Europe Olive Market Size, Share, Growth, Trends & Analysis Report, Segmented By Product, Application, By Country (Germany, U.K., Italy, France, Spain, Switzerland, Russia, Turkey, Belgium, Netherlands, Rest of Europe), Industry Analysis From (2026 to 2034)

Europe Olive Market Report Summary

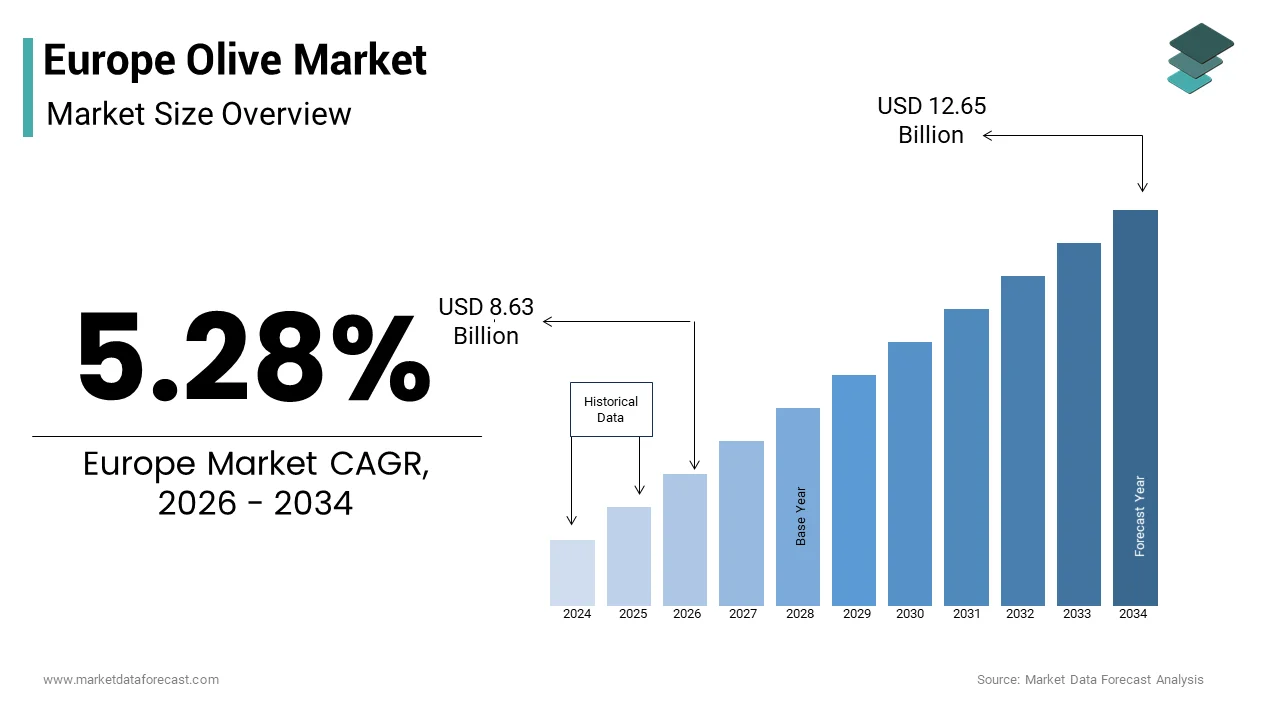

The Europe olive market was valued at USD 8.19 billion in 2025, is estimated to reach USD 8.63 billion in 2026, and is projected to reach USD 12.65 billion by 2034, growing at a CAGR of 5.28% during the forecast period from 2026 to 2034. The Europe olive market continues to expand steadily, supported by the region's long-standing olive cultivation heritage, strong domestic consumption, and rising global demand for premium olive-based products. Increasing consumer preference for healthy diets, particularly the Mediterranean dietary pattern, has significantly boosted the consumption of olives and olive oil across food, beverage, and culinary applications. Growing awareness of the nutritional benefits of olives, including their healthy fats, antioxidants, and anti-inflammatory properties, is further stimulating market growth. Additionally, product innovation, expansion of organic olive farming, premium extra virgin olive oil offerings, and increasing exports from major producing countries are strengthening Europe's position as the global leader in olive production and processing.

Key Market Trends

- Premium extra virgin olive oil continues to witness strong demand as consumers increasingly prioritize quality, authenticity, and nutritional value.

- Organic olive cultivation is expanding across Europe, supported by sustainable farming initiatives and growing consumer interest in clean-label food products.

- Producers are investing in traceability, geographical indication certifications, and premium branding to strengthen product differentiation in domestic and export markets.

- Rising adoption of olives and olive oil in functional foods, gourmet cuisine, and health-focused diets is creating new consumption opportunities.

- Sustainable production practices, water-efficient cultivation techniques, and eco-friendly packaging are becoming important competitive priorities for olive producers.

Segmental Insights

Based on product, the olive oil segment held the largest share of the Europe olive market in 2025. The segment's leadership is driven by widespread household consumption, growing demand for premium extra virgin olive oil, expanding culinary applications, and increasing recognition of its nutritional and health benefits.

Based on application, the food and beverage segment accounted for the dominant share of the Europe olive market in 2025. Olives and olive-derived products remain essential ingredients across cooking, food processing, bakery, sauces, dressings, and ready-to-eat meal categories, supporting the segment's continued market leadership.

Regional Insights

Spain remained the leading contributor to the Europe olive market in 2025, supported by its extensive olive cultivation area, world-leading olive oil production capacity, and strong export performance. Italy secured the second-largest market position, benefiting from its internationally recognized premium olive oil brands, regional specialties, and strong domestic consumption. Greece continues to maintain a notable market share owing to its high per capita olive oil consumption and reputation for producing premium extra virgin olive oil. France remains an important market driven by demand for high-quality regional olive products protected by geographical indication certifications, while Germany is expected to register steady growth during the forecast period due to increasing consumer awareness of healthy dietary habits and rising imports of premium olive products.

Competitive Landscape

The Europe olive market is characterized by the presence of well-established olive growers, processors, and international food companies competing through product quality, geographical authenticity, sustainable production, and premium brand positioning. Leading manufacturers are investing in organic cultivation, advanced processing technologies, quality certification programs, and environmentally responsible farming practices to strengthen their market presence. Strategic expansion into export markets, product portfolio diversification, and investments in value-added olive products such as flavored oils, specialty olives, and functional food ingredients are further enhancing competitiveness. Companies are also leveraging digital marketing, direct-to-consumer sales channels, and premium packaging innovations to reach health-conscious consumers across global markets. As demand for natural, nutritious, and sustainably produced food products continues to rise, innovation, traceability, and product authenticity will remain central to long-term growth in the Europe olive market.

Prominent players in the Europe olive market include Cargill, Incorporated (U.S.), Deoleo (Spain), Aceites del Sur, Del Monte Foods, Inc. (U.S.), Gallo Worldwide (U.S.), Grupo SOS, Borges International Group, S.L.U. (Spain), Sovena (Portugal), Sun Grove Foods Inc. (U.S.), EU Olive Oil Ltd. (UK), Artajo Oil (Spain), Salov Group (Italy), Aceites Sandúa (Spain), Tucan Olive Oil Company Ltd. (UK), Domenico Manca S.p.A. (Italy), Les Huiles d'Olive Lahmar (Tunisia), Grampians Olive Co. (Australia), Victorian Olive Groves (Australia), Gourmet Foods Inc. (U.S.), Olive Line International S.L., Chrisnas Olives, and Agrotiki S.A.

Europe Olive Market Size

The Europe olive market size was valued at USD 8.19 billion in 2025 and is anticipated to reach USD 8.63 billion in 2026 to reach USD 12.65 billion by 2034, growing at a CAGR of 5.28% during the forecast period from 2026 to 2034.

Current Market Overview and Definition

The olive forms a cornerstone of the continent's agricultural heritage and dietary patterns. This market is predominantly concentrated in the Mediterranean basin, where climatic conditions favor the growth of Olea europaea, yet its influence extends across Northern and Central Europe through robust trade networks and evolving consumer preferences. The cultural significance of olives is deeply embedded in European gastronomy, serving as a staple ingredient in traditional cuisines and a symbol of healthy living. As per the European Commission, the European Union accounts for approximately 68% of global olive oil production, while global grove distribution is concentrated heavily across the broader Mediterranean basin rather than the EU alone. As per Eurostat, the European Union is home to over 500 million olive trees, with Spain, Italy, and Greece driving the vast majority of the continent's planted area and agricultural output. According to Eurostat, the total utilized agricultural area under olive tree cultivation in the European Union stands at approximately 4.6 million hectares, spanning across key Mediterranean member states. Beyond production, the market is characterized by a strong emphasis on quality differentiation, with Protected Designation of Origin labels playing a crucial role in value addition. Consumer awareness regarding the health benefits of monounsaturated fats and polyphenols has elevated olives from a culinary condiment to a functional food item. Regulatory frameworks within the EU strictly govern labeling and quality standards, ensuring transparency and protecting geographical indications. This regulatory environment supports premiumization while maintaining high safety standards for both domestic consumption and export markets.

MARKET DRIVERS

Rising Health Consciousness and Adoption of Mediterranean Diet Protocols

The escalating adoption of the Mediterranean diet across the region accelerates the growth of the Europe Olive Market. This is fueled by widespread medical endorsement and public health campaigns promoting cardiovascular health. Nutritional guidelines increasingly emphasize the replacement of saturated fats with monounsaturated fats found abundantly in olives and olive oil, positioning them as essential components of a preventive health strategy. According to the World Health Organization Regional Office for Europe, noncommunicable diseases account for approximately 90% of all deaths in the European Region, heavily driving regional public health initiatives to advocate for healthy Mediterranean-style dietary patterns. Clinical studies have consistently demonstrated that regular consumption of olives improves lipid profiles and reduces inflammation, leading to increased recommendation by healthcare professionals. This medical validation has transcended traditional Mediterranean countries, driving demand in Northern and Eastern European nations where olive consumption was historically lower. Supermarkets in countries like Germany and Sweden have expanded their olive sections to include diverse varieties and functional formats such as pitted, stuffed, and organic options. The trend toward clean eating and whole foods further amplifies this demand, as consumers seek minimally processed ingredients with recognized health benefits. Educational initiatives by nutritionists and dietitians highlight the role of olives in weight management and metabolic health, reinforcing their status as a superfood. This shift is not merely a fleeting trend but a structural change in eating habits, supported by long term public health policies. The resulting increase in per capita consumption creates a stable and growing demand base for high quality olive products across the continent.

Expansion Of Premium and Organic Segments in Retail Channels

The rapid expansion of premium and organic olive segments in regional retail channels drives the expansion of the Europe olive market. This caters to discerning consumers who prioritize quality, sustainability, and ethical sourcing. As disposable incomes rise and food literacy improves, shoppers are increasingly willing to pay a premium for certified organic olives and those with Protected Designation of Origin status. As per the Research Institute of Organic Agriculture (FiBL), total organic retail sales in the broader European market surpassed 58 billion euros, showing a continuous upward consumer trajectory for premium food categories like extra virgin and organic olive oil. Retailers are responding to this demand by dedicating more shelf space to specialty olive products, offering detailed information on origin, cultivar, and harvesting methods. The proliferation of gourmet food stores and online specialty retailers has made niche olive varieties accessible to a broader audience, fostering experimentation and brand loyalty. Consumers are particularly attracted to single estate oils and table olives that offer unique flavor profiles and traceability, distinguishing them from mass produced commodities. Marketing campaigns emphasizing biodiversity conservation and traditional harvesting techniques resonate with environmentally conscious buyers, enhancing the perceived value of premium products. Furthermore, the integration of olives into ready to eat meals and artisanal snack boxes introduces them to new consumer segments seeking convenience without compromising on quality. This premiumization trend encourages producers to invest in sustainable practices and quality improvement, creating a virtuous cycle of higher value and better standards. The focus on authenticity and terroir strengthens the competitive advantage of European olives in the global marketplace.

MARKET RESTRAINTS

Climate Change Induced Water Scarcity And Yield Volatility

The increasing frequency and severity of droughts caused by climate change directly impact water availability and crop yields, which inhibit the growth of the Europe olive market. Olive trees are traditionally drought tolerant, but prolonged periods of extreme heat and insufficient rainfall during critical flowering and fruit setting stages can lead to substantial production losses. According to the European Drought Observatory, large parts of Southern Europe experienced severe to exceptional drought conditions in recent years, affecting millions of hectares of agricultural land including olive groves. In regions like Andalusia in Spain and Apulia in Italy, water restrictions have forced farmers to reduce irrigation, resulting in smaller fruit size and lower oil content. This volatility disrupts supply chains and leads to price fluctuations that can deter consistent consumer purchasing. The unpredictability of harvests makes it difficult for producers to plan long term investments and maintain stable contracts with buyers. Furthermore, changing temperature patterns may alter the suitability of traditional growing regions, potentially requiring costly adaptation measures such as switching to more resilient varieties or implementing advanced irrigation systems. Small scale farmers, who constitute a significant portion of the sector, often lack the financial resources to implement these adaptations, making them particularly vulnerable to climate shocks. The cumulative effect of consecutive poor harvests can lead to abandonment of groves, reducing the overall productive capacity of the region. This environmental pressure threatens the long term viability of olive cultivation in its traditional heartlands, necessitating urgent strategic responses.

Proliferation Of Plant Pathogens and Pest Outbreaks

The spread of devastating plant pathogens, particularly Xylella fastidiosa, is a severe constraint to the Europe olive market. This threatens the health and productivity of olive trees across multiple countries. This bacterial disease, transmitted by insect vectors, causes olive quick decline syndrome, leading to leaf scorch, branch dieback, and eventual tree death. According to the European Food Safety Authority, Xylella fastidiosa has been detected in several EU member states including Italy, France, and Spain, affecting thousands of hectares of olive orchards and prompting strict containment measures. Infected trees must be removed and destroyed to prevent further spread, resulting in significant economic losses for farmers and disruption of local economies dependent on olive production. The implementation of quarantine zones restricts the movement of plant material, complicating trade and replanting efforts. Farmers face high costs for monitoring, testing, and replacing infected trees, while also dealing with reduced yields from stressed but not yet dead trees. The psychological impact on farming communities is profound, as centuries old groves are lost, eroding cultural heritage and landscape identity. Research into resistant varieties is ongoing, but widespread deployment takes time, leaving the sector vulnerable in the interim. The threat of other pests such as the olive fruit fly, exacerbated by warmer winters, further compounds the challenge. These biological threats require coordinated international action and substantial investment in research and extension services, diverting resources from other areas of development.

MARKET OPPORTUNITIES

Development Of High Density and Super High Density Planting Systems

The adoption of high density and super-high-density planting systems offers a major opportunity for the Europe olive market. This helps to enhance productivity, mechanization, and resource efficiency. Traditional extensive orchards are being replaced or supplemented by intensive systems that allow for higher tree counts per hectare, facilitating mechanical harvesting and reducing labor costs. As per the International Olive Council (IOC), super-high-density planting systems can achieve olive yields multiple times higher, often scaling from two to three times the volume of traditional extensive groves, while drastically reducing ongoing harvesting costs via over-the-row machine automation. This intensification enables farmers to remain competitive in a global market characterized by fluctuating prices and rising input costs. The uniform structure of these orchards allows for the use of specialized machinery for pruning, harvesting, and soil management, addressing the chronic shortage of agricultural labor in rural Europe. Furthermore, high density systems are often designed with integrated drip irrigation and fertigation, optimizing water and nutrient use efficiency, which is crucial in water scarce regions. This technological advancement supports sustainable intensification, allowing for greater output without expanding the agricultural footprint. Younger farmers and agribusinesses are increasingly investing in these modern systems, bringing fresh capital and innovation to the sector. The standardization of fruit quality and ripening in intensive orchards also improves the consistency of processed products, meeting the demands of industrial buyers. This shift towards industrial agriculture models offers a pathway to modernize the sector and improve its resilience against economic and environmental pressures.

Diversification Into Value Added Olive Derivatives and Cosmetics

The diversification of olive production into value-added derivatives such as cosmetics, pharmaceuticals, and bioenergy paves the way to maximize revenue and reduce waste, which is anticipated to boost the expansion of the Europe olive market. Olive pomace, leaves, and wastewater, traditionally considered byproducts, are rich in bioactive compounds like hydroxytyrosol and squalene, which are highly valued in the cosmetic and nutraceutical industries. According to sources, the global natural cosmetics market is growing rapidly, with European brands increasingly incorporating olive derived ingredients for their antioxidant and moisturizing properties. Extracting these compounds creates new revenue streams for producers, improving the overall economics of olive farming and promoting a circular economy approach. Additionally, olive biomass can be used for bioenergy production, providing renewable energy for farm operations and reducing dependency on fossil fuels. The development of innovative products such as olive leaf tea, supplements, and skincare lines appeals to health and beauty conscious consumers, expanding the market beyond culinary applications. Collaborations between agricultural cooperatives and research institutions are driving innovation in extraction technologies, making these processes more efficient and cost effective. This diversification reduces reliance on volatile olive oil and table olive prices, stabilizing farmer incomes. It also enhances the sustainability profile of the sector by utilizing all parts of the crop, minimizing environmental impact. The growing consumer interest in natural and sustainable personal care products supports this expansion, creating a robust demand for high quality olive extracts.

MARKET CHALLENGES

Labor Shortages and Aging Farmer Demographics

Persistent labour shortages and an aging demographic among farmers are causing a critical challenge in the Europe olive market. Ultimately, this situation threatens the continuity of traditional cultivation practices. : According to Eurostat, the vast majority of agricultural managers in the EU are over 55 years old, with more than one-third of all farm managers crossing the 65-year threshold, highlighting an acute labor deficit in traditional olive farming communities where younger demographics remain scarce. This demographic shift leads to a loss of traditional knowledge and skills essential for managing complex orchards, particularly in mountainous or terraced areas where mechanization is difficult. The reliance on seasonal migrant labor for harvesting is becoming increasingly unreliable due to changing immigration policies and competition from other sectors. Labor shortages result in delayed harvesting, which can negatively impact oil quality and fruit integrity, leading to lower market values. The physical demanding nature of olive harvesting discourages younger generations from pursuing farming careers, exacerbating the succession crisis. Without adequate labor, many small holdings risk abandonment, leading to landscape degradation and loss of biodiversity. Addressing this challenge requires significant investment in mechanization, training programs, and policies that make farming more attractive to youth. However, the transition to mechanized systems is not feasible for all terrains, leaving many traditional groves vulnerable. This structural issue undermines the social fabric of rural communities and the long-term sustainability of the olive sector.

Market Fragmentation and Lack of Supply Chain Coordination

The fragmentation of the olive supply chain, characterized by a large number of small-scale producers and weak coordination among stakeholders, is a significant challenge to the efficiency and competitiveness of the Europe olive market. The majority of olive farms in Europe are small family-owned holdings, which limits their bargaining power and ability to invest in modern technologies or marketing initiatives. According to surveys, over 60% of olive farms in the EU are less than 5 hectares in size, leading to dispersed production and inconsistent quality standards. This fragmentation hinders the formation of strong cooperatives or producer organizations that could negotiate better prices and streamline logistics. The lack of coordination results in inefficiencies in processing, storage, and distribution, increasing costs and reducing profitability. Small producers often sell their harvest to intermediaries at low prices, capturing only a small fraction of the final retail value. The absence of unified branding and marketing strategies weakens the position of European olives against competitors from other regions who operate with greater scale and coordination. Improving supply chain integration requires significant effort in building trust, standardizing practices, and fostering collaboration among diverse actors. Without stronger collective action, the sector remains vulnerable to price volatility and market pressures, limiting its potential for growth and innovation. Enhancing organizational structures is essential to improve resilience and value capture for producers.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 5.28% |

| Segments Covered | By Product, Application, And By Country |

| Various Analyses Covered | Global, Regional & Country Level Analysis; Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic & Rest of Europe |

| Market Leaders Profiled | Cargill, Incorporated (U.S.), Deoleo (Spain), Aceites del Sur, Del Monte Foods, Inc. (U.S.), Gallo Worldwide (U.S.), Grupo SOS, Borges International Group, S.L.U. (Spain), Sovena (Portugal), Sun Grove Foods Inc. (U.S.), EU Olive Oil Ltd (UK), Artajo Oil (Spain), Salov Group (Italy), Aceites Sandúa (Spain), Tucan Olive Oil Company Ltd (UK), Domenico Manca S.p.a. (Italy), Les Huiles d'Olive Lahmar (Tunisia), Grampians Olive Co. (Australia), Victorian Olive Groves (Australia), Gourmet Foods Inc. (U.S.), Olive Line International S.L., Chrisnas Olives, Agrotiki S.A. |

SEGMENTAL ANALYSIS

By Product Insights

Olive Oil

The olive oil segment led the Europe olive market and captured a significant share in 2025. This dominance of the segment was driven by its entrenched status as a culinary staple and essential ingredient in daily cooking across the continent. Unlike table olives which are often consumed as snacks or appetizers, olive oil is used extensively for frying, sautéing, dressing salads, and baking, resulting in significantly higher volume consumption. According to the International Olive Council (IOC), the average annual per capita consumption of olive oil varies dramatically in the European Union, spiking to over 11 to 12 kilograms per person in core producing nations like Greece and Spain, maintaining a distinct market leadership far exceeding table olives. This high usage rate is driven by the deep cultural integration of olive oil in Mediterranean cuisines, which have gained global popularity and influence dietary habits in Northern and Central Europe. The versatility of olive oil allows it to replace other vegetable oils and fats in a wide variety of recipes, making it indispensable in both household and commercial kitchens. Restaurants and food service providers heavily rely on olive oil for its flavor profile and health credentials, further boosting demand. The widespread availability of olive oil in various grades, from extra virgin to refined, ensures accessibility for different budget segments and culinary applications. This ubiquitous presence in the food chain secures its dominance over table olives, which remain a more niche product. The consistent demand for cooking oil ensures steady market growth and revenue generation for producers and retailers alike.

The prominence of this segment is further reinforced by robust scientific evidence supporting its role in cardiovascular protection and overall health maintenance. Medical professionals and nutritionists consistently recommend olive oil as a primary source of healthy monounsaturated fats, which help reduce bad cholesterol levels and lower the risk of heart disease. According to the European Society of Cardiology, diets rich in olive oil are associated with a significant reduction in cardiovascular mortality, prompting widespread adoption among health-conscious consumers. The high content of polyphenols and antioxidants in extra virgin olive oil provides additional anti-inflammatory benefits, appealing to individuals seeking preventive health measures. This medical endorsement has transformed olive oil from a mere cooking ingredient into a functional food item, driving premiumization and increased consumption. Public health campaigns across Europe emphasize the benefits of the Mediterranean diet, with olive oil as its cornerstone, influencing consumer purchasing decisions. The availability of certified high phenolic olive oils caters to specific health needs, creating a specialized sub segment within the broader market. Consumers are willing to pay higher prices for oils with verified health claims, supporting value growth. The alignment with wellness trends ensures that olive oil remains the preferred choice for health-oriented individuals, sustaining its leading position in the olive market.

Table Olives

The table olive segment is growing at the highest CAGR of 5.8% due to the increasing consumer preference for convenient, healthy, and savory snacks. As lifestyles become busier, Europeans are seeking ready to eat options that provide nutritional value without requiring preparation, and table olives fit this need perfectly. According to research, the snack food sector in Europe has seen a shift toward healthier alternatives, with nut and olive based snacks gaining significant traction among millennials and Gen Z consumers. Retailers are responding by offering a wider variety of pitted, stuffed, and marinated table olives in portable packaging, making them easy to consume on the go. The versatility of table olives as appetizers in social settings and party platters also contributes to their growing popularity. Food service establishments are incorporating olives into tapas boards and mezze platters, introducing them to new audiences. The availability of diverse flavors such as garlic, herb, and chili infused olives appeals to adventurous palates, driving trial and repeat purchases. The convenience factor combined with the perception of olives as a wholesome snack supports rapid market expansion. This trend is particularly strong in urban areas where health conscious snacking is prevalent. The growth of online grocery shopping further facilitates access to specialty table olive products, expanding the customer base beyond traditional retail channels.

The quick growth of this segment is boosted by the expansion of gourmet and artisanal varieties that cater to discerning consumers seeking unique sensory experiences. Producers are moving beyond standard green and black olives to offer rare cultivars, organic options, and traditionally cured products with distinct flavor profiles. According to the International Olive Council, European consumer appetite for geographic-specific, gourmet, and premium table olive varieties continues to expand, driven by an accelerating retail premium placed on regional origin labeling and artisanal authenticity. Consumers are increasingly interested in the origin and production methods of their food, driving demand for Protected Designation of Origin labeled olives from specific regions in Spain, Italy, and Greece. Gourmet food stores and specialty delis are dedicating more space to these high end products, often providing tasting opportunities to educate customers. The trend toward foodie culture and culinary exploration encourages consumers to experiment with different olive types, such as Kalamata, Manzanilla, and Niçoise. Social media influencers and food bloggers play a crucial role in highlighting these artisanal products, creating buzz and driving demand. The premium positioning of gourmet olives allows for higher profit margins, incentivizing retailers and producers to invest in this segment. The focus on craftsmanship and tradition resonates with consumers who value sustainability and ethical sourcing. This shift toward premiumization ensures sustained growth and diversification of the table olive market.

By Application Insights

Food And Beverage

The Food and Beverage segment dominated the Europe olive market and accounted for a substantial share in 2025. Olives and olive oil are fundamental ingredients in both traditional Mediterranean dishes and modern culinary creations. The vast majority of olive production is directed toward human consumption in the form of cooking oil, salad dressings, marinades, and direct eating. As per the International Olive Council, the food and beverage industry consumes the absolute majority of global olive yields, accounting for roughly 90% or more of total output allocated directly to consumer culinary oils and raw food preparations. The versatility of olives allows them to be integrated into a wide range of products, from pasta sauces and pizzas to sandwiches and salads. The food service sector, including restaurants, cafes, and catering services, relies heavily on olive products for menu development, driving bulk demand. The rise of home cooking trends during recent years has further boosted household consumption of olive ingredients. Consumer familiarity and acceptance of olives as a standard pantry item ensure consistent and high-volume demand. The integration of olives into processed foods such as crackers, breads, and ready meals expands their application scope beyond fresh consumption. This broad usage across various food categories solidifies the dominance of the Food and Beverage segment. The cultural significance of olives in European gastronomy ensures their continued relevance and high consumption levels.

The supremacy of the Food and Beverage segment is further supported by extensive industrial processing and the development of value added olive products. Manufacturers are innovating with olive based ingredients to create new product lines that appeal to changing consumer preferences. Olive oil is used as a key ingredient in mayonnaise, sauces, and dressings, while table olives are incorporated into spreads, pâtés, and stuffed snacks. According to studies, the processed food sector in Europe is increasingly adopting clean label ingredients, with olive oil replacing synthetic additives and less healthy fats. This shift drives demand for high quality olive inputs from food manufacturers. The development of olive-based beverages, such as olive leaf tea and olive juice, introduces new applications for olive derivatives. Food technologists are exploring ways to enhance the stability and functionality of olive ingredients in various formulations. The scalability of industrial processing allows for mass production and distribution, reaching a wide consumer base. Collaborations between olive producers and food companies lead to co branded products that leverage the health halo of olives. This industrial integration ensures a steady and large scale demand for olive products, reinforcing the leadership of the Food and Beverage segment. The continuous innovation in food applications keeps the segment dynamic and growing.

Personal Care and Cosmetics

The Personal Care and Cosmetics segment is anticipated to witness the fastest CAGR of 7.2% during the forecast period owing to the surging demand for natural and organic skincare ingredients. Consumers are increasingly avoiding synthetic chemicals in their beauty routines, turning to plant based alternatives like olive oil and olive leaf extracts for their nourishing and protective properties. As per Cosmetics Europe (the successor to COLIPA), premium skincare formulations are displaying sustained integration of olive-sourced oleic acids, squalane, and active extracts due to their highly stable moisturizing performance. Olive oil is rich in squalene, vitamin E, and polyphenols, which help hydrate skin, reduce signs of aging, and protect against environmental damage. Beauty brands are formulating creams, serums, lotions, and hair care products with olive extracts to appeal to health conscious buyers. The certification of olive based cosmetic ingredients as organic and eco friendly enhances their appeal to ethical consumers. The transparency of sourcing and the sustainability of olive cultivation align with the values of the clean beauty movement. This trend is supported by marketing campaigns that highlight the historical use of olives in beauty rituals. The effectiveness of olive ingredients in improving skin health drives consumer loyalty and repeat purchases. The shift toward natural personal care ensures sustained growth for this segment.

The rapid growth of the Personal Care and Cosmetics segment is fueled by innovation in bioactive extraction technologies and the development of premium formulations. Advances in extraction methods allow for the isolation of high potency compounds from olive leaves, pomace, and fruit, such as hydroxytyrosol and oleuropein, which offer superior anti aging and anti-inflammatory effects. According to research, the demand for high performance natural actives in cosmetics is rising, with olive extracts gaining recognition for their efficacy compared to synthetic alternatives. Cosmetic companies are investing in research to stabilize these bioactives and enhance their penetration into the skin. The creation of luxury skincare lines featuring rare olive varieties and cold pressed oils commands higher price points and attracts affluent consumers. The integration of olive ingredients into men’s grooming products and baby care items expands the target audience. Collaborations between agricultural cooperatives and cosmetic laboratories ensure the supply of high quality raw materials. The emphasis on sustainability and circular economy principles, by utilizing olive byproducts, enhances brand image and appeals to environmentally conscious buyers. This technological and product innovation drives differentiation and growth in the competitive cosmetics market. The perceived value of olive based premium products supports margin expansion and market penetration.

COUNTRY LEVEL ANALYSIS

Spain Olive Market Analysis

Spain outperformed other counties in the Europe olive market and accounted for a commanding share in 2025. Additionally, it operates as the world’s leading producer and exporter of both olive oil and table olives. As per the European Commission Directorate-General for Agriculture and Rural Development, Spain's vast olive groves, particularly in Andalusia, contribute significantly to global supply, with Spain historically accounting for up to 63% to 70% of the EU’s total olive oil production rather than just half. According to the Ministry of Agriculture, Fisheries and Food of Spain, the country produced only around 663,000 tons of olive oil in the historical 2022/2023 campaign, as severe climate challenges and drought cut normal outputs roughly in half. Spanish producers are leaders in high density planting systems and mechanized harvesting, enhancing efficiency and competitiveness. The domestic market is characterized by high per capita consumption, with olives being a staple in daily meals. Spain is also a major hub for olive oil blending and bottling, exporting branded products worldwide. The government supports the sector through subsidies for sustainable practices and irrigation modernization. Spanish companies are actively investing in quality certification and branding to differentiate their products in premium markets. The country’s strategic location facilitates trade with North Africa and the Americas. Spain’s dominance is underpinned by its scale, technology, and established export networks. The focus on innovation and sustainability ensures its continued leadership in the European olive sector.

Italy Olive Market Analysis

Italy was the next prominent country in the Europe olive market and captured a significant share in 2025. It is renowned for its high-quality extra virgin olive oils and diverse table olive varieties. Although production volumes are lower than Spain, Italy commands premium prices due to its strong brand reputation and Protected Designation of Origin labels. According to ISMEA, the Italian agricultural market institute, the value of Italian olive oil exports reached record levels in recent years, driven by demand for authentic and high-quality products. Italian consumers are highly discerning, prioritizing sensory qualities and origin authenticity. The country is a major importer of bulk olive oil for blending and re export, leveraging its branding expertise. Italy leads in organic olive production, catering to the growing demand for sustainable and chemical free products. The tourism sector boosts local olive oil sales, with visitors purchasing directly from estates. Italian researchers are at the forefront of combating Xylella fastidiosa, developing resistant varieties and containment strategies. The strong cooperative structure supports small scale farmers in accessing markets and technology. Italy’s focus on quality over quantity distinguishes its market position. The emphasis on culinary heritage and gastronomy drives domestic and international demand. Italy remains a key influencer in setting global standards for olive quality.

Greece Olive Market Analysis

Greece holds a notable share in the Europe olive market due to its high per capita consumption and production of premium Extra Virgin Olive Oil. As per Recomed (Mediterranean Olive Oil Cities Network), Greece is the third largest olive oil producer in the EU, with over 80% of its output classified as extra virgin due to ideal microclimates and optimal cultivation practices rather than traditional pressing methods. According to the European Commission, Greece maintains the highest per capita olive oil consumption globally, historical estimates reaching up to 12 to 18 kilograms annually per person, reflecting deep cultural and dietary integration. Greek olives are prized for their robust flavor and high polyphenol content, appealing to health conscious consumers. The sector is dominated by small family farms, which preserve traditional practices but face challenges in scaling and modernization. Greece is a major exporter of table olives, particularly the Halkidiki variety, which is popular globally. The government is promoting organic farming and geographical indications to enhance value. Climate change poses a significant threat to Greek production, prompting investments in water management. The strong domestic demand provides a stable base for producers. Greece’s reputation for quality and authenticity supports its premium positioning. The focus on preserving heritage while adopting modern techniques defines its market strategy.

France Olive Market Analysis

France is also a promising player in the Europe olive market. It is known for its regional specialties and Protected Designation of Origin oils. Production is concentrated in Provence, Corsica, and the Rhône Valley, where specific cultivars produce distinctively flavored oils. According to the French Ministry of Agriculture, French olive oil production is modest but highly valued for its quality and terroir characteristics . French consumers are increasingly interested in local and artisanal products, driving demand for domestically produced oils. The country is a significant importer of olive oil to meet domestic demand, which exceeds local production. France is a leader in organic olive cultivation, with a growing number of certified estates. The culinary reputation of French cuisine enhances the prestige of its olive products. Tourism plays a vital role in direct sales and brand building. French researchers are actively working on disease resistance and climate adaptation. The market is characterized by high prices and strong brand loyalty. France’s focus on quality and sustainability aligns with premium market trends. The emphasis on regional identity strengthens its competitive advantage.

Germany Olive Market Analysis

Germany is expected to grow further in the Europe olive market during the forecast period. It holds a significant position as a major importer and consumer of olive products in Northern Europe. This is despite having negligible domestic production. The country is one of the largest markets for olive oil in the EU, driven by rising health consciousness and the popularity of the Mediterranean diet. According to the German Federal Office for Agriculture and Food, olive oil imports have steadily increased, with consumers preferring extra virgin and organic varieties. German retailers have expanded their offerings to include a wide range of olive products, from basic cooking oils to gourmet table olives. The strong purchasing power of German consumers supports the premium segment. Health campaigns and nutritional advice promote olive oil as a healthy fat alternative. The country serves as a distribution hub for olive products entering Central and Eastern Europe. German companies are involved in blending, bottling, and distributing olive oils under private labels. The demand for sustainable and ethically sourced products is high. Germany’s market dynamics are driven by consumer education and retail innovation. The lack of domestic production makes it entirely dependent on imports, ensuring steady demand for exporters.

COMPETITIVE LANDSCAPE

The competition in the Europe olive market is characterized by a mix of large multinational corporations, regional cooperatives, and niche artisanal producers who vie for dominance through quality branding and supply chain efficiency. The market exhibits moderate fragmentation with established players holding strong positions in specific segments such as premium extra virgin oil or bulk commodity trading. Key competitors distinguish themselves through authentic origin stories, certified sustainability practices, and innovative product formulations rather than price alone. The barrier to entry remains relatively high for new brands due to the capital intensity of production and the strength of existing geographical indications. Companies invest significantly in marketing and consumer education to differentiate their offerings in a crowded marketplace. Brand reputation and trust are critical assets as consumers become more knowledgeable about quality indicators and production methods. Strategic alliances with retailers and distributors enhance market penetration and shelf presence. The competitive landscape is further shaped by the growing demand for organic and eco friendly products which forces players to adopt rigorous environmental standards. Innovation in packaging and digital engagement serves as a key differentiator. Overall the market rewards companies that can combine traditional authenticity with modern transparency and customer centricity.

KEY MARKET PLAYERS

A few of the market players that are in the Europe olive market are

- Cargill, Incorporated (U.S.)

- Deoleo (Spain)

- Aceites del Sur

- Del Monte Foods, Inc. (U.S.)

- Gallo Worldwide (U.S.)

- Grupo SOS

- Borges International Group, S.L.U. (Spain)

- Sovena (Portugal)

- Sun Grove Foods Inc. (U.S.)

- EU Olive Oil Ltd (UK)

- Artajo Oil (Spain)

- Salov Group (Italy)

- Aceites Sandúa (Spain)

- Tucan Olive Oil Company Ltd (UK)

- Domenico Manca S.p.a. (Italy)

- Les Huiles d'Olive Lahmar (Tunisia)

- Grampians Olive Co. (Australia)

- Victorian Olive Groves (Australia)

- Gourmet Foods Inc. (U.S.)

- Olive Line International S.L.

- Chrisnas Olives

- Agrotiki S.A

Top Players In The Market

- Deoleo operates as a global leader in the olive oil sector with a significant footprint across European markets through its portfolio of premium brands including Carbonell, Bertolli, and Carapelli. The company focuses on delivering high quality extra virgin olive oils that cater to diverse consumer preferences for health and culinary excellence. Recent actions include the strategic divestment of non core assets to streamline operations and enhance financial stability while investing heavily in digital marketing campaigns to engage younger demographics. Deoleo has strengthened its market position by expanding its sustainable sourcing initiatives and obtaining additional organic certifications to meet growing environmental demands. The company actively collaborates with retailers to develop exclusive private label products, ensuring broad distribution channels. Their commitment to traceability and transparency builds consumer trust in an increasingly scrutinized market. Deoleo continues to innovate with new packaging solutions that preserve freshness and reduce plastic waste. This holistic approach ensures long term competitiveness and brand loyalty in the dynamic European landscape.

- Grupo SOS is a prominent Spanish agri food company with a strong presence in the European olive oil and table olive segments through well recognized brands such as Coosur and La Española. The company leverages its vertical integration from orchard to shelf to ensure consistent quality and supply chain efficiency. Recent strategic initiatives include significant investments in modernizing production facilities to improve extraction yields and product purity. Grupo SOS has strengthened its position by launching innovative flavored olive oils and gourmet table olive ranges that appeal to adventurous consumers seeking unique taste experiences. The company actively participates in international trade fairs to showcase its premium offerings and build relationships with key distributors. Their focus on sustainability is evident in water conservation projects and renewable energy adoption in processing plants. Grupo SOS emphasizes educational campaigns to highlight the health benefits of olives, driving consumer awareness. This combination of quality innovation and ethical practices sustains their relevance in the competitive European market.

- Aceites del Sur is a major cooperative based in Andalusia that plays a crucial role in the European olive oil market by representing thousands of local farmers and producing high volume bulk and branded oils. The company is known for its Jaén Selección brand which exemplifies the quality of Spanish extra virgin olive oil. Recent actions include the expansion of storage capacity and the implementation of advanced quality control systems to maintain superior standards during peak harvest seasons. Aceites del Sur has strengthened its market position by forming strategic alliances with international distributors to increase export volumes to Northern and Central Europe. The cooperative invests in research and development to optimize irrigation techniques and combat climate change impacts on crop yields. Their commitment to fair compensation for members ensures social sustainability and community support. Aceites del Sur actively promotes the cultural heritage of olive growing through tourism and educational programs. This integrated approach supports both economic viability and environmental stewardship in the region.

Major Strategies Used By Key Market Participants

Key players in the Europe olive market employ several strategic approaches to maintain competitiveness and drive growth amidst changing consumer preferences and environmental challenges. Brand differentiation through premiumization and geographical indication labels serves as a primary strategy to command higher prices and build consumer loyalty. Companies invest heavily in sustainable sourcing practices and organic certification to align with environmental values and regulatory requirements. Digital transformation and e commerce expansion enable direct engagement with consumers and broader market reach beyond traditional retail channels. Product innovation including flavored oils and convenient packaging formats addresses evolving lifestyle needs and culinary trends. Strategic partnerships with retailers and food service providers ensure widespread availability and visibility in key markets. Investment in supply chain transparency and traceability technologies builds trust and mitigates fraud risks. Marketing campaigns emphasizing health benefits and Mediterranean heritage educate consumers and stimulate demand. These combined strategies allow participants to navigate volatility and capitalize on the growing appreciation for high quality olive products.

MARKET SEGMENTATION

This research report on the Europe olive market is segmented and sub-segmented into the following categories.

By Product

- Olive Oil

- Table Olive

By Application

- Food & Beverage

- Pharmaceuticals

- Personal Care & Cosmetics

- Others

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

Why is the Europe olive market experiencing steady growth?

The market is expanding due to increasing demand for healthy foods, growing consumption of Mediterranean diets, rising exports, and expanding applications of olives in the food and beverage industry.

What are olives and why are they widely consumed across Europe?

Olives are nutrient-rich fruits valued for their flavor, healthy fats, antioxidants, and versatility in culinary, food processing, and olive oil production applications.

Which product segment accounts for the largest share of the Europe olive market?

Olive oil accounts for the largest market share due to its widespread use in cooking, food processing, and health-conscious consumer diets.

How do olives contribute to a healthy diet?

Olives provide monounsaturated fats, antioxidants, vitamins, and beneficial plant compounds that support heart health, reduce oxidative stress, and promote overall well-being.

What factors are driving the growth of the Europe olive market?

Increasing consumer preference for natural foods, rising demand for premium olive oil, expanding organic farming, and growing exports are driving market growth.

Which industries generate the highest demand for olives and olive-based products?

Food and beverage manufacturers, olive oil producers, restaurants, retail chains, cosmetic companies, and nutraceutical manufacturers are the primary end users.

What trends are shaping the future of the Europe olive market?

Organic olive cultivation, premium extra virgin olive oil, sustainable farming, traceable supply chains, functional foods, and eco-friendly packaging are shaping the market.

How are olive producers improving product quality and sustainability?

Producers are adopting precision agriculture, water-efficient irrigation, sustainable harvesting methods, advanced processing technologies, and certified quality standards.

What challenges could affect the growth of the Europe olive market?

Climate change, olive tree diseases, fluctuating production volumes, labor shortages, and volatile commodity prices could affect market growth.

Which countries are expected to lead the Europe olive market?

Spain leads the market, followed by Italy, Greece, Portugal, and France, owing to their extensive olive cultivation, strong olive oil industries, and established export markets.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com