Europe Potash Market Size, Share, Trends, & Growth Forecast Report By Product (Potassium Chloride, Potassium Sulphate, Potassium Nitrate, Other Products), End-Use and Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic and Rest of Europe), Industry Analysis From 2025 to 2033

Europe Potash Market Report Summary

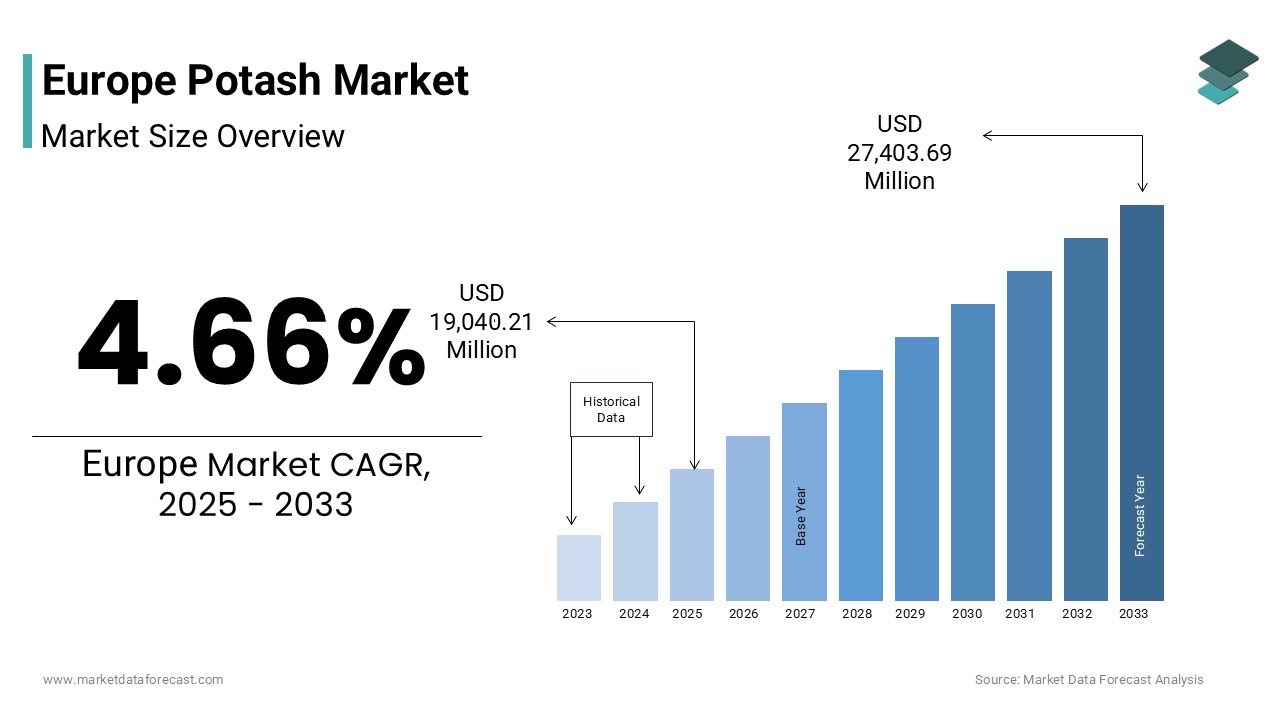

The Europe Potash Market was valued at USD 18,192.28 million in 2024, is estimated to reach USD 19,040.21 million in 2025, and is projected to reach USD 27,403.69 million by 2033, growing at a CAGR of 4.66% during the forecast period from 2025 to 2033. The growth of the European potash market is primarily driven by increasing agricultural demand, rising focus on soil nutrient management, and the adoption of sustainable farming practices across the region. Furthermore, technological advancements in fertilizer production and supportive government policies promoting crop yield enhancement are fueling market expansion.

Key Market Trends

- Increasing demand for potash-based fertilizers to improve soil fertility and crop productivity.

- Rising adoption of sustainable agriculture and precision farming practices across Europe.

- Expansion of domestic potash mining and processing capacities to reduce import dependency.

- Growing awareness about the role of potash in climate-resilient and organic farming systems.

- Strategic collaborations between fertilizer producers and agricultural cooperatives for distribution efficiency.

Segmental Insights

- Based on Product, Potassium Sulphate segment held the major market share in 2024, driven by its suitability for chloride-sensitive crops and premium fertilizer formulations.

- Based on End-Use, Others segment dominated the market in 2024, reflecting its diverse applications in non-agricultural industries, including chemical manufacturing and industrial processes.

Regional Insights

- Germany emerged as the top-performing country, accounting for 23.7% of the European potash market share in 2024.

- Countries such as France, the United Kingdom, and Spain are witnessing steady growth due to expanding agricultural production and modernization of crop nutrient management systems.

- Eastern Europe is showing potential growth opportunities driven by the expansion of crop acreage and increasing fertilizer consumption per hectare.

Competitive Landscape

The Europe potash market is moderately consolidated, with major players focusing on capacity expansion, technological innovation, and sustainable mining practices. Companies are also investing in renewable energy-based extraction and distribution networks to minimize environmental impact. Key market players include K+S AG, EuroChem Group AG, Yara International ASA, JSC Belaruskali, and ICL Group Ltd.

Europe Potash Market Size

The europe potash market size was valued at USD 18,192.28 million in 2024 and is anticipated to reach USD 19,040.21 million in 2025 from USD 27,403.69 million by 2033, growing at a CAGR of 4.66% during the forecast period from 2025 to 2033.

Potash is a potassium-based fertilizer essential for sustaining agricultural productivity across the continent. Potash serves as a primary source of potassium and a macronutrient critical for the growth of major European crops such as wheat, barley, potatoes, and sugar beets. Unlike regions with abundant domestic reserves, Europe relies heavily on imports due to limited mining operations and historically sourcing the majority of its potash from Russia and Belarus. According to the Food and Agriculture Organization of the United Nations (FAO, 2023), cereals occupy about one-third of Europe’s arable land, which is driving consistent demand for potassium supplementation to sustain crop productivity. As per the European Environment Agency (EEA, 2023), more than 60% of agricultural soils in the EU have suboptimal potassium levels, which is requiring regular fertilization to maintain yield potential. Recent geopolitical developments, particularly sanctions following the 2022 Ukraine conflict have disrupted traditional supply routes, which is compelling EU member states to reconfigure sourcing strategies. Concurrently, the European Green Deal’s Farm to Fork Strategy targets a 20% reduction in overall fertilizer use by 2030, yet explicitly recognizes potash’s irreplaceable role in soil fertility during the transition to sustainable agriculture. This dynamic interplay of agronomic necessity, regulatory pressure, and supply chain volatility defines the current structure and trajectory of the Europe potash market.

MARKET DRIVERS

Intensifying Demand for High-Yield Cereal Production

The growing agricultural output of cereal cultivation in Europe is one of the major factors propelling the growth of the European potash market. According to Eurostat (2023), cereals covered nearly 58 million hectares of agricultural land across Europe, which is confirming the region’s continued reliance on cereal cultivation. Crops such as wheat, barley, and maize exhibit high potassium requirements with winter wheat typically needing 60–100 kilograms of potassium oxide per hectare for optimal yield. As per the European Commission’s Directorate-General for Agriculture and Rural Development (DG AGRI, 2022), Germany, France, and Poland are the EU’s top cereal producers and collectively harvested over 250 million metric tons of cereals, which is inherently driving substantial potash consumption. Moreover, climate-induced stresses, including recurrent droughts in Southern Europe have increased the need for potassium to support osmoregulation and disease resistance in crops. Field trials by Germany’s Julius Kühn Institute demonstrated that adequate potash application improved wheat yield stability by up to 18% under water-limited conditions. With urbanization reducing available farmland and global food security concerns mounting, European farmers are under pressure to maximize output per hectare, which is reinforcing the agronomic imperative for balanced potassium nutrition. Consequently, the structural reliance on high-yield cereal systems ensures sustained and resilient demand for potash across the region.

Expansion of Precision Agriculture and Nutrient Management Policies

The integration of precision agriculture technologies is transforming potash application from blanket broadcasting to data-driven and site-specific dosing, which is further driving the growth of the potash market in Europe. According to Eurostat (2023), around 25% of EU farms use precision agriculture technologies, including satellite-based soil monitoring and variable rate nutrient application systems. This shift aligns with stringent EU regulatory frameworks such as the Nitrates Directive and national Nutrient Management Plans, which mandate balanced fertilization to curb environmental degradation. According to the European Environment Agency, imbalanced fertilizer use has contributed to nutrient surpluses in agricultural watersheds that are prompting tighter controls on all nutrient applications, including potassium. The European Court of Auditors confirms that the Common Agricultural Policy (CAP) 2023–2027 cycle allocates significant funding to digital farming infrastructure, which is accelerating the adoption of smart nutrient management tools. In the Netherlands, research by Wageningen University showed that precision mapping helped reduce potassium application rates without compromising crop yields. Thus, rather than diminishing potash use, these policies are refining its application and creating a more sophisticated, technology-enabled demand base.

MARKET RESTRAINTS

Geopolitical Disruptions in Traditional Supply Chains

The historical dependence of Europe on potash imports from Russia and Belarus has exposed the market to acute supply volatility, which is one of the significant restraints to the growth of the European potash market. According to the United Nations Comtrade Database (2021), Russia and Belarus together accounted for the majority of the EU’s potash supply prior to 2022. Following sanctions and logistical restrictions after Russia’s invasion of Ukraine, Belarusian exports via the Lithuanian port of Klaipėda halted completely while Russian shipments faced severe banking and shipping barriers. As per the European Commission’s Trade Statistics Unit, a sharp decline was seen in potash imports from both countries in 2022. Although Canada, Germany, and Israel emerged as alternative sources, their capacity could not immediately offset the shortfall. Freight costs also rose significantly, with bulk carrier rates from Vancouver to Rotterdam more than doubling during the first half of 2022, according to the Baltic Exchange. These disruptions led to inventory shortages, delayed planting cycles, and price spikes for end users. While new rail and transshipment routes are being developed, they remain inefficient and costly. This structural fragility demonstrates how external political events can destabilize potash availability independent of underlying agricultural demand, posing a persistent risk to the potash market growth in Europe.

Stringent Environmental Regulations Limiting Fertilizer Application

The environmental legislation of the European Union imposes significant constraints on potash usage through broad nutrient reduction mandates, which is further hampering the regional market expansion. The Farm to Fork Strategy explicitly targets a 20% reduction in overall fertilizer use by 2030 compared to 2018 levels, as stated in the European Commission’s Green Deal communications. Although potassium is not a primary water pollutant like nitrogen or phosphorus, it is often regulated within holistic nutrient management frameworks. The EU Fertilising Products Regulation requires mandatory soil testing before potassium application in nitrate vulnerable zones, which cover a substantial portion of the EU’s agricultural land, according to the European Environment Agency. National policies reinforce these restrictions; in Denmark, regulations on excess potassium applications have led to a measurable decline in potash sales, according to Statistics Denmark. Additionally, the Water Framework Directive compels member states to monitor nutrient runoff, indirectly discouraging liberal potash use. These overlapping regulations create compliance burdens that suppress market volume growth, even when soil testing indicates potassium deficiency, thereby constraining the European potash market growth.

MARKET OPPORTUNITIES

Diversification of Import Sources and Strategic Stockpiling Initiatives

In response to supply chain shocks, European institutions and private actors are actively diversifying procurement and establishing strategic reserves, which is considered as a promising opportunity in the European potash market. The European Commission’s Fertilisers Europe Security of Supply Task Force has prioritized Canada, Germany, and Israel as key alternative suppliers. According to Natural Resources Canada (2023), potash exports to the EU rose significantly totaling over 4 million metric tons, which is supported by long-term contracts with producers such as Nutrien and Mosaic. Domestically, Germany’s K+S Group increased output from its Werra mines to meet regional demand, as reported by the German Federal Institute for Geosciences and Natural Resources. Beyond sourcing, strategic stockpiling is gaining traction. The Netherlands launched a national fertilizer reserve in 2023 with substantial storage capacity, sufficient to cover a notable portion of its annual potash needs, according to the Dutch Ministry of Agriculture, Nature and Food Quality. Similar buffer programs are advancing in Poland and France, where cooperatives are mandated to maintain minimum supply reserves. These initiatives enhance supply resilience, stabilize pricing, and reduce vulnerability to external disruptions, which is creating a more secure and adaptive market structure for potash in Europe.

Advancement in Potash-Efficient Crop Varieties and Soil Health Programs

Innovations in plant genetics and regenerative agriculture are redefining how potash is utilized in European farming systems, which is a promising opportunity for the market participants in the regional market. According to the European Commission’s Horizon Europe Programme (2023), several EU-funded agricultural research projects are developing crop varieties that sustain yields with reduced potassium inputs through improved nutrient uptake efficiency. These advances are supported by the EU’s Soil Mission initiative, which has committed over €1 billion to soil regeneration practices such as cover cropping, compost application, and reduced tillage. The Joint Research Centre has reported that such methods can increase soil nutrient availability across pilot regions in Europe. In Sweden, farms participating in the national Soil Health Certification Scheme have reported reduced synthetic potash purchases while maintaining stable yields, according to the Swedish Board of Agriculture. These developments align with sustainability goals yet preserve potash’s relevance by optimizing its biological cycling and application timing, thereby opening a nuanced growth pathway centered on efficiency rather than volume.

MARKET CHALLENGES

Persistent Soil Potassium Depletion Across Arable Land

The widespread potassium deficiency threatens the long-term productivity of European farmland is majorly challenging the growth of the potash market in Europe. According to the European Environment Agency (EEA, 2023), large portions of EU agricultural soils show nutrient imbalances with potassium deficiencies increasingly observed in intensively farmed regions. The situation is more severe in Eastern Europe with countries like Romania and Bulgaria report significantly lower average soil potassium concentrations based on national soil monitoring data compiled by the Joint Research Centre. Continuous cropping without adequate replenishment has created a significant potassium deficit across the EU. This depletion directly compromises crop performance; research from the Leibniz Centre for Agricultural Landscape Research shows that potassium-deficient soils can increase cereal lodging and reduce potato tuber quality. Farmers attempting to comply with fertilizer reduction targets often underapply potassium, which is mistaking it for a dispensable input. Without targeted policy recognition of potassium’s unique role, this silent soil degradation could erode yield stability and undermine food security and presenting a critical agronomic challenge that transcends market dynamics.

Logistical Bottlenecks in Alternative Import Infrastructure

The rapid shift of Europe to non-Russian potash suppliers has exposed severe limitations in port, rail, and inland distribution infrastructure, which is also challenging the growth of the potash market in Europe. Canadian potash, which is now the dominant import source and arrives in large capesize vessels requiring deep-water berths and specialized bulk handling equipment. According to European Sea Ports Organisation, the EU’s largest hubs such as Port of Rotterdam handled around 437 million tons of cargo in recent years, underscoring the concentration of deep-sea bulk capacity in very few ports. About a handful of major European ports have the deep‑water, large‑bulk facilities needed for oversized shipments, which is creating heavy reliance on transshipment hubs and resulting in added transit delays. Inland freight infrastructure also faces serious gaps with shortage of suitable wagon‑types and bottlenecks particularly in Southern and Eastern Europe. For example, potash deliveries from one Spanish port to regional farms took much longer than equivalent nitrogen fertilizer shipments. These infrastructural gaps inflate costs, delay seasonal applications, and limit the scalability of alternative sourcing are posing a systemic barrier to supply‑chain resilience in the European potash market.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| Segments Covered | By Product, End-Use, and Region. |

| Various Analyses Covered | Global, Regional, and Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, the Netherlands, Turkey, the Czech Republic, and the Rest of Europe |

| Market Leaders Profiled | K+S AG, EuroChem Group AG, Yara International ASA, JSC Belaruskali, ICL Group Ltd |

SEGMENTAL ANALYSIS

By Product Insights

The potassium sulphate segment occupied the major share of the European potash market in 2024. The growth of the potassium sulphate segment in the European market is attributed to its chloride free composition which makes it ideal for chloride sensitive crops such as potatoes grapes and tobacco that are widely cultivated across Western and Southern Europe. According to Eurostat, the EU harvested approximately 48.3 million tonnes of potatoes in 2023, with Germany (11.6 million t), France (17.9 % of total), and Netherlands (13.4 %) together accounting for roughly 55.4 % of the output. These crops exhibit high potassium demands and are highly responsive to sulphate‑based potassium sources which also supply essential sulphur, which is a nutrient increasingly deficient in European soils. According to the Joint Research Centre, many parts of the EU show sulphur deficiency in soils, which is exacerbating reliance on potassium sulphate. Regulatory frameworks under the Nitrates Directive discourage chloride‑based fertilizers in vulnerable zones, which cover a substantial portion of agricultural land as per European Environment Agency data. Leading producers such as K+S Group in Germany and ICL Group have expanded specialty potash production capacity to meet this demand, which is reflecting the entrenched dominance of the potassium sulphate segment in the European market.

The potassium nitrate segment is estimated to grow at a CAGR of 6.12% over the forecast period in the European potash market owing to its dual nutrient profile and rising adoption in high value horticulture and protected cultivation systems. According to Eurostat (2023), the European protected agriculture sector, including greenhouses and vertical farms continues to expand steadily with Spain, the Netherlands, and Italy leading in greenhouse vegetable production. Potassium nitrate is preferred in these controlled environments because it supplies both potassium and nitrogen in nitrate form, which is immediately available to plants and does not acidify soil. As per the European Environment Agency (EEA), a decline was seen in the use of ammonium-based fertilizers in recent years, which is reflecting the European Green Deal’s emphasis on reducing ammonia emissions and promoting more sustainable nutrient sources. Furthermore, potassium nitrate enhances fruit quality and shelf life that is making it indispensable for export-oriented horticulture. According to the Spanish Ministry of Agriculture, Fisheries and Food (2023), Spain remains one of Europe’s largest exporters of fresh fruits and vegetables with potassium nitrate widely used in greenhouse tomato and pepper cultivation. This convergence of policy support, technological adoption and market demand for premium produce are expected to boost the expansion of the potassium nitrate segment in the European market.

By End Use Insights

The Others segment held the dominating share of the European potash market in 2024. According to Eurostat (2023), the utilized agricultural area of Europe spans about 157 million hectares, which is confirming the scale of fertilizer demand across the continent. Potash remains fundamental to maintaining soil fertility with Germany, France, Poland, and Italy among the largest consumers of potassium-based fertilizers. Unlike North America, where fluid catalytic cracking (FCC) catalysts in petroleum refining utilize potassium compounds, the refining sector of Europe has largely transitioned toward low- or potassium-free catalyst formulations due to stricter emissions standards and reduced crude processing volumes. According to the European Environment Agency (EEA), refinery throughput in the EU has declined notably in recent years, which is reinforcing this shift. Consequently, agricultural demand remains the dominant driver of potash consumption with virtually no large-scale industrial FCC catalyst usage. This structural reality ensures that the others segment maintains overwhelming dominance driven by the Europe’s agronomic needs rather than industrial chemical applications.

The FCC catalyst segment is experiencing modest but steady growth in the European market due to the niche applications in renewable fuel production and catalyst regeneration technologies. As per the International Energy Agency Europe’s renewable diesel and sustainable aviation fuel capacity is expected to increase fivefold by 2027 requiring advanced refining processes where potassium doped catalysts enhance selectivity and stability. Finland’s Neste and Italy’s Eni have commissioned new biorefineries that utilize potassium containing zeolite catalysts for hydrotreating vegetable oils and waste fats as confirmed by the European Renewable Fuels Association. Additionally, research from the Technical University of Munich demonstrated that potassium modified FCC catalysts improve coke resistance by 12% extending catalyst life in co processing units. While Europe’s conventional oil refining continues to contract the emerging bio refining sector creates a specialized demand for potassium based catalytic materials. The ReFuelEU Aviation Initiative of the European Union mandates 2% sustainable aviation fuel by 2025 further incentivizes this shift.

REGIONAL ANALYSIS

Germany Potash Market Analysis

Germany stood as the top performer and accounted for the leading share of 23.7% of the European potash market in 2024. The dominance of Germany in the European potash market driven by its intensive agricultural sector and domestic mining capacity. According to the German Federal Institute for Geosciences and Natural Resources (BGR, 2023), Germany produced around 3 million metric tons of potash, which is making it the only major producer in Western Europe. The agricultural output of Germany is highly potassium-intensive with millions of hectares dedicated to cereals and hundreds of thousands to potato cultivation, as reported by the Federal Statistical Office (Destatis). The farmers of Germany apply substantial quantities of potassium-based fertilizers annually to sustain yields on intensively cultivated soils. K+S Group, headquartered in Kassel, operates Europe’s largest potash mining complex in the Werra region by supplying both domestic and export markets. Regulatory compliance under Germany’s Fertilizer Ordinance mandates soil testing and balanced nutrient management and has further institutionalized efficient potash application. Additionally, the leadership of Germany in precision farming with a significant share of farms using GPS-guided fertilizer systems ensures optimal potassium utilization. This combination of production capability, agronomic demand, and technological advancement are further contributing to the dominating role of Germany in the European market.

France Potash Market Analysis

France held the second largest share of the European potash market in 2024. France holds a pivotal role in the Europe potash market as the continent’s largest agricultural producer with a strong emphasis on cereals oilseeds and viticulture. According to FranceAgriMer (2023), France harvested approximately 65 million metric tons of cereals, including around 34 million metric tons of soft wheat, which has high potassium requirements to support grain filling and straw strength. French farmers apply significant volumes of potassium-based fertilizers annually, with particularly high usage in the Grand Est and Hauts-de-France regions where soil potassium depletion is widespread. As per the French Ministry of Agriculture, large portions of arable land in these regions test below optimal potassium levels requiring consistent nutrient replenishment. Despite the Farm to Fork Strategy’s fertilizer reduction objectives, France maintains robust potash demand due to its export-oriented agricultural sector with farm exports exceeding €80 billion in 2023, according to INSEE. France also benefits from strong logistics infrastructure. According to the Haropa Port Authority, the Port of Le Havre handles substantial volumes of fertilizer-grade potassium salts annually. This combination of agronomic intensity, export competitiveness, and logistical capacity are primarily driving the prominence of France in the European potash market.

Poland Potash Market Analysis

Poland has emerged as a key growth engine in the Europe potash market. The potash market in Poland is majorly fuelled by its expanding agricultural exports and strategic shift away from Russian Belarusian supplies. According to Poland’s Central Statistical Office (GUS, 2023), Poland imported approximately 1.8 million metric tons of potash with Canada and Germany replacing the majority of previously sourced volumes from Eastern suppliers. The agricultural sector of Poland that represents a small but vital share of national GDP produced about 32 million metric tons of cereals and 7 million metric tons of potatoes in 2023. These crops are cultivated on soils naturally low in potassium, particularly in the eastern voivodeships where soil monitoring data from the Institute of Soil Science and Plant Cultivation indicates below-optimal nutrient levels. The government’s Agricultural Market Agency established a national fertilizer reserve in 2023 to stabilize prices and ensure availability during planting seasons. Additionally, Poland’s participation in the EU Common Agricultural Policy has accelerated farm modernization with a significant portion of farms now using digital soil mapping tools to optimize potassium application, as noted by the Polish Federation of Fertilizer Producers. This blend of policy support, agronomic necessity, and supply chain restructuring are a few of the key factors propelling the potash market growth in Poland.

Italy Potash Market Analysis

Italy is anticipated to account for a substantial share of the European potash market over the forecast period owing to its specialization in high value horticulture and permanent crops which exhibit elevated potassium requirements. According to ISTAT (2023), Italy dedicates over 1.2 million hectares to fruit orchards and around 600,000 hectares to vegetable cultivation with crops such as tomatoes, grapes, and olives requiring consistent potassium nutrition to maintain quality and yield. Italian farmers apply substantial volumes of potassium-based fertilizers annually, particularly in southern regions like Puglia and Sicily where sandy soils have low potassium retention capacity. As per the Italian National Institute of Agricultural Economics, potassium sulphate remains the dominant potash type used nationwide due to the prevalence of chloride-sensitive crops. The reliance of Italy on imports is nearly total with the Port Authority of the Upper Adriatic reporting that the Port of Trieste handles large volumes of fertilizer-grade potash each year. The nation’s participation in the EU’s Farm Sustainability Tool for Nutrients has further driven adoption of potassium management practices, with many farms implementing digital nutrient tracking systems by 2023, according to the Ministry of Agricultural Policies. This combination of premium crop focus, agronomic necessity, and precision fertilization are favouring the potash market growth in Italy.

Spain Potash Market Analysis

Spain is estimated to register a notable CAGR in the Europe potash market over the forecast period due to its extensive greenhouse agriculture and export driven horticultural sector. According to the Spanish Ministry of Agriculture, Fisheries and Food (MAPA, 2023), Spain leads the EU in greenhouse vegetable production with over 30,000 hectares under protected cultivation, which is primarily concentrated in Almería. These intensive systems require frequent potassium applications, as crops like tomatoes and peppers demand high nutrient inputs to maintain yield and quality. In 2023, Spain imported significant volumes of potash, with a growing shift toward potassium nitrate due to its compatibility with fertigation systems used in controlled environments. As per the Spanish Agricultural Guarantee Fund (FEGA), horticultural exports exceeded €16 billion in 2023 in Spain, which is making nutrient efficiency a commercial priority for growers. Additionally, recurring drought conditions have increased reliance on potassium to enhance crop water-use efficiency with field trials by the Institute for Sustainable Agriculture demonstrating improved yields under deficit irrigation when potassium nutrition is optimized. Spain’s strategic Mediterranean location also positions it as a key logistics hub for North African potash flows. This confluence of climatic challenges, export orientation, and advanced agronomic practices are driving the Spanish potash market growth.

COMPETITVE LANDSCAPE

The Europe potash market features a dynamic competitive landscape shaped by the interplay of domestic producers global exporters and evolving regulatory pressures. Traditional dominance by Eastern European suppliers has given way to intensified competition from Canadian North African and Middle Eastern producers seeking to fill the supply gap. Domestic players like K S Group benefit from logistical proximity and policy support but face cost pressures from imported alternatives. Competition is increasingly shifting from price alone to service differentiation including digital tools agronomic support and sustainability credentials. New entrants are leveraging niche products such as low chloride or slow release formulations to capture premium segments. At the same time consolidation among distributors is creating gatekeeper entities that influence supplier access. This multifaceted rivalry drives innovation in both product and delivery models as participants strive to secure reliable long term relationships with European agricultural stakeholders amid persistent geopolitical and environmental uncertainty.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the europe potash market include

- K+S AG

- EuroChem Group AG

- Yara International ASA

- JSC Belaruskali

- ICL Group Ltd

Top Players in the Europe Potash Market

K S Group

K S Group is a leading European potash producer headquartered in Germany with extensive mining operations in the Werra region. The company plays a pivotal role in supplying potassium fertilizers to European farmers and contributes significantly to global specialty potash output. In recent years K S Group has invested heavily in expanding its production capacity and modernizing its extraction technologies to enhance efficiency and reduce environmental impact. The company launched its sustainability roadmap in 2023 focusing on water recycling and carbon neutrality which aligns with EU regulatory expectations and strengthens its position as a reliable domestic supplier amid geopolitical supply uncertainties.

ICL Group

ICL Group is a global specialty minerals company with a strong footprint in the European potash market through its potassium sulphate and controlled release fertilizers. Headquartered in Israel ICL serves high value crop sectors across Southern and Western Europe. The company has intensified its engagement with European distributors and agronomic advisors to promote precision nutrient solutions. In 2023 ICL inaugurated a new logistics hub in the Netherlands to improve delivery reliability and reduce lead times for European customers reflecting its strategic commitment to regional market responsiveness and service excellence.

Nutrien

Nutrien is a major North American integrated agricultural company that supplies significant volumes of potash to Europe following the disruption of Eastern European sources. The company leverages its Canadian mining assets to meet European demand and has strengthened its distribution partnerships across Germany France and Poland. In 2024 Nutrien enhanced its digital agronomy platform for European growers offering tailored potassium recommendations based on soil and crop data. This move reinforces its value proposition beyond commodity supply by embedding technical support and sustainability metrics into its customer engagement model.

Top Strategies Used by the Key Market Participants

Key players in the Europe potash market are prioritizing supply chain diversification to reduce reliance on geopolitically sensitive regions. They are investing in strategic port and rail infrastructure to ensure timely delivery across the continent. Companies are expanding specialty potash production particularly potassium sulphate and nitrate to cater to high value crops and environmental regulations. Digital agronomy platforms are being deployed to offer data driven nutrient management services enhancing customer retention. Long term offtake agreements with European cooperatives and distributors are being signed to secure market access. Sustainability initiatives including carbon footprint reduction and water stewardship are being integrated into operations to align with EU policy frameworks. These strategies collectively aim to build resilience efficiency and customer centricity in a volatile market environment.

MARKET SEGMENTATION

The research report on the europe potash market has been segmented and sub-segmented based on categories.

By Product

- Potassium Chloride

- Potassium Sulphate

- Potassium Nitrate

- Other Products

By End Use

- FCC Catalyst

- Agriculture

- Other End Uses

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

What is the Europe Potash Market?

The Europe Potash Market focuses on the production, distribution, and utilization of potassium-based fertilizers, primarily used to improve soil fertility and crop yield across the region.

What factors are driving the growth of the Europe Potash Market?

Key growth drivers include the increasing need for high-yield crops, advancements in fertilizer efficiency, government support for balanced nutrient use, and growing demand for organic and sustainable fertilizers.

What are the main applications of potash in Europe?

Potash is primarily used in agriculture as a vital nutrient for crops like wheat, corn, potatoes, and sugar beet. It also finds limited use in industrial applications such as glass manufacturing and chemical processing.

Which countries dominate the Europe Potash Market?

Major consumers and importers include Germany, France, the United Kingdom, Poland, and Spain, owing to their large-scale agricultural output and developed fertilizer industries.

Who are the key players in the Europe Potash Market?

Leading companies include K+S AG, EuroChem Group AG, Yara International ASA, JSC Belaruskali, and ICL Group Ltd — all of which have strong production, distribution, and research capabilities in the potash sector.

What challenges does the Europe Potash Market face?

The market faces challenges such as fluctuating raw material prices, environmental regulations, and the limited availability of natural potash reserves within Europe, leading to reliance on imports.

How is sustainability influencing the potash market in Europe?

Sustainability initiatives are promoting eco-friendly mining practices, nutrient management programs, and low-impact fertilizer formulations to support Europe’s green agriculture goals.

What is the future outlook for the Europe Potash Market?

The market is expected to witness steady growth, supported by digital agriculture, precision farming technologies, and increasing awareness of balanced nutrient management among European farmers.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com