Europe outboard Engines Market Size, Share, Trends & Growth Forecast Report, Segmented By Type, System Type, Provider Type, End-User And By Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic and Rest of Europe), Industry Analysis From (2025 to 2033)

Europe Outboard Engines Market Size

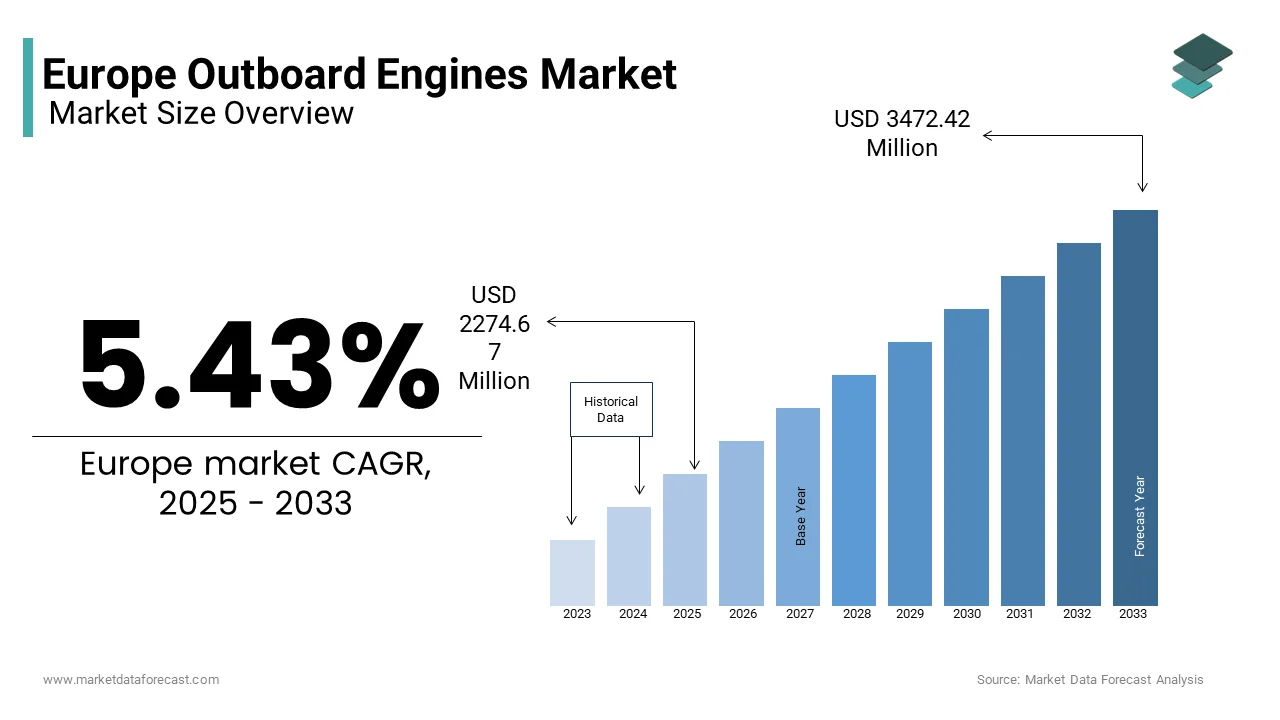

In 2024, the Europe outboard engines market is expected to grow from USD 2157.52 million in 2024 to USD 3472.42 million by 2033, growing at a CAGR of 5.43%.

Outboard engines are propulsion systems mounted externally on the transom of boats, commonly used in recreational, commercial fishing, and maritime patrol vessels. These engines provide mobility, maneuverability, and ease of maintenance, making them a preferred choice across a wide range of small to medium-sized watercraft. In Europe, outboard engines are integral to both leisure boating and professional marine operations, with increasing demand for fuel-efficient and environmentally compliant models. Additionally, advancements in hybrid and battery-powered outboards have begun gaining traction, supported by subsidies and incentives from national governments aiming to reduce carbon footprints in the marine sector. As per the International Council on Clean Transportation (ICCT), over 60% of new outboard engine sales in Western Europe now meet Tier III emission norms, which reflects a clear shift toward cleaner propulsion solutions.

MARKET DRIVERS

Growth in Recreational Boating and Water Sports

One of the primary drivers of the Europe outboard engines market is the growing popularity of recreational boating and water sports across the continent. The increasing disposable incomes, coupled with favorable policies promoting tourism and outdoor leisure activities, have contributed to a surge in private boat ownership and charter services, directly boosting demand for outboard engines. According to the European Travel Commission, leisure travel and outdoor recreation saw a 24% increase in participation post-pandemic, with water-based activities emerging as a preferred form of relaxation among urban populations. Countries such as Sweden, Finland, and Germany reported a notable rise in lake and coastal boating activities, which is leading to higher registrations of personal watercraft equipped with outboard motors. Moreover, the presence of numerous lakes, rivers, and canals has facilitated the expansion of inland waterway tourism, particularly in Eastern and Central Europe.

Regulatory Push for Emission Reductions and Cleaner Technologies

Another key driver shaping the Europe outboard engines market is the increasing regulatory focus on reducing emissions from marine propulsion systems. Governments and environmental agencies across the EU have implemented stringent emission norms, compelling manufacturers to transition from traditional two-stroke engines to cleaner four-stroke and electric alternatives.

Under the European Union’s Recreational Craft Directive (RCD), all new outboard engines must comply with Tier III emission standards, which mandate significantly lower levels of hydrocarbons, nitrogen oxides, and particulate matter. In response, leading companies such as Yamaha Marine and Mercury Marine have accelerated the development of low-emission outboard engines. For instance, Mercury’s new line of Verado engines launched in 2023 incorporated advanced fuel injection systems designed to improve efficiency while reducing environmental impact. Furthermore, national governments are offering subsidies and tax incentives for purchasing eco-friendly engines. Norway, for example, introduced a green incentive program for boat owners opting for zero-emission propulsion by encouraging broader adoption of electric outboards. These regulatory and financial measures are reshaping product portfolios and driving technological innovation within the European outboard engines market.

MARKET RESTRAINTS

High Cost of Electric and Hybrid Propulsion Systems

One of the most significant restraints affecting the Europe outboard engines market is the high cost associated with electric and hybrid propulsion systems. While regulatory pressures and consumer preferences are pushing manufacturers toward cleaner alternatives, the premium pricing of these technologies remains a barrier to widespread adoption among budget-conscious consumers and small-scale operators. Additionally, the limited availability of charging infrastructure on inland waterways and coastal areas hampers the practicality of electric engines for extended use. These cost and infrastructure limitations slow down the transition to greener propulsion technologies, which is creating a challenge for manufacturers seeking to balance sustainability goals with affordability and accessibility in the European market.

Supply Chain Disruptions and Component Shortages

Another critical restraint impacting the Europe outboard engines market is the ongoing disruptions in global supply chains and shortages of essential components such as semiconductors, electronic control units, and raw materials like aluminum and copper. As per McKinsey & Company, the semiconductor shortage that began in 2021 continued to affect automotive and marine industries through 2023, with lead times for microchips used in engine management systems extending beyond 26 weeks in some cases. This scarcity has forced manufacturers like Suzuki Marine and Tohatsu to delay new model launches and limit output capacities. Moreover, the war in Ukraine and trade restrictions imposed by certain countries have disrupted the flow of raw materials, particularly affecting engine casings, wiring harnesses, and electronic modules.

MARKET OPPORTUNITIES

Expansion of Electric and Hybrid Outboard Engine Technologies

An emerging opportunity in the Europe outboard engines market is the rapid expansion of electric and hybrid propulsion technologies, driven by tightening environmental regulations and growing consumer interest in sustainable boating solutions. Companies such as Torqeedo (a subsidiary of DEUTZ AG) and Pure Watercraft have introduced high-performance electric outboards capable of delivering speeds comparable to conventional engines, which is attracting interest from both recreational and commercial users. Additionally, several European cities are promoting zero-emission boating zones in lakes, canals, and protected waterways. For instance, Amsterdam and Berlin have introduced bans on combustion-engine boats in certain inner-city waterways, encouraging the uptake of electric alternatives. National governments are also supporting this transition through grants and tax exemptions for green propulsion systems.

Growth in Boat Sharing and Rental Services

The rise of boat sharing and rental services presents a substantial opportunity for the Europe outboard engines market, particularly in urban and tourist-heavy regions. With increasing demand for short-term recreational boating experiences, there is a growing fleet of rental boats that require durable, easy-to-maintain propulsion systems, making outboard engines an ideal choice. According to Statista, Europe’s shared mobility market grew by 18% in 2023, with boat-sharing platforms expanding in countries such as France, Italy, and Croatia. This trend is particularly evident in Germany, where companies like Boatsharing Berlin and NautiQ have deployed fleets of electric and hybrid boats equipped with modern outboard engines.

MARKET CHALLENGES

Balancing Performance with Environmental Compliance

One of the most pressing challenges facing the Europe outboard engines market is the difficulty of balancing performance requirements with increasingly stringent environmental regulations. Consumers expect powerful, responsive, and durable engines, yet regulatory bodies are imposing tighter limits on emissions, noise levels, and fuel efficiency, forcing manufacturers to rethink design and engineering strategies. For example, the European Union’s Recreational Craft Directive (RCD) mandates strict limits on exhaust emissions, requiring engine makers to incorporate advanced catalytic converters, direct fuel injection, and electronic engine management systems. However, these modifications often result in added weight and complexity, potentially compromising performance metrics such as acceleration and top speed.

Volatility in Raw Material Prices and Energy Costs

Another significant challenge impacting the Europe outboard engines market is the volatility in raw material prices and rising energy costs, which are affecting production economics and profit margins. Outboard engines rely on metals such as aluminum, copper, and steel, all of which have experienced sharp price fluctuations due to geopolitical tensions, trade restrictions, and energy market instability. These cost pressures are compounded by logistical bottlenecks and transportation inflation, which have extended delivery times for imported components. The European Chemical Industry Council noted that shipping lead times from Asia to Europe remained elevated throughout 2023, contributing to inventory shortages and production slowdowns.

Integration of Smart Technologies and Connectivity Features

Another growing challenge for the Europe outboard engines market is the integration of smart technologies and connectivity features into propulsion systems. While companies like Mercury Marine and Yamaha Marine have made strides in this area with products such as the VesselView and Helm Master EX systems, the implementation of such technologies in marine environments poses unique challenges. Additionally, cybersecurity concerns related to connected propulsion systems have raised questions about data privacy and system integrity, especially in commercial and governmental applications. Moreover, retrofitting older vessel fleets with smart outboard engines requires compatibility assessments and additional investments in onboard electrical systems, which the pace of technology adoption.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| CAGR | 4.50% |

| Segments Covered | By Type, Application, And Region. |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, the Czech Republic, and the Rest of Europe. |

| Market Leaders Profiled | SECO GmbH, Yamaha Motor Co., Ltd., Suzuki Motor Corporation, Torqeedo GmbH, Honda Motor Co., Ltd., DEUTZ AG, E.P. Barrus Ltd., Marine Tech, Vector Outboards, and Selva S.p.A. |

SEGMENTAL ANALYSIS

By Type Insights

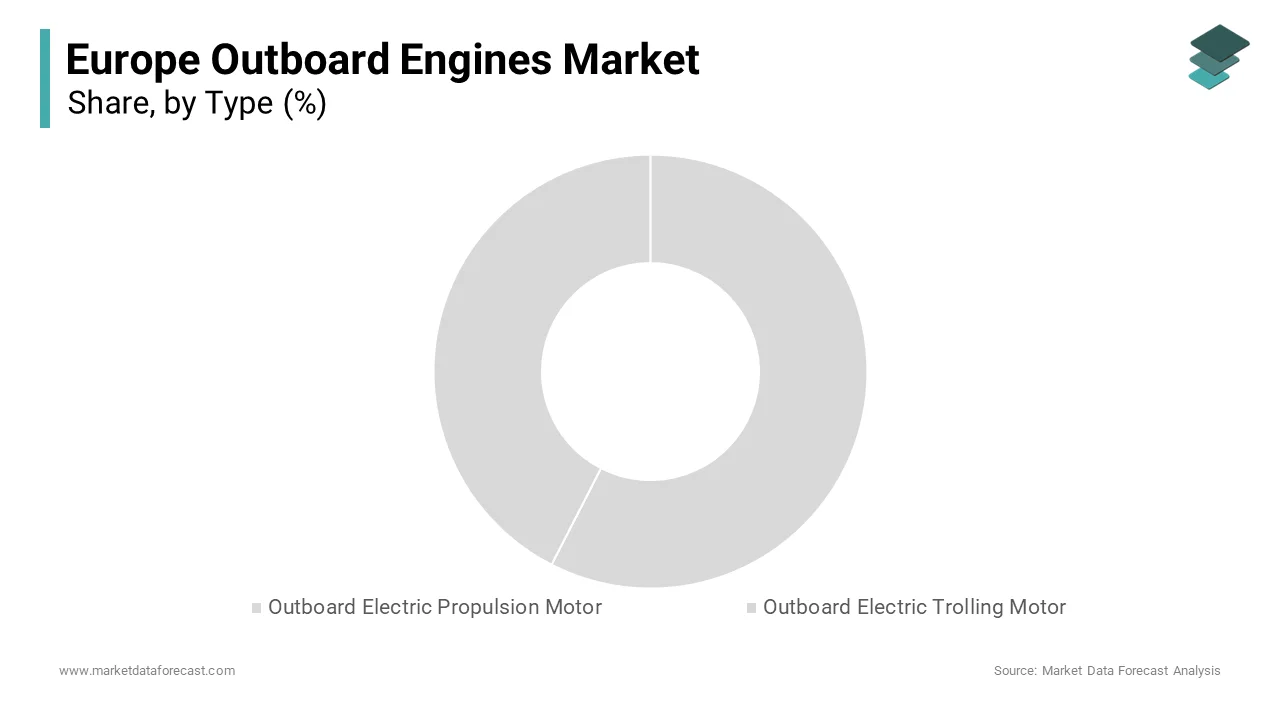

The Outboard Electric Propulsion Motor segment accounted in holding 58.4% of the Europe outboard engines market share in 2024. One key driver behind the widespread use of electric propulsion motors is the European Union’s push for emission-free waterways, particularly in protected lakes, rivers, and urban canals. As per the European Environment Agency (EEA), over 40 cities across Europe have introduced bans or restrictions on combustion engine boats in designated zones, encouraging the uptake of zero-emission alternatives. Additionally, advancements in lithium-ion battery technology and motor efficiency have improved the performance of electric outboards, making them viable replacements for traditional gasoline-powered models. Companies like Torqeedo and Pure Watercraft have launched high-torque, long-range electric propulsion units that appeal to both recreational and commercial users. Moreover, national governments are offering financial incentives for green boating, including tax exemptions and subsidies for purchasing electric outboard engines.

The Outboard Electric Trolling Motor segment is lucratively to grow with an estimated CAGR of 14.7% in the coming years. A major contributing factor is the increasing number of inland fishing destinations and organized angling competitions across countries like Germany, Sweden, and Finland. Furthermore, technological advancements such as GPS integration, autopilot features, and mobile app connectivity have enhanced the functionality of electric trolling motors, attracting tech-savvy users. Major manufacturers like Minn Kota and Raymarine have introduced smart trolling motors with adaptive steering and power management, further boosting consumer interest. In addition, governments and environmental agencies are promoting low-noise boating in ecologically sensitive areas, aligning with conservation efforts and wildlife protection initiatives.

By Application Insights

The Civil Entertainment application segment was the largest and held 45.3% of the Europe outboard engines market share in 2024. One of the primary drivers is the rising participation in leisure boating and water-based tourism, especially among middle- and high-income households. Moreover, the presence of numerous lakes, rivers, and canals has made boating an accessible and popular pastime. Countries such as Sweden and Germany have invested in waterway tourism infrastructure, including marinas, docking stations, and eco-friendly fueling points, which is supporting broader adoption of outboard engines for entertainment purposes. Additionally, boat-sharing platforms and short-term rental services have expanded access to recreational boating, particularly in urban centers.

The Municipal application segment is anticipated to grow with a CAGR of 13.2% throughout the forecast period. A key growth enabler is the expansion of municipal patrol and cleaning operations on city canals and rivers, particularly in urban centers like Amsterdam, Berlin, and Venice. As per the European Environment Agency (EEA), municipal authorities in over 20 European cities have deployed electric-powered patrol boats for surveillance and environmental monitoring, reducing reliance on fossil fuels. Additionally, the rise of zero-emission ferry services and water taxis in metropolitan areas is fueling demand for clean propulsion systems. For instance, Amsterdam’s municipal transport authority integrated 15 new electric patrol boats into its fleet in 2023, equipped with advanced electric outboard motors for silent and sustainable operation.

COUNTRY ANALYSIS

Germany

Germany was the top performer in the Europe outboard engines market by capturing 18.3% of the share in 2024. One of the core drivers is the strong domestic boating culture, which is supported by extensive inland waterways and well-developed marina infrastructure. Additionally, Germany leads in the adoption of electric and hybrid outboard technologies, aided by federal incentives for zero-emission mobility.

France

France was ranked second with 14.3% of the Europe outboard engines market share in 2024. A key growth catalyst is the French government’s initiative to promote sustainable waterway transportation in regions like Provence-Alpes-Côte d'Azur and Brittany, where canal and river tourism is prevalent. The Ministry of Ecological Transition reported that over EUR 200 million was allocated in 2023 for greening inland maritime transport, including subsidies for electric boat purchases. Moreover, Paris’s efforts to integrate water taxis into its public transport network have led to increased deployment of electric outboard engines on Seine River shuttles. As noted by the Paris Port Authority, electric-powered passenger boats accounted for 35% of new municipal contracts in 2023, reinforcing the trend toward cleaner propulsion.

Italy

Italy's outboard engines market growth is expected to have dominant growth opportunities throughout the forecast period. One of the main drivers is the popularity of Lake Garda, Lake Como, and the Amalfi Coast, which attract millions of tourists annually and support a thriving charter and rental industry. The Italian Tourism Board reported that over 500,000 boat rentals occurred in 2023, necessitating durable and easy-to-maintain outboard engines. Additionally, the country is witnessing rising interest in electric propulsion systems, particularly in protected marine reserves and historical canals. Venice, for instance, has implemented strict regulations against combustion engines in certain canals, leading to increased adoption of electric outboards in gondolas and service boats. Government-backed programs such as "Green Mobility on Water" provide financial assistance for transitioning to eco-friendly propulsion, further strengthening Italy’s role in the European outboard engines market.

Sweden

Sweden's outboard engines market is likely to gain huge traction over the growth rate in the coming years, with the early adoption of electric and hybrid propulsion technologies, driven by stringent environmental policies and a strong tradition of lake-based recreation. According to the Swedish Environmental Protection Agency, over 65% of new outboard engine sales in Sweden in 2023 were electric or hybrid models, one of the highest rates in Europe. This transition is supported by national carbon neutrality goals and regional incentives for zero-emission boating. Moreover, Sweden’s vast inland water network, comprising over 95,000 lakes and extensive river systems, supports a large base of private and rental boat operators who increasingly favor electric outboards for their quiet operation and reduced environmental impact.

Netherlands

The Netherlands is also to showcase prominent opportunities for the European outboard engines market growth with the expansion of urban water mobility solutions in cities like Amsterdam and Utrecht. A key growth driver is the Dutch government’s "Blue Mobility Strategy," aimed at integrating waterways into the national transport system. The Ministry of Infrastructure and Water Management reported that over 40 new electric water taxis were deployed in Amsterdam in 2023, all powered by advanced outboard propulsion systems. Additionally, canal tourism and boat-sharing platforms are expanding rapidly.

Russia

Russia's outboard engines market growth is driven by the steady demand driven by both recreational and commercial sectors. As per the Russian State Committee for Water Transport, the number of registered private boats in Russia increased by 12% in 2023 in regions surrounding Lake Baikal and the Volga River.

Additionally, the government has been upgrading maritime search-and-rescue capabilities, requiring specialized outboard engines capable of operating in diverse conditions. Despite geopolitical and supply chain challenges, Russia remains a significant player in the Eastern European outboard engines market, with a consistent demand base and expanding inland waterway utilization.

KEY MARKET PLAYERS

SECO GmbH, Yamaha Motor Co., Ltd., Suzuki Motor Corporation, Torqeedo GmbH, Honda Motor Co., Ltd., DEUTZ AG, E.P. Barrus Ltd., Marine Tech, Vector Outboards, and Selva S.p.A. These are the market players that are dominating the Europe outboard engines market.

Top Players In The Market

Yamaha Marine Group

Yamaha Marine is a global leader in outboard engine technology, known for its reliability, innovation, and broad product range. In Europe, Yamaha holds a strong market position due to its advanced four-stroke engines that combine performance with low emissions. The company plays a pivotal role in shaping industry standards by integrating smart technologies such as digital networking, remote diagnostics, and fuel-efficient propulsion systems. Yamaha’s commitment to environmental sustainability has led to the development of cleaner, quieter engines that align with European emission regulations. Its extensive dealer network and customer-centric service model further reinforce its dominance in the region.

Mercury Marine

Mercury Marine is a key player in the European outboard engines market, offering a diverse portfolio from entry-level to high-performance models. The company is recognized for its innovative engineering, including the development of hybrid propulsion systems and digital control interfaces tailored for recreational and commercial applications. Mercury's dominance is also driven by its investment in R&D and strategic partnerships with boat manufacturers across Europe. With a focus on durability, performance, and user experience, Mercury continues to expand its presence through localized support services and eco-conscious product lines.

Honda Marine

Honda Marine is a trusted name in the European outboard engines sector, known for delivering fuel-efficient, lightweight, and durable propulsion solutions. The company emphasizes technological precision and environmental responsibility, offering a wide range of models that meet stringent European emission norms. Honda’s reputation for reliability and low maintenance costs has made it a preferred choice among private boaters and rental operators. Honda continues to strengthen its foothold in the European market while supporting sustainable boating practices by focusing on clean combustion technologies and compact designs.

Top Strategies Used By Key Market Participants

One of the most impactful strategies used by leading players in the Europe outboard engines market is investing in electric and hybrid propulsion technology. Companies are prioritizing research and development to launch cleaner, more efficient alternatives that comply with strict EU emissions regulations while meeting consumer demand for sustainable boating options.

Another key approach is expanding product portfolios to cater to diverse user segments, including recreational, municipal, and commercial applications. Manufacturers enhance their appeal across both private and institutional buyers by offering modular engine configurations, smart connectivity features, and after-sales service packages.

Strengthening distribution networks and local service infrastructure has become a core strategy for market leaders. Establishing regional service centers, partnering with authorized dealers, and providing training programs ensures seamless customer support and enhances brand loyalty across key European markets.

COMPETITION OVERVIEW

The competition in the Europe outboard engines market is shaped by a combination of established global brands, emerging electric propulsion specialists, and regional manufacturers seeking niche opportunities. Market leaders such as Yamaha Marine, Mercury Marine, and Honda Marine dominate due to their long-standing reputations, technological expertise, and comprehensive product portfolios. These companies benefit from strong brand recognition, extensive dealer networks, and ongoing investments in research and development to maintain their competitive edge. However, the landscape is evolving as new entrants specializing in electric and hybrid propulsion systems challenge traditional players with innovative, eco-friendly alternatives. Companies like Torqeedo and Pure Watercraft are gaining traction by addressing the growing demand for zero-emission boating solutions, particularly in urban waterways and protected natural reserves. Additionally, regulatory pressures and shifting consumer preferences toward sustainability are compelling legacy brands to accelerate their transition to greener technologies. This dynamic environment fosters continuous innovation, prompting firms to differentiate through performance, digital integration, and environmental compliance.

RECENT HAPPENINGS IN THE MARKET

- In January 2023, Yamaha Marine introduced an updated lineup of high-efficiency four-stroke engines designed specifically for European waterways. This initiative was aimed at enhancing fuel economy and reducing emissions, aligning with the region’s tightening environmental regulations and strengthening Yamaha’s position in the premium outboard segment.

- In August 2023, Mercury Marine launched a new line of digitally integrated outboard motors equipped with mobile app connectivity and real-time diagnostics. This move was intended to improve user experience and offer greater control over engine performance by appealing to tech-savvy consumers and professional mariners alike.

- In March 2024, Honda Marine expanded its production capacity in Italy, establishing a dedicated facility to streamline supply chain operations and better serve European customers. This expansion supported faster delivery times and enhanced after-sales service capabilities across major boating hubs in Western and Central Europe.

- In October 2024, Torqeedo, a leader in electric marine propulsion, partnered with several European boat manufacturers to integrate its electric outboards into mass-produced leisure boats. This collaboration was aimed at accelerating the adoption of zero-emission boating and expanding Torqeedo’s footprint in the mainstream market.

- In December 2024, Mercury Marine acquired a German-based battery systems developer, strengthening its ability to develop fully integrated electric outboard solutions. This acquisition was intended to bolster Mercury’s presence in the rapidly growing electric propulsion segment and support its long-term sustainability goals.

MARKET SEGMENTATION

This research report on the Europe outboard Engines Market is segmented and sub-segmented into the following categories.

By Type

- Outboard Electric Propulsion Motor

- Outboard Electric Trolling Motor

By Application

- Civil Entertainment

- Municipal

- Commercial

- Others

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

What is the current market size of the Europe outboard engines market?

The current market size of the Europe outboard engines market was valued at USD 2172.52 Mn by 2024.

What is driving the growth of the outboard engines market in Europe?

The European outboard engines market is growing due to increased recreational boating activities, especially in countries like Germany, France, Italy, and Sweden. Additionally, rising disposable incomes, government initiatives promoting water tourism, and a growing interest in eco-friendly marine propulsion systems are contributing to market expansion.

Who are the market players that are dominated the Europe outboard engines market?

SECO GmbH, Yamaha Motor Co., Ltd., Suzuki Motor Corporation, Torqeedo GmbH, Honda Motor Co., Ltd., DEUTZ AG, E.P. Barrus Ltd., Marine Tech, Vector Outboards, and Selva S.p.A. These are the market players that are dominating the Europe outboard engines market.

Which types of outboard engines are most popular in Europe?

In Europe, mid-range horsepower engines (20–150 HP) dominate the market as they are ideal for both recreational and light commercial use. There's also a growing demand for electric and hybrid outboard engines, particularly in environmentally conscious markets like Norway and the Netherlands

How does environmental regulation affect the outboard engine industry in Europe?

Europe enforces strict emission norms under directives such as the EU Recreational Craft Directive (RCD), which mandates cleaner engine technologies. This has pushed manufacturers to innovate with fuel-efficient and low-emission models, including electric outboards, making sustainability a central focus of product development.

Are electric outboard engines gaining traction in Europe?

Yes, electric outboard engines are gaining popularity across Europe, especially in regions with protected waterways and noise-sensitive areas. Countries like Finland, Denmark, and Austria have seen increased adoption due to stricter regulations on emissions and noise pollution, along with government incentives for green mobility solutions.

Which countries in Europe are leading in outboard engine sales?

Germany leads in terms of volume due to its strong boating culture and robust distribution networks. France and Italy follow closely, driven by coastal tourism and leisure boating. Scandinavian countries, while smaller in volume, show high per capita usage and innovation adoption.

What role do local brands play in the European outboard engine market?

While global players like Yamaha, Mercury, and Honda dominate the market, local European brands and distributors are playing an increasing role in after-sales service, customization, and niche product offerings. Some regional companies specialize in retrofitting and electric conversions, catering to specific national preferences.

How important is the aftermarket segment in Europe’s outboard engines industry?

The aftermarket is highly significant in Europe due to the long lifespan of outboard engines and the emphasis on maintenance and upgrades. Spare parts, servicing, and retrofitting — especially for older engines — form a substantial part of the revenue stream for dealers and independent service providers.

What challenges does the European outboard engines market face?

Key challenges include fluctuating raw material prices, regulatory compliance costs, and seasonal demand patterns tied to weather conditions. Additionally, supply chain disruptions post-pandemic and geopolitical tensions have affected production timelines and import/export logistics.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com