Europe Portable Air Compressor Market Size, Share, Growth, Trends, And Forecasts Report, Segmented By End-User And By Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic & Rest of Europe), Industry Analysis From 2025 to 2033

Europe Portable Air Compressor Market Size

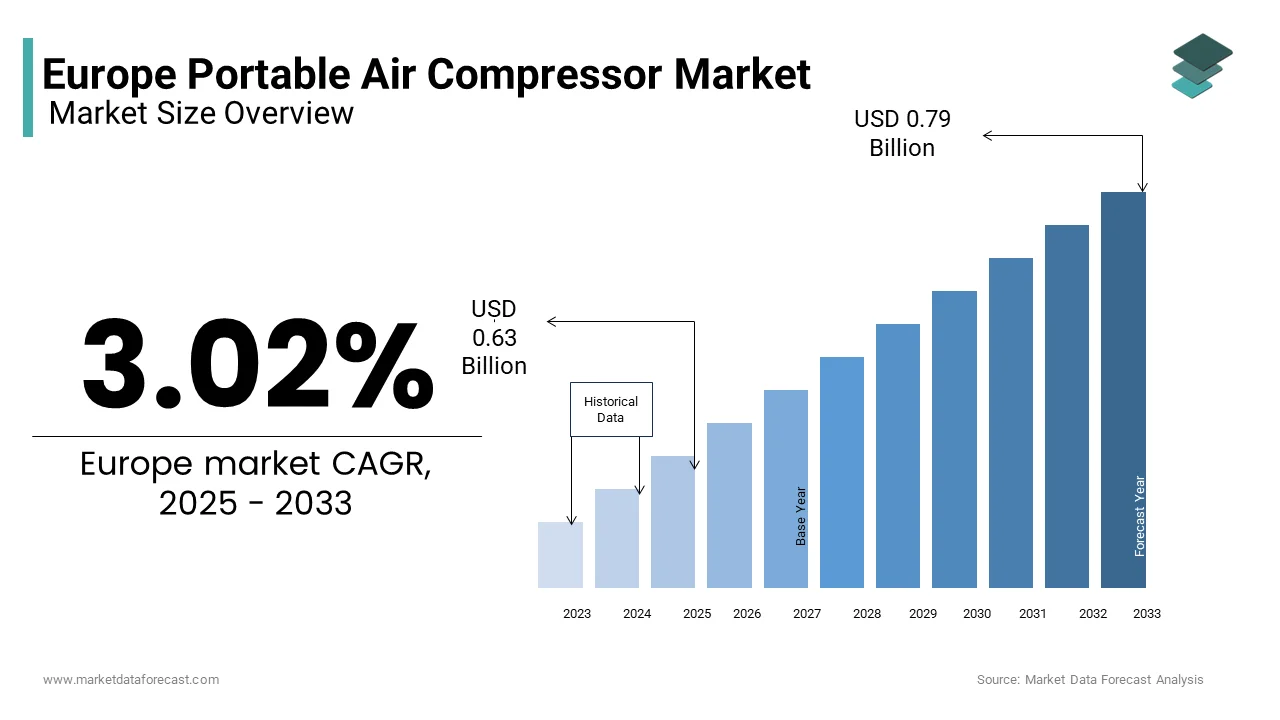

The Europe portable air compressor market was valued at USD 0.61 billion in 2024 and is anticipated to reach USD 0.63 billion in 2025 from USD 0.79 billion by 2033, growing at a CAGR of 3.02% during the forecast period from 2025 to 2033.

The Europe portable air compressor market covers a range of compact, mobile air compression systems designed for diverse industrial, commercial, and residential applications. These devices are essential in construction, automotive repair, manufacturing, and energy services, where a flexible and on-site compressed air supply is critical. Portable air compressors are favored for their mobility, ease of deployment, and adaptability across varying terrains and job conditions. Europe maintains a strong industrial base that significantly contributes to the demand for portable air compressors. Countries such as Germany, France, the UK, and Italy continue to invest in infrastructure modernization and industrial automation, driving a consistent need for reliable pneumatic tools and equipment. In addition to traditional sectors, emerging applications in renewable energy maintenance, particularly wind turbine servicing, are creating new avenues for portable air compressor deployment. As per the European Environment Agency, over 20,000 onshore wind turbines were operational across Europe in 2023, many situated in remote or hard-to-reach locations where portable compressed air systems are indispensable. Manufacturers are responding to these evolving demands by focusing on energy efficiency, noise reduction, and integration with digital diagnostics.

MARKET DRIVERS

Growth in Construction and Infrastructure Development

One of the primary drivers of the Europe portable air compressor market is the sustained growth in construction and infrastructure development. The construction industry remains a cornerstone of economic activity across the continent, with governments investing heavily in urbanization, transportation networks, and housing projects. According to the European Construction Industry Federation, the sector witnessed a 6.8% increase in new project commencements in 2023, particularly in Eastern and Southern Europe. Portable air compressors are integral to construction activities such as concrete spraying, jackhammering, nail gun operation, and surface preparation. Their mobility and ease of use make them preferable over stationary compressors on dynamic job sites. This level of spending has directly boosted the demand for high-performance portable air compressors capable of operating under challenging site conditions. Moreover, small and medium-sized enterprises (SMEs) dominate the European construction sector, and they rely heavily on rental equipment rather than capital purchases. As per the European Rental Association, equipment rental usage among construction firms grew significantly in recent years, with pneumatic tools and compressors being among the most frequently rented items.

Expansion of the Automotive and Manufacturing Sectors

Another significant driver for the Europe portable air compressor market is the continued expansion of the automotive and manufacturing industries, both of which extensively utilize compressed air-driven tools and systems. According to the European Automobile Manufacturers’ Association, vehicle production in the EU increased in 2023 after a prolonged period of decline, signaling renewed confidence and investment in the sector. Portable air compressors play a crucial role in assembly lines, tire inflation stations, robotic arms, and paint booths, making them indispensable in automotive production and service environments. Manufacturing, too, is experiencing a revival, especially in countries like Poland, Spain, and the Czech Republic, where industrial output has seen robust growth. Within this context, portable compressors are increasingly used for maintenance tasks, material handling, and precision tooling operations across plants. Additionally, there is growing adoption of lightweight and fuel-efficient compressors equipped with advanced motor controls and energy-saving features. Manufacturers such as Atlas Copco and Kaeser Kompressoren have introduced models tailored for industrial portability, aligning with the sector’s shift toward lean manufacturing and operational efficiency.

MARKET RESTRAINT

Stringent Emission and Noise Regulations

A key restraint affecting the Europe portable air compressor market is the imposition of stringent emission and noise regulations, particularly concerning diesel-powered models. The European Union has implemented strict directives such as the Stage V emissions standards, which mandate significant reductions in particulate matter and nitrogen oxide emissions from non-road mobile machinery. As outlined by the European Environment Agency, these standards have forced manufacturers to either redesign existing products or phase out older, less compliant models, leading to higher production costs and longer development cycles. Furthermore, noise pollution is a growing concern in urban and industrial settings, prompting municipalities and regulatory bodies to impose decibel limits on equipment used in built-up areas. While these changes enhance environmental and occupational safety, they also increase product pricing and complexity, deterring price-sensitive buyers. This regulatory environment disproportionately impacts smaller manufacturers who lack the financial resources to invest in extensive R&D. Consequently, some players are exiting the market or limiting their offerings to electric alternatives, which, while compliant, may not meet all performance requirements.

High Maintenance Costs and Technical Complexity

Another major limitation facing the Europe portable air compressor market is the relatively high cost of maintenance and the technical expertise required for regular servicing. Unlike consumer-grade tools, industrial portable compressors require frequent inspections, oil changes, filter replacements, and calibration to ensure optimal performance and longevity. Moreover, the increasing integration of digital monitoring systems and variable speed drives has added a layer of complexity to compressor operation and troubleshooting. Technicians must be trained in electronics and software diagnostics, which many regional repair shops do not yet support. The European Equipment Rental Association highlights that the availability of skilled technicians lags behind demand, leading to longer downtime and higher service charges for operators across Central and Eastern Europe. These factors collectively contribute to reduced product appeal among budget-conscious customers, particularly those in the DIY and home improvement sectors. Some end-users opt for lower-cost, less durable alternatives that may not offer the same efficiency or reliability.

MARKET OPPORTUNITY

Adoption of Battery-Powered and Hybrid Technologies

A transformative opportunity emerging in the Europe portable air compressor market is the increasing adoption of battery-powered and hybrid models, driven by the region’s commitment to reducing carbon emissions and enhancing workplace safety. As part of the European Green Deal, national governments and industry regulators have intensified efforts to phase out fossil-fuel-based equipment in favor of cleaner alternatives. Battery-powered portable air compressors eliminate exhaust emissions, reduce noise levels, and offer greater flexibility in indoor and confined spaces where ventilation is limited. Companies like Atlas Copco and Hitachi have launched high-capacity lithium-ion models that provide extended runtime and rapid recharging capabilities, making them suitable for a wide range of industrial applications. Additionally, innovations in thermal management and energy density are improving the reliability and efficiency of these units. Beyond environmental benefits, government incentives and subsidies are accelerating market uptake. For instance, the French Ministry of Ecological Transition offers tax credits for companies investing in zero-emission tools, encouraging fleet modernization. Similarly, the UK’s Clean Air Strategy promotes the use of electric equipment in urban zones designated as Ultra Low Emission Zones.

Rise of Remote and Off-Grid Industrial Operations

The growing prevalence of remote and off-grid industrial operations across Europe is creating new demand opportunities for portable air compressors, particularly in sectors such as mining, oil and gas, and renewable energy maintenance. Many of these operations are located in geographically isolated regions where access to centralized power grids is limited or nonexistent, necessitating self-sufficient equipment solutions. Portable air compressors, especially those powered by hybrid engines or advanced batteries, are well-suited for these conditions due to their ability to function independently of permanent power infrastructure. Wind farm maintenance, for example, requires on-the-move pneumatic tools for blade repair and tower bolt tightening, often performed at elevated heights without convenient electrical access. Beyond energy, the agricultural and forestry industries are also leveraging portable compressors for tasks such as fence installation, irrigation system maintenance, and wood processing. With increasing mechanization and automation in these traditionally labor-intensive fields, the need for reliable and mobile air supply units is expected to grow.

MARKET CHALLENGE

Volatility in Raw Material Prices

One of the foremost challenges confronting the Europe portable air compressor market is the volatility in raw material prices, particularly for steel, copper, and rare earth metals essential for compressor manufacturing. These materials form the core components of motors, casings, and electronic controls, and their fluctuating costs directly impact production expenses and final product pricing. According to the European Steel Association, steel prices in the EU surged in 2023 compared to the previous year due to energy cost spikes and supply chain disruptions. Copper, another critical input used in motor windings and wiring, has also experienced extreme price swings. Data from the London Metal Exchange indicates that copper prices reached a ten-year high in mid-2023 before stabilizing later in the year. Such unpredictability makes it difficult for manufacturers to forecast production costs accurately, leading to potential delays in product launches and inventory adjustments. This instability affects not only large OEMs but also regional suppliers and distributors dependent on stable pricing structures for competitive positioning. As a result, some companies have begun sourcing alternative materials or renegotiating supplier contracts to mitigate financial exposure.

Supply Chain Disruptions and Component Shortages

Another pressing issue affecting the Europe portable air compressor market is ongoing supply chain disruptions and shortages of critical electronic and mechanical components. The post-pandemic recovery, combined with geopolitical tensions and logistical bottlenecks, has led to extended lead times and inconsistent availability of parts such as microcontrollers, pressure sensors, and inverters. These disruptions hinder the timely production and distribution of portable air compressors, especially models incorporating smart features like digital displays, automatic pressure regulation, and IoT-enabled diagnostics. Semiconductor scarcity, in particular, has had a pronounced effect on manufacturers reliant on programmable logic controllers (PLCs) for compressor automation. Smaller manufacturers lacking diversified supplier networks are especially vulnerable, often facing production halts or order cancellations. Larger firms, though better positioned, still experience margin compression due to expedited shipping fees and dual-sourcing strategies aimed at mitigating risks.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| CAGR | 3.02% |

| Segments Covered | By End-User and Country |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, the Czech Republic, and the Rest of Europe |

| Market Leaders Profiled | Atlas Copco AB, BAC Compressors, BAUER COMPRESSORS INC, Doosan Portable Power Co., Draper Tools Ltd., Elgi Equipments Ltd, Hitachi Ltd., Hubei Teweite Power Technology Co. Ltd., Ingersoll Rand Inc., KAESER KOMPRESSOREN SE, Kaishan Compressor USA, MAT Holdings Inc., Metabowerke GmbH, Mi T M Corp, Remeza JSC, Rolair Systems, Satnam Pumps and Electricals, Stanley Black and Decker Inc., Sumake Industrial Co. Ltd., Universal Air and Gas Products Corp. |

SEGMENTAL ANALYSIS

By End-User Insights

The manufacturing sector dominated the Europe portable air compressor market by holding a8.5% of the total demand in 2024. This segment encompasses industries such as automotive, electronics, food and beverage, pharmaceuticals, and general machinery, all of which rely heavily on compressed air for automation, assembly, packaging, and material handling applications. According to the European Commission’s Directorate-General for Internal Market, Industry, Entrepreneurship and SMEs (GROW), the industrial automation sector in Europe expanded by 6.1% in 2023, directly fueling demand for reliable and mobile compressed air solutions. One of the primary drivers behind this dominance is the increasing adoption of pneumatic systems in production lines. Besides, the growth of just-in-time manufacturing models has heightened the need for mobile maintenance units capable of rapid deployment across plant floors. Another contributing factor is the rising number of small and medium-sized enterprises (SMEs) investing in modular production setups that favor portable over fixed compressor systems.

The energy sector is emerging as the fastest-growing application area for portable air compressors in Europe, projected to expand at a CAGR of 7.9% through 2033. This development is mainly driven by the expansion of renewable energy infrastructure and the ongoing maintenance requirements of conventional power generation facilities. According to WindEurope, installed wind capacity in the EU reached nearly 200 GW by the end of 2023, with over 20,000 turbines operational across the continent. Portable air compressors play a critical role in wind turbine maintenance, particularly in blade repair, bolt tightening, and insulation testing—activities often conducted in remote or offshore locations where stationary systems are impractical. In response, major operators like Ørsted and Iberdrola have integrated mobile compressed air units into their service fleets, enhancing field efficiency and reducing downtime. Also, natural gas and oil exploration projects in regions such as the North Sea and Eastern Europe continue to utilize portable compressors for pipeline cleaning, valve actuation, and emergency operations.

COUNTRY-LEVEL ANALYSIS

Germany Portable Air Compressor Market Analysis

Germany was the best performer in the Europe portable air compressor market by accounting for 22.8%, owing to its status as the continent’s industrial powerhouse. The country’s dense network of manufacturing hubs, especially in Baden-Württemberg, Bavaria, and North Rhine-Westphalia, drives consistent demand for pneumatic tools and mobile air compression solutions. A key factor supporting market growth is the strong presence of domestic manufacturers such as Atlas Copco, Kaeser Kompressoren, and Bauer Kompressoren, which serve both local and international markets. These companies invest heavily in R&D, focusing on energy-efficient and digitally integrated portable compressors. Also, Germany’s leadership in renewable energy infrastructure, including wind and solar farms, has increased reliance on mobile air compression units for maintenance and installation activities.

France Portable Air Compressor Market Analysis

France witnessed a strong industrial base and diversified demand, which is supported by a well-established industrial ecosystem and expanding infrastructure projects. The country’s diverse economy, spanning automotive, aerospace, chemical processing, and construction sectors, ensures steady demand for portable air compressors tailored to various operational needs. According to France’s National Institute of Statistics and Economic Studies (INSEE), industrial production in the manufacturing sector grew by 4.1% in 2023, reflecting increased utilization of automated and pneumatic systems. The French government’s focus on modernizing transport networks and public utilities has also contributed to market expansion. Besides, France’s growing renewable energy sector, particularly in offshore wind, has spurred demand for portable compressors used in turbine maintenance and substation construction.

United Kingdom Portable Air Compressor Market Analysis

The United Kingdom saw steady growth amid industrial transition and is maintaining a stable position despite economic uncertainties and post-Brexit trade adjustments. The UK’s industrial sector, particularly in engineering, pharmaceuticals, and construction, continues to be a significant driver of demand for portable air compression solutions. According to the Office for National Statistics, the construction industry saw a notable increase in output during 2023, driven by both residential and commercial development projects. One of the key growth areas is the energy transition sector, where portable compressors are increasingly deployed for maintenance and repair tasks in wind farms and hydrogen production facilities. The Department for Business, Energy & Industrial Strategy reports that the UK added over 2 GW of new wind capacity in 2023, necessitating regular turbine servicing using mobile pneumatic equipment. Additionally, the rise in offshore oil and gas exploration in the North Sea has sustained demand for ruggedized and explosion-proof compressors suited for harsh environments. The UK’s rental equipment market also plays a crucial role in shaping demand dynamics. These trends contribute to the UK’s resilient yet evolving position in the European portable air compressor market.

Italy Portable Air Compressor Market Analysis

Italy holds a notable share of the Europe portable air compressor market, benefiting from a resurgence in industrial activity and renewed emphasis on infrastructure development. The country’s manufacturing base, particularly in Lombardy, Emilia-Romagna, and Piedmont, remains a key consumer of compressed air technologies. Infrastructure modernization is another major catalyst. The Italian government has allocated over €12 billion under the National Recovery and Resilience Plan (PNRR) for transportation, energy, and water management projects. These initiatives involve extensive use of portable compressors for road construction, tunnel boring, and pipeline maintenance. Additionally, Italy’s push toward renewable energy has increased demand for portable compressors in photovoltaic plant installation and wind turbine servicing. Ansaldo Energia and other domestic firms have reported higher procurement of mobile air compression units for these applications.

Netherlands Portable Air Compressor Market Analysis

The Netherlands commands a comparatively smaller share of the Europe portable air compressor market, leveraging its role as a logistics and industrial hub with a strong focus on sustainability. The country’s advanced manufacturing and port infrastructure, particularly in Rotterdam and Amsterdam, drive consistent demand for mobile compressed air solutions across sectors such as chemicals, food processing, and precision engineering. A distinguishing feature of the Dutch market is its early adoption of clean and electric-powered portable compressors, in line with national decarbonization goals. Apart from these, the Netherlands’s prowess in hydrogen and offshore wind development has created new demand channels. Companies like Shell and Siemens Gamesa have incorporated portable compressors into their maintenance workflows for hydrogen refueling stations and offshore wind farms. Moreover, the Dutch rental market is highly developed, with firms like Boels Rental and Europower offering extensive fleets of mobile air compression units.

COMPETITIVE LANDSCAPE

The competition in the Europe portable air compressor market is marked by a mix of established multinational corporations and agile regional manufacturers vying for market share through continuous innovation and strategic positioning. With a strong industrial base and increasing emphasis on energy efficiency, the region presents both opportunities and challenges for market participants. Leading companies compete not only on product performance but also on sustainability credentials, service support, and adaptability to evolving end-user needs.

Market players differentiate themselves by introducing technologically advanced, lightweight, and low-emission models tailored for specific applications such as construction, manufacturing, and renewable energy maintenance. The growing demand for electric and hybrid compressors has intensified R&D activities, prompting companies to invest heavily in next-generation solutions. At the same time, smaller manufacturers are leveraging cost-effective production models and niche market expertise to capture segments overlooked by larger firms.

Distribution networks and after-sales service play a crucial role in maintaining brand loyalty and ensuring customer retention. Companies are expanding their presence through partnerships, acquisitions, and localized support centers.

KEY MARKET PLAYERS

These are the market players that are dominating the Europe portable air compressor market,inincluding

- Atlas Copco AB

- BAC Compressors

- BAUER COMPRESSORS INC

- Doosan Portable Power Co.

- Draper Tools Ltd.

- Elgi Equipment Ltd

- Hitachi Ltd.

- Hubei Teweite Power Technology Co. Ltd.

- Ingersoll Rand Inc.

- KAESER KOMPRESSOREN SE

- Kaishan Compressor USA

- MAT Holdings Inc.

- Metabowerke GmbH

- Mi T M Corp

- Remeza JSC

- Rolair systems

- Satnam Pumps and Electricals

- Stanley Black

- Decker Inc.

- Sumake Industrial Co. Ltd.

- Universal Air

- Gas Products Corp

Top Players In The Market

- Atlas Copco is a global leader in compressed air technology and plays a pivotal role in shaping the European portable air compressor market. The company is known for its innovation, reliability, and comprehensive range of industrial-grade portable compressors tailored for construction, mining, and energy applications. Atlas Copco's commitment to sustainability and digital integration has positioned it at the forefront of industry transformation. Its emphasis on energy-efficient solutions and customer-centric service models has influenced global standards and driven adoption across diverse sectors.

- Kaeser Kompressoren is a major German manufacturer renowned for its engineering excellence and robust product portfolio in fixed and portable air compression systems. The company has significantly contributed to the advancement of mobile compressor technologies by focusing on performance, durability, and environmental responsibility. Kaeser’s strategic investments in R&D have led to the development of compact, high-efficiency units that cater to evolving industrial demands. Its strong distribution network and localized support services have reinforced its leadership in Europe and expanded its influence in international markets.

- Ingersoll Rand has long been a dominant force in the portable air compressor sector, offering a wide array of products designed for heavy-duty industrial and commercial applications. Following its separation and restructuring into specialized entities, the legacy of Ingersoll Rand continues through advanced product lines that emphasize fuel efficiency, portability, and smart diagnostics. The company’s technological foresight and global reach have made it a trusted name in both traditional and emerging markets, contributing to broader industry advancements in compressed air utilization.

Top Strategies Used By Key Market Participants

One of the primary strategies employed by leading players in the Europe portable air compressor market is the introduction of energy-efficient and electric-powered models. As regulatory pressure intensifies and industries shift toward greener operations, manufacturers are prioritizing the development of low-emission, battery-operated compressors that align with sustainability goals while meeting performance requirements.

Another key approach is expanding service networks and after-sales support. Given the technical complexity of modern portable compressors, companies are investing in training programs, spare parts availability, and rapid-response maintenance services to enhance customer satisfaction and ensure long-term equipment reliability, particularly among industrial users.

Lastly, firms are increasingly adopting digital integration and smart monitoring features in their products. By incorporating IoT-enabled sensors and remote diagnostics, manufacturers are improving operational efficiency, predictive maintenance capabilities, and user experience, thereby strengthening their competitive edge in a rapidly evolving market landscape.

RECENT MARKET NEWS

- In February 2024, Atlas Copco launched its new line of battery-powered portable air compressors specifically designed for indoor and emission-sensitive applications, reinforcing its commitment to sustainable industrial solutions and expanding its footprint in environmentally regulated sectors.

- In August 2023, Kaeser Kompressoren announced a strategic partnership with a leading European rental equipment provider to integrate its latest portable compressors into rental fleets, enhancing accessibility for SMEs and project-based contractors across multiple industries.

- In May 2024, Ingersoll Rand, through its successor entity Gardner Denver, introduced an AI-driven diagnostic system for its portable compressors, enabling real-time performance monitoring and predictive maintenance, thus improving uptime and operational efficiency.

- In October 2023, Doosan Portable Power opened a new regional service center in Poland to support growing demand in Central and Eastern Europe, ensuring faster response times and improved after-sales support for industrial clients.

- In December 2024, Husky Air Products acquired a French distributor specializing in pneumatic tools and compressors, aiming to strengthen its distribution network and increase visibility in the Southern European market.

MARKET SEGMENTATION

This research report on the Europe portable air compressor market is segmented and sub-segmented into the following categories.

By End-user

- Manufacturing

- Construction and mining

- Energy

- Healthcare

- Others

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

What’s driving the demand for portable air compressors across Europe right now?

Demand is primarily fueled by the growth in DIY home improvement projects, increasing adoption in automotive repair (especially in independent garages), and rising investments in construction and infrastructure—particularly in Eastern and Southern Europe. Additionally, stricter EU regulations on emissions have pushed users toward electric and battery-powered compressors over traditional gas models.

Are battery-powered portable compressors gaining traction in Europe?

Yes—significantly. With urban noise restrictions and the EU’s focus on reducing carbon emissions, cordless and battery-operated compressors are becoming preferred, especially in residential areas and mobile service applications. Brands like Bosch, Metabo, and Makita are leading this shift with lithium-ion models offering better run times and faster recharge cycles.

How do EU energy efficiency regulations affect portable compressor design?

The EU’s Ecodesign Directive and Energy Labelling Regulation now influence compressor motor efficiency, standby power consumption, and lifecycle emissions. Manufacturers are redesigning units with variable-speed drives, improved thermal management, and lighter materials to comply—without compromising performance.

Which European countries show the strongest market potential for portable compressors?

Germany remains the largest market due to its robust industrial base and automotive sector. However, Poland, Spain, and Italy are seeing faster growth, driven by construction booms and a surge in e-commerce-enabled tool rentals. Nordic countries are also notable for early adoption of green, low-noise models.

Is the “right to repair” movement impacting compressor sales or design in Europe?

Absolutely. Under the EU’s Right to Repair framework, manufacturers are now designing compressors with modular components, longer spare-part availability (often 7–10 years), and clearer service manuals. This not only builds consumer trust but also reduces long-term ownership costs—key selling points for both trade professionals and DIYers.

How are rental and subscription models influencing the market?

Tool-as-a-Service (TaaS) is growing, especially among SMEs and contractors who avoid large capital outlays. Companies like Hilti and Würth offer bundled packages with maintenance, insurance, and upgrades. This model is reshaping purchasing behavior—particularly in countries with high labor mobility like the Netherlands and Belgium.

What role does noise level play in compressor selection across Europe?

Critical. Many European cities enforce strict noise ordinances (often ≤70 dB during daytime hours). As a result, manufacturers are prioritizing quieter operation through advanced mufflers, vibration-dampening casings, and brushless motors. “Whisper-quiet” models are now a standard marketing feature—not just a premium add-on.

Are there supply chain challenges affecting availability in 2025?

While global chip shortages have eased, localized bottlenecks persist—especially for high-efficiency motors and rare-earth magnets used in brushless systems. However, European brands are increasingly sourcing components within the EU (e.g., from Czechia or Romania) to reduce lead times and comply with “strategic autonomy” initiatives.

How do professionals vs. DIY consumers differ in their compressor preferences?

Professionals prioritize duty cycle, durability, and serviceability—often opting for oil-lubricated or industrial-grade units. DIY users lean toward lightweight, oil-free models with intuitive controls and compact storage. Interestingly, the line is blurring: prosumer models with smart diagnostics (via Bluetooth apps) are bridging both segments.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com