Europe Pecan Market Size, Share, Growth, Trends & Analysis Report, Segmented By Product From, Application, Distribution Channel, By Country (Germany, U.K., Italy, France, Spain, Switzerland, Russia, Turkey, Belgium, Netherlands, Rest of Europe), Industry Analysis From (2026 to 2034)

Europe Pecan Market Report Summary

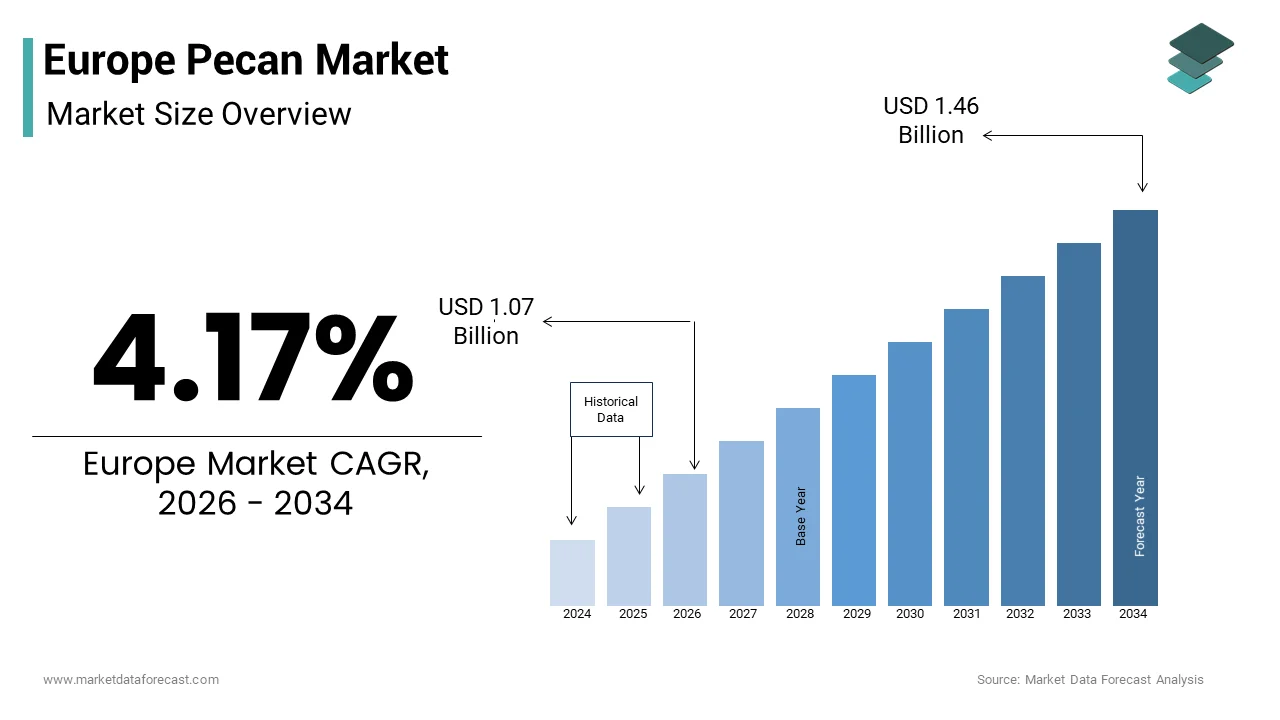

The Europe pecan market was valued at USD 1.03 billion in 2025, is estimated to reach USD 1.07 billion in 2026, and is projected to reach USD 1.46 billion by 2034, expanding at a CAGR of 4.17% during the forecast period from 2026 to 2034. The Europe pecan market is experiencing steady growth, driven by increasing consumer preference for nutrient-rich nuts, rising awareness of healthy snacking habits, and expanding applications of pecans across the food and beverage industry. Growing demand for plant-based ingredients, premium bakery products, breakfast cereals, confectionery, and dairy alternatives is supporting higher pecan consumption across European countries. Consumers are increasingly seeking foods rich in healthy fats, dietary fiber, antioxidants, and plant-based proteins, positioning pecans as a preferred ingredient in health-conscious diets. Furthermore, the expansion of organized retail, premium food imports, and product innovation in functional and gourmet food categories is creating favorable opportunities for long-term market growth across Europe.

Key Market Trends

- Rising consumer interest in healthy snacking is increasing demand for pecans as a natural source of healthy fats, protein, and essential nutrients.

- Food manufacturers are incorporating pecans into premium bakery products, confectionery, cereals, dairy alternatives, and plant-based food formulations.

- Organic, sustainably sourced, and clean-label pecan products are gaining popularity among environmentally conscious consumers.

- Premium retail brands are expanding value-added pecan offerings, including flavored, roasted, and ready-to-eat snack products.

- Growing e-commerce penetration and specialty food retailing are improving consumer access to imported pecans across European markets.

Segmental Insights

Based on product form, the shelled pecans segment accounted for the largest share of the Europe pecan market in 2025. The segment's dominance is driven by greater convenience, reduced preparation time, and widespread utilization in bakery, confectionery, food processing, and household cooking applications.

Based on application, the food and beverage segment held the leading share of the Europe pecan market in 2025. Strong demand from bakery products, desserts, breakfast cereals, snack foods, dairy products, and gourmet culinary applications continues to support the segment's market leadership.

Based on distribution channel, the retail channels segment captured 60.5% of the Europe pecan market share in 2025. Supermarkets, hypermarkets, specialty food stores, and online retail platforms remain the primary sales channels due to their broad product availability, consumer convenience, and expanding premium food assortments.

Regional Insights

Germany led the Europe pecan market by accounting for 21.5% of the regional market share in 2025, supported by strong consumer demand for healthy foods, a well-developed retail sector, and growing consumption of premium nuts and functional ingredients. France maintained a significant market position, driven by its rich culinary tradition and increasing use of pecans in gourmet bakery, confectionery, and specialty food products. The United Kingdom continues to represent an important market despite post-Brexit trade adjustments, supported by stable import volumes and sustained demand for healthy snack ingredients. Italy is steadily expanding its market presence through growing applications of pecans in traditional and modern cuisine, while Spain is strengthening its strategic role as a major import and re-export hub supported by its advanced logistics infrastructure and international trade connectivity.

Competitive Landscape

The Europe pecan market is characterized by the presence of established nut producers, international suppliers, processors, and food ingredient companies competing through product quality, supply chain efficiency, and portfolio diversification. Leading market participants are investing in sustainable sourcing practices, premium product offerings, value-added processing, and advanced packaging technologies to meet evolving consumer preferences. Strategic partnerships with food manufacturers, retailers, and distributors are expanding market reach while strengthening regional supply networks. Companies are also focusing on organic certifications, clean-label positioning, and innovative product formats to capitalize on the growing demand for nutritious, convenient, and premium snack products. As health-conscious consumption and plant-based food trends continue to gain momentum across Europe, product innovation, sustainability, and reliable sourcing will remain essential competitive advantages.

Prominent players in the Europe pecan market include Royalty Pecan Farms, Blue Diamond Growers, Merritt Pecan, Archer Daniels Midland Company, Navarro Pecan Inc., Farmers Investment Co., Diamond Foods, Inc., Humphrey Pecan S.A. de C.V., John B. Sanfilippo and Son Inc., and Stahmanns Inc.

Europe Pecan Market Size

The Europe pecan market size was valued at USD 1.03 billion in 2025 and is anticipated to reach USD 1.07 billion in 2026 to reach USD 1.46 billion by 2034, growing at a CAGR of 4.17% during the forecast period from 2026 to 2034.

Current Introduction and Definition of the Europe Pecan Market

Pecans serve as a premium ingredient in confectionery baking and healthy snacking segments driven by their rich nutritional profile, including high levels of monounsaturated fats and antioxidants. According to sources, the European Union imports approximately 11,800 to 14,000 metric tonnes of pecans annually (varying by season), with the Netherlands, Germany, and Spain acting as the primary entry points and distribution hubs. As per Eurostat, the value of pecan imports into the European Union was estimated at approximately €109 million in recent estimates, while total EU agri-food imports reached roughly €158.6 billion in 2023. According to USDA and International Nut & Dried Fruit Council (INC) data, the United States and Mexico are the dominant producers, collectively accounting for approximately 80–93% of global production. However, the US share alone fluctuates between 40% and 50%, often rivalled or surpassed by Mexico in recent crop years. Consumer awareness regarding heart health benefits has propelled demand as medical institutions increasingly recommend regular nut consumption for cardiovascular wellness. The European Food Safety Authority acknowledges the role of tree nuts in reducing cholesterol levels, which further validates their inclusion in dietary guidelines. Retailers across major cities have expanded their organic and raw nut sections to accommodate this growing interest. Supply chain logistics play a critical role since pecans require careful storage to prevent rancidity due to their high oil content. This market operates within a complex framework of international trade agreements and agricultural policies that shape accessibility and affordability for end consumers throughout the region.

MARKET DRIVERS

Rising Health Consciousness Among European Consumers Drives Pecan Demand

European consumers demonstrate increasing prioritisation of preventive healthcare through dietary choices, which significantly boosts demand for nutrient-rich foods and, in turn, drives the growth of the Europe pecan market. As per the World Health Organization, cardiovascular diseases maintain their status as the leading cause of death across the European region, claiming over 10,000 lives daily and prompting widespread shifts toward heart-healthy eating habits. This alarming statistic has prompted individuals to seek natural solutions for heart health maintenance, leading to a higher incorporation of tree nuts into daily diets. Pecans contain elevated levels of oleic acid and plant sterols, which clinical studies confirm help lower low-density lipoprotein cholesterol levels. The European Society of Cardiology recommends consuming 30 grams of nuts daily as part of a heart-healthy diet, which translates to substantial market potential. As per the Centre for the Promotion of Imports (CBI), European buyers are aggressively expanding their intake of whole foods, placing clean-label products and premium tree nuts into high retail demand. Pecans fit perfectly into this category due to their versatility in both sweet and savoury applications. The rise of functional food trends has further accelerated adoption as manufacturers develop pecan-based snack bars and spreads targeting health-aware demographics. Social media platforms amplify this movement, with nutritionists and influencers promoting pecan recipes that align with Mediterranean and plant-based dietary patterns. This cultural shift toward wellness-orientated consumption creates a robust foundation for sustained growth in the pecan sector across multiple European markets.

Expansion of Plant-Based and Vegan Food Trends Fuels Market Growth

The rapid proliferation of plant-based diets across the region is a powerful factor for pecan consumption as consumers seek alternative protein and fat sources, which further propels the expansion of the Europe pecan market. According to ProVeg International, the European plant-based marketplace is growing rapidly, with approximately 37% of consumers actively reducing their meat intake or adopting entirely plant-centred lifestyles. Pecans provide essential amino acids, healthy fats and minerals that compensate for nutrients typically obtained from animal products, making them indispensable in vegan meal planning. As per the Good Food Institute, retail sales for plant-based foods across major European markets continue to demonstrate multi-billion-euro commercial momentum, expanding the baseline usage of tree nuts in alternative protein applications. Food manufacturers leverage pecans in dairy-free cheeses, meat alternatives and dessert formulations to enhance texture and nutritional value. Major retail chains have dedicated entire aisles to plant-based products, where pecan items feature prominently due to their premium perception. Culinary innovation drives further adoption as chefs incorporate pecans into gourmet vegan dishes that appeal to flexitarians and health-conscious diners. The European Commission supports sustainable food systems through its Farm to Fork Strategy, which encourages reduced animal agriculture and increased plant protein consumption. This policy environment creates favourable conditions for pecan suppliers who position their products as environmentally friendly and ethically sourced. Consumer willingness to pay premium prices for high-quality plant-based ingredients ensures profitable opportunities for market participants who effectively communicate the sustainability and health benefits of pecans.

MARKET RESTRAINTS

Limited Domestic Production Capacity Constrains Supply Availability

The region faces significant geographical and climatic limitations that prevent large-scale domestic pecan cultivation and thereby create dependency on international imports. This restricts the growth of the Europe pecan market. Pecan trees require specific growing conditions, including long, hot summers, mild winters and deep, well-drained soils, which are predominantly found in regions like the southern United States, Mexico and parts of South America. According to EU agricultural data profiles, commercial pecan nut orchards are almost exclusively restricted to microclimates in Southern European countries like Spain and Italy, rendering regional farming outputs negligible compared to global competitors. As per CBI, over 95% of the European pecan supply is sourced externally, leaving consumer markets heavily vulnerable to container freight blockages and international supply chain pressures. Climate variability in producing countries directly impacts European availability, as droughts, floods or extreme weather events in North America can cause sudden price spikes and shortages. According to UN Comtrade database records, the European Union relies continuously on external trading pipelines to satisfy its annual premium pecan supply, sourcing the bulk of its shelled and in-shell varieties directly from the Americas (9%). Transportation costs add another layer of complexity since pecans must travel thousands of kilometres, requiring specialised refrigerated logistics to maintain freshness. Any disruption in shipping routes, port operations or customs procedures immediately affects retail stock levels. This structural dependency limits the ability of European distributors to negotiate favourable terms with suppliers and reduces market resilience during periods of global scarcity. Companies must maintain extensive inventory buffers, which tie up capital and increase operational costs, ultimately affecting profit margins and consumer pricing.

Volatility in Global Currency Exchange Rates Impacts Pricing Stability

Fluctuations in currency exchange rates between the euro and the US dollar create pricing instability for importers in the Europe Pecan market. Because most transactions occur in dollars, this volatility significantly impacts import costs. According to the United States Department of Agriculture (USDA), the dominant volume of global pecans originates within the Americas, which permanently establishes US dollar-denominated financial contracts as the baseline industry standard. When the euro weakens against the dollar, European buyers face higher acquisition costs, which they often pass on to retailers and consumers, leading to reduced demand elasticity. As per the European Central Bank, periodic fluctuations in the EUR/USD exchange rate alter the procurement costs of dollar-denominated commodity contracts for European importers. This currency volatility makes long-term procurement planning difficult for distributors who struggle to predict final landed costs. Small- and medium-sized enterprises lack sophisticated hedging instruments to mitigate foreign exchange risk, leaving them particularly vulnerable to sudden rate changes. Price sensitivity among European consumers means that even modest increases can trigger shifts toward cheaper alternatives such as walnuts or almonds, which may have more stable supply chains. Retailers hesitate to commit to large orders when future pricing remains uncertain, resulting in inconsistent shelf availability. This financial unpredictability discourages new market entrants who perceive the sector as high risk despite strong underlying demand. Established players must absorb some currency losses to maintain competitive positioning, which compresses profitability and limits investment in marketing or product development initiatives.

MARKET OPPORTUNITIES

Emergence of Organic and Sustainable Certification Programs Creates New Avenues

Growing consumer preference for certified organic and sustainably sourced pecans presents substantial growth opportunities for suppliers who can verify ethical production practices in the Europe pecan market. According to the Research Institute of Organic Agriculture (FiBL), Europe’s retail organic market commands multi-billion euro values, reflecting sustained regional buyer demand for verified environmental and social production practices. As per Centre for the Promotion of Imports (CBI) guidelines, gaining official EU organic or sustainable verification enables nut exporters to break into high-end, specialised retail niches and escape generic commodity price traps. Retailers increasingly prioritise suppliers with transparent supply chains as shoppers demand assurance that their purchases support responsible farming methods. The European Green Deal emphasises sustainable agriculture and biodiversity protection, creating regulatory incentives for importing eco-friendly commodities. Distributors who partner with certified orchards can differentiate their offerings through clear labelling and storytelling that resonates with environmentally conscious buyers. Online platforms facilitate direct connections between European consumers and certified producers, enabling traceability from farm to table. This transparency builds trust and loyalty, which translates into repeat purchases and brand advocacy. Speciality stores and health food chains actively seek organic pecan suppliers to expand their curated selections catering to niche demographics. Marketing campaigns highlighting water conservation, soil health and fair labor practices further enhance product appeal. Companies investing in certification processes position themselves advantageously as regulatory requirements tighten and consumer expectations evolve toward greater accountability in food sourcing.

Innovation in Value-Added Pecan Products Expands Application Scope

Development of innovative pecan-based products beyond traditional whole nuts opens diverse revenue streams and attracts broader consumer segments in the Europe pecan market. Food technologists create pecan butter, oils, flours and snack blends that cater to specific dietary needs and culinary preferences. According to research, value-added food processing innovations are driving deep consumer interest in premium tree nut spreads as healthy replacements for legacy confectionery items. Pecan oil commands premium pricing due to its high smoke point and delicate flavour, making it attractive for gourmet cooking and cosmetic applications. Manufacturers incorporate pecan flour into gluten-free baking mixes, addressing the needs of individuals with coeliac disease or wheat sensitivities. Ready-to-eat snack packs featuring roasted, seasoned pecans appeal to busy professionals seeking convenient, healthy options. E-commerce platforms enable direct-to-consumer sales of specialty pecan products, bypassing traditional retail constraints and allowing for personalised marketing. Collaborations between pecan suppliers and artisanal food brands result in unique offerings such as chocolate covered pecans honey glazed varieties or spice-infused mixes that stand out in crowded markets. Product diversification reduces dependence on commodity pricing and enhances brand value through differentiation. Consumer education campaigns demonstrate versatile uses for pecan derivatives, encouraging experimentation in home kitchens. This innovation cycle continuously refreshes market interest and prevents saturation while capturing higher-margin opportunities across multiple product categories.

MARKET CHALLENGES

Climate Change Threatens Long-Term Supply Chain Reliability

An increasing frequency of extreme weather events linked to climate change poses serious risks to pecan production volumes and quality in key growing regions, which challenges the growth of the Europe pecan market. The Intergovernmental Panel on Climate Change warns that rising temperatures and altered precipitation patterns will disrupt agricultural output globally, with nut crops being particularly sensitive to environmental stressors. As per the United States Department of Agriculture (USDA) Pecan Production report, southwestern growing areas face persistent moisture strains that dictate year-to-year volume fluctuations for top-tier improved pecan varieties. These climatic disruptions cause supply shortages that ripple through international markets, affecting European availability and pricing. Prolonged heat waves accelerate pest proliferation, requiring increased pesticide use, which conflicts with organic certification requirements and consumer preferences for clean-label products. Unpredictable frost events during flowering seasons can devastate entire harvests, leaving suppliers unable to fulfil contractual obligations. European importers face heightened uncertainty when planning inventory levels, as historical production data becomes a less reliable predictor of future outcomes. Insurance costs for agricultural operations rise as climate risks intensify, further inflating production expenses. Some growers consider relocating orchards to cooler regions, but this transition requires years of investment before trees reach maturity. The lack of immediate alternatives exacerbates vulnerability since few other nuts replicate the unique flavour and nutritional profile of pecans. Market participants must develop contingency strategies, including diversified sourcing and enhanced storage capabilities, to buffer against climate-induced supply shocks.

Stringent Food Safety Regulations Increase Compliance Burdens

European Union food safety regulations impose rigorous testing and documentation requirements on imported nuts, which further hinders the expansion of the Europe pecan market. This creates operational challenges for pecan suppliers and distributors. The European Food Safety Authority mandates comprehensive screening for contaminants such as aflatoxins, pesticide residues and microbial pathogens, which necessitates advanced laboratory facilities and frequent inspections. Non-compliance results in product recalls, border rejections and reputational damage that can permanently exclude suppliers from the European market. As per the European Rapid Alert System for Food and Feed (RASFF), persistent border monitoring highlights that contamination issues like high aflatoxin levels remain a primary cause for enforcement actions against incoming edible nut shipments. Small-scale producers in developing countries often lack resources to meet these stringent standards, limiting the pool of qualified suppliers and concentrating market power among large corporations. Compliance costs include certification fees, testing expenses and administrative overhead, which reduce profit margins, especially for smaller operators. Traceability requirements demand detailed record-keeping from orchard to retail shelf, requiring sophisticated digital systems that many traditional farmers do not possess. Language barriers and differing regulatory interpretations between exporting and importing countries create additional friction in documentation processes. Delays at customs due to incomplete paperwork or failed inspections disrupt supply chains and increase holding costs. Companies must invest continuously in training staff, updating protocols and auditing suppliers to maintain compliance status. This regulatory complexity acts as a barrier to entry for new participants and increases operational risks for existing players who must navigate an evolving landscape of food safety expectations.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 4.17% |

| Segments Covered | By Product Form, Application, Distribution Channel, And By Country |

| Various Analyses Covered | Global, Regional & Country Level Analysis; Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic & Rest of Europe |

| Market Leaders Profiled | Royalty Pecan Farms, Blue Diamond Growers, Merritt Pecan, Archer Daniels Midland Company, Navarro Pecan Inc, Farmers Investment Co, Diamond Foods, Inc, Humphrey Pecan S.A. de C.V., John B. Sanfilippo and Son Inc., Stahmanns Inc |

SEGMENTAL ANALYSIS

By Product Form Insights

The shelled pecans segment was the largest in the European market and occupied a commanding share in 2025. This prominence of the segment was credited to its immediate usability and convenience for modern consumers. The main driver for this dominance is the shift toward ready-to-eat and easy-to-prepate food options among busy urban populations across major European cities. According to the Centre for the Promotion of Imports (CBI), shelled pecans dominate European imports because regional snack manufacturers, confectioners, and consumers heavily favour pre-shelled convenience to avoid traditional manual extraction. This preference aligns with broader lifestyle trends where efficiency in meal preparation is highly valued. Shelled pecans integrate seamlessly into baking recipes, salad toppings and snack mixes without requiring additional processing steps. Retailers favour shelled products because they offer higher profit margins per unit weight and occupy less shelf space compared to bulky in-shell varieties. The food industry also drives demand as manufacturers require consistent quality and uniform size for industrial applications such as confectionery coatings and bakery inclusions. Shelled pecans reduce waste for commercial buyers who do not have the infrastructure to handle shell disposal. Furthermore, the perceived hygiene and safety of pre-packaged shelled nuts appeal to health-conscious consumers who worry about contamination during manual cracking. This segment benefits from advanced sorting and packaging technologies that ensure freshness and prevent rancidity, which is critical for maintaining consumer trust in premium nut products.

On the other hand, the in-shell pecans segment is on the rise and is expected to be the fastest-growing segment in the market by witnessing a CAGR of 6.2% from 2026 to 2034 due to its popularity as festive gifts and novelty snack items. The growth is primarily fuelled by the cultural tradition of gifting premium nuts during holiday seasons, particularly Christmas and Easter, in countries like Germany, France and the United Kingdom. As per the International Nut and Dried Fruit Council (INC), in-shell pecan demand across European wholesale channels experiences sharp seasonal surges around autumn and winter holiday periods, aligning with legacy consumer preferences for festive holiday roasting traditions. In-shell pecans offer an interactive eating experience that appeals to younger demographics looking for engaging snacking activities. Social media trends showcasing unboxing and cracking videos have amplified interest in whole- nuts as entertainment-focused food items. Specialty retailers capitalise on this trend by offering aesthetically pleasing packaging and mixed nut assortments that feature in-shell pecans as premium components. The novelty factor attracts consumers who view the cracking process as a mindful activity that slows down consumption and enhances enjoyment. Additionally, in-shell pecans have a longer shelf life since the shell protects the kernel from oxidation and moisture, allowing distributors to maintain inventory for extended periods without quality degradation. This characteristic reduces spoilage rates and improves profitability for sellers who can store products seasonally. The segment also benefits from sustainable packaging initiatives, as shells are biodegradable and reduce plastic usage compared to vacuum-sealed shelled nut packs.

By Application Insights

In 2025, the food and beverage segment held the majority share of the Europe pecan market because of the widespread incorporation of pecans in baked goods, confectionery, and dairy products. Pecans' ability to enhance flavour, texture, and nutrition across various foods drives the segment's market dominance. According to sources, premium industrial bakers are steadily diversifying their ingredient formulations, integrating tree nuts like pecans into high-end artisanal pastries, cookies, and health-focused snack bars to satisfy growing consumer interest in clean-label products. Chocolate manufacturers extensively use pecans in bars, pralines and truffles, creating high-value products that command premium pricing in retail channels. The rise of artisanal food movements has further boosted adoption as chefs and small-batch producers seek distinctive ingredients to differentiate their offerings. Pecans pair exceptionally well with European culinary traditions, including French patisserie, German chocolate making and Italian gelato production. Health-orientated food brands incorporate pecans into granola bars, breakfast cereals and plant-based milk alternatives to boost protein and healthy fat content. The snack food industry leverages pecans in trail mixes and roasted nut blends, targeting health-conscious consumers seeking convenient nutrition. Food-Service establishments, including cafes and restaurants, feature pecan-crusted dishes and desserts on menus to attract discerning diners. This broad application base ensures steady demand regardless of seasonal fluctuations in other sectors. The ability of pecans to complement both sweet and savoury profiles makes them indispensable in product development pipelines across the food industry.

However, the dietary supplements segment is expected to exhibit a noteworthy CAGR of 7.5% during the forecast period owing to increasing consumer focus on preventive healthcare and natural wellness solutions. Scientific validation of pecan nutrients, such as antioxidants, vitamin E, and magnesium, is fuelling the growth of this segment. Consequently, these nutrients are extracted for use in capsule and powder formulations. As per studies, the functional food and nutraceutical industries are expanding their utilisation of tree nut oils and extracts to capitalise on consumer interest in natural vitamin E, zinc, and healthy monounsaturated fatty acids. Consumers increasingly prefer whole-food-based supplements over synthetic alternatives, believing that nutrients from natural sources offer superior absorption and efficacy. Pecan oil capsules are marketed for heart health and skin vitality, appealing to ageing demographics seeking anti-ageing benefits. Fitness enthusiasts consume pecan protein powders as part of post-workout recovery routines due to their balanced amino acid profile. The clean label movement supports this growth as shoppers avoid artificial additives and preservatives commonly found in conventional supplements. Online health platforms educate consumers about the specific benefits of pecan compounds, such as ellagic acid and flavonoids, driving informed purchasing decisions. Regulatory support for natural health products under the European Union's traditional herbal medicinal products directive facilitates market entry for pecan-based supplements. Manufacturers invest in clinical trials to substantiate health claims, which builds consumer trust and justifies premium pricing. This segment benefits from cross-promotion with fitness influencers and nutritionists who endorse pecan supplements as part of holistic wellness regimes.

By Distribution Channel Insights

The retail channels segment dominated the Europe pecan market and accounted for a 60.5% share in 2025. This dominance of the segment was driven by its widespread presence and direct consumer access. One of the major drivers of this segment is the ability of retail networks to provide immediate product availability and diverse brand choices under one roof. According to CBI, conventional supermarkets, specialised healthy food shops, and premium grocery chains serve as the primary distribution networks for getting packaged pecan products directly to end consumers. Major supermarket chains such as Carrefour, Tesco and Aldi have expanded their premium nut sections featuring organic and imported pecan varieties to cater to evolving consumer preferences. Private label brands offered by retailers provide cost-effective alternatives that attract price-sensitive shoppers while maintaining quality standards. Specialty health food stores contribute significantly by offering curated selections of raw, organic and fair-trade pecans that appeal to niche demographics. Retail promotions and seasonal displays during holidays drive impulse purchases and introduce new customers to pecan products. The convenience of one-stop shopping encourages bulk-buying behaviour, especially among families who stock up on healthy snacks. Retailers also benefit from established supply chain relationships that ensure consistent stock levels and competitive pricing. In-store sampling events and educational signage help consumers understand the benefits of pecans, fostering loyalty and repeat purchases. The physical presence of retail stores allows for immediate gratification, which online channels cannot fully replicate for perishable goods.

Apart from these, the wholesale and bulk buyers segment is predicted to witness the highest CAGR of 5.8% between 2026 and 2034. This quick surge of the segment is propelled by increasing demand from food manufacturers, bakeries and institutional clients seeking cost-effective sourcing solutions. Industrial food production facilities across Europe are expanding rapidly. This growth is fuelled by their need for large volumes of consistent quality pecans for processing. As per sources, industrial food processors choose to source raw pecans through massive wholesale contract volumes, which lets them hedge against seasonal price volatility and secure stable raw materials for downstream snack manufacturing. Bulk buyers benefit from economies of scale that lower per-unit prices, enabling competitive positioning in final product markets. Food service providers, including hotel chains, catering companies and restaurant groups, purchase pecans in bulk to maintain menu consistency and control expenses. The rise of cloud kitchens and delivery-only brands has further accelerated bulk purchasing as these operations prioritise efficiency and standardised ingredients. Wholesale distributors offer value-added services such as custom grading, packaging and logistics support that simplify procurement for industrial clients. Direct contracts between growers and bulk buyers ensure traceability and quality assurance, which is critical for meeting regulatory standards. This channel also serves smaller retailers who lack the volume to negotiate directly with international suppliers relying on wholesalers for aggregated shipments. The flexibility of wholesale arrangements allows buyers to adjust order quantities based on seasonal demand fluctuations, reducing inventory risks. Digital B2B platforms facilitate transparent pricing and efficient ordering processes, enhancing the attractiveness of wholesale channels for diverse buyer segments.

COUNTRY-LEVEL ANALYSIS

Germany Pecan Market Analysis

Germany maintained the lead in the Europe pecan market and captured a 21.5% share in 2025. This leading position of the German market was attributed to a robust economy, high disposable income and strong cultural affinity for nuts and baked goods. As per European trade data distributed by Tridge, Germany represents a premier entry hub in Europe for raw pecan nuts, registering over 6.5 million kilograms in annual import demands. German consumers prioritise quality and sustainability, leading to high demand for organic and fair-trade- certified pecans. The extensive bakery sector in Germany utilises pecans in traditional pastries, breads and Christmas stollen, creating steady industrial demand. Retail chains such as Rewe and Edeka have expanded their premium nut offerings, catering to health-conscious shoppers who view pecans as essential dietary components. The presence of major food processing companies in Germany facilitates large-scale procurement and value-adding activities. Consumer awareness campaigns by health organisations promote nut consumption for cardiovascular benefits, further boosting retail sales. Germany serves as a re-export hub for neighbouring countries, leveraging its strategic location and efficient logistics infrastructure. The country hosts numerous trade fairs and food exhibitions that showcase innovative pecan products, fostering business connections and market expansion. Strict adherence to food safety standards ensures high-quality imports that meet consumer expectations. The growing vegan population in Germany drives demand for plant-based proteins, including pecans, which are incorporated into meat alternatives and dairy-free products.

France Pecan Market Analysis

France followed closely behind in the Europe pecan market because of its renowned culinary heritage and increasing integration of international ingredients into gourmet cuisine. According to the Centre for the Promotion of Imports (CBI), France is systematically categorised among the largest Western European buyers, offering competitive business opportunities for edible nut and pecan exporters. French chefs and patissiers incorporate pecans into haute cuisine dishes, chocolates and desserts, elevating their status as premium ingredients. The rise of fusion cuisine has introduced pecans to traditional French recipes, creating novel flavour combinations that appeal to adventurous diners. Specialty food boutiques and artisanal markets feature locally roasted and seasoned pecans, attracting tourists and locals alike. Consumer interest in healthy snacking has increased retail sales of packaged pecans in urban areas. The French government supports sustainable agriculture through policies that encourage imports of eco-friendly products aligning with pecan suppliers who emphasise environmental stewardship. Wine pairing trends have also boosted pecan consumption as sommeliers recommend nut accompaniments for certain vintages. Online gourmet food platforms facilitate direct sales of premium pecan products reaching niche audiences nationwide. The hospitality sector, including luxury hotels and restaurants, drives demand for high-quality pecans used in signature dishes. Cultural appreciation for fine dining ensures that pecans remain associated with sophistication and quality influencing purchasing behavior across demographic segments.

United Kingdom Pecan Market Analysis

The United Kingdom holds a strong position in the Europe pecan market despite post-Brexit trade adjustments, maintaining steady import volumes driven by strong consumer demand for healthy snacks and baking ingredients. As per sources, the United Kingdom tracks closely behind Germany and the Netherlands in European raw pecan nut demand, recording an individual volume threshold of approximately 4.05 million kilograms. British consumers have embraced plant-based diets and health-conscious eating habits, boosting retail sales of raw and roasted pecans. Major supermarket chains, including Tesco, Sainsbury's and Waitrose, have expanded their world food aisles featuring premium nut varieties. The vibrant bakery sector in the UK utilises pecans in cakes, scones and breads, supporting industrial demand. Online grocery shopping has facilitated easier access to specialty pecan products, reaching rural and urban consumers alike. Trade agreements with non-EU countries have diversified supply sources, reducing dependency on single markets. Consumer education initiatives by health charities promote nut consumption for heart health, driving awareness and adoption. The hospitality industry recovers steadily post-pandemic, with restaurants reintroducing pecan-based menu items. Seasonal traditions such as Christmas puddings and mince pies sustain demand during winter months. The UK market benefits from high English proficiency among international suppliers, facilitating smoother communication and contract negotiations. Innovation in packaging and branding appeals to younger demographics who value convenience and aesthetic appeal in food products.

Italy Pecan Market Analysis

Italy gradually expanded in the European pecan market. It integrates pecans into both traditional and modern culinary practices, driving steady market growth through diverse application channels. As per the Ministry of Foreign Affairs CBI market reports, Italy positions itself as one of the major consumer environments for imported processed edible nuts, though its volume is outpaced by core Northern European logistics hubs. Italian confectioners use pecans in torrone nougat and chocolate creations, blending local traditions with international ingredients. The rising popularity of healthy Mediterranean diet variations includes pecans as nutrient-dense additions to salads and pasta dishes. Retailers such as Coop and Conad have introduced private-label organic pecan lines catering to health-aware consumers. The tourism sector boosts demand as visitors seek authentic food experiences featuring premium local and imported ingredients. Italian food manufacturers export pecan-containing products to other European markets, leveraging the country's reputation for quality food production. Government initiatives promoting sustainable food systems align with ethical sourcing practices of major pecan suppliers. Urban centres like Milan and Rome host food festivals that showcase innovative nut-based recipes, fostering consumer interest. The growth of e-commerce platforms enables direct sales of artisanal pecan products from small producers to nationwide audiences. Culinary schools incorporate pecan usage in curricula, training future chefs to utilise versatile ingredients. The combination of tradition and innovation ensures sustained relevance of pecans in the Italian food landscape.

Spain Pecan Market Analysis

Spain emerges as a key player in the Europe pecan market by leveraging its strategic geographic location and port infrastructure to facilitate pecan imports and re-exports. According to Eurostat, Spain handles a verified 9% of the European Union's total imported pecan volumes to satisfy rising domestic demand for premium healthy snacks. Spanish consumers increasingly adopt healthy snacking habits, driving domestic retail demand for packaged pecans. The hospitality industry in tourist destinations incorporates pecans into menus catering to international visitors familiar with nut-based cuisines. Local food processors use pecans in turrón and other traditional sweets, creating seasonal demand spikes. The government supports agricultural diversification, including experimental pecan cultivation in suitable microclimates, although volumes remain small. Retail chains like Mercadona and Carrefour Spain expand their healthy food sections featuring imported nuts. E-commerce growth enables wider reach of specialty pecan products to rural areas. Trade relations with Latin American suppliers provide alternative sourcing options, enhancing supply chain resilience. The Mediterranean diet's emphasis on nuts and healthy fats aligns with pecan nutritional profiles, driving consumer acceptance. Food safety authorities enforce strict quality controls, ensuring high standards for imported products. The combination of logistical advantages and growing domestic consumption positions Spain as a vital node in the European pecan supply network.

COMPETITIVE LANDSCAPE

The competition in the Europe pecan market is characterized by a mix of international giants and specialized regional distributors who vie for consumer attention through quality innovation and branding. Large multinational corporations leverage their extensive supply chains and economies of scale to offer competitive pricing and consistent availability to major retail chains. These players invest heavily in marketing and product development to differentiate their offerings in a crowded marketplace. Smaller niche suppliers focus on premium organic and fair trade certifications to attract discerning customers willing to pay higher prices for ethical and sustainable products. The market sees intense rivalry in the retail segment where private label brands from supermarkets challenge established names by offering cost effective alternatives. Industrial buyers negotiate aggressively for bulk contracts pushing suppliers to optimize operational efficiency and reduce costs. Innovation in value added products such as seasoned snacks and nut butters creates new battlegrounds for competition as companies seek to capture emerging trends. Regulatory compliance acts as a barrier to entry ensuring that only well capitalized firms can maintain consistent access to the market. The dynamic nature of consumer preferences requires continuous adaptation and strategic agility from all participants to sustain relevance and profitability in this evolving sector.

KEY MARKET PLAYERS

A dominating market players that are in the Europe pecan market are

- Royalty Pecan Farms

- Blue Diamond Growers

- Merritt Pecan

- Archer Daniels Midland Company

- Navarro Pecan Inc

- Farmers Investment Co

- Diamond Foods, Inc

- Humphrey Pecan S.A. de C.V.

- John B. Sanfilippo and Son Inc.

- Stahmanns Inc

Top Players In The Market

- Blue Diamond Growers maintains a significant presence in the European pecan market through its extensive distribution network and strong brand recognition. The cooperative leverages its global sourcing capabilities to ensure consistent supply of high quality shelled and in shell pecans to major retailers across the continent. Recent initiatives include launching premium organic pecan lines tailored to health conscious European consumers who prioritize sustainable and clean label products. The company has strengthened partnerships with leading supermarket chains in Germany and France to expand shelf visibility. Investment in advanced packaging technologies helps preserve freshness and extend shelf life which is critical for maintaining product quality during long distance transportation. Blue Diamond also engages in consumer education campaigns highlighting the nutritional benefits of pecans to drive demand. Their strategic focus on innovation includes developing value added products such as roasted and seasoned varieties that appeal to diverse taste preferences. These actions reinforce their position as a trusted supplier in the competitive European landscape.

- John B Sanfilippo and Son Inc operates prominently in the Europe pecan market under its Fisher Nuts brand offering a wide range of premium nut products. The company focuses on delivering high quality pecans through established relationships with European distributors and retail partners. Recent efforts involve expanding their portfolio of convenience focused snacks including single serve packs and mixed nut blends featuring pecans. They have invested in sustainability initiatives by sourcing from certified orchards to meet growing consumer demand for ethically produced food items. The company enhances its market position through targeted marketing campaigns that emphasize the superior taste and texture of their pecans. Participation in major European food trade shows allows them to showcase new product innovations and connect with potential business partners. Their commitment to quality control ensures that all products meet strict European food safety standards. This dedication to excellence and customer satisfaction helps them maintain a loyal consumer base across multiple countries.

- Archer Daniels Midland Company plays a crucial role in the Europe pecan market by supplying bulk ingredients to food manufacturers and industrial clients. The multinational corporation utilizes its vast logistics network to facilitate efficient import and distribution of pecans throughout the region. Recent strategies include enhancing traceability systems to provide transparency in sourcing which appeals to brands committed to responsible supply chain practices. The company has expanded its processing facilities to offer customized pecan products such as chopped pieces and flour for bakery and confectionery applications. Collaborations with local European partners enable them to better understand regional preferences and adapt their offerings accordingly. Investment in research and development leads to innovative ingredient solutions that help clients create unique food products. Their focus on operational efficiency and reliability makes them a preferred supplier for large scale food production. These efforts strengthen their reputation as a key provider of high quality pecan ingredients in the European market.

Top Strategies Used By Key Market Participants

Key players in the Europe pecan market employ several strategic approaches to enhance their competitive positioning and drive growth. Product differentiation remains a primary strategy as companies introduce organic and sustainably sourced pecans to cater to health conscious consumers. Innovation in packaging technologies helps preserve freshness and appeal to environmentally aware shoppers who prefer eco friendly materials. Strategic partnerships with local distributors and retailers enable broader market reach and improved shelf visibility across diverse regions. Companies invest in digital marketing campaigns to educate consumers about the nutritional benefits of pecans and promote versatile usage ideas. Expansion into value added segments such as flavored snacks and nut butters allows firms to capture higher margins and reduce dependence on commodity pricing. Supply chain optimization through direct sourcing from growers ensures consistent quality and reduces costs associated with intermediaries. Compliance with stringent European food safety regulations builds trust and facilitates smoother market entry. These combined strategies help participants navigate challenges and capitalize on emerging opportunities in the dynamic European landscape.

MARKET SEGMENTATION

This research report on the Europe pecan market is segmented and sub-segmented into the following categories.

By Product

- In-Shell

- Shelled

By Application

- Food & Beverage

- Cosmetics & Personal Care

- Dietary Supplements

By Distribution Channel

- Retail (Online & Offline)

- Foodservice & Industrial

- Wholesale & Bulk Buyers

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

Why is the Europe pecan market experiencing steady growth?

The market is expanding due to rising consumer demand for healthy snacks, increasing awareness of the nutritional benefits of tree nuts, and growing use of pecans in food processing and bakery products.

What are pecans and why are they becoming popular in Europe?

Pecans are nutrient-rich tree nuts valued for their healthy fats, protein, fiber, vitamins, and antioxidants, making them popular in snacks, desserts, and functional foods.

Which product segment accounts for the largest share of the Europe pecan market?

Raw and shelled pecans account for the largest market share due to their widespread use in retail, baking, confectionery, and healthy snack products.

How do pecans contribute to a healthy diet?

Pecans provide heart-healthy fats, dietary fiber, antioxidants, vitamins, and minerals that support cardiovascular health, digestion, and overall wellness.

What factors are driving the growth of the Europe pecan market?

Increasing health consciousness, growing demand for plant-based nutrition, rising consumption of premium snack foods, and expanding applications in bakery and confectionery products are driving market growth.

Which industries generate the highest demand for pecans?

Food and beverage manufacturers, bakery and confectionery companies, snack producers, retailers, restaurants, and nutraceutical manufacturers are the primary end users.

What trends are shaping the future of the Europe pecan market?

Organic pecans, clean-label snacks, plant-based foods, premium nut products, sustainable sourcing, and innovative nut-based ingredients are shaping the market.

How are manufacturers improving pecan products to meet changing consumer preferences?

Manufacturers are introducing value-added snack options, improving packaging for freshness, expanding organic product lines, and developing flavored and ready-to-eat pecan products.

What challenges could affect the growth of the Europe pecan market?

Fluctuating raw material prices, climate-related supply risks, import dependence, changing consumer spending patterns, and supply chain disruptions could affect market growth.

Which countries are expected to lead the Europe pecan market?

Germany, the United Kingdom, France, Italy, and Spain are leading markets due to rising demand for healthy foods, premium snacks, and nut-based ingredients.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com