Europe Molecular Diagnostics Market Size, Share, Trends & Growth Forecast Report By Product (Instruments, Reagents), By Test Location (Point of Care, Self-Test), By Technology, By Application, and Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic & Rest of Europe) Industry Analysis From 2026 to 2034.

Market Size, 2025

$8.25 BnMarket Estimate, 2026

$8.56 BnMarket Forecast, 2034

$11.51 BnCAGR, 2026–2034

3.77%Europe Molecular Diagnostics Market Report Summary

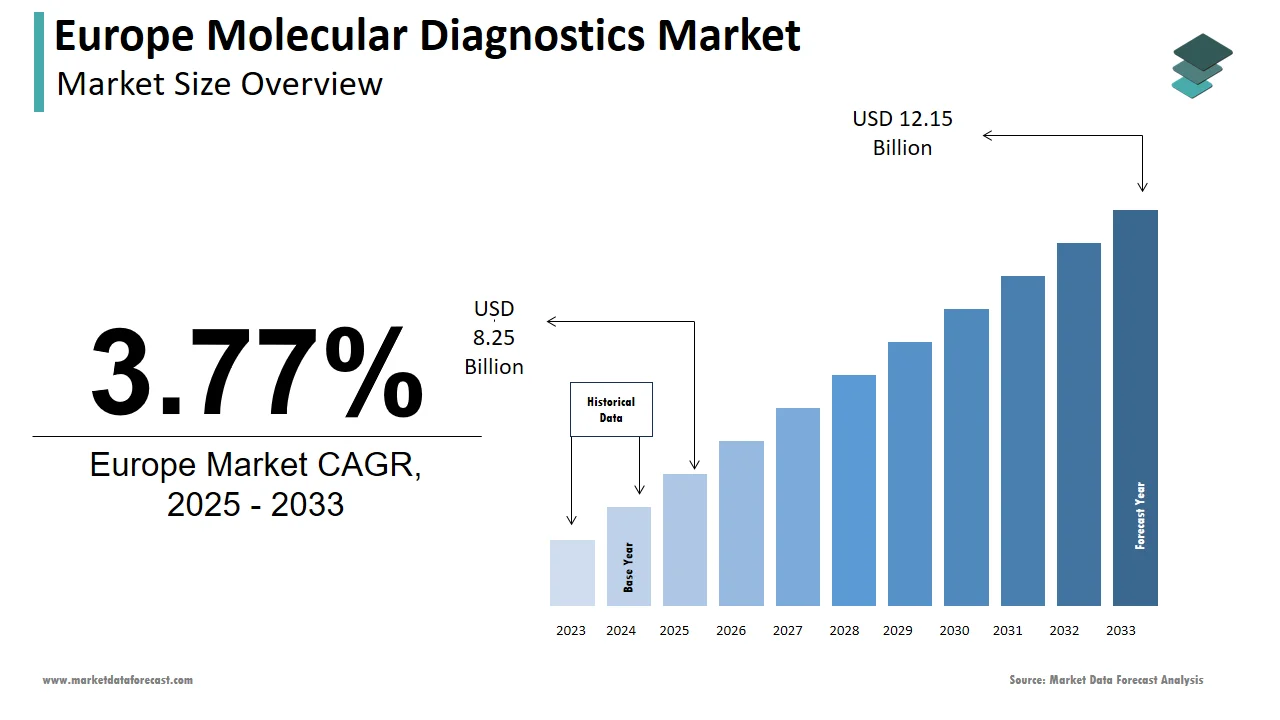

The Europe molecular diagnostics market was valued at USD 8.25 billion in 2025 and is expected to reach USD 11.51 billion by 2034, exhibiting a CAGR of 3.77% from 2026 to 2034. Growth is driven by increasing use of genomic-based testing in oncology care pathways, expansion of infectious disease surveillance programs, and deeper integration of molecular profiling into national screening, reimbursement, and treatment frameworks.

Key Market Trends

- Rising adoption of companion diagnostics is aligned with targeted cancer therapy approvals.

- Expansion of syndromic multiplex testing in emergency and ICU environments to support same-visit decisions.

- Increasing incorporation of non-invasive prenatal testing into publicly funded maternal care systems.

- Surge in instrument automation to reduce turnaround time and support high-volume testing.

- Growing transition toward decentralised and point-of-care PCR testing in hospitals.

Segmental Insights

- Based on product, reagents held the largest share of the Europe molecular diagnostics market in 2024, supported by continuous test utilisation across oncology, virology, and respiratory infection workflows. Consumable-based recurring demand continues to sustain segment dominance.

- Based on test location, point-of-care accounted for the largest market share in 2024 as rapid near-patient testing improves treatment decision speed, reduces hospitalization burden, and supports antimicrobial stewardship initiatives.

- Based on technology, PCR remained the most widely adopted molecular testing approach in 2024 due to high sensitivity, rapid results, standardized clinical usage, and broad platform availability across public laboratories.

- Based on application, oncology dominated in 2024, driven by mandated biomarker profiling and growing use of genomic information in treatment selection and therapy sequencing across leading cancer centres.

Regional Insights

The Europe molecular diagnostics market reflects strong standardization of test adoption, clinically governed reimbursement structures, and structured diagnostic integration into patient pathways.

- Germany led the regional market in 2024, supported by its large hospital lab network, national reimbursement programs for genomic testing, and strong reference lab capacity.

- The United Kingdom ranked among top markets, driven by centralized genomic medicine infrastructure within the NHS and nationwide diagnostic hub deployment.

- France also held a notable share, supported by mandated biomarker testing, national sequencing initiatives, and structured public health laboratory networks.

- Italy continues to expand molecular capabilities, backed by diagnostic modernization programs and regional oncology-based initiatives.

- The Netherlands remains a high-efficiency market, with strong uptake of NIPT, structured lab integration, and early adoption of digital workflows.

Competitive Landscape

The market features strong participation from multinational diagnostic manufacturers, supported by validated testing portfolios, regulatory readiness, and established hospital partnerships. Leadership continues to be driven by companies offering broad assay menus, automated workflows, and companion diagnostic alignment across oncology, infectious diseases, and genomic medicine. Increased investment in CE-IVD-certified panels and decentralized sample testing platforms is shaping competitive momentum.

Major companies operating in the Europe molecular diagnostics market include: BD; bioMérieux; Bio-Rad Laboratories, Inc.; Abbott; Agilent Technologies, Inc.; Danaher; Hologic Inc.; Illumina, Inc.; Grifols; Roche Diagnostics; Thermo Fisher Scientific Inc.; Siemens Healthineers AG; and Sysmex Corporation.

Europe Molecular Diagnostics Market Size

The molecular diagnostics market size in Europe was valued at USD 8.25 billion in 2025. The European market is estimated to be worth USD 11.51 billion by 2034 from USD 8.56 billion in 2026, growing at a CAGR of 3.77% from 2026 to 2034.

Molecular diagnostics includes laboratory and point-of-care technologies that analyse nucleic acids such as DNA and RNA to detect genetic variations, infectious agents, and biomarkers for disease diagnosis, prognosis, and therapeutic guidance. Unlike conventional serology or culture methods, molecular diagnostics offer high sensitivity, rapid turnaround, and the ability to identify pathogens or mutations at the genomic level. Europe’s adoption is shaped by advanced healthcare infrastructure, a strong emphasis on precision medicine, and coordinated public health surveillance. Most EU member states had integrated real‑time PCR testing into national infectious disease monitoring by 2023. According to Eurostat, a high density of clinical laboratories across the EU in 2023 is enabling widespread test accessibility. The European Medicines Agency approved dozens of companion diagnostic assays between 2020 and 2023 to support targeted oncology therapies, which reflects deep regulatory alignment between diagnostics and therapeutics. This ecosystem of public health readiness, clinical integration, and regulatory sophistication positions molecular diagnostics as a cornerstone of Europe’s modern healthcare strategy.

MARKET DRIVERS

Integration of Molecular Testing into National Cancer Screening Programs Accelerates Adoption

The growing incidence of chronic diseases across Europe is one of the key factors propelling the growth of the European molecular diagnostics market. Countries such as France, Germany, and the Netherlands now mandate molecular profiling of tumor tissue to guide therapy selection for non‑small cell lung cancer, colorectal cancer, and melanoma. According to the European Commission’s 2023 State of Health in the EU report, 22 member states have updated their national cancer plans to include routine EGFR, ALK, and KRAS testing as standard of care. As per the Federal Joint Committee (G‑BA), statutory health insurers in Germany reimburse next‑generation sequencing (NGS) panels for advanced cancers, with coverage formalized in 2024. Similarly, France’s National Cancer Institute has mandated reflex testing for HER2, BRAF, and MSI status across public hospitals to ensure equitable access. These policies not only increase test volumes but also create stable reimbursement frameworks that incentivize laboratory investment in sequencing platforms. As the EU’s Beating Cancer Plan targets early detection and personalized treatment, molecular diagnostics are transitioning from optional tools to essential clinical infrastructure.

Persistent Threat of Antimicrobial Resistance Drives Demand for Rapid Pathogen Identification

The rapidly growing antimicrobial resistance crisis in Europe is another key driver propelling the growth of the molecular diagnostics market. According to the European Centre for Disease Prevention and Control (ECDC), antimicrobial resistance causes more than 35,000 deaths annually in the EU/EEA. As per the European Commission’s Action Plan on Antimicrobial Resistance, tertiary hospitals are required to strengthen infection prevention and implement rapid molecular testing as part of stewardship strategies. According to the European Society of Clinical Microbiology and Infectious Diseases (ESCMID), multiplex PCR panels are increasingly used in European hospitals to detect resistance markers directly from blood cultures, which is reducing time to targeted therapy from 72 hours to under 6 hours. This speed not only improves patient outcomes but also curbs unnecessary broad‑spectrum antibiotic use, which is a key pillar of EU stewardship policy. Consequently, molecular diagnostics have become indispensable tools in Europe’s strategy to contain resistance and preserve antibiotic efficacy.

MARKET RESTRAINTS

Complex and Fragmented Regulatory Approval Pathways Delay Test Commercialization

The inconsistent implementation of the In Vitro Diagnostic Regulation (IVDR) 2017/746 across member states is primarily restraining the molecular diagnostics market growth in Europe. According to MedTech Europe’s 2024 IVDR survey, notified body bottlenecks and divergent interpretations of performance requirements have extended approval timelines, with average certification taking 14–18 months. As per the European Diagnostics Manufacturers Association, over 60% of small and mid‑sized diagnostic firms reported delayed product launches in 2023 due to regulatory backlogs. Countries such as Italy and Spain impose additional verification steps beyond EU requirements, further fragmenting access. This regulatory friction disproportionately impacts innovative tests for rare diseases or emerging pathogens, which discourages investment in niche but clinically vital diagnostics and slows Europe’s response to evolving health threats.

High Cost of Advanced Platforms Limits Access in Public and Rural Healthcare Settings

The supply chain disruptions and fiscal constraints are hampering the European molecular diagnostics market growth. According to the European Federation of Laboratory Medicine (EFLM), advanced sequencing and PCR platforms can cost over €300,000 per instrument, with annual maintenance exceeding €150,000. As per WHO Europe’s Global Health Expenditure Database, diagnostic spending per capita in Romania and Bulgaria remains below €20 annually, compared to over €90 in Germany and Sweden. According to the European Society of Pathology, only 38% of pathology departments in Greece and Portugal have on‑site molecular capabilities for solid tumor profiling. This inequity not only delays treatment but also undermines the EU’s goal of universal access to precision medicine and creates a two‑tier diagnostic landscape.

MARKET OPPORTUNITIES

Expansion of Non-Invasive Prenatal Testing into Public Prenatal Care Systems

The progressive integration of non-invasive prenatal testing into state-funded maternity services is a major opportunity for the molecular diagnostics market in Europe. According to the Amsterdam UMC TRIDENT study, NIPT became a structural part of the Dutch national prenatal screening program in 2023, freely available to all pregnant women. As per RIVM, NIPT was rolled out nationally in the Netherlands from April 2023. According to the French National Authority for Health, France expanded its NIPT program in 2023 to include microdeletion screening and cover hundreds of thousands of pregnancies annually. Sweden’s guidelines also recommend NIPT as first‑tier screening for trisomies 21, 18, and 13nfog.org. According to the studies of the European Commission’s Joint Research Centre and health economics, NIPT reduces costs per accurate diagnosis compared to combined first‑trimester screening. This shift reduces procedure‑related miscarriages and generates sustainable volume for molecular platforms across public healthcare systems.

Adoption of Syndromic Multiplex Panels in Emergency and Critical Care Settings

The development of syndromic multiplex panels offers another promising avenue for the European molecular diagnostics market expansion. According to the European Society of Intensive Care Medicine (ESICM), syndromic panels are increasingly adopted in trauma and emergency medicine to accelerate diagnosis. As per multicenter evaluations, the BioFire Blood Culture Identification panel reduced pathogen detection time from 48 hours to 1.5 hours in European hospitals, including Charité Berlin. According to the ECDC, syndromic testing pilots in Italy and Spain reduced unnecessary antibiotic prescriptions by nearly 30%. This clinical utility, coupled with favorable health technology assessments, is driving procurement in acute care settings where speed directly impacts survival and resource utilization.

MARKET CHALLENGES

Shortage of Skilled Personnel to Operate and Interpret Complex Molecular Assays

The absence of adequately trained personnel is primarily challenging the European molecular diagnostics market. According to the European Federation of Clinical Chemistry and Laboratory Medicine (EFLM), over 40% of EU countries report deficits of molecular biologists and bioinformaticians. As per the European Society of Pathology, 68% of pathology residency programs in Southern Europe lack dedicated molecular diagnostics training modules. According to the WHO Europe’s Bucharest Declaration 2023, workforce shortages are acute in Romania and Bulgaria, where district hospitals lack in‑house molecular staff. This gap leads to underutilization of installed equipment, extended turnaround times, and reliance on external reference labs. Without targeted education and workforce development, this bottleneck will constrain the full realization of precision medicine ambitions.

Data Management and Interoperability Barriers in Genomic Medicine Implementation

The growing instability due to fragmented data governance is also challenging the expansion of the European molecular diagnostics market. According to the European Health Data Space (EHDS) proposal, fewer than 30% of EU hospitals currently have interoperable systems capable of incorporating genomic results into clinical decision support tools. As per the European Journal of Public Health, inconsistent data formats and a lack of common ontologies hinder cross‑institutional genomic data sharing across Europe. According to the EORTC SPECTAcolor platform, centralized molecular screening is required to streamline patient inclusion in pan‑European clinical trials. Furthermore, GDPR creates uncertainty around cross‑border genomic data transfer, which is impeding large‑scale collaborations. Until Europe establishes unified data governance frameworks, the clinical value of molecular diagnostics will remain partially unrealized.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Product, Test Location, Technology, Application, and Region. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, Asia Pacific, Latin America, Middle East & Africa |

| Market Leaders Profiled | BD, bioMérieux, Bio-Rad Laboratories, Inc., Abbott, Agilent Technologies, Inc., Danaher, Hologic Inc. (Gen Probe), Illumina, Inc., Grifols, Roche Diagnostics, Thermo Fisher Scientific Inc., Siemens Healthineers AG, Sysmex Corporation, and Others. |

SEGMENTAL ANALYSIS

By Product Insights

The reagents segment led the market and accounted for 62.1% of the Europe molecular diagnostics market share in 2024, owing to the recurring nature of reagent consumption compared to one‑time instrument purchases. According to the European Centre for Disease Prevention and Control, reference laboratories in major EU countries routinely run multiple syndromic panels weekly for respiratory, gastrointestinal, and bloodstream infections, which require calibrated primers, probes, enzymes, and master mixes. As per the European Commission, member states procured substantial volumes of molecular reagent units in 2023 under EU pathogen monitoring initiatives to ensure cross‑country data comparability. According to EU antimicrobial resistance surveillance frameworks, standardized reagent kits are mandated to support stewardship and reliable reporting. This segment is expected to sustain dominance over the forecast period as laboratories expand multiplex menus and maintain quality‑controlled consumable inventories.

The instruments segment is anticipated to grow at a promising CAGR of 8.1% over the forecast period in the European market. According to the German Federal Ministry of Health, national programs for diagnostic digitization have directed significant funding to molecular instruments, including high‑throughput NGS and digital PCR platforms. As per the UK National Health Service, genomic medicine centers are scaling instrument capacity to support large projects and routine oncology testing. According to the French High Authority for Health, reimbursement approvals for comprehensive genomic profiling in oncology have accelerated instrument adoption. This segment is expected to expand steadily over the forecast period as precision medicine funding and clinical demand drive the modernization of molecular laboratories.

By Test Location Insights

The point‑of‑care segment captured 78.7% of the Europe molecular diagnostics market share in 2024. The dominance of the point‑of‑care segment in this European market is driven by rapid near‑patient platforms in hospitals and urgent care that deliver pathogen identification in under an hour to guide same‑visit therapy. According to the European Antimicrobial Resistance Surveillance Network, hospitals implementing point‑of‑care molecular testing reported meaningful reductions in unnecessary antibiotic prescriptions. As per the European Society of Clinical Microbiology and Infectious Diseases, systems such as GeneXpert and FilmArray are widely used for sepsis and meningitis workups in emergency departments. According to EU cross‑border health threat regulations, hospitals must maintain on‑site rapid molecular capacity for priority biothreat agents, embedding point‑of‑care workflows. This segment is expected to remain dominant over the forecast period as stewardship imperatives and emergency readiness sustain utilization.

The self‑test segment is expected to grow at the fastest CAGR of 14.3% over the forecast period in the European market. According to the European Commission, CE‑marked self‑collected molecular tests have been authorized in select categories, enabling consumers to submit samples to certified labs with app‑based reporting. As per the Swedish Public Health Agency, national programs distributing at‑home STI testing have increased early detection and broadened access. According to the European Society of Human Genetics, digital counseling and connected laboratory workflows improve interpretation and follow‑up for direct‑to‑consumer genetic testing. This segment is expected to expand rapidly over the forecast period as regulatory acceptance, reimbursement pilots, and telehealth integration mainstream self‑administered molecular testing.

By Technology Insights

The Polymerase chain reaction (PCR) technology segment holds 45.3% of the European molecular diagnostics market share in 2024. This prominence is due to PCR's unparalleled sensitivity and specificity in detecting nucleic acids, making it indispensable for applications like infectious disease testing. For instance, PCR-based assays were the backbone of Europe's COVID-19 response, with over 700 million tests conducted since the pandemic's onset. Additionally, advancements such as real-time PCR have enhanced its utility by enabling simultaneous amplification and detection, reducing processing times by up to 60%. A study by a European clinical diagnostics association has shown that real-time PCR reduces false negatives by 20% by ensuring reliable results. The widespread availability of PCR platforms is coupled with their adaptability across various applications, which escalates their dominance.

The isothermal nucleic acid amplification technology (INAAT) segment is swiftly emerging with an estimated CAGR of 13.5% in the foreseen years. This growth is driven by INAAT's ability to perform nucleic acid amplification at a constant temperature, simplifying the diagnostic process and reducing energy consumption. For example, loop-mediated isothermal amplification (LAMP) assays are increasingly used for tuberculosis detection, with a reported sensitivity of 95%. A study by a European biotech consortium notes that INAAT-based platforms reduce operational costs by 25% compared to traditional PCR systems by making them attractive for resource-limited settings. Furthermore, the development of portable INAAT devices has expanded their application in point-of-care testing by addressing the growing demand for rapid diagnostics.

By Application Insights

The oncology segment was the largest with 35.4% of the European molecular diagnostics market share of 35.4% in 2024, with the increasing incidence of cancer across Europe, with over 4 million new cases diagnosed annually. Molecular diagnostics play a pivotal role in oncology by identifying genetic mutations that guide personalized treatment plans. For instance, HER2 testing for breast cancer has become standard practice, with over 200,000 tests conducted annually in Europe. Additionally, the integration of liquid biopsy technologies has revolutionized cancer monitoring, enabling non-invasive detection of tumor DNA. According to the European Oncology Association, liquid biopsies improve early detection rates by 30% by enhancing survival outcomes. The growing emphasis on precision medicine further solidifies oncology's dominance in the market.

The infectious disease testing segment is expected to hit a prominent CAGR of 12.4% during the forecast period. This growth is fueled by the rising prevalence of infectious diseases due to globalization and climate change. For example, molecular diagnostics have become critical in managing antibiotic-resistant infections, which are projected to cause 300,000 deaths annually in Europe by 2050. A study by a European infectious disease research group notes that rapid molecular tests reduce diagnostic times by 50% by enabling timely interventions. Additionally, the emergence of multiplex assays, capable of detecting multiple pathogens simultaneously that has enhanced diagnostic efficiency. These innovations, combined with increasing awareness of preventive healthcare, position infectious disease testing as a rapidly expanding segment in the molecular diagnostics market.

COUNTRY LEVEL ANALYSIS

Germany Molecular Diagnostics Market Analysis

Germany dominated the European molecular diagnostics market in 2024 by holding 22% of the regional share owing to its dense network of university hospitals, extensive reference laboratories, statutory health insurance coverage, and strong public investment in advanced diagnostics. According to the Robert Koch Institute, Germany operates over 450 high‑complexity molecular labs certified under national medical guidelines. As per the Federal Ministry of Health, the Hospital Future Act allocated €180 million in 2023 specifically for molecular diagnostic upgrades, including next‑generation sequencing and automated extraction systems. According to the Federal Joint Committee, reimbursement for over 45 oncology biomarker tests, including PD‑L1, BRCA, and MSI. Integration of molecular data into the German Cancer Registry further enables real‑world evidence generation. Germany is expected to remain Europe’s diagnostic innovation hub in the coming years.

United Kingdom Molecular Diagnostics Market Analysis

The United Kingdom held a substantial share of the European molecular diagnostics market in 2024. The growth of the UK is supported by centralized genomic medicine infrastructure, rapid adoption of new assays, and strong policy frameworks for equitable access. According to NHS England, the NHS Genomic Medicine Service performs over 500,000 molecular diagnostic tests annually, supporting rare disease and cancer care. As per Genomics England, the 100,000 Genomes Project laid the foundation for routine whole‑exome sequencing, with results integrated into electronic health records. In 2023, the NHS expanded its Molecular Diagnostic Hub network to 12 sites across England. NICE reported that over 30 new molecular assays were approved in 2023, which is enabling swift reimbursement. The UK Biobank remains Europe’s largest public biobank, linking genomic and clinical data for test validation. The UK is expected to remain at the forefront of diagnostic implementation in the coming years.

France Molecular Diagnostics Market Analysis

France captured a notable position in the European molecular diagnostics market in 2024. The strong national coordination, mandatory biomarker testing, and integration of diagnostics into public health pathways are propelling the growth of the French market. According to the Plan France Médecine Génomique 2025, 13 regional genomic platforms were established to serve public hospitals nationwide. As per the French National Cancer Institute, over 92% of non‑small cell lung cancer patients received EGFR, ALK, and ROS1 testing in 2023. The National Reference Centre for Respiratory Viruses conducts over 2 million molecular tests annually, distributing standardized reagent kits to more than 1,200 labs. France also pioneered rapid point‑of‑care molecular deployment in nursing homes under the 2022 pandemic preparedness law. France is expected to sustain its relevance and efficiency in diagnostics in the coming years.

Italy Molecular Diagnostics Market Analysis

Italy maintained a significant role in the European molecular diagnostics market in 2024. Growth is driven by regional innovation, rising oncology demand, and national investment in laboratory modernization. According to the Italian Ministry of Health, the National Recovery and Resilience Plan allocated €450 million in 2023 to modernize diagnostic laboratories, with €120 million dedicated to molecular platforms such as digital PCR and NGS. Lombardy and Emilia‑Romagna operate centralized molecular hubs serving multiple provinces, reducing turnaround times to under 48 hours for critical tests. As per the National Cancer Plan, biomarker testing is mandated for colorectal and lung cancers, with coverage expanded to include HER2 in gastric cancer in 2023. Italy also hosts one of Europe’s largest hospital‑based point‑of‑care molecular networks for sepsis and meningitis. Italy is expected to sustain robust growth in molecular diagnostics in the coming years.

Netherlands Molecular Diagnostics Market Analysis

The Netherlands remained an important participant in the European molecular diagnostics market in 2024. Growth is supported by integrated national laboratory networks, strong reimbursement policies, and leadership in self‑testing innovation. According to the Netherlands Comprehensive Cancer Organisation, the Dutch Pathology Registry links molecular test results to treatment outcomes for over 95% of cancer patients. As per the Dutch National Institute for Public Health and the Environment, the country operates a national laboratory network for infectious disease molecular testing, ensuring uniform protocols and real‑time data sharing with the ECDC. The national reimbursement system covers non‑invasive prenatal testing for all pregnant women and expanded carrier screening for 50 genetic conditions. The Netherlands also leads in self‑testing innovation, with reimbursed at‑home STI molecular kits distributed via pharmacies and online portals. The Netherlands is expected to remain a model for sustainable diagnostic deployment in the coming years.

COMPETITIVE LANDSCAPE

The Europe molecular diagnostics market features a highly sophisticated competitive landscape where global leaders coexist with agile regional innovators. Competition is increasingly defined by clinical validation, regulatory readiness, and integration into national healthcare frameworks rather than product novelty alone. Large players like Roche and Thermo Fisher leverage scale and end-to-end solutions to dominate high complexity testing in oncology and genomics, while European specialists such as BioMérieux excel in rapid infectious disease syndromic panels. The implementation of the In Vitro Diagnostic Regulation has raised entry barriers favoring firms with robust quality management systems and clinical evidence generation capabilities. Public procurement policies in countries like Germany and the UK further intensify competition by mandating cost-effectiveness and interoperability. Meanwhile, the rise of laboratory-developed tests and academic spin-offs introduces innovation but faces scalability challenges. This environment rewards companies that combine scientific rigor, regulatory agility, and deep alignment with Europe’s public health and precision medicine vision.

KEY MARKET PLAYERS

The leading companies operating in the Europe application lifecycle management market include:

- BD

- bioMérieux

- Bio-Rad Laboratories, Inc.

- Abbott

- Agilent Technologies, Inc.

- Danaher

- Hologic Inc. (Gen Probe)

- Illumina, Inc.

- Grifols

- Roche Diagnostics

- Thermo Fisher Scientific Inc

- Siemens Healthineers AG

- Sysmex Corporation

TOP PLAYERS IN THE MARKET

- Roche Diagnostics maintains a prominent presence in the Europe molecular diagnostics market through its comprehensive portfolio of automated platforms, including the cobas 6800 and 8800 systems used for infectious disease, oncology, and virology testing. Headquartered in Switzerland, the company supplies reagents and instruments to national reference laboratories and hospital networks across Germany, France, and the UK. In 2023, Roche expanded its pan-European companion diagnostic portfolio with CE-marked assays for EGFR exon 20 insertions and NTRK fusions in non-small cell lung cancer. It also integrated its molecular data into the NAVIFY Decision Support portfolio, enabling seamless linkage with electronic health records. These actions reinforce Roche’s leadership in precision medicine and strengthen its alignment with Europe’s oncology and public health strategies.

- Thermo Fisher Scientific Inc. plays a strategic role in the Europe molecular diagnostics market via its Applied Biosystems and Ion Torrent platforms, which support both clinical and research-grade genomic testing. The company serves national genomic medicine initiatives in the UK, Netherlands, and Sweden with next-generation sequencing solutions and validated oncology panels. In early 2024, Thermo Fisher launched the Oncomine Precision Assay CE-marked for over 50 solid tumor biomarkers, including emerging targets like RET and MET. It also established a dedicated IVD reagent manufacturing line in Erembodegem, Belgium, to ensure EU supply chain resilience under the In Vitro Diagnostic Regulation. These moves enhance its ability to meet Europe’s growing demand for high-throughput comprehensive genomic profiling in routine diagnostics.

- BioMérieux SA is a key European player specializing in syndromic molecular diagnostics for infectious diseases through its BioFire FilmArray and ePlex platforms. Based in France, the company supplies rapid multiplex panels for respiratory, gastrointestinal, and bloodstream infections to over 2000 hospitals across the continent. In 2023, BioMérieux received CE marking for its FilmArray Torch system, featuring cloud-connected analytics and expanded antimicrobial resistance detection. It also partnered with the European Antimicrobial Resistance Surveillance Network to standardize resistance gene reporting across member states. These initiatives position BioMérieux at the intersection of rapid diagnostics, antimicrobial stewardship, and digital health integration in Europe’s acute care settings.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Key players in the Europe molecular diagnostics market are prioritizing regulatory compliance with the In Vitro Diagnostic Regulation by securing CE IVD certifications for comprehensive genomic and infectious disease assays. Companies are localizing reagent and instrument manufacturing within the EU to mitigate supply chain risks and ensure timely notified body audits. Strategic collaborations with national health systems and reference laboratories are being established to embed proprietary platforms into public screening and oncology pathways. Investment in digital health integration, such as cloud-based analytics and EHR connectivity, is enhancing clinical utility and data interoperability. Additionally, firms are expanding syndromic and companion diagnostic menus to align with antimicrobial resistance strategies and precision oncology mandates. These approaches collectively address Europe’s dual priorities of diagnostic excellence and healthcare system sustainability.

EUROPE MOLECULAR DIAGNOSTICS MARKET NEWS

- In January 2024, Roche Diagnostics partnered with a European hospital network to integrate AI-driven analytics into diagnostic systems, improving result accuracy by 30%.

- In March 2024, Thermo Fisher Scientific launched a portable molecular testing device designed for point-of-care use, targeting remote areas.

- In June 2023, Thermo Fisher Scientific acquired a European biotech firm specializing in liquid biopsy technologies, expanding its oncology diagnostics portfolio.

- In May 2024, Agilent Technologies introduced a novel pharmacogenomic assay to optimize drug prescriptions based on genetic profiles.

- In August 2023, QIAGEN collaborated with Italian authorities to establish a nationwide campaign promoting early detection of infectious diseases through molecular testing.

MARKET SEGMENTATION

This Europe molecular diagnostics market research report is segmented and sub-segmented into the following categories. Top of Form

By Product

- Instruments

- Regards

- Others

By Test Location

- Point of care

- Self-test or OTC

- Central laboratories

By Technology

- Polymerase chain reaction (PCR)

- PCR, by Procedure

- Nucleic Acid Extraction

- Others

- PCR, by Type

- Multiplex PCR

- Other PCR

- PCR, by Product

- Instruments

- Reagents

- Others

- In Situ Hybridization (ISH)

- Instruments

- Reagents

- Others

- Isothermal Nucleic Acid Amplification Technology (INAAT)

- Instruments

- Reagents

- Others

- Chips and Microarrays

- Instruments

- Reagents

- Others

- Mass Spectrometry

- Instruments

- Reagents

- Others

- Transcription Mediated Amplification (TMA)

- Instruments

- Reagents

- Others

- Others

- Instruments

- Reagents

- Others

- PCR, by Procedure

By Application

- Oncology

- Breast Cancer

- Prostate Cancer

- Colorectal Cancer

- Cervical

- Kidney

- Liver

- Blood

- Lung

- Other

- Pharmacogenomics

- Infectious disease

- MRSA

- Clostridium difficile

- Vancomycin-resistant enterococci

- Carbapenem-resistant bacteria testing

- Flu

- Respiratory syncytial virus (RSV)

- Candida

- Tuberculosis and drug-resistant TB

- Meningitis

- Gastrointestinal panel testing

- Chlamydia

- Gonorrhea

- HIV

- Hepatitis C

- Hepatitis B

- Other Infectious Diseases

- Genetic testing

- Newborn screening

- Predictive and presymptomatic testing

- Others

- Neurological disease

- Cardiovascular disease

- Microbiology

- Others

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

1. What is the europe molecular diagnostics market?

The europe molecular diagnostics market refers to molecular-level testing technologies (PCR, sequencing, kits, instruments) used in labs and hospitals for disease detection, genetic tests, infectious diseases and oncology.

2. How large is the europe molecular diagnostics market currently?

The europe molecular diagnostics market was valued at about USD 7.66 billion in 2024.

3. What is the projected value of the europe molecular diagnostics market?

The europe molecular diagnostics market is forecast to reach approximately USD 12.15 billion by 2033.

4. What is the expected growth rate (CAGR) for the europe molecular diagnostics market?

The europe molecular diagnostics market is projected to grow at a CAGR of roughly 3.77% from 2025 to 2033.

5. Which technologies dominate the europe molecular diagnostics market?

The europe molecular diagnostics market is led by PCR-based systems, next-gen sequencing (NGS), DNA/RNA extraction kits, and other molecular assay instruments.

6. What applications drive the europe molecular diagnostics market demand?

Key applications in the europe molecular diagnostics market include infectious disease diagnostics, genetic testing, oncology biomarker testing, and personalized medicine profiling.

7. Who are the primary users in the europe molecular diagnostics market?

The europe molecular diagnostics market serves hospitals, diagnostic laboratories, oncology clinics, genetic testing centers, and research institutions.

8. Which countries lead the europe molecular diagnostics market?

Germany, France, UK, Italy, and other Western European nations lead the europe molecular diagnostics market thanks to strong health infrastructure and high testing adoption.

9. What factors drive growth in the europe molecular diagnostics market?

Rising chronic disease prevalence, demand for early detection, personalized medicine, infectious disease screening, and innovations in molecular testing boost the europe molecular diagnostics market.

10. What challenges does the europe molecular diagnostics market face?

The europe molecular diagnostics market faces challenges including high instrumentation costs, need for skilled staff, regulatory hurdles, and variability in reimbursement across regions.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com