Europe Optogenetics Market Research Report – Segmented By Sensor type (Genetically Encoded Calcium Indicators, pH Sensors, Neurotransmitter Release, Voltage-Sensitive Fluorescent Proteins), Techniques, Application, Light equipment and Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic and Rest of Europe) - Industry Analysis From 2026 to 2034

Europe Optogenetics Market Report Summary

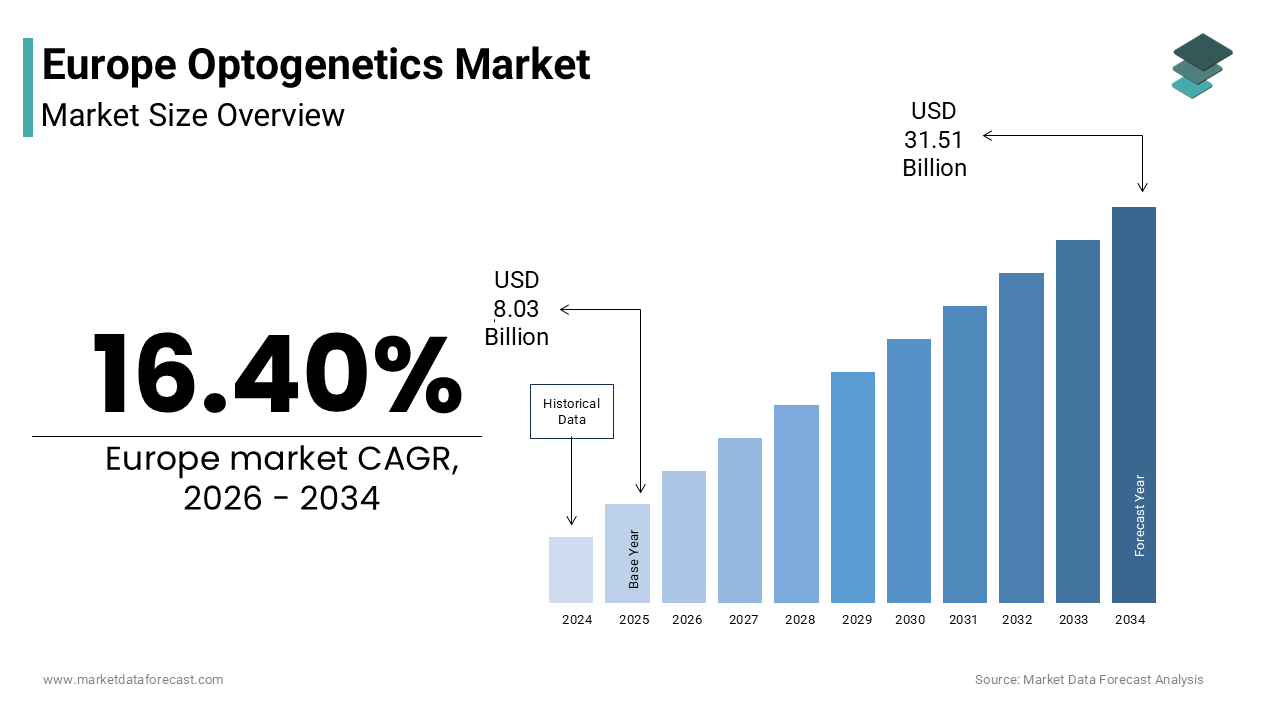

The Europe optogenetics market was valued at USD 8.03 billion in 2025 and is anticipated to reach USD 9.35 billion in 2026 from USD 31.51 billion by 2034, growing at a CAGR of 16.40% during the forecast period from 2026 to 2034. The growth of the Europe optogenetics market is driven by the rising prevalence of neurological disorders, increasing investments in neuroscience research, and continuous advancements in gene therapy technologies. Growing adoption of viral vector delivery systems, expanding collaborations between academic institutions and biotechnology companies, and increasing funding for brain research programs are further accelerating market growth. Moreover, the integration of optogenetics with closed-loop brain-machine interfaces, expansion into non-neuronal therapeutic applications, and ongoing innovations in light-sensitive proteins are supporting the expansion of the Europe optogenetics market.

Key Market Trends

-

Rising adoption of optogenetics in neuroscience research for precise neural circuit mapping.

-

Increasing development of advanced viral vector delivery systems for efficient gene transfer.

-

Growing integration of optogenetics with closed-loop brain-machine interface technologies.

-

Rising expansion of optogenetic applications beyond neuroscience into cardiovascular and metabolic disease research.

-

Increasing investments in advanced imaging technologies and next-generation light-sensitive proteins.

Segmental Insights

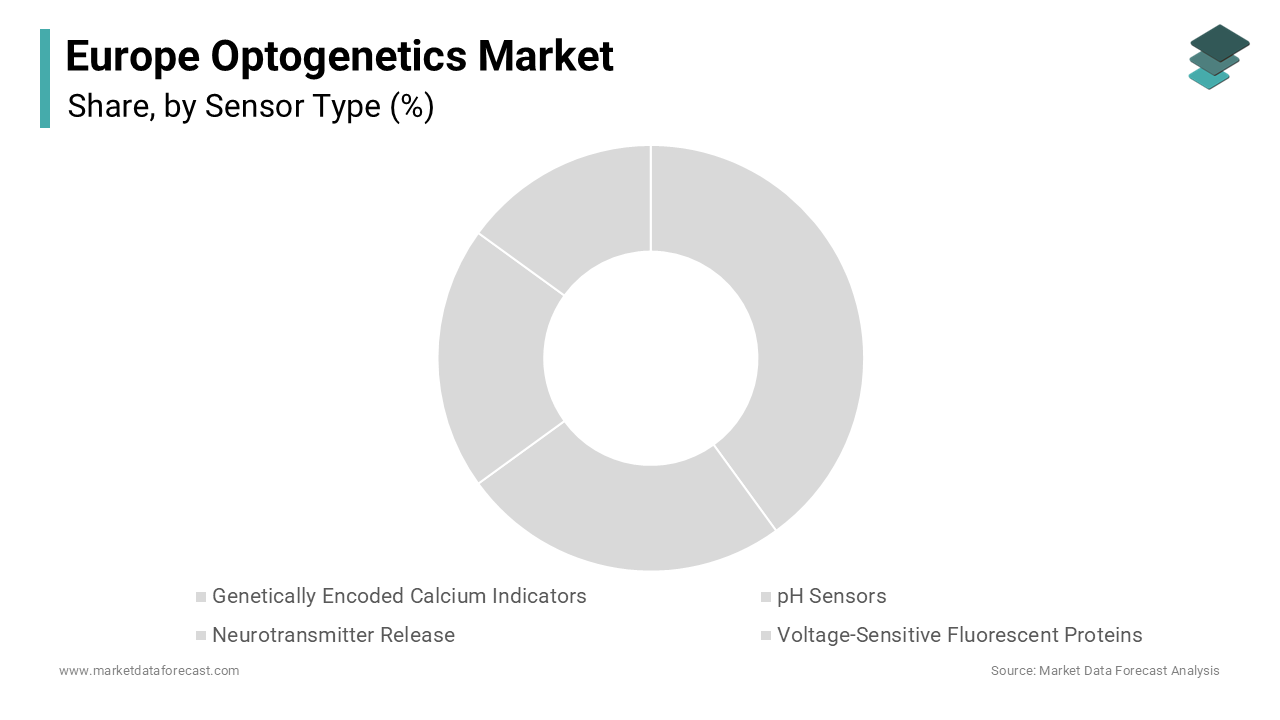

- Based on sensor type, the genetically encoded calcium indicators segment dominated the Europe optogenetics market and accounted for 45.7% of the market share in 2025. The dominance of the segment is attributed to its superior signal stability, widespread adoption in neuroscience research, compatibility with advanced imaging systems, and ability to visualize neuronal activity with high spatial resolution. Increasing utilization in long-term neural circuit mapping studies further strengthens segment growth.

- The voltage-sensitive fluorescent proteins segment is projected to witness the fastest CAGR of 14.5% during the forecast period owing to increasing demand for real-time neuronal activity monitoring, expanding adoption of high-speed imaging technologies, growing development of next-generation voltage indicators, and rising research focused on high-frequency neural signaling and epilepsy.

- Based on techniques, the channelrhodopsin segment dominated the Europe optogenetics market and accounted for 55.3% of the market share in 2025. The growth of the segment is driven by its proven effectiveness in neuronal excitation, widespread research adoption, availability of multiple engineered variants, increasing utilization in behavioral neuroscience, and compatibility with affordable optical stimulation systems.

- The archaerhodopsin segment is anticipated to register the fastest CAGR of 12.8% during the forecast period due to increasing demand for neuronal inhibition techniques, growing utilization in psychiatric and behavioral research, expanding bidirectional neural circuit studies, and continuous development of enhanced inhibitory opsins with improved performance and reduced toxicity.

- Based on application, the neuroscience segment dominated the Europe optogenetics market and accounted for 65.9% of the market share in 2025. The dominance of the segment is attributed to increasing research on neurodegenerative diseases, expanding brain mapping initiatives, growing pharmaceutical investments in neurological drug discovery, and rising adoption of optogenetic tools for understanding neural connectivity and brain function.

- The retinal disease treatment segment is expected to witness the fastest CAGR of 16.2% during the forecast period owing to promising clinical trial outcomes, increasing development of optogenetic vision restoration therapies, growing prevalence of retinal degenerative diseases, expanding investments in gene therapy, and rising commercialization of ophthalmic optogenetic technologies.

Regional Insights

- Germany dominated the Europe optogenetics market and accounted for 22.1% of the regional market share in 2025. The country's leadership is driven by world-class neuroscience research institutions, strong government funding for life sciences, advanced biotechnology infrastructure, and increasing collaborations between academia and industry. Continuous investments in neurotechnology research further strengthen market growth.

- The United Kingdom held 18.4% of the Europe optogenetics market share in 2025 owing to its globally recognized academic research centers, increasing public funding for brain research, expanding biotechnology ecosystem, and growing commercialization of optogenetic innovations. Strong regulatory support for advanced therapies continues to support market expansion.

- France continues to maintain a significant position in the European market due to its centralized research organizations, strong neuroscience research capabilities, expanding biotechnology clusters, and increasing collaborations under Horizon Europe research programs. Growing investments in neurological disease research further strengthen market development.

- Switzerland is witnessing strong growth supported by its advanced pharmaceutical industry, prestigious research institutions, increasing translational neuroscience research, expanding precision medicine initiatives, and strong investments in next-generation optogenetic technologies.

- The Rest of Europe is expected to experience notable growth during the forecast period owing to increasing government investments in neuroscience, expanding adoption of advanced research technologies, growing academic collaborations, improving laboratory infrastructure, and rising demand for innovative tools supporting neurological disease research.

Competitive Landscape

The Europe optogenetics market is highly competitive and characterized by the presence of biotechnology companies, life science reagent suppliers, and advanced optical equipment manufacturers competing through technological innovation, product quality, and integrated research solutions. Leading companies are focusing on developing next-generation opsins, advanced viral vector delivery platforms, miniaturized optical devices, and high-performance imaging technologies to support cutting-edge neuroscience research. Strategic collaborations with academic institutions, expansion of manufacturing capabilities, investments in research and development, and continuous product innovation continue to strengthen competitive positioning across the Europe optogenetics market. The prominent players operating in the Europe optogenetics market include Coherent Inc., Noldus Information Technology, Thorlabs, Inc., Cobalt Inc., Scientifica, Bruker Corporation, Laserglow Technologies, REGENXBIO Inc., GenSight Biologics, Addgene, Penn Vector Core, and The Jackson Laboratory.

Europe Optogenetics Market Size

The Europe optogenetics market size was valued at USD 8.03 billion in 2025 and is anticipated to reach USD 9.35 billion in 2026 from USD 31.51 billion by 2034, growing at a CAGR of 16.40% during the forecast period from 2026 to 2034.

Optogenetics is a sophisticated segment of the life sciences industry focused on the precise control of cellular activity using light and genetically encoded, light-sensitive proteins. This technology enables researchers to manipulate neuronal firing with millisecond precision, offering unparalleled insights into brain function neural circuits and disease mechanisms. The European landscape is characterized by robust academic research institutions advanced neuroscience centers and strong governmental support for biomedical innovation. According to the European Commission, brain health research is centrally driven by the European Partnership for Brain Health (EP BrainHealth). Co-funded under the Horizon Europe framework, this partnership unites over 60 participants from 30+ countries to systematically align national funding strategies for neurological conditions. The World Health Organization and the European Academy of Neurology reveals that neurological disorders are a premier public health challenge affecting an estimated 449.2 million people across the WHO European Region. This immense burden is tracked under the WHO’s Global Status Report on Neurology to accelerate country-level healthcare policy reform. The prevalence of diseases such as Alzheimer’s Parkinson’s and epilepsy drives the demand for high resolution investigative techniques that optogenetics provides. Countries like Germany France and the United Kingdom host leading laboratories equipped with state of the art imaging and laser systems essential for optogenetic experiments. The integration of optogenetics with other modalities such as electrophysiology and calcium imaging enhances its utility in mapping brain connectivity. Regulatory bodies across Europe maintain strict guidelines for genetic modification and animal welfare ensuring ethical standards are met during research. The growing collaboration between academia and biotechnology firms facilitates the translation of basic research into potential clinical applications. This market is poised for expansion as technological advancements reduce costs and improve the accessibility of optogenetic tools for broader scientific communities.

MARKET DRIVERS

Increasing Prevalence of Neurological Disorders Driving Research Investment

The rising burden of neurological disorders across the region drives the adoption of optogenetics in preclinical research and drug discovery, which boosts the overall growth of the Europe optogenetics market. The European Brain Council (EBC) confirmed that the collective economic burden of brain disorders, uniting both neurological and psychiatric illnesses, exceeds €800 billion annually across Europe through direct healthcare expenses and lost productivity. Alzheimer Europe demonstrates that over 7.8 million Europeans live with dementia, and this aggregate population is projected to double to more than 16.2 million cases by 2050. This escalating health crisis necessitates a deeper understanding of neural circuitry and pathological mechanisms which optogenetics uniquely provides through precise temporal and spatial control of neuronal activity. Governments and private foundations are increasing funding for neuroscience initiatives to accelerate the development of novel therapies. The European Union’s Horizon Europe program has allocated significant resources to brain research projects focusing on neurodegenerative diseases. Researchers utilize optogenetic tools to model disease states in animals allowing for the identification of specific neural pathways involved in symptom manifestation. This capability accelerates the validation of drug targets reducing the time and cost associated with traditional screening methods. Pharmaceutical companies are increasingly incorporating optogenetics into their early stage discovery pipelines to enhance the predictive validity of preclinical models. The ability to dissect complex behaviors and cognitive functions at the cellular level offers critical insights that conventional pharmacological approaches cannot achieve. Hence, the urgent need to address the growing prevalence of neurological conditions drives sustained investment in optogenetic technologies across the region.

Advancements in Gene Therapy and Viral Vector Delivery Systems

Technological progress in gene therapy and viral vector delivery systems greatly accelerates the expansion of the Europe optogenetics market. This improves the efficiency and safety of introducing light sensitive opsins into target cells. Recent developments in adeno associated virus vectors have enhanced transduction rates and reduced immunogenicity making them ideal for delivering optogenetic constructs in vivo. According to the European Medicines Agency several gene therapy products have received marketing authorization in recent years demonstrating the regulatory pathway for advanced biological interventions. These advancements facilitate the widespread adoption of optogenetics in both academic and industrial settings by providing reliable tools for genetic manipulation. Researchers can now target specific cell types with greater precision minimizing off target effects and enhancing experimental reproducibility. The availability of commercially available viral vectors with optimized promoters and fluorescent markers simplifies the experimental workflow for scientists. Collaborations between virology experts and neuroscientists have led to the development of novel opsins with improved kinetics and spectral properties expanding the range of applications. Institutions in Germany and the United Kingdom are at the forefront of developing next generation vectors that offer higher titers and stability. The integration of these delivery systems with CRISPR Cas9 technology further enhances the versatility of optogenetic approaches allowing for simultaneous gene editing and functional modulation. As these technologies mature, they lower the technical barriers to entry. This enables more laboratories to incorporate optogenetics into their research protocols, thereby driving market growth.

MARKET RESTRAINTS

Stringent Ethical Regulations and Animal Welfare Concerns

Strict ethical regulations and heightened awareness regarding animal welfare are major restraints for the Europe optogenetics market. This trend is particularly visible in preclinical research involving invasive procedures. The European Union Directive 2010/63/EU on the protection of animals used for scientific purposes imposes rigorous standards for housing care and use of laboratory animals requiring justification for any procedure causing pain or distress. The European Commission shows that first-time scientific animal use has steadily decreased to approximately 8.4 million animals annually, with basic research in nervous system disorders remaining a primary domain. Optogenetic experiments often require surgical implantation of optical fibers or cranial windows which are classified as moderate to severe procedures necessitating extensive ethical review and approval processes. These regulatory hurdles can delay project timelines and increase operational costs for research institutions and pharmaceutical companies. Public sentiment against animal testing is growing with various non governmental organizations advocating for the replacement reduction and refinement of animal use in research. This pressure encourages the development of alternative methods such as in vitro models and computer simulations which may not fully replicate the complexity of intact neural circuits. Compliance with varying national interpretations of EU directives adds another layer of complexity for multinational studies. Researchers must demonstrate that no non animal alternative exists before obtaining approval which can be a lengthy and uncertain process. These ethical and regulatory constraints limit the scale and speed of optogenetic research potentially slowing the translation of findings into clinical applications.

High Technical Complexity and Specialized Infrastructure Requirements

The inherent technical complexity of optogenetics and the need for specialized infrastructure are severe barriers to widespread adoption across the European market. Successful implementation requires expertise in multiple disciplines including molecular biology virology optics and electrophysiology which are not commonly found in single research teams. To resolve complex infrastructure demands, the Federation of European Neuroscience Societies (FENS) provides hands-on technical training through dedicated technical schools, enabling decentralized access to high-precision optical and genetic equipment. The setup involves expensive components such as high power lasers micromanipulators and high speed cameras which require significant capital investment and regular maintenance. Small academic institutions and startups often struggle to secure funding for such specialized equipment limiting their ability to compete with well funded centers. Additionally the optimization of experimental parameters such as light intensity wavelength and pulse duration requires extensive trial and error consuming valuable time and resources. The variability in opsin expression levels and tissue penetration depth further complicates data interpretation requiring advanced analytical skills. Lack of standardized protocols across different laboratories leads to reproducibility issues hindering the comparison of results between studies. Training personnel to handle these complex systems is time consuming and costly. These technical and financial barriers restrict the user base primarily to elite research institutions slowing the democratization of optogenetic tools and limiting market expansion to smaller players who might otherwise drive innovation.

MARKET OPPORTUNITIES

Integration with Closed Loop Brain Machine Interfaces

The integration of optogenetics with closed-loop brain-machine interfaces paves the way for the growth of the Europe optogenetics market. It enables real-time monitoring and modulation of neural activity. This approach allows for dynamic adjustment of stimulation parameters based on instantaneous neuronal feedback offering precise control over pathological brain states. Translational neuroscience teams, notably at Stanford University, successfully pioneered real-time closed-loop optogenetic systems that detect abnormal neural oscillations to trigger immediate light pulses that effectively suppress epileptic seizures in animal models. This technology holds potential for developing next generation neuroprosthetics and therapeutic devices for conditions such as Parkinson’s disease and chronic pain. European research consortia are actively exploring these applications through collaborative projects funded by the European Research Council. The development of miniaturized wireless devices capable of delivering light and recording electrical signals simultaneously enhances the translational potential of these systems. Companies specializing in neural engineering are partnering with academic labs to commercialize these integrated platforms. The ability to restore normal brain function through adaptive stimulation offers a significant advantage over open loop systems which deliver fixed stimuli regardless of brain state. This precision reduces side effects and improves therapeutic efficacy making it an attractive avenue for clinical translation. As regulatory frameworks evolve to accommodate active implantable medical devices, the pathway for bringing these innovations to patients becomes clearer. This clarity is driving investment and interest in the emerging sector.

Expansion into Non Neuronal Cell Types and Peripheral Applications

Expanding the application of optogenetics beyond neurons to other cell types such as cardiomyocytes immune cells and pancreatic beta cells opens new avenues for growth in the European market. Researchers are increasingly utilizing light sensitive ion channels to control heart rhythm immune responses and insulin secretion offering novel therapeutic strategies for cardiovascular autoimmune and metabolic diseases. In studies published by researchers at Texas A&M University, optogenetic tools were successfully integrated into T-cells to create near-infrared and blue-light controlled immune switches, offering precise temporal control over cancer immunotherapy activation. This diversification reduces reliance on neuroscience applications and taps into larger patient populations suffering from common chronic conditions. The development of red shifted opsins that penetrate deeper into tissues facilitates applications in peripheral organs where blue light absorption is limited. Pharmaceutical companies are exploring optogenetic approaches for drug screening in cardiac and metabolic assays improving the predictive power of preclinical models. The versatility of optogenetic tools allows for the dissection of complex signaling pathways in non excitable cells providing insights into disease mechanisms that were previously inaccessible. Collaborations between immunologists cardiologists and bioengineers are driving innovation in this space leading to the creation of specialized tools tailored for specific cell types. As the understanding of light-mediated cellular control expands, the market for optogenetic reagents and equipment grows beyond traditional neuroscience suppliers. This expansion is attracting new entrants and investors interested in broad therapeutic applications.

MARKET CHALLENGES

Limited Penetration Depth of Light in Biological Tissues

Limited penetration depth of light in biological tissues restricts the ability to stimulate deep brain structures without invasive implants, which is a major challenge to the Europe optogenetics market. Blue and green light commonly used to activate standard opsins such as Channelrhodopsin 2 are strongly scattered and absorbed by hemoglobin and other tissue components limiting effective penetration to a few millimeters. The invasiveness poses risks of tissue damage inflammation and infection complicating long term studies and potential clinical applications. While red shifted opsins offer improved penetration they often exhibit slower kinetics or lower sensitivity requiring higher light intensities that can cause thermal damage. Developing efficient upconversion nanoparticles or waveguide structures to deliver light to deep targets remains technically challenging and expensive. The need for surgical intervention limits the scalability of optogenetic therapies and raises ethical concerns regarding human application. Researchers are exploring minimally invasive alternatives such as sonogenetics or magnetogenetics but these lack the temporal precision of optogenetics. Until non-invasive deep tissue stimulation methods are perfected, the utility of optogenetics remains constrained. Consequently, it is limited to superficial structures or requires complex surgical setups, which hinders broader clinical adoption.

Reproducibility Issues and Lack of Standardized Protocols

The lack of standardized protocols and reproducibility issues across different laboratories is a significant inhibition to the credibility and advancement of the Europe optogenetics market. Variability in viral vector production opsin expression levels light source calibration and experimental design leads to inconsistent results that are difficult to compare or replicate. Also, the inconsistency undermines confidence in findings and slows the translation of basic research into clinical applications. The absence of universal standards for reporting light intensity at the target site rather than just at the source creates ambiguity in interpreting dose response relationships. Different laboratories use varying animal strains ages and housing conditions which can influence neural physiology and opsin performance. Efforts to establish best practice guidelines are underway but adoption remains uneven across the diverse European research landscape. Funding agencies and journals are increasingly demanding rigorous statistical analysis and transparent reporting but enforcement is inconsistent. The resulting fragmentation hinders collaborative progress and wastes resources on failed replication attempts. Addressing these issues requires coordinated efforts from professional societies funding bodies and publishers to enforce strict standards and promote open science practices ensuring that optogenetic research maintains high scientific integrity and reliability.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 16.40% |

| Segments Covered | By Sensor Type, Techniques, Application, Light Equipment, and Country. |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, the Netherlands, Turkey, the Czech Republic, and the Rest of Europe. |

| Market Leaders Profiled | Coherent Inc., Noldus, Thorlabs Inc., Cobalt Inc., Scientifica, Bruker, Laserglow Technologies, Regenxbio Inc., Gensight, Addgene, UPenn Vector Core, and Jackson Laboratories. |

SEGMENTAL ANALYSIS

By Sensor Type Insights

The genetically encoded calcium indicators segment led the Europe optogenetics market and captured a 45.7% share in 2025. Its robust signal stability and widespread adoption in neuroscience research have contributed to the leading position of this segment. Calcium influx serves as a reliable proxy for neuronal activity allowing researchers to visualize functional connectivity with high spatial resolution. To evaluate microcircuit dynamics, research teams increasingly rely on all-optical neurophysiology, which couples in vivo calcium imaging with target optogenetic photostimulation to read out and alter single-cell resolution patterns simultaneously. The development of advanced variants has significantly improved brightness and kinetics enabling the detection of single action potentials in vivo. Researchers share and optimize advanced two-photon all-optical physiology templates via open scientific repositories to ensure cross-laboratory procedural replication. The compatibility of calcium indicators with two photon microscopy systems widely available in European core facilities further drives their dominance. Researchers prefer these sensors for long term longitudinal studies because they exhibit minimal phototoxicity and bleaching compared to synthetic dyes. The availability of numerous transgenic mouse lines expressing calcium indicators under specific promoters allows for cell type specific interrogation without additional viral injections. This ease of use combined with extensive validation data makes genetically encoded calcium indicators the default choice for mapping neural circuits understanding sensory processing and investigating disease mechanisms in preclinical models across the region.

On the other hand, the voltage sensitive fluorescent proteins segment is likely to experience the fastest CAGR of 14.5% over the forecast period owing to the critical need for millisecond temporal resolution in studying rapid neuronal events. Unlike calcium indicators which integrate activity over hundreds of milliseconds voltage sensors directly report membrane potential changes providing precise timing information essential for understanding spike timing dependent plasticity and network oscillations. As documented in the journal Cell, genetically encoded voltage indicators like ASAP3 provide sub-millisecond tracking of single voltage spikes and subthreshold membrane potential fluctuations that slower calcium sensors cannot capture. Recent engineering efforts have improved the brightness and voltage sensitivity of these proteins making them viable for in vivo applications in deep brain structures. The growing interest in studying high frequency gamma oscillations and fast ripple events in epilepsy research necessitates tools that can capture rapid dynamics without temporal smoothing. European funding agencies are prioritizing projects that utilize high speed imaging technologies to decode complex neural codes driving demand for these advanced sensors. Collaborations between protein engineers and electrophysiologists have led to the development of red shifted voltage sensors that minimize interference with blue light activated opsins enabling simultaneous stimulation and recording. As microscopy hardware improves to support faster frame rates the adoption of voltage sensitive fluorescent proteins is accelerating among researchers seeking to bridge the gap between electrical recordings and optical imaging.

By Techniques Insights

The channelrhodopsin segment was the largest in the Europe optogenetics market and occupied a 55.3% share in 2025. This leading position of the segment was attributed to its proven efficacy in depolarizing neurons and triggering action potentials with high reliability. Derived from the green alga Chlamydomonas reinhardtii Channelrhodopsin 2 responds to blue light by allowing cation influx which effectively excites target cells. Channelrhodopsins remain the premier choice for optogenetic optical activation because of their fast kinetics, while institutions like the Allen Institute actively focus on co-developing high-density nanophotonic neural probes to record these evoked responses. The availability of multiple engineered variants such as ChR2 H134R and ChETA allows researchers to tune the temporal precision and desensitization properties to suit specific experimental needs. Its widespread use is supported by an extensive library of validated viral vectors and transgenic animal models available from European biological resource centers. The simplicity of using blue light which is easily generated by inexpensive laser diodes and LEDs lowers the barrier to entry for new laboratories. Channelrhodopsin has been successfully applied in diverse contexts ranging from motor control studies to pain perception research demonstrating its versatility. The well characterized safety profile and minimal off target effects in mammalian tissues further reinforce its dominance. Regulatory bodies view Channelrhodopsin based approaches as established methodologies facilitating easier ethical approval for animal studies. Continuous improvements in expression levels and membrane trafficking ensure that it remains the gold standard for excitatory optogenetic control in both academic and industrial research settings.

However, the archaerhodopsin segment is on the rise and is expected to be the fastest growing segment in the market by witnessing a CAGR of 12.8% from 2026 to 2034 due to the increasing demand for all optical inhibition strategies that complement excitatory Channelrhodopsin experiments. Archaerhodopsin functions as a light driven proton pump that hyperpolarizes neurons upon exposure to green or yellow light effectively silencing neuronal activity. The capability is crucial for dissecting complex neural circuits where excitation and inhibition must be balanced to understand network dynamics. European researchers are increasingly adopting Archaerhodopsin for behavioral studies requiring precise temporal suppression of specific brain regions to determine causal roles in cognition and emotion. The development of enhanced variants with higher proton pumping efficiency and reduced cellular toxicity has improved its performance in long term experiments. The ability to combine Archaerhodopsin with red shifted excitatory opsins enables sophisticated bidirectional control experiments that were previously impossible. Funding initiatives supporting the study of inhibitory interneurons in psychiatric disorders have further accelerated its adoption. As laboratories upgrade their optical setups to include multiple wavelengths the integration of Archaerhodopsin into experimental workflows is becoming standard practice driving its rapid growth relative to other inhibitory techniques like Halorhodopsin which suffers from slower kinetics and chloride dependency issues.

By Application Insights

In 2025, the neuroscience segment held a 65.9% majority share of the Europe optogenetics market because of substantial public funding for basic brain research and the urgent need to elucidate mechanisms of neurological disorders. Optogenetics provides unparalleled precision in mapping neural circuits which is essential for understanding the pathophysiology of conditions such as Alzheimer’s disease Parkinson’s disease and schizophrenia. Researchers utilize optogenetic tools to identify specific neural pathways involved in memory formation motor control and sensory processing providing targets for therapeutic intervention. The ability to causally link neuronal activity to behavior makes optogenetics indispensable for validating hypotheses generated from observational studies. Major European initiatives such as the Human Brain Project incorporate optogenetic data to build comprehensive models of brain function. Academic institutions collaborate closely with pharmaceutical companies to use optogenetics in drug discovery pipelines ensuring that candidate molecules modulate the correct neural circuits. The high prevalence of mental health disorders in Europe creates a strong societal imperative for advancing neuroscience knowledge. Thus, the majority of optogenetic reagents equipment and services are directed toward neuroscience applications sustaining its dominant position in the market.

But the retinal disease treatment segment is expected to exhibit a noteworthy CAGR of 16.2% during the forecast period. This swift expansion of the segment is fuelled by promising clinical trial results and the potential to restore vision in patients with retinitis pigmentosa and age related macular degeneration. Unlike neuroscience applications which remain largely preclinical retinal optogenetics has advanced to human trials due to the accessibility of the eye and the natural light sensitivity of retinal cells. These therapies aim to bypass damaged photoreceptors and directly stimulate neural signals to the brain offering hope for millions of visually impaired individuals. The success of early stage trials has attracted significant venture capital investment into biotechnology firms specializing in ocular optogenetics. Regulatory pathways for gene therapies in the eye are more established compared to brain interventions facilitating faster progression to market. The aging population in Europe increases the prevalence of degenerative eye diseases creating a large addressable patient population. Advances in wearable light stimulating devices that pair with optogenetic treatments enhance functional outcomes. As these technologies move closer to commercialization the demand for specialized manufacturing and clinical support services is accelerating driving rapid growth in this segment.

COUNTRY ANALYSIS

Germany Optogenetics Market Analysis

Germany dominated the Europe optogenetics market and accounted for a 22.1% share in 2025. This dominance of the segment was driven by its world class research infrastructure and strong government support for life sciences. The country is home to leading institutions such as the Max Planck Institute for Neurobiology of Behavior which pioneers advancements in optogenetic tools and applications. According to the German Research Foundation (DFG), funding is allocated directly to knowledge-driven projects, including multi-phase genetically engineered models and spatial proteomics, rather than fixed billion-euro programmatic blocks. optogenetic drug discovery in Germany is primarily driven by academic-industrial alliances and specialized research consortia funded to improve the predictive validity of preclinical models. The presence of specialized equipment manufacturers in cities like Jena and Munich ensures easy access to high quality lasers and microscopy systems. Also, the Paul-Ehrlich-Institut (PEI) manages the rigorous regulatory authorization of clinical trials utilizing genetically modified investigational medicinal products via the centralized EU E-Submission platform. Collaborative networks between universities and industry partners accelerate the translation of basic research into commercial products. The country’s emphasis on precision medicine aligns with the capabilities of optogenetics to dissect disease mechanisms at the cellular level. Skilled workforce availability in molecular biology and optics further strengthens Germany’s leadership position. Investment in startup incubators focused on neurotechnology fosters innovation and commercialization of novel optogenetic solutions.

United Kingdom Optogenetics Market Analysis

The United Kingdom was positioned second and occupied an 18.4% share of the Europe optogenetics market in 2025. This growth of the regional market was supported by strong academic excellence and significant investment in brain research initiatives. Institutions such as University College London and the University of Oxford are global leaders in developing new optogenetic probes and applying them to study neurological disorders. UK Research and Innovation (UKRI) separately backs advanced brain-circuit interface research through its dedicated £69 million Precision Neurotechnologies programme. The presence of major contract research organizations facilitates outsourcing of optogenetic studies by pharmaceutical companies seeking specialized expertise. The UK Medicines and Healthcare products Regulatory Agency (MHRA) evaluates optogenetic therapies under its standard Advanced Therapy Medicinal Products (ATMPs) framework while exploring new early feasibility pathways to safely accelerate next-generation neurotechnology clinical trials. In addition, the UK’s strong tradition in publishing high impact neuroscience research attracts international talent and collaborations. Venture capital funding for biotech startups in Cambridge and London supports the commercialization of optogenetic tools and services. The National Health Service’s interest in novel therapies for neurodegenerative diseases drives demand for preclinical validation using optogenetics. Post Brexit regulatory adjustments have streamlined certain approval processes for research materials enhancing operational efficiency. The country’s focus on open science and data sharing promotes reproducibility and accelerates scientific progress in the field.

France Optogenetics Market Analysis

France holds a significant position in the Europe optogenetics market due to its centralized research organizations and strong focus on fundamental neuroscience. The Centre National de la Recherche Scientifique and the Institut Pasteur lead numerous projects utilizing optogenetics to investigate brain connectivity and disease mechanisms. France has a strong tradition in mathematics and physics which contributes to the development of sophisticated computational models integrated with optogenetic data. The country hosts several biotechnology clusters in Paris and Lyon that specialize in producing viral vectors and optogenetic reagents for domestic and international markets. Regulatory oversight by the National Agency for the Safety of Medicines and Health Products ensures rigorous safety standards for genetic research. Collaborations with European partners through Horizon Europe programs enhance resource sharing and expertise exchange. The growing prevalence of neurodegenerative diseases in the aging French population drives public interest and funding for innovative research tools. Academic hospitals integrate optogenetic findings into clinical trial designs for neurological conditions. The availability of skilled engineers and scientists supports the maintenance and operation of complex optical systems required for high quality research.

Switzerland Optogenetics Market Analysis

Switzerland is moving ahead steadfastly in the Europe optogenetics market owing to its high research intensity and prestigious academic institutions. The Swiss Federal Institutes of Technology in Zurich and Lausanne are at the forefront of developing miniaturized optogenetic devices and advanced imaging techniques. The country’s strong pharmaceutical sector including Novartis and Roche utilizes optogenetics for target validation and mechanistic studies in drug development. Switzerland’s neutral political status and stable regulatory environment attract international collaborations and investments in biotechnology. The presence of specialized manufacturers of precision optical components supports the local research ecosystem. Ethical review processes are rigorous but efficient ensuring high standards of animal welfare and scientific integrity. The country focuses on translational research bridging the gap between basic science and clinical applications. High quality infrastructure and generous funding enable researchers to access state of the art equipment. Collaboration with neighboring countries enhances the scope and impact of optogenetic research projects. The emphasis on innovation and quality ensures that Swiss contributions remain highly influential in the global optogenetics community.

COMPETITIVE LANDSCAPE

The competition in the Europe optogenetics market is characterized by a dynamic mix of specialized biotechnology firms established life science suppliers and innovative hardware manufacturers. Leading players differentiate themselves through product quality technical support and the breadth of their portfolios ranging from genetic constructs to optical equipment. Academic spin offs often introduce groundbreaking technologies such as novel opsins or miniaturized devices which are subsequently licensed or acquired by larger corporations. Price competition is moderate as researchers prioritize reliability and reproducibility over cost savings given the high stakes of experimental outcomes. Strategic partnerships between hardware providers and reagent suppliers create integrated solutions that simplify experimental workflows for customers. Intellectual property disputes occasionally arise regarding proprietary opsin sequences driving companies to invest in unique engineering improvements. Customer loyalty is built on consistent performance and responsive technical assistance rather than brand recognition alone. The market sees continuous innovation driven by the need for deeper tissue penetration and multi color compatibility. Regulatory compliance serves as a barrier to entry ensuring that only reputable players maintain long term presence. Collaborative ecosystems involving universities industry and funding agencies accelerate technological advancements and market expansion.

KEY MARKET PLAYERS

A few notable companies in the European optogenetics market include

- Coherent Inc.

- Noldus Information Technology

- Thorlabs, Inc.

- Cobalt Inc.

- Scientifica

- Bruker Corporation

- Laserglow Technologies

- REGENXBIO Inc.

- GenSight Biologics

- Addgene

- Penn Vector Core

- The Jackson Laboratory

Top Players in the Global Market

Addgene

Addgene serves as a critical global provider of high quality viral vectors and plasmids essential for optogenetic research. The company supports neuroscientists by offering a vast library of pre validated constructs including various Channelrhodopsin and Archaerhodopsin variants. Recent actions include expanding its European distribution network to ensure faster delivery of temperature sensitive biological materials to researchers in Germany and France. Addgene collaborates with leading academic institutions to develop next generation opsins with improved kinetics and spectral properties. Their commitment to quality control ensures reproducibility in experiments which is vital for scientific progress. By providing comprehensive technical support and detailed protocol guides they lower the barrier to entry for new laboratories. These efforts strengthen their position as a trusted partner in the life sciences community facilitating advancements in neural circuit mapping and disease modeling across the globe.

Thorlabs

Thorlabs is a major manufacturer of precision optical components and systems that are fundamental to optogenetic experimental setups. The company provides high power lasers light emitting diodes and fiber optic couplers required for precise light delivery in vivo. Recent actions involve launching miniaturized wireless head stages designed specifically for freely behaving animal studies which enhance data quality by reducing tethering artifacts. Thorlabs has expanded its manufacturing facilities in Europe to reduce lead times and provide localized customer support. They invest heavily in research and development to create integrated systems that combine stimulation and recording capabilities. Their focus on modularity allows researchers to customize setups according to specific experimental needs. By offering robust and reliable hardware Thorlabs enables scientists to perform complex optogenetic experiments with confidence. These strategic initiatives reinforce their leadership in providing the technological infrastructure necessary for cutting edge neuroscience research.

MilliporeSigma

MilliporeSigma operates as a key supplier of life science tools and reagents supporting the optogenetics workflow from gene delivery to protein expression. The company offers a wide range of viral vector production services and cell culture media optimized for neuronal health. Recent actions include acquiring specialized biotechnology firms focused on gene therapy manufacturing to enhance their capacity for producing clinical grade optogenetic vectors. MilliporeSigma has established partnerships with European contract research organizations to streamline the supply chain for academic and industrial clients. They provide end to end solutions including custom opsin synthesis and purification services. Their global logistics network ensures timely delivery of critical materials maintaining experimental continuity. By integrating digital tools for inventory management and order tracking they improve operational efficiency for customers. These developments solidify their role as an enabler of innovation in the optogenetics field supporting both basic research and therapeutic development.

Top Strategies Used by Key Market Participants

Key players in the Europe optogenetics market primarily focus on strategic collaborations with academic institutions to co develop novel opsins and delivery systems tailored for specific research needs. Companies invest heavily in expanding their manufacturing capabilities for viral vectors to meet the growing demand for high titer and pure biological reagents. Product diversification through the introduction of miniaturized wireless devices and red shifted opsins addresses the limitations of traditional tethered setups and shallow light penetration. Market participants prioritize regulatory compliance and ethical standards to navigate the strict European guidelines for genetic modification and animal welfare. Geographic expansion through local distribution centers ensures rapid delivery of temperature sensitive products enhancing customer satisfaction. Intellectual property protection via patents on unique protein variants secures competitive advantages. Digital integration for remote monitoring and data analysis adds value to hardware offerings. Pricing strategies balance affordability for academic users with premium positioning for specialized industrial applications. These multifaceted approaches drive sustainable growth and foster innovation in the rapidly evolving landscape of neuroscience research tools.

MARKET SEGMENTATION

This research report on the European optogenetics market has been segmented & sub-segmented into the following categories

By Sensor Type

- Genetically Encoded Calcium Indicators

- pH Sensors

- Neurotransmitter Release

- Voltage-Sensitive Fluorescent Proteins

By Techniques

- Archaerhodopsin

- Channelrhodopsin

- Halorhodopsin

By Application

- Retinal Disease Treatment

- Cardioversion

- Neuroscience

- Behavioral Tracking and Pacing

By Light Equipment

- Lasers

- LEDs

- Others

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com