented ecosystem of proprietary platforms that do not communicate with each other or with broader farm management software plagues the Europe livestock monitoring system market. Consequently, this creates operational inefficiencies. The European agricultural machinery sector is highly fragmented, with numerous competing brands utilizing proprietary, non-interoperable data systems that hinder seamless integration, prompting industry calls for harmonized standards. Data from the European Commission suggests that a significant majority of agricultural digital tools in the EU, particularly in livestock management, operate in isolation, leading to high reliance on manual entry or intermediate software to exchange data between systems. This siloed data environment forces farmers to manage multiple dashboards reducing the practical utility of real time insights. National pilot programs in Finland and Belgium attempting to establish common data standards under the EU Code of Conduct for Agri Data have yet to achieve industry wide adoption. Consequently producers face lock in risks and integration headaches that discourage investment particularly when scaling operations or switching vendors. Until true interoperability is achieved through regulatory or industry led standardization the full potential of data driven livestock management will remain unrealized across European farms.

MARKET OPPORTUNITIES

Integration with Carbon Footprint and Emission Tracking for Green Certification

Emerging environmental mandates are creating a strategic opportunity for the Europe livestock monitoring system market. These systems can serve as data engines for sustainability compliance and carbon accounting. The EU is transitioning toward a voluntary, standardized, and certified carbon farming framework, with methodological development ongoing and potential pilot schemes for livestock expected around 2026. Monitoring systems that track feed intake manure output and animal activity can now estimate enteric fermentation and nitrogen excretion using validated algorithms. The agricultural sector is implementing advanced monitoring and mitigation techniques, such as precision feeding and improved manure management, to reduce overall carbon footprints, although progress in reducing agricultural emissions across Europe has been slower than other sectors. In Switzerland and Denmark certification schemes like “Climate Positive Milk” already require digital monitoring data to validate environmental claims. Moreover the EU Eco Scheme under the Common Agricultural Policy offers premium payments to farms that demonstrate emission reductions using approved digital tools. This regulatory alignment transforms livestock monitoring from a health and productivity tool into a gateway for green subsidies market differentiation and carbon credit eligibility across European agricultural value chains.

Expansion of AI Driven Predictive Analytics for Reproductive and Disease Management

Advancements in artificial intelligence and machine learning are unlocking new capabilities in the Europe livestock monitoring system market. These technologies enable predictive rather than reactive management. European Union institutions are increasing investment in Precision Livestock Farming (PLF) technologies, with a focus on AI-driven early detection of respiratory and metabolic issues in pigs and cattle. Companies in the Netherlands and Sweden now offer systems that analyze movement rumination and feeding patterns using neural networks trained on millions of animal hours. AI-based heat detection systems are improving reproductive performance in dairy herds by accurately identifying estrus, which increases conception rates and reduces the interval between calving and subsequent pregnancy. Furthermore the European Food Safety Authority recognizes predictive monitoring as a valid component of antimicrobial stewardship programs. Computing power is increasing, and edge processing is becoming more affordable. Consequently, these intelligent systems are transitioning from research prototypes to commercially viable solutions. These solutions enhance welfare, productivity, and compliance across diverse European livestock operations.

MARKET CHALLENGES

Data Privacy Concerns and Ambiguous Ownership Rights Undermine Farmer Trust

The lack of clear legal frameworks governing farm data ownership privacy and usage rights is a critical yet underaddressed challenge in the Europe livestock monitoring system market. According to the European Data Protection Supervisor agricultural data generated by monitoring systems often falls into a regulatory gray area not fully covered by the General Data Protection Regulation which primarily addresses personal data. As per a 2023 report by the European Farmers’ Coordination farmers express deep concern that their operational data could be used by input suppliers insurers or processors to influence pricing or contract terms without consent. A significant, yet unverified, proportion of dairy farmers in major European production countries are resisting the sharing of farm-level operational data with, for example, input suppliers or insurance companies, due to significant concerns regarding how that data might be used against them in commercial negotiations. Although the EU Code of Conduct on Agricultural Data Sharing promotes voluntary principles enforcement remains weak. This trust deficit discourages data sharing essential for benchmarking disease modeling and collective health initiatives thereby limiting the scalability and societal value of livestock monitoring ecosystems across Europe.

Technical Complexity and Insufficient On Farm Digital Literacy Impede Effective Utilization

Insufficient digital skills among farm operators and support personnel is also negatively impacting the expansion of the Europe livestock monitoring system market. This compromises the practical effectiveness of livestock monitoring systems, despite hardware availability. There is a significant digital skills gap among EU agricultural workers compared to the general population, with adoption rates of advanced technology remaining low in rural areas. The utilization of digital monitoring systems on smaller EU farms is hindered by technical, operational, and user-interface challenges, according to agricultural digitalization reports. The increasing complexity of data-driven, precision livestock farming (PLF) requires advanced digital skills that many livestock veterinarians have not yet acquired, which limits the potential of data-driven advice. While manufacturers provide user interfaces many remain overly technical or not localized into regional languages. The promise of precision livestock farming will remain unrealized for a majority of European producers despite technology availability. Success requires parallel investment in hands-on training, simplified user design, and rural digital education.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 18% |

| Segments Covered | By Offering, Application, Species, and By Country |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

| Regions Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, the Czech Republic, and the Rest of Europe |

| Market Leaders Profiled | Afimilk Ltd. (Israel), BouMatic LLC (U.S.), SCR Dairy, Inc. (Israel), DeLaval (Sweden), GEA Group AG (Germany), and livestock monitoring software and service providers such as DairyMaster (Ireland), SUM-IT Computer Systems, Ltd. (U.K.), and Valley Agriculture Software (U.S.). |

SEGMENTAL ANALYSIS

By Offering Insights

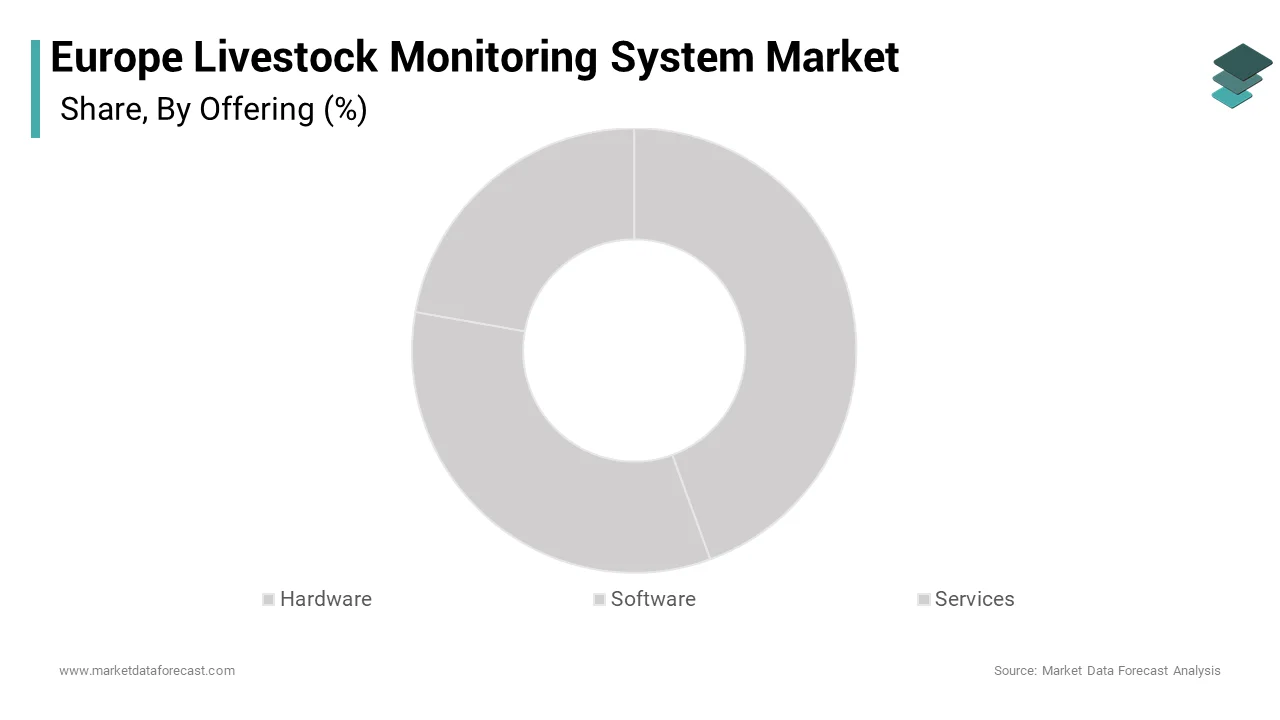

The hardware segment was the largest segment of the Europe livestock monitoring system market and accounted for a 61.9% share in 2025. The supremacy of the segment is attributed to the foundational role of physical sensors tags and readers in data collection. The adoption of digital tools for livestock health monitoring, particularly wearable technologies, is increasing rapidly across European farms, often driven by the need for better health monitoring and data-driven management. The European Commission’s Digital Agriculture Strategy emphasizes on farm infrastructure investment with national programs in Germany and the Netherlands subsidizing up to forty percent of hardware costs for small and medium farms. The deployment of electronic ear tags and monitoring sensors is growing significantly, with the cattle segment holding a dominant share in the adoption of these technologies. These devices must withstand harsh barn environments operate for months on a single charge and comply with EU radio equipment directives which favors established manufacturers with robust engineering. The one time capital nature of hardware purchases combined with regulatory and environmental pressures ensures sustained demand across dairy beef and swine operations throughout Europe.

The software segment is on the rise and is expected to be the fastest growing segment in the market by witnessing a CAGR of 12.3% between 2026 and 2034 due to the shift from data collection to intelligent analytics and decision support. Funding and support for digital livestock tracking and artificial intelligence in agriculture are expanding through collaborative European research initiatives to improve sustainable production and animal welfare. Modern platforms now integrate real time sensor data with weather feed inventory and genetic records to generate actionable insights on heat detection disease risk and feed efficiency. The European agricultural machinery industry is increasingly integrating digital farming solutions and smart technologies into new equipment to enhance precision and data-driven decision-making for farmers. In Denmark and Sweden national cooperatives like Arla and LRF provide centralized software dashboards to member farms enabling herd benchmarking and early warning systems. This convergence of regulatory pressure labor constraints and data monetization is transforming software from an accessory into the strategic brain of precision livestock farming across Europe.

By Application Insights

The breeding management segment held the majority share of 29.7% of the Europe livestock monitoring system market in 2025. The prominence of the segment is credited to the economic imperative to optimize reproductive efficiency in dairy and beef herds. Extending the time a dairy cow remains open beyond the voluntary waiting period decreases overall economic efficiency and revenue due to reduced total milk yield over the animal's lifetime. The use of precision livestock monitoring tools (such as accelerometers and rumination trackers) generally yields a higher accuracy in detecting estrus compared to traditional manual observation. The European Commission’s Genetic Improvement Program promotes data driven breeding with national milk recording schemes in Germany France and Italy now integrating estrus alerts from monitoring platforms. Automated, technology-driven management systems (like milking robots and activity monitors) in the EU are associated with enhanced reproductive efficiency and reduced involuntary culling compared to conventional systems. Breeding management continues to be the most crucial use of livestock monitoring technology in Europe, driven by the need for precise timing and the challenges of labor shortages in visual heat detection.

The heat stress management segment is expected to exhibit a noteworthy CAGR of 13.1% from 2026 to 2034 owing to rising ambient temperatures and the economic toll of thermal stress on productivity. Data indicates that Europe is experiencing a rise in frequency and intensity of extreme heat days and tropical nights, resulting in reduced summer milk production in southern and central regions due to increased animal heat stress. Monitoring systems now combine animal based sensors, such as elevated respiration rate and reduced rumination, with environmental data on temperature humidity and wind speed to generate real time heat stress indices. The European Commission promotes the adoption of climate-resilient farming practices, and studies show that proactive heat stress management, such as using alert systems to improve cooling, can mitigate declines in milk production and reproductive efficiency in Mediterranean dairy farms. National agricultural ministries in France and Germany have begun subsidizing thermal monitoring as part of climate resilience packages. Proactive heat stress management has become critical to maintaining welfare and productivity across European livestock industries, driven by predictions of increased future warming.

By Species Insights

In 2025, the cattle segment led the Europe livestock monitoring system market and accounted for a substantial share. The leading position of the segment is driven by its high individual value long production cycles and regulatory scrutiny on welfare and emissions. The EU is experiencing a consistent, long-term decline in total bovine populations (down roughly 5-9% over the last decade) and a parallel reduction in dairy cow numbers, while milk yields per cow continue to rise. The European Commission mandates detailed health and reproduction records for all dairy herds under the Integrated Administration and Control System which aligns seamlessly with digital monitoring data. There is a strong, growing trend in Western Europe toward adopting automated milking systems (AMS) and digital monitoring sensors (activity/rumination) to replace manual labor and improve herd health, particularly in larger, modernizing dairy operations. National breeding programs in the Netherlands Germany and Denmark require precise fertility data which monitoring systems provide automatically. Furthermore cattle’s size and docility make sensor attachment and data collection more reliable than in smaller or more active species. These economic regulatory and biological factors solidify cattle as the dominant species segment in the European monitoring landscape.

The poultry segment is predicted to witness the highest CAGR of 14.6% during the forecast period. The rapid growth of the segment is propelled by intensification of production biosecurity demands and EU animal welfare reforms. Poultry production in the EU showed a recovery in 2023, led by Poland, Spain, and France, driven by intensive industrial production systems. Monitoring systems now use computer vision microphones and environmental sensors to track feed conversion mortality vocal stress indicators and litter moisture in real time. Research is ongoing into the use of smart technologies (AI/Audio) to monitor broiler health for early disease detection to support antimicrobial reduction efforts, though specific high-percentage reductions directly attributed to these technologies are not formally recognized by EFSA in 2023. The EU’s updated Broiler Directive requires continuous welfare assessment which automated systems fulfill more reliably than manual scoring. Additionally integrators like PHW Group and Couche Tard are mandating monitoring data from contract growers to ensure brand compliance. Flock density is increasing and welfare regulations are tightening. As a result, the poultry sector is rapidly adopting scalable digital monitoring to maintain efficiency and compliance.

COUNTRY ANALYSIS

Netherlands Livestock Monitoring System Market Analysis

The Netherlands dominated the Europe livestock monitoring system market and captured a 21.4% share in 2025. This dominance is attributed to its ultra intensive livestock sector world class agri tech ecosystem and national commitment to digital farming. Dutch dairy farming is characterized by high cow density and a strong, increasing trend towards adopting automated, sensor-based monitoring systems to manage health and production, particularly in larger herds. The Dutch government provides various, often shifting, subsidies and incentives for sustainable and innovative agricultural technology, with a trend toward requiring data transparency for environmental and health tracking (e.g., in animal health monitoring systems). Companies like Lely and Nedap headquartered in the Netherlands export monitoring solutions globally while deploying them domestically at scale. Wageningen University serves as a research hub validating AI algorithms for lameness and ketosis prediction. There is a significant, ongoing trend toward automating farm management, with many Dutch dairy farms upgrading to integrated robotic systems to increase efficiency and data availability, although it is far from universa. This synergy of density policy innovation and infrastructure cements the Netherlands as the most advanced and penetrated market in Europe.

Germany Livestock Monitoring System Market Analysis

Germany followed closely in the Europe livestock monitoring system and held a 18.7% share in 2025. The expansion of the segment is driven by its vast dairy and pig sectors stringent animal welfare laws and strong engineering base for agricultural technology. The German livestock sector is experiencing a significant, long-term decline in animal numbers, coupled with a shift towards fewer, larger farms and increased legal requirements for animal welfare. Precision livestock farming technology adoption, particularly for reproductive monitoring in dairy and emission management in pig housing, is accelerating. Public funding in Germany is increasingly directed towards digitizing agricultural processes to improve sustainability and efficiency. German manufacturers like GEA and Big Dutchman supply monitoring hardware across Europe while integrating with domestic software platforms. This combination of regulatory pressure scale and industrial capability sustains Germany’s leadership in both volume and technological sophistication.

Denmark Livestock Monitoring System Market Analysis

Denmark maintains a noteworthy position in the Europe livestock monitoring system market due to its cooperative agricultural model science based policy and pioneering use of data for sustainability and health. Danish dairy farms extensively utilize national digital monitoring systems to track and reduce antibiotic use, resulting in one of the lowest antibiotic consumption rates in European dairy production. The Danish Veterinary and Food Administration mandates real time reporting of mortality and medicine use from poultry and pig farms which is fulfilled through integrated monitoring systems. Research institutions like Aarhus University have developed validated algorithms for predicting calving time and lameness using accelerometer data now deployed nationwide. Regulatory, mandatory measures on nitrogen application and improved precision feeding techniques have successfully lowered the average nitrogen surplus and excretion per cow across Danish farms, contributing to a significant decline in overall agricultural nitrogen pollution into the environment. Strong farmer cooperatives like Arla are driving standardization while government backing supports data-driven compliance. As a result, Denmark represents a high-adoption, high-impact market within Northern Europe.

France Livestock Monitoring System Market Analysis

France is a major part of the Europe livestock monitoring system market owing to national digital agriculture initiatives and rising pressure to reduce antibiotic use in its large cattle and poultry sectors. FranceAgriMer reports indicate a slightly declining or stable total compound feed production, accompanied by an increased adoption of precision monitoring technologies for animal health and efficiency. The French government supports digital innovation and IoT adoption in agriculture. The French Agency for Food Environmental and Occupational Health and Safety now recognizes automated heat detection data as valid for official fertility records easing administrative burden. In key French livestock areas, advanced monitoring systems for cattle health and automated welfare surveillance in poultry are becoming standard. As labor shortages intensify and environmental regulations tighten French farms are rapidly transitioning to data driven management making France a dynamic and policy led market.

Sweden Livestock Monitoring System Market Analysis

Sweden is predicted to expand in the Europe livestock monitoring system market over the forecast period due to its early adoption of welfare focused monitoring systems strong public investment in rural connectivity and leadership in sustainable livestock practices. Swedish dairy farms are rapidly adopting automated technology for health monitoring and breeding, supported by various environmental and investment subsidies. The Swedish University of Agricultural Sciences has pioneered research on predictive lameness detection using gait analysis now commercialized by Swedish startups like HerdDogg. Major Swedish operators are aggressively upgrading 4G and 5G networks, focusing on rural and remote northern areas to ensure high-speed connectivity. Additionally the country’s strict animal welfare laws prohibit tethering and mandate daily health checks which digital systems fulfill more consistently than manual methods. This blend of regulatory foresight technological infrastructure and research excellence positions Sweden as an innovation leader in the European livestock monitoring landscape.

COMPETITIVE LANDSCAPE

The Europe livestock monitoring system market features dynamic competition among established agricultural technology firms specialized sensor developers and emerging AI startups. While large players like DeLaval and Lely dominate through integrated robotic ecosystems niche companies differentiate via superior sensor accuracy open data policies or species specific algorithms. The market is highly innovation driven with competition centered on predictive capability ease of use data ownership transparency and regulatory alignment with EU animal welfare and antibiotic reduction goals. Fragmentation persists due to divergent national subsidy programs rural connectivity gaps and varying levels of farmer digital literacy. However the trend is shifting toward holistic platforms that combine hardware software and advisory services rather than standalone devices. As climate adaptation and carbon reporting become mandatory the ability to link animal monitoring data to environmental metrics will further reshape competitive dynamics favoring companies with robust data infrastructure and cross sector partnerships.

KEY MARKET PLAYERS

Key market players that are dominating the Europe livestock monitoring system market

- Afimilk Ltd. (Israel)

- BouMatic LLC (U.S.)

- Lely Holding Sàrl

- Nedap Livestock Management

- DeLaval International AB

- SCR Dairy, Inc. (Israel)

- DeLavall (Sweden)

- GEA Group AG (Germany)

- DairyMaster (Ireland)

- SUM-IT Computer Systems, Ltd. (U.K.)

- Valley Agriculture Software (U.S.).

Top Players In The Market

- DeLaval International AB is a Sweden based global leader in dairy farming solutions with a strong presence in the Europe livestock monitoring system market through its integrated activity rumination and milking monitoring technologies. The company contributes globally by embedding real time health and fertility alerts into its robotic milking and feeding ecosystems used on thousands of farms worldwide. In Europe DeLaval supports compliance with animal welfare and antibiotic reduction mandates by providing predictive analytics for early disease detection. It also expanded its remote diagnostics service network across Eastern Europe to ensure rapid technical support. These initiatives reinforce DeLaval’s role as a holistic partner in data driven and sustainable dairy production across the continent.

- Lely Holding Sàrl is a Netherlands headquartered innovator in agricultural robotics and livestock monitoring with a significant footprint in the European dairy sector. The company supplies smart cow collars robotic milking systems and centralized farm management platforms that enable real time monitoring of health fertility and feeding behavior. Lely contributes globally by pioneering sensor fusion technologies that combine movement rumination and milk conductivity data to predict metabolic disorders. The company also opened a digital training academy in Germany to help farmers interpret monitoring data and improve decision making. These efforts position Lely at the forefront of precision livestock farming by merging hardware intelligence with actionable farm insights.

- Nedap Livestock Management is a Dutch technology firm specializing in wearable monitoring solutions for dairy and beef cattle with a growing influence across European farming communities. The company’s CowLine and Velos systems use advanced accelerometers and rumination sensors to deliver accurate estrus detection and health alerts. Nedap contributes globally by offering open architecture platforms that integrate with third party feeding and milking systems fostering interoperability. It also partnered with national cooperatives in France and Denmark to link monitoring data with genetic and milk recording databases. These actions strengthen Nedap’s position as a flexible and farmer centric provider committed to transparency and data utility in Europe’s evolving digital agriculture landscape.

Top Strategies Used By The Key Market Participants

Key players in the Europe livestock monitoring system market focus on integrating hardware with advanced software analytics to deliver predictive rather than reactive insights on animal health and productivity. They invest in artificial intelligence and machine learning to enhance accuracy in estrus detection lameness prediction and heat stress alerts using multimodal sensor data. Companies expand regional service and training networks to support farmers in data interpretation and system maintenance particularly in Eastern Europe. Strategic partnerships with cooperatives national databases and research institutions validate algorithms and enable benchmarking. Additionally they design open platform architectures to ensure interoperability with feeding milking and herd management systems thereby reducing vendor lock in and increasing farmer trust in long term digital transformation.

MARKET SEGMENTATION

This research report on the Europe livestock monitoring system market is segmented and sub-segmented into the following categories.

By Offering

- Hardware

- Software

- Services

By Application

- Breeding management

- Feeding management

- Milk harvesting management

- Heat stress management

- Animal comfort management

- Other applications

By Species

- Poultry

- Swine

- Cattle

- Equine

- Others

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

Why are European farmers adopting livestock monitoring systems?

They want real-time insights into animal health without constant physical inspection.

What problem do monitoring systems solve on large dairy farms?

They detect early signs of illness before productivity drops noticeably.

How does wearable sensor technology improve herd management?

Activity tracking helps identify breeding cycles and health irregularities quickly.

Why is data accuracy important in livestock monitoring?

Reliable data prevents false alerts and unnecessary veterinary intervention.

How do monitoring systems support animal welfare standards in Europe?

Continuous observation ensures animals are managed according to regulatory guidelines.

What operational benefit do farmers notice after implementation?

Labor time shifts from manual checking to data-based decision-making.

Why are milk yield analytics integrated into monitoring platforms?

Production trends help optimize feeding and breeding strategies.

How does remote access change livestock management practices?

Farmers can monitor herds from mobile devices without being physically present.

Why are small farms cautious about adopting monitoring technology?

Initial investment and system learning curves can be concerns.

How does livestock monitoring reduce economic losses?

Early disease detection minimizes treatment costs and production downtime.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com