Europe Medical Waste Management Market Research Report – Segmented By Service (collection, recycling ) Type of Waste ( non-hazardous, infectious waste ) Treatment ( offsite treatment, onsite treatment) & Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic & Rest of EU) - Industry Analysis on Size, Share, Trends & Growth Forecast (2026 to 2034)

Market Size, 2025

$10.11 BnMarket Estimate, 2026

$10.73 BnMarket Forecast, 2034

$17.23 BnCAGR, 2026–2034

6.1%Executive Summary: Europe Medical Waste Management Market

- Market Scope: Comprehensive regional medical waste management market analysis covering service categories, waste types, treatment methods, country-specific leadership frameworks, and key strategic developments.

- Market Valuation: Valued at USD 10.11 billion (2025), estimated at USD 10.73 billion (2026), and projected to reach USD 17.23 billion by 2034, registering a robust CAGR of 6.1% (2026–2034).

- Primary Growth Drivers: Stringent regulatory frameworks (European Waste Framework Directive), rising healthcare expenditures, and an aging population. Opportunities include IoT-enabled waste monitoring, circular economy recycling initiatives, and advanced offsite/onsite treatment methods (autoclaving/microwaving).

Key Market Segment Metrics (2026–2034)

| Category | Leading Segment (2025 Position) | Fastest-Growing Segment |

|---|---|---|

| By Service & Waste Type | Collection segment (held 40.1% share); Non-hazardous waste (captured largest share of 60.1%) | Recycling segment (highest CAGR of 12.6%); Infectious waste segment (anticipated CAGR of 10.4%) |

| By Treatment & Region | Offsite treatment (held dominant share); Germany (led market with 22.3% share in 2025) | Onsite treatment segment (CAGR of 9.2%); United Kingdom (projected CAGR of 12.3%) |

Major Market Players & Market Structure

Market Structure: Highly competitive European environmental services and medical waste landscape featuring major multinational waste management corporations competing intensely on centralized treatment expansion, IoT tracking, and recycling startups.

Key Companies: Veolia Group, SUEZ Group, Stericycle Inc., FCC Environmental Services, Renewi, Biffa PLC, Saica Group, Coventa Holding Corporation, Indver, Viridor, REMONDIS SE & Co. KG, and Fortum.

Europe Medical Waste Management Market Size

The Europe Medical Waste Management Market is projected to grow from USD 10.11 billion in 2025 to USD 10.73 billion in 2026 and reach USD 17.23 billion by 2034, registering a CAGR of 6.10% from 2026 to 2034.

The Europe medical waste management market is a critical segment within the broader healthcare infrastructure due to the region's emphasis on sustainability and public health safety. According to Eurostat, the European Union generates approximately 2.5 million tons of medical waste annually, with countries like Germany, France, and the UK contributing significantly to this volume. The stringent regulatory framework, such as the European Waste Framework Directive, mandates safe disposal and treatment of medical waste by ensuring compliance across member states. As per the World Health Organization, improper disposal of medical waste poses significant risks by including environmental contamination and public health hazards, which has led to increased investments in advanced waste management technologies. The market is witnessing steady growth that is driven by rising healthcare expenditures and an aging population that amplifies medical waste generation. Furthermore, the COVID-19 pandemic acted as a catalyst is increasing the demand for efficient waste management systems due to the surge in infectious waste. This scenario underscores the importance of robust infrastructure, with private players increasingly collaborating with governments to meet these demands. The market's maturity is evident from its adoption of innovative solutions, such as autoclaving and microwaving, alongside traditional incineration methods.

MARKET DRIVERS

Stringent Regulatory Framework

The regulatory environment in Europe plays a pivotal role in driving the medical waste management market. According to the European Environment Agency, regulations such as the Waste Incineration Directive and the Medical Devices Regulation impose strict guidelines on waste segregation, treatment, and disposal. These regulations mandate healthcare facilities to adopt environmentally sustainable practices, thereby boosting demand for professional waste management services. For instance, as per a study by the European Commission, non-compliance with waste management protocols can result in fines exceeding €500,000 in certain jurisdictions, incentivizing institutions to partner with certified waste management providers. Additionally, the EU’s Circular Economy Action Plan emphasizes reducing landfill use and promoting recycling, further propelling investments in advanced waste treatment technologies. Data from the European Federation of Waste Management indicates that over 80% of medical waste in the region is now treated through compliant methods, reflecting the impact of regulatory enforcement. These measures have created a lucrative market for service providers offering end-to-end solutions by ensuring adherence to legal standards while minimizing ecological footprints.

Rising Healthcare Expenditures

Europe’s escalating healthcare expenditures are another significant driver of the medical waste management market. According to the Organisation for Economic Co-operation and Development (OECD), healthcare spending in Europe reached approximately €2 trillion in 2022, with countries like Germany and France accounting for the largest shares. Increased funding translates into expanded healthcare infrastructure, including hospitals, diagnostic centers, and pharmaceutical manufacturing units, all of which generate substantial medical waste. According to the European Observatory on Health Systems, hospital waste alone constitutes nearly 40% of total medical waste in the region. Furthermore, advancements in medical treatments and surgeries, coupled with an aging population, contribute to higher waste volumes. For example, as per Eurostat, the number of surgical procedures performed annually in Europe has grown by 15% over the past decade is directly correlating with increased waste generation. This trend necessitates robust waste management systems, creating opportunities for specialized service providers to address the growing demand.

MARKET RESTRAINTS

High Operational Costs

One of the primary restraints impacting the Europe medical waste management market is the high operational costs associated with waste treatment and disposal. According to a study by the European Healthcare Waste Management Association, the cost of treating one ton of medical waste through advanced methods like autoclaving or incineration ranges between €500 and €1,000, depending on the technology and location. These expenses are primarily driven by the need for specialized equipment, energy consumption, and compliance with stringent environmental regulations. For instance, as per the European Environment Agency, incineration facilities require substantial capital investment, with installation costs often exceeding €10 million. Smaller healthcare facilities, particularly in rural areas, struggle to afford these services, leading to fragmented adoption rates. Additionally, fluctuations in energy prices further exacerbate operational challenges, with natural gas price volatility in 2022 increasing incineration costs by nearly 20%. Such financial burdens limit the scalability of waste management solutions for low-margin healthcare providers, thereby hindering market expansion.

Limited Awareness and Training

Another significant restraint is the limited awareness and training among healthcare professionals regarding proper waste management practices. According to a survey conducted by the European Centre for Disease Prevention and Control, over 30% of healthcare workers in Europe lack adequate knowledge about waste segregation and handling protocols. This gap in understanding often leads to improper disposal, increasing contamination risks and undermining waste management efficiency. For example, as per a report by the European Public Health Alliance, approximately 15% of medical waste in the region is incorrectly segregated is resulting in higher treatment costs and environmental hazards. Moreover, inadequate training programs and inconsistent implementation of guidelines across member states exacerbate the issue. While initiatives like the EU’s Green Deal aim to promote education and awareness, progress remains slow due to resource constraints and varying priorities among healthcare institutions. This lack of preparedness not only compromises waste management outcomes but also limits the adoption of innovative solutions is impeding market growth.

MARKET OPPORTUNITIES

Adoption of Digital Technologies

The integration of digital technologies presents a significant opportunity for the Europe medical waste management market. According to a report by the European Digital Health Observatory, the adoption of Internet of Things (IoT) devices and artificial intelligence (AI) in waste management is likely to surge in the next coming fortune years. IoT-enabled sensors can monitor waste levels in real-time, optimizing collection schedules and reducing operational inefficiencies. For instance, as per a case study by the European Innovation Council, a hospital in Sweden implemented IoT-based waste bins by resulting in a 25% reduction in logistics costs. Similarly, AI-driven predictive analytics can forecast waste generation patterns by enabling better resource allocation and cost management. The European Commission estimates that digitization could save up to €2 billion annually in waste management expenses across the region. Furthermore, blockchain technology offers enhanced traceability by ensuring compliance with regulatory standards. These innovations not only improve operational efficiency but also align with the EU’s sustainability goals that is making digital transformation a key growth avenue.

Expansion of Recycling Initiatives

Recycling initiatives represent another promising opportunity for the Europe medical waste management market. According to the European Recycling Industries’ Confederation, less than 10% of medical waste is currently recycled by leaving substantial room for improvement. Non-hazardous waste, such as packaging materials and unused medical supplies, accounts for nearly 70% of total medical waste, as per data from the European Federation of Waste Management. Implementing advanced recycling technologies, such as chemical recycling and biodegradable material processing, can significantly reduce landfill dependency and promote circular economy principles. For example, a pilot project in the Netherlands demonstrated that recycling plastic medical waste could recover up to 90% of raw materials, generating additional revenue streams. The European Green Deal emphasizes increasing recycling rates to 65% by 2030 by providing a regulatory push for innovation in this space. Stakeholders can unlock new market potential while contributing to environmental sustainability by investing in recycling infrastructure and fostering partnerships with recyclers.

MARKET CHALLENGES

Complex Regulatory Compliance

Navigating the complex regulatory landscape poses a significant challenge for the Europe medical waste management market. According to the European Environmental Bureau, each member state interprets EU directives differently is leading to fragmented regulations and inconsistent enforcement. For instance, while Germany mandates 100% compliance with waste segregation protocols, other countries may allow partial adherence by creating operational difficulties for multinational service providers. According to a report by the European Parliament, discrepancies in waste classification and reporting standards often result in legal ambiguities that is increasing administrative burdens. Additionally, frequent updates to regulations, such as the recent amendments to the Medical Devices Regulation, require continuous adaptation, straining resources. As per the European Healthcare Waste Management Association, over 40% of companies cite regulatory complexity as a major obstacle to market entry.

Resistance to Change

Resistance to adopting new waste management practices is another pressing challenge in the Europe medical waste management market. According to a study by the European Health Management Association, nearly 40% of healthcare facilities resist transitioning from traditional incineration methods to advanced technologies like autoclaving or microwaving. For example, as per a survey by the European Hospital and Healthcare Federation, many institutions prioritize short-term budgetary constraints over long-term sustainability benefits is delaying the adoption of eco-friendly solutions. Furthermore, cultural barriers and entrenched practices exacerbate the issue, with some stakeholders viewing change as unnecessary or burdensome. The European Commission notes that overcoming resistance requires targeted awareness campaigns and financial incentives, yet progress remains slow due to limited funding and competing priorities.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Service, Type of Waste, Treatment and Country. |

| Various Analyses Covered | Global, Regional, & Country Level Analysis; Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Country Covered | UK, Germany, Italy, France, Spain, Sweden, Denmark, Poland, Switzerland, Netherlands, Rest of Europe. |

| Market Leaders Profiled | FCC Environmental Services, SUEZ,Veolia,Renewi,Biffa PLC,Saica Group,Coventa Holding Corporation |

SEGMENT ANALYSIS

By Service Insights

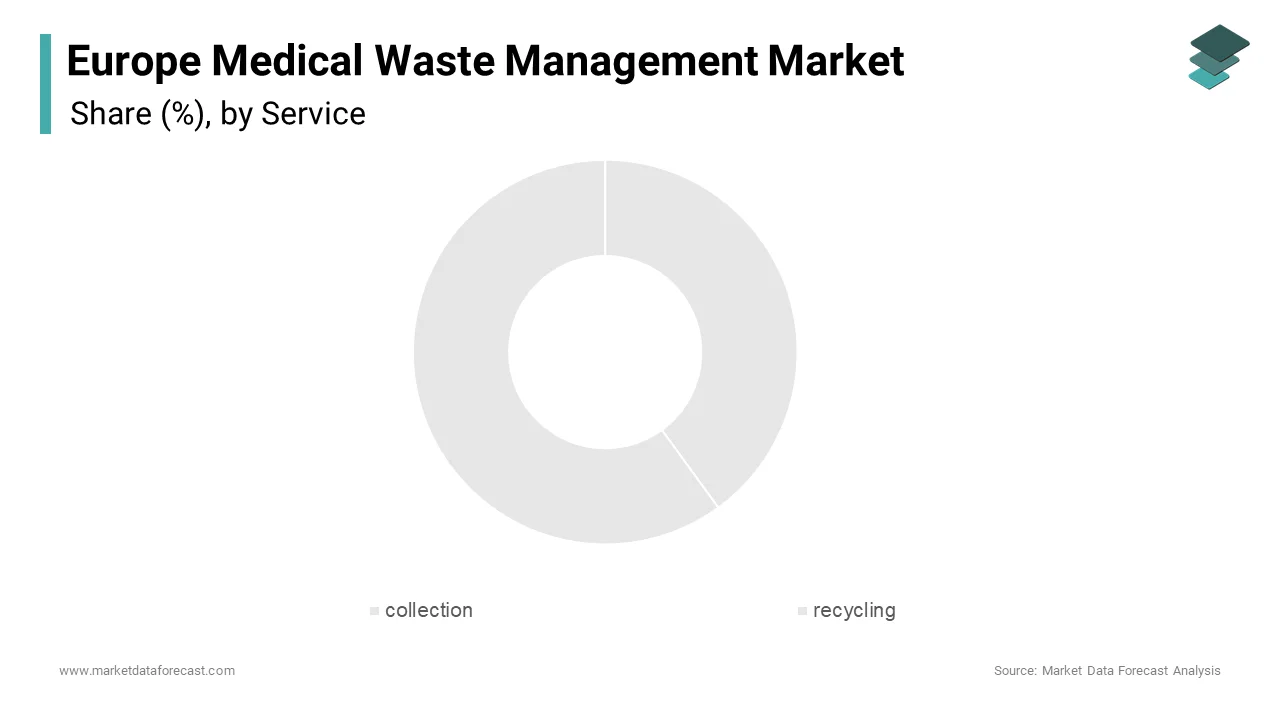

The collection segment dominated the Europe medical waste management market by capturing 40.1% of the share in 2025. The growth of the segment is driven by the critical need for timely and efficient waste removal from healthcare facilities to prevent contamination and ensure compliance with regulations. According to a report by the European Environment Agency, improper collection practices can lead to a 30% increase in environmental and health risks. The rise in outpatient care facilities and diagnostic centers, which generate significant waste volumes, further fuels demand for collection services. For instance, as per Eurostat, the number of outpatient visits in Europe increased by 25% over the past five years is correlating with higher waste generation. Additionally, government initiatives promoting door-to-door collection services have bolstered adoption rates. The European Commission estimates that optimized collection systems could reduce waste-related risks by up to 50% with the segment's pivotal role in ensuring public safety and environmental protection.

The recycling segment is gaining huge traction in the Europe medical waste management market with a projected CAGR of 12.6% from 2025 to 2033. This rapid growth is fueled by increasing awareness of sustainability and the EU’s commitment to achieving a circular economy. For example, as per the European Green Deal, member states are mandated to increase recycling rates to 65% by 2030 is driving investments in advanced recycling technologies. Non-hazardous waste, which constitutes nearly 70% of total medical waste, offers immense recycling potential. According to a study by the European Federation of Waste Management, recycling plastic medical waste can recover up to 90% of raw materials is creating economic value and reducing landfill dependency.

By Type of Waste Insights

The non-hazardous waste was the largest segment in the Europe medical waste management market with an estimated share of 60.1% in 2025 owing to the high volume of packaging materials, disposable plastics, and unused medical supplies generated by healthcare facilities. According to a report by the European Commission, non-hazardous waste accounts for over 70% of total medical waste. The increasing adoption of single-use medical devices, driven by hygiene considerations, further amplifies waste volumes. Additionally, regulatory frameworks emphasizing waste segregation have streamlined the identification and management of non-hazardous waste is enhancing recycling potential. According to the European Green Deal, recycling non-hazardous waste can reduce landfill dependency by up to 40% is positioning it as a cornerstone of sustainable waste management practices.

The infectious waste segment is likely to witness a significant CAGR of 10.4% during the forecast period. This growth is driven by the rising incidence of infectious diseases and the increased use of personal protective equipment (PPE) during the COVID-19 pandemic. For example, as per a study by the European Public Health Alliance, infectious waste volumes surged by 30% in 2020, with no signs of abating as healthcare systems remain vigilant against future outbreaks. Hospitals and diagnostic centers, which generate the majority of infectious waste, are prioritizing safe disposal methods to mitigate contamination risks. The European Federation of Waste Management notes that advanced treatment technologies, such as autoclaving and microwaving, are increasingly adopted to handle infectious waste efficiently. Furthermore, government initiatives promoting the development of specialized treatment facilities have bolstered market growth.

By Treatment Site Insights

The offsite treatment segment held the dominant share of the Europe medical waste management market in 2025. The segment growth is attributed by the centralized nature of offsite facilities, which offer economies of scale and advanced treatment capabilities. According to the European Environment Agency, offsite treatment ensures higher compliance with regulatory standards, as these facilities are equipped with state-of-the-art technologies like incineration and autoclaving. For instance, a report by the European Commission have shown that the offsite facilities treat over 70% of hazardous medical waste will escalate the importance. The proliferation of small healthcare facilities in rural areas will further drives demand for offsite services, as they lack the infrastructure for onsite treatment. Additionally, government subsidies and incentives encourage the use of centralized facilities thereby reducing operational costs for healthcare providers. The European Green Deal emphasizes the role of offsite treatment in achieving sustainability goals is positioning it as a cornerstone of the market.

The onsite treatment segment is likely to grow with a CAGR of 9.2% in the foreseen years. This growth is fueled by the increasing adoption of compact, modular treatment systems that enable healthcare facilities to manage waste internally. For example, as per a study by the European Innovation Council, hospitals using onsite autoclaving systems reported a 20% reduction in waste management costs is driving adoption rates. The rising focus on sustainability and carbon footprint reduction further supports this trend, as onsite treatment minimizes transportation emissions. The European Commission notes that onsite solutions align with the EU’s circular economy objectives, promoting localized waste management practices. Additionally, advancements in technology, such as portable incinerators and microwave systems, have made onsite treatment more accessible and cost-effective. These factors position onsite treatment as a transformative force in the market is addressing both environmental and economic priorities.

Country Level Analysis

Germany was the top performer in the Europe medical waste management market with a significant CAGR of 22.3% of share in 2025 with the robust healthcare infrastructure and stringent regulatory framework, which mandates sustainable waste management practices. According to the German Federal Environment Agency, the nation generates over 300,000 tons of medical waste annually, with infectious waste accounting for nearly 40%. The adoption of advanced technologies like autoclaving and microwaving has surged, supported by €500 million in government subsidies for eco-friendly solutions. Additionally, Germany’s Circular Economy Act emphasizes recycling, with a target to recycle 65% of non-hazardous waste by 2030.

The UK medical waste management market is projected to experience a significant CAGR of 12.3% in the next coming years. driven by its focus on sustainability and public health safety. As per the UK Health Security Agency, the country generated approximately 250,000 tons of medical waste in 2022, with infectious waste witnessing a 20% surge post-COVID-19. The UK’s National Health Service (NHS) has implemented strict segregation protocols, ensuring compliance with EU directives despite Brexit. According to a report by the UK Department for Environment, Food & Rural Affairs, investments in offsite treatment facilities have grown by 15% annually since 2020, enhancing waste management capacity. Furthermore, the UK’s commitment to achieving net-zero emissions by 2050 has accelerated the adoption of energy-efficient incineration technologies.

France medical waste management market is to have steady growth opportunities in the next coming years owing to its emphasis on environmental sustainability and innovation. According to the French Ministry of Ecological Transition, the country treats over 200,000 tons of medical waste annually, with recycling rates exceeding 50% for non-hazardous waste. The implementation of the French Circular Economy Roadmap has encouraged hospitals and clinics to adopt advanced recycling technologies, reducing landfill dependency. A study by the European Environment Agency notes that France’s investment in modular onsite treatment systems has increased by 25% over the past five years, enabling localized waste management. Additionally, the French government provides €300 million annually in subsidies for sustainable practices. The rise in outpatient care facilities, which generate significant waste volumes that will further fuels demand for efficient waste management solutions.

Italy is to have prominent growth rate in the next coming years owing to its growing healthcare sector and regulatory compliance. According to the Italian National Institute of Health, the country generates around 180,000 tons of medical waste annually, with pharmaceutical waste being a major concern. Italy’s Green Public Procurement policies mandate the use of eco-friendly disposal methods by promoting the adoption of autoclaving and chemical treatment technologies. According to a report by the Italian Environmental Protection Agency, over 80% of medical waste is treated through compliant methods is reflecting high adherence to standards. Furthermore, the Italian government allocates €200 million annually for waste management infrastructure upgrades.

Spain holds an 8% share of the Europe medical waste management market, supported by its expanding healthcare infrastructure and focus on sustainability. According to the Spanish Ministry of Health, the country generates approximately 150,000 tons of medical waste annually, with infectious waste accounting for nearly 30%. Spain’s National Waste Management Plan emphasizes reducing landfill use and increasing recycling rates, aligning with EU sustainability goals. A study by the Spanish Confederation of Healthcare Technology Companies notes that investments in digital waste management solutions, such as IoT-enabled tracking systems, have grown by 20% annually since 2021. Additionally, the government provides €150 million in annual funding for advanced treatment technologies. The rise in outpatient visits, which increased by 18% over the past five years, correlates with higher waste volumes, driving demand for efficient management practices and cementing Spain’s position in the regional market.

Top 3 Players in the market

Veolia Group

Veolia Group plays a pivotal role in the Europe medical waste management market by offering comprehensive solutions that align with sustainability goals. The company specializes in advanced waste treatment technologies, including autoclaving and microwaving, which ensure compliance with stringent EU regulations. Veolia’s partnerships with healthcare institutions and governments have enabled the establishment of centralized treatment facilities to reduce operational costs and environmental impact. The company’s innovative approach includes integrating digital tools like IoT sensors to monitor waste levels and optimize collection schedules by enhancing efficiency.

SUEZ Group

SUEZ Group is a key contributor to the Europe medical waste management market, leveraging its expertise in resource recovery and waste reduction. The company focuses on developing modular onsite treatment systems, enabling healthcare facilities to manage waste internally while minimizing transportation emissions. SUEZ’s advanced recycling technologies, such as chemical processing, have positioned it as a leader in sustainable waste management. Its collaboration with regulatory bodies ensures adherence to EU directives, fostering trust among clients. SUEZ’s strategic investments in R&D have resulted in energy-efficient incineration methods, reducing carbon footprints.

Stericycle Inc.

Stericycle Inc. is a prominent player in the Europe medical waste management market, renowned for its specialized services in handling infectious and hazardous waste. The company’s state-of-the-art treatment facilities utilize autoclaving and shredding technologies to ensure safe disposal. Stericycle’s focus on education and training programs enhances awareness among healthcare professionals, promoting proper waste segregation practices. Its scalable solutions cater to diverse client needs, from small clinics to large hospitals, ensuring operational flexibility. Stericycle’s commitment to sustainability is reflected in its efforts to reduce landfill dependency by 50% through advanced recycling initiatives. The company’s global reach and localized strategies enable it to maintain a competitive edge in the market.

Top strategies used by the key market participants

Strategic Partnerships and Collaborations

Key players in the Europe medical waste management market leverage strategic partnerships to enhance their service offerings and expand their reach. For instance, collaborations with healthcare institutions and government bodies ensure compliance with regulatory standards while fostering trust. Veolia Group partnered with the French Ministry of Health to develop centralized treatment facilities, streamlining waste management processes. Such alliances enable companies to access new markets, share technological expertise, and co-invest in sustainable infrastructure to strengthen their market position.

Adoption of Digital Technologies

The integration of digital technologies is a cornerstone strategy for market leaders. Companies like SUEZ Group invest in IoT-enabled systems to monitor waste levels and optimize logistics, reducing operational inefficiencies. These innovations improve traceability and compliance, aligning with EU directives. Additionally, AI-driven predictive analytics forecast waste generation patterns, enabling proactive resource allocation.

Focus on Sustainability and Recycling

Sustainability-focused strategies are critical for maintaining relevance in the Europe medical waste management market. Stericycle Inc. emphasizes recycling initiatives, recovering raw materials from non-hazardous waste to promote circular economy principles. Investments in energy-efficient incineration and chemical recycling technologies reduce environmental impact. These efforts align with EU sustainability goals, attracting environmentally conscious clients.

KEY MARKET PLAYERS AND COMPETITIVE LANDSCAPE

Companies playing a prominent role in the Europe Medical Waste Management Market are FCC Environmental Services, SUEZ,Veolia,Renewi,Biffa PLC,Saica Group,Coventa Holding Corporation,Indver,Viridor,REMONDIS SE & Co. KG,Fortum .

The Europe medical waste management market is characterized by intense competition, driven by the presence of established players and emerging innovators. Key companies like Veolia Group, SUEZ Group, and Stericycle Inc. dominate the landscape, leveraging their expertise in advanced treatment technologies and sustainable practices. The market’s competitive dynamics are shaped by stringent EU regulations, which mandate compliance with waste management protocols, creating a high barrier to entry. Smaller players often struggle to compete due to high operational costs and complex regulatory frameworks. However, the rise of digital technologies and recycling initiatives presents opportunities for niche players to carve out specialized segments. Strategic partnerships, mergers, and acquisitions are common tactics used to consolidate market share and expand service portfolios. For instance, collaborations with healthcare institutions enable companies to offer end-to-end solutions, enhancing customer loyalty.

RECENT HAPPENINGS IN THE MARKET

In April 2023, Veolia Group launched a €100 million initiative to expand its network of centralized medical waste treatment facilities across Germany and France. This move aims to enhance waste management capacity and ensure compliance with EU regulations.

In June 2023, SUEZ Group announced a partnership with the Spanish Ministry of Health to implement IoT-enabled waste monitoring systems in 50 major hospitals. This collaboration seeks to optimize waste collection and reduce operational inefficiencies.

In September 2023, Stericycle Inc. acquired a UK-based recycling startup specializing in non-hazardous medical waste. This acquisition strengthens Stericycle’s recycling capabilities and aligns with its sustainability objectives.

In November 2023, Veolia Group signed a five-year contract with the Italian National Health Service to provide advanced autoclaving services for infectious waste. This agreement escalates Veolia’s commitment to innovation and regulatory compliance.

In January 2024, SUEZ Group introduced a pilot program in the Netherlands to test portable incineration units for onsite waste treatment. This initiative targets rural healthcare facilities, addressing logistical challenges and reducing transportation emissions.

MARKET SEGMENTATION

This research report on the Europe Medical Waste Management Market has been segmented and sub-segmented into the following categories.

By Service

- collection

- recycling

By Type of Waste

- non-hazardous

- infectious waste

By Treatment

- offsite treatment

- onsite treatment

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe.

Frequently Asked Questions

What is the Europe Medical Waste Management Market?

The Europe Medical Waste Management Market refers to the industry that deals with the collection, treatment, disposal, and recycling of medical waste generated by healthcare facilities, laboratories.

What are the major factors driving the growth of the medical waste management market in Europe?

Increasing healthcare waste due to the rise in hospital admissions & Strict government regulations and environmental policies.

Which countries in Europe have the largest medical waste management market?

Germany ,United Kingdom ,France, Italy & Spain

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com