Europe Optical Fiber Market Size, Share, Trends & Growth Forecast Report, Segmented By Type (Multi-mode, Single mode, Plastic Optical Fiber (POF)), Application, End User, And Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic & Rest of Europe) - Industry Analysis From (2026 To 2034)

Market Size, 2025

$3.52 BnMarket Estimate, 2026

$3.81 BnMarket Forecast, 2034

$7.13 BnCAGR, 2026–2034

8.15%Europe Optical Fiber Market Report Summary

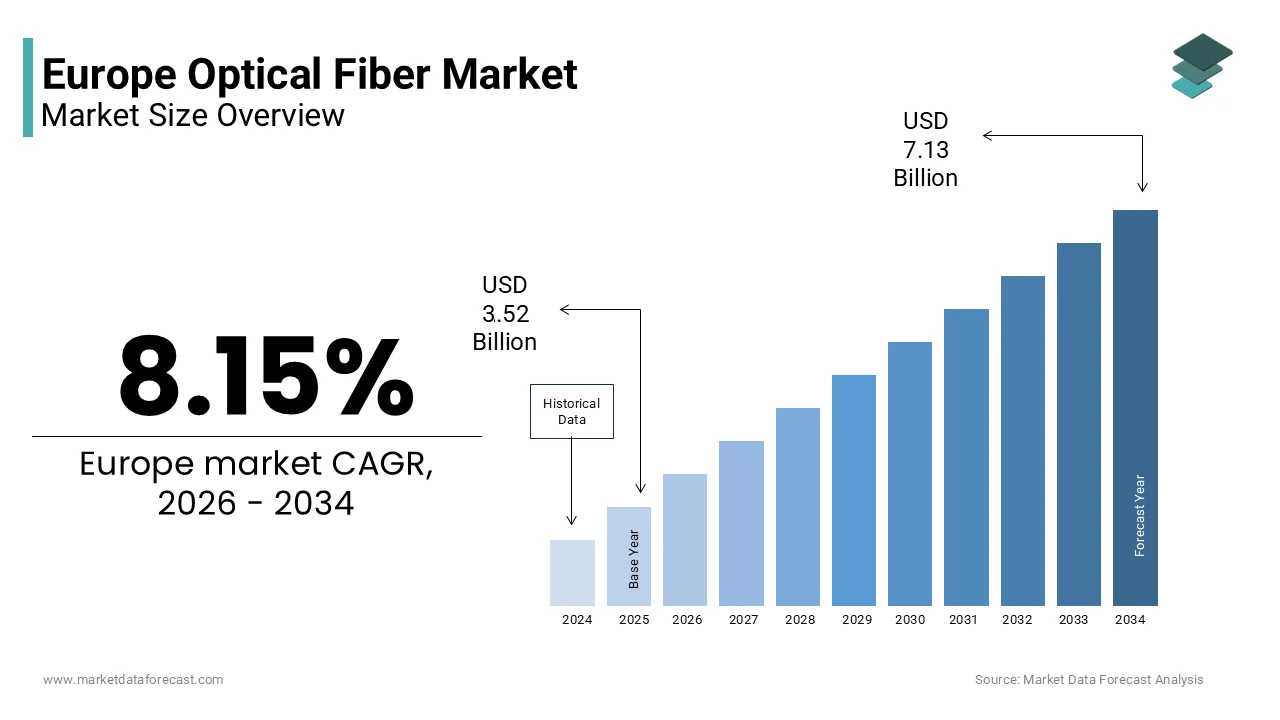

The Europe optical fiber market was valued at USD 3.52 billion in 2025 and is estimated to reach USD 3.81 billion in 2026, and is projected to grow to USD 7.13 billion by 2034, expanding at a CAGR of 8.15% during the forecast period. The growth of the Europe optical fiber market is primarily driven by the increasing demand for high speed internet connectivity, rapid expansion of 5G infrastructure, and the growing deployment of fiber to the home and fiber to the building networks across the region. Governments and telecom operators across Europe are investing heavily in digital infrastructure modernization to support data intensive applications, cloud services, and smart city initiatives. Additionally, the rising need for reliable and high bandwidth communication networks in data centers, enterprise connectivity, and industrial automation is further accelerating the adoption of optical fiber technologies across Europe.

Key Market Trends

- Increasing deployment of fiber broadband networks across Europe driven by government backed digital transformation programs and expanding gigabit connectivity goals.

- Rapid expansion of 5G infrastructure requiring high capacity fiber backhaul networks to support faster and more reliable mobile communication.

- Growing investments in data centers and cloud infrastructure increasing demand for high performance optical fiber connectivity.

- Rising adoption of fiber to the home and fiber to the building networks to deliver ultra fast internet services to residential and commercial users.

- Technological advancements in optical fiber manufacturing improving transmission efficiency, durability, and network scalability.

Segmental Insights

- Based on type, the single mode fiber segment held the dominant share of the Europe optical fiber market in 2025. The leadership of this segment is attributed to its ability to transmit data over long distances with minimal signal loss, making it highly suitable for telecom backbone networks, metropolitan area networks, and long haul communication infrastructure.

- Based on application, the telecom segment accounted for a significant share of the Europe optical fiber market in 2025. The dominance of this segment is driven by the continuous expansion of high speed broadband services, large scale deployment of fiber based communication networks, and the increasing need for reliable connectivity to support 5G and next generation mobile networks.

Regional Insights

- The Europe optical fiber market is experiencing steady expansion across several countries supported by strong investments in telecommunications infrastructure and digital connectivity initiatives.

- Germany was the largest contributor to the Europe optical fiber market, accounting for 22.7% of the market share in 2025. The country’s leadership is supported by increasing fiber broadband rollouts, strong industrial digitalization initiatives, and significant investments by telecom operators in upgrading national communication networks.

- Other European countries are also accelerating fiber deployment projects to strengthen broadband penetration, support smart city development, and enhance high speed connectivity across urban and rural regions.

Competitive Landscape

The Europe optical fiber market is characterized by the presence of several global and regional manufacturers focusing on expanding production capacity, improving fiber performance, and strengthening supply chains to meet the growing demand for advanced communication infrastructure. Companies are investing in research and development to enhance fiber transmission efficiency and support emerging technologies such as 5G networks, cloud computing, and data center connectivity. Strategic collaborations with telecom operators and infrastructure providers are also helping market players expand their presence across the European region. Prominent players operating in the Europe optical fiber market include Corning Inc, Prysmian Spa, Jiangsu Zhongtian Technology Co Ltd, Yangtze Optical Fiber and Cable Joint Stock Ltd, Fiberhome Telecommunication Technologies Co Ltd, CommScope Holding Co Inc, Nexans SA, Furukawa Electric Co Ltd, Sumitomo Electric Industries Ltd, and Coherent Corp.

Europe Optical Fiber Market Size

The Europe optical fiber market size was calculated to be USD 3.52 billion in 2025 and is anticipated to be worth USD 7.13 billion by 2034, growing from USD 3.81 billion in 2026 at a CAGR of 8.15% during the forecast period.

The optical fiber is indispensable for supporting bandwidth intensive applications ranging from ultra high definition streaming to industrial automation and cloud computing. The strategic importance of this sector has intensified as European nations aggressively pursue digital sovereignty and connectivity targets. As per the European Commission, the Digital Decade policy program mandates that all European households should have access to gigabit connectivity by 2030, a goal that necessitates a massive expansion of fiber to the premises networks. The International Telecommunication Union indicates that fixed broadband subscriptions in Europe have seen a consistent shift toward fiber based technologies, displacing older copper based systems. This push is not merely commercial but is deeply rooted in the socio economic requirement to ensure equitable access to digital services for over 447 million citizens.

MARKET DRIVERS

Escalating Demand for High Bandwidth Cloud Services and Remote Work Infrastructure

The exponential surge in cloud computing adoption and the structural shift toward remote work models serve is propelling the growth of Europe optical fiber market. Enterprises and public sector entities are increasingly migrating operations to hybrid and multi cloud environments, which necessitates low latency and high throughput connections that only optical fiber can reliably provide. As per Eurostat, the enterprises in the European Union using cloud computing services rose to 41% in recent years, with large corporations reaching adoption rates exceeding 80%. This migration places immense pressure on existing network backbones to handle massive data transfers without congestion. Simultaneously, the normalization of telecommuting has altered residential traffic patterns, requiring last mile networks to support simultaneous high-definition video conferencing and large file uploads from millions of homes. Data from the Organisation for Economic Co-operation and Development reveals that broadband traffic in European countries increased during peak hours, following the widespread adoption of flexible work policies. Traditional copper networks struggle to maintain signal integrity over long distances at these speeds, making fiber the only viable solution for sustained performance. Consequently, telecommunications operators are accelerating their fiber roll out plans to meet service level agreements demanded by corporate clients and discerning residential users.

Strategic Implementation of Smart City Initiatives and Industrial Automation

The concerted push toward smart city development and Industry 4.0 adoption is attributed in fuelling the growth of Europe optical fiber market. Municipalities, across the continent are integrating Internet of Things sensors, intelligent traffic management systems, and automated utility grids to enhance urban efficiency and sustainability. These interconnected ecosystems generate vast volumes of real time data that require robust transmission channels with minimal latency to function effectively. As per the European Smart Cities Marketplace, hundreds of cities have launched large scale projects relying on dense sensor networks that monitor everything from air quality to energy consumption, all of which depend on fiber optic backhaul for data aggregation. In the industrial sector, the transformation toward automated manufacturing relies heavily on machine to machine communication and real time analytics to optimize production lines. The European Commission notes that the industrial internet of things market is projected to connect billions of devices, creating an urgent need for industrial grade fiber networks within factory floors and logistics hubs. Governments are actively funding these initiatives through various cohesion funds, recognizing that advanced digital infrastructure is a prerequisite for economic competitiveness. This systemic integration of digital technologies into the physical fabric of cities and factories ensures a steady and growing demand for optical fiber cables and related active equipment.

MARKET RESTRAINTS

High Capital Expenditure and Complex Civil Engineering Requirements

The prohibitive costs associated with civil engineering and trenching activities with the rapid expansion of optical fiber networks is majorly limiting the growth of Europe optical fiber market. Deploying fiber to the premises often requires extensive excavation works to lay cables underground, a process that is both financially draining and logistically complex, particularly in densely populated urban centers or regions with challenging geological conditions. As per the Body of European Regulators for Electronic Communications, the cost of civil works can account for up to 80% of the total expenditure in a fiber rollout project by making the return on investment timeline unattractive for many private operators. Additionally, the fragmentation of regulatory frameworks across different member states creates administrative bottlenecks, where obtaining permits for street works can take months or even years. Data from national regulatory authorities in several countries indicates that permit delays are a leading cause of slowed deployment rates, discouraging investors from committing capital to less profitable rural areas. The financial burden is exacerbated by the need to coordinate with multiple utility providers to avoid damaging existing gas, water, and electricity lines.

Shortage of Skilled Technical Workforce for Installation and Maintenance

The shortage of qualified technicians and engineers capable of installing and maintaining advanced fiber optic infrastructure is also degrading the growth of Europe optical fiber market. The deployment of fiber networks requires specialized skills in splicing, testing, and network design that differ significantly from traditional copper wire installation, yet the current labor pool lacks sufficient numbers of trained professionals to meet the aggressive rollout targets. As per the European Centre for the Development of Vocational Training, the information and communication technology sector in Europe faces a deficit of hundreds of thousands of skilled workers, a gap that directly impacts the pace of physical network construction. Training programs have struggled to keep up with the speed of technological advancement and the scale of government mandated connectivity goals. This scarcity drives up labor costs and leads to project delays as operators compete for a limited number of certified installers. Furthermore, the complexity of modern fiber networks demands continuous upskilling, as new technologies such as passive optical networking evolve rapidly. Industry associations report that recruitment difficulties are particularly acute in rural areas where the allure of urban employment draws talent away from regions that desperately need connectivity improvements.

MARKET OPPORTUNITIES

Integration of Fiber Networks with Next Generation 5G Mobile Architecture

The emergence of fixed fiber infrastructure with new mobile is likely to set up new opportunities for the growth of Europe optical fiber market. While 5G is often perceived as a wireless technology, its full potential regarding ultra-low latency and massive device connectivity relies heavily on a dense underlying fiber optic backbone to connect cell sites to the core network. As per the GSM Association, achieving true 5G performance requires fiber to be extended much closer to the end user, often directly to small cells deployed on street furniture and building facades. This architectural necessity means that every new 5G base station effectively drives demand for additional fiber strands and deeper network penetration. European mobile network operators are increasingly investing in fiber assets to support their wireless ambitions, recognizing that wireless and wired networks are becoming inextricably linked. The rollout of 5G standalone networks, which promise to enable autonomous vehicles and remote surgery, cannot proceed without comprehensive fiber coverage. Government spectrum auctions often include coverage obligations that implicitly force operators to expand their fiber footprints to comply with service quality standards. As countries accelerate their 5G deployments to maintain technological leadership, the concurrent requirement for fiber densification ensures a sustained pipeline of projects for cable manufacturers and installation firms, opening new revenue streams beyond traditional residential broadband services.

Expansion of Fiber Connectivity into Underserved Rural and Peripheral Regions

The extending optical fiber networks to rural and remote areas of Europe that have historically been neglected by commercial operators due to low population density is additionally to leverage the growth of Europe optical fiber market. Recent policy shifts and substantial public funding mechanisms are altering the economic calculus, making these regions viable targets for infrastructure development. As per the Connecting Europe Facility, the European Union has allocated billions of euros specifically to support digital connectivity projects in less developed regions, which is aiming to eliminate the digital divide between urban and rural communities. These funds often take the form of grants or low interest loans that de risk private investment by encouraging operators to enter markets they previously avoided. The focus on territorial cohesion means that governments are actively partnering with private entities to build open access networks that can be used by multiple service providers, enhancing competition and service quality in remote locations. Agriculture technology and rural tourism sectors are also emerging as key demand drivers, as farms adopt precision agriculture tools and rural businesses require reliable connectivity to compete globally. The systematic mapping of white spots, or areas with no broadband coverage, by national regulators provides a clear roadmap for targeted deployment.

MARKET CHALLENGES

Regulatory Fragmentation and Inconsistent Permitting Procedures Across Member States

The lack of harmonized regulatory frameworks and inconsistent permitting procedures across European member states poses a formidable challenge to the seamless expansion of the Europe optical fiber market. Each country maintains its own set of rules regarding right of way access, infrastructure sharing, and civil work permissions by creating a complex patchwork that hinders cross border operators and increases compliance costs. As per the European Commission's Digital Economy and Society Index, disparities in administrative burdens remain a top obstacle to efficient network rollout, with some nations requiring dozens of separate approvals for a single deployment project. This fragmentation prevents economies of scale and slows down the pace of investment, as operators must navigate unique legal landscapes in every jurisdiction they enter. Inconsistent application of the European Electronic Communications Code further exacerbates the issue, leading to unequal playing fields where some markets enjoy streamlined processes while others suffer from bureaucratic inertia. The inability to implement standardized deployment strategies forces companies to maintain diverse operational teams and legal departments, draining resources that could otherwise be directed toward network construction. Moreover, the uncertainty surrounding future regulatory changes in specific countries can deter long term capital commitment.

Intense Competition from Alternative Fixed Wireless and Satellite Technologies

The escalating competition from advanced fixed wireless access and low earth orbit satellite technologies that offer viable alternatives for last mile connectivity is also to limit the growth of Europe optical fiber market. While fiber remains the gold standard for performance, newer wireless technologies have improved significantly in terms of speed and latency, presenting a cost effective solution for areas where trenching is prohibitively expensive or physically impossible. As per the Broadband Stakeholder Group, fixed wireless access utilizing millimeter wave spectrum can now deliver gigabit speeds in certain conditions, challenging the monopoly fiber once held on high bandwidth services. Additionally, the emergence of large satellite constellations promises global coverage with reduced latency, appealing to remote users who previously had no options other than expensive and slow satellite links. These alternatives reduce the urgency for immediate fiber deployment in marginal areas, potentially stranding assets if wireless solutions become sufficiently robust. Telecommunications operators are increasingly adopting a mixed technology approach, deploying wireless solutions where the return on investment for fiber is weak. This competitive pressure forces fiber proponents to constantly justify the higher capital expenditure against rapidly improving wireless benchmarks.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 8.15% |

| Segments Covered | By Type, Application, End User, and Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, and the Czech Republic |

| Market Leaders Profiled | Corning Inc, Prysmian Spa, Jiangsu Zhongtian Technology Co Ltd, Yangtze Optical Fiber and Cable Joint Stock Ltd, Fiberhome Telecommunication Technologies Co Ltd, CommScope Holding Co Inc, Nexans SA, Furukawa Electric Co Ltd, Sumitomo Electric Industries Ltd, and Coherent Corp |

SEGMENTAL ANALYSIS

By Type Insights

The single mode fiber segment was the largest by holding a dominant share of the Europe optical fiber market in 2025. The growth of the segment is likely to grow with the superior capability to transmit data over long distances with minimal signal loss by making it the indispensable choice for telecommunications backbones and metropolitan area networks. The relentless expansion of fiber to the home architectures across the continent further cements its position as the industry standard. The dominance of single mode fiber is its unparalleled ability to support high bandwidth over extended distances without the need for frequent signal regeneration. Unlike multi-mode variants, single mode fiber utilizes a smaller core diameter that allows light to travel in a single path, virtually eliminating modal dispersion and enabling transmission speeds that meet the rigorous demands of modern internet traffic. Telecommunications operators prioritize this technology because it future proofs their investments against escalating capacity requirements. The ability to upgrade existing single mode lines to higher speeds simply by changing terminal equipment, without replacing the cable itself, offers a compelling economic advantage.

The plastic optical fiber segment is expanding at a fastest CAGR of 11.2% during the forecast period. The segment growth is attributed to driven by the increasing integrating Plastic Optical Fiber into vehicle architectures to manage the surging data demands of advanced driver assistance systems and in vehicle infotainment. POF offers distinct advantages over copper and glass fiber in this environment, including immunity to electromagnetic interference, ease of installation due to its larger core size, and resistance to vibration and harsh temperatures. The shift toward electric vehicles in Europe, which saw sales exceed 2 million units in recent years, further accelerates this trend as manufacturers seek to reduce vehicle weight to extend battery range. POF is significantly lighter than traditional copper harnesses by contributing to overall vehicle efficiency. Major European car manufacturers are standardizing POF for multimedia systems and control networks, driving a steady increase in consumption.

By Application Insights

The telecom application segment was accounted in holding a significant share of the Europe optical fiber market in 2025. The relentless push by European governments and private operators to deploy Fiber to the Home networks is the primary factor driving the dominance of the telecom segment. National broadband plans across the region have set ambitious targets to replace aging copper networks with optical fiber to ensure universal high-speed access. As per the European Commission, member states have committed to investing over 40 billion euros in digital infrastructure to achieve the Digital Decade goals, with a significant portion allocated to last mile fiber deployments. Countries like Spain and Portugal have already achieved fiber coverage in over 90% of households, setting a benchmark that other nations are striving to match. This massive civil engineering effort requires millions of kilometers of optical fiber cable annually to connect residential buildings to the network core. The competitive landscape among telecommunications providers further accelerates this deployment, as operators vie for market share by offering superior gigabit speeds that are only possible with direct fiber connections. The regulatory push for open access networks also stimulates demand, allowing multiple service providers to utilize the same physical infrastructure, thereby maximizing the utility and volume of fiber deployed.

The medical application segment is poised to register a CAGR of 9.8% from 2026 to 2034. The rising preference for minimally invasive surgical techniques across European healthcare systems is a major driver propelling the demand for optical fiber in medical applications. These procedures rely heavily on endoscopic and laparoscopic equipment that utilizes fiber optic bundles to transmit high resolution images from inside the human body to external monitors, allowing surgeons to operate with precision through small incisions. Optical fibers are critical components in these devices, providing the illumination and image transmission necessary for successful operations. The aging population in Europe, with the proportion of citizens over 65 expected to reach 30% by 2050 according to the study, is leading to a higher incidence of conditions requiring surgical intervention, further boosting the volume of these procedures. Hospitals are increasingly investing in state of the art surgical suites equipped with advanced fiber optic imaging systems to improve outcomes. The shift toward outpatient surgery centers also drives demand, as these facilities require compact and efficient optical tools.

REGIONAL ANALYSIS

Germany Optical Fiber Market Analysis

Germany was the largest contributor of the Europe optical fiber market by holding 22.7% of share in 2025 with its robust industrial base and delayed but accelerating residential fiber rollout. The country has historically lagged behind its southern European neighbors in fiber to the home penetration due to a heavy reliance on vectoring technology over existing copper lines. However, the current market dynamic is characterized by a massive corrective investment phase. As per the German Federal Ministry for Digital and Transport, the government has set a target to provide gigabit connectivity to every household and business by 2030, prompting a surge in deployment activities. Major telecommunications operators and alternative network builders are engaged in aggressive expansion projects, particularly in urban centers like Berlin and Munich. The industrial sector, which forms the backbone of the German economy, is a significant consumer of fiber for factory automation and Industry 4.0 applications. The manufacturing industry's demand for low latency connections to support robotic systems and real time data analytics drives substantial B2B fiber installations. Furthermore, the government has streamlined permitting processes to reduce the time required for civil works, addressing one of the primary bottlenecks.

France Optical Fiber Market Analysis

France was ranked second by capturing 18.2% of the Europe optical fiber market share in 2025 that has resulted in rapid network expansion across both urban and rural territories. The growth of the segment is likely to grow with a unique public private partnership model that has successfully accelerated fiber deployment. The "Plan France Très Haut Débit" has been instrumental in mobilizing resources to connect less densely populated areas, ensuring that rural communities are not left behind. This comprehensive approach has created a balanced market where competition among service providers is fierce, driving down prices and increasing adoption rates. The presence of major infrastructure players who manage open access networks has fostered an environment conducive to rapid scaling. Additionally, the French government's emphasis on digital sovereignty has led to increased investments in secure fiber networks for public administration and critical infrastructure.

Spain Optical Fiber Market Analysis

Spain optical fiber market growth is ascribed to witness a fastest CAGR in coming years with the most advanced and extensive fiber optic networks on the continent. As per the National Markets and Competition Commission of Spain, fiber to the home coverage exceeds 90% of the population, a feat achieved through aggressive investment by major telecommunications operators and a favorable regulatory environment. This maturity in the residential market is now shifting focus toward enterprise solutions and the integration of fiber with 5G networks to support next generation applications. Furthermore, the government continues to support initiatives that promote digital inclusion, ensuring that remote regions maintain high connectivity standards. The established infrastructure provides a solid foundation for innovation in smart city technologies and digital services, sustaining Spain's position as a key driver of the European optical fiber market.

United Kingdom Optical Fiber Market Analysis

The United Kingdom optical fiber market growth is propelled with the substantial private investment and a strategic shift away from copper legacy networks. Historically, the UK relied heavily on fiber to the cabinet solutions, but the market narrative has shifted decisively toward full fiber to the premises. As per Ofcom, the UK communications regulator, the rollout of full fiber has accelerated dramatically, with coverage reaching over 40% of premises and targeting universal availability by 2030. This surge is largely fueled by the entry of alternative network providers, often referred to as altnets, which are challenging incumbent operators by building independent fiber networks in various regions. The government's Project Gigabit initiative provides billions of pounds in funding to support deployment in hard to reach areas, stimulating activity in rural markets. The financial services sector in London and other major cities demands ultra low latency connections, driving high value enterprise fiber projects. Additionally, the increasing consumption of streaming content and the rise of remote work have heightened consumer expectations for reliable high speed internet. European landscape.

Italy Optical Fiber Market Analysis

Italy optical fiber market growth is likely to have a prominent growth with the dual strategy of state led initiatives in underserved areas and aggressive commercial deployment in major urban centers. The Italian optical fiber market is experiencing a renaissance driven by the National Recovery and Resilience Plan, which allocates substantial funds to digital infrastructure as part of post pandemic economic recovery efforts. As per the Italian Communications Authority, there is a concerted push to bridge the digital divide between the industrialized north and the less connected south. Major telecommunications operators are investing heavily in fiber networks, supported by government incentives that reduce the financial risk of deployment in low density areas. The historic nature of many Italian cities poses unique challenges for civil engineering, yet innovative installation techniques are being employed to preserve heritage while expanding connectivity. The growing demand for digital services among Italian businesses, particularly in the fashion and manufacturing sectors, is also driving enterprise fiber adoption. Furthermore, the integration of fiber with mobile networks is gaining momentum as operators prepare for advanced 5G services.

COMPETITION OVERVIEW

The competitive landscape of the Europe optical fiber market features a dynamic interplay between established multinational corporations and emerging regional specialists. Intense rivalry centers on technological differentiation with companies investing heavily in research to develop fibres with lower attenuation and higher bandwidth capacity. Price competition remains significant particularly in standardized product segments prompting manufacturers to optimize production efficiency through automation and scale. Regulatory frameworks across European nations create varied market entry conditions requiring players to adapt strategies to local permitting processes and infrastructure sharing mandates. The convergence of fixed and mobile network technologies has intensified competition as fibre providers compete with wireless alternatives for last mile connectivity contracts. Strategic alliances between cable manufacturers and telecommunications operators have become increasingly common to secure long term supply agreements and share deployment risks. Innovation in installation techniques and connector designs serves as another battleground where companies seek to reduce total cost of ownership for network builders.

KEY MARKET PLAYERS

A few major players of the Europe optical fiber market include

- Corning Inc

- Prysmian Spa

- Jiangsu Zhogtian Technology Co Ltd

- Yangtze Optical Fiber and Cable Joint Stock Ltd

- Fiberhome Telecommunication Technologies Co Ltd

- CommScope Holding Co Inc

- Nexans SA

- Furukawa Electric Co Ltd

- Sumitomo Electric Industries Ltd

- Coherent Corp

Top Strategies Used by Key Market Participants

Key players in the Europe optical fiber market employ several strategic approaches to strengthen their competitive position. Companies prioritize vertical integration by controlling raw material sourcing and manufacturing processes to ensure quality and cost efficiency. Strategic partnerships with telecommunications operators enable co development of customized fibre solutions aligned with network rollout timelines. Geographic expansion through new manufacturing facilities in high growth regions reduces logistics costs and improves supply chain resilience. Investment in research and development drives innovation in low loss fibres and high density cable designs that meet evolving bandwidth demands. Companies also pursue sustainability initiatives by optimizing energy consumption in production and developing recyclable cable materials. Acquisition of specialized technology firms allows rapid integration of advanced capabilities such as micro fibre splicing or intelligent monitoring systems.

MARKET SEGMENTATION

This research report on the Europe optical fiber market has been segmented and sub-segmented based on type, application, and region.

By Type

- Multi-mode

- Single mode

- Plastic Optical Fiber (POF)

By Application

- Telecom

- Oil & Gas

- Military & Aerospace

- BFSI

- Medical

- Railway

- Other Application

By End User

- Telecom and Networking

- Industrial Automation

- Medical

- Defense

By Region

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

1.What is the current outlook of the Europe Optical Fiber Market?

The Europe optical fiber market is experiencing strong growth due to increasing demand for high speed internet connectivity, expansion of 5G infrastructure, and rising investments in fiber to the home networks across the region.

2.What factors are driving the growth of the Europe Optical Fiber Market?

The market growth is driven by the rapid rollout of 5G networks, increasing demand for high bandwidth data transmission, expansion of broadband infrastructure, and rising investments in smart city projects.

3.What are the major applications of optical fiber in Europe?

Optical fiber is widely used in telecommunications networks, data centers, broadband internet services, cable television systems, healthcare imaging technologies, and military communication systems.

4.Which countries are leading the Europe Optical Fiber Market?

Germany, the United Kingdom, France, Italy, and Spain are leading the market due to strong telecommunications infrastructure development and increased deployment of fiber optic networks.

5.How is 5G deployment influencing the Europe Optical Fiber Market?

The deployment of 5G networks is increasing the demand for optical fiber as fiber optic cables are essential for connecting base stations and enabling high speed and low latency data transmission.

6.What are the key challenges faced by the Europe Optical Fiber Market?

Major challenges include high installation costs, complex network deployment in rural areas, and the requirement for significant investments in digital infrastructure.

7.What types of optical fiber are commonly used in Europe?

Single mode fiber and multi mode fiber are the most commonly used types, with single mode fiber dominating due to its capability to transmit data over long distances with minimal signal loss.

8.Which industries are the major end users of optical fiber in Europe?

Major end users include telecommunications providers, data center operators, government organizations, healthcare institutions, and industrial automation sectors.

9.How is the growth of data centers impacting the Europe Optical Fiber Market?

The rapid expansion of data centers across Europe is increasing the demand for high capacity optical fiber networks to support large scale data transmission and cloud computing services.

10.What are the future trends in the Europe Optical Fiber Market?

Future trends include increasing adoption of fiber to the home networks, rising investments in 5G infrastructure, growth of smart cities, and expanding digital transformation initiatives across European countries.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com