Europe Masterbatch Market Size, Share, Trends & Growth Forecast Report Segmented By Resin Type (Color, White, Additive, Filler etc.), Polymer, Application, and Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic and Rest of Europe), Industry Analysis From 2026 to 2034

Market Size, 2025

$4.02 BnMarket Estimate, 2026

$4.22 BnMarket Forecast, 2034

$6.21 BnCAGR, 2026–2034

4.94%Europe Masterbatch Market Report Summary

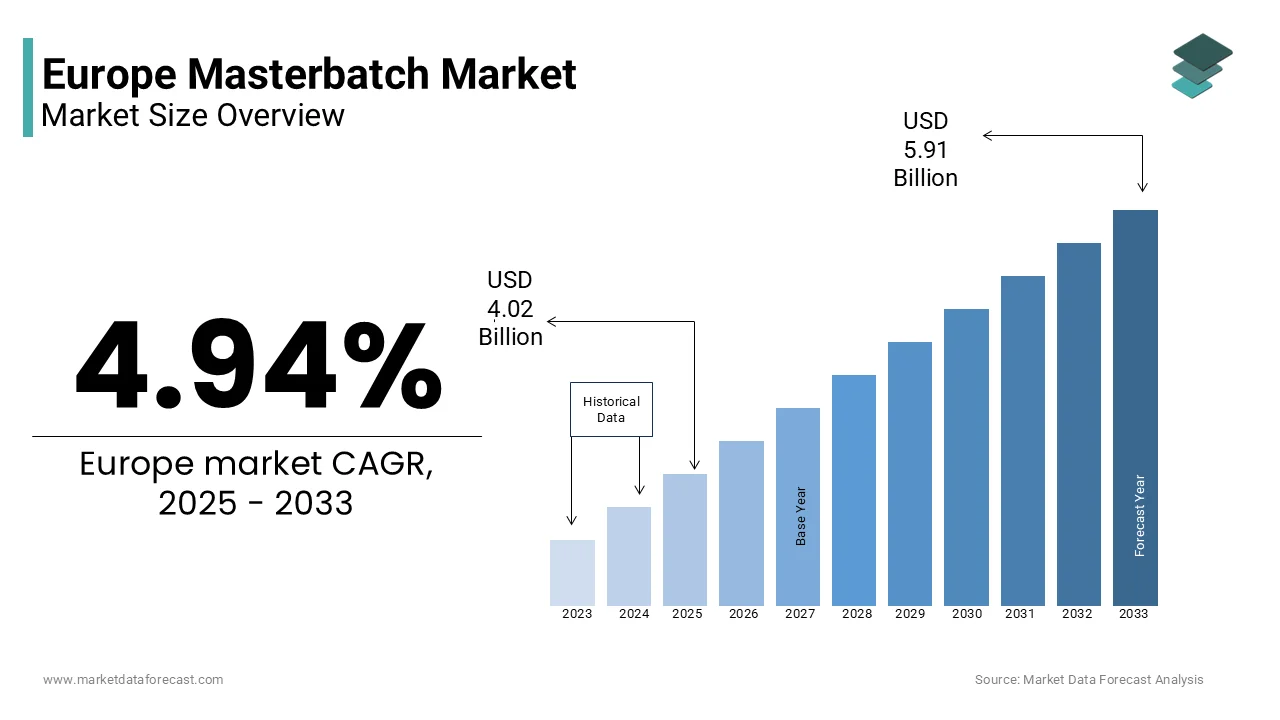

The Europe masterbatch market was valued at USD 4.02 billion in 2025, is estimated to reach USD 4.22 billion in 2026, and is projected to reach USD 6.21 billion by 2034, growing at a CAGR of 4.94% during the forecast period. Market growth is driven by increasing demand for high performance plastics, rising use of additives and colorants in polymer processing, and expanding applications across packaging, automotive, and construction industries. Masterbatch is widely used to enhance material properties such as color, strength, UV resistance, and durability. The growing demand for sustainable and lightweight plastic solutions is further supporting steady market expansion across Europe.

Key Market Trends

- Rising demand for customized and high performance plastic materials is driving market growth.

- Increasing use of color and additive masterbatches in packaging and consumer goods is boosting demand.

- Growing focus on lightweight and durable materials in automotive and construction sectors is supporting expansion.

- Expansion of sustainable and recyclable plastic solutions is influencing product innovation.

- Technological advancements in polymer processing are improving product efficiency and quality.

Segmental Insights

- Based on type, the colour masterbatch segment was the largest and held 46.1% of the Europe masterbatch market share in 2025. This dominance is attributed to high demand for aesthetic enhancement and product differentiation across packaging and consumer products.

- Based on polymers, the polypropylene segment accounted for 36.7% of the Europe masterbatch market share in 2025. The segment’s growth is driven by its versatility, cost effectiveness, and widespread use in various industrial applications.

- Based on application, the packaging segment dominated with 41.5% of the Europe masterbatch market share in 2025, supported by increasing demand for flexible and rigid packaging solutions.

Regional Insights

The Europe masterbatch market is experiencing steady growth across key countries, supported by industrial demand and polymer processing activities.

Germany was the largest contributor, accounting for 23.3% of the Europe masterbatch market share in 2025, driven by a strong manufacturing base, advanced plastic processing industry, and high demand for innovative materials.

Competitive Landscape

The Europe masterbatch market is moderately competitive, with key players focusing on product innovation, customization, and expansion of production capacities to strengthen their market position. Companies are investing in advanced formulations, sustainable materials, and strategic partnerships. Prominent players in the Europe masterbatch market include Ampacet Corporation, A Schulman Inc, Polyone Corporation, and Penn Color Inc.

Europe Masterbatch Market Size

The Europe masterbatch market size was valued at USD 4.02 billion in 2025, and the market size is expected to reach USD 6.21 billion by 2034 from USD 4.22 billion in 2026. The market is growing at a CAGR of 4.94%.

Masterbatch comprises specialized additive concentrates that impart color or enhanced properties to polymers during plastic manufacturing. These concentrates consist of pigments or additives encapsulated within a carrier resin, ensuring uniform dispersion and superior performance in the final plastic product. The region stands as a mature hub for advanced polymer processing, driven by stringent quality standards and a robust automotive and packaging infrastructure. As per Eurostat, the European Union produced approximately 58.7 million tons of plastics in 2022, with Germany, Italy, and France accounting for nearly half of this total output. This substantial production volume creates a consistent baseline demand for masterbatches across various industrial applications. The regulatory landscape in Europe heavily influences material composition, pushing manufacturers toward compliant and sustainable solutions. According to Plastics Europe, the recycling rate for plastic packaging waste in the EU reached 41% in 2022, reflecting a strong shift toward circular economy principles. This transition necessitates high quality masterbatches that can perform effectively in recycled polymer matrices without compromising aesthetic or mechanical integrity. The market is characterized by a high degree of technical sophistication, where manufacturers must align their formulations with evolving environmental directives. The integration of bio based carriers and non-toxic pigments have become paramount, which is aligning with the European Green Deal objectives. Consequently, the market dynamics are not merely defined by volume but by the technological capability to deliver sustainable and high performance additive solutions that meet the rigorous demands of downstream industries such as automotive, construction, and consumer goods.

MARKET DRIVERS

Stringent Environmental Regulations Driving Sustainable Formulations

Regulatory pressure is primarily fuelling the adoption of eco-friendly masterbatch solutions across Europe, which is one of the major factors driving the European masterbatch market growth. The European Commission’s Circular Economy Action Plan mandates that all plastic packaging be reusable or recyclable by 2030, which is compelling manufacturers to reformulate their products. This legislative framework drives demand for masterbatches that facilitate recycling processes rather than hinder them. Traditional additives often contaminate recycling streams, but newer generations of masterbatches are designed to be compatible with mechanical and chemical recycling methods. As per the European Environment Agency, approximately 35% of plastic waste was recycled in 2020 and is indicating the urgent need for improved material design. Manufacturers are increasingly investing in research and development to create masterbatches with bio based carriers and reduced heavy metal content. The Restriction of Hazardous Substances Directive further limits the use of specific hazardous materials, pushing suppliers to innovate with safer alternatives. This regulatory environment ensures that only high quality and compliant masterbatches gain market access and thereby raising the overall standard of products available. Companies that fail to adapt face significant barriers to entry and potential legal repercussions. Consequently, the drive for compliance is not merely a legal obligation but a strategic imperative that shapes product development pipelines. The emphasis on sustainability also aligns with consumer preferences, creating a dual push from both regulatory bodies and end users for greener plastic solutions. This dynamic fosters a competitive landscape where innovation in sustainable formulation becomes a key differentiator for market leaders.

Growth in Automotive Lightweighting Initiatives Boosting Demand

The automotive sector’s relentless pursuit of lightweight vehicles significantly propels the demand for high performance masterbatches in Europe, which is further contributing to the European masterbatch market expansion. Vehicle manufacturers utilize engineered plastics to reduce weight, improve fuel efficiency, and lower carbon emissions. Masterbatches play a critical role in enhancing the mechanical properties, thermal stability, and aesthetic appeal of these plastic components. According to the European Automobile Manufacturers Association, the average CO2 emissions from new passenger cars in the EU were 108.2 grams per kilometer in 2022, which is driving the need for lighter materials to meet stricter targets. Plastic components, reinforced with specialized additives, offer a viable alternative to heavier metals without compromising safety or durability. The shift toward electric vehicles further amplifies this trend, as battery range optimization requires significant weight reduction. Masterbatches that provide flame retardancy, UV resistance, and enhanced strength are particularly sought after for interior and exterior automotive parts. As per Statista, the European automotive plastics market is expected to grow steadily, supported by the increasing penetration of electric vehicles. This growth trajectory ensures a sustained demand for advanced masterbatch solutions that can meet the rigorous performance standards of modern automotive design. Manufacturers are collaborating closely with automotive OEMs to develop customized formulations that address specific application requirements. This synergy between material suppliers and automakers fosters innovation and ensures that masterbatch technologies evolve in tandem with automotive engineering advancements. The result is a robust demand segment that values performance and precision over cost alone.

MARKET RESTRAINTS

Volatility in Raw Material Prices Impacting Profit Margins

Fluctuating costs of raw materials is a significant impediment to the growth of the European masterbatch market. Masterbatch production relies heavily on polymers such as polyethylene and polypropylene, as well as various pigments and additives, whose prices are linked to crude oil markets. Geopolitical tensions and supply chain disruptions have led to considerable volatility in these input costs. As per the International Energy Agency, Brent crude oil prices averaged 82 USD per barrel in 2023, which is exhibiting significant fluctuations that directly impact polymer prices. This unpredictability makes it challenging for masterbatch manufacturers to maintain stable pricing structures, often forcing them to pass costs onto customers or absorb margins. Small and medium sized enterprises are particularly vulnerable to these shocks, as they lack the bargaining power and financial reserves of larger corporations. Additionally, the energy intensive nature of masterbatch production means that rising electricity and natural gas prices further exacerbate cost pressures. According to Eurostat, industrial producer prices for chemicals and chemical products in the Euro area increased by 19.3% in 2022 compared to the previous year. Such inflationary pressures squeeze profit margins and can lead to reduced investment in research and development. Manufacturers must employ sophisticated hedging strategies and supply chain diversification to mitigate these risks, but complete insulation from market volatility remains elusive. This financial uncertainty can delay expansion plans and limit the ability to innovate, thereby restraining overall market growth potential in the short to medium term.

Complex Recycling Infrastructure Limiting Recycled Content Usage

The fragmented and complex recycling infrastructure across Europe restricts the widespread adoption of masterbatches designed for recycled plastics, which is further impacting the regional market expansion. While there is a strong push for circularity, the quality and consistency of recycled polymer feedstocks vary significantly between member states. Masterbatch manufacturers face challenges in creating formulations that perform consistently across different batches of recycled material, which may contain varying levels of contaminants or degradation. As per Plastics Europe, the mechanical recycling rate for plastics in Europe stood at 35% in 2021, indicating that a large portion of plastic waste still ends up in landfills or incineration. This inconsistency in feedstock quality necessitates extensive testing and customization of masterbatch products, increasing development time and costs. Furthermore, the lack of standardized collection and sorting systems across different European countries complicates the supply chain for high quality recycled resins. Manufacturers must navigate a patchwork of local regulations and infrastructure capabilities, which hinders economies of scale. The European Commission has acknowledged these disparities and is working toward harmonizing recycling standards, but progress is gradual. Until a more uniform and reliable supply of high quality recycled polymers is established, the full potential of masterbatches in circular applications remains constrained. This infrastructural limitation acts as a brake on innovation, as manufacturers hesitate to invest heavily in specialized products for a market that lacks consistent input quality. Overcoming this barrier requires coordinated efforts between policymakers, waste management companies, and material producers.

MARKET OPPORTUNITIES

Expansion of Bio Based and Biodegradable Masterbatch Solutions

The rising demand for bio based and biodegradable plastics is a substantial opportunity for the European masterbatch market. Consumers and regulators are increasingly favoring materials that reduce reliance on fossil fuels and minimize environmental impact. Masterbatch manufacturers can capitalize on this trend by developing additives specifically designed for bio polymers such as polylactic acid and polyhydroxyalkanoates. These materials often require specialized processing aids and stabilizers to overcome inherent limitations such as brittleness and low thermal resistance. As per the European Bioplastics association, the global production capacity of bioplastics is expected to increase from 2.2 million tons in 2022 to 6.3 million tons in 2027, with Europe being a key market. This growth trajectory offers a lucrative avenue for masterbatch suppliers who can provide tailored solutions that enhance the performance and processability of bio based plastics. Additionally, the development of compostable masterbatches aligns with the growing interest in organic waste management and industrial composting facilities. Manufacturers that invest in research and development in this niche can establish a first mover advantage and build strong relationships with brands committed to sustainability. The opportunity extends beyond mere product development to include educational initiatives that help processors understand how to effectively utilize bio based masterbatches. By positioning themselves as partners in the transition to a bio economy, companies can capture significant value in this emerging segment. The alignment with European Green Deal objectives further enhances the strategic importance of this opportunity, ensuring long term market relevance and growth potential.

Technological Advancements in Digital Color Matching and Customization

Advancements in digital technologies offer a significant opportunity for the European masterbatch market. Digital color matching tools and artificial intelligence driven formulation software enable faster and more accurate development of custom masterbatch solutions. This technology allows manufacturers to respond rapidly to customer requests for specific shades and effects, reducing lead times and minimizing waste during the trial phase. As per industry analysis, the adoption of Industry 4.0 technologies in the chemical sector is accelerating, with digital twins and predictive analytics improving production precision. For the masterbatch market, this means the ability to offer highly customized products at competitive prices, catering to the diverse needs of sectors such as packaging and consumer goods. Brands are increasingly seeking unique visual identities for their products, driving demand for bespoke color solutions. Digital platforms also facilitate better communication between suppliers and customers, allowing for real time collaboration on design and specification. This level of customization and responsiveness strengthens customer loyalty and creates barriers to entry for competitors lacking such technological capabilities. Furthermore, digital tools can optimize inventory management and production scheduling, leading to cost savings and improved sustainability metrics. By leveraging these technological advancements, masterbatch producers can transform from commodity suppliers into value added partners. The integration of digital solutions not only enhances product quality but also improves the overall customer experience, positioning companies for sustained growth in a competitive market landscape.

MARKET CHALLENGES

Supply Chain Disruptions Affecting Raw Material Availability

Persistent supply chain disruptions are a major challenge to the Europe masterbatch market by impacting the timely availability of critical raw materials. The reliance on global supply networks for pigments, additives, and carrier resins makes the industry vulnerable to geopolitical instability, trade restrictions, and logistical bottlenecks. Recent events have exposed the fragility of these networks, leading to delays and shortages that disrupt production schedules. As per the European Central Bank, supply chain constraints contributed significantly to inflationary pressures in the Eurozone, which saw headline inflation reach 8.4% in 2022, affecting various manufacturing sectors including chemicals. For masterbatch manufacturers, these disruptions can result in inability to fulfill orders on time, damaging customer relationships and reputation. The concentration of certain raw material sources in specific regions exacerbates this risk, limiting options for alternative sourcing. Additionally, transportation costs have remained elevated, further straining operational budgets. Manufacturers are compelled to hold higher inventory levels as a buffer, which ties up capital and increases storage costs. This shift from just in time to just in case inventory management alters traditional business models and requires significant adjustment. The challenge is compounded by the need to maintain product quality while sourcing from alternative suppliers who may not meet established standards. Ensuring continuity of supply thus becomes a complex logistical and strategic endeavor. Companies must invest in supply chain resilience through diversification and closer collaboration with suppliers, but these measures take time and resources to implement effectively.

Intense Competition and Price Pressure from Asian Imports

The intense competition from low cost imports, particularly from Asian manufacturers that exerts downward pressure on prices is further challenging the expansion of the European masterbatch market. Countries such as China and India have developed robust masterbatch production capacities, benefiting from lower labor and raw material costs. These imports often compete on price rather than technical superiority, challenging European manufacturers who operate under higher regulatory and operational cost structures. As per the United Nations Comtrade database, imports of plastic additives and masterbatches from Asia to Europe have shown a steady increase over the past decade, reflecting the growing competitiveness of Asian suppliers. This influx forces European companies to continuously optimize their operations and justify premium pricing through value added services and superior product quality. However, in price sensitive segments such as general purpose packaging, maintaining market share becomes increasingly difficult. The disparity in production costs creates an uneven playing field, where European manufacturers must innovate constantly to differentiate their offerings. Additionally, the presence of numerous small and medium sized enterprises in Europe fragments the market, leading to aggressive pricing strategies among local players as well. This competitive intensity limits profit margins and can restrict investment in long term research and development initiatives. Manufacturers must therefore focus on niche applications and high performance segments where technical expertise and regulatory compliance provide a competitive edge. Balancing cost competitiveness with quality assurance remains a persistent challenge in this globalized market environment.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 4.94% |

| Segments Covered | By Resin Type, Polymer, Application, and Region |

| Various Analyses Covered | Global, Regional, & Country Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, and the Czech Republic |

| Market Leaders Profiled | Ampacet Corporation, A Schulman Inc.,Polyone Corporation, Penn Color Inc. |

SEGMENTAL ANALYSIS

By Type Insights

The colour masterbatch segment dominated the market by capturing 46.1% of the regional market share in 2025. The dominance of colour segment in this regional market is driven by the relentless demand for visually appealing packaging and consumer products. In the competitive retail landscape, brand differentiation through vibrant and consistent coloring is crucial for capturing consumer attention. As per Euromonitor International, the European packaging industry was valued at approximately 200 billion EUR in 2023, with a significant portion utilizing colored plastics for branding purposes. The versatility of colour masterbatches allows manufacturers to achieve precise shades and effects, ranging from metallic finishes to transparent tints, which are essential for high end consumer goods. Furthermore, the rise of e commerce has increased the importance of unboxing experiences, where aesthetic packaging plays a pivotal role. Manufacturers are increasingly investing in advanced pigment technologies that offer superior light fastness and thermal stability, ensuring that colors remain vibrant throughout the product lifecycle. The ability to customize colors rapidly using digital matching tools further strengthens the position of this segment. Regulatory compliance regarding food contact materials also drives innovation, as suppliers develop non toxic and migration resistant pigments. This combination of aesthetic necessity, technological advancement, and regulatory adherence ensures that colour masterbatches remain the cornerstone of the European market, sustaining their leading position through continuous adaptation to consumer trends and industrial requirements.

On the other side, the additive masterbatch segment is estimated to register a CAGR of 7.4% over the forecast period in this European market owing to the increasing need for enhanced polymer performance and sustainability features. Additives such as UV stabilizers, flame retardants, and antistatic agents are critical for extending the lifespan and safety of plastic products. As per the European Chemicals Agency, the demand for flame retardant additives has surged due to stricter fire safety regulations in construction and automotive sectors. Additionally, the push for circular economy practices has boosted the demand for processing aids that facilitate the use of recycled materials. These additives help mitigate the degradation of mechanical properties in recycled polymers, making them viable for high value applications. The automotive industry’s shift toward electric vehicles also contributes to this growth, as specialized additives are required for battery components and lightweight structures. According to the Society of Motor Manufacturers and Traders, the production of electric vehicles in the UK grew by 48% in 2023, driving demand for high performance additive solutions. Furthermore, innovations in bio based additives align with environmental goals, offering sustainable alternatives to traditional chemical modifiers. This multifaceted demand from various industries, coupled with technological advancements in additive formulations, positions this segment as the fastest growing component of the market, reflecting the industry’s evolution toward functionality and sustainability.

By Polymers Insights

The polypropylene segment led the market by accounting for 36.7% of the European market share in 2025. The promising position of polypropylene segment in the European market can be driven by the widespread use of PP in automotive, packaging, and textile applications due to its excellent balance of properties, including chemical resistance, flexibility, and cost effectiveness. The automotive sector is a major consumer, utilizing PP for interior trim, bumpers, and under the hood components. As per the European Automobile Manufacturers Association, PP constitutes nearly 40% of the plastic content in modern vehicles, driven by lightweighting initiatives. The packaging industry also relies heavily on PP for rigid containers, caps, and films, benefiting from its barrier properties and recyclability. According to Plastics Europe, PP recycling rates in Europe have improved, reaching 30% in 2022, which enhances its appeal in sustainable product design. The material’s ability to withstand high temperatures makes it suitable for hot fill applications in food packaging, further expanding its utility. Additionally, the development of high melt strength PP grades has opened new opportunities in thermoforming and foam applications. Manufacturers are increasingly focusing on developing masterbatches that enhance the surface quality and printability of PP, addressing aesthetic demands in consumer goods. The combination of functional versatility, economic viability, and improving sustainability credentials ensures that PP remains the preferred polymer substrate for masterbatch incorporation, maintaining its substantial market share across diverse industrial sectors.

However, the polyurethane segment is on the rise and is estimated to witness a CAGR of 8.1% over the forecast period in this regional market owing to the stringent energy efficiency regulations in the building and construction sector, which mandate high performance insulation materials. PUR foams are widely used for thermal insulation in residential and commercial buildings due to their superior insulating properties and structural integrity. As per the European Commission, the Energy Performance of Buildings Directive aims to reduce greenhouse gas emissions from buildings by 60% by 2030, stimulating demand for effective insulation solutions. Masterbatches play a crucial role in enhancing the fire resistance and durability of PUR foams, ensuring compliance with safety standards. The automotive industry also contributes to this growth, as PUR is increasingly used in seating, dashboards, and soundproofing components. According to the International Organization of Motor Vehicle Manufacturers, the demand for comfortable and safe vehicle interiors has risen, boosting PUR consumption. Additionally, innovations in bio based polyols for PUR production align with sustainability goals, attracting environmentally conscious manufacturers. The development of masterbatches that improve the cell structure and mechanical properties of PUR foams further enhances their application potential. This convergence of regulatory pressure, performance requirements, and sustainable innovation propels the PUR segment to the forefront of market growth, reflecting its critical role in energy efficient and high performance applications.

By Application Insights

The packaging segment commanded for the dominating share of 41.5% of the regional market in 2025. The growth of the packaging segment in the European market is attributed to the essential role of packaging in preserving food quality, ensuring safety, and facilitating logistics. The rise of e-commerce has significantly amplified the demand for durable and aesthetically pleasing packaging solutions. As per Eurostat, e commerce sales in the EU increased by 15% in 2023, leading to higher consumption of plastic packaging for shipping and protection. Masterbatches are integral to this sector, providing color, UV protection, and antimicrobial properties that extend shelf life and maintain product integrity. The shift toward sustainable packaging has also influenced market dynamics, with manufacturers developing masterbatches compatible with recycled materials and bio based plastics. According to Plastics Europe, the recycling rate for plastic packaging in Europe reached 41% in 2022, encouraging the use of masterbatches that enhance the quality of recycled content. Furthermore, consumer preference for convenient and portable packaging formats, such as single serve portions and flexible pouches, drives innovation in film applications. The ability of masterbatches to provide barrier properties against moisture and oxygen is crucial for food preservation, reducing waste and enhancing sustainability. This combination of functional necessity, regulatory compliance, and consumer trends solidifies the packaging segment’s leading position, ensuring sustained demand for specialized masterbatch solutions.

However, the automotive segment is experiencing the fastest growth in the Europe masterbatch market and is predicted to register a CAGR of 9.3% over the forecast period due to the transition to electric vehicles and the ongoing emphasis on lightweighting to improve energy efficiency. Electric vehicles require specialized materials for battery housings, charging components, and interior parts, many of which utilize engineered plastics enhanced with masterbatches. As per the European Alternative Fuels Observatory, the number of battery electric vehicles on European roads surpassed 4 million units in 2023, creating a surge in demand for high performance plastic components. Masterbatches provide essential properties such as flame retardancy, electrical conductivity, and thermal stability, which are critical for safety and performance in electric drivetrains. Additionally, the push for weight reduction to extend battery range has increased the use of plastic composites in structural and semi structural applications. According to the European Automobile Manufacturers Association, the average weight of plastic components in new vehicles has increased by 10% over the past five years. The aesthetic demands of modern vehicle interiors also drive the use of colour and effect masterbatches for premium finishes. Furthermore, the development of sustainable masterbatches aligns with automotive manufacturers’ goals to reduce their carbon footprint. This synergy of technological innovation, regulatory pressure, and market transformation positions the automotive segment as a key growth engine for the masterbatch industry.

REGIONAL ANALYSIS

Germany Masterbatch Market Analysis

Germany accounted for the leading share of 23.3% of the European market in 2025. The dominance of Germany in the European market is driven by the country’s robust manufacturing base, particularly in the automotive and chemical sectors. Germany is home to major automotive original equipment manufacturers who extensively use high performance plastics and masterbatches for vehicle production. As per the German Federal Statistical Office, the chemical industry in Germany generated revenues of approximately 230 billion EUR in 2023, underscoring its significance as a consumer of additive technologies. The country’s strong emphasis on engineering excellence and quality standards necessitates the use of premium masterbatches that meet rigorous specifications. Additionally, Germany is a pioneer in sustainable manufacturing, with strict regulations promoting the use of recycled materials and bio based additives. The German government’s commitment to the Circular Economy Action Plan has spurred investment in recycling infrastructure, creating demand for masterbatches compatible with post-consumer recycled plastics. The presence of leading masterbatch producers and research institutions further fosters innovation and technological advancement. The automotive sector’s transition to electric mobility also contributes to market growth, as specialized additives are required for battery components and lightweight structures. This combination of industrial strength, regulatory leadership, and technological innovation ensures that Germany remains the central hub for the European masterbatch market, setting trends and standards for the region.

Italy Masterbatch Market Analysis

Italy held the second largest share of the European masterbatch market in 2025. The country’s strong presence in the packaging, automotive, and consumer goods sectors fuels this significant market presence in Italy. Italy is renowned for its design led consumer products, which rely heavily on high quality colour and effect masterbatches to achieve distinctive aesthetics. As per ISTAT, the Italian packaging industry produced over 10 million tons of materials in 2023, with plastics constituting a substantial portion. The automotive sector, particularly in the northern regions, also contributes significantly to demand, with manufacturers focusing on lightweight and stylish vehicle components. The country’s emphasis on sustainability is evident in its adoption of recycled plastics, driven by European Union directives. Italian manufacturers are increasingly integrating masterbatches that enhance the performance of recycled materials, supporting circular economy goals. Additionally, the construction sector’s recovery post pandemic has boosted demand for masterbatches used in pipes, profiles, and insulation materials. The presence of numerous small and medium sized enterprises specializing in niche applications further diversifies the market. Italy’s ability to blend artistic design with technical precision creates a unique demand profile for masterbatches, distinguishing it from other European markets. This dynamic interplay of aesthetics, functionality, and sustainability sustains Italy’s prominent role in the regional market.

France Masterbatch Market Analysis

France is anticipated to account for a prominent share of the European masterbatch market during the forecast period due to the diversified industrial base, including strong automotive, aerospace, and packaging sectors. France is a key player in the European automotive industry, with major manufacturers utilizing advanced plastics and masterbatches for vehicle production. As per the French Ministry of Economy, the automotive sector contributed 4% to the national GDP in 2023, highlighting its economic importance. The packaging industry is also a significant consumer, driven by stringent regulations on single use plastics and a shift toward sustainable alternatives. French consumers are increasingly environmentally conscious, prompting brands to adopt eco friendly packaging solutions that utilize bio based and recyclable masterbatches. The construction sector’s focus on energy efficiency has also increased demand for masterbatches used in insulation and building materials. France’s commitment to the European Green Deal has led to investments in recycling infrastructure and sustainable material research. The presence of leading chemical companies and research centers fosters innovation in masterbatch formulations. Additionally, the luxury goods sector, prominent in France, demands high quality colour and effect masterbatches for premium packaging and product components. This diverse range of applications, combined with a strong regulatory framework for sustainability, ensures steady growth and stability in the French masterbatch market.

United Kingdom Masterbatch Market Analysis

The United Kingdom is anticipated to account for a notable share of the European masterbatch market during the forecast period. Despite leaving the European Union, the UK maintains strong trade links and regulatory alignment in many areas, influencing its market dynamics. The country’s robust packaging and automotive sectors are primary drivers of demand. As per the Office for National Statistics, the UK manufacturing sector output grew by 1.2% in 2023, supported by increased production in automotive and chemical industries. The packaging industry is undergoing a transformation due to the Plastic Packaging Tax, which incentivizes the use of recycled materials. This policy has spurred demand for masterbatches that enhance the quality and processability of recycled plastics. The automotive sector’s shift toward electric vehicles also contributes to market growth, as specialized additives are required for new component designs. The UK’s strong focus on sustainability and circular economy principles drives innovation in bio based and biodegradable masterbatches. Additionally, the construction sector’s recovery has increased demand for masterbatches used in pipes, cables, and insulation materials. The presence of leading multinational masterbatch producers and local specialists ensures a competitive and innovative market environment. The UK’s ability to adapt to regulatory changes and embrace sustainable practices positions it as a key player in the European masterbatch landscape, maintaining its relevance and growth potential.

Spain Masterbatch Market Analysis

Spain is expected to grow at a healthy CAGR in the European masterbatch market over the forcast period owing to its growing industrial capabilities and strategic location. The country’s market is driven by the packaging, automotive, and construction sectors, which have shown resilience and growth in recent years. As per the National Institute of Statistics of Spain, the industrial production index decreased by 0.8% in 2023, indicating a challenging but stabilizing manufacturing environment. The packaging industry is a major consumer, benefiting from the growth of e commerce and export oriented agricultural products. Spanish manufacturers are increasingly adopting sustainable packaging solutions, driving demand for masterbatches compatible with recycled and bio based materials. The automotive sector, particularly in Catalonia and the Basque Country, is a significant contributor, with manufacturers focusing on lightweight and efficient vehicle designs. The construction sector’s recovery, supported by European Union funds, has boosted demand for masterbatches used in building materials and infrastructure projects. Spain’s commitment to renewable energy and sustainability aligns with the development of eco-friendly masterbatch solutions. The country’s strategic position as a gateway to Latin America and Africa also offers export opportunities for Spanish masterbatch producers. This combination of domestic growth, sustainability initiatives, and export potential ensures that Spain remains a dynamic and important market within the European masterbatch market.

COMPETITIVE LANDSCAPE

The competition in the Europe masterbatch market is characterized by a fragmented landscape featuring a mix of large multinational corporations and specialized regional players. Multinational entities leverage their extensive resources and global networks to offer comprehensive product portfolios and standardized solutions across various industries. In contrast, smaller regional firms compete by providing highly customized services and niche expertise that cater to specific local requirements. This dynamic creates a competitive environment where innovation and customer service are critical differentiators. Companies are increasingly focusing on sustainability as a key competitive advantage, developing eco-friendly formulations that comply with strict European regulations. The pressure to reduce costs while maintaining high quality standards drives continuous improvement in manufacturing processes and supply chain management. Technological advancements such as digital color matching and automated production systems are being adopted to enhance efficiency and responsiveness. Strategic mergers and acquisitions are common as firms seek to expand their market reach and acquire new technologies. The intensity of competition is further heightened by the entry of low cost imports from Asian markets, forcing European producers to emphasize value added services and technical superiority. This competitive milieu encourages constant innovation and adaptation, ensuring that only the most agile and customer focused companies thrive in the evolving market landscape.

Key Market Players

Some of the notable companies in the Europe masterbatch market are

- Ampacet Corporation

- A Schulman Inc.

- Polyone Corporation

- Penn Color Inc

Top Players in the Market

- Clariant AG stands as a pivotal innovator within the European masterbatch landscape, leveraging its Swiss heritage to deliver high performance additive solutions. The company focuses extensively on sustainable product lines such as AddWorks and Ceridust which cater to diverse industrial needs including automotive and packaging sectors. Clariant has recently intensified its commitment to circular economy principles by launching bio based and recycled content compatible masterbatches. Their strategic investments in research and development facilities across Germany and Italy enable rapid customization for local clients. By integrating digital color matching technologies, Clariant enhances service efficiency and reduces waste during production. The company actively collaborates with brand owners to develop unique aesthetic effects that differentiate products in competitive retail environments. Clariant’s robust supply chain network ensures consistent quality and timely delivery across the continent. Their proactive approach to regulatory compliance positions them as a trusted partner for manufacturers seeking safe and environmentally responsible material solutions. This dedication to innovation and sustainability reinforces their leadership role in shaping the future of polymer additives in Europe.

- Ampacet Corporation maintains a formidable presence in the European market through its extensive manufacturing footprint and diverse product portfolio. The global leader in masterbatch production operates several key facilities in France, Germany, and the United Kingdom to serve regional demands effectively. Ampacet specializes in providing customized color and additive solutions for packaging, consumer goods, and healthcare applications. The company has recently expanded its capabilities in sustainable technologies by introducing masterbatches designed for mono material packaging and enhanced recyclability. Their innovation centers focus on developing lightweighting solutions that help automotive and industrial clients reduce material usage without compromising performance. Ampacet emphasizes close collaboration with customers to co create tailored formulations that address specific processing challenges. The company’s investment in advanced extrusion technologies ensures superior dispersion and consistency in every batch. By prioritizing customer centric innovation and operational excellence, Ampacet strengthens its reputation as a reliable supplier of high quality masterbatches. Their strategic focus on sustainability and technical expertise continues to drive growth and reinforce their competitive position in the dynamic European marketplace.

- Gabriel Chemie Group distinguishes itself as a specialized player with deep roots in the Austrian chemical industry, focusing on high value niche applications. The company excels in producing premium color and additive masterbatches for technical plastics, films, and fibers. Gabriel Chemie has recently strengthened its market position by expanding its production capacities in Central and Eastern Europe to meet growing demand. Their product range includes innovative solutions for agricultural films, construction materials, and automotive components, emphasizing durability and performance. The group prioritizes sustainability by developing masterbatches that facilitate the use of recycled polymers and bio based carriers. Their agile business model allows for rapid response to customer requests and market trends, fostering strong long term relationships. Gabriel Chemie invests heavily in technical support services, helping processors optimize their manufacturing processes and improve product quality. The company’s commitment to environmental responsibility is evident in their continuous efforts to reduce carbon footprints and enhance resource efficiency. By combining technical expertise with a customer focused approach, Gabriel Chemie solidifies its status as a key contributor to the European masterbatch industry’s evolution toward sustainable and high performance solutions.

Top Strategies Used by the Key Market Participants

Key players in the Europe Masterbatch Market primarily employ strategies centered on sustainability innovation and strategic partnerships to maintain competitiveness. Companies are heavily investing in research and development to create bio based and recyclable masterbatch formulations that align with stringent European environmental regulations. This focus allows them to meet the growing demand for circular economy solutions from downstream industries. Another prevalent strategy involves geographic expansion and capacity enhancement through the establishment of new production facilities or the acquisition of local competitors. These moves enable firms to strengthen their supply chains and reduce lead times for regional customers. Digitalization also plays a crucial role as manufacturers integrate advanced color matching software and artificial intelligence to improve formulation accuracy and operational efficiency. Additionally, companies are forming collaborative alliances with raw material suppliers and end users to co-develop customized solutions that address specific application requirements. This collaborative approach fosters innovation and ensures that products meet evolving market needs. By combining these strategic initiatives, market participants aim to differentiate their offerings, enhance customer loyalty, and secure a sustainable competitive advantage in the rapidly changing European landscape.

MARKET SEGMENTATION

This research report on the Europe masterbatch market has been segmented and sub-segmented based on the following categories.

By Type

- Colour

- White

- Filler

- Additive

By Polymers

- PP

- LDPE

- HDPE

- PVC

- PUR

- PS

By Application

- Building and Construction

- Paper and Cardboards

- Consumer Goods

- Automotive

- Textile

- Household

- Personal Care

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

1. What is masterbatch?

Masterbatch is a concentrated mixture of pigments or additives encapsulated in a carrier resin and used to color or enhance plastic properties.

2. What is the Europe masterbatch market?

The Europe masterbatch market includes production and supply of color, additive, and filler masterbatches used in plastic processing industries.

3. What factors are driving growth of the masterbatch market in Europe?

Growth is driven by demand from packaging, automotive, and construction industries along with increasing use of functional additives.

4. Which countries dominate the Europe masterbatch market?

Germany, Italy, France, and the United Kingdom are major markets due to strong manufacturing and plastics processing sectors.

5. What are the main types of masterbatch available in Europe?

Major types include color masterbatch, additive masterbatch, filler masterbatch, and specialty masterbatch.

6. What are the key applications of masterbatch in Europe?

Masterbatch is widely used in packaging, automotive components, consumer goods, construction materials, and agriculture films.

7. How does sustainability influence the Europe masterbatch market?

Sustainability drives demand for biodegradable, recyclable, and bio based masterbatch solutions.

8. What role does the packaging industry play in the masterbatch market?

Packaging is a major application segment due to high demand for colored and functional plastic packaging materials.

9. How do regulations impact the masterbatch market in Europe?

Strict environmental and safety regulations influence formulation choices and promote use of compliant additives

10. What challenges affect the Europe masterbatch market?

Challenges include volatile raw material prices, regulatory compliance costs, and increasing competition.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com