Europe Document Management Services Market Analysis Report – Segmented By Application, Solution, Mode of Delivery, End-User and Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic and Rest of Europe) - Industry Analysis, Size, Share, Trends & Growth Forecast (2025 to 2033)

Europe Document Management Services Market Size

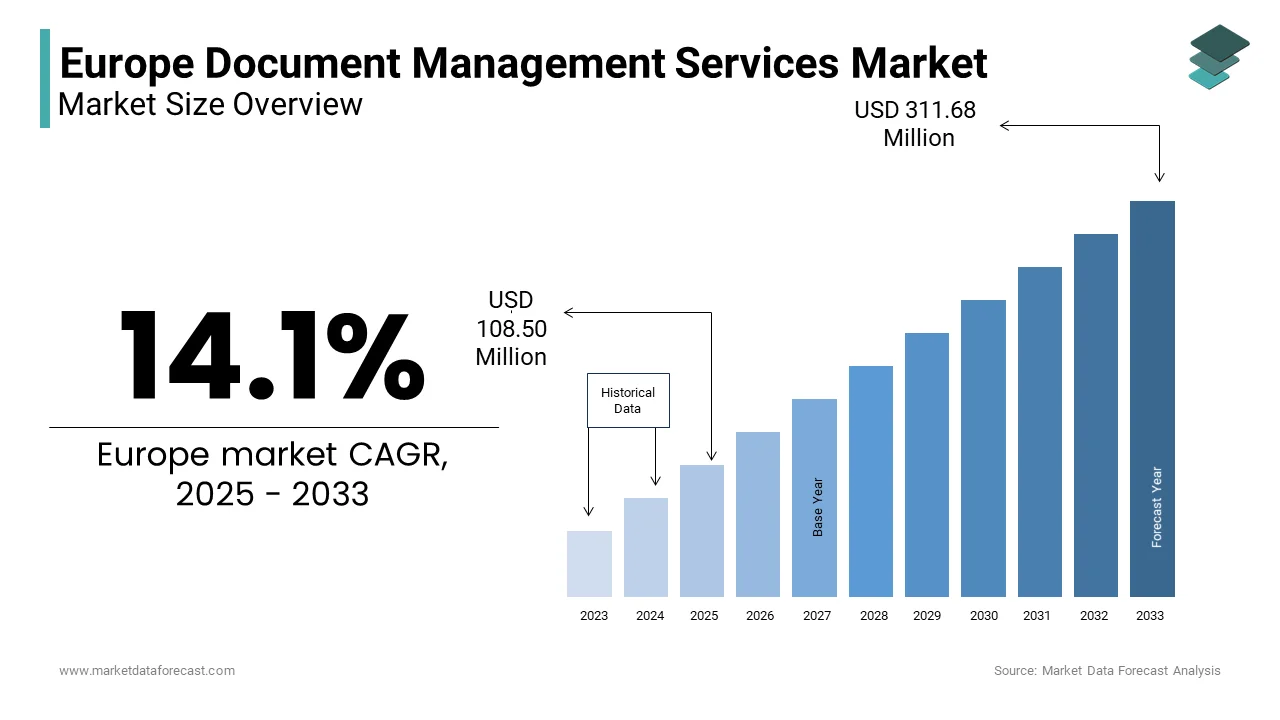

The Europe Document Management Services Market was valued at USD 95.09 million in 2024. The Europe Document Management Services Market is expected to have 14.1% CAGR from 2025 to 2033 and be worth USD 311.68 million by 2033 from USD 108.50 million in 2025.

The document management services include cloud-based and on-premises document storage, workflow automation, compliance management, electronic archiving, and digitization of paper-based records. The growing emphasis on regulatory compliance, data security, and operational efficiency has accelerated the adoption of these services across public and private sectors. Regulatory frameworks such as the General Data Protection Regulation (GDPR) have played a pivotal role in shaping the demand for compliant document handling systems. As per the European Data Protection Board, organizations failing to maintain proper digital documentation risked fines amounting to 4% of annual global turnover by reinforcing the necessity of robust document management infrastructure. Moreover, the rise of remote work culture post-pandemic has further emphasized the need for centralized, accessible, and secure document platforms.

MARKET DRIVERS

Regulatory Compliance and Data Governance Mandates

One of the primary drivers of the Europe document management services market is the increasing stringency of regulatory compliance and data governance mandates across industries. The General Data Protection Regulation (GDPR), enacted in 2018, remains a cornerstone of data protection policy in the region, requiring organizations to maintain structured, secure, and auditable records of personal data processing activities. According to the European Data Protection Board, non-compliance with GDPR can result in penalties up to 4% of a company’s global annual turnover by prompting businesses to invest in document management solutions that ensure traceability, retention policies, and secure access controls. In sectors such as finance, healthcare, and legal services, where record-keeping is mandatory, organizations are adopting integrated document management systems to meet audit requirements and reduce administrative risks.

Additionally, national laws like Germany’s Bundesdatenschutzgesetz (BDSG) and France’s Loi Informatique et Libertés impose stricter documentation protocols, further reinforcing the need for standardized digital archives. As per Deloitte’s 2023 Legal and Compliance Outlook, over 60% of surveyed companies indicated that regulatory pressures were the main reason for upgrading their document management infrastructure.

Digital Transformation Across Enterprises and Public Institutions

Another significant driver of the Europe document management services market is the accelerating pace of digital transformation across both private enterprises and public institutions. The shift toward paperless operations, streamlined workflows, and remote collaboration tools has intensified the demand for efficient document lifecycle management solutions. As per Eurostat, in 2023, more than 65% of large enterprises in the EU had adopted cloud-based document storage systems, enabling real-time access and reducing physical storage costs. Public sector digitization efforts have also played a major role. In addition, the rise of artificial intelligence (AI) and robotic process automation (RPA) in document classification and retrieval has enhanced the appeal of advanced document management platforms.

MARKET RESTRAINTS

High Implementation Costs for Small and Medium-Sized Enterprises

A key restraint affecting the Europe document management services market is the high implementation cost associated with deploying comprehensive document management systems, particularly for small and medium-sized enterprises (SMEs). While larger corporations can absorb the upfront investment required for software licensing, system integration, employee training, and cybersecurity enhancements, SMEs often struggle with budget constraints. Moreover, legacy IT infrastructures in some SMEs require extensive upgrades before integrating modern document management platforms, adding to the overall cost burden. As per the Federation of European Accountants (FEE), retrofitting outdated accounting and HR systems to align with new document repositories could increase project expenses by up to 30%. Additionally, concerns around return on investment (ROI) persist among smaller firms. A 2023 survey conducted by the German Chamber of Industry and Commerce (DIHK) revealed that only 32% of SMEs believed that digital document management would yield measurable productivity gains within the first year of deployment.

Fragmentation of Standards and Interoperability Challenges

Another critical restraint impacting the Europe document management services market is the fragmentation of standards and interoperability challenges across different systems and jurisdictions. For instance, while the European Committee for Standardization (CEN) has endorsed EN 16124 as a standard for digital document authentication, individual countries have implemented additional specifications. According to the European Commission’s 2023 report on digital single market progress, discrepancies in metadata tagging, encryption protocols, and archiving durations hinder seamless cross-border document exchange. This lack of uniformity increases integration costs and delays deployment timelines, especially for multinational corporations and law firms managing pan-European transactions. As per PwC’s 2023 Digital Governance Survey, 58% of legal professionals reported difficulties in reconciling document formats across EU jurisdictions by leading to inefficiencies in contract management and compliance reporting. Moreover, the absence of universally accepted APIs and middleware solutions exacerbates compatibility issues between legacy systems and newer cloud-based platforms. The European Union Agency for Cybersecurity (ENISA) noted in its 2023 report that inconsistent data exchange protocols also pose security risks, which is making organizations more vulnerable to breaches during document transfers.

MARKET OPPORTUNITIES

Integration of Artificial Intelligence and Machine Learning in Document Processing

An emerging opportunity in the Europe document management services market lies in the integration of artificial intelligence (AI) and machine learning (ML) technologies into document processing workflows. These advancements enable automated categorization, intelligent search capabilities, anomaly detection, and predictive analytics, significantly enhancing the efficiency and accuracy of document handling. According to IDC’s 2023 European Enterprise Software Trends report, organizations leveraging AI-driven document management solutions experienced a 35% reduction in manual data entry tasks and a 28% improvement in retrieval speed. This is particularly beneficial in sectors such as legal, healthcare, and financial services, where timely access to accurate information is critical.

Leading vendors like DocuWare, M-Files, and OpenText have introduced AI-powered features such as natural language processing (NLP) for document summarization and optical character recognition (OCR) enhancements for improved scanned document readability. As per Accenture’s 2023 Intelligent Automation Benchmark, law firms using AI-integrated document systems reduced case preparation time by up to 40%.

Moreover, AI-assisted compliance monitoring helps organizations detect inconsistencies or missing documentation in real time, ensuring adherence to evolving regulatory landscapes. The European Data Protection Board has acknowledged the potential of AI in automating GDPR-related record checks, minimizing human error and oversight gaps.

Expansion of Remote Work and Hybrid Business Models

Another transformative opportunity for the Europe document management services market is the sustained expansion of remote work and hybrid business models. The pandemic-induced shift toward decentralized workplaces has reinforced the necessity of secure, cloud-accessible document platforms that support seamless collaboration regardless of location.

Businesses are increasingly adopting unified content management platforms such as Microsoft SharePoint, Google Workspace, and Dropbox, which integrate document management with communication and workflow automation tools. As per McKinsey’s 2023 Workplace of the Future Report, companies investing in cloud-based document ecosystems saw a 25% increase in employee productivity and a 20% reduction in document-related errors.

Government agencies have also embraced this model, particularly in countries like Finland and the Netherlands, where digital-first policies support telecommuting and virtual public services. The Dutch Ministry of Interior Affairs reported in 2023 that digital document accessibility contributed to a 30% faster decision-making process in public procurement.

MARKET CHALLENGES

Data Security and Privacy Concerns in Cloud-Based Document Systems

A pressing challenge confronting the Europe document management services market is the heightened concern around data security and privacy, particularly concerning cloud-based document storage and sharing platforms. According to the European Union Agency for Cybersecurity (ENISA), ransomware attacks targeting cloud infrastructure increased by 42% in 2023 compared to the previous year with the vulnerability of digital document ecosystems. In response, enterprises must implement multi-layered security measures, including end-to-end encryption, multi-factor authentication, and continuous threat monitoring, which add complexity and cost. Privacy concerns are further amplified by stringent regulations such as the General Data Protection Regulation (GDPR), which mandates strict control over how personal data is stored and processed. As per the European Data Protection Board, non-compliant cloud document systems can result in substantial fines and reputational damage, compelling businesses to conduct rigorous vendor assessments before deployment. Additionally, the proliferation of third-party integrations in document management platforms introduces additional risks. The UK’s Information Commissioner’s Office (ICO) warned in 2023 that improper API configurations in cloud document systems were responsible for several high-profile data leaks involving employee and client records.

Resistance to Change Among Legacy Organizations

Another significant challenge facing the Europe document management services market is the resistance to change observed among legacy organizations, particularly in traditional sectors such as legal, manufacturing, and public administration. Many institutions remain deeply entrenched in paper-based workflows and legacy IT systems, hindering the adoption of modern digital document solutions.

According to a 2023 study conducted by the European Central Bank, nearly 38% of micro-enterprises in Southern and Eastern Europe still relied on physical document storage due to familiarity, skepticism about digital reliability, and limited awareness of available tools. This reluctance is particularly prevalent in older groups and rural enterprises with minimal digital literacy.

Moreover, the transition to digital document management often requires extensive retraining of staff and changes in internal procedures, which many organizations perceive as disruptive and resource-intensive. As per the French National Institute of Statistics and Economic Studies (INSEE), only 29% of SMEs in France had fully digitized their document processes by mid-2023, citing employee pushback as a major hurdle. Public sector inertia further compounds the issue. In Italy, for example, the Ministry of Innovation reported that despite national digitization mandates, many local government offices continued to rely on physical records due to bureaucratic inertia and insufficient funding for digital upgrades.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| CAGR | 14.1 % |

| Segments Covered | By Service, End-user and Country. |

| Various Analyses Covered | Global, Regional, & Country Level Analysis; Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Country Covered | UK, Germany, Italy, France, Spain, Sweden, Denmark, Poland, Switzerland, Netherlands, Rest of Europe. |

| Market Leaders Profiled | McKesson Corporation (U.S.), Toshiba Medical Systems Corporation (Japan) |

SEGMENT ANALYSIS

By Service Insights

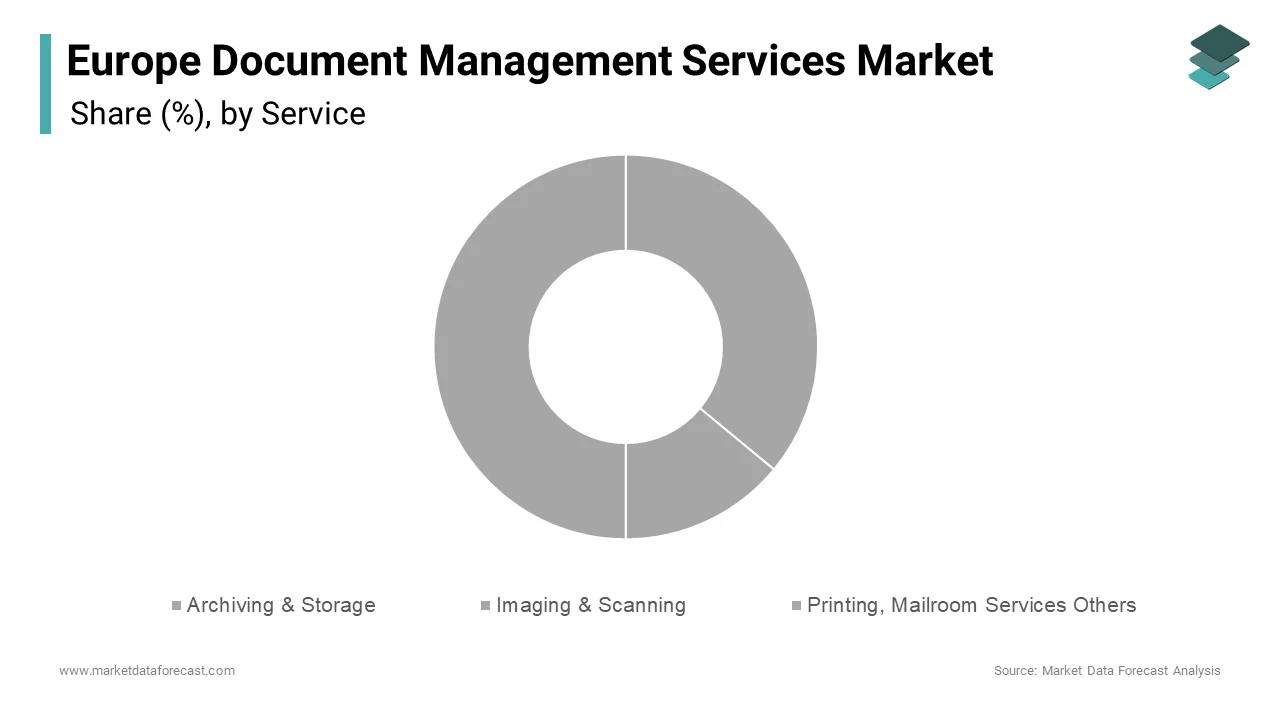

The archiving and storage segment dominated the Europe document management services market by accounting for 36.3% of share in 2024 with the growing need for secure, scalable, and compliant digital repositories that support long-term data retention across regulated industries. Another key driver is the increasing volume of electronic records generated by businesses in financial institutions, legal firms, and government agencies. Additionally, cloud-based archiving solutions have gained traction due to their flexibility and cost-efficiency compared to traditional on-premises systems. Furthermore, the rise of AI-powered metadata tagging and search functionalities has enhanced retrieval efficiency, which is making digital archives more valuable beyond mere compliance.

The imaging and scanning segment is swiftly emerging with a CAGR of 11.8% from 2024 to 2033. A major catalyst is the push by national governments to modernize administrative processes through e-governance initiatives. In Germany, for instance, the Federal Archives reported that over 2.3 million historical documents were digitized in 2023 under a state-funded program aimed at preserving cultural and legal records. France’s Ministry of Justice launched a nationwide initiative to convert court records into digital formats is significantly boosting demand for high-volume scanning services. Moreover, healthcare institutions are increasingly adopting medical imaging digitization to improve patient record accessibility and reduce physical storage burdens. According to the European Health Information Initiative, nearly 60% of hospitals in Western Europe implemented centralized document scanning systems by mid-2023 by enhancing interdepartmental coordination and regulatory compliance. Advancements in optical character recognition (OCR) technology have also made scanned documents searchable and editable by adding value beyond simple conversion.

By End-user Insights

The Banking, Financial Services, and Insurance (BFSI) sector held 28.6% of the Europe document management services market share in 2024. Financial institutions are subject to extensive documentation requirements imposed by regulators such as the European Banking Authority (EBA) and the Financial Conduct Authority (FCA). As per EBA’s 2023 Compliance Report, banks must retain transaction records, customer identification documents, and internal communications for periods ranging from five to ten years, necessitating robust digital archiving solutions. Moreover, the shift toward digital banking and insurance claims processing has amplified the need for automated document workflows. Additionally, the BFSI sector has been an early adopter of cloud-based document repositories to ensure disaster recovery and business continuity.

The healthcare segment is likely to grow with a CAGR of 12.4% from 2025 to 2033. This surge is driven by the increasing digitization of medical records, rising regulatory demands, and the need for seamless interoperability in patient care. The implementation of electronic health records (EHRs) has become a priority for national health systems across Europe. According to the European Commission’s 2023 Digital Health Strategy, all EU member states had adopted some form of digital health infrastructure, with countries like Sweden and Estonia leading in full-scale implementation. Hospitals and clinics are also adopting document management systems integrated with AI and machine learning to enhance diagnostic accuracy and operational efficiency. A 2023 study by the Karolinska Institute found that AI-assisted document indexing reduced medical transcription errors by 37%, improving clinical decision-making.

COUNTRY LEVEL ANALYSIS

Germany was the top performer in the Europe document management services market with 19.7% of share in 2024. As Europe’s largest economy, Germany benefits from a mature digital infrastructure and stringent regulatory mandates that encourage widespread adoption of compliant document management systems. According to the German Federal Office for Information Security (BSI), in 2023, over 80% of large enterprises had implemented GDPR-compliant document management solutions to avoid regulatory penalties. Moreover, Germany’s industrial sector, particularly manufacturing and automotive, relies heavily on digital document workflows to streamline supply chain operations and product lifecycle management. Public sector digitization efforts, including the “Digital Agenda for the Public Sector” launched by the Federal Ministry of the Interior, have further accelerated adoption.

The United Kingdom was ranked second with 14.3% of the Europe document management services market share in 2024. The UK’s position is largely supported by strong demand from the banking, finance, and legal sectors, which prioritize document security, audit readiness, and compliance with evolving data regulations.

Following Brexit, UK firms have faced additional complexities in aligning with both domestic and EU regulatory frameworks, prompting greater reliance on sophisticated document management solutions. According to the Financial Conduct Authority (FCA), over 70% of financial institutions in the UK updated their document retention policies in 2023 to accommodate post-Brexit compliance needs.

France document management services market growth is swiftly growing with the aggressive government-led digitization programs and a growing emphasis on public sector efficiency. The French government’s “France Relance” digital strategy has prioritized the modernization of administrative processes, leading to increased adoption of digital document workflows in taxation, social services, and justice departments.

According to the Direction Interministérielle du Numérique (DINUM), over 90% of public sector agencies had deployed electronic document management systems by mid-2024, facilitating faster citizen service delivery and reducing bureaucratic delays. Additionally, the Ministry of Justice initiated a nationwide project to digitize court records, which is significantly boosting demand for imaging and content management services.

Spain document management services market is likely to grow with significant growth opportunities with the increasing digital transformation efforts in public administration and healthcare, supported by national funding and policy incentives. The Spanish government’s "Digital Spain 2025" strategy includes a mandate for all public institutions to implement electronic document management systems by 2026. Healthcare institutions are also accelerating digitization to comply with EU-wide health data exchange standards. The Ministry of Health reported that in 2023, nearly 50% of hospitals had transitioned to centralized document management systems to manage patient records, prescriptions, and discharge summaries more efficiently.

Moreover, the legal sector is embracing digital archiving to meet new judicial process reforms requiring electronic submission of court filings. As per the Spanish Bar Association, over 40% of law firms now use cloud-based document platforms for secure client communication and evidence tracking.

Italy document management services market growth is driven by a strong push toward e-government initiatives and corporate digitization in the wake of national recovery plans funded by the European Union. In the private sector, financial institutions and insurance companies are leveraging document management solutions to meet Solvency II and MiFID II compliance requirements. PwC’s 2024 Italian Financial Services Review indicated that 62% of surveyed firms had upgraded their document infrastructure to enhance audit trails and risk reporting capabilities.

Additionally, the legal profession is undergoing a digital shift, with law firms adopting AI-powered contract analysis tools to streamline litigation and transactional work. The Italian National Bar Council reported that in 2024, nearly half of all legal professionals used digital document platforms daily for case management and client interactions.

KEY MARKET PLAYERS AND COMPETITIVE LANDSCAPE

Companies playing a significant role in the European medical documents management market are McKesson Corporation (U.S.), Toshiba Medical Systems Corporation (Japan), Cerner Corporation (U.S.), Kofax Ltd. (U.S.), EPIC Systems (U.S.), 3M Company (U.S.), Siemens Medical Solutions USA, Inc. (U.S.), GE Healthcare (U.S.), Allscripts Healthcare Solutions, Inc. (U.S.) and Hyland Software (U.S.)

The competition in the Europe document management services market is marked by a blend of established enterprise software providers and agile niche players offering specialized solutions. As regulatory pressures intensify and digital transformation accelerates, vendors are continuously innovating to differentiate their offerings and capture a larger share of the market. Large players like OpenText and DocuWare focus on comprehensive, end-to-end platforms that cater to complex organizational needs, while emerging providers emphasize ease of use, affordability, and vertical-specific customization. The demand for cloud-native architectures, artificial intelligence integration, and seamless interoperability has intensified rivalry, prompting strategic investments in R&D and ecosystem expansion. Additionally, the growing emphasis on compliance with data protection laws such as GDPR has heightened the need for secure and auditable document handling solutions. Companies are also competing on customer experience, offering personalized onboarding, training, and support to ensure long-term client retention.

Top Players in the Market

OpenText Corporation

OpenText is a leading global provider of enterprise information management solutions, with a strong presence in the Europe document management services market. The company offers a comprehensive suite of tools designed to streamline document capture, workflow automation, compliance management, and secure content collaboration. OpenText’s platform supports large enterprises across banking, healthcare, and government sectors by enabling seamless digital transformation. Its emphasis on integration with legacy systems and support for regulatory frameworks such as GDPR makes it a trusted partner for European organizations seeking scalable and secure document infrastructure.

DocuWare GmbH

DocuWare specializes in cloud-based document management and workflow automation, catering to both mid-sized businesses and large corporations across Europe. Known for its user-friendly interface and modular architecture, DocuWare enables organizations to digitize paper-based processes, automate approvals, and improve data accessibility. The company has been instrumental in helping SMEs transition to digital document workflows without significant IT overhead.

M-Files Corporation

M-Files stands out for its intelligent information management platform that organizes documents and data based on context rather than storage location. This approach enhances searchability, access control, and metadata-driven organization, making it ideal for knowledge-intensive industries. In Europe, M-Files has gained traction among legal firms, engineering companies, and public institutions requiring advanced document classification and retrieval capabilities.

Top strategies used by the key market participants

A primary strategy employed by leading players in the Europe document management services market is enhancing product portfolios through continuous innovation in AI-driven document processing, metadata tagging, and automated workflow orchestration to meet evolving business needs.

Another major tactic involves deepening partnerships with cloud service providers and ERP vendors , allowing document management platforms to integrate seamlessly with broader enterprise ecosystems and ensuring compatibility with widely used business applications.

Companies are expanding localized service offerings and strengthening regional support structures , including multilingual customer assistance and compliance-specific configurations tailored to national regulations, thereby improving adoption across diverse European markets.

RECENT HAPPENINGS IN THE MARKET

In February 2024, OpenText expanded its cloud-based document security suite with enhanced encryption and audit trail features specifically tailored for EU financial institutions by reinforcing its dominance in GDPR-compliant document management.

In May 2024, DocuWare launched a new AI-powered document classification module designed to automate tagging and retrieval for law firms and legal departments across Germany and France, enhancing efficiency and reducing manual processing time.

In July 2024, M-Files partnered with SAP to deepen integration between its document management platform and SAP S/4HANA, enabling real-time document access within enterprise resource planning workflows for manufacturing clients in Italy and Spain.

In September 2024, Lexmark acquired a Finnish document analytics startup to bolster its intelligent capture capabilities, aiming to offer more advanced insights and automation features to public sector clients in Scandinavia and Benelux countries.

In November 2024, Hyland integrated its OnBase platform with Microsoft Teams across Europe, allowing businesses to manage document workflows directly within collaboration tools, enhancing productivity for remote and hybrid teams.

MARKET SEGMENTATION

This research report has been segmented the european medical document management market into the following sub-segments.

By Service

- Archiving & Storage

- Imaging & Scanning

- Printing, Mailroom Services Others

By End-user

- BFSI

- IT & Telecom

- Government

- Manufacturing

- Retail

- Healthcare

- Others

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

What is driving the growth of the Document Management Services market in Europe?

Key drivers include: Rising digital transformation across industries Increasing regulatory compliance requirements (e.g., GDPR) Growth in remote/hybrid working models

Which industries are the primary adopters of Document Management Services in Europe?

Major sectors include: Healthcare BFSI (Banking, Financial Services & Insurance) Government Legal Manufacturing

How does GDPR impact the Document Management Services market in Europe?

GDPR mandates strict data privacy and storage rules, increasing the demand for secure and compliant document management solutions that can track access and ensure proper data handling.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com