Europe Prefilled Syringes Market Research Report By Material, Type, Design, Application, Distribution Channel, By Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic & Rest of Europe) - Industry Analysis on Size, Share, Trends, COVID-19 Impact & Growth Forecast (2025 to 2033)

Europe Prefilled Syringes Market Size

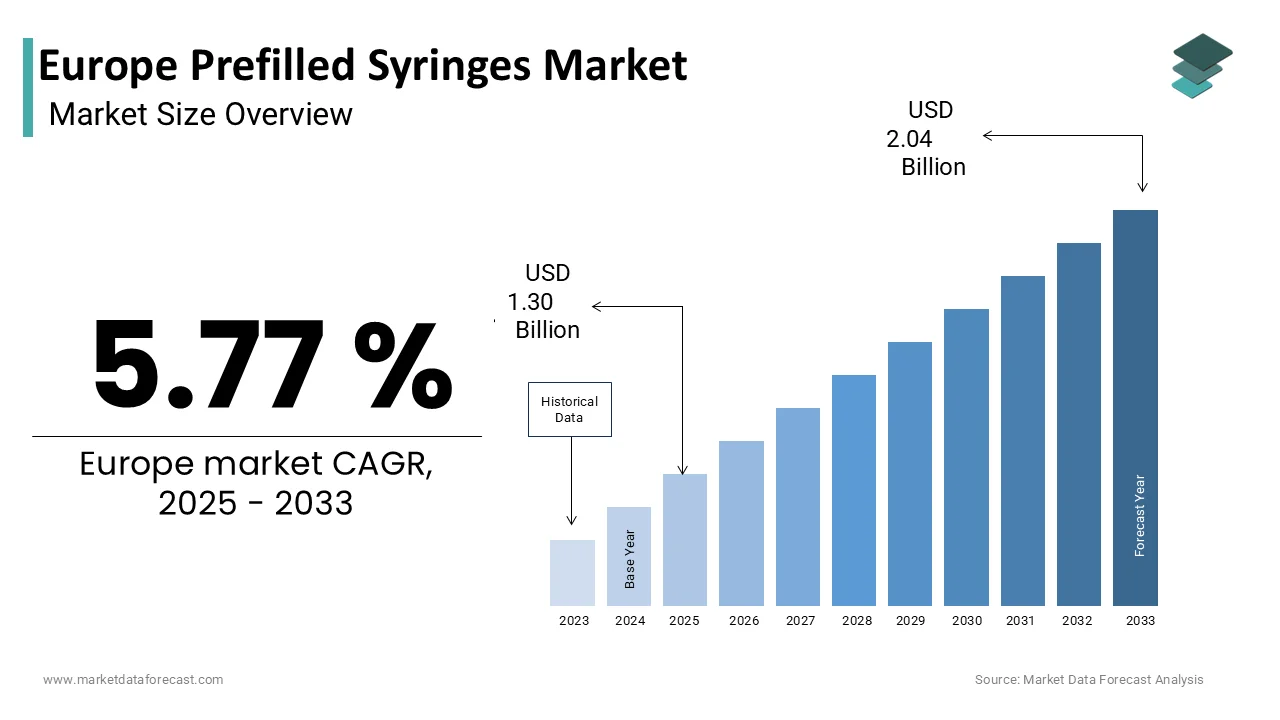

The europe prefilled syringes market was valued at USD 1.23 billion in 2024, is expected to have a 5.77 % CAGR from 2025 to 2033, and be worth USD 2.04 billion by 2033 from USD 1.30 billion in 2025.

The prefilled syringes are sterile single-use delivery systems preloaded with precise doses of injectable pharmaceuticals ranging from vaccines and biologics to chronic disease therapeutics. These devices integrate drug containment and administration into one unit, eliminating the need for vial reconstitution and reducing the risk of dosing errors or contamination. In Europe, their adoption is propelled by evolving healthcare models that prioritize patient safety, outpatient care, and self-administration for long-term conditions. According to the European Centre for Disease Prevention and Control, over 75 million Europeans manage chronic illnesses such as diabetes, rheumatoid arthritis, or multiple sclerosis, often requiring regular subcutaneous injections. National health systems across Germany, France, and the Nordic countries increasingly reimburse home-based injection therapies to alleviate hospital burdens. Furthermore, the European Medicines Agency has issued specific guidelines for container closure integrity and extractables testing for prefilled syringes used with sensitive biologics, reflecting their critical role in modern drug delivery infrastructure.

MAREKT DRIVERS

Rising Prevalence of Chronic Diseases Drives Demand for Self-Administration on Devices

The growing burden of chronic non-communicable diseases is elevating the demand to adopt self-administration devices, where patients increasingly manage treatment at home is solely fuelling the growth of the European prefilled syringes market. According to the World Health Organization Regional Office for Europe, many deaths in the EU are linked to chronic conditions, including diabetes, cancer, and autoimmune disorders, many of which require injectable biologics. For instance, the European Federation of Pharmaceutical Industries and Associations estimates that more than 3.2 million Europeans receive biologic therapies for rheumatoid arthritis, psoriasis, or inflammatory bowel disease, with administered subcutaneously via prefilled syringes. Countries like Sweden and the Netherlands have formalized home therapy pathways where nurses train patients to use prefilled devices, reducing clinic visits.

Expansion of Biologics and Biosimilars Portfolio Intensifies Need for Advanced Delivery Systems

The robust pipeline and commercialization of biologic and biosimilar drugs in Europe necessitate primary packaging solutions that ensure stability, sterility, and accurate dosing is another attribute prompting the growth of Europe's prefilled syringes market. As per the European Medicines Agency, over 80 new biologics were approved between 2020 and 2024, with monoclonal antibodies accounting for nearly half. These large-molecule drugs are highly sensitive to surface interaction, shear stress, and air-liquid interfaces, making traditional vial transfer risky. Prefilled syringes manufactured with coated glass or polymer barrels minimize protein adsorption and aggregation. Furthermore, the European Commission’s biosimilar uptake initiative actively promotes cost-effective alternatives with 15 biosimilars for monoclonal antibodies now marketed across the EU. These products overwhelmingly adopt prefilled syringes to match originator convenience and ensure patient adherence.

MARKET RESTRAINTS

Stringent Regulatory Requirements for Extractables and Leachables Increase Development Complexity

The European regulatory framework imposes rigorous analytical demands on prefilled syringes, particularly concerning extractables and leachables that can compromise drug safety or efficacy, which is hampering the growth of the European prefilled syringes market. As per the European Medicines Agency Guideline on Plastic Immediate Packaging Materials, manufacturers must conduct extensive simulation studies using worst-case conditions to identify potential interactions between the drug formulation and syringe components, including stopper,s barre, ls, and lubricants. Moreover, the EU Medical Devices Regulation indirectly affects combination products by requiring full traceability of device components.

High Material and Manufacturing Costs Limit Accessibility in Price-Sensitive Markets

The higher production expenses than traditional vials due to specialized materials, precision assembly, and sterility assurance protocols, which constrain their adoption in cost-conscious healthcare systems, are additionally hampering the growth of the European prefilled syringes market. According to the European Industrial Pharmacy Consortium, the average cost of a coated glass prefilled syringe with a staked needle ranges from 1.80 to 3.20 euros compared to 0.25 euros for a standard Type I glass vial. Polymer alternatives like cyclic olefin copolymer reduce breakage risk but cost up to 40% more than glass. These differentials become critical in public procurement, where price often outweighs convenience. In Spain, for example, tenders for insulin analogs awarded 92% of volume to vial formats in 2024 due to budget constraints.

MARKET OPPORTUNITIES

Integration with Digital Health Platforms Enables Smart Injection Monitoring

The integration of prefilled syringes with digital health technologies to enhance treatment adherence and real-world data collection is significantly posing new opportunities for the growth of the European prefilled syringes market. European pharmaceutical companies are increasingly embedding sensors or pairing syringes with companion apps that record injection time, dose confirmation, and even physiological responses. Novo Nordisk’s partnership with digital health firm Gocap enabled Bluetooth-enabled caps for its prefilled insulin pens, now used by over 200,000 patients in Germany and the UK. Furthermore, the EU’s Digital Europe Programme allocated 120 million euros in 2024 to support interoperable injection monitoring tools under its chronic disease management pillar.

Growth of Home Healthcare Ecosystems Fuels Demand for User-Friendly Delivery Formats

The shift toward decentralized care models is designed for patient or caregiver use outside clinical settings, which is another attribute enhancing the growth of the European prefilled syringes market. According to the Organisation for Economic Co-operation and Development, home healthcare expenditure in the EU grew by 9.4% annually from 2020 to 2024, with injectable therapies constituting a major service line. National initiatives such as France’s Plan Ma Santé 2022 and Germany’s Home Therapy Directive now cover nurse-led training for self-injection of biologics, enabling over 1.5 million patients to receive treatment at home. This transition requires delivery devices that prioritize ease of use, safety, and psychological comfort. Features like needle shielding, automatic injection, and ergonomic grips have become standard in new prefilled designs. Additionally, community pharmacies across the Netherlands and Denmark now offer prefilled syringe dispensing and disposal services integrated into chronic care pathways.

MARKET CHALLENGES

Supply Chain Vulnerabilities for Specialty Glass Create Production Bottlenecks

The reliance on a narrow global supply base of high-quality borosilicate glass tubing, with the primary material, is one of the restraining factors for the growth of the European prefilled syringes market. According to the European Medicines Agency, over 90% of glass prefilled syringes used in the EU depend on tubing sourced from just three international suppliers, two of which are outside Europe. As per the European Association of Pharmaceutical Full Line Suppliers, lead times for glass syringes extended from 12 weeks to over 30 weeks in 2022, causing temporary shortages for critical drugs, including epinephrine and certain oncology biologics.

Inconsistent Reimbursement Policies Across Member States Hinder Market Harmonization

The fragmented reimbursement frameworks that treat delivery devices as cost adders rather than value enablers are additionally hindering the growth of the European prefilled syringe market. According to the European Network for Health Technology Assessment, only eight EU countries conduct formal health technology assessments that account for administration benefits such as reduced dosing errors or nursing time when evaluating prefilled formats. This disconnect persists despite EU-level guidance from the Pharmaceutical Forum advocating for holistic value assessment.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| Segments Covered | By Material, Type, Design, Application, Distribution Channel, and Region. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, Rest of Europe |

| Market Leaders Profiled | Becton Dickinson and Company, Gerresheimer AG, SCHOTT AG, West Pharmaceutical Services, Inc., Ompi, Catalent, Inc., Weigao Group, Vetter Pharma International GmbH, Nipro Corporation, MedPro Inc. |

SEGMENTAL ANALYSIS

By Material Insights

The glass segment was accounted in holding a prominent share of the European prefilled syringes market in 2024 to the established regulatory acceptance and superior barrier properties of Type I borosilicate glass, which protects sensitive biologics from moisture,e oxy, gen, and leachables. As per the European Directorate for the Quality of Medicines, over 95% of marketing authorizations for injectable biologics in the EU specify glass primary containers due to extensive historical compatibility data. Glass syringes have been used for decades in hospital and home settings with a well-documented safety profile. According to the Paul Ehrlich Institute in Germany, glass containers exhibit negligible levels of extractables even when in contact with high pH monoclonal antibody formulations for extended periods. Additionally, major European pharmaceutical manufacturers such as Roche and Sanofi maintain legacy filling lines optimized for glass, reducing the incentive to re-validate for alternative materials.

The plastic prefilled syringes segment is expected to grow with an expected CAGR of 13.7% from 2025 to 2033, owing to the rising demand for flexible and lightweight delivery systems, especially in home care and emergency settings. Cyclic olefin copolymer and polymer blends now offer barrier properties approaching those of glass while eliminating risks of glass particulates and needlestick injuries from shattered barrels. Companies like Gerresheimer and Stevanato Group have also secured European Medicines Agency scientific advice for polymer platforms supporting high-concentration biologics, further accelerating regulatory confidence and commercial adoption.

By Type Insghts

The conventional segment was accounted for in holding a prominent share of the European prefilled syringes market in 2024, from widespread use in chronic disease management, where patients are trained in standard injection techniques, and cost remains a key consideration for public payers. According to the European Federation of Pharmaceutical Industries and Associations, originator biologics launched before 2020 used conventional designs due to simpler regulatory pathways and lower development costs. Many home therapy systems are engineered to accept standard dimension syringes, enabling modular device strategies. In Germany and France, national health insurers reimburse drugs and devices separately, often favoring lower-cost conventional formats unless safety features are clinically mandated. Additionally, in hospital settings where healthcare professionals administer injections, the perceived need for active safety mechanisms is reduced. This institutional inertia, combined with established manufacturing infrastructure, ensures conventional syringes remain the default choice for a broad range of therapies from insulin to fertility hormones.

The safety segment is expected to register a CAGR of 15.2% from 2025 to 2033, with stringent EU mandates to prevent needlestick injuries, which affect over 1 million healthcare workers annually, as documented by the European Agency for Safety and Health at Work. Directive 2010/32/EU requires all member states to implement measures eliminating sharps injuries, including the use of safety-engineered devices. As per the German Statutory Accident Insurance, over 85% of public hospitals in Germany now procure only safety-integrated syringes for parenteral administration.

By Distribution Channel Insights

The hospitals segment was the largest by holding 52.3% of the European prefilled syringes market share in 2024, with the high volume of acute and chronic injectable therapies administered in inpatient and outpatient departments, including oncology, immunology, and emergency care. National and regional hospital purchasing groups negotiate bulk contracts that favor standardized formats with proven sterility and traceability. These institutions also serve as early adopters for new biologics, which are initially launched in hospital settings before transitioning to home care. Additionally, hospitals maintain strict cold chain and inventory management systems that align with the storage requirements of prefilled syringes containing temperature-sensitive formulations.

The mail order pharmacies segment is likely to register a CAGR of 18.4% throughout the forecast period with the integration of home-based care models, digital prescriptions, and direct-to-patient logistics. National e-prescription systems enable seamless routing of biologic therapies to licensed mail order providers, such as Apotheka and DocMorris, who specialize in temperature-controlled shipping and patient training kits. The second catalyst is payer efficiency. Additionally, these pharmacies integrate adherence support through SMS reminders and video tutorials, significantly improving treatment continuity.

COUNTRY LEVEL ANALYSIS

Germany Prefilled Syringes Market Analysis

Germany was the top performer in the European prefilled syringes market by accounting for 24.3% the market in 2024, with a high prevalence of chronic disease, a robust biopharmaceutical industry, and advanced home care reimbursement frameworks. The country also hosts major pharmaceutical manufacturers and device developers, including Boehringer Ingelheim and Schott Pharma, which drive local innovation in primary packaging. Regulatory clarity further supports market stability as the Paul Ehrlich Institute maintains expedited evaluation pathways for combination products with established container closure systems. Additionally, Germany’s nursing care insurance scheme reimburses home injection training, creating a sustainable ecosystem for patient-centric delivery. These structural factors ensure Germany remains the strategic anchor for prefilled syringe adoption and development across Europe.

France Prefilled Syringes Market Analysis

France's prefilled syringes market growth is likely to be driven by the aggressive biosimilar uptake policies and strong institutional support for home-based therapies. France’s Transparency Committee mandates that all new biologics and biosimilars demonstrate delivery convenience as part of their added therapeutic value assessment, effectively incentivizing prefilled formats. Over 1.2 million French patients now self-inject biologics for conditions like psoriasis and Crohn’s disease, supported by the national “Hospital at Home” program, which provides nurse-led training and home delivery. The French Medicines Agency also enforces strict needlestick injury prevention protocols requiring safety-engineered devices in all public health facilities. Additionally, France’s centralized procurement system through UNOCAM negotiates volume-based pricing for prefilled syringes, ensuring broad access across public and private clinics.

United Kingdom Prefilled Syringes Market Analysis

The United Kingdom's prefilled syringes market growth is likely to register the fastest CAGR during the forecast period, from a well-established home care infrastructure and proactive adoption of digital health tools. The NHS Long Term Plan explicitly promotes self-administration of injectables to reduce outpatient burden, with over 900,000 patients enrolled in home therapy programs for rheumatoid arthritis, multiple sclerosis, and diabetes as of 2024. The National Institute for Health and Care Excellence recommends prefilled syringes as first-line delivery for all new biologics due to reduced error rates and nursing dependency. Furthermore, the UK’s Medicines and Healthcare products Regulatory Agency has streamlined combination product reviews, enabling faster market access for novel drug-device systems. Post-Brexit regulatory autonomy has also allowed accelerated adoption of polymer prefilled platforms not yet widely approved in the EU.

Italy Prefilled Syringes Market Analysis

Italy's prefilled syringes market growth is likely to grow with a large aging population and high incidence of autoimmune disorders requiring long-term injectable therapy. Over 3.5 million Italians suffer from rheumatoid arthritis or psoriasis, and national guidelines mandate biologic treatment escalation when conventional therapy fails. Additionally, Italy has one of Europe’s highest rates of home nursing, with over 420,000 patients receiving weekly injections at home as documented by Istituto Superiore di Sanità. This ecosystem creates consistent demand for user-friendly prefilled syringes with safety features. Italian pharmaceutical companies like Chiesi Farmaceutici are also investing in local filling capabilities for both glass and polymer formats, enhancing supply chain resilience and supporting domestic innovation in advanced delivery systems.

Spain Prefilled Syringes Market Analysis

Spain's prefilled syringes market growth is likely to grow with the expanding biosimilar adoption and growing home care initiatives in chronic inflammatory diseases. Spain has approved 22 adalimumab biosimilars as of 2024, the highest in Europe, and nearly all are marketed in prefilled syringes to match originator convenience. As per the Ministry of Health, over 850,000 Spanish patients now manage their conditions via home injections supported by regional telehealth platforms that monitor adherence. Additionally, Spain’s warm climate increases the need for stable primary packaging, with glass syringes preferred for their thermal resistance during summer transport. Recent investments in cold chain logistics by pharmacy cooperatives like COFAS have further enabled reliable home delivery.

TOP LEADING PLAYERS IN THE MARKET

- Gerresheimer AG is a Germany-based global leader in pharmaceutical packaging and drug delivery systems with a strong footprint in the European prefilled syringes market. The company supplies both glass and polymer syringes to major biopharmaceutical firms and has pioneered cyclic olefin polymer platforms that address breakage and extractables concerns. In Europe, Gerresheimer leverages its regulatory expertise and local manufacturing sites in Germany, Italy, and Switzerland to ensure supply chain resilience. It also launched a new coated glass syringe with reduced silicone oil migration, specifically designed for high-concentration monoclonal antibodies. These actions reinforce its role as a strategic partner in Europe’s transition toward advanced and patient-centric delivery solutions.

- Schott AG is a German specialty glass technology company and a key enabler of the European prefilled syringes market through its high-quality borosilicate glass tubing and ready-to-fill syringes. The company supplies the majority of European pharmaceutical fill and finish facilities and plays a critical role in ensuring container integrity for sensitive biologics. Schott has invested heavily in expanding its European production network, including a new facility in Switzerland dedicated to syringes with enhanced surface coatings. Schott also collaborates with device integrators to support combination product development. These initiatives solidify its position as a foundational materials provider in Europe’shigh-integrityy drug delivery ecosystem.

- Stevanato Group is an Italian multinational offering integrated capabilities in glass forming, secondary packaging, and visual inspection systems for prefilled syringes. The company has deepened its presence in Europe by supplying syringes to both originator and biosimilar manufacturers with a focus on high precision and sterility assurance. Its proprietary EZ fill platform enables pharmaceutical companies to outsource finished syringe production while maintaining full regulatory control. In 2023, Stevanato inaugurated a new syringe production line in Piombino, Italy, dedicated to safety-integrated formats with passive needleshielding. The company also partnered with a leading Nordic biotech firm to co-develop a polymer syringe for a novel GLP-1 agonist. These strategic moves highlight its commitment to innovation, scalability, and compliance with evolving European safety and sustainability standards.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Key players in the European Prefilled Syringes Market focus on vertical integration by combining primary packaging manufacturing with drug filling and inspection services to offer end-to-end solutions. Companies invest in advanced material science to develop low-interaction glass coatings and break-resistant polymers that meet stringent biologic compatibility requirements. Strategic collaborations with pharmaceutical firms enable co-development of drug-device combinations aligned with regulatory and patient needs. Expansion of European production capacity ensures supply chain security amid global logistics volatility. Firms also prioritize compliance with EU safety directives by integrating passive or active needle protection mechanisms into syringe designs. Additionally, manufacturers engage in early dialogue with the European Medicines Agency to secure scientific advice on novel container closure systems, accelerating market access and reinforcing trust among regulators and payers.

COMPETITIVE LANDSCAPE

The Europe Prefilled Syringes Market features a competitive landscape defined by technological sophistication, regulatory compliance, and strategic alignment with pharmaceutical innovation. Competition is dominated by established European packaging specialists who leverage local manufacturing regulatory familiarity and longstanding relationships with biopharma clients. While global players participate in the market favors firms with regional production facilities due to stringent supply chain expectations and preference for reduced transport emissions. Differentiation centers on material performance, safety integration, and compatibility with withigh-concentrationon or viscous formulations rather than price. Regulatory complexity, particularly around extractables and leachables, and container closure integrity, creates high entry barriers limiting disruption from low-cost manufacturers. The rise of biosimilars and home-based therapies has intensified demand for both conventional and safety syringes, prompting continuous innovation in user experience and sterility assurance. Companies increasingly compete on ecosystem value, offering everything from coated glass barrels to ready-to-fill syringes with full traceability.

KEY MARKET PLAYERS

The key market players that dominate the europe prefilled syringes market are analysed in this report.

- Becton Dickinson and Company

- Gerresheimer AG

- SCHOTT AG

- West Pharmaceutical Services, Inc.

- Ompi,

- Catalent, Inc.

- Weigao Group

- Vetter Pharma International GmbH

- Nipro Corporation

- MedPro Inc.

MARKET SEGMENTATION

This research report on the europe prefilled syringes market has been segmented and sub-segmented into the following categories.

By Material

-

Glass

- Plastic

By Type

- Conventional

- Safety

By Design

- Single-Chamber

- Dual-Chamber

By Application

- Vaccines

- Monoclonal Antibodies

By Distribution Channel

- Hospitals

- Ambulatory Surgical Centres

- Mail-Order Pharmacies

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

1. What is driving growth in the Europe Prefilled Syringes Market?

The Europe Prefilled Syringes Market is driven by rising chronic diseases, expanding biologics and vaccines, preference for self-administration, and

demand for safe, dose-accurate drug delivery that reduces medication errors and hospital workload.

2. How important are vaccines to the Europe Prefilled Syringes Market?

Vaccines hold a major share in the Europe Prefilled Syringes Market because large-scale immunization programs and newer mRNA and recombinant vaccines

require reliable, ready-to-administer formats that ensure sterility, accurate dosing, and rapid deployment.

3. How do biologics and biosimilars influence the Europe Prefilled Syringes Market?

Biologics and biosimilars significantly boost the Europe Prefilled Syringes Market, as high-value injectable therapies benefit from precise dosing,

minimal wastage, and contamination control offered by advanced prefilled syringe and packaging solutions.

4. Which countries lead the Europe Prefilled Syringes Market?

Germany, France, Italy, the UK, and Spain are key contributors to the Europe Prefilled Syringes Market, supported by strong pharma manufacturing,

high healthcare spending, active vaccination programs, and a growing shift toward home-based injectable care

5. What role does home and self-injection play in the Europe Prefilled Syringes Market?

Home and self-injection are central to the Europe Prefilled Syringes Market, as patients managing chronic conditions increasingly use auto-injector

compatible prefilled syringes to avoid hospital visits and simplify long-term treatment adherence.

6. How is technology transforming the Europe Prefilled Syringes Market?

Technology is reshaping the Europe Prefilled Syringes Market via smart, IoT-enabled devices, improved glass and polymer materials, and automated

fill-finish and packaging equipment that enhance safety, quality control, and manufacturing efficiency

7. What are the main challenges in the Europe Prefilled Syringes Market?

The Europe Prefilled Syringes Market faces challenges such as glass breakage risk, extractables and leachables, regulatory compliance, and the need

for designs that balance safety, compatibility with biologics, and cost-effective large-scale production

8. Which end users drive demand in the Europe Prefilled Syringes Market?

Hospitals, clinics, home care settings, and pharmaceutical manufacturers are the main end users in the Europe Prefilled Syringes Market, collectively

driving demand for prefilled formats that streamline workflows and support self-administration.

9. How do regulatory standards impact the Europe Prefilled Syringes Market?

Strict European regulatory standards for drug safety, device performance, and packaging integrity shape product design and approvals in the Europe

Prefilled Syringes Market, encouraging robust quality systems and innovation in safer delivery formats.

10. What is the growth outlook for the Europe Prefilled Syringes Market?

The Europe Prefilled Syringes Market is expected to grow steadily over the next decade, supported by rising biologic use, chronic disease burden,

expanded vaccination, and Europe’s strong position as a leading region in global prefilled syringes.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com