Europe Nematicides Market Size, Share, Growth, Trends, and Forecasts Report, Segmented By Type, Application, Form, Mode of Application, And By Region (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic and Rest of Europe), Industry Analysis From (2026 to 2034)

Europe Nematicides Market Size

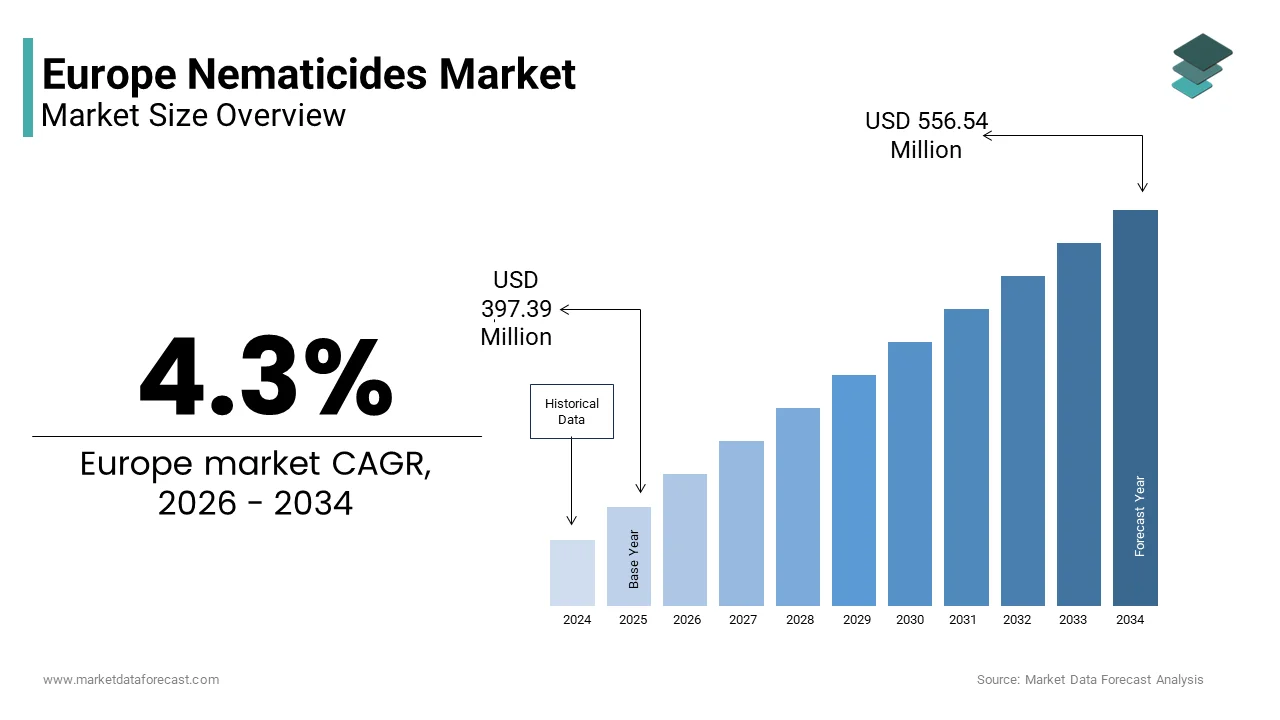

The Europe nematicides market size will reach USD 381.01 million in 2025 and is anticipated to reach USD 397.39 million in 2026 to USD 556.54 million by 2034, growing at a CAGR of 4.3% during the forecast period from 2026 to 2034.

Current Introduction of The Europe Nematicides Market

Nematicides refer to chemical or biological agents applied to manage plant parasitic nematodes, microscopic soil-dwelling worms that impair root function and reduce crop yields across key agricultural sectors. These pests are particularly destructive in high-value crops such as potatoes, sugar beets, vegetables, and vineyards, where root integrity directly influences marketable output. Plant-parasitic nematodes significantly impact European agriculture, with root-knot and potato cyst species causing substantial economic losses in farmland across the EU. In areas with poor management or without treatment, nematode infestations significantly diminish potato production, particularly in regions across Eastern and Southern Europe. The ongoing reduction of authorized chemical pesticides in the EU, following the phase-out of traditional hazardous broad-spectrum chemicals, is driving agricultural reliance on targeted bio-nematicides and integrated, soil-focused management practices. Consequently, the Europe nematicides market is evolving from reliance on conventional chemistry toward precision biocontrol and resistance management aligned with the Farm to Fork Strategy’s goal of reducing synthetic pesticide use by 2030.

MARKET DRIVERS

Escalating Yield Losses in High-Value Crops Due to Nematode Infestations

Plant parasitic nematodes pose a severe and growing threat to the region’s specialty crop production, which acts as a major accelerator of the Europe nematicides market. Documented yield losses are compelling farmers to adopt nematicidal interventions. Potato cyst nematodes are widely distributed across several key potato-producing nations where the crop serves as a vital resource for both local consumption and international trade. Unmanaged infestations of specific nematode species are observed to significantly lower tuber yields, which affects the stability of agricultural supply chains and producer revenue. Sugar beet cultivation in various regions experiences consistent yield reductions linked to soil-borne pests. Economic factors have led to changes in traditional planting cycles, which appear to have increased the prevalence of nematode-related issues in certain crops. In viticulture, root-knot nematodes are associated with a gradual weakening of vines, which tends to shorten the overall duration of a vineyard's productive life. These quantifiable agronomic impacts create persistent demand for effective nematicides, particularly in regions where crop value justifies input investment and where regulatory pathways permit targeted chemical or biological solutions.

Regulatory Phase Out of Legacy Nematicides and Demand for Safer Alternatives

The European Union’s stringent pesticide re-evaluation process has systematically withdrawn high-risk nematicides, accelerating the search for compliant alternatives, which fuels the expansion of the Europe nematicides market. As per sources, manyconventional nematicide active substances have been revoked since 20,15 including oxamyl and fosthiaz,, ate due to concerns over groundwater contamination and toxicity to non-target organisms. This regulatory attrition has left critical gaps in nematode management, especially in intensive horticultural systems that previously relied on soil fumigants. The resulting void has driven adoption of lower risk chemistries such as fluensulfone and biological agents like Purpureocillium lilacinum, which meet the criteria under Regulation EC No 1107 2009 for approval. National strategies within regional directives are increasingly promoting the replacement of conventional products, with certain nations providing financial support for testing biological alternatives. The approval process for innovative, gene-based control agents is evolving, reflecting a policy trend toward supporting newer, technologically advanced solutions. Governmental frameworks are acting to encourage the adoption of alternative, sustainable approaches to pest management. Regulatory approaches are shifting to accommodate and facilitate the introduction of novel biological products. These regulatory dynamics not only constrain legacy options but also actively reshape the market toward sustainable and precision nematode control tools.

MARKET RESTRAINTS

Stringent EU Restrictions on Soil Fumigants and Synthetic Active Ingredients

The European Union’s precautionary approach toward persistent and mobile chemical substances, particularly those applied to soil, restrains the growth of the Europe nematicides market. Stringent environmental standards concerning groundwater safety and ecological impact have reduced the available options for effective nematode control. A substantial number of potential new nematicides do not gain approval due to identified risks to aquatic life and soil organisms. The elimination of previously used, broad-spectrum fumigants has decreased the methods for managing pests in high-value crops. Even recently developed chemical solutions are subject to usage restrictions in areas with sensitive water sources. The reclassification of certain existing substances has created uncertainty about their future availability. These regulatory hurdles substantially reduce the arsenal available to farmers and discourage investment in novel synthetic nematicides due to high development costs and uncertain approval timelines.

Limited Efficacy and Field Performance of Bio-Nematicides Under Cool Climates

Biological nematicides, often promoted as sustainable alternatives, struggle with inconsistent performance in the region’s temperate and cool climate zones, which dominate agricultural production. This poses a major obstacle to the Europe nematicides market expansion. Biological control agents derived from fungi and bacteria demonstrate lower efficacy in managing root-knot nematodes when compared to traditional chemical treatments under similar environments. The effectiveness of these microbial solutions is closely linked to soil temperature, as their activity levels tend to fluctuate based on thermal conditions. In certain European regions, soil temperatures during the early stages of the planting season may not reach the levels necessary for optimal performance of biological agents. The use of bio-nematicides is frequently concentrated in managed environments where climate variables are regulated, which may indicate challenges in applying these methods to broad-scale outdoor farming. Environmental variability presents a significant factor in the performance gap between synthetic and biological pest management strategies. Furthermore, shelf life and formulation stability issues increase logistical complexity and cost. The transition to biologicals is constrained by the limited field reliability of bio-nematicides across Europe's diverse regions.

MARKET OPPORTUNITIES

Advancement of RNAInterference-Basedd and Species-Specific Nematicides

The emergence of RNA interference technology offers a potential opportunity in the Europe nematicides market. It enables highly targeted nematode control with minimal ecological impact. Regulatory bodies in Europe have introduced a specialized authorization pathway for innovative, precise biological products, resulting in the approval of a new RNA interference (RNAi) tool designed to control specific parasitic nematodes. This approach uses genetic silencing to target particular pest species while aiming to minimize effects on beneficial organisms in the soil ecosystem. Evidence suggests that the application of this technology can significantly reduce the prevalence of potato cyst nematodes in agricultural trials. Observations indicate that this method leaves no detectable traces of the treatment within the harvested tubers or the surrounding groundwater. The technology aligns with the Farm to Fork Strategy’s emphasis on non-chemical alternatives and has attracted co-investment from the EU Horizon Europe program. Companies are developing delivery systems using clay nanocarriers to protect RNA molecules in cool soils. This precision paradigm shift promises to overcome the efficacy and safety limitations of both chemical and traditional biological nematicides, opening a new frontier in sustainable nematode management.

Integration of Nematicides into Soil Health and Regenerative Agriculture Frameworks

Nematicides are increasingly being repositioned not as standalone inputs but as components of holistic soil health programs that combine biological chemistry and agronomic practices, which is likely to propel the expansion of the Europe nematicides market. Agricultural initiatives across Europe are increasingly exploring integrated nematode management systems that combine biological agents, cover cropping, biofumigation, and resistant cultivars. In specific sugar beet regions, farmers employing these diversified, integrated approaches are observing reduced nematode pressure compared to traditional monoculture methods. Governmental support for nematicide usage is becoming more conditional, often requiring that these applications be integrated into multi-year crop rotation and soil organic matter improvement plans. Agricultural advisory services are shifting toward recommending chemical intervention only as a last resort within broader, regenerative farming protocols. This systems-based approach enhances long term efficacy, reduces chemical dependependenced aligns nematicide use with the EU agthe roecological transition goals,lgoalsr eatingvalue-addedded niche for products that support integrated soil stewardship rather than isolated pest suppression.

MARKET CHALLENGES

Lack of Rapid and Affordable Nematode Diagnostic Tools for Field Use

The absence of accessible real-time diagnostic tools to confirm nematode presence and species before treatment inhibits the growth of the Europe nematicides market. According to sources, a significant majority of nematicide applications in Southern European agricultural sectors are applied preventively rather than curatively. Traditional laboratory methods for extracting and identifying soil nematodes typically involve a lengthy, multi-week turnaround time. This reactive or precautionary spraying increases input costs and environmental risk while often targeting non-damaging nematode populations. Only a small minority of German potato growers conduct pre-planting testing for nematodes, according to research. Detailed soil nematode testing in Germany represents a significant investment per sample for detailed diagnostic analysis. Despite providing highly accurate, species-level diagnosis, DNA-based qPCR is confined to laboratories due to strict regulatory requirements and the need for complex, specialized equipment. Farmers cannot implement targeted nematicide applications without on-site diagnostic kits, akin to those used for plant pathogens. This diagnostic deficit perpetuates inefficient usage patterns and hampers the market’s shift toward targeted and sustainable nematode management.

Resistance Development in Key Nematode Populations to Repeated Chemical Use

Repeated application of limited nematicide chemistries has accelerated resistance development in major plant parasitic nematodes across the region, which threatens long term control efficacy, and thereby holds back the expansion of the Europe nematicides market. Observations indicate that certain nematode populations show increased resilience in environments with repeated chemical treatments. Continuous use of specific compounds in some regions may reduce their effectiveness against certain types of nematodes. A limited range of available chemical categories leads to reliance on a small number of active ingredients. Patterns of usage suggest that without diverse management techniques, the long-term effectiveness of current control measures may decrease. This biological reality demands integrated approaches, yetregulatory and economic pressures often discourage diverdiversificationr ting a precarious cycle of dependency and diminishing returns in Europehigh-valuelue crop systems.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 4.3% |

| Segments Covered | By Type, Application, Form, Mode of Application, And By Country |

| Various Analyses Covered | Global, Regional & Country Level Analysis; Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, & Rest of Europe |

| Market Leaders Profiled | BASF SE, Bayer CropScience AG, The Dow Chemical Company, E.I. Du Pont De Nemours and Company, and Monsanto Company. The other companies that are profiled are Syngenta AG, FMC Corporation, Adama Agricultural Solutions Ltd., Ishihara Sangyo Kaisha Ltd., and Valent Corporation. |

SEGMENT ANALYSIS

By Type Insights

In 2025, the bio-based nematicides segment secured the majority share of the Europe nematicides market. The leading position of the bio-based nematicides segment is driven by the European Union’s aggressive regulatory phase-out of synthetic active ingredients and strong policy support for biological alternatives. Recently authorized nematicidal products show a shift in approval toward biological or microbially derived alternatives. European policy objectives prioritize biocontrol agents over higher-risk pesticide options, with increasing funding directed towards bacterial and fungal agents. Regulatory frameworks in certain nations require justification for synthetic nematicide use, emphasizing trials of biological options. Furthermore, major potato and vegetable cooperatives across France and Germany have adopted certification schemes that award premium prices for produce grown with bio-nematicides. This convergence of regulatory mandates,, ec mic incentivesecoomic incenincentivesn d supply chain pressure has firmly establishbio-basedsed solutions as the dominant type in Europe’s evolving nematode management landscape.

The bio-based nematicides segment is also predicted to witness the highest CAGR of 12.4% from 2026 to 2034 due to breakthroughs in formulation stability and field efficacy, particularly in open field conditions previously dominated by chemistry. Specialized formulations of certain biological control agents are showing reliable effectiveness in managing root-knot nematodes, even under cooler soil conditions. Regulatory updates regarding RNA interference-based technologies are facilitating the introduction of new, highly specific options for pest control. Financial incentives are becoming more common to support growers who are incorporating these biological products into their pest management strategies. These scienscientific policieseconomic enablers collectively propel bio-based nematicides as the most dynamically advancing segment in Europe.

By Application Insights

The agricultural segment dominated the Europe nematicides market in 2025 as plant parasitic nematodes primarily threaten cultivated crops rather than non-agricultural environments. Agricultural land across the region represents a substantial area, with a significant portion dedicated to crops susceptible to nematode infestation, including potatoes, sugar beets, vegetables, and vineyards. A notable volume of potato production is at risk of loss to nematodes when intervention measures are not applied. The presence of nematodes in these crops represents a potential threat to economic stability and food production. The impact of nematode damage affects the livelihoods of those working in the agricultural sector. National crop protection guidelines in Spain, Italy, and the Netherlands include nematicides in integrated management programs for these high-value commodities. Moreover, the EU’s Common Agricultural Policy increasingly ties direct payments to sustainable pest control practices, incentivizing documented nematicide use within rotation plans. Non-agriculturalications, such as turf or ornamental management, are minimal due to urban pesticide bans in countries like Germany and Sweden. Thus, the overwhelming agronomic necessity and policy alignment ensure that agriculture remains the exclusive application domain for nematicides in Europe.

The agricultural segment is also estimated to register the fastest CAGR of 10.8% over the forecast period, owing to the intensification of high-value horticulture in Southern and Eastern Europe, where nematode pressure is acute. Vegetable cultivation in certain Mediterranean regions has experienced growth, influenced by demand from international markets. These agricultural products face significant vulnerability to infestations from specific nematode species. New environmental regulations require farms seeking specific incentives to monitor soil health and evaluate nematode risks. These policy changes have resulted in increased, proactive use of nematicides. Furthermore, new resistant crop varieties often still require nematicide support during early establishment phases. Stringent urban pesticide regulations have stalled non-agricultural alternatives, allowing the agricultural segment to monopolize market innovation and expansion.

By Form Insights

The liquid formulations segment led the Europe nematicides market in 2025. The supremacy of the liquid formulations segment is attributed to its compatibility with precision application systems and superior soil distribution compared to granular alternatives. Many bio-nematicides and RNA interference products are formulated as liquids, allowing them to be applied through existing irrigation systems. In specific agricultural regions, a significant portion of farming operations utilize irrigation systems that deliver nutrients and treatments directly to the root zone. The use of liquid formulations in specialized irrigation systems is a method employed to increase effectiveness and reduce environmental exposure. The infrastructure for applying treatments via irrigation is common in certain European agricultural areas, facilitating the use of liquid products. Regulatory agencies also favor liquids as they typically contain fewer inert carriers that could leach into groundwater. Additionally, liquid forms allow for on-farm tank mixing with fertilizers or biostimulants, streamlining operations. This technical and regulatory alignment with modern agronomic practices solidifies liquid formulations as the preferred delivery format across European farming systems.

The liquid formulations segment is anticipated to witness the fastest CAGR of 11.3% from 2026 to 2034. The rapid growth of this segment is propelled by the rise of water-soluble bio-nematicides and the expansion of micro-irrigation infrastructure across Europe. The use of precision irrigation methods, such as drip and sprinkler systems, is growing in Mediterranean agricultural areas experiencing significant nematode challenges. Liquid products created from Streptomyces metabolites are proving more stable when applied via irrigation. Field assessments suggest that liquid applications can achieve higher root colonization than granular options, aligning with revised guidance that promotes liquid delivery for improved safety and reduced dust exposure. These infrastructural produproductsregulatory synergies position liquid nematicides as the most scalable anfuture-readydy format in Europe’s precision agriculture ecosystem.

By Mode of Application Insights

The irrigation-based application segment was the largest in the Europe nematicides market in 2025 because of its precision, efficiency, and alignment with water management practices in high-value cropping systems. In certain southern European areas, a notable amount of nematicide is applied using targeted irrigation to place treatments directly where roots are located. This method helps to concentrate the active ingredient and reduces the possibility of drift. Utilizing drip or micro-sprinkler systems for application permits lower dosages and aligns with current nutrient management routines. The application of bio-nematicides through irrigation seems to improve root colonization in some vegetable plants when compared to broadcast methods. National water efficiency programs in Greece and Portugal further incentivize chemigation by linking subsidies to integrated input delivery. Regulatory bodies also favor this mode as it limits soil and groundwater contamination risks compared to soil drenching or fumigation. These agronomic, econoecnomicd environmental advantages make irrigation the dominant and most sustainable application mode in Europe.

The seed treatment segment is likely to experience the fastest CAGR of 13.1% from 2026 to 2034. The swift expansion of the seed treatment is fuelled by the development of systemic and film coating technologies that protect young seedlings during the most vulnerable growth stages. The use of certain novel nematicidal compounds applied to sugar beet and maize seeds appears to be linked to a reduction in early root damage from Heterodera and Pratylenchus species. Environmental concerns leading to restrictions on in-furrow granular applications are accelerating a shift towards seed treatment methods for delivering systemic nematicides, which are becoming standard practice in some European countries. Agricultural companies are observed to be offering integrated seed health packages that combine nematicides with fungicides and biostimulants. This precision at source approach reduces overall chemical load while ensuring consistent plant pprotectionthe most innovative and rapidly scaling application mode.

COUNTRY ANALYSIS

Spain Nematicides Market Analysis

Spain was the top performer in the Europe nematicides market by accounting for a 22.5% share in 2025. The prominence of the Spanish market is credited to its extensive horticultural production under warm climates that favor high nematode reproduction rates. The country is Europe’s largest user of drip irrigation, enabling widespread adoption of liquid bio-nematicides through fertigation systems. National Integrated Production protocols mandate nematode monitoring and require documented control measures for export certification. Furthermore, Spain’s research institution includehe Instituto de Agricultura Sostenible, lead EU-funded trials on RNAi nematicides. These agronomic regu,latory and,, and infrastructural factors position Spain as the most intensive and technologically advanced nematicide market in Europe.

Italy Nematicides Market Analysis

Italy followed closely in the Europe nematicides market by occupying a 18.3% share in 2025. The growth of the Italian market is supported by its high density of vegetable, potato, and vineyard cultivation innematode-prone areass. Italy cultivates significant agricultural areas with crops susceptible to plant-parasitic nematodes, particularly in vegetthe able and greenhouse sectors. The presence of these crops in warmer soil conditions, often sandy, creates potential for high infestation and risks to productivity. National agricultural strategies are increasingly funding sustainable methods, including incentives for using biological controls for pests. This indicates a shift towards mitigating environmental impacts by supporting biological alternatives over chemical products for nematode control. Additionally, Italian cooperatives enforce strict pre-harvest testing for export tomatoes and zucchinis driv,, driving consistent product demand. Despite regulatory stringency, Italy maintains pragmatic flexibility for high-value crops ensu, ring nematicides remain a critical component of its intensive agricultural model.

Netherlands Nematicides Market Analysis

The Netherlands holds a significant share of the Europe nematicides market owing to its leadership in potato seed production and protected cultivation systems. According to the Dutch Ministry of Agriculture, over ninety percent of the country’s two hundred thousand hectare potato crop is grown for seed export, with zero tolerance for Globodera contamination mand, mandating rigorous nematicide use. The Netherlands functions as a prominent hub for research and development into microbial methods for controlling plant-parasitic nematodes. Companies in the area are involved in developing and testing biological control agents under strict safety guidelines. Greenhouse farms producing tomatoes and peppers in the region frequently use liquid nematicides within their cultivation systems. These applications are often part of closed-loop irrigation systems intended to support root health and consistent production. National regulations prohibit soil fumigants but permit targeted bio and systemic chemistries under integrated pest management certification. This combination of export-driven standards, technological sophistication, re u latory clarity makes the Netherlands a high high-valueision nematicide market.

France Nematicides Market Analysis

France is moving ahead consistently in the Europe nematicides market due to its vast sugar beet and potato sectors whic, which face chronic nematode pressure. A significant portion of land in primary potato-growing regions faces widespread, chronic issues with soil-borne pests. Efforts to reduce reliance on conventional synthetic treatments are being encouraged through financial support for the adoption of alternative biological pest control methods. The country is advancing the validation and testing of genetically-based solutions through collaborative research initiatives between public and private entities. Sugar beet growers in Grand Est face Heterodera schachtii infestations that reduce yields byup too twenty-fivepercentt, prompting the adoption of seed treatments and in-furrow treatments. National guidelines now require nematode risk mapping before planting rein, forcing systematic intervention. These structural crop economics and policy supports sustain France’s significant role in the European nematicide landscape.

Germany Nematicides Market Analysis

Germany is anticipated to grow in the Europe nematicides market from 2026 to 2034 owin, owing to stringent regulregulationssnced with high high-value needs. According to the Julius Kühn Institute pota, potato and vegetable production in Lower Saxony and Bavaria faces significant pressure from Globodera and Meloidogyne species despite cool climates. The approval of nematicides in Germany is constrained to a limited range of active ingredients, focusing on specific chemical and biological options. Application of these products is contingent upon verified, documented evidence of infestation through soil analysis. Technological advancements in diagnostic testing are increasingly used by regional agricultural authorities to guide the precise application of control measures. Regulatory standards for seed potato certification require validation of nematode-free status for fields, which is supported by mandatory crop rotation practices and targeted control methods. The Federal Office of Consumer Protection and Food Safety enforces ground monitoring, ng which favors liquid systemic and seed seed-appliedats over soil fumigants. This science-based model ensures that nematicide use remains targeted, minimal, mal and highly effective ssolvingingg Germany’s role as quality-driven compliance-orientedet.

COMPETITIVE LANDSCAPE

Competition in the Europe nematicides market is defined by a tight race among multinational agrochemical firms and specialized biocontrol developers to deliver compliant effe,ctive and sustainable nematode solutions under one of the world’s strictest pesticide regulatory regimes. The withdrawal of legacy fumigants and broad-spectrum insecticides has created a high barrier to entry fav, favoring companies with strong regulatory dossiers and proven efficacy data. Differentiation centers on the mode of action delivery format and integration with digital or agronomic advisory services. Multinationals like BASF Baye,r and,, Syngenta lead through R and D scale and global pipelineswhilee European bioinnovators gain traction through niche microbial or RNA bRNA-baseducts. National farming practices also shape competition, with Southern Europe favoring irrigation applied liquids and Northern Europe emphasizing seed treatments and soil diagnostics. The lack of rapid diagnostics and inconsistent bio-nematicide performance further complicates ultimate ssuccesss which, whichs hinges on balancing regulatory ccompliance noeconomiceliability, and alignment with the EU’s agroecological transition goals.

KEY MARKET PLAYERS

The key players in this market are

- BASF SE

- Bayer CropScience AG

- The Dow Chemical Company

- E.I. Du Pont De Nemours and Company

- Monsanto Company

- Syngenta AG

- FMC Corporation

- Adama Agricultural Solutions Ltd.

- Ishihara Sangyo Kaisha Ltd.

- Valent Corporation.

Top Players In The Market

- BASF SE is a significant contributor to the Europe nematicides market through its portfolio of innovative chemical and biological solutions targeting plant parasitic nematodes in high-value crops. The company’s fluopfluopyram-basedticides are widely used across potato and vegetable farms in Germany, the Netherlands, and France due to their systemic activity and compatibility with integrated pest management. BASF has strengthened its position by investing in RNA interference research in partnership with European academic institutions to develop next-generation species-specific pesticides. These efforts align with EU sustainability goals while reinforcing BASF’s global leadership in crop protection innovation and its commitment to science-driven management solutions.

- Syngenta Group plays a pivotal role in the Europe nematicides market by offering advanced seed treatment technologies and biological nematicides tailored for sugar beet pota, toes andvegetables. The company leverages its global R and D network to develop formulations that meet Europe’s stringent regulatory standards while delivering consistent field performance. Recently Sy, Syngenta expanded its bio-nematicide line with a new Streptomyces-based product approved under the EU’s streamlined bio-innovative way. The company also collaborates with European farming cooperatives in Spain and Italy to demonstrate the economic benefits of earlyearly-seasonticide application through on-farm trials. These initiatives support Syngenta’s broader mission to advance sustainable agriculture and position it as a key enabler of soil health-focused protection strategies across Europe and globally.

- Bayer AG actively shapes the Europe nematicides market through its integrated approach combining chemical nematicides with digital agronomic advisory tools. The company’s nematicide solutions are embedded within its Climate FieldView platform whic, which uses soil health data to recommend targeted applications based on nematode risk maps. Bayer has intensified its focus on biologicals by acquiring European biocontrol startups and co deco-developingoencapsulated fungal nematicides with extended field persistence. These actions reflect Bayer’s strategy to merge precision chemistry, digital innovation, and biological innovation crea,, creating holistic nematode management systems that serve both European sustainability mandates and global farming needs.

Top Strategies Used By The Key Market Participants

Key players in the Europe nematicides market prioritize the development of bio-based RNA interference-enabled products that align with the EU’s pesticide reduction targets and regulatory frameworks. They invest in precision delivery systems such as seed treatments and irrigation-compatible formulations to minimize environmental impact and enhance efficacy. Companies form strategic partnerships with research institutifarmingrming cooperatives, and digital agriculture platforms to validate performance and drive adoption. Regulatory engagement is central, with firms actively participating in EU biotechivative approval pathways to accelerate market access. Additionally, they focus on integrated soil health programs that position nematicides as one component of a broader agronomic strategy rather than a standalone chemical intervention.

MARKET SEGMENTATION

This research report on the Europe nematicides market is segmented and sub-segmented into the following categories.

By Type

- Fumigants

- Carbamates

- Organophosphates

- Bio-based Nematicides

By Application

- Agricultural

- Non-Agricultural

By Form

- Liquid

- Granular

By Mode of Application

- Irrigation

- Spraying

- Fumigation

- Seed Treatment

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

What is the Europe nematicides market?

The Europe nematicides market includes chemical and biological products used to control nematodes — microscopic worms that damage roots and reduce crop yields — across major agricultural crops.

Why are nematicides important in agriculture?

Nematicides protect crops from root-knot, lesion, and cyst nematodes, improving root health, nutrient uptake, yield, and overall farm profitability.

What products are included in this market?

Key products include synthetic chemical nematicides, bio-nematicides (biological controls), fumigants, and seed treatment solutions that reduce nematode populations in soil or on seeds.

What drives growth in the Europe nematicides market?

Market growth is driven by rising awareness of nematode crop damage, demand for higher yields, adoption of integrated pest management (IPM), and regulatory shifts toward safer alternatives.

Which crops benefit most from nematicides?

Major crops include vegetables (tomato, potato), fruits, cereals (wheat, barley), sugar beet, pulses, and high-value horticultural crops prone to nematode infestation.

What trends are shaping this market?

Key trends include bio-based nematicides, precision application technologies, biological seed treatments, and reduced-risk chemistries aligned with sustainability goals.

What challenges does the Europe nematicides market face?

Challenges include stringent EU regulations on chemical pesticides, environmental and human health concerns, development of resistance, and demand for eco-friendly alternatives.

How do biological nematicides differ from chemical ones?

Biological nematicides use microbes, metabolites, or plant extracts to suppress nematodes, offering lower toxicity and better environmental safety compared to conventional chemicals.

What role does integrated pest management (IPM) play?

IPM combines nematicides with crop rotation, resistant varieties, soil health practices, and monitoring to sustainably manage nematode populations and reduce reliance on chemicals.

How do regulations influence this market?

European regulations restrict or phase out certain chemical nematicides to protect ecosystems, promoting safer formulations, compliance standards, and environmental risk assessment.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com