Europe Poultry Feed Market Size, Share, Growth, Trends, And Forecast Report, Segmented By Type, Feed Additives, And By Region (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic and Rest of Europe), Industry Analysis From (2026 to 2034

Europe Poultry Feed Market Size

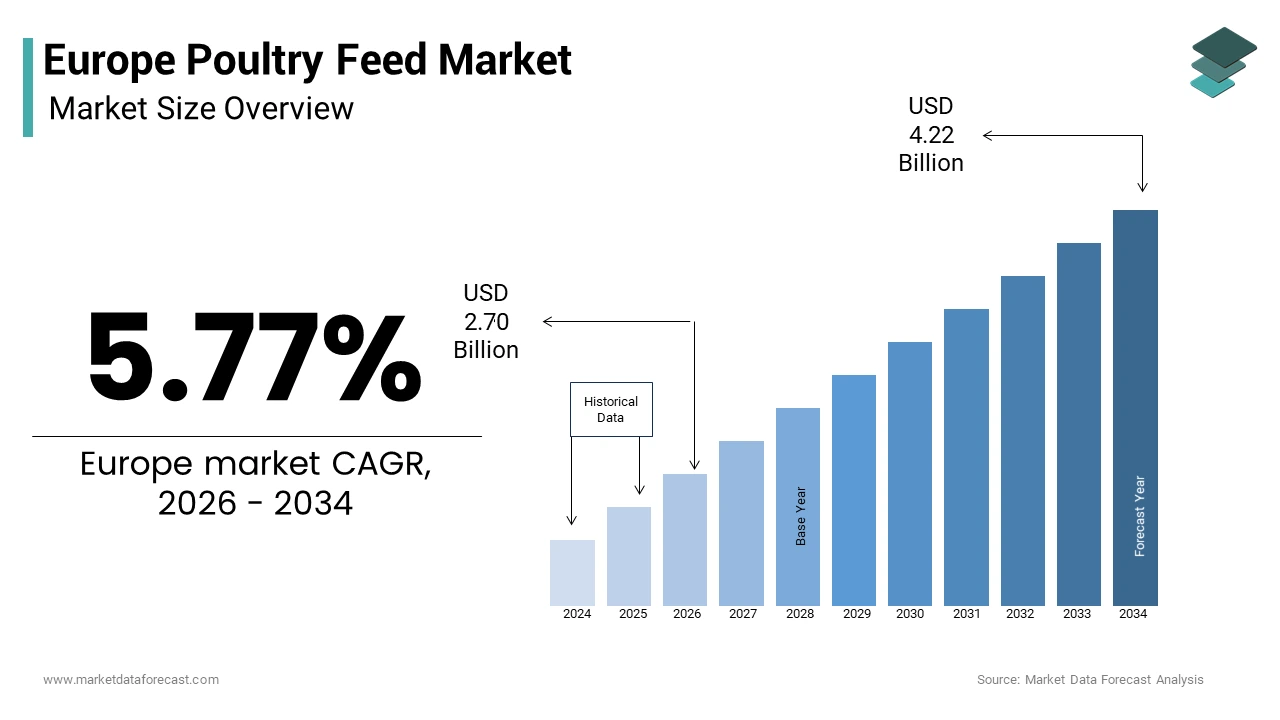

The European poultry feed market was valued at USD 2.55 billion in 2025 and is anticipated to reach USD 2.70 billion in 2025 from USD 4.22 billion by 2034, estimated to grow at a CAGR of 5.77% from 2026 to 2034.

Current Introduction of the European Poultry Feed Market

Poultry feed is a nutritionally complete food specially formulated for domestic birds like chickens, ducks, and geese to support their growth, health, and production of meat or eggs. These feeds are primarily composed of cereals such as wheat and maize, protein sources like soybean meal and rapeseed cake, along with essential vitamins, minerals, and increasingly, functional additives including probiotics, prebiotics, and phytogenics. Unlike generic animal feed, poultry rations are precisely calibrated to meet species-specific metabolic demands at different life stages while complying with stringent EU regulations on antibiotic use, genetically modified organisms, and environmental impact. Poultry has become a dominant pillar of the European meat market, consistently expanding its production volume and securing its position as a primary protein source for consumers as traditional red meat sectors decline. Rising environmental standards are forcing poultry farmers to use specialized feed that cuts nitrogen waste and lowers the industry’s high pollution levels. Furthermore, European policy is aggressively phasing out the use of traditional medications in livestock, sparking a major transition toward natural health boosters and more sustainable farming methods to safeguard public health. This regulatory, nutritional, and environmental nexus defines the strategic contours of the European poultry feed sector.

MARKET DRIVERS

Rising Poultry Meat Consumption and Production Intensification

Poultry has become the most consumed meat in several European countries due to its affordability, perceived health benefits, and lower environmental footprint compared to red meat, which accelerates the growth of the European poultry feed market. This shift is directly fueling demand for specialized feed formulations. According to Eurostat and EU market observers, EU poultry consumption continues to rise, driven by consumer preference for affordable protein, allowing it to surpass other meats. Poultry production has experienced a significant rebound, with major producing nations in 2024 driving overall growth above 2020 levels. This shift is particularly pronounced in Southern and Eastern Europe. In Spain and Poland, the poultry sector is experiencing strong growth and represents a primary share of national meat production, driven by both high domestic consumption and significant export demand. The intensification of production to meet this demand necessitates high efficiency feed conversion ratios, pushing integrators toward precision nutrition. Research into feeding strategies demonstrates that optimized dietary formulations are successfully enhancing the efficiency of poultry production, leading to a reduction in the amount of feed necessary for producing chicken meat. Additionally, the rise of integrated poultry companies like PHW Group in Germany and Aviagen in the UK ensures vertical control over feed quality and composition, reinforcing reliance on scientifically balanced rations. Poultry feed is the foundational lever for productivity, welfare, and compliance as the industry expands to meet rising demand for sustainable, lean protein.

EU Ban on Antibiotic Growth Promoters Driving Adoption of Alternatives

The European Union’s long-standing prohibition on antibiotic growth promoters, fully enforced since 2006 and reinforced by the 2021 Veterinary Medicinal Products Regulation, has fundamentally reshaped poultry feed formulation toward functional alternatives and propelled the expansion of the European poultry feed market. According to the European Medicines Agency (EMA), sales of antimicrobials for food-producing animals in Europe have seen a substantial, long-term decline, with poultry production playing a key role in adopting alternative health solutions. This regulatory environment has catalyzed investment in feed additives such as probiotics, organic acids, and phytogenic compounds that enhance gut health and immunity without contributing to antimicrobial resistance. Research confirms that poultry diets enhanced with natural substitutes, such as specific probiotics and phytobiotics, demonstrate better weight gain and improved survival rates under commercial farming conditions. Feed manufacturers have responded by launching “antibiotic-free” premix portfolios certified under EU feed hygiene regulations. Moreover, the Farm to Fork Strategy’s target of halving antimicrobial use by 2030 incentivizes further innovation. The European feed industry is experiencing a significant rise in the adoption of innovative, natural feed additives, driven by regulatory goals for better animal welfare and reduced dependence on pharmaceutical interventions. This regulatory-driven transformation has turned feed from a mere nutritional input into a strategic health management tool, ensuring compliance while maintaining flock performance in an era of responsible production.

MARKET RESTRAINTS

Stringent Regulations on Genetically Modified Ingredients Limiting Raw Material Options

The European Union’s restrictive stance on genetically modified organisms severely constrains the availability and the cost of key protein ingredients in poultry feed, particularly soybean meal, and the growth of the European poultry feed market. The European Commission permits the import of a limited number of genetically modified crop species for food and feed, all of which are prohibited from commercial cultivation within the EU. A vast majority of the soybean meal used in European poultry production is sourced from South America, with almost all of that supply consisting of genetically modified varieties. However, consumer and retailer pressure, especially in Germany, France, and Austria, has led major integrators and supermarkets to mandate non-GM or “GM-free” labeling, forcing feed mills to source more expensive identity-preserved soy or substitute with alternative proteins like rapeseed or sunflower meal. Analyses of European feed markets indicate that non-GM soybean meal holds a significant, persistent price premium over conventional genetically modified equivalents, often driven by the high costs of supply chain segregation. This cost differential squeezes margins for small and medium producers who lack scale to absorb price volatility. Consequently, feed formulators face constant trade-offs between nutritional adequacy, cost control, and market access, a constraint that stifles innovation and increases dependency on politically sensitive supply chains outside Europe.

Volatility in Global Cereal and Protein Prices Disrupting Feed Cost Stability

High vulnerability to fluctuations in global commodity landscapes, particularly for wheat, maize, and soybean meal, impedes the expansion of the European poultry feed market. These commodities constitute a significant share of feed costs. Grain markets have experienced significant price instability driven by logistical disruptions, climate-related production challenges, and evolving policy demands. Localized agricultural downturns in key production regions have reduced available supply, necessitating increased reliance on imports from other areas. Increased freight costs for procuring essential inputs have created additional pressure on supply chains. Livestock producers operating on tight margins find it difficult to fully pass on increased feed expenses to consumers, often resulting in reduced output or herd reductions. The use of financial instruments to mitigate price volatility remains limited among businesses responsible for processing and supplying animal feed. This exposure discourages long term investment in poultry infrastructure and pushes smaller farms out of business. Feed cost volatility poses a persistent risk to EU food security and sector resilience until strategic grain reserves are implemented and domestic protein crop cultivation is expanded under the Common Agricultural Policy (CAP).

MARKET OPPORTUNITIES

Expansion of Insect Meal and Single-Cell Proteins as Sustainable Alternatives

The approval of novel protein sources under EU feed legislation is opening high-potential opportunities for sustainable poultry nutrition, which is likely to fuel the growth of the European poultry feed market. Regulatory bodies in Europe have expanded approved sources for animal feed to include insect-derived ingredients and microorganisms. The inclusion of insect protein for poultry marked an initial expansion in alternative feed ingredients, followed by the authorization of microbial-based options. Production capacity for insect-based feed components has expanded within key European regions. Industry output for insect-derived protein has increased as facilities have scaled up their operations. These ingredients offer compelling advantages. Black soldier fly larvae meal contains a notable share of crude protein and can be reared on organic waste streams, reducing land and water use compared to soy, as per a study. Leading integrators are piloting adoption. Observations indicate that incorporating a small percentage of insect meal into broiler diets can result in growth rates and intestinal health outcomes similar to those observed in conventional soybean-based diets. The utilization of insect-based ingredients aligns with broader European efforts to increase domestic protein sources and enhance the stability of feed supply chains. As part of a strategy to improve environmental sustainability and circularity, insect meals are emerging as a viable component in future poultry nutrition strategies.

Development of Precision Feeding Systems Using Real-Time Data Analytics

Digitalization is enabling a paradigm shift from static batch mixing to dynamic precision feeding tailored to individual flock needs, presenting a transformative opportunity for feed efficiency and sustainability, and for the European poultry feed market. Large-scale poultry operations in several European countries are increasingly adopting connected systems that adjust feed composition in real time based on environmental sensors, animal weight, and health indicators. Manufacturers are integrating technology into feed lines to continuously monitor nutrient content, ensuring consistent delivery regardless of fluctuations in raw materials. Trials indicate that using AI-driven feeding systems to precisely match amino acid supply to metabolic demand can lower nitrogen excretion and reduce feed costs. Furthermore, these systems generate data for carbon footprint reporting required under the EU’s upcoming livestock emission regulations. Advancements in digital connectivity and farm management software are transforming precision feeding from an optional upgrade into an industry standard.

MARKET CHALLENGES

Supply Chain Fragmentation and Lack of Integrated Protein Sourcing Within the EU

The region’s heavy reliance on imported soybean meal exposes the poultry feed sector to geopolitical and logistical risks that affect resilience and the growth of the European poultry feed market. Efforts to increase domestic legume production within the region have not yet resulted in these crops meeting a significant portion of total protein requirements. Logistical challenges, such as shipping delays, can create immediate pressures on supply chains and lead to rapid adjustments in feed formulation. The infrastructure for consolidating, processing, and storing protein crops is less integrated compared to other major agricultural regions, creating logistical hurdles for farmers. The adoption of agricultural policies intended to promote protein crop cultivation has occurred at a slow pace, resulting in a limited percentage of arable land being used for these crops. Europe's poultry production is at risk from external shocks and cost volatility unless it invests in regional crushing, contract farming, and improved quality standards.

Skills Gap in Nutritional Formulation and Digital Feed Management

The rapid evolution of poultry feed science, encompassing alternative proteins, microbiome modulators, and data-driven formulation, has outpaced the availability of skilled professionals capable of optimizing complex rations, which holds back the expansion of the European poultry feed market. Observations indicate a limited availability of personnel trained in advanced nutritional modeling and digital management systems within certain regional feed production sectors. Reports suggest that certified animal nutritionists are not frequently employed in smaller-scale feed manufacturing operations. Data points toward potential inconsistencies in nutrient formulation that may affect efficiency and alignment with livestock requirements. This gap is exacerbated by the retirement of experienced formulators. Consequently, many farms rely on generic premixes rather than customized solutions, missing opportunities for efficiency and sustainability. Wageningen and Bologna offer advanced education, yet their practical training fails to keep pace with industry demands. Public-private partnerships must expand continuing education and digital literacy in feed science to unlock the full potential of next-generation poultry nutrition across Europe’s diverse production landscape.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 5.77% |

| Segments Covered | By Type of Poultry Product, Feed Additives, And By Region |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis; Segment-Level Analysis; DROC; PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, the Czech Republic, and the Rest of Europe |

| Market Leaders Profiled | BASF Badische Anilin und Soda Fabrik) (Germany) and Evonik Industries AG (Germany). |

SEGMENTAL ANALYSIS

By Type of Poultry Product

The broilers segment dominated the Europe poultry feed market by accounting for a 64.5% share in 2025. The dominance of the boilers segment is driven by the high volume and rapid turnover of broiler production systems designed to meet surging consumer demand for affordable white meat. According to European Commission data, EU poultrymeat production reached a new high in 2024, driven by increasing consumer demand for affordable, lower-fat meat alternatives. This upward trend in poultry production and consumption continues to outpace the consumption of beef and veal, which are experiencing a long-term decline in market share. A further key factor sustaining this leadership is the economic efficiency of broiler farming. Broiler chickens reach slaughter weight within a short period, requiring specialized, phased feeding programs to optimize nutrient uptake. Industry practices focus on enhancing the efficiency with which birds convert feed into body mass. Research indicates that adjusting dietary rations can result in a measurable decrease in the amount of feed required to produce a kilogram of live weight. These improvements in feed efficiency are observed in commercial production environments. Furthermore, integrated poultry companies like PHW Group in Germany and Aviagen in the UK control the entire value chain from breeding to feed formulation, ensuring consistent demand for specialized broiler feed. Retailers also reinforce this trend. Supermarket private label chicken programs in the UK and Spain rely on standardized broiler supply chains that mandate specific nutritional protocols. Broiler feed remains central to the European poultry industry, driven by the need for affordable, accessible protein.

The layers segment is likely to experience the fastest CAGR of 5.9% between 2026 and 2034 due to rising demand forhigh-qualityy eggs driven by nutritional awareness, food service recovery, and policy shifts toward enriched housing systems. Egg consumption in the European Union has shown an upward trend, driven by consumer preference for protein-rich diets and home baking. The transition toward alternative housing systems for laying hens, such as free-range and organic, has influenced production and consumer choices. In specific European nations, a significant majority of laying hens are kept in enriched or outdoor environments rather than conventional cages. The shift in housing systems has been supported by regulatory changes, contributing to the evolving landscape of egg production. These welfare-compliant systems require more nutrient-dense feed to support bone health and sustained egg production over longer laying cycles. Additionally, functional egg trends, such as omega three or vitamin D-enriched eggs, are driving adoption of specialized premixes containing flaxseed algae or cholecalciferol. Layer feed innovation is essential for driving productivity and market differentiation, driven by the convergence of consumer ethics and nutritional requirements.

By Feed Additives Insights

The amino acids segment led theEuropeane poultry feed market by capturing a 32.1% share in 2025. The leading position of the amino acids market is propelled by its critical role in enabling low crude protein diets that reduce nitrogen excretion while maintaining bird performance, a priority under the EU’s environmental and antimicrobial reduction strategies. Synthetic lysine, methionine, and threonine allow formulators to precisely balance essential amino acid profiles without overfeeding protein, directly supporting the Farm to Fork Strategy’s target of cutting agricultural ammonia emissions by 2030. Poultry production is recognized as a notable contributor to agricultural ammonia emissions, highlighting a growing focus on optimizing livestock nutrition to manage environmental impact. Studies indicate that lowering dietary crude protein levels, paired with the addition of specific synthetic amino acids, can effectively reduce nitrogen excretion while maintaining broiler performance. To meet the rising demand for these specialized nutritional solutions, ingredient manufacturers are increasing their production capacities within the European market. Amino acids offer the best, most cost-effective solution for optimizing poultry productivity, sustainability, and regulatory compliance, particularly when dealing with volatile feed costs and tightening regulations.

The feed enzymes segment is on the rise and is expected to be the fastest-growing segment in the market by witnessing a CAGR of 7.3% over the forecast period, owing to its dual function in enhancing nutrient digestibility and enabling the use of alternative raw materials amid soy dependency concerns. Phytases, xylanase,se, and protease enzymes break doanti-nutritionalnal factors in cereals and oilseeds, releasing bound phosphorus and amino acids that would otherwise be excreted. Multi-enzyme complexes in wheat-based broiler diets enhance nutrient utilization, which can reduce the reliance on supplemental fats. Enzyme supplementation supports the inclusion of local pulse ingredients, allowing for the partial substitution of soybean meal with faba beans in layer diets without affecting production. These findings indicate that dietary enzyme technology can improve ingredient flexibility in poultry diets while maintaining performance. Regulatory alignment further accelerates adoption. The European Food Safety Authority EFSA recognizes phytase as a tool for reducing inorganic phosphate supplementation, lowering manure phosphorus load. Hence, enzymes are transitioning from optional enhancers to essential enablers of circular and sustainable poultry nutrition.

COUNTRY LEVEL ANALYSIS

Germany Poultry Feed Market Analysis

Germany was the top performer in the European poultry feed market by accounting for a 19.8% share in 2025. The supremacy of the German market is attributed to a dense network of integrated poultry producers, stringent environmental regulations, and advanced feed manufacturing infrastructure. The nation features a major poultry integrator with extensive farming and feed production infrastructure. Government environmental regulations regarding livestock emissions are encouraging the adoption of specialized, lower-protein feed formulations that include synthetic amino acids. Legislative changes regarding housing systems have transitioned the majority of egg production toward enriched or free-range environments. The shift in housing systems has necessitated adjustments in feed, requiring higher levels of calcium and trace minerals for layers. The presence of global additive leaders like Evonik and BASF ensures access to cutting-edge feed solutions. Strong collaboration between industry and academic partners, such as the University of Hohenheim, has established Germany as the premier, science-driven hub for sustainable poultry nutrition in Europe.

France Poultry Feed Market Analysis

France followed closely in the European poultry feed market by capturing a 16.5% share in 2025, with its diverse production systems, from intensive broiler hubs in Brittany to Label Rouge free range operations in the Southwest, each demanding tailored feed formulations. Brittany maintains a significant regional dominance in French poultry production, necessitating a substantial annual volume of feed for its operations. A major driver is the national “Protein Plan,n” which incentivizethe s incorporation of peas and lupins into poultry rations. Through the ongoing national strategy to boost plant protein self-sufficiency, there is a push to increase the use of domestically produced legumes in livestock, including broiler feed. Consumer demand for high-welfare products further shapes demand. The Label Rouge certification, which mandates more extensive farming practices and longer growth cycles, leads to a higher rate of total feed consumption per bird relative to standard, intensive production methods. Additionall,y France’s strict antibiotic reduction targets under the EcoAntibio 2 plan have accelerated the adoption of probiotics and organic acids. This blend of regional diversity policy support and premium market segmentation sustains France’s influential position in both volume and value segments of the poultry feed landscape.

Spain Poultry Feed Market Analysis

Spain is also a major player in the European poultry feed market due to scale efficiency and climate adaptation. As the EU’s second largest poultry producer,r Spain operates highly concentrated broiler complexes in Castilla y León and Catalonia that consume millions of metric tons of feed annually. Water scarcity and heat stress necessitate specialized formulations. Feed mills routinely add betaine and electrolytes to mitigate thermal stress effects on feed intake. A key enabler is export orientation. The region maintains a significant role in supplying poultry products to diverse international markets. Expanding trade relationships with partneronin various continentsnecessitate a focus on meeting rigorous global quality requirements. There is a visible trend toward upgrading production facilities to enhance overall operational efficiency. Sector strategies increasingly emphasize the integration of sustainable and circular components into animal nutrition. Institutional support is being directed toward modernizing infrastructure to better align with evolving environmental and safety standards. Furthermore, drought resilience is critical. Thus, Spain’s feed market thrives on operational scale,e climatic pragmatism,m and global market responsiveness.

United Kingdom Poultry Feed Market Analysis

The United Kingdom grew steadily in theEuropeane poultry feed market. Post Brexit,t the UK has maintained strong demand through retailer-driven standards and integrated production models. A high proportion of broiler production operates under assured schemes that mandate specific feed protocols, including restrictions on certain ingredients and antibiotics. These assurance standards have encouraged investment in identity-preserved, non-GM, and alternative protein sources. Market demand for non-GM feed options has experienced a notable increase within the poultry sector. Anticipated regulatory changes regarding housing systems are influencing demand for layer feed with higher nutrient density. The transition toward alternative poultry housing systems is driving adjustments in nutritional requirements. The UK’s departure from EU feed additive regulations has enabled faster approval of novel enzymes and phytogenics through the Veterinary Medicines Directorate. Tight collaboration between UK retailers like Tesco and supply chain integrators such as Moy Park drives a focus on traceability, ethical sourcing, and rapid adaptation to policy shifts, creating a dynamic environment for premium and compliant food solutions.

Netherlands Poultry Feed Market Analysis

The Netherlands is likely to expand in the European poultry feed market from 2026 to 2034. Despite its small land area, the country exerts disproportionate influence through technological intensity and export-oriented feed innovation. Dutch feed mills produce over 3 million metric tons annually, serving both domestic mega farms and neighboring countries via efficient logistics. A defining feature is the early adoption of precision nutrition. Broiler feed formulation is increasingly utilizing advanced, real-time nutrient profiling based on, for example, near-infrared spectroscopy of raw materials to enhance precision. The region is seeing a shift toward incorporating circular, sustainable ingredients into livestock feed, with notable investment in insect-based, locally sourced protein sources for poultry. Regulatory limitations on nitrogen emissions are actively shaping the poultry industry, necessitating, for example, advancements in diet formulation to improve nutrient efficiency and reduce environmental impact. The industry is shifting toward maximizing productivity per bird through the adoption of, for example, enzymes and phytochemicals in feed to adapt to environmental constraints. The region is developing as a center for sustainable, data-driven poultry nutrition through specialized research and a focus on high-efficiency, technological farming methods.

COMPETITIVE LANDSCAPE

Competition in the European Poultry Feed Market is shaped by a mix of large integrated cooperatives, multinational ingredient suppliers, and regional mills competing on nutritional precision, sustainability credentials,s and supply chain resilience rather than price alone. The market is highly regulated with strict limits on antibiotics, genetically modified ingredients, and environmental emissions, driving innovation in alternative additives and low-protein diets. Leading players differentiate through digitalization,n offering real-time formulation services and farm advisory platforms that link feed performance to bird outcomes. Vertical integration is common with major poultry producers owning feed mills to ensure quality control and cost stability. Barriers to entry remain high due to capital intensity, regulatory complexity, it,y and established relationships with integrators and retailers. However, competition is intensifying as novel proteins like insect meal gain traction and national policies push for domestic protein self-sufficiency. Companies that combine scientific rigor,r circular ssourcin, and data-driven services are best positioned to lead in a market increasingly defined by planetary boundaries and ethical consumption.

KEY MARKET PLAYERS

Some of the major companies dominating the market, by their product services, include

- BASF (Badische Anilin und Soda Fabrik) (Germany)

- ForFarmers Group N.V.

- Agrifirm Cooperatie U.A.

- Evonik Industries AG (Germany).

Top Players In The Market

- ForFarmers is a leading European feed producer with extensive operations across the Netherlands,s Germany, Belgium,m and the United Kingdom,, supplying tailored poultry rations to integrated farms and independent producers. The company emphasizes sustainability through precision nutrition, low protein formulations,ons and circular ingredient sourcing. It also enhanced its digital feed advisory platform, enabling real-time ration adjustments based on flock performance and raw material variability. These initiatives reinforce its role asa science-drivenn partner supporting both productivity and environmental compliance,e not only in Europe but increasingly in global markets through technical collaborations.

- Agrifirm is a major Dutch agricultural cooperative serving over fifteen thousand livestock farmers,s including a significant poultry segment across Benelux and Northern France. The company focuses on integrated solutions combining feed additives,s nutritional advice, and farm management services. It also expanded its amino acid balancing service using near infrared spectroscopy to optimize digestibility and reduce nitrogen excretion. Agrifirm strengthens its reputation as a reliable local partner with international reach in sustainable poultry farming by adhering to regional policies and supply chain transparency standards.

- Evonik is a global specialty chemicals leader that supplies critical feed additives,s including synthetic amino acids, enzymes, and gut health solutions to the European poultry sector. Headquartered in Germany, the company plays a pivotal role in enabling low crude protein diets that comply with EU ammonia reduction targets. It also launched a digital formulation tool that integrates real-time raw material data with bird performance models to recommend optimal additive dosages. Evonik’s innovative solutions for sustainable intensification, spanning nutritional efficiency and environmental care, are establishing new industry standards throughout Europe, Asia, and the Americas.

Top strategies used by the key market participants

Key players in the EEuropeanPoultry Feed Market develop low crude protein formulations supplemented with synthetic amino acids to reduce nitrogen excretion and comply with environmental regulations. They invest in alternative protein sources such as insect meal and European legumes to decrease dependency on imported soy. Companies integrate digital tools for real-time feed optimization based on flock data and raw material analysis. Strategic partnerships with retailers and certification bodies ensure alignment withnon-GM andwelfaree standards. Additionally, they expand production capacity for essential additives like methionine and phytase to secure supply chains and support circular economy goals.

MARKET SEGMENTATION

This research report on theEuropeane poultry feed market is segmented and sub-segmented into the following categories.

By Type of Poultry Product

- Broilers

- Turkeys

- Layers

- others

By Feed Additives

- Amino acids

- Feed enzymes

- Antioxidants

- Vitamins

- Antibiotics

- Feed acidifiers

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

What is the Europe poultry feed market?

The Europe poultry feed market includes all commercial feed products formulated to improve growth, health, and egg or meat output in poultry farms across the region.

Why is poultry feed demand rising in Europe?

Demand is rising because poultry meat is affordable, quick to produce, and widely accepted across European diets.

Which poultry segment consumes the most feed?

Broiler chickens consume the largest share of feed because they grow faster and are produced in higher volumes than other poultry types.

What ingredients are most common in European poultry feed?

Corn, wheat, soybean meal, amino acids, vitamins, and minerals form the base of most poultry feed formulas.

How does feed quality impact poultry productivity?

Better feed quality directly improves bird growth, immunity, egg output, and reduces disease-related losses.

What role do feed additives play in poultry nutrition?

Feed additives help improve digestion, protect gut health, and increase feed efficiency in modern poultry systems.

How does sustainability affect poultry feed formulation?

Feed producers are reducing reliance on imported soy and using alternative proteins to lower environmental impact.

What challenges does the Europe poultry feed market face?

High raw-material prices, regulatory compliance, and disease outbreaks remain the biggest market challenges.

How do regulations influence poultry feed production?

Strict European safety and labeling rules control ingredient selection, manufacturing, and traceability standards.

Are organic and non-GMO feeds gaining popularity?

Yes, more farmers and retailers are choosing natural and non-GMO feeds to meet consumer trust and clean-label demand.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com