Europe Phase Change Materials Market Size, Share, Trends & Growth Forecast Report By Type (Organic, Inorganic, Eutectic), Application (Building & Construction, HVAC, Cold Chain & Packaging, Electronics), and Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, Rest of Europe) – Industry Analysis From 2025 to 2033.

Europe Phase Change Materials Market Size

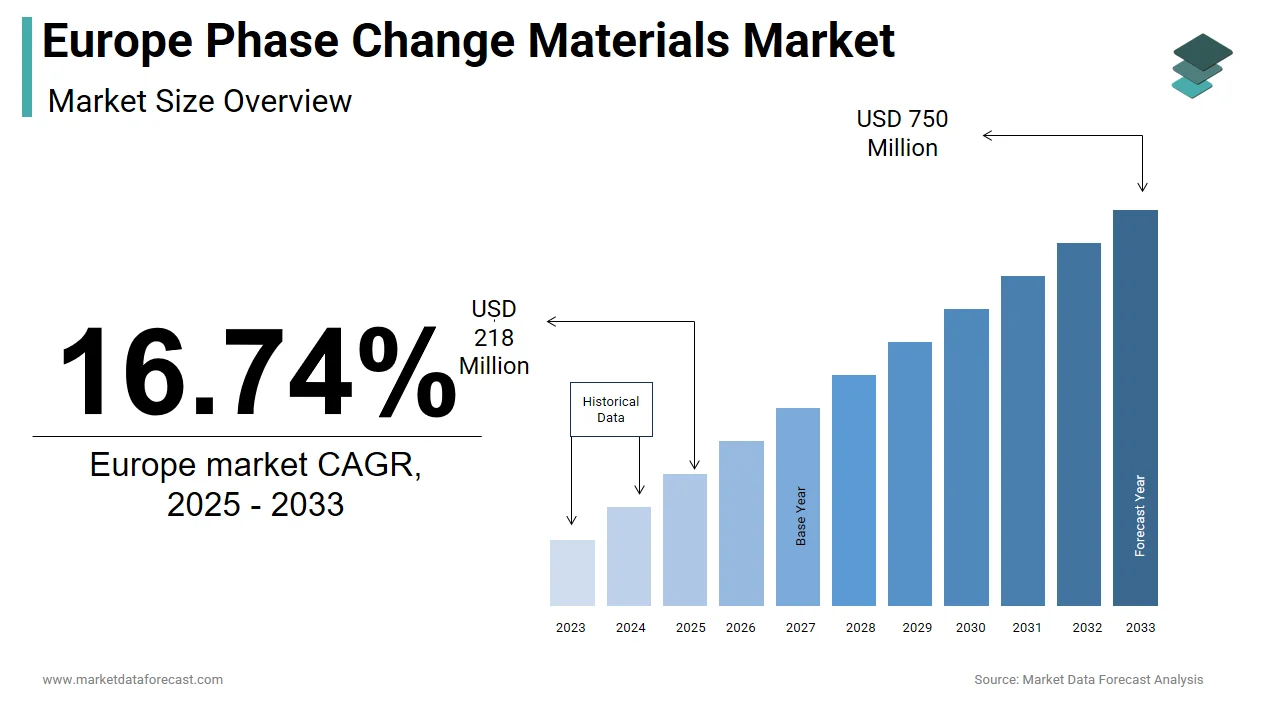

The phase change materials market size in Europe was valued at USD 186.35 million in 2024. The European market is estimated to be worth USD 750 million by 2033 from USD 218 million in 2025, growing at a CAGR of 16.74% from 2025 to 2033.

The Europe phase change materials (PCMs) market is witnessing steady growth. It is driven by advancements in thermal energy storage technologies and increasing demand for sustainable solutions. The region's focus on renewable energy integration has bolstered PCM adoption across industries such as construction and HVAC. Also, Germany leads the regional market by contributing a notable share of the total revenue. This dominance of the market is due to stringent energy efficiency regulations and government incentives promoting green technologies. Furthermore, the European Union’s Green Deal initiative, which aims for carbon neutrality by 2050, has created a favorable environment for PCM innovations. Despite economic uncertainties, the market remains resilient, supported by rising investments in smart buildings and cold chain logistics.

MARKET DRIVERS

Rising Demand for Energy-Efficient Building Solutions

The growing emphasis on reducing energy consumption in buildings is a key driver for the Europe PCM market. According to Eurostat, residential and commercial buildings account for nearly 40% of the EU’s total energy use. PCMs are being increasingly incorporated into walls, ceilings, and floors to stabilize indoor temperatures and lessen dependence on heating and cooling systems. For instance, incorporating PCMs in building materials can lower energy costs significantly. This trend aligns with the European Commission’s Energy Performance of Buildings Directive, which mandates improved insulation standards.

Expansion of Cold Chain Logistics

The surge in cold chain logistics is another significant driver. This aspect is fueled by the pharmaceutical and food industries. PCMs are critical in maintaining temperature-sensitive shipments, ensuring product integrity during transportation. Also, Companies like Croda International have capitalized on this trend, developing bio-based PCMs tailored for perishable goods. With the rise of e-commerce and stricter regulatory frameworks, the demand for reliable thermal management solutions is set to escalate further.

MARKET RESTRAINTS

High Initial Costs

A primary barrier to PCM adoption is the high upfront investment required for implementation. Integrating PCMs into building infrastructure can initially increase construction costs. This financial burden often deters small and medium enterprises (SMEs) from adopting these technologies. Additionally, the payback period for PCM installations typically ranges from 5 to 10 years, which may not align with short-term business goals. A significant number of SMEs in Europe consider sustainability initiatives financially viable. Consequently, cost sensitivity remains a significant restraint, limiting widespread adoption despite long-term benefits.

Technical Limitations and Material Constraints

Technical challenges associated with PCM performance also hinder market growth. As per insights from the European Materials Research Society, certain PCMs exhibit low thermal conductivity, reducing their efficiency in real-world applications. Moreover, material degradation over time poses durability concerns, particularly in extreme climates. For example, paraffin-based PCMs, widely used in HVAC systems, degrade by approximately 10% after five years of continuous use, according to a report by the Fraunhofer Institute. These limitations necessitate frequent replacements, adding to operational costs.

MARKET OPPORTUNITIES

Advancements in Bio-Based PCMs

The development of bio-based PCMs presents a lucrative opportunity for the European market. These eco-friendly alternatives are gaining traction due to their biodegradability and reduced carbon footprint. Companies like Climator AB are pioneering innovations in plant-derived PCMs, targeting the burgeoning demand for sustainable solutions. With the EU’s Circular Economy Action Plan emphasizing renewable resources, bio-based PCMs are poised to capture a significant share of the market.

Integration with Smart Technologies

The convergence of PCMs with smart technologies offers another promising avenue. PCMs integrated with IoT-enabled systems enable real-time monitoring and optimization of thermal energy usage. For instance, Honeywell’s recent innovations demonstrate how PCMs combined with AI-driven analytics can enhance energy efficiency. This synergy aligns with the European Smart Cities Initiative, which promotes intelligent urban infrastructure. The growing adoption of smart cities across Europe positions PCMs as a critical enabler of next-generation energy management systems.

MARKET CHALLENGES

Regulatory Hurdles

Navigating complex regulatory frameworks poses a significant challenge for PCM manufacturers. According to the European Chemicals Agency, compliance with REACH regulations requires extensive testing and documentation, increasing operational burdens. Small-scale innovators often struggle to meet these stringent requirements, limiting their ability to compete. Furthermore, disparities in national policies across member states create additional hurdles. For example, France mandates specific fire safety standards for PCMs, while Germany focuses on environmental impact assessments.

Lack of Awareness and Expertise

A pervasive lack of awareness about PCM benefits and implementation methods impedes market penetration. The European Construction Industry Federation notes that a significant portion of construction professionals are familiar with advanced thermal storage technologies. This knowledge gap results in underutilization, particularly among smaller firms. Additionally, the absence of standardized training programs exacerbates the issue. Without adequate expertise, potential users hesitate to invest in PCMs, fearing suboptimal outcomes.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| Segments Covered | By Type, Application, and Region. |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, and the Rest of Europe. |

| Market Leaders Profiled | Honeywell International Inc. (US), DuPont de Nemours, Inc. (US), Croda International Plc (UK), Boyd Corporation (US), Sasol Limited (South Africa), Outlast Technologies LLC (US), Climator Sweden AB (Sweden), Rubitherm Technologies GmbH (Germany), PureTemp LLC (US), Phase Change Solutions (US), and others. |

SEGMENTAL ANALYSIS

By Type Insights

The organic PCMs segment dominated the Europe market by holding a share of 58.4% in 2024. Their popularity is credited to superior thermal stability and compatibility with various applications. Paraffin waxes, a subset of organic PCMs, are widely used in HVAC systems due to their high latent heat capacity. Organic PCMs can cut energy consumption by up to 30.1% in commercial buildings. This segment’s place is further reinforced by ongoing R&D efforts aimed at enhancing performance metrics, ensuring sustained demand.

The eutectic PCMs segment is the fastest-growing segment, with a CAGR of 9.2% projected through 2033. This rapid expansion is attributed to their versatility in cold chain applications. According to the European Cold Chain Federation, eutectic PCMs are ideal for maintaining precise temperature ranges, making them indispensable in pharmaceutical logistics.

By Application Insights

Building & Construction held the largest market share at 42.7% in 2024. This dominance of the segment is fueled by stringent energy efficiency mandates and rising urbanization. According to the Ozone Cell, PCMs in this segment reduce HVAC loads by 15-20%, fostering widespread adoption.

The electronics segment is quickly emerging with a CAGR of 8.7% in this landscape. The proliferation of compact devices necessitates efficient thermal management, as noted by the European Semiconductor Industry Association.

COUNTRY LEVEL ANALYSIS

Germany was at the forefront of the Europe PCM market with a commanding share of 28.4%. This position in the market is backed by the country’s robust industrial base, stringent energy efficiency regulations, and significant investments in renewable energy. The nation’s commitment to achieving carbon neutrality by 2045 has further accelerated adoption. For instance, BASF SE, a leading player headquartered in Germany, reported that over 60% of its domestic sales in 2023 were driven by demand from the building and construction sector. This emphasizes Germany's pivotal role in shaping the regional market.

Spain is the fastest-growing market in Europe, with a projected CAGR of 10.3% during the forecast period. This rapid growth is fueled by the country’s increasing focus on renewable energy integration and solar thermal applications. Spain’s National Integrated Energy and Climate Plan highlights a target of installing 76 GW of solar capacity by 2030, creating substantial opportunities for PCMs in thermal energy storage. In 2022 alone, the Spanish government invested an amount in renewable energy projects. The proliferation of smart grid technologies and urbanization further amplifies demand, positioning Spain as a key growth driver in the region.

France, Italy, and the UK are expected to exhibit steady growth, which is supported by favourable government policies and technological advancements. The French Environment and Energy Management Agency (ADEME) supports and encourages the use of Phase Change Materials (PCMs) in HVAC systems as part of France's broader energy efficiency initiatives. Meanwhile, Italy benefits from its strong manufacturing base and growing demand for cold chain logistics. The UK’s market is driven by post-Brexit sustainability goals, with the Department for Business, Energy & Industrial Strategy emphasizing green technologies. These countries collectively contribute majorly to the European PCM market, ensuring balanced regional development.

KEY MARKET PLAYERS

A few notable companies operating in the Europe phase change materials market profiled in this report are Honeywell International Inc. (US), DuPont de Nemours, Inc. (US), Croda International Plc (UK), Boyd Corporation (US), Sasol Limited (South Africa), Outlast Technologies LLC (US), Climator Sweden AB (Sweden), Rubitherm Technologies GmbH (Germany), PureTemp LLC (US), Phase Change Solutions (US), and others.

TOP LEADING PLAYERS IN THE MARKET

The Europe PCM market is led by three major players—BASF SE, Croda International, and Climator AB—who collectively account for nearly 45% of the global market share. BASF SE, headquartered in Germany, is a pioneer in developing innovative bio-based and hybrid PCMs. The company leverages its extensive R&D capabilities to introduce cutting-edge solutions tailored for the construction and electronics sectors. Croda International, based in the UK, specializes in bio-based PCMs derived from renewable feedstocks. Its strategic focus on sustainability aligns with the EU’s Green Deal objectives, enabling it to capture a significant market share. Climator AB, a Swedish innovator, excels in eutectic PCMs, catering primarily to the cold chain and packaging industries. Together, these companies drive innovation, set industry standards, and shape the competitive landscape.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in the Europe PCM market employ a variety of strategies to consolidate their positions and drive growth. Strategic partnerships are a cornerstone, with companies collaborating to enhance product offerings. Product launches are another critical strategy, as seen when BASF SE introduced a new line of bio-based PCMs in March 2023, targeting eco-conscious consumers. Geographic expansion is also prominent, with Climator AB expanding its production facilities in September 2023 to meet rising demand in Northern Europe. Additionally, heavy R&D investments ensure continuous innovation, while mergers and acquisitions enable companies to broaden their portfolios and enter new markets.

COMPETITION OVERVIEW

The Europe PCM market is characterized by intense competition, driven by the presence of both established players and emerging startups. According to a report by the European Chemical Industry Council, the market is fragmented yet highly dynamic, with companies vying for dominance through differentiation and innovation. BASF SE, Croda International, and Climator AB lead the pack, leveraging their expertise in bio-based and hybrid PCMs to maintain an edge. Smaller firms focus on niche applications like electronics and cold chain logistics to carve out specialized niches. The competitive landscape is further intensified by collaborations between academia and industry, fostering breakthroughs in material science. With sustainability at the forefront, companies increasingly emphasize eco-friendly solutions, driving a race toward greener technologies.

RECENT MARKET DEVELOPMENTS

- In March 2023, BASF SE launched a new line of bio-based phase change materials designed for energy-efficient building applications. This initiative strengthened its position as a leader in sustainable innovations.

- In June 2023, Croda International announced a strategic partnership with Siemens to integrate PCMs into smart HVAC systems. This collaboration enhanced the company’s ability to offer comprehensive thermal management solutions.

- In September 2023, Climator AB expanded its manufacturing facilities in Sweden to meet surging demand for eutectic PCMs in the cold chain and packaging sectors.

- In December 2023, Honeywell acquired a startup specializing in advanced hybrid PCMs, bolstering its portfolio for high-performance electronics applications.

- In February 2024, Dow Chemical introduced a novel hybrid PCM tailored for solar thermal energy storage. This move positioned the company as a key player in renewable energy solutions.

MARKET SEGMENTATION

This Europe phase change materials market research report is segmented and sub-segmented into the following categories.

By Type

- Organic

- Inorganic

- Eutectic

By Application

- Building & Construction

- HVAC

- Cold Chain & Packaging

- Electronics

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

1. What is the current size and projected growth of the Europe phase change materials market?

The market was valued at USD 186.35 million in 2024 and is expected to reach USD 750 million by 2033, growing at a CAGR of 16.74% from 2025 to 2033.

2. What are the main drivers of the phase change materials market in Europe?

Growth is driven by advancements in thermal energy storage, increasing demand for sustainable building solutions, stringent energy efficiency regulations, and rising cold chain logistics needs in the pharmaceutical and food industries.

3. Which countries lead the Europe phase change materials market market?

Germany leads with a 28.4% market share due to strong regulations and investments in renewable energy, while Spain is the fastest-growing market with a CAGR of 10.3%, driven by solar energy integration and smart grid adoption.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com