Europe Marine Composites Market Size, Share, Trends, & Growth Forecast Report By Composite Type (Metal Matrix Composite (MMC), Ceramic Matrix Composite (CMC), and Polymer Matrix Composite (PMC)), Fiber Type, Resin Type, Vessel Type, Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic & Rest of Europe), Industry Analysis From 2026 to 2034

Europe Marine Composites Market Size

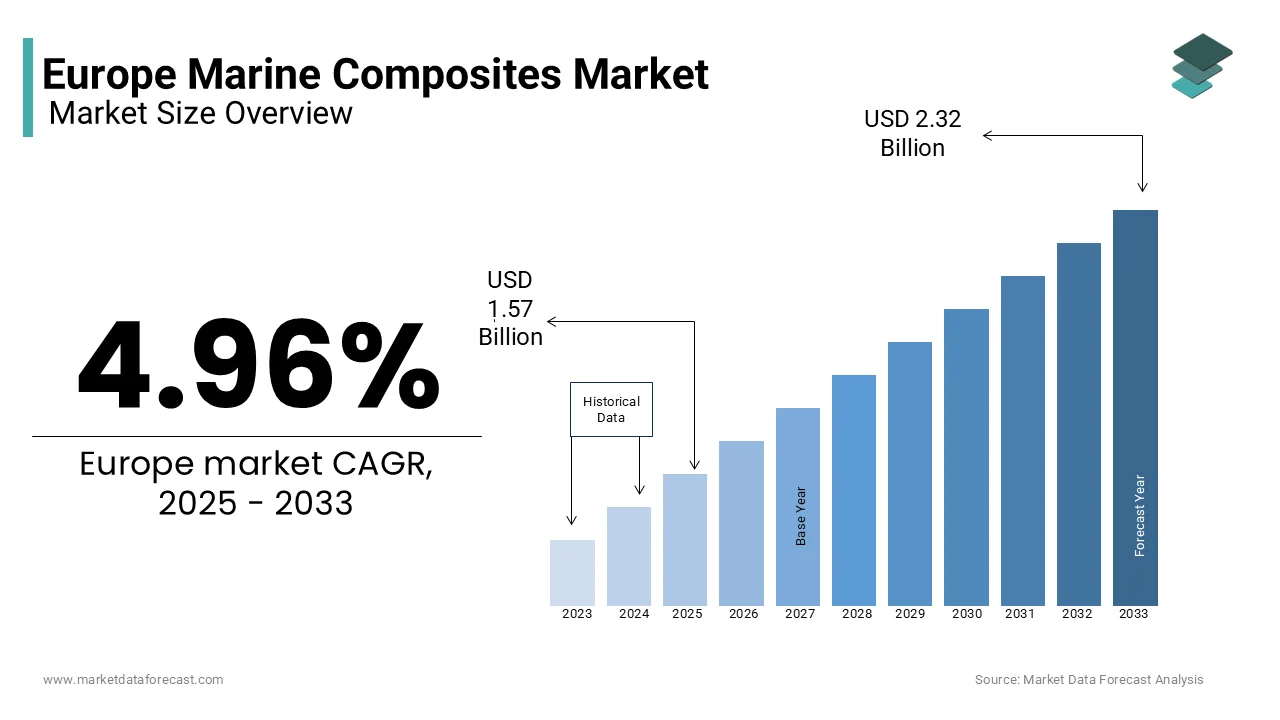

The Europe marine composites market was size was valued USD 1.57 billion in 2025 and is anticipatd to reach USD 1.65 billion in 2026 to reach USD 2.43 billion by 2034, growing at a CAGR of 4.96% from 2026 to 2034.

Marine composites are high-performance materials created by combining two or more distinct substances, typically a fiber reinforcement and a resin matrix, specifically engineered to withstand harsh saltwater environments. These materials, primarily comprising glass fiber, carbon fiber, and aramid fibers embedded in thermoset or thermoplastic resin matrices, offer superior strength-to-weight ratios, corrosion resistance, and design flexibility compared to traditional steel or aluminum. The strategic shift toward composites is driven by the urgent need to enhance fuel efficiency and reduce emissions across the European shipping fleet. As per the International Maritime Organization (IMO), the maritime sector accounts for approximately 3% of global greenhouse gas emissions, while EMSA reports indicated it constitutes roughly 3–4% of the EU's total CO2 emissions. This has prompted regulatory pressure to adopt lighter hull materials that lower energy consumption. The European Union has mandated a reduction in the greenhouse gas intensity of energy used on board by 6% by 2030 under the FuelEU Maritime regulation (part of the Fit for 55 package), alongside the IMO’s separate target to reduce carbon intensity by at least 40% by 2030. These distinct mandates incentivize shipbuilders to utilize composite solutions for superstructures and hulls to ensure compliance. Furthermore, the region boasts a robust recreational boating industry, with an estimated fleet of over 6 million leisure boats in European waters, serving as a primary testing ground for high-performance composite applications. The presence of major naval defense programs in nations like France and Italy further accelerates adoption, as modern warships increasingly rely on non-magnetic composite materials for mine countermeasure vessels to ensure operational safety. This convergence of environmental mandates, recreational demand, and defense modernization defines the current operational landscape of the market.

PRIMARY MARKET DRIVERS

Stringent Environmental Regulations Driving Lightweighting Initiatives

The European Union’s implementation of aggressive decarbonization targets is a paramount driver for the adoption of these high-performance materials and the overall Europe marine composites market. Weight reduction is critical for achieving fuel efficiency goals. The International Maritime Organization and EU regulations now require significant cuts in sulfur oxides and carbon dioxide emissions, forcing naval architects to seek materials that minimize vessel displacement without compromising structural integrity. European maritime policy is driving a rapid transition toward carbon neutrality, forcing shipbuilders to move beyond traditional heavy materials to meet increasingly strict legal standards. Composite materials can reduce hull weight compared to steel, leading to a proportional decrease in fuel consumption and emissions during operation. This physical advantage is particularly vital for the growing sector of electric and hybrid propulsion ferries, where battery weight is a limiting factor. The move toward electric propulsion for shorter sea routes is placing a premium on vessel lightweighting to offset the significant weight of modern battery systems. Additionally, the corrosion resistance of composites eliminates the need for heavy anti-fouling paints and frequent maintenance docking, further reducing the lifecycle environmental footprint. Shipbuilders in Norway and the Netherlands are already deploying all-composite high-speed passenger ferries to comply with zero-emission zone regulations in fjords and harbors. This regulatory ecosystem ensures that the demand for lightweight composite solutions will remain inextricably linked to compliance strategies across the European maritime domain.

Expansion of the Luxury Yacht and Recreational Boating Sector

The robust performance of the luxury yacht and recreational boating industry in the region has fuelled the growth of the Europe marine composites market. This growth is primarily driven by the demand for high-performance aesthetics and customization. Europe remains the global epicenter for superyacht construction, with countries like Italy, Germany, and the Netherlands accounting for a significant share of the global superyacht building capacity. The European boating landscape remains a vital economic pillar, driving continuous investment in high-performance materials as the industry expands. High-net-worth individuals increasingly demand vessels that offer superior speed, stability, and interior design flexibility, attributes that are best achieved through composite construction. The ability to mold complex hydrodynamic shapes and integrate structural components into single pieces reduces assembly time and enhances performance characteristics such as vibration damping and noise reduction. Recent trends show a surge in orders for vessels exceeding 24 meters in length, with builders utilizing carbon fiber extensively to maximize deck space and stability while maintaining sleek profiles. The Mediterranean and Baltic regions serve as key hubs where charter companies and private owners prioritize low-maintenance materials that withstand harsh saline environments without degradation. This sustained investment in high-end leisure maritime assets ensures a steady flow of contracts for composite manufacturers who can deliver the precision and quality required by this discerning segment. The cultural significance of boating in coastal European nations further cements this sector as a resilient driver of material innovation and volume consumption.

KEY MARKET RESTRAINTS

Volatility in Raw Material Prices and Supply Chain Instability

Raw material cost fluctuations and supply chain disruptions are major concerns for the European Marine Composites Market. These factors significantly hinder project feasibility and the broad adoption of these materials. The production of marine grade composites relies heavily on petrochemical-derived resins such as epoxy, polyester, and vinyl ester, as well as energy-intensive fibers like carbon and glass, all of which are subject to global commodity price volatility. According to sources, the producer prices for chemical intermediates in the European Union experienced swings in recent years due to energy crises and geopolitical tensions, directly impacting the cost structure of boat builders. The reliance on imported carbon fiber precursors from outside Europe exacerbates this vulnerability, as logistics bottlenecks can lead to significant delays in production schedules for large vessel projects. Small and medium-sized shipyards, which constitute a large portion of the European marine manufacturing base, often lack the financial buffers to absorb these sudden cost increases, forcing them to delay orders or revert to cheaper, heavier alternatives. Furthermore, the shortage of skilled labor capable of handling advanced composite layup processes compounds the issue, as training new workers takes time and resources that are strained during periods of economic uncertainty. The inconsistency in supply availability makes long-term planning difficult for naval architects who must guarantee delivery dates to clients. This economic instability creates a barrier to entry for new composite applications in commercial shipping, where profit margins are already thin and sensitive to material cost variations. Supply chains must stabilize and pricing must become more predictable. Until then, the growth potential of the market will remain partially capped by these financial risks.

Complex Recycling Challenges and End-of-Life Disposal Issues

The lack of established and economically viable recycling infrastructure for end-of-life marine composites serves as a major restraint to the Europe marine composites market. This situation directly conflicts with the European Union's circular economy ambitions.Unlike metals which can be easily melted down and reused, thermoset composites used in marine applications are notoriously difficult to separate into their constituent fibers and resins, leading to significant waste management challenges. As per guidelines from the European Environment Agency, the disposal of composite materials often results in landfilling or incineration, practices that are increasingly frowned upon and regulated under stricter waste directives. The marine industry faces a looming wave of decommissioned vessels as the first generation of mass-produced fiberglass boats from the 1970s and 1980s reaches the end of its service life, creating a mounting waste stream that current facilities cannot adequately handle. The high cost of mechanical or thermal recycling processes makes reclaimed fibers less competitive than virgin materials, discouraging shipbuilders from adopting recycled content in new constructions. Regulatory pressure is mounting, with proposals to extend producer responsibility schemes to include the maritime sector, which would force manufacturers to bear the cost of disposal. This potential liability increases the total cost of ownership for composite vessels and dampens enthusiasm for their use in cost-sensitive segments. Achieving a breakthrough in chemical recycling or a unified European framework for composite waste is essential. Without these, the environmental paradox of "green" materials creating persistent waste will continue to hinder market expansion and draw scrutiny from sustainability-focused investors.

EMERGING MARKET OPPORTUNITIES

Development of Bio-Based and Sustainable Composite Materials

The transition toward bio-based resins and natural fiber reinforcements provides a transformative opportunity for the Europe Marine Composites Market. This shift allows the industry to align with stringent sustainability goals and differentiate its products. European research institutions and chemical companies are pioneering the development of resins derived from plant oils and fibers sourced from flax, hemp, and basalt, which offer a reduced carbon footprint compared to traditional petroleum-based counterparts. European bioplastics capacity is seeing steady growth driven by EU packaging and circular economy policies, gradually increasing the availability of renewable materials for specialized industrial use. These sustainable composites appeal to environmentally conscious yacht owners and commercial operators seeking to minimize the lifecycle impact of their vessels. Natural fibers like flax, which is abundantly cultivated in France and Belgium, provide excellent vibration damping properties and lower density, making them ideal for interior panels and non-structural components of leisure boats. Major shipbuilders are beginning to integrate these materials into flagship projects to demonstrate corporate social responsibility and comply with emerging green procurement policies. The European Union's Horizon Europe funding program is actively supporting projects that validate the durability and performance of bio-composites in harsh marine environments, accelerating their commercial readiness. As technology matures, the cost gap between bio-based and conventional materials is expected to narrow, opening up new market segments that were previously price-sensitive. This shift not only addresses disposal concerns but also creates a unique selling proposition for European manufacturers in the global export market, positioning the region as a leader in green maritime innovation.

Integration of Composites in Offshore Wind Energy Infrastructure

The offshore wind energy sector in the region is experiencing explosive growth, which is likely to contribute to the expansion of the Europe marine composites market. This development offers a lucrative avenue for applying large-scale marine composites in turbine blades and floating platform structures. Europe is the global leader in offshore wind capacity, with plans to install 111 gigawatts by 2030 as part of its renewable energy strategy, necessitating the construction of thousands of massive turbine components. As per data from WindEurope, the average size of newly installed turbines is increasing, with rotor diameters exceeding 200 meters, requiring blades made entirely of advanced composite materials to maintain structural integrity while minimizing weight. The push toward floating wind farms in deeper waters further amplifies this opportunity, as floating platforms benefit significantly from the corrosion resistance and buoyancy characteristics of composite materials compared to steel concrete hybrids. Manufacturers are exploring the use of thermoplastic composites for blades to enable faster production cycles and easier recyclability at the end of the turbine's life. The proximity of European composite supply chains to major wind farm installation sites in the North Sea and Baltic Sea provides a logistical advantage for delivering these oversized components. Government subsidies and long-term power purchase agreements de-risk investments in this sector, ensuring a steady demand pipeline for composite fabricators. This synergy between the maritime and renewable energy sectors allows composite manufacturers to diversify their revenue streams beyond traditional boat building, leveraging their expertise in large-scale molding and marine-grade durability to support the continent's energy transition.

CRITICAL MARKET CHALLENGES

Shortage of Specialized Labor and Technical Expertise

The acute shortage of skilled technicians and engineers proficient in advanced composite manufacturing techniques and repair methodologies continues to be an obstacle for the Europe Marine Composites Market. The fabrication of marine vessels using carbon fiber and complex resin systems requires highly specialized knowledge in layup procedures, vacuum infusion, and curing processes that cannot be easily automated or learned through general vocational training. According to the European Boating Industry, the sector faces a demographic cliff as a significant portion of the experienced workforce approaches retirement age, while insufficient numbers of young professionals are entering the field to replace them. This skills gap leads to production bottlenecks, increased error rates, and higher labor costs, which erode the competitive advantage of European shipyards against Asian competitors with larger labor pools. The complexity of modern composite designs, which often involve intricate sandwich structures and integrated sensor systems, further elevates the training requirements. Educational institutions have been slow to update curricula to match the evolving technological demands of the industry, resulting in a mismatch between graduate skills and employer needs. Companies are forced to invest heavily in internal training programs, which strains resources and delays project timelines. Without a coordinated effort to promote careers in marine composites and standardize certification across the EU, the labor shortage will remain a critical constraint on the industry's ability to scale up production and innovate. This human capital deficit threatens to stall the adoption of next-generation composite technologies despite strong market demand.

High Initial Capital Investment and Certification Barriers

Setting up advanced composite manufacturing facilities requires substantial capital expenditure, which negatively impacts the Europe marine composites market. Additionally, navigating rigorous certification processes acts as a formidable barrier to market entry and expansion. Establishing a production line capable of handling large marine composite structures involves significant investment in autoclaves, large-format molds, robotic layup systems, and ventilation infrastructure to manage volatile organic compounds. As per industry benchmarks, the cost of equipping a modern composite shipyard can exceed several million euros, a figure that is prohibitive for small and medium-sized enterprises without access to substantial financing. Furthermore, the maritime industry is heavily regulated, with classification societies such as DNV, Lloyd's Register, and Bureau Veritas imposing strict testing and validation protocols for any new composite material or design before it can be approved for use. The certification process is time-consuming and expensive, often taking years to complete, which delays the return on investment for innovators. This regulatory rigor, while necessary for safety, creates a conservative environment where shipowners and builders are hesitant to adopt unproven composite solutions due to fear of insurance complications or operational downtime. The high upfront costs combined with the lengthy approval timelines discourage experimentation and slow the pace of technological diffusion within the market. Consequently, only large conglomerates with deep pockets can afford to lead the transition to advanced composites, potentially stifling competition and limiting the diversity of solutions available to the broader European maritime sector.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 4.96% |

| Segments Covered | By Composite Type, Fiber Type, Resin Type , Vessel Type, and Country |

| Various Analyses Covered | Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

| Countries Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, and Rest of Europe |

| Market Leaders Profiled | Toray Industries, Inc., Owens Corning, Nippon Electric Glass Co., Ltd., Huntsman International LLC, SGL Carbon SE, Hexcel Corporation, DowDuPont Inc., Compagnie de Saint-Gobain S.A., Weyerhaeuser Company, Momentive Performance Materials, Inc., Solvay SA, China Jushi Co., Ltd., 3A Composites GmbH (Schweiter Technologies), GMS Composites, Gurit AG, Hyosung Marine Co. Ltd., Teijin Limited, and Zoltek Corporation (Toray Industries). |

SEGMENTAL ANALYSIS

By Composite Insights

The Polymer Matrix Composites (PMC) segment dominated the Europe Marine Composites Market and accounted for a substantial share in 2025. The material's unparalleled balance of corrosion resistance, design flexibility, and cost-effectiveness aligns perfectly with the harsh saline environments of European waters, and drives the dominance of this segment. Among these, the main factor for this domination is the extensive use of glass fiber reinforced plastics in the region's massive recreational boating sector. According to the European Boating Industry, there are over 6 million leisure boats registered across Europe, the vast majority of which utilize PMC hulls and decks due to their durability and low maintenance requirements compared to steel or aluminum. Furthermore, the established manufacturing infrastructure for resin transfer molding and hand lay-up processes in countries like Italy and France creates a high barrier to entry for alternative matrix types. In addition, this segment is supported by the adaptability of PMCs for large-scale structures such as wind turbine blades used in offshore installations. Data from WindEurope indicates that the continent plans to install 111 gigawatts of offshore wind capacity by 2030, requiring millions of tons of epoxy and polyester-based composites for blade construction. The ability of PMCs to be molded into complex hydrodynamic shapes while maintaining structural integrity at a fraction of the weight of metals makes them the default choice for naval architects. Additionally, the continuous improvement in vinyl ester and epoxy resin formulations has enhanced the fire resistance and mechanical properties of PMCs, allowing their penetration into commercial ferry and defense vessel markets where safety standards are rigorous.

The Ceramic Matrix Composite (CMC) segment is anticipated to witness the fastest CAGR of 9.4% between 2026 and 2034. This accelerated growth is fueled by the increasing demand for materials capable of withstanding extreme thermal and mechanical stresses in high-performance marine propulsion and defense applications. Apart from these, a major driver is the modernization of European naval fleets, where CMCs are increasingly utilized in gas turbine components and exhaust systems to improve fuel efficiency and reduce heat signatures. As per sources, member states have committed to increasing defense spending to meet NATO targets, leading to significant procurement budgets for next-generation frigates and destroyers that incorporate advanced thermal protection systems. CMCs offer superior temperature resistance compared to metal alloys, allowing engines to operate at higher efficiencies which is critical for reducing the carbon footprint of military vessels. A different factor driving this growth is the emergence of hypersonic and high-speed maritime technologies where traditional materials fail under aerodynamic heating. Research institutions in Germany and the United Kingdom are actively developing silicon carbide-based CMCs for specialized underwater vehicles and sensor housings that require exceptional hardness and wear resistance. The European Union's Horizon Europe program has allocated substantial funding for advanced material research, specifically targeting ceramic composites for dual-use maritime applications. These technologies are maturing from the laboratory to commercial production. Consequently, the adoption of CMCs in niche but high-value marine sectors is expected to surge, outpacing the growth of traditional polymer-based solutions.

By Fiber Insights

In 2025, the Glass Fiber segment remained the largest segment in the Europe Marine Composites Market and captured a significant share. This position of the glass fiber is supported by the economic viability and proven performance of glass fiber reinforced polymers in the construction of small to medium-sized vessels which constitute the bulk of European maritime traffic. The top factor for this segment is the sheer volume of the recreational boating industry, where cost sensitivity dictates material selection. According to research, traditional glass fiber remains the primary structural material for the mass-market boating industry due to its proven reliability and low material cost. Glass fiber offers an optimal strength-to-cost ratio that carbon fiber cannot match for non-critical structural applications, making it the standard for mass production. An additional driver is the extensive use of glass fiber in the repair and maintenance sector across Europe's aging fleet. With thousands of kilometers of coastline and a high density of marinas, the demand for glass fiber mats and cloths for routine upkeep and collision repair remains consistently high. The aging of the global shipping fleet is driving a major market for maintenance and repair services, though traditional metals still dominate the commercial cargo sector. Furthermore, advancements in recycling technologies for glass fiber are beginning to address end-of-life concerns, enhancing its sustainability profile. The widespread availability of raw materials and the deep expertise of the European workforce in handling glass fiber ensure that it will remain the backbone of the marine composites industry for the foreseeable future.

The Carbon Fiber segment is likely to experience the fastest CAGR of 8.7% during the forecast period owing to the intensifying pursuit of lightweighting to meet stringent emissions regulations and enhance vessel performance. Moreover, the leading cause for this segment is the luxury yacht sector, where owners demand larger deck spaces and higher speeds without increasing displacement. As per statistics from the Superyacht Builders Association, European shipyards deliver over 50% of the world's superyachts, increasingly utilizing carbon fiber for hulls, masts, and superstructures to achieve weight reductions of up to 30% compared to aluminum. This material allows for sleeker designs and improved fuel efficiency, which is becoming a key selling point for environmentally conscious buyers. One more point that adds strength is the adoption of carbon fiber in high-speed electric ferries and hydrofoils. The European Union's push for zero-emission transport has spurred projects like the "Sea Bubble" and various electric foil-assisted commuters that rely on the high stiffness and low weight of carbon fiber to maximize battery range and payload capacity. Data from the International Council on Clean Transportation highlights that electrification of short-sea shipping is impossible without drastic weight reduction, making carbon fiber indispensable. Additionally, the defense sector is integrating carbon fiber into mine countermeasure vessels to ensure non-magnetic signatures, further boosting demand. As production costs gradually decrease and automated laying techniques improve, carbon fiber is transitioning from a niche luxury material to a critical component for sustainable maritime mobility.

By Vessel Insights

The power boats segment led the Europe Marine Composites Market and held a 45.7% share in 2025 because of the immense popularity of motorized leisure activities across the continent and the specific suitability of composites for high-speed hull designs. The main thing making this grow is the cultural significance of boating in Mediterranean and Northern European nations, where power boats are the preferred choice for coastal tourism and weekend recreation. According to studies, sales of power boats consistently outpace sailboats, with hundreds of thousands of units sold annually, each requiring significant quantities of composite materials for hulls, decks, and internal structures. The versatility of composites allows manufacturers to create complex planing hull shapes that optimize fuel efficiency and stability at high speeds, a critical requirement for this vessel type. Added support for this segment comes from the expansion of the commercial workboat sector, including patrol boats, pilot vessels, and crew transfer vessels for the offshore wind industry. Data from the Global Wind Organisation indicates that Europe leads the world in offshore wind operations, necessitating a large fleet of fast, durable crew transfer vessels that almost exclusively utilize composite construction to withstand harsh sea states while minimizing weight. The corrosion resistance of composites is particularly valued in these commercial applications where downtime for maintenance must be minimized. Furthermore, the trend towards larger, more luxurious power catsamarans and explorer yachts continues to drive up the volume of composite materials per unit. The combination of high-volume recreational production and specialized commercial demand solidifies the power boat segment as the primary consumer of marine composites in the region.

The Cruise Ships segment is on the rise and is expected to be the fastest growing segment in the market by witnessing a CAGR of 7.9% over the forecast period due to the industry's shift towards constructing larger, more energy-efficient vessels that incorporate advanced composite materials for superstructures and interior fittings. The primary driver is the "green cruising" initiative, where major operators based in Europe are under pressure to reduce emissions per passenger kilometer. As per Cruise Lines International Association Europe, newbuild orders are increasingly specifying composite materials for upper decks and funnels to lower the vessel's center of gravity and reduce overall weight, thereby improving fuel economy. Modern cruise ships are becoming floating cities, and the use of lightweight composites allows for additional amenities and passenger capacity without exceeding port draft limits. This segment is also shaped by the stringent fire safety and hygiene standards that composites can meet through advanced resin systems. The European Union's maritime safety regulations require materials that offer superior fire resistance and low smoke toxicity, prompting shipyards in Italy, Germany, and Finland to adopt specialized fire-retardant composite panels for cabins, galleys, and public areas. The trend towards modular construction, where entire cabin units are prefabricated using composite sandwich panels off-site and then installed, significantly reduces build time and labor costs. This method is gaining traction as shipyards strive to meet tight delivery schedules for record-breaking vessel sizes. As the cruise industry rebounds and expands its fleet with next-generation eco-friendly ships, the demand for high-performance marine composites in this segment will surge.

COUNTRY-LEVEL ANALYSIS

Italy Marine Composites Market Analysis

Italy dominated the Europe Marine Composites Market and accounted for a 24.8% share in 2025. The growth of the Italian market is driven by its status as the world's premier hub for luxury yacht construction. The country's market position also shows a dense cluster of world-renowned shipyards in regions like Liguria, Tuscany, and Marche, which specialize in building high-value superyachts that rely heavily on advanced carbon and glass fiber composites. A primary driving factor is the concentration of top-tier brands such as Ferretti, Benetti, and Sanlorenzo, which collectively account for a significant portion of global superyacht deliveries. According to sources, the sector generates billions in export revenue annually, with composite materials representing a substantial portion of the production cost. Along with this, the country’s market is driven by the deep integration of the supply chain, where local manufacturers of resins, fibers, and core materials work closely with shipyards to develop customized solutions. This proximity fosters rapid innovation in molding techniques and material performance. Furthermore, the Italian government supports the sector through incentives for technological modernization and sustainability, encouraging the adoption of bio-based resins and recycling initiatives. The cultural heritage of craftsmanship combined with cutting-edge engineering ensures that Italian shipyards remain at the forefront of composite utilization. The demand for bespoke, high-performance vessels from international clients ensures a steady and high-volume consumption of premium marine composites, securing Italy's dominant position in the regional landscape.

Germany Marine Composites Market Analysis

Germany was the next prominent country in the Europe Marine Composites Market and occupied a 17.9% share in 2025. The expansion of the German market is propelled by its strong engineering base and leadership in both commercial shipbuilding and offshore wind infrastructure. The country's market status is known for a focus on high-tech applications, including sophisticated naval vessels, luxury motor yachts, and massive wind turbine blades. A key driving factor is the presence of major industrial conglomerates and specialized shipyards like Lürssen and Blohm+Voss, which construct some of the world's most complex composite vessels for defense and private clients. According to research, the sector invests heavily in research and development, particularly in automating composite layup processes to enhance precision and reduce labor costs. A further key driver is Germany's pivotal role in the European offshore wind energy transition. A study shows that the country is a leading installer of offshore wind farms, creating immense demand for large-scale composite blades manufactured by companies like Siemens Gamesa. The push for hydrogen-powered ships and electric ferries further accelerates the need for lightweight composite structures to maximize energy efficiency. German regulatory frameworks emphasize sustainability and circular economy principles, pushing manufacturers to develop recyclable composite solutions. The combination of high-value yacht building, robust defense contracts, and a booming renewable energy sector creates a diverse and resilient demand profile for marine composites in Germany.

France Marine Composites Market Analysis

France served as a key market for marine composites in Europe. It is supported by a powerful combination of naval defense programs and a vibrant recreational boating industry. The country's market status is unique due to the significant influence of state-led defense projects that utilize advanced composites for mine countermeasure vessels and frigates. A primary driving factor is the strategic modernization of the French Navy, led by entities like Naval Group, which increasingly incorporates composite materials to reduce magnetic signatures and enhance survivability. As per sources, defense spending has increased to support the construction of next-generation patrol boats and submarines that rely on non-magnetic composite components. A further reason for this growth is the strong leisure boating culture along the Atlantic and Mediterranean coasts, supported by major manufacturers like Beneteau and Jeanneau. These companies produce vast numbers of sailboats and powerboats for the global market, utilizing glass fiber composites extensively. Research indicates that the sector is a major exporter, driving consistent demand for raw materials. Additionally, France is a leader in research regarding bio-sourced composites, leveraging its agricultural sector to produce flax and hemp fibers for marine applications. This dual engine of high-tech defense manufacturing and mass-market leisure production ensures France remains a critical pillar of the European marine composites ecosystem.

Netherlands Marine Composites Market Analysis

The Netherlands is moving ahead steadfastly in the Europe marine composites market due to its specialization in inland waterway vessels, high-performance workboats, and innovative composite technologies. The country's market status is defined by its extensive network of rivers and canals, which necessitates a specific type of vessel design where composites offer distinct advantages in durability and weight. Apart from these, a major driving factor is the dominance of the Dutch shipbuilding sector in constructing specialized vessels such as tugboats, pilot boats, and crew transfer vessels for the North Sea oil and gas and wind industries. According to studies, the country is a global leader in building efficient, low-emission workboats that increasingly utilize composite hulls to reduce fuel consumption and increase payload. The second driver is the nation's commitment to innovation and sustainability, hosting numerous research institutes and startups focused on advanced recycling and bio-composite development. The Dutch government's aggressive climate goals have spurred the adoption of electric and hybrid propulsion systems in shipping, which rely on lightweight composite structures to extend battery range. Furthermore, the presence of major resin and chemical companies in the Rotterdam port area provides a robust local supply chain for marine-grade materials. The synergy between practical inland waterway needs, offshore energy support, and a forward-looking regulatory environment positions the Netherlands as a dynamic and growing market for marine composites.

United Kingdom Marine Composites Market Analysis

The United Kingdom is likely to grow notably in the European market from 2026 to 2034 owing to a strong focus on high-performance racing yachts, specialized naval vessels, and offshore energy support. The country's market status is influenced by its rich maritime heritage and its role as a hub for cutting-edge marine technology and design. A primary driving factor is the UK's prominence in the superyacht refit and custom build sector, particularly in the South of England, where shipyards utilize advanced carbon fiber composites to enhance the performance of racing and luxury vessels. The second driver is the robust defense sector, with the Royal Navy investing in composite technologies for minehunters and patrol vessels to ensure operational superiority. The UK's leadership in offshore wind energy also contributes significantly, with major manufacturing facilities producing turbine blades and floating platform components using marine-grade composites. Sources indicate growing investment in floating wind technologies, which rely heavily on composite materials for buoyancy and structural integrity. Despite Brexit-related challenges, the UK's expertise in engineering and design continues to attract international projects, maintaining its position as a key player in the specialized segments of the European marine composites market.

COMPETITIVE LANDSCAPE

The competition in the Europe Marine Composites Market is characterized by a dynamic interplay between global material giants and specialized regional providers who vie for dominance through technological superiority and service excellence. Major multinational corporations leverage their extensive research capabilities to introduce next generation fibers and resins that set new benchmarks for strength and durability. These large entities often compete on the breadth of their product portfolios and their ability to provide integrated solutions ranging from raw materials to engineering consulting. Regional players differentiate themselves by offering highly responsive customer service and flexible manufacturing capabilities that can adapt quickly to specific shipyard requirements. The intensity of rivalry is heightened by the critical nature of the products where material failure can lead to catastrophic consequences for vessels operating in harsh seas. Consequently trust and proven track records become significant barriers to entry for new competitors. Price competition exists but is often secondary to quality assurance and regulatory compliance which are paramount for buyers in the defense and commercial shipping sectors. Strategic alliances and long term contracts are common as suppliers seek to secure key accounts amidst growing demand for lightweight and sustainable solutions. This environment fosters a culture of constant improvement where only those who can consistently deliver innovation and reliability thrive in the market.

KEY MARKET PLAYERS

The major players in the Europe marine composites market include

- Toray Industries, Inc.

- Owens Corning

- Nippon Electric Glass Co., Ltd.

- Huntsman International LLC

- SGL Carbon SE

- Hexcel Corporation

- DowDuPont Inc

- Compagnie de Saint-Gobain S.A.

- Weyerhaeuser Company

- Momentive Performance Materials, Inc.

- Solvay SA

- China Jushi Co., Ltd.

- 3A Composites GmbH (Schweiter Technologies)

- GMS Composites

- Gurit AG

- Hyosung Marine Co. Ltd.

- Teijin Limited

- Zoltek Corporation (Toray Industries).

Top Players In The Market

- Owens Corning stands as a global titan in the production of glass fiber reinforcements which are fundamental to the Europe Marine Composites Market. The company supplies advanced E glass and S glass fibers that enable shipbuilders to construct durable and lightweight vessels capable of withstanding harsh marine environments. Their contribution to the global market is defined by continuous innovation in resin compatibility and fiber performance which sets industry standards for strength and corrosion resistance. Recently Owens Corning has strengthened its position by launching new sustainable fiber technologies designed to reduce the carbon footprint of boat manufacturing processes. They have also expanded their technical support services in Europe to assist naval architects in optimizing composite designs for fuel efficiency. By collaborating with major European yacht builders and offshore wind developers the company ensures its materials meet the rigorous demands of modern maritime applications. Their commitment to research and development allows them to offer solutions that address both performance requirements and environmental regulations driving the sector forward.

- Hexcel Corporation is a leading provider of high performance carbon fiber and prepreg systems that are critical for advanced marine applications across Europe. The company plays a pivotal role in the global market by supplying materials used in luxury superyachts high speed ferries and naval defense vessels where weight reduction is paramount. Their advanced composite solutions offer superior stiffness and fatigue resistance which are essential for large scale structures and dynamic hull forms. To strengthen their market presence Hexcel has recently invested in expanding their production capacity for aerospace grade carbon fibers which are increasingly adapted for marine use. They have also formed strategic partnerships with European shipyards to develop customized prepreg formulations that cure faster and offer improved thermal stability. These initiatives allow Hexcel to support the growing demand for electrified vessels and eco friendly designs that require maximum structural efficiency. Their focus on innovation and customer collaboration ensures they remain at the forefront of the high end marine composites sector.

- Gurit Holding AG is a Swiss based specialist renowned for delivering comprehensive composite solutions including core materials prepregs and adhesives tailored specifically for the marine industry. Their global contribution is marked by a deep understanding of naval architecture and a portfolio that supports everything from small leisure boats to massive wind turbine blades. In Europe Gurit maintains a strong presence by providing localized engineering support and rapid supply chain responses to major shipbuilding hubs. The company has recently strengthened its market position by acquiring niche manufacturers to broaden its range of sustainable core materials such as recycled PET foams. They have also introduced new digital tools that help designers simulate composite performance under real world sea conditions ensuring optimal material usage. Gurit actively participates in European research projects focused on circular economy principles aiming to make marine composites more recyclable. Their dedication to quality and sustainability makes them a preferred partner for builders seeking to balance performance with environmental responsibility in an evolving regulatory landscape.

Top Strategies Used By Key Market Participants

Key players in the Europe Marine Composites Market primarily utilize strategies focused on product innovation and sustainability to maintain competitive advantage. Companies heavily invest in research and development to create advanced fiber and resin systems that offer superior mechanical properties while reducing environmental impact. Strategic acquisitions represent another vital approach where leading firms purchase specialized material scientists or smaller manufacturers to expand their technological portfolios and access new customer bases. Expansion of local production facilities and distribution networks is crucial to ensure reliable supply chains and reduce lead times for European shipyards facing tight deadlines. Partnerships with naval architects and classification societies allow suppliers to co develop certified solutions that meet stringent safety and performance regulations. Additionally firms are increasingly adopting circular economy practices by developing recyclable composite materials and establishing take back programs for end of life vessel components. These multifaceted strategies enable market participants to navigate complex regulatory environments and cater to the evolving needs of the maritime industry.

MARKET SEGMENTATION

This research report on the Europe marine composites market is segmented and sub-segmented into the following categories.

By Composite Type

- Metal Matrix Composite (MMC)

- Ceramic Matrix Composite (CMC)

- Polymer Matrix Composite (PMC)

By Fiber Type

- Glass Fiber

- Carbon Fiber

- Aramid Fiber

- Natural Fiber

- Others

By Resin Type

- Polyester

- Vinyl Ester

- Epoxy

- Thermoplastic

- Phenolic

- Acrylic

- Others

By Vessel Type

- Power Boats

- Sailboats

- Cruise Ships

- Others

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

What are marine composites used for in the maritime industry?

Marine composites are lightweight and corrosion-resistant materials used to manufacture boat hulls, decks, and other marine structures.

Why is the demand for marine composites increasing in Europe?

Growing boat production and the need for durable, lightweight materials are driving the adoption of marine composites.

What types of materials are commonly used in marine composites?

Fiberglass, carbon fiber, and resin-based materials are widely used to produce strong and lightweight marine components.

Which marine applications use composite materials the most?

Recreational boats, yachts, naval vessels, and offshore structures are major applications for marine composites.

How do marine composites improve vessel performance?

Their lightweight nature helps reduce fuel consumption and improves overall vessel efficiency.

What factors are driving growth in the Europe marine composites market?

Increasing demand for leisure boating and advancements in composite manufacturing technologies are key growth drivers.

How do marine composites benefit long-term vessel durability?

They offer excellent resistance to corrosion, moisture, and harsh marine environments.

What challenges affect the marine composites market in Europe?

High production costs and complex manufacturing processes can limit wider adoption.

Which countries play a major role in the Europe marine composites market?

Countries such as Italy, France, Germany, and the United Kingdom are significant contributors due to strong marine industries.

What future trend is expected in the Europe marine composites market?

Increasing use of advanced composite materials and sustainable manufacturing methods is expected to shape market growth.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com