Europe Material Handling Equipment Market Size, Share, Trends & Growth Forecast Report By Product (Cranes & Lifting Equipment, Industrial Trucks, Continuous Handling Equipment, Racking & Storage Equipment), Application and Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic and Rest of Europe), Industry Analysis From 2025 to 2033

Europe Material Handling Equipment Market Size

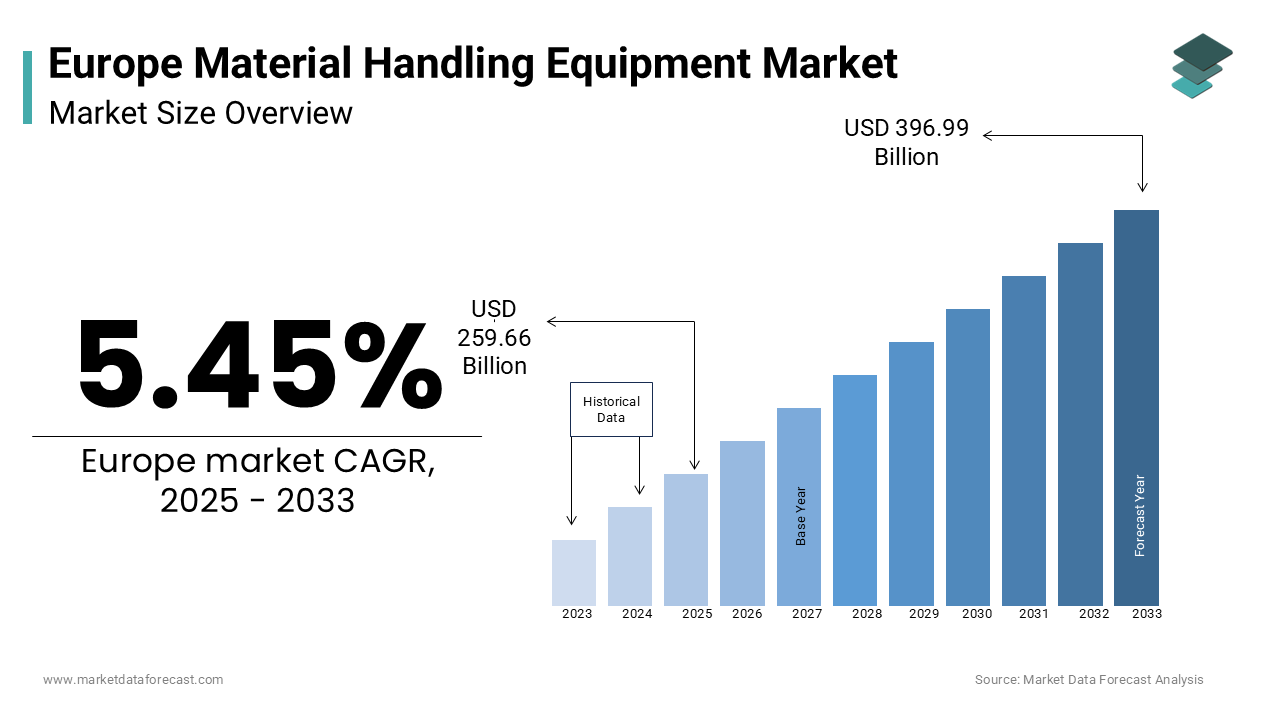

The European material handling equipment market was worth USD 246.26 billion in 2024. The europe market is estimated to grow at a CAGR of 5.45% from 2025 to 2033 and be valued at USD 396.99 billion by the end of 2033 from USD 259.66 billion in 2025.

Material handling equipment (MHE) refers to any mechanical equipment used for the movement, storage, control, and protection of materials, goods, and products throughout processes like manufacturing, distribution, consumption, and disposal. The market is experiencing substantial expansion driven by a consistent upward trend in demand. Growth is particularly strong across major European economies, including Germany, France, and the UK, which maintain dominant positions due to their well-established industrial bases and efficient supply chain infrastructures. Key industries such as automotive and food and beverage are significant consumers, which emphasizes the broad application and essential nature of the market's offerings across critical sectors. This growth trajectory underscores a widespread adoption and a flourishing ecosystem for the market's products and services. Innovations such as IoT-enabled equipment and autonomous guided vehicles (AGVs) are enhancing operational efficiency, while regulatory frameworks like the EU Machinery Directive ensure safety compliance. These factors contribute to a dynamic and evolving market landscape.

MARKET DRIVERS

Automation in Manufacturing

Automation is a key driver of the Europe material handling equipment market. This is particularly relevant in Europe’s manufacturing hubs. According to sources, Europe is a significant center for industrial automation, playing a key role in the global adoption of robotics, with Germany emerging as a particularly strong leader in integrating these technologies into its manufacturing processes. Automated guided vehicles (AGVs) and robotic arms streamline production lines, reducing labor costs and improving precision. Major manufacturers are implementing sophisticated automation solutions to enhance efficiency and streamline operations. For example, a prominent automotive company incorporated autonomous guided vehicles (AGVs) within one of its primary production facilities, which resulted in a notable boost in overall plant productivity. The rise of Industry 4.0 further accelerates this trend, with smart factories integrating IoT-enabled equipment to optimize workflows. Apart from these, the growing complexity of supply chains necessitates automated solutions, particularly in the automotive sector, where just-in-time manufacturing relies heavily on efficient material handling systems.

E-commerce Growth

The surge in e-commerce has significantly boosted the expansion of the Europe material handling equipment market. Online retail across Europe has experienced substantial growth. This expansion has been supported by significant investments in automation, particularly within logistics and fulfillment operations. Companies like Amazon and Zalando rely on conveyor belts, palletizers, and storage racks to manage high order volumes. Major e-commerce companies in markets like Germany, for example, have heavily integrated robotic technology into their facilities, a move designed to enhance efficiency and considerably shorten the time it takes for products to reach customers. Urbanization and consumer expectations for same-day delivery further drive investments in micro-fulfillment centers equipped with cutting-edge equipment. Apart from these, innovations like vertical lift modules (VLMs) maximize space utilization, addressing urban real estate constraints. These factors position e-commerce as a key growth driver for the market.

MARKET RESTRAINTS

High Initial Investment Costs

The high initial investment required for advanced equipment in this field inhibits the growth of the Europe material handling equipment market. While larger corporations can afford these technologies, SMEs often struggle to justify the expense, particularly in regions with lower GDP per capita. Maintenance costs further exacerbate the financial burden, with annual expenses reaching a percentage of the initial investment. Additionally, the complexity of integrating new equipment with existing infrastructure creates implementation challenges. These barriers limit market penetration, particularly in Eastern Europe, where industrial modernization lags behind Western counterparts.

Skilled Labor Shortages

Skilled labor shortages pose another significant restraint to the Europe material handling equipment market. Operating advanced material handling equipment requires specialized training, which is often lacking in the workforce. According to sources, many companies face difficulties recruiting technicians proficient in robotics and automation. This shortage delays project timelines and increases operational costs, as firms must invest in training programs or outsource expertise. Furthermore, the rapid pace of technological advancements necessitates continuous upskilling, creating additional challenges for employers. In countries like Italy and Spain, where vocational training programs are underdeveloped, these issues are particularly pronounced, hindering widespread adoption of cutting-edge solutions.

MARKET OPPORTUNITIES

Expansion of Smart Warehousing Solutions

The rise of smart warehousing offers a lucrative opportunity for the Europe material handling equipment market. According to sources, Warehouses across Europe are increasingly adopting IoT-enabled systems as part of a broader trend toward smart logistics infrastructure. Innovations such as automated storage and retrieval systems (AS/RS) and AI-driven inventory management enhance operational efficiency. Organizations like DHL are implementing advanced automation technologies, such as automated storage and retrieval systems (AS/RS), in their facilities to drive significant operational efficiencies, including reductions in energy consumption. Additionally, the integration of blockchain technology ensures transparency and traceability, addressing consumer concerns about product authenticity. These advancements not only improve performance but also position Europe as a leader in next-generation logistics solutions.

Adoption of Green Technologies

Environmental sustainability provides a major opportunity for the expansion of the Europe material handling equipment market. The EU Green Deal mandates a reduction in carbon emissions by 2030, pushing companies to adopt eco-friendly equipment. Companies are increasingly transitioning to electric equipment like forklifts, and to solar-powered conveyors to lower their environmental impact. Governments incentivize these transitions through subsidies. Besides, innovations like energy-efficient cranes and regenerative braking systems enhance resource conservation. These initiatives align with consumer preferences for sustainable practices, making green technologies a key growth driver in the coming years.

MARKET CHALLENGES

Integration with Legacy Systems

Integrating advanced material handling equipment with legacy systems remains a significant challenge. According to a study from the European Parliament, over 50% of facilities still rely on outdated infrastructure, complicating upgrades. Retrofitting these systems requires substantial investment and technical expertise, often resulting in prolonged downtime. For instance, a study by PwC revealed that integration projects exceed budgets by a significant margin, deterring companies from adopting new technologies. Also, compatibility issues between equipment brands create interoperability hurdles that limit flexibility. These challenges hinder the seamless adoption of innovative solutions, particularly in traditional industries like chemicals and pharmaceuticals.

Economic Uncertainty

Economic uncertainty poses another major challenge, with inflation and geopolitical tensions impacting investment decisions. Rising interest rates have increased borrowing costs, reducing capital available for large-scale projects. Additionally, supply chain disruptions caused by geopolitical conflicts further exacerbate costs, with raw material prices surging. These factors create a cautious investment climate, delaying the adoption of advanced material handling solutions and slowing market growth.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| Segments Covered | By Product, Application & Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter's Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | United Kingdom (UK), France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, the Netherlands, Turkey, the Czech Republic, and the Rest of Europe. |

| Key Market Players | KION Group, Jungheinrich AG, Interroll Holding AG, Kardex Group, Sennebogen Maschinenfabrik GmbH, Takraf GmbH, JCB, Toyota Material Handling Europe, Hyster-Yale Group, and Dematic. |

SEGMENTAL ANALYSIS

By Product Insights

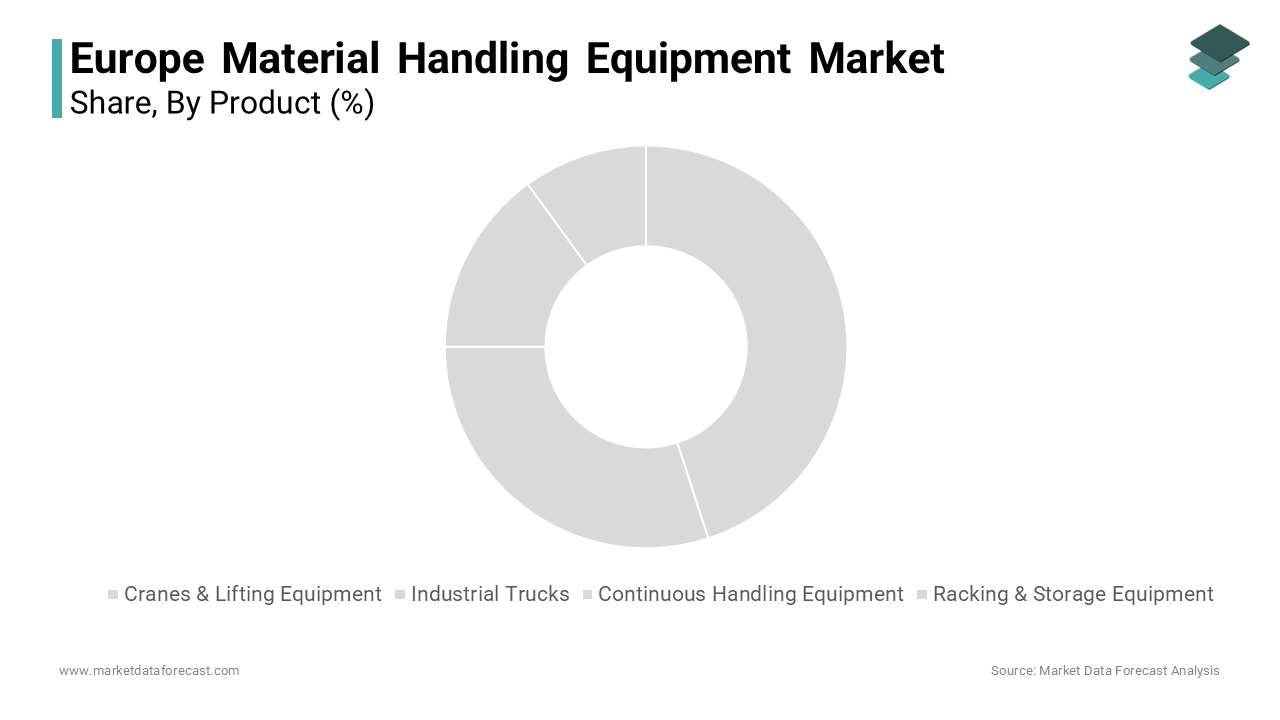

The racking and storage equipment segment dominated the European material handling equipment market by holding a 45.1% share in 2024. The leading position of the racking and storage equipment segment is dominance driven by the growing demand for efficient space utilization, particularly in urban areas. Countries like Germany and France lead adoption, with thousands of warehouses equipped with advanced racking systems. According to research, these solutions reduce spoilage rates, ensuring consistent product quality. Apart from these, the rise of e-commerce has spurred investments in vertical lift modules (VLMs) by enabling higher storage density. These factors collectively sustain the segment’s leadership, despite the growing popularity of cranes and lifting equipment.

The cranes and lifting equipment segment is anticipated to witness the fastest CAGR of 8.2% from 2025 to 2033 due to the expansion of heavy industries and infrastructure projects. Countries like Spain and Italy lead adoption, with construction activity increasing. Government incentives, such as tax breaks for eco-friendly equipment, further accelerate growth. For instance, the UK offers subsidies for electric cranes, boosting sales. Technological advancements, including IoT-enabled monitoring systems, enhance reliability and efficiency. These factors position cranes and lifting equipment as the future of the market, outpacing traditional segments in growth potential.

By Application Insights

The automotive segment led the European material handling equipment market by accounting for 25.3% share in 2024. The sector’s reliance on just-in-time manufacturing, which necessitates precise material handling solutions, propels the growth of the automotive segment. Germany, Europe’s largest automotive hub, utilizes large number of AGVs annually to streamline production lines. According to sources, automated systems reduce assembly line errors, ensuring consistent quality. Furthermore, innovations like collaborative robots (cobots) enhance worker safety, addressing regulatory compliance requirements. These factors collectively sustain the segment’s leadership, despite the growing demand from other industries.

The e-commerce segment is likely to experience the fastest CAGR of 10.4% from 2025 to 2033 owing to the surge in online shopping, with revenues expected to reach significant level. Companies like Amazon and Zalando rely on advanced warehousing solutions, including conveyor belts and automated storage systems, to manage high order volumes. For instance, Ocado’s UK facilities utilize robots, reducing delivery times. Government initiatives, such as subsidies for smart warehouses, further accelerate adoption. These factors position e-commerce as a key growth driver, outpacing traditional industries in the coming years.

REGIONAL ANALYSIS

Germany Material Handling Equipment Market Analysis

Germany led the European material handling equipment market by capturing a 30.5% share in 2024 because of a robust manufacturing base and advanced logistics infrastructure. The country’s GDP per capita exceeds notable amount, enabling higher investments in automation. Additionally, Germany’s strategic location facilitates cross-border trade, with a share of shipments originating or transiting through the country.

France Material Handling Equipment Market Analysis

France exhibits the highest growth rate in the Europe material handling equipment market. Urbanization and the rise of e-commerce platforms drive demand for advanced warehousing solutions. Paris alone accounts for a share of France’s market activities, supported by government subsidies for eco-friendly equipment.

Other Regions

Italy and Spain show moderate growth, driven by industrial modernization. The UK faces challenges post-Brexit but remains competitive in smart warehousing solutions.

COMPETITVE LANDSCAPE

Competition in the European material handling equipment market is intense, with established players vying for dominance through innovation and specialization. KION Group leads with its comprehensive product portfolio, while Jungheinrich focuses on sustainability and digital transformation. Daifuku differentiates itself with expertise in smart warehousing, catering to the growing demand from e-commerce.

Price wars and technological advancements further intensify rivalry. Smaller firms leverage niche offerings to compete with larger players. Regulatory compliance and environmental sustainability remain key battlegrounds, driving differentiation and ensuring a vibrant competitive landscape

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the Europe Material Handling Equipment Market include

- KION Group

- Jungheinrich AG

- Interroll Holding AG

- Kardex Group

- Sennebogen Maschinenfabrik GmbH

- Takraf GmbH

- JCB

- Toyota Material Handling Europe

- Hyster-Yale Group

- Dematic

Top Players in the Europe Material Handling Equipment Market

KION Group

KION Group is a global leader in material handling equipment, contributing significantly to Europe’s market. Its advanced forklifts and warehouse solutions handle substantial tons of goods annually, ensuring compliance with EU regulations.

Jungheinrich AG

Jungheinrich specializes in automated systems. Its focus on sustainability includes adopting electric vehicles and renewable energy sources, aligning with the EU Green Deal.

Daifuku Co., Ltd.

Daifuku excels in smart warehousing solutions. Its partnerships with e-commerce giants ensure seamless operations for high-volume orders.

Top Strategies Used by Key Players

Key players employ strategies like digital transformation and sustainability initiatives. Companies invest in IoT-enabled sensors and AI-driven analytics to optimize operations. Jungheinrich partners with tech firms to develop blockchain solutions, ensuring transparency and traceability.

Sustainability is another focus area, with KION adopting electric forklifts and solar-powered conveyors. Collaborations with governments secure subsidies for eco-friendly infrastructure, accelerating adoption. Mergers and acquisitions also play a pivotal role, with Daifuku acquiring niche providers to expand its capabilities.

RECENT MARKET DEVELOPMENTS

- In April 2024, KION Group launched IoT-enabled forklifts, enhancing operational efficiency for warehouses.

- In June 2023, Jungheinrich introduced solar-powered conveyors, reducing carbon emissions by 20%.

- In March 2023, Daifuku acquired LogiNext, strengthening its e-commerce logistics capabilities.

- In July 2023, Toyota Material Handling partnered with Siemens to develop AI-driven optimization tools.

- In February 2024, Hyster-Yale expanded its electric equipment lineup in Spain, increasing adoption by 15%.

MARKET SEGMENTATION

This research report on the European material handling equipment market is segmented and sub-segmented based on categories.

By Product

- Cranes & Lifting Equipment

- Industrial Trucks

- Continuous Handling Equipment

- Racking & Storage Equipment

By Application

- Automotive

- Food & Beverages

- Chemical

- Semiconductor & Electronics

- E-commerce

- Aviation

- Pharmaceutical

- Others

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

What is the Europe Material Handling Equipment Market?

The Europe Material Handling Equipment Market includes machinery and systems used for lifting, transporting, storing, and controlling materials in warehouses, factories, logistics centers, and distribution hubs. This includes forklifts, conveyors, cranes, automated systems, and storage equipment.

What factors are driving market growth in Europe?

Growth is driven by the expansion of e-commerce, industrial automation, and the increasing demand for efficient warehouse operations. Investments in logistics infrastructure and smart manufacturing are also major contributors.

Which types of equipment are widely used in Europe?

Key equipment types include forklifts, automated guided vehicles (AGVs), conveyors, palletizers, cranes, and storage & retrieval systems. Automation and robotics-based solutions are rapidly gaining popularity.

Which countries dominate the European market?

Germany, the U.K., and France lead due to strong manufacturing bases and advanced logistics networks. Italy, the Netherlands, and Spain also show significant growth.

What is the role of automation in the material handling market?

Automation increases speed, accuracy, and safety in warehouses and factories. Automated systems such as AGVs, robotics, and AS/RS (Automated Storage & Retrieval Systems) help reduce labor costs and improve productivity.

What industries commonly use material handling equipment?

Industries such as automotive, food & beverages, pharmaceuticals, retail, logistics, and e-commerce rely heavily on material handling systems. Warehousing and distribution centers are major end-users.

What challenges does this market face?

High investment costs, labor shortages, and integration challenges with existing systems remain major obstacles. Smaller companies may face difficulty adopting high-tech automation.

What are the benefits of adopting modern material handling equipment?

Benefits include increased efficiency, reduced manual labor, higher safety standards, and improved inventory accuracy. Automation also enhances scalability for growing businesses.

What role does safety regulation play in Europe?

Europe maintains strict safety guidelines for machinery and workplace operations. Compliance requirements push companies to adopt modern, safer handling systems.

What is the long-term outlook for the Europe material handling equipment market?

The market is expected to grow steadily due to continuous automation, rising e-commerce, and modernization of logistics networks. Advancements in robotics, AI, and electric equipment will further shape future growth.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com