Europe Online Betting Market Size, Share, Trends, & Growth Forecast Report By Type (Sports Betting, Casinos, Poker Bingo Others), Device and Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic and Rest of Europe), Industry Analysis From 2026 to 2034

Europe Online Betting Market Report Summary

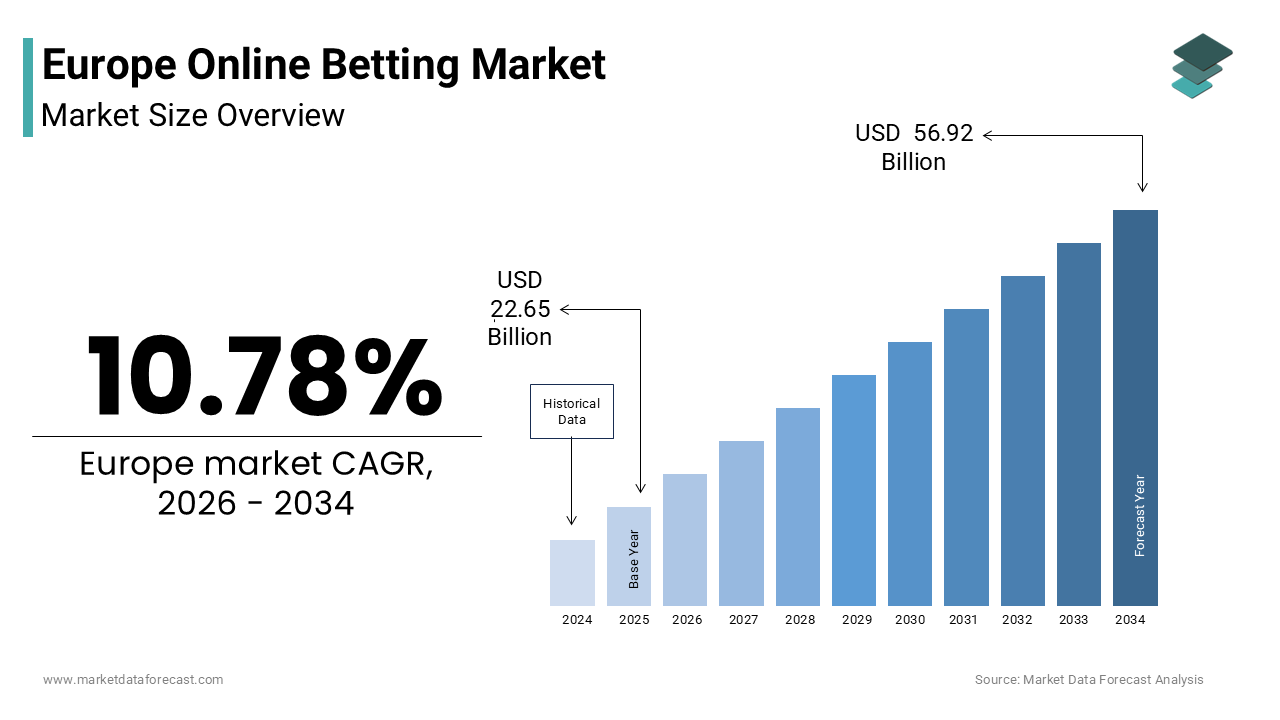

The Europe online betting market was valued at USD 22.65 billion in 2025, is estimated to reach USD 25.10 billion in 2026, and is projected to reach USD 56.92 billion by 2034, growing at a CAGR of 10.78% during the forecast period from 2026 to 2034. The growth of the Europe online betting market is driven by widespread smartphone penetration, high-speed broadband expansion, increasing adoption of mobile-first betting platforms, and the rising popularity of esports and live in-play wagering. Online gambling accounted for a substantial share of total European gambling revenue in 2024, reflecting a structural shift from retail betting shops to digital platforms. The integration of artificial intelligence for dynamic odds calculation, personalized promotions, and responsible gambling monitoring is further transforming the competitive landscape. Although regulatory fragmentation and responsible gaming mandates pose operational challenges, technological innovation and mobile dominance continue to propel long-term market expansion across Europe.

Key Market Trends

-

Rapid shift toward mobile-first betting platforms, with smartphones generating the majority share of online gambling revenue.

-

Strong growth of live in-play betting is supported by real-time data analytics and low-latency streaming.

-

Increasing popularity of esports betting among younger digital-native demographics.

-

Adoption of artificial intelligence for personalized marketing, churn prediction, and risk management.

-

Expansion of licensed regulatory frameworks across major European markets, enhancing consumer trust and tax contributions.

Segmental Insights

- Based on type, the sports betting segment dominated the Europe online betting market with a 52.8% share in 2025, supported by Europe’s strong football culture, year-round sports calendars, and integrated live-stream betting features.

- Based on device, the mobile devices segment held the largest share of the Europe online betting market in 2025, reflecting the dominance of smartphones, app-based wagering, biometric authentication, and integrated mobile payment systems.

Regional Insights

The Europe online betting market exhibits strong regional variation shaped by regulatory frameworks, digital infrastructure, and cultural betting traditions.

-

United Kingdom led the market with 28.6% share in 2025, supported by a mature regulatory regime under the UK Gambling Commission, a strong sports culture, and high digital adoption.

-

Germany accounted for 18.3% of the market share in 2025, driven by regulatory normalization under the State Treaty on Gambling and a large football-centric consumer base.

-

Italy remains a key market, characterized by early digital regulation, strong football and horse racing betting activity, and high mobile penetration.

-

France demonstrates steady growth, supported by regulated sports betting and poker markets alongside strong equestrian betting traditions.

-

Spain is projected to expand considerably, fueled by high mobile usage, La Liga-driven wagering volumes, and consolidation among licensed operators.

Competitive Landscape

The Europe online betting market is highly competitive, featuring multinational gambling groups, regional operators, and digital-native entrants competing across sports betting, casino, and emerging esports verticals. Market leaders focus on mobile optimization, AI-driven personalization, live streaming integration, omnichannel retail-digital convergence, and compliance with country-specific licensing regimes. Intense competition for customer acquisition has elevated marketing costs, prompting firms to emphasize retention strategies and product differentiation. Strategic mergers and acquisitions remain common to secure licenses and expand geographic footprint. Prominent players operating in the Europe online betting market include Flutter Entertainment plc, Entain plc, Bet365 Group Ltd., 888 Holdings plc, Kindred Group plc, Betsson AB, FDJ United, Tipico Group, LeoVegas AB, and William Hill Ltd.

Europe Online Betting Market Size

The Europe online betting market size was valued at USD 22.65 billion in 2025 and is anticipated to reach USD 25.10 billion in 2026 from USD 56.92 billion by 2034, growing at a CAGR of 10.78% during the forecast period from 2026 to 2034.

Online betting (also known as iGaming or iGambling) is the act of placing wagers on the outcome of sports events, casino games, or other uncertain occurrences through digital platforms such as websites and mobile apps. This sector has evolved from simple telephone betting to sophisticated mobile applications utilizing real-time data analytics and live streaming capabilities. The fundamental shift in consumer behavior toward digital engagement defines the current landscape as physical betting shops face declining footfall. According to 2024 data, 60.2% of the EU population aged 16-74 ordered goods or services over the internet, and online gambling is a subset of this, with online gambling revenue accounting for 39% of the total European gambling market in 2024. The penetration of high-speed broadband infrastructure supports this growth. As of the end of 2024, approximately 82.5% of European households had access to fixed very high capacity networks (VHCN), while FTTH (fiber-to-the-home) reached 70.5%. Smartphone usage remains a critical component. Mobile devices are dominant, but EGBA reported they generated 58% of European online gambling gross gaming revenue in 2024, projected to increase to 67% by 2029. The regulatory environment shaped by varying national laws influences how operators license and offer services making compliance a central operational requirement. This market functions as a significant revenue source for many governments through taxation while providing entertainment to millions of users daily. The integration of artificial intelligence for odds calculation and responsible gambling tools further distinguishes the modern European betting landscape from traditional models.

MARKET DRIVERS

Widespread Smartphone Penetration Fuels Mobile Betting Adoption

The ubiquitous presence of smartphones serves as the Driving force behind the growth of the Europe online betting market. Consumers increasingly rely on mobile devices for instant access to betting markets allowing them to place wagers anytime and anywhere which drives unprecedented engagement levels. According to sources, unique mobile subscriber penetration in Europe is very high, with a large majority of the population subscribed to mobile services, and the region is experiencing steady, moderate growth in subscription numbers. This ubiquity ensures that betting operators can reach users during live sporting events thereby increasing in-play betting volumes significantly. The rollout of fifth generation networks has further accelerated this trend by enabling seamless live streaming of matches directly within betting applications without latency issues. 5G network coverage has expanded significantly across Europe, covering a large majority of the population and providing the necessary infrastructure for low-latency digital applications and services. Operators specifically capitalize on this connectivity through push notifications that alert users to odds changes or special promotions instantly. The shift is evident in revenue figures where mobile betting often accounts for a significant share of total online turnover for major operators. As mobile commerce volumes continue to climb the dependency on mobile optimized betting interfaces becomes absolute for business survival. This structural change in device usage patterns guarantees that mobile will remain the dominant channel for betting investment in the foreseeable future.

Growing Popularity of Esports Attracts Younger Demographics

The exponential rise of esports acts as a primary demand driver compelling betting operators to invest heavily in specialized markets tailored to competitive gaming audiences, which further accelerates the expansion of the Europe online betting market. The decline in younger viewership for traditional sports has driven digital-native generations toward competitive gaming, specifically targeting fast-paced titles that facilitate interactive betting. The global esports audience continues to grow, primarily driven by engagement in Asia, while Europe holds a smaller, more mature share of the total audience. This migration of viewer attention necessitates continuous innovation in betting products such as wagering on specific in-game events like first blood or map winners. Operators utilize live data feeds to offer thousands of micro-betting markets per match which offers measurable engagement compared to traditional pre-match wagers. The rise of streaming platforms like Twitch further intensifies interest as viewers watch professional gamers compete in real time while placing bets simultaneously. Esports betting is rapidly growing in popularity across Europe, with a significant increase in betting volume and average bet size, attracting a more engaged audience. This cross-over dynamic encourages operators to adopt gaming-centric marketing strategies to resonate with diverse younger audiences. The need for real-time odds adjustment ensures that trading teams remain active around the clock to manage risk effectively. Consequently, the health of the online betting market is inextricably linked to the vitality of the regional esports ecosystem.

MARKET RESTRAINTS

Stringent Regulatory Frameworks Limit Operational Flexibility

The implementation of rigorous gambling laws acts as a significant restraint on the Europe online betting market. These laws restrict the ability of operators to market freely and offer certain product features across different jurisdictions. Each European nation maintains its own licensing regime with varying rules on advertising bonuses and stake limits which fragments the single market potential. European online gambling operators face a rising, fragmented regulatory burden, requiring them to manage multiple, disparate national licenses and compliance standards. This regulatory pressure has led to bans on credit card betting in several countries including the United Kingdom and Spain which reduces the total addressable market for high rollers. Major advertising restrictions have followed suit with countries like Italy and Germany imposing strict limits on gambling commercials during sports broadcasts. The cost of compliance for gaming operators is significantly high, with regulatory overheads impacting net profits for companies operating in multiple jurisdictions. Operators now face higher barriers to entry and must invest heavily in local compliance teams to navigate complex legal landscapes. The fragmentation of rules across different member states adds complexity for pan-European campaigns requiring legal teams to constantly monitor changes. These constraints reduce the overall efficiency of marketing spend and limit the granularity of promotional offers available to players. The industry continues to grapple with balancing commercial growth against the social responsibility mandates imposed by European governments.

Rising Concerns Over Problem Gambling Impact Brand Reputation

Persistent societal concerns regarding gambling addiction and its harmful effects act as a formidable constraint for the Europe online betting market. This is causing governments to impose stricter controls and consumers to scrutinize operator ethics. When public awareness of gambling harm increases due to media coverage of addiction stories regulators often respond with harsher measures that constrain industry growth. Gambling disorder is increasingly recognized as a public health issue in Europe, with rising concerns over high-risk gambling behaviors, particularly in online environments, triggering tighter regulatory and policy responses across various jurisdictions. This social strain leads authorities to mandate mandatory deposit limits cooling-off periods and self-exclusion schemes that directly reduce betting volumes. Large operators which form the bulk of the European market fabric are particularly vulnerable to reputational damage and may face boycotts or heavy fines for perceived negligence. The UK Gambling Commission is increasing its compliance and oversight activities, focusing heavily on operator failures regarding customer interaction and social responsibility, which continues to result in significant financial penalties and settlements for betting operators. The volatility makes it difficult for operators to forecast long-term revenue as new protective measures can be introduced abruptly. Operators demand more robust identity verification systems which compresses margins and slows down user onboarding processes. Furthermore, the fluctuating public sentiment impacts the willingness of payment processors and banks to service gambling transactions. This macro-social headwind creates a cautious environment where expansion plans stagnate or contract despite the underlying demand for betting services.

MARKET OPPORTUNITIES

Integration of Artificial Intelligence Enhances Personalization

The rapid adoption of artificial intelligence and machine learning opens up major possibilities for operators to deliver hyper-personalized betting experiences, which is likely to promote the growth of the Europe online betting market. These experiences drive customer loyalty and lifetime value. As users expect tailored recommendations operators can leverage AI algorithms to analyze betting patterns and suggest relevant markets in real time. AI adoption among large European enterprises is rising rapidly, driven by investments in data analytics and automation, with significant growth in text mining and language processing technologies. This transition allows brands to create dynamic odds and personalized bonuses that resonate with individual user behaviors significantly improving conversion rates. The ability to predict churn and intervene with targeted retention offers enhances the relevance of communications and improves customer satisfaction scores. Smart data processing continues to rise. European betting firms are heavily adopting artificial intelligence to analyze player performance and data in real-time, using AI-driven analytics to enhance the user experience and drive, and personalize, their services. Operators are increasingly allocating portions of their technology budgets to these digital channels to capture deeper insights into player preferences. The format supports responsible gambling initiatives by identifying risky behavior patterns early and triggering automated safeguards bridging the gap between profit and protection. As data libraries expand and models become more sophisticated the inventory for personalized marketing will grow substantially. This evolution represents a paradigm shift where every user interaction becomes a programmable touchpoint for sophisticated engagement strategies.

Expansion of Live In-Play Betting Markets Drives Engagement

The continuous enhancement of live in-play betting technologies offers a potential opportunity to capitalize on the excitement of real-time sporting action and maintain user engagement throughout events, which is predicted to propel the expansion of the Europe online betting market. These tools enable operators to offer thousands of dynamic markets that update instantly based on game progress predicting outcomes and automating odds adjustments without human intervention. Live in-play wagering has become the dominant driver of revenue in the European sports betting market, with a rapid shift toward mobile-enabled, real-time consumption. Generative data models allow for the creation of micro-markets tailored to specific moments such as the next corner kick or point scored ensuring that each user sees the most relevant options possible. This level of immediacy was previously unattainable at scale and significantly boosts betting frequency while reducing idle time between wagers. Predictive analytics help operators anticipate market movements and adjust their risk exposure proactively rather than reacting to historical data. The technology also improves fraud detection by identifying suspicious betting patterns more accurately thereby protecting integrity and revenue. Natural language processing facilitates better commentary integration allowing companies to synchronize odds with live text and video feeds seamlessly. As streaming latency decreases the barrier to entry for high-frequency betting lowers enabling casual players to participate actively. This technological leap ensures that the European market remains at the forefront of betting innovation driving efficiency and excitement across all verticals.

MARKET CHALLENGES

Fragmentation of Licensing Regimes Complicates Compliance

The highly fragmented nature of the European regulatory landscape poses a significant challenge for operators within the Europe online betting market. Consequently, this makes it difficult to maintain compliance and operate efficiently across multiple borders. The continent comprises numerous distinct legal frameworks cultures and enforcement mechanisms which necessitates localized strategies that complicate unified reporting and analysis. According to the European Gaming and Betting Association the existence of over thirty distinct national licensing regimes with varying tax rates and technical requirements makes it difficult to establish standardized operational procedures. Operators often struggle with disparate data reporting obligations where information formats from different countries do not integrate seamlessly leading to incomplete pictures of regional performance. The lack of a single European gambling license means that user access is scattered across countless jurisdictional boundaries diluting the impact of broad marketing campaigns. Cross-border payment processing remains problematic especially with the rise of anti-money laundering directives that limit transaction flows between regulated and unregulated markets. Operators are facing increased operational complexity due to fragmented and inconsistent regulations in different European jurisdictions. This fragmentation increases the cost and complexity of running pan-European operations requiring specialized local knowledge and multiple technology stacks. The inability to harmonize standards accurately undermines confidence in digital channels and hampers strategic decision making. Overcoming this disjointed ecosystem requires substantial investment in legal counsel and harmonized compliance frameworks.

Intensifying Competition for Customer Acquisition Elevates Costs

The saturation of the digital space with an ever-increasing number of licensed operators creates intense competition for limited customer attention driving up the cost of acquisition significantly, and thereby slowing down the expansion of the Europe online betting market. More brands are vying for the same bettors on popular platforms, causing auction dynamics to intensify. Consequently, this results in inflated cost per click and cost per acquisition rates. Data indicates that rising digital competition and increasing regulation in European gambling markets are creating upward pressure on customer acquisition costs, leading to pressure on profit margins. This bidding war disproportionately affects smaller operators that lack the deep pockets of multinational corporations to sustain high marketing burns. The sheer volume of bonus offers displayed to consumers daily leads to promotion fatigue where users subconsciously ignore promotional content reducing overall effectiveness. Regulators continuously update their guidelines to restrict aggressive bonus structures forcing brands to spend more on brand building just to maintain visibility. The competition extends beyond traditional sportsbooks as casinos and lottery providers enter the sports betting space adding to the congestion. Attention spans are shrinking. Analysis of general mobile user behavior suggests a trend toward shorter application session durations, which increases the need for content creators to implement faster engagement hooks. Operators must therefore invest more in high-quality creative production and affiliate partnerships to break through the noise which further escalates campaign budgets. This relentless upward pressure on costs threatens the sustainability of customer acquisition models for many digital native betting businesses.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 10.78% |

| Segments Covered | By Type, Device and Region. |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Country Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, the Netherlands, Turkey, the Czech Republic, and the Rest of Europe. |

| Market Leaders Profiled | Flutter Entertainment plc, Entain plc, Bet365 Group Ltd., 888 Holdings plc, Kindred Group plc, Betsson AB, FDJ United, Tipico Group, LeoVegas AB, and William Hill Ltd. |

SEGMENTAL ANALYSIS

By Type Insights

The sports betting segment led the Europe online betting market and captured a 52.8% share in 2025. The dominance of the segment is attributed to the profound cultural significance of football and other major sports across the continent which drives consistent wagering activity throughout the year. Among these, a key driver is the extensive calendar of professional leagues and international tournaments that provide continuous betting opportunities for enthusiasts. European club football has experienced a significant post-pandemic resurgence in live match attendance, with total attendance figures in the hundreds of millions for top-tier and lower-tier leagues. The integration of live streaming services directly into betting platforms has further solidified this position by allowing users to watch events and place bets simultaneously without switching applications. Online gambling in Europe is experiencing consistent growth, with mobile-based betting becoming the dominant method of placement, and casino games leading in revenue generation. Sponsorship deals between betting operators and top tier clubs have also normalized gambling as part of the fan experience increasing brand visibility and trust. The diversity of available markets ranging from match outcomes to player statistics caters to both casual and sophisticated bettors ensuring broad appeal. This symbiotic relationship between professional sports and betting infrastructure guarantees that sports betting remains the cornerstone of the European online gambling industry.

The online casino segment is anticipated to witness the fastest CAGR of 14.8% from 2026 to 2034 due to technological advancements that replicate the immersive atmosphere of physical casinos within digital environments. The primary factor driving this growth is the proliferation of live dealer games which use high definition video streams to connect players with real human croupiers in real time. The Live Casino segment is experiencing sustained, high-double-digit growth driven by player demand for immersive and social gaming experiences. The introduction of virtual reality and augmented reality features allows users to explore three dimensional casino floors and interact with slots in novel ways that traditional screens cannot match. Mobile devices have become the dominant platform for online gambling, with, generally, a significant portion of the player base preferring the convenience of smartphones. Game developers are continuously releasing branded slots based on popular movies and television shows which attract non-traditional gamblers looking for entertainment value. The flexibility of playing at any time without travel constraints appeals strongly to younger demographics who prioritize instant access. Regulatory frameworks in several key markets have also evolved to specifically license online casino operations providing a legal pathway for expansion. This convergence of technology content and accessibility ensures the casino segment will outpace other categories in growth velocity.

By Device Insights

In 2025, the mobile devices segment dominated the Europe online betting market and occupied a significant share. The demand for these devices is supported by the fundamental shift in consumer behavior where smartphones have become the primary interface for digital entertainment and financial transactions. The ubiquity of dedicated betting applications provides users with instant access to markets push notifications for odds changes and biometric security features that desktop environments lack. Unique mobile subscription rates in Europe are very high, but overall growth is slow, with the focus shifting towards increasing 5G adoption. The integration of mobile payment wallets such as Apple Pay and Google Pay has streamlined the deposit process reducing friction and encouraging spontaneous betting decisions. Social media usage is heavily skewed toward mobile with operators leveraging these platforms to drive app installs and engage users through short form video content. Mobile devices have become the primary method for internet access in the EU, while desktop usage has fallen below that of portable, handheld devices. The rollout of fifth generation networks has enhanced mobile betting capabilities by supporting ultra-low latency live streaming and rapid data updates essential for in-play wagering. The portability of mobiles ensures constant connectivity allowing operators to engage users during commutes breaks and live events. This structural change in device usage patterns guarantees that mobile will remain the primary channel for betting activity.

The mobile segment is also the fastest growing segment in the Europe online betting market with a projected CAGR of 16.2% over the forecast period. The rapid growth of the segment is propelled by the continuous improvement in smartphone hardware and software ecosystems that enable richer and more complex betting experiences. A major factor that aids this segment is the optimization of betting interfaces for smaller screens which now offer full functionality including cash out features bet builders and multi-view live streaming. Smartphone shipments in Europe showed signs of recovery in 2024, with premiumization trends indicating a continued shift toward advanced display technologies like high refresh rates, largely driven by Chinese vendors expanding their footprint. These superior screens offer an ideal canvas for high impact visual advertising and immersive game graphics that perform poorly on older devices. The rise of fifth generation standalone networks has further reduced latency to under ten milliseconds enabling seamless real-time interaction critical for fast paced betting markets. 5G connectivity has achieved widespread population coverage across the European Union, with a growing focus on deploying standalone 5G to enhance network performance for high-bandwidth applications. Operators are increasingly adopting a mobile first development strategy prioritizing app features over desktop versions to capture the attention of younger users who rarely own computers. The integration of geolocation services allows for hyper-localized promotions and compliance checks that enhance user safety and relevance. The rising capability of mobile hardware, specifically longer battery life and faster processors, will enable mobile to secure a greater portion of high-value betting.

REGIONAL ANALYSIS

United Kingdom Online Betting Market Analysis

The United Kingdom led the Europe online betting market and accounted for a 28.6% share in 2025. The leading position of the UK market is driven by its long established regulatory framework and a deeply ingrained betting culture that spans generations. This segment is also attributed to the presence of the UK Gambling Commission which provides a clear albeit strict licensing regime that fosters consumer trust and operator stability. Gambling participation rates among adults in Great Britain show that online platforms are established as the primary method for engagement, with overall participation rates in gambling activities remaining stable. The country serves as the global headquarters for many major betting operators who centralize their technology and compliance operations within British borders. A strong tradition of sports sponsorship and advertising has normalized betting as a mainstream leisure activity despite recent restrictions. The gambling industry in the UK continues to be a substantial source of tax revenue for the government, with recent figures indicating an upward trend in tax receipts from online and remote gaming activities. The widespread adoption of responsible gambling tools such as GamStop demonstrates a mature market focused on sustainability. The high penetration of broadband and smartphones ensures that digital platforms reach virtually every demographic segment. This combination of regulatory clarity cultural acceptance and technological infrastructure ensures the UK retains its top rank.

Germany Online Betting Market Analysis

Germany followed closely in the Europe online betting market and captured a 18.3% share in 2025. The expansion of the German market is fuelled by its massive population and recent regulatory normalization. The nation benefits from a passionate sports fan base particularly for football which drives immense volume during league seasons and international tournaments. A further key driving factor is the implementation of the State Treaty on Gambling which created a unified federal licensing system replacing the previous fragmented approach. Following the 2021 Interstate Treaty, a regulated market was established, transitioning numerous formerly unlicensed"gray market" operators to a licensed framework, though many illegal, unlicensed, or "white-label" operators still operate in Germany. The restriction on advertising has forced operators to focus on product quality and customer retention rather than aggressive acquisition leading to a more sustainable market structure. Licensed sports betting turnover (handle) in Germany has generally shown a strong upward trend since regulation, with substantial, consistent revenue figures, particularly around major sporting events. The strong economy and high disposable income of German consumers support significant wagering volumes despite strict stake limits. Operators are investing heavily in compliance technology to meet rigorous reporting requirements ensuring long term viability. The shift from illegal offshore sites to regulated domestic platforms has unlocked substantial tax revenue for the state. This transition from a restricted to a regulated giant cements Germany as a pivotal market.

Italy Online Betting Market Analysis

Italy remains a vital player in the Europe online betting market due to its vibrant sports culture and early adoption of online gambling regulation. The market status is characterized by a high frequency of betting activity driven by a deep love for football and horse racing among the populace. Among these, a major driving factor is the comprehensive licensing framework managed by the Customs and Monopolies Agency which has successfully migrated a large portion of players from the black market to legal channels. Online gambling in Italy continues to experience significant growth, driven by rapid adoption of digital channels, although online casino games generally hold a larger share of that revenue than sports betting. The popularity of fantasy sports and daily fantasy competitions has introduced a new demographic of younger players to the betting ecosystem. The Italian gambling market is shifting heavily toward digital platforms, with a strong consumer preference for mobile devices to place bets, although the specific share of mobile wagering is likely lower than the eighty percent threshold mentioned. The government has utilized gambling taxes to fund public projects creating a political incentive to maintain a robust regulated market. Local operators have developed highly localized products catering to regional preferences and dialects which enhances user engagement. The integration of betting outlets with online platforms allows for seamless omnichannel experiences that drive loyalty. This blend of tradition and innovation ensures Italy remains a key growth engine.

France Online Betting Market Analysis

France saw regular growth within the Europe online betting market owing to its strong equestrian traditions and football passion to sustain steady demand for licensed betting services. The market status is defined by a state-controlled monopoly model for certain game types while allowing competition in sports betting and poker under strict oversight. Online gaming accounts in France are growing significantly, driven by sports betting, reflecting a stronger engagement in digital platforms. A key driving factor is the rigorous protection of the domestic market which limits international operators but ensures high compliance standards and consumer safety. The popularity of horse racing events like the Prix de l'Arc de Triomphe drives significant seasonal spikes in wagering volumes. Online sports betting turnover in France is experiencing consistent, strong growth, with user preference shifting towards digital platforms over traditional retail outlets. The government has recently explored expanding the range of allowable betting markets to capture more value from international sporting events. Strict advertising bans have pushed operators to innovate with content marketing and sponsorship alternatives. The focus on channeling players away from unlicensed sites remains a central policy goal driving enforcement actions. This cautious yet steady approach defines the unique market character of France.

Spain Online Betting Market Analysis

Spain is anticipated to expand considerably in the Europe online betting market over the forecast period due to its recovering economy and enthusiastic sports following. The nation has emerged as a critical battleground for operators due to its large population and high mobile penetration rates. The market status is characterized by rapid consolidation as major international groups acquire local license holders to secure market access. The Spanish online gambling market has experienced a significant, sustained, and rapid increase in gross gaming revenue, with casinos and betting driving record-high figures. A primary driving factor is the intense popularity of La Liga football which generates massive betting volumes during match days and transfer windows. The government has implemented strict advertising regulations including bans during certain hours which has reshaped marketing strategies toward digital and affiliate channels. The Spanish population shows a consistently high and growing rate of daily internet usage, with near-total digital adoption among young and middle-aged adults, creating a vast addressable digital market. The rise of esports betting has found a particularly receptive audience among Spanish youth driving innovation in product offerings. Regional licensing requirements add complexity but also create opportunities for localized operators to thrive. The ongoing digital transformation of the retail betting sector is bridging the gap between physical and online experiences. These factors combine to create a resilient and rapidly evolving market environment in Spain.

COMPETITIVE LANDSCAPE

The competition in the Europe online betting market is intensely fierce characterized by a constant battle for market share among established giants and agile new entrants. Dominant players leverage vast data ecosystems and proprietary technology to offer superior odds and wider market coverage that smaller competitors struggle to match. However niche operators thrive by focusing on specific sports or localized communities where they can offer tailored experiences and better customer service. The landscape is further complicated by stringent regulatory frameworks that vary significantly between nations forcing all participants to maintain robust compliance teams. New entrants from the fantasy sports and esports sectors are disrupting traditional models by attracting younger demographics with innovative gamified products. Price wars occasionally erupt in acquisition costs but differentiation increasingly relies on user experience speed and reliability of payouts. Mergers and acquisitions remain common as companies seek to consolidate licenses and expand their geographic footprint efficiently. This dynamic environment ensures rapid evolution where adaptability technological prowess and ethical standards determine long term survival and success in the region.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the Europe Online Betting Market include

- Flutter Entertainment plc

- Entain plc

- Bet365 Group Ltd.

- 888 Holdings plc

- Kindred Group plc

- Betsson AB

- FDJ United

- Tipico Group

- LeoVegas AB

- William Hill Ltd.

Top Players in the Market

Flutter Entertainment

Flutter Entertainment stands as a global leader in sports betting and gaming with a profound impact on the European landscape through brands like Paddy Power and Betfair. The company drives innovation by leveraging advanced data analytics to offer dynamic pricing and personalized user experiences across multiple jurisdictions. Recent actions include the full integration of its US operations while simultaneously upgrading its European technology stack to enhance mobile performance. The firm continues to expand its live streaming capabilities allowing users to watch events directly within their apps which boosts engagement significantly. Globally Flutter sets benchmarks for operational excellence and sustainable growth strategies. Their commitment to merging retail and digital channels creates a seamless omnichannel experience that strengthens customer loyalty and drives long term value across all markets they serve.

Entain plc

Entain plc operates as a major force in the Europe online betting market with a diverse portfolio including Ladbrokes Coral and bwin that serves millions of customers daily. The company focuses heavily on technological transformation and sustainability to maintain its competitive edge in a regulated environment. Recent initiatives involve the rollout of its proprietary LeoVegas mobile platform across its existing brands to improve user interface and retention rates. Entain has partnered with leading sports leagues to secure exclusive data rights enabling faster and more accurate in-play betting markets for users. The firm actively invests in advanced artificial intelligence systems to personalize marketing offers while adhering to stringent responsible gaming standards. Globally Entain contributes by pioneering the adoption of green energy in its retail shops and digital infrastructure. Their strategic emphasis on customer safety and product innovation ensures they remain at the forefront of industry developments. This dual focus on ethics and technology solidifies their reputation as a trusted operator worldwide.

Bet365 Group

Bet365 Group remains a dominant private entity in the Europe online betting market renowned for its extensive coverage of sports markets and superior live streaming services. The company distinguishes itself through vertical integration controlling its own technology development which allows for rapid deployment of new features and markets. Recent actions include significant investments in cloud infrastructure to ensure platform stability during peak traffic periods such as major football tournaments. Bet365 has expanded its in-play betting options to include micro markets that appeal to younger demographics seeking instant gratification. The firm continues to refine its algorithmic trading models to manage risk effectively while offering competitive odds to customers. Globally Bet365 influences the sector by setting high standards for product depth and reliability without relying on external suppliers. Their dedication to organic growth and customer centric design fosters strong brand loyalty. This independent approach allows them to adapt quickly to changing regulatory landscapes while maintaining profitability across diverse international regions.

Top Strategies Used by Key Market Participants

Key players in the Europe online betting market primarily focus on mobile first development to capture the growing segment of smartphone users who prefer betting on the go. Companies heavily invest in artificial intelligence and machine learning to personalize user experiences and optimize odds compilation in real time. Strategic partnerships with professional sports leagues and media broadcasters help secure exclusive data rights and increase brand visibility among fans. Major participants are expanding their live streaming capabilities to keep users engaged within their applications for longer durations during events. Development of comprehensive responsible gambling tools ensures compliance with strict regulations and builds trust with consumers and regulators alike. Firms also prioritize omnichannel integration to provide seamless experiences between physical retail shops and digital platforms. Continuous localization of content and payment methods addresses the diverse cultural and linguistic needs of different European countries. These strategies collectively aim to maximize customer lifetime value while navigating complex legal frameworks effectively.

MARKET SEGMENTATION

This research report on the Europe Online Betting Market has been segmented and sub-segmented based on the following categories.

By Type

- Sports Betting

- Casinos

-

- iSlots

- iTable

- iDealer

- Other iCasino Games

-

- Poker

- Bingo

- Others

By Device

- Desktop

- Mobile

- Others

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

What is meant by the Europe Online Betting Market?

The Europe Online Betting Market refers to digital platforms that allow users to place wagers on sports and other events via websites and mobile applications across European countries

. What are the primary types of online betting in Europe?

Major types include fixed-odds sports betting, live/in-play betting, exchange betting, eSports betting, and virtual sports betting.

What factors are driving the growth of the Europe Online Betting Market?

Key drivers include increasing smartphone penetration, high internet usage, digital payment adoption, regulatory legalization in several countries, and growing sports engagement.

What is the expected growth trend of the market during the forecast period?

The market is projected to witness steady growth due to technological innovation, expansion of licensed operators, and rising consumer demand for online entertainment

Which countries dominate the Europe Online Betting Market?

The United Kingdom, Germany, Italy, France, and Spain represent the largest revenue-generating markets in the region.

What role does mobile betting play in market expansion?

Mobile betting accounts for a significant share of total revenues, as users prefer app-based wagering due to convenience, real-time updates, and secure payment integrations.

What regulatory framework governs online betting in Europe?

Online betting regulations are primarily governed at the national level, with licensing authorities ensuring compliance with responsible gambling, AML policies, and consumer protection laws.

What are the major challenges faced by operators in Europe?

Challenges include strict advertising restrictions, high taxation rates, cross-border regulatory complexities, cybersecurity risks, and responsible gambling mandates.

What technological innovations are shaping the market?

Artificial intelligence, big data analytics, blockchain-based payment systems, and real

What are the key customer demographics in the European market?

The market primarily includes adults aged 18–45, with increasing participation among digitally active users and sports enthusiasts.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com