Europe Neurostimulation Devices Market Size, Share, Trends & Growth Forecast Report By Technology, Application, and Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic and Rest of Europe) - Industry Analysis, From (2025 to 2033)

Europe Neurostimulation Devices Market Summary

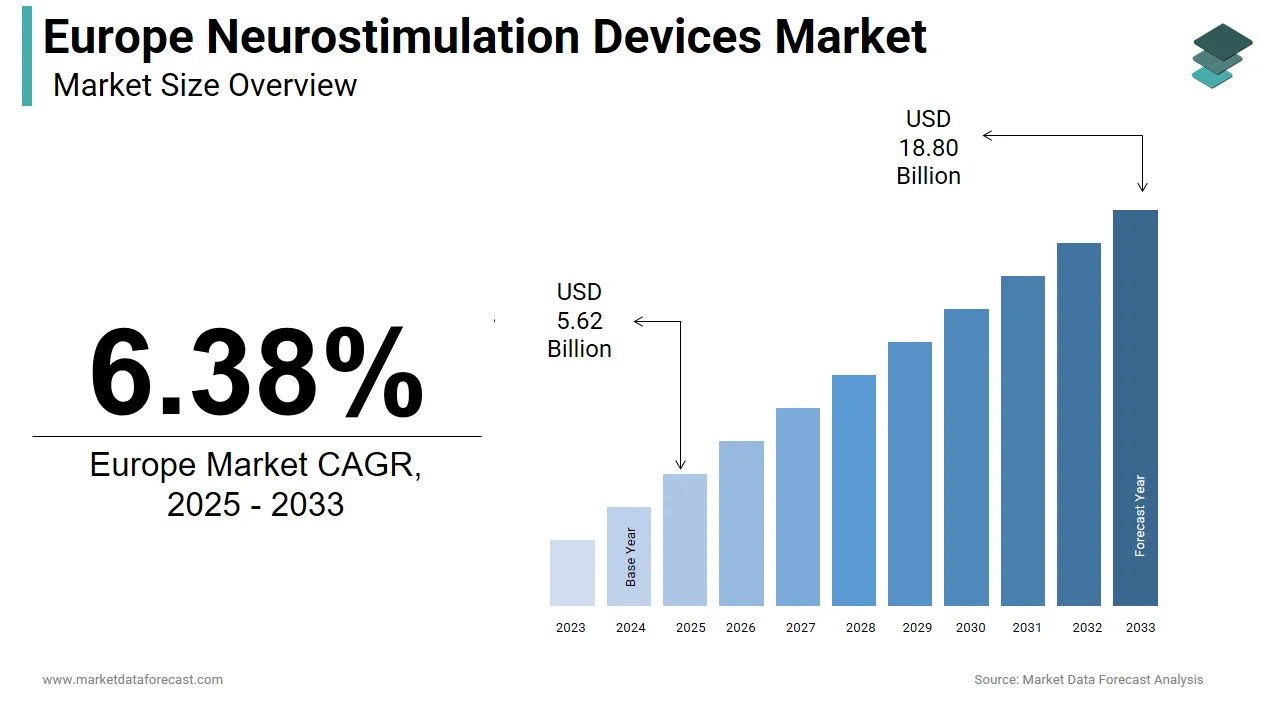

Market Size & Growth Projections

- 2024 Market Size: USD 4.83 billion

- 2025 Market Size: USD 5.62 billion

- 2033 Forecast Value: USD 18.80 billion

- Growth Outlook (2025–2033): CAGR of 6.38%, driven by rising neurological disease burden and expanding therapeutic indications.

Key Regional Dynamics

- Largest Markets: Germany, France, United Kingdom

- Fastest-Growing Sub-region: Northern Europe, supported by early adoption of advanced neuromodulation and strong reimbursement frameworks

- Dominant Countries: Germany, France, UK, Italy, Spain

- Emerging Markets: Czech Republic, Turkey, Eastern Europe

Regional Highlights

- Western Europe dominates market revenues due to strong neurology infrastructure, high procedural volumes, and comprehensive reimbursement coverage for implantable devices.

- Northern Europe shows accelerated uptake of non-invasive and outpatient neurostimulation solutions aligned with digital health policies.

- Southern & Eastern Europe demonstrate uneven growth due to budget constraints, reimbursement variability, and specialist shortages.

Segmental Insights

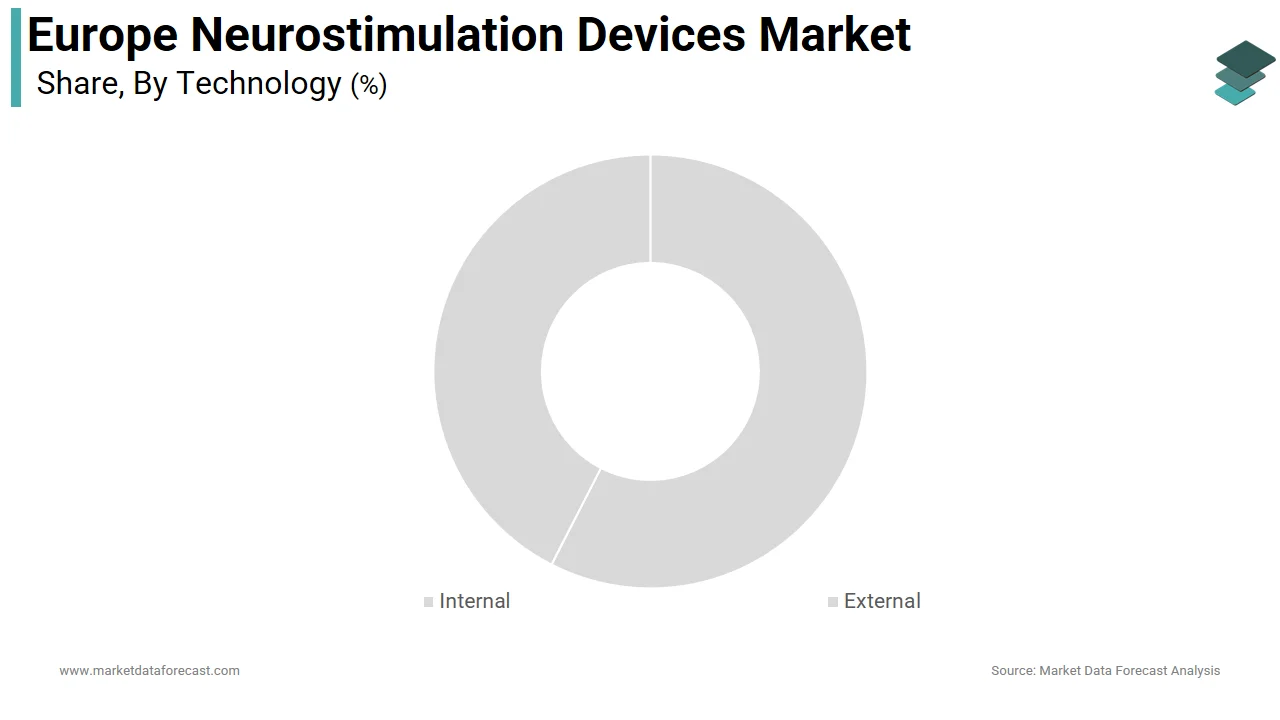

- Internal Neurostimulation Devices led the market in 2024, supported by widespread adoption of spinal cord stimulation and deep brain stimulation for chronic pain and Parkinson’s disease.

- External Neurostimulation Devices are expected to grow at the fastest rate, driven by demand for non-invasive, home-based, and digitally connected therapies.

- Spinal Cord Stimulation held the largest share in 2024 due to the high prevalence of chronic neuropathic pain.

- Transcranial Magnetic Stimulation (TMS) is projected to record the fastest growth, supported by expanding use in depression, OCD, migraine, and stroke rehabilitation.

Key Growth Trends

- Rising prevalence of chronic neurological and pain disorders across aging European populations.

- Expansion of reimbursement coverage for neuromodulation therapies in major EU economies.

- Technological advances in closed-loop systems, miniaturization, and adaptive stimulation.

- Shift toward outpatient, non-invasive, and home-based neurostimulation solutions.

Key Players

- Abbott Laboratories, Aleva Neurotherapeutics SA, Boston Scientific Corporation, ElectroCore Inc., EndoStim Inc., Medtronic plc, Nevro Corporation, Neuronetics Inc., NeuroSigma, Inc., and Synapse Biomedical Inc.

Europe Neurostimulation Devices Market Size

The size of the Europe neurostimulation devices market was valued at USD 4.83 billion in 2024. This market is expected to grow at a CAGR of 6.38% from 2025 to 2033 and be worth USD 18.80 billion by 2033 from USD 5.62 billion in 2025.

Neurostimulation devices are medical technologies engineered to modulate neural activity through targeted delivery of electrical or magnetic impulses to specific regions of the nervous system. Within Europe, these devices are primarily employed in treating chronic pain, movement disorders, epilepsy, depression, and bladder dysfunction. The therapeutic scope continues to expand as clinical validation grows and technological refinements enhance precision and patient safety. According to sources, neurological disorders represent a major public health challenge and are one of the leading causes of illness and disability across the European Union, affecting a very large portion of the population. This high prevalence underscores a substantial and ongoing clinical need for diverse treatment options, including innovative therapies like neurostimulation. As per data from Eurostat, the share of Europeans aged 65 years and above reached 21.6 percent in 2024, a demographic reality that intensifies demand for advanced neuromodulation solutions given the age-related prevalence of conditions like Parkinson’s disease and chronic neuropathic pain. Furthermore, the European regulatory framework for medical technologies, including neurostimulation devices, is distinct from the process for medicinal products. This confluence of demographic pressure, clinical burden, and evolving regulatory pathways underscores the strategic importance of the Europe neurostimulation devices market in the broader landscape of medical technology.

MARKET DRIVERS

Rising Prevalence of Chronic Neurological Conditions Fuels Device Adoption

The persistent and escalating burden of chronic neurological diseases across the region serves as a major accelerator for the Europe neurostimulation devices market. The prevalence of Parkinson's disease across Europe demonstrates a significant public health burden. Similarly, A large and growing proportion of the European population is affected by chronic pain and epilepsy. These conditions often become refractory to conventional pharmacological interventions, compelling clinicians to consider neuromodulation as a viable alternative. Spinal cord stimulation offers a significant degree of pain reduction for many eligible patients who have not found relief with other therapies. Deep brain stimulation provides lasting motor symptom management for the majority of individuals with advanced Parkinson's disease. This clinical validation, coupled with the expanding pool of eligible patients due to aging demographics, creates a compelling demand dynamic. European healthcare systems, despite budgetary constraints, increasingly recognize the cost-effectiveness of neurostimulation in reducing long-term disability and pharmacotherapy dependence, further accelerating device integration across specialized neurology and pain management centers.

Expanding Reimbursement Coverage Strengthens Market Accessibility

Favourable reimbursement frameworks across several European nations significantly enhance patient access to neurostimulation therapies and propel the expansion of the Europe neurostimulation devices market. In Germany, statutory health insurers routinely cover deep-brain stimulation for Parkinson’s disease and spinal cord stimulation for chronic pain, provided specific clinical criteria are met. France's National Health Insurance Fund provides substantial coverage for sacral nerve stimulation (SNS) for appropriate urinary conditions, with the primary public system covering a large portion of the approved costs and complementary private insurance playing a significant role in minimizing patient out-of-pocket expenses. Out-of-pocket expenses for medical goods vary significantly across high-income European countries and other OECD regions; generally, robust third-party payment mechanisms lead to lower patient direct costs in many European systems, a contrast to potentially higher patient contributions observed elsewhere. The United Kingdom’s National Institute for Health and Care Excellence (NICE) has provided positive guidance for certain neurostimulation procedures in the treatment of chronic pain, facilitating widespread National Health Service (NHS) access under specific conditions, while its guidance for the use of neurostimulation for treatment-resistant depression is more cautious, typically limiting its use to a research context. These structured reimbursement pathways reduce financial barriers for both patients and providers, encouraging earlier intervention and broader clinical trial participation. This institutional support not only drives volume but also incentivizes manufacturers to pursue CE certification and local health technology assessments, thereby reinforcing a virtuous cycle of innovation, access, and clinical integration.

MARKET RESTRAINTS

Stringent Regulatory Requirements Delay Market Entry and Increase Costs

The rigorous regulatory landscape governing medical devices in the region poses a significant barrier to the timely commercialization of neurostimulation systems. This hampers the growth of the Europe neurostimulation devices market. Neurostimulation devices have a Class III classification under the current regulation. The classification is due to the devices being implantable and interacting directly with the central nervous system. Also, the regulatory process for these devices requires comprehensive clinical evidence. Conformity assessments by independent bodies are a necessary part of this process. The time required to obtain necessary approval for high-risk medical devices has notably increased. Approval times often extend over a significant duration. Moreover, the notified body capacity remains constrained. These bottlenecks translate into extended development timelines and elevated compliance expenditures, particularly burdensome for small and medium-sized enterprises lacking established regulatory infrastructure. Besides, post-market surveillance obligations under the new regulation require continuous data collection and risk management updates, further increasing operational costs. Such regulatory friction not only stifles innovation velocity but also limits patient access to next-generation therapies, especially in indications with limited existing treatment options.

High Procedure Costs and Limited Specialist Availability Restrict Widespread Utilization

The substantial financial and human resource requirements associated with neurostimulation procedures hinder the expansion of the Europe neurostimulation devices market. Spinal cord stimulator implantation involves a significant expense per patient. Deep-brain stimulation procedures incur high costs. The expenses associated with these surgical interventions cover the device, the operation, hospital stays, and post-surgical programming. These treatment costs are a notable factor in regional healthcare budgeting. High costs, performance issues, and potential complications are areas of interest for research. Some analyses indicate that these treatments can be cost-effective over time, especially when compared to other ongoing medical management options. These expenses, while partially reimbursed, still deter cost-conscious payers in Southern and Eastern European nations where healthcare spending per capita remains low. Compounding this issue is the acute shortage of trained specialists. As per sources, a limited number of neurosurgeons in the EU possess certified expertise in functional neurosurgery, translating to less than one specialist per million inhabitants in several member states. This scarcity results in prolonged wait times for evaluation and implantation. Furthermore, multidisciplinary teams required for optimal outcomes, including neurologists, pain specialists, and electrophysiologists, are concentrated in urban academic centers, which limits rural access. Consequently, despite proven benefits, neurostimulation remains inaccessible to a significant segment of the eligible patient population, particularly in resource-constrained regions.

MARKET OPPORTUNITIES

Technological Advancements in Miniaturization and Closed Loop Systems Unlock New Applications

Innovations in device engineering, particularly in miniaturization and adaptive stimulation algorithms, are creating potential opportunities for the Europe neurostimulation devices market. Recent developments have yielded leadless spinal cord stimulators measuring under two centimeters in length, enabling percutaneous implantation with reduced surgical morbidity. More significantly, closed-loop or responsive neurostimulation systems, which adjust stimulation parameters in real time based on neural feedback, have demonstrated superior outcomes in epilepsy and mood disorders. Responsive neurostimulation is showing promising results in reducing seizure frequency for individuals with drug-resistant epilepsy. In some cases, this approach has demonstrated a notable improvement compared to open-loop stimulation alternatives. Adaptive deep-brain stimulation trials are indicating better outcomes in managing motor symptoms for Parkinson’s patients. This adaptive method appears to offer a more significant improvement when contrasted with conventional continuous stimulation techniques. These advances not only enhance therapeutic precision but also expand eligibility criteria to include patients previously deemed unsuitable due to comorbidities or anatomical constraints. Once these cutting-edge platforms receive regulatory approval and clinical validation, they are positioned to address significant unmet needs in conditions like treatment-resistant depression, obsessive-compulsive disorder, and obesity, thereby expanding the available therapeutic options across various neurological and psychiatric fields.

Growing Emphasis on Outpatient and Home-Based Neuromodulation Drives Adoption

A paradigm shift toward decentralized care models in European healthcare systems is opening new prospects for the Europe neurostimulation devices market. This gives a new pathway for the deployment of these devices beyond traditional hospital settings. Transcutaneous and non-invasive neurostimulation technologies, such as vagus nerve stimulation via the ear or trigeminal nerve stimulation through the forehead, enable safe, repeatable treatment in home environments. Countries like Sweden and the Netherlands have integrated these devices into national chronic pain management protocols by allowing general practitioners to initiate therapy without specialist referral. This trend aligns with broader health policy objectives. The European Commission’s Digital Health Action Plan prioritizes technologies that reduce hospital admissions and empower patient self-management. Besides, reimbursement agencies are adapting. This convergence of policy support, clinical validation, and patient-centric design is transforming neurostimulation from a last resort surgical intervention into an accessible frontline therapy, which significantly expands the addressable patient pool and accelerates market penetration across primary and community care networks.

MARKET CHALLENGES

Complex Reimbursement Heterogeneity Across European Countries Impedes Uniform Market Growth

The absence of harmonized reimbursement policies across European member states creates significant commercial and access disparities for neurostimulation technologies. As a result, this challenges the growth of the Europe neurostimulation devices market. While Germany and France maintain structured coverage for a wide range of neuromodulation procedures, countries in Southern and Eastern Europe often lack specific reimbursement codes or impose restrictive criteria that limit eligibility. Reimbursement pathways for sacral nerve stimulation are not formal in all member states. A limited number of member states offer coverage for certain newer applications, such as gastric electrical stimulation for gastroparesis. This fragmentation forces manufacturers to navigate a patchwork of health technology assessment requirements, pricing negotiations, and administrative hurdles, delaying market entry and inflating operational costs. Moreover, disparities in healthcare expenditure exacerbate inequities. Bulgaria and Romania allocate a smaller amount per capita annually to healthcare, making high-cost devices economically unviable despite clinical need. This regulatory reimbursement asymmetry not only stifles cross-border scalability but also perpetuates geographic inequities in patient access, which affects the potential for Europe-wide therapeutic impact and constrains the ability of innovators to achieve sustainable commercial returns across the region.

Long-Term Device Safety and Cybersecurity Risks Undermine Stakeholder Confidence

Persistent concerns regarding the long-term biocompatibility of implantable neurostimulation systems and emerging cybersecurity vulnerabilities pose an obstacle to the Europe neurostimulation devices market. Implant-related complications, including lead migration, tissue fibrosis, and device erosion, occur in a portion of spinal cord stimulation cases within five years, as per research. These adverse events necessitate revision surgeries, increasing patient morbidity and healthcare costs. More critically, the integration of wireless connectivity for remote programming has introduced cybersecurity risks. The mere potential for harm damages trust between clinicians and patients, even without documented incidents. Regulatory bodies have responded with stricter post-market surveillance; however, harmonized cybersecurity certification standards for active implantable medical devices remain under development. Consequently, hospitals in countries like Austria and Finland have temporarily restricted the procurement of wirelessly enabled stimulators pending further risk mitigation. This caution, while clinically prudent, slows adoption of technologically advanced platforms and discourages investment in connected health features that could otherwise enhance patient monitoring and outcomes. Market expansion and innovation diffusion will remain hindered until universally accepted safety and cybersecurity protocols are robustly institutionalized.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| Segments Covered | By Technology, Application, and Region. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, and the Rest of Europe |

| Market Leaders Profiled | Abbott Laboratories, Aleva Neurotherapeutics SA, Boston Scientific Corporation, ElectroCore Inc., EndoStim Inc., Medtronic plc, Nevro Corporation, Neuronetics Inc., NeuroSigma, Inc., and Synapse Biomedical Inc. |

SEGMENTAL ANALYSIS

By Technology Insights

In 2024, the internal neurostimulation devices segment led the Europe neurostimulation devices market and captured a substantial share. The dominance of the internal neurostimulation devices segment is attributed to its proven efficacy in managing severe and chronic neurological conditions that require sustained, targeted intervention. The widespread clinical adoption of implantable systems such as spinal cord and deep-brain stimulators for conditions with limited pharmacological solutions also drives the growth of this segment. According to various studies, deep brain stimulation is an established treatment option for select patients with advanced Parkinson's disease, though its utilization varies, and many eligible patients may experience delays in receiving the therapy after diagnosis. Besides, Long-term studies have shown that many implanted patients experience significant motor improvement that can be sustained for several years post-surgery, providing durable symptom management. An additional growth factor is the robust reimbursement infrastructure in high-income European countries. Deep brain stimulation is an established and integrated therapy within the German and French healthcare systems, covered by national health insurance for patients meeting the approved clinical indications. These policies, coupled with CE-marked device proliferation, create a favourable ecosystem for sustained market leadership of internal technologies.

The external neurostimulation devices segment is anticipated to witness the fastest CAGR of 12.4% between 2025 and 2033. The rapid expansion of the external neurostimulation devices segment is primarily fueled by rising demand for non-invasive, patient-centric neuromodulation solutions supported by evolving digital health policies. A principal growth driver is the integration of external devices into national primary care frameworks for chronic pain and mental health. Several European Union member states have incorporated transcutaneous electrical nerve stimulation and transcranial magnetic stimulation into standard reimbursed outpatient healthcare protocols. These treatment options are being applied to conditions such as migraine and certain types of depression. The general adoption and prescription of these external devices in clinical settings reflect a growing trend in patient care. A further growth enabler is technological convergence with consumer electronics. Wearable neurostimulators now feature smartphone connectivity, AI-driven dose titration, and cloud-based outcome tracking. These innovations, combined with shorter regulatory pathways for non-implantables under the EU Medical Device Regulation, position external technologies as the vanguard of accessible neuromodulation.

By Application Insights

The spinal cord stimulation segment was the largest in the Europe neurostimulation devices market by accounting for 32.4% in 2024. The supremacy of the spinal cord stimulation segment is credited to the escalating burden of chronic neuropathic pain and the therapy’s established position as a second-line intervention after failed conservative management. The high and growing prevalence of treatment-refractory pain conditions further propels the growth of this segment. Chronic low back pain represents a significant and escalating global health burden, impacting quality of life and contributing to substantial healthcare costs across Europe. Clinical endorsement further entrenches its dominance. Clinical practice guidelines for managing low back pain emphasize an integrated, interprofessional approach and often caution against the long-term use of certain pharmacological treatments like opioids due to limited evidence of effectiveness and potential harms. A second factor is technological maturation. Modern systems with high-frequency and burst stimulation waveforms achieve superior paresthesia-free pain relief, accelerating adoption. Spinal cord stimulation is an established treatment option for carefully selected patients with chronic neuropathic pain when other therapies have failed, offering relief and improved daily functioning for many. Combined with partial or full reimbursement in a number of EU countries, these elements secure spinal cord stimulation’s position as the cornerstone application in European neuromodulation.

The transcranial magnetic stimulation segment is likely to experience the fastest CAGR of 14.1% from 2025 to 2033 due to expanding clinical indications beyond major depressive disorder into areas like obsessive compulsive disorder, post-stroke rehabilitation, and chronic migraine. An additional driver of this segment is regulatory and policy alignment. Regulatory bodies and healthcare systems in various regions are increasingly acknowledging the effectiveness of rTMS for treatment-resistant obsessive-compulsive disorder. Simultaneously, national health systems are decentralizing access. In Sweden and elsewhere, there is a growing trend towards expanding the scope of practice and treatment settings for licensed mental health professionals, which enhances the delivery of mental health services. A further growth driver is compelling health economic data. Recent economic evaluations and health technology assessments show that transcranial magnetic stimulation is generally a cost-effective intervention for depression when compared to standard care, which may encourage broader adoption by healthcare payers. So, this non-invasive, office-based therapy is rapidly transitioning from niche intervention to mainstream psychiatric care.

COUNTRY-LEVEL ANALYSIS

Germany Neurostimulation Devices Market Analysis

Germany outperformed other countries in the Europe neurostimulation devices market by occupying a 23.7% share in 2024. The leading position of the German market is driven by its functioning as the region’s clinical innovation and reimbursement benchmark. Its dominance is supported by a sophisticated neurology and pain management infrastructure, universal health coverage, and early adoption of advanced neuromodulation therapies. Thousands of neurostimulation procedures were performed in Germany, the highest in Europe, according to sources. The statutory health insurance system covers deep brain stimulation, spinal cord stimulation, and sacral nerve stimulation for approved indications with minimal patient cost sharing, creating a stable demand environment. Besides, Germany hosts Europe’s densest concentration of functional neurosurgery centers, with several university hospitals offering multidisciplinary implant programs. The Federal Joint Committee’s rapid health technology assessment process further accelerates new therapy integration. Coupled with a population of millions of people aged 65 or older, facing neurodegenerative and chronic pain conditions, Germany maintains unparalleled market depth and serves as the launchpad for pan-European commercialization.

France Neurostimulation Devices Market Analysis

France secured the second position in the Europe neurostimulation devices market and held an 18.1% share in 2024. The growth of these devices in France is attributed to its centralized reimbursement system and strong neurosurgical tradition. The French National Authority for Health maintains a transparent list of reimbursed neurostimulation procedures, with high coverage rates for spinal cord and deep brain stimulation. This predictability has fostered high procedural volumes. There has been a notable volume of implants in the recent period. Also, the region demonstrates leadership in adopting new medical technologies. A trial involving a closed-loop stimulation treatment for pain has been conducted. The treatment method showed a significant reduction in pain among participants in the trial. The country’s aging population amplifies demand. Furthermore, France’s national digital health strategy actively promotes connected neurostimulation devices, with many platforms integrated into the state-backed Mon Espace Santé patient portal. These institutional enablers solidify France’s position as a high-volume and high-access market.

United Kingdom Neurostimulation Devices Market Analysis

The United Kingdom continues to be a key player in the Europe neurostimulation devices market because of evidence-based policy and centralized procurement through the National Health Service. The National Institute for Health and Care Excellence (NICE) continues to issue positive guidance for various neurostimulation applications, a process that involves assessing both clinical effectiveness and cost-effectiveness under budgetary review. This has driven standardized adoption across integrated care systems. Participation in the UK Neuromodulation Registry is encouraged by NICE to track the use and long-term outcomes of procedures like spinal cord stimulation, reflecting an ongoing effort to gather real-world evidence. The UK also excels in post-market real-world evidence generation, with mandatory participation in national outcome registries that track device performance over time. The burden of neurological disease further sustains demand. A significant proportion of the UK population lives with a neurological condition, and chronic pain is a prevalent and increasing health challenge, particularly among older adults. The MHRA maintains strong alignment with EU regulatory frameworks post-Brexit, balancing divergence with the need for swift patient access to devices and a strong UK presence in the European market.

Italy Neurostimulation Devices Market Analysis

Italy is expected to be the most lucrative region in the Europe neurostimulation devices market due to strong clinical demand in the north and persistent access barriers in the south. Northern regions such as Lombardy and Emilia Romagna operate world-class neuromodulation centers with reimbursement parity to Germany, performing a large number of implants annually, according to sources. Several people suffer from chronic neuropathic pain, and its occurrence is rising in the population. An advancement in medical care for overactive bladder involved a specific treatment being covered as a standard service. Coverage for this particular treatment is now the same across all regions. However, procedural density remains uneven; southern regions report wait times exceeding several months due to specialist shortages and budget caps. Despite these challenges, private insurance uptake is rising, enabling faster access for affluent patients. These dynamics position Italy as a high-potential, asymmetric market where policy harmonization could unlock substantial growth.

Switzerland Neurostimulation Devices Market Analysis

Switzerland is likely to grow notably in the Europe neurostimulation devices market during the forecast period owing to its premium adoption patterns, high per capita spending, and rapid integration of next-generation technologies. Though not an EU member, Switzerland’s Swissmedic agency maintains mutual recognition agreements with the European Commission, enabling swift market entry for CE-marked devices. The country’s universal compulsory health insurance covers neurostimulation for all major indications, with patients contributing only a portion of co-payment after an annual deductible. This accessibility, combined with high income levels, fuels early uptake of advanced platforms. Moreover, Switzerland hosts key research hubs, which partner with industry to accelerate clinical translation. These attributes make Switzerland a high-value testbed for innovation despite its modest population size.

COMPETITIVE LANDSCAPE

Competition in the Europe Neurostimulation Devices Market is intense yet concentrated among a handful of global medtech leaders with complementary portfolios and deep regulatory expertise. The landscape is characterized by continuous technological iteration rather than price-based rivalry, with players competing on clinical outcomes, device longevity, and digital ecosystem integration. Regulatory complexity under the EU Medical Device Regulation has raised barriers to entry, favoring established firms with robust quality management systems and post-market surveillance infrastructure. Differentiation hinges on waveform sophistication, adaptive capabilities, and seamless clinician-patient interfaces. While implantable segments remain dominated by incumbents, external neuromodulation has attracted agile startups, prompting larger players to pursue partnerships or acquisitions. Geographic disparities in reimbursement and specialist availability further shape competitive tactics, with companies customizing market access strategies by country. Overall, innovation velocity and health economic validation are the decisive factors in maintaining leadership across Europe’s heterogeneous healthcare environments.

KEY MARKET PLAYERS

The leading companies operating in the Europe neurostimulation devices market include:

- Abbott Laboratories

- Aleva Neurotherapeutics SA

- Boston Scientific Corporation

- ElectroCore Inc.

- EndoStim Inc.

- Medtronic plc

- Nevro Corporation

- Neuronetics Inc.

- NeuroSigma, Inc.

- Synapse Biomedical Inc.

TOP PLAYERS IN THE MARKET

- Medtronic is a global pioneer in neurostimulation technologies with a strong footprint across Europe. The company offers a comprehensive portfolio covering spinal cord stimulation, deep brain stimulation, and sacral nerve stimulation systems. Medtronic has consistently advanced therapeutic precision through innovations such as adaptive stimulation and high-frequency waveforms. In recent years, it has strengthened its position by expanding clinical evidence generation through multicenter European trials and enhancing digital integration with remote programming platforms. The company also collaborates closely with regulatory and reimbursement bodies across EU member states to facilitate early adoption of next-generation devices, ensuring sustained access for patients and providers throughout the region.

- Boston Scientific has emerged as a formidable force in the European neurostimulation landscape through its differentiated spinal cord stimulation platforms. The company’s focus on patient-centric waveform technologies like BurstDR and its miniaturized implantable pulse generators has garnered significant clinical interest. Boston Scientific actively engages in health technology assessment processes across Western and Northern Europe to secure reimbursement. In 2024, it launched a pan-European digital support program for chronic pain patients, integrating wearable sensors with its stimulation systems. This initiative reinforces its commitment to outcomes-driven care and positions the company as a leader in integrated neuromodulation solutions within the region.

- Abbott Laboratories plays a critical role in Europe’s neurostimulation ecosystem primarily through its advanced spinal cord stimulation offerings. The company emphasizes closed-loop systems that respond in real time to patient physiology, delivering personalized therapy. Abbott has deepened its European presence by investing in training centers for clinicians in Germany, France, and the UK to ensure optimal device programming and patient follow-up. It also partners with academic institutions to validate long-term efficacy in real-world settings. Recent enhancements to its wireless patient controller and cloud-based data analytics platform reflect a strategic pivot toward digital health, reinforcing its relevance in Europe’s evolving value-based care environment.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Key players in the Europe Neurostimulation Devices Market prioritize regulatory and reimbursement alignment as a foundational strategy, actively engaging with national health technology assessment bodies to secure early coverage decisions. They invest heavily in clinical evidence generation through multicenter European trials to demonstrate long-term efficacy and cost-effectiveness. Product differentiation via waveform innovation, miniaturization, and closed-loop algorithms remains central to competitive positioning. Companies also expand digital health capabilities by integrating remote monitoring, cloud analytics, and patient-facing mobile applications. Strategic collaborations with academic medical centers and training programs for implanting physicians further strengthen clinical adoption and brand loyalty across diverse European healthcare systems.

MARKET SEGMENTATION

This Europe neurostimulation devices market research report is segmented and sub-segmented into the following categories.

By Technology

- Internal

- External

By Application

- Spinal Cord Stimulation

- Deep Brain Stimulation

- Sacral Nerve Stimulation

- Gastric Electrical Stimulation

- Transcutaneous Electrical Nerve Stimulation

- Transcranial Magnetic Stimulation

- Respiratory Electrical Stimulation

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

1. What is the size of the Europe neurostimulation devices market?

The Europe neurostimulation devices market reached USD 5.62 billion in 2025, projected to hit USD 18.80 billion by 2025-2033. Growth reflects pain management demand.

2. What drives growth in the Europe neurostimulation devices market?

Chronic pain prevalence, aging populations, and minimally invasive options propel the Europe neurostimulation devices market. Reimbursement improvements accelerate adoption.

3. Who are key players in the Europe neurostimulation devices market?

Leaders in the Europe neurostimulation devices market include Medtronic, Boston Scientific, Abbott, LivaNova, and Nevro. They dominate SCS and DBS innovations.

4. Which countries dominate the Europe neurostimulation devices market?

Germany leads the Europe neurostimulation devices market, followed by UK and France via advanced neurology centers.

5. What is SCS in the Europe neurostimulation devices market?

Spinal cord stimulation holds largest share in the Europe neurostimulation devices market for failed back surgery syndrome.

6. How does chronic pain impact the Europe neurostimulation devices market?

Chronic pain drives 60% demand in the Europe neurostimulation devices market through refractory case treatments.

7. What trends shape the Europe neurostimulation devices market?

Closed-loop and MR-compatible devices trend in the Europe neurostimulation devices market for better outcomes.

8. Is DBS prominent in the Europe neurostimulation devices market?

Deep brain stimulation grows in the Europe neurostimulation devices market for Parkinson's and dystonia.

9. How competitive is the Europe neurostimulation devices market?

Oligopolistic competition defines the Europe neurostimulation devices market with high R&D barriers.

10. What role does pain management play in the Europe neurostimulation devices market?

Pain neuromodulation captures majority revenue in the Europe neurostimulation devices market via opioid alternatives.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com