Europe Plastics Market Size, Share, Trends, & Growth Forecast Report By Type (Polyethylene (PE), Polycarbonate (PC)), End-User Industry and Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic and Rest of Europe), Industry Analysis From 2025 to 2033

Europe Plastics Market Size

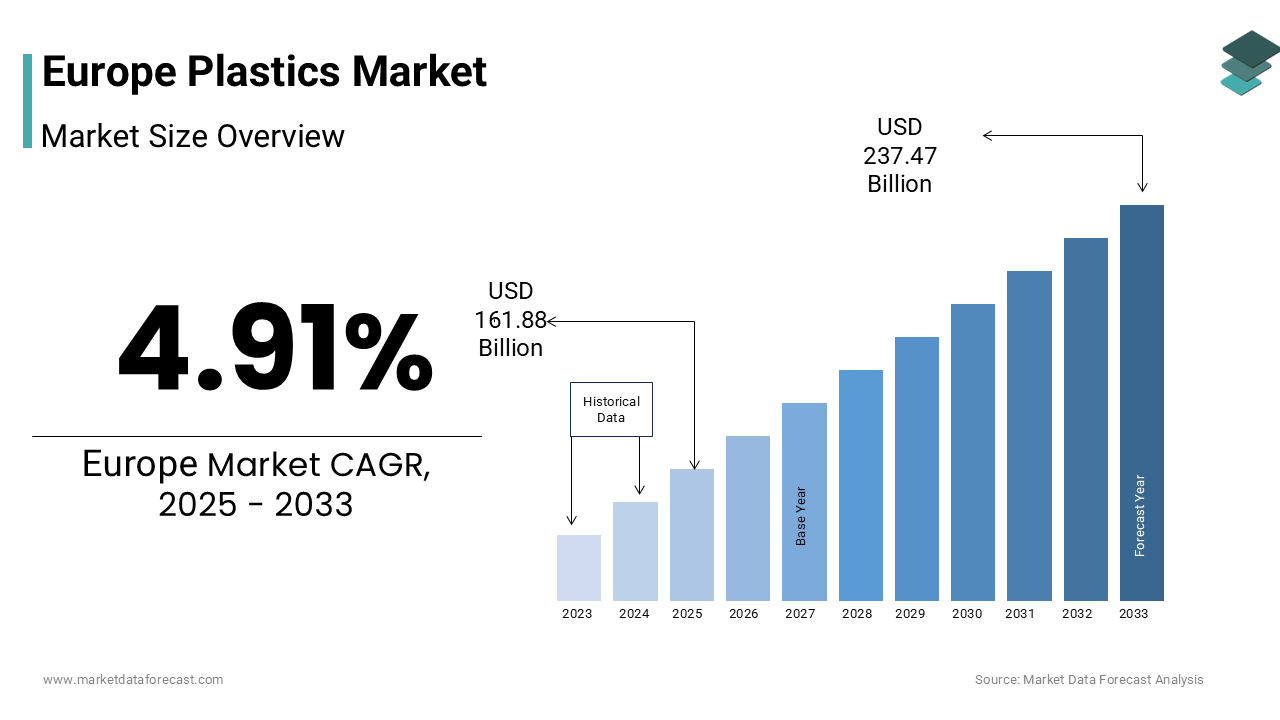

The europe plastics market size was valued at USD 154.31 billion in 2024 and is anticipated to reach USD 161.88 billion in 2025 from USD 237.47 billion by 2033, growing at a CAGR of 4.91% during the forecast period from 2025 to 2033.

Plastics are synthetic and semi synthetic polymers across industrial consumer and infrastructure sectors and serve as a foundational material system for modern economies. Plastics in Europe are primarily derived from fossil feedstocks such as naphtha and natural gas liquids though bio-based alternatives are gaining traction under policy pressure. According to Plastics Europe, Europe produced 58 million metric tons of plastics in 2022 with packaging accounting for the largest end-use segment. According to Eurostat, only 32% of post-consumer plastic waste was recycled in the EU in 2022 while 25% was incinerated with energy recovery and 22% landfilled, which is revealing a significant gap between policy ambition and material circularity. This structural tension between functional indispensability and environmental accountability defines the current trajectory of the European plastics market.

MARKET DRIVERS

Essential Role of Plastics in Medical and Healthcare Applications Sustains Core Demand

The irreplaceable function of plastics in medical devices pharmaceutical packaging and sterile healthcare environments constitutes a resilient driver of demand across Europe, insulated from consumer sustainability pressures. High performance polymers such as polypropylene polycarbonate and polyvinyl chloride are critical for syringes IV bags surgical gloves and diagnostic equipment due to their sterility durability and cost efficiency. According to Eurostat, 21.6% of the EU population was aged 65 or over, which is driving increased healthcare utilisation and associated plastic consumption. The use of plastics in medical‑device components and single‑use hospital consumables remains widespread, which is also reflecting the combination of hygiene, safety and functionality imperatives in healthcare settings. The regulatory environment of Europe recognises that medical‑grade plastics have distinct requirements and therefore addresses them separately from restrictions on other single‑use items to ensure stable and non‑discretionary demand that anchors the industrial base of the European plastics sector.

Lightweighting in Automotive and Transport Fuels Material Substitution Toward Plastics

The imperative to reduce vehicle weight and improve fuel efficiency continues to drive structural substitution of metals with engineering plastics and composites across Europe’s automotive and transport sectors, which is further boosting the expansion of the European plastics market. According to research, a 10% reduction in vehicle weight can lead to about a 6–8% improvement in fuel economy. The average share of plastics by mass in passenger cars remains significant, which is reflecting the broader trend towards lighter and more efficient vehicle designs. The regulatory push under fleet‑wide CO₂ standards in the EU means that material substitution away from all‑metal designs is a key enabler of compliance. Electric vehicles often require additional insulation, battery enclosures and thermal management systems that tend to increase the use of polymeric materials compared with internal‑combustion‑engine‑based counterparts. The intersection of weight‑reduction strategy, emissions regulation and increasing electrification confirms why plastics maintain both functional importance and strategic value in the automotive sector.

MARKET RESTRAINTS

Stringent EU Regulations on Single Use Plastics Curtail Traditional Applications

The EU Directive 2019 904 on single use plastics has imposed binding restrictions that directly suppress demand for conventional plastic items across food service packaging and consumer goods is one of the key restraints to the growth of the European plastics market. According to Directive (EU) 2019/904, the legislation bans ten specific products including cutlery, plates, straws, stirrers and expanded polystyrene food containers. According to European Environment Agency, these items collectively represent around 70 % of marine litter in the EU. Member States were required to achieve a “significant reduction” in the consumption of certain food containers and beverage cups by 2026, and set intermediate targets for 2025 under national measures. The legislation also imposes extended producer responsibility (EPR) schemes forcing manufacturers to cover clean‑up costs and awareness raising. The structural tension between restricting single‑use items and managing producer/sectoral transition remains a key dynamic for the plastics market in Europe.

Persistent Deficiency in High Quality Recycled Feedstock Limits Circular Transition

The critical bottleneck in accessing sufficient volumes of food grade and engineering grade recycled polymers that is undermining its ability to meet mandatory recycled content targets is further impeding the growth of the European market. According to European Food Safety Authority (EFSA), only three recycling processes for polyethylene terephthalate (PET) had been authorised for food contact materials as of early 2024. The Packaging and Packaging Waste Regulation (PPWR) mandates that all plastic beverage bottles contain 30% recycled content by 2030. According to Plastics Europe, current collection and sorting infrastructure yields less than 12% food‑grade rPET annually, which is significantly limiting supply. The challenges of contamination from multilayer packaging and black plastics further degrade output quality. According to the Eurostat, only 14%of post‑consumer plastic waste is processed into high‑value applications, the remainder is down‑cycled or exported. This feedstock scarcity forces converters to rely on virgin polymers or pay steep premiums for certified recyclate, which is eroding competitiveness and delaying the circular‑economy transition despite strong policy intent.

MARKET OPPORTUNITIES

Expansion of Advanced Recycling Infrastructure Unlocks New Material Pathways

The deployment of chemical and molecular recycling technologies presents a potential opportunity for the Europe plastics market by enabling the recovery of high purity monomers from mixed or contaminated plastic waste streams. Unlike mechanical recycling, which degrades polymer quality over cycles, advanced methods such as pyrolysis depolymerization and solvent purification can produce virgin equivalent output suitable for food contact and medical applications. According to the European Commission, the Innovation Fund has committed over €1.8 billion to support large-scale low-carbon technology demonstration projects across the EU. The plastics and recycling sectors are among the beneficiaries of this funding stream. Advanced recycling initiatives are being scaled and major chemical companies are beginning to integrate mass-balance certified circular polymers into their supply chains. Policy development is underway for criteria that would allow chemically-recycled outputs to qualify as “end of waste,” thereby enabling them to count toward regulatory recycled-content targets and unlocking demand from brand-owners committed to circular-economy packaging. This evolving funding, industry integration and regulatory alignment are creating a more favourable environment for circular plastics solutions even as supply-chain, technology and market-uptake challenges remain.

Growth of Bio Based and Biodegradable Polymers in Niche Applications

The development of certified bio based and industrially compostable plastics is creating new market avenues for the European plastics market. Polylactic acid polyhydroxyalkanoates and starch blends are gaining adoption in agricultural films tea bags and organic waste bags where contamination with food or soil renders conventional recycling ineffective. According to European Bioplastics, global bioplastics production capacity was around 2.18 million tonnes in 2023 and is projected to increase significantly toward 2028. The EU’s Fertilising Products Regulation now allows biodegradable mulch films to be tilled into soil after use, which is lowering retrieval costs for farmers. Additionally, revisions to the EN 13432 compostability standard have increased credibility, with certified products carrying the Seedling label under TÜV Austria. While bioplastics still represent a small portion of total plastic use, their alignment with organic-waste collection mandates creates a policy-driven niche that supports innovation and broadens Europe’s polymer portfolio beyond fossil dependence.

MARKET CHALLENGES

Fragmented Waste Collection and Sorting Systems Impede Recycling Efficiency

The absence of harmonized municipal waste management frameworks across EU member states severely is one of the notable challenges to the growth of the European plastics market. According to the European Environment Agency, by 2022 only about 65% of packaging waste in the EU was recycled, which is indicating that significant volumes of collected material still do not meet high‑quality recycling thresholds. Many EU Member States have yet to implement fully consistent systems of separate collection for packaging waste and this is leading to contamination issues and supply‑chain inefficiencies for recycled plastics. Some countries maintain high recycling performance while others lag behind, which is creating logistical imbalances for pan‑European converters. Fragmented practices in bin labelling, public awareness and collection design further compound these challenges and pushing up sorting and recovery costs and undermining efforts to secure the consistent and high‑quality feedstock needed for scaling circular‑plastics production.

Carbon Intensity of Virgin Plastic Production Conflicts With EU Climate Goals

The fossil fuel dependent production process for conventional plastics generates significant greenhouse gas emissions that increasingly conflict with Europe’s decarbonization mandates, which is further challenging the growth of the European market. According to the European Environment Agency (EEA), the plastics value chain in the EU produced about 193 million metric tons of CO₂‑equivalent emissions in 2022. The most emissions originate from production and feedstock extraction, indicating that upstream processes remain highly carbon intensive. The use of steam crackers are among the most energy intensive industrial facilities in the region. The Carbon Border Adjustment Mechanism (CBAM), set to become fully operational in 2026 and will impose tariffs on imported polymers based on embedded emissions, thereby pressuring European producers to decarbonise or risk losing competitiveness. Meanwhile, the EU Emissions Trading System (EU ETS) has seen allowance prices around €80 per tonne of CO₂ in recent years. Without access to green hydrogen, renewable electricity or carbon‑capture solutions, the plastics sector risks being locked out of future low‑carbon supply chains, particularly as automotive and electronics brands increasingly demand Scope 3 emission reductions from their material suppliers.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| Segments Covered | By Type, End-user Industry, and Region. |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, the Netherlands, Turkey, the Czech Republic, and the Rest of Europe |

| Market Leaders Profiled | Borealis GmbH, ALPLA Group, Gerresheimer AG, Amcor PLC, Berry Global Inc., Constantia Flexibles GmbH, Saint-Gobain SA, and LANXESS AG. |

SEGMENTAL ANALYSIS

By Type Insights

The polyethylene segment accounted for the leading share of 32.3% of the European market in 2024. The growth of the polyethylene segment in the European market is primarily driven by its unparalleled versatility, cost efficiency, and dominance in packaging applications. The irreplaceable role of polyethylene in flexible and rigid packaging that accounts for a significant percentage of all polyethylene consumption in the region is also contributing to the domination of the polyethylene segment in this regional market. According to Eurostat, plastic packaging accounted for about 19 % of total packaging waste generation in the EU in 2022. Supermarkets and e‑commerce logistics rely heavily on low‑density and linear low‑density polyethylene films for food preservation and parcel wrapping due to their moisture resistance and sealability. High‑density polyethylene is extensively used in blow‑moulded containers for detergents and personal‑care products, which is benefiting from established recycling streams under extended‑producer‑responsibility schemes. The compatibility with mechanical recycling of polyethylene particularly in bottle form is further entrenches its position as the EU mandates recycled content targets in HDPE bottles under the Packaging and Packaging Waste Regulation.

The polycarbonate segment is another major segment and is anticipated to register the fastest CAGR of 6.8% over the forecast period. Factors such as the critical performance of polycarbonate attributes in high value applications where safety, transparency, and thermal stability are non-negotiable and the electrification of transport are primarily driving the growth of the polycarbonate segment in the European market. Electric vehicle battery enclosures require flame retardant and impact resistant materials that can withstand thermal runaway events and polycarbonate composites meet these specifications better than most alternatives. According to European Automobile Manufacturers Association (ACEA), electric cars in the EU grew significantly in 2023, which is reflecting a rapid shift toward battery‑electric vehicle production. The construction sector is adopting polycarbonate glazing for energy efficient skylights and noise barriers due to its far higher impact strength compared with glass and its superior thermal insulation. Polycarbonate materials are increasingly used in new non‑residential buildings across some European markets, which is supporting rising demand tied to sustainability and performance criteria. These dual demand vectors position polycarbonate as a strategic material in Europe’s industrial transition and drive the growth of the polycarbonate segment in the European plastics market.

By End-use Industry Insights

The packaging segment dominated the market by accounting for 41.2% of the regional market share in 2024. The leading position of packaging segment in the European market can be credited to the functional necessity of plastics in preserving food to reduce waste and enable modern supply chains. The food safety and shelf-life extension are also boosting the domination of the packaging segment in the European market. According to the European Food Safety Authority (EFSA), packaging plays an essential role in preventing damage or spoilage of food. The supermarkets and e‑commerce logistics sectors rely heavily on low‑density and linear low‑density polyethylene films for food‑preservation and parcel‑wrapping due to their moisture‑resistance and sealability. Modified‑atmosphere packaging using multi‑layer polyethylene and polypropylene films can greatly extend the shelf‑life of fresh meat and other perishable goods, which is significantly curbing household and retail waste. The rise of e‑commerce has intensified demand for protective void‑fillers and moisture‑barrier wraps, and while online retail sales in the EU grew noticeably in recent years, each parcel continues to carry plastic‑based packaging. Despite regulatory pressure, the indispensability of packaging sector in public health and logistics ensures continued volume, especially as recyclable mono‑material designs begin replacing complex laminates under the EU’s design‑for‑recycling guidelines.

The healthcare and pharmaceutical segment is expected to experience a promising CAGR of 7.4% over the forecast period in the European plastics market owing to the demographic shifts and the non-substitutable role of high purity polymers in medical applications. The aging population in Europe is a key catalyst to the growth of the healthcare and pharmaceutical segment in the European market. According to Eurostat, 21.3% of the EU’s population was aged 65 or older as of 1 January 2023. The post‑pandemic reinforcement of healthcare resilience has prompted significant investment through the EU4Health programme with an initial budget of approximately €5.3 billion. Regulatory frameworks explicitly recognise that medical‑grade plastics in single‑use devices remain outside general single‑use bans under Directive 2019/904 due to hygiene imperatives. Innovations in bio‑resorbable polymers for implants and drug‑delivery systems, such as polylactic acid stents are also gaining clinical adoption, which is further boosting the expansion of the healthcare and pharmaceutical segment in the European plastics market.

REGIONAL ANALYSIS

Germany Plastics Market Analysis

Germany accounted for the major share of 24.2% of the European plastics market in 2024. The recognition of Germany as an industrial powerhouse and Germany being a hub for automotive chemical and packaging manufacturing are primarily contributing to the domination of Germany in the European plastics market. Germany hosts Europe’s most integrated polymer value chain and anchored by BASF Covestro and LyondellBasell production complexes along the Rhine River. According to the German Association of the Plastics Converters (GKV), the German plastics-converting industry comprises more than 310,000 employees across nearly 3,000 enterprises. The leading position of Germany in the European market is also attributed to its dual focus on circularity and performance. Germany achieves a high packaging-waste recycling rate while simultaneously driving demand for engineering plastics in electric-vehicle production. The High-Tech Strategy 2025 of German government has committed significant funding to sustainable-materials innovation, including chemical-recycling and bio-based polymers. This balance between regulatory-rigor and industrial capability is significantly boosting the domination of Germany in the European market.

France Plastics Market Analysis

France is also a promising market for plastics in Europe and is expected to account for a substantial share of the European market over the forecast period owing to its strong policy driven approach to plastic management and advanced medical and aerospace sectors. According to the French Ministry for Ecological Transition, France consumes approximately 4.8 million tonnes of plastics annually. According to the French Federation of Plastics and Rubber Industries, local output directed toward sterile medical packaging and aircraft-interior components is significant. The Anti‑Waste Law for a Circular Economy (2020) has accelerated investment in recyclate infrastructure. France now operates multiple certified food-grade rPET plants according to ADEME, which is positioning it among the most advanced in Europe. Moreover, via Citeo France manages an extended-producer-responsibility fund of around €1.2 billion annually for collection and sorting of packaging waste. The aerospace cluster around Toulouse (home to Airbus) demands high-performance thermoplastics like polyetheretherketone, which is creating a premium application base that offsets declines in single-use packaging. This strategic diversification confirms the robust position of France in the European plastics market.

Italy Plastics Market Analysis

Italy is estimated to account for a notable share of the European plastics market over the forecast period due to its dense network of small and medium enterprises specializing in packaging films and consumer goods. According to data from Italy’s packaging waste statistics, plastic packaging waste was recycled at about 48.9% of the material placed on the market in 2022. The Italian plastics-converting sector handles millions of tonnes of materials each year with a substantial share used for packaging applications, particularly flexible films for food and agriculture. The strong position of Italy in fresh-produce agriculture drives demand for items like mulch films and greenhouse covers made from low-density polyethylene. However, Italy faces circular-economy challenges in plastics waste management. In response, its national recovery plan allocates significant funding to modernise sorting and promote design-for-recycling solutions. The agility of Italy’s converter base, able to rapidly adapt to brand-owner demands for mono-material solutions ensures continued relevance even as systemic circularity gaps persist.

United Kingdom Plastics Market Analysis

The United Kingdom is expected to showcase a healthy CAGR in the European plastics market over the forecast period owing to its financial services, pharmaceuticals, and advanced manufacturing sectors despite post Brexit regulatory divergence. According to the British Plastics Federation (BPF), the UK plastics industry processes around 3.4 million metric tons of plastic annually. The Plastic Packaging Tax (PPT) of the UK that came into effect in April 2022 is charged at £200 per tonne (rising to £210.82 per tonne from April 2023) for plastic packaging containing less than 30 % recycled content. The tax has driven increased focus on recyclate use in the packaging supply chain. London’s status as a green-finance hub has also helped channel capital into circular-economy startups focused on advanced recycling and sustainable materials.

Netherlands Plastics Market Analysis

The Netherlands is estimated to grow at a prominent CAGR in the European plastics market over the forecast period. Netherlands is functioning as Europe’s logistics and chemical gateway through the Port of Rotterdam. According to a Dutch government estimate, the Netherlands accounts for almost 11% of the EU’s total plastics production, which is positioning it among Europe’s largest plastics manufacturing hubs. The plastics market growth is Netherlands is also driven by integrated chemical and polymer clusters located in major industrial zones, which is offering logistic advantages and co-location of converters and producers. The Netherlands has achieved a plastic-packaging recycling rate of around 45.7 % in 2022, which is reflecting solid infrastructure for separation and recovery. Circular-economy policy and networks such as the national plastics pact support innovation and reuse efforts. At the same time, Amsterdam’s role as a sustainability-standards hub helps shape procurement policies across Europe and reinforces the strategic importance of Netherlands as a plastics-ecosystem enabler.

COMPETITIVE LANDSCAPE

Competition in the Europe plastics market is characterized by a strategic pivot from volume based growth to sustainability driven differentiation. Traditional petrochemical giants are contending with agile circular economy startups and global material suppliers vying for influence in high value segments like medical and electric vehicle applications. The competitive landscape is increasingly defined by access to certified recycled feedstock technological capability in advanced recycling and alignment with EU regulatory milestones such as the Packaging and Packaging Waste Regulation. Companies that can offer traceable mass balance polymers design for recycling expertise and compliance with carbon intensity thresholds gain preferential access to brand owner contracts. Simultaneously price pressure persists in commodity segments due to overcapacity and energy cost volatility. This duality fosters both collaboration through industry coalitions like the Plastics Pact and intense rivalry in innovation where speed to market with credible circular solutions determines leadership.

KEY MARKET PLAYERS

A few of the major companies in the europe plastics market include

- Borealis GmbH

- ALPLA Group

- Gerresheimer AG

- Amcor PL

- Berry Global Inc.

- Constantia Flexibles GmbH

- Saint-Gobain SA

- LANXESS AG.

Top Players in the Market

BASF SE

BASF SE is a cornerstone of the Europe plastics market through its extensive portfolio of engineering plastics and polyolefins used across automotive electronics and packaging sectors. The company supplies high performance materials such as Ultramid polyamide and Ultrason polycarbonate to global manufacturers with European operations. BASF has intensified its circularity initiatives by scaling its ChemCycling program, which converts plastic waste into pyrolysis oil for virgin quality polymer production. In 2023, it expanded mass balance certified product availability to over 50 grades and partnered with major automotive OEMs to validate circular polymers in safety critical components. These actions reinforce BASF’s role as a technology enabler in Europe’s transition toward a circular plastics economy while maintaining its global leadership in specialty materials innovation.

LyondellBasell Industries NV

LyondellBasell is a pivotal player in the Europe plastics market through its integrated production of polyethylene and polypropylene at major sites in Germany Italy and the Netherlands. The company operates one of the continent’s largest polymer manufacturing networks and supplies both commodity and advanced circular polymers under its Circulen brand. Recently, LyondellBasell commissioned Europe’s first commercial scale molecular recycling unit in Ferrara Italy, capable of processing 30,000 metric tons of mixed plastic waste annually into feedstock. It has also secured long term offtake agreements with consumer goods leaders for CirculenRecover and CirculenRevive resins. These strategic moves position LyondellBasell at the forefront of scaling advanced recycling infrastructure and meeting EU mandated recycled content requirements across multiple value chains.

SABIC

SABIC contributes significantly to the Europe plastics market through its production of engineering thermoplastics and certified circular polymers tailored for automotive healthcare and electronics applications. The company operates major compounding and polymer facilities in the Netherlands and Spain and supplies TRUCIRCLE portfolio materials that incorporate mechanically and chemically recycled content. In 2023, SABIC achieved full certification under the ISCC PLUS mass balance system for its European sites and launched new grades of certified renewable polycarbonate derived from bio based feedstocks. It also collaborated with European packaging converters to develop mono material flexible packaging solutions compliant with recyclability guidelines. These initiatives underscore SABIC’s commitment to enabling circularity while supporting brand owners in meeting evolving EU sustainability regulations.

Top Strategies Used by the Key Market Participants

Key players in the Europe plastics market are prioritizing circularity through vertical integration of advanced recycling technologies to secure high quality feedstock. They are expanding mass balance certified product portfolios to meet regulatory recycled content mandates while maintaining performance standards. Strategic partnerships with brand owners converters and waste management firms are being forged to close material loops and validate circular claims. Investment in bio based polymer research is accelerating to diversify feedstock sources beyond fossil fuels. Companies are also actively engaging in policy dialogues to shape harmonized definitions for recyclability and end of waste criteria ensuring regulatory alignment across member states and reducing market fragmentation.

RECENT MARKET DEVELOPMENTS

- In March 2024, BASF SE inaugurated a new compounding line in Ludwigshafen Germany dedicated to producing mass balance certified Ultramid grades for automotive customers strengthening the Europe plastics market presence.

- In January 2024, LyondellBasell Industries NV signed a ten year offtake agreement with a leading European beverage company for CirculenRevive rPET resin enhancing the Europe plastics market presence.

- In November 2023, SABIC launched a new portfolio of certified circular polycarbonate grades at its facility in Geleen Netherlands reinforcing the Europe plastics market presence.

- In May 2024, BASF SE partnered with a German waste management consortium to scale pyrolysis oil supply for its ChemCycling program bolstering the Europe plastics market presence.

- In February 2024, LyondellBasell Industries NV received ISCC PLUS certification for its polypropylene production unit in Ferrara Italy advancing the Europe plastics market presence.

MARKET SEGMENTATION

This research report on the Europe plastics market has been segmented based on the following categories.

By Type

- Polyethylene (PE)

- Polycarbonate (PC)

By End-Use Industry

- Packaging

- Healthcare and Pharmaceutical

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

What is the Europe Plastics Market?

The Europe Plastics Market covers the production, consumption, and trade of plastic materials and products across various sectors such as packaging, automotive, construction, and healthcare.

What factors are driving the growth of the Europe Plastics Market?

The market growth is driven by increasing demand from packaging and healthcare industries, the rise of lightweight materials in automotive applications, and recycling advancements supported by EU sustainability regulations.

Which countries lead the Europe Plastics Market?

Germany, France, Italy, the United Kingdom, and the Netherlands are the leading countries due to strong manufacturing bases and advanced recycling infrastructure.

What challenges does the Europe Plastics Market face?

Key challenges include strict environmental regulations, plastic waste management, and the transition toward bio-based and recyclable alternatives.

What is the growth outlook for the Europe Plastics Market?

The market is expected to witness steady growth over the next few years due to innovation in recyclable materials, government support for circular economy initiatives, and rising demand from sustainable packaging applications.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com