Europe Quartz Market Size, Share, Trends & Growth Forecast Report By Type, By End-User Industry, and By Country (Germany, Italy, France, Spain, United Kingdom & Rest of Europe) – Industry Analysis and Forecast, 2026 to 2034

Europe Quartz Market Size

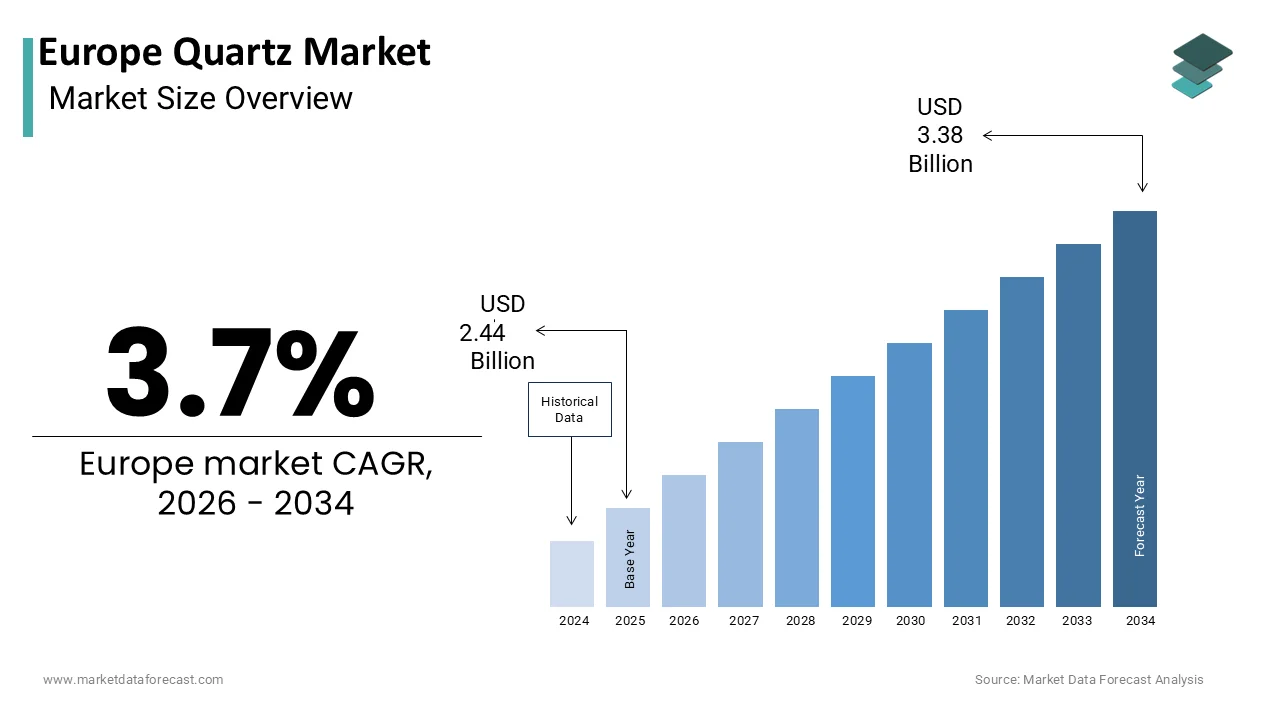

The Europe quartz market was valued at USD 2.44 billion in 2025, is estimated to reach USD 2.53 billion in 2026, and is projected to reach USD 3.38 billion by 2034, growing at a CAGR of 3.7% from 2026 to 2034.

The European quartz market primarily serves the construction, interior design, and high technology industries, with engineered quartz surfaces gaining prominence in residential and commercial spaces. The market is characterized by a shift towards sustainable and durable materials driven by stringent environmental regulations and evolving consumer preferences for low-maintenance aesthetics. The construction sector, which is a primary consumer of quartz products, is forecast to see a production increase of 1.5% in 2026 after a period of stagnation. This recovery provides a foundational boost to the demand for quartz-based building materials. Furthermore, as per the European Union, the new Construction Products Regulation standards in 2026 mandate carbon data declarations, thereby influencing the sourcing and manufacturing processes of quartz products. The market also includes high-purity quartz essential for semiconductor and photovoltaic applications, although this segment faces distinct supply chain dynamics. The integration of quartz into modern architectural designs reflects a broader trend towards premiumization in the European housing market. With renovation activities remaining a key component of the construction landscape, the demand for quartz countertops and flooring continues to exhibit resilience despite economic fluctuations. The interplay between regulatory compliance, aesthetic demand, and industrial utility defines the current operational environment for quartz manufacturers and distributors in the region.

MARKET DRIVERS

Resurgence in Residential Renovation and Remodeling Activities

The revitalization of the residential renovation sector is a pivotal driver for the Europe quartz market due to the material's durability and aesthetic versatility. Homeowners are increasingly prioritizing high-quality interior finishes during remodeling projects, with quartz countertops emerging as a preferred choice over traditional granite or marble. For instance, the global remodeling market is expected to experience significant growth in the coming decade, growing at a compound annual growth rate of 3.8% from 2025. This global trend is mirrored in Europe, where aging housing stock necessitates continuous upgrades and modernization. The demand for low-maintenance and hygienic surfaces in kitchens and bathrooms has significantly boosted the adoption of engineered quartz, which offers superior resistance to stains and scratches. For instance, the Europe quartz kitchen countertops market is anticipated to advance at a compound annual growth rate of 7.98% during the period from 2026 to 2033 and reach a valuation of 14.63 billion USD in 2025. This robust growth trajectory underscores the strong consumer preference for quartz in renovation projects. Additionally, the rise in disposable income among European households has facilitated investment in premium home improvement solutions. The visual appeal of quartz combined with its functional benefits aligns perfectly with the contemporary design trends prevalent in urban European apartments and suburban homes. Consequently, manufacturers are expanding their product portfolios to include diverse colors and patterns that cater to the specific tastes of the renovation market. This sustained demand from the residential sector provides a stable revenue stream for quartz producers and reinforces the material's position as a staple in modern interior design.

Expansion of Commercial Hospitality and Retail Infrastructure

The expansion of the commercial hospitality and retail sectors is further boosting the expansion of the Europe quartz market due to the material's ability to withstand high traffic environments. Hotels, restaurants, and retail outlets are increasingly incorporating quartz surfaces in their designs to project an image of luxury and cleanliness while ensuring long-term durability. The retail and hospitality sectors are significant contributors to the demand for quartz stone table tops in Europe, as these spaces require materials that can endure frequent use without compromising on aesthetic appeal. Quartz offers a seamless and non-porous surface that is easy to clean and maintain, making it ideal for food service areas and customer-facing counters. For instance, the Europe countertop material market is evolving rapidly due to rising renovation rates and the need for sustainable building materials in commercial establishments. The post-pandemic recovery in the tourism and hospitality industry has led to a surge in new hotel openings and restaurant refurbishments across major European cities. This resurgence has directly translated into increased procurement of quartz slabs for lobbies, bars, and dining areas. Furthermore, the retail sector's focus on creating immersive shopping experiences has led to the adoption of customized quartz designs that enhance brand identity. The material's versatility allows for integration with lighting and other architectural elements, providing designers with creative freedom. As commercial real estate developers prioritize sustainability, quartz manufacturers are responding by offering eco-friendly options that meet green building certifications. This alignment with corporate sustainability goals further accelerates the adoption of quartz in commercial projects. The consistent demand from these high-value sectors ensures steady growth for the quartz market, independent of residential cycles.

MARKET RESTRAINTS

Stringent Occupational Health Regulations and Silicosis Concerns

The implementation of stringent occupational health regulations aimed at preventing silicosis is a significant restraint for the Europe quartz market, particularly for engineered stone products. Silicosis is a severe and often fatal lung disease caused by the inhalation of respirable crystalline silica dust, which is generated during the cutting, grinding, and polishing of quartz surfaces. For instance, there has been an increase in silicosis cases linked to the fabrication of engineered quartz, which contains silica. In response, several European countries are considering or have already introduced stricter controls on the processing of these materials. For instance, according to reports from authorities in Spain, there have been numerous cases of silicosis among workers in the artificial stone industry, prompting calls for regulatory intervention. Similarly, as per updates from lawmakers in the United Kingdom, there are renewed pushes to ban high-silica artificial stone to protect workers from this deadly disease. These regulatory pressures can lead to increased operational costs for manufacturers and fabricators who must invest in advanced dust suppression systems and personal protective equipment. In some cases, potential bans on certain types of engineered stone could restrict market access and limit product offerings. As per occupational safety perspectives in Germany, bans are rarely indicated, but strict compliance with safety standards is enforced, which adds to the administrative burden. The negative publicity surrounding silicosis risks can also dampen consumer confidence and lead to a shift towards alternative materials such as porcelain or natural stone with lower silica content. This regulatory landscape creates uncertainty for market participants and may slow down the adoption of engineered quartz in regions with heightened health and safety scrutiny. Consequently, companies must navigate complex compliance requirements while maintaining profitability, which poses a considerable challenge to market growth.

Volatility in Raw Material Supply and Energy Costs

The volatility in raw material supply and escalating energy costs is another substantial restraint for the Europe quartz market, which is affecting production efficiency and profit margins. The manufacturing of engineered quartz requires significant amounts of silica sand, resins, and pigments, along with intensive energy consumption for curing and processing. For instance, Europe faces a scarcity of ultra-pure quartz resources, which demands reliance on imports from external markets, thereby exposing manufacturers to supply chain disruptions and price fluctuations. High-purity quartz manufacturing faces significant challenges from rising energy costs across Europe, which are critical for the purification process. According to trade observations, geopolitical tensions and logistical bottlenecks in global shipping have further exacerbated these issues, leading to cost pressures across the engineered quartz supply chain in 2026. These increased input costs are often passed on to consumers, resulting in higher prices for quartz products, which can dampen demand in price-sensitive segments. Additionally, the dependence on imported raw materials makes the market vulnerable to currency fluctuations and trade policy changes. The European Union's focus on reducing carbon emissions has also led to higher energy prices for industrial users, which is impacting the competitiveness of local quartz producers. For instance, fluctuations in raw material prices can significantly impact the profitability of high-purity quartz sand operations. This economic pressure forces manufacturers to seek alternative sourcing strategies or invest in more efficient production technologies, which require substantial capital expenditure. The combination of supply chain instability and rising operational costs creates a challenging environment for market expansion. Companies must carefully manage their inventory and hedging strategies to mitigate these risks, but the inherent volatility remains a persistent restraint on the market's potential.

MARKET OPPORTUNITIES

Development of Sustainable and Eco-Friendly Quartz Solutions

The development of sustainable and eco-friendly quartz solutions offers a significant opportunity for the Europe quartz market, as consumers and regulators increasingly prioritize environmental responsibility. Manufacturers are innovating to produce quartz surfaces with recycled content and lower carbon footprints, which aligns with the European Union's green deal objectives. The Europe green construction materials and services market is anticipated to advance at a compound annual growth rate of 14.96%, which reflects the strong demand for sustainable options. By incorporating recycled glass and industrial waste into their products, quartz producers can appeal to environmentally conscious buyers and achieve green building certifications. This shift towards sustainability not only enhances brand reputation but also opens up new market segments in public infrastructure and corporate projects that mandate sustainable procurement. For instance, the preference for engineered and recycled quartz stones reflects current shifts toward high-performance materials and environmental responsibility. Furthermore, advancements in manufacturing technologies have enabled the production of quartz with reduced water usage and energy consumption during the curing process. These innovations help manufacturers comply with stringent environmental regulations while reducing operational costs. The availability of eco-friendly quartz options also differentiates products in a competitive market, allowing companies to command premium prices. According to the new Construction Products Regulation, effective in 2026, mandatory carbon data declarations will favor manufacturers with transparent and sustainable supply chains. This regulatory framework incentivizes the adoption of green practices and provides a competitive advantage to early adopters. The opportunity to lead in sustainability positions the quartz market for long-term growth as the construction industry transitions towards a circular economy model.

Integration of Digital Design and Customization Technologies

The integration of digital design and customization technologies presents a major opportunity for the Europe quartz market by enhancing consumer engagement and product differentiation. Advanced digital tools allow customers to visualize quartz surfaces in their own spaces using augmented reality and three-dimensional modeling software. This technological integration simplifies the selection process and reduces the likelihood of post-installation dissatisfaction. As per market analysis, the Europe quartz market is experiencing significant growth because of the rising demand for durable and customizable surfaces. Manufacturers are leveraging digital printing techniques to create intricate patterns and textures that mimic natural stone, wood, or concrete with high fidelity. This level of customization appeals to architects and designers who seek unique solutions for high-end residential and commercial projects. The ability to offer bespoke designs enables quartz producers to capture value in the premium segment of the market. Furthermore, digital platforms facilitate direct interaction between manufacturers and consumers, streamlining the supply chain and reducing lead times. The adoption of Industry 4.0 principles in quartz manufacturing also improves production efficiency and quality control. For instance, the competitive market for quartz in countries like Italy, France, and the Netherlands is fueled by technological advancements and an emphasis on sustainable building materials. These technologies not only enhance the aesthetic appeal of quartz but also improve its functional properties through precise engineering. The opportunity to combine digital innovation with material science allows the quartz market to expand its application boundaries and attract a broader customer base. This technological evolution positions quartz as a modern and versatile material capable of meeting the diverse needs of contemporary design.

MARKET CHALLENGES

Complexity of Regulatory Compliance across Member States

The complexity of regulatory compliance across different European member states is a significant challenge for the Europe quartz market due to varying national standards and enforcement mechanisms. While the European Union provides an overarching framework for construction products and occupational safety, individual countries often implement additional restrictions or interpretations that create a fragmented regulatory landscape. For example, the approach to managing silica dust exposure varies between nations, with some imposing stricter limits on airborne particles than others. This inconsistency requires manufacturers and distributors to adapt their operations and documentation for each market, increasing administrative burdens and costs. For instance, the new Construction Products Regulation took effect in January 2026, imposing mandatory carbon data declarations on natural stone and engineered products. Navigating these evolving regulations requires continuous monitoring and legal expertise, which can be resource-intensive for smaller market players. Additionally, the lack of harmonized testing methods for quartz durability and environmental impact can lead to discrepancies in product certification. This regulatory fragmentation can hinder cross-border trade and limit market access for companies that are unable to meet diverse requirements. The challenge is further compounded by the dynamic nature of environmental policies, which are frequently updated in response to climate goals. As per industry observations, the European construction sector is entering a period of profound structural transformation, which requires constant adaptation. Companies must invest in compliance management systems to ensure adherence to all relevant laws. Failure to comply can result in fines, product recalls, and reputational damage. Thus, the regulatory complexity remains a persistent challenge that requires strategic planning and flexibility from market participants.

Intense Competition from Alternative Surface Materials

The intense competition from alternative surface materials, such as porcelain, ceramic, and compact laminate, is another key challenge for the Europe quartz market. These alternatives offer similar aesthetic and functional benefits, often at lower price points or with perceived environmental advantages. Porcelain slabs, for instance, are gaining popularity due to their thin profile, lightweight nature, and resistance to heat and UV radiation. As per market trends, the Europe countertop material market is evolving rapidly, with consumers exploring various options beyond traditional quartz. The advancement in digital printing technology has enabled porcelain manufacturers to replicate the look of natural stone and quartz with high accuracy, making it a viable substitute. Additionally, compact laminates are being promoted as a more sustainable option due to their lower carbon footprint and recyclability. This competitive pressure forces quartz manufacturers to continuously innovate and justify their premium pricing through superior performance or unique design features. The presence of numerous local and international players in the alternative materials sector further intensifies the competition. For instance, the Europe engineered quartz market faces strategic challenges from substitute products that offer comparable durability and aesthetics. Market share erosion is a constant risk if quartz producers fail to differentiate their offerings effectively. The challenge is particularly acute in the mid-range segment, where price sensitivity is higher. Consumers are increasingly informed and willing to switch brands or materials based on value propositions. Therefore, quartz companies must invest in marketing and education to highlight the distinct advantages of their products. The ability to withstand this competitive pressure is crucial for maintaining growth and profitability in the Europe quartz market.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Type, End-User Industry, and Region. |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, Rest of Europe |

| Market Leaders Profiled | Sibelco Group, Imerys S.A., The Quartz Corporation, Covia Holdings LLC, Momentive Technologies, Heraeus Holding GmbH, Saint-Gobain S.A., Kyocera Corporation, Murata Manufacturing Co., Ltd., Tosoh Corporation, Jiangsu Pacific Quartz Co., Ltd., Russian Quartz LLC |

SEGMENTAL ANALYSIS

By Type Insights

The quartz surface and tile segment commanded the largest share of 64.6% of the European market in 2025. The dominance of quartz surface and tile segment in the European market is attributed to the extensive adoption of engineered quartz in residential and commercial interior design due to its superior aesthetic appeal and durability. The material has become the preferred choice for kitchen countertops, bathroom vanities, and flooring in modern European homes. For instance, the demand for quartz surfaces in the renovation sector has seen significant interest among homeowners in Western Europe during remodeling projects. The non-porous nature of quartz surfaces ensures hygiene and ease of maintenance, which aligns with the post-pandemic health consciousness among consumers. Furthermore, the versatility in design allows manufacturers to replicate the look of marble and granite without the associated maintenance issues. The construction industry's recovery in key markets, such as Germany and France, has further bolstered this segment. According to construction statistics, new housing starts in the European Union have increased, leading to higher procurement of interior finishing materials, including quartz tiles. The segment also benefits from strong distribution networks and brand recognition among interior designers and architects, who specify quartz for high-end projects. The ability to produce large-format slabs with minimal joints has also enhanced its appeal in contemporary architectural designs. This widespread acceptance across various application areas solidifies the leading position of the quartz surface and tile segment in the regional market.

However, the fused quartz crucible segment is anticipated to witness the fastest CAGR of 10.4% over the forecast period, owing to the expanding semiconductor and photovoltaic industries, which rely heavily on high-purity quartz components for crystal growth processes. Fused quartz crucibles are essential for holding molten silicon during the production of monocrystalline and polycrystalline silicon ingots. The increasing demand for solar energy and advanced electronic devices has spurred significant investments in silicon manufacturing capacity across Europe. For instance, the global solar photovoltaic market is expected to grow steadily, which is driving the need for high-quality quartz crucibles. The European Union's strategic initiative to boost local semiconductor production under the European Chips Act has further accelerated this trend. For instance, the act aims to significantly increase the EU's share of global semiconductor production, which will substantially increase the demand for specialized quartz materials. Additionally, advancements in crucible technology, such as larger diameters and higher purity levels, are enabling more efficient silicon production. These technological improvements support the scaling up of manufacturing operations. The scarcity of high-purity quartz raw materials has also led to vertical integration strategies among key players, ensuring stable supply chains. This combination of robust demand from high-growth industries and technological advancements positions the fused quartz crucible segment for exceptional expansion in the coming years.

By End-User Industry Insights

The buildings and construction segment led the market by holding 54.7% of the European market share in 2025. The growth of the building and construction segment in the European market can be credited to the extensive use of quartz surfaces in residential and commercial building projects for countertops, flooring, wall cladding, and decorative elements. The construction industry is a major consumer of engineered quartz due to its durability, aesthetic appeal, and low maintenance characteristics. For instance, the European building sector represents a major portion of material consumption in the region, with renovation activities playing a significant role. The recovery in construction output following recent economic uncertainties has revitalized demand for interior finishing materials. The preference for modern and sleek designs in urban developments has further boosted the adoption of quartz products. For instance, the residential renovation market in Europe maintains a high valuation annually, which provides a substantial base for quartz sales. Commercial projects, such as hotels, offices, and retail spaces, also contribute significantly to this segment due to the need for durable and hygienic surfaces. The integration of quartz in green building projects has also enhanced its appeal among developers seeking sustainable certifications. The widespread availability of quartz products through established distribution channels ensures easy access for contractors and builders. This broad application scope and consistent demand from both new constructions and renovations secure the leading status of the buildings and construction segment in the Europe quartz market.

On the other hand, the electronics and semiconductor segment is anticipated to register a CAGR of 12.4% over the forecast period. The rising demand for high-purity quartz in the manufacturing of semiconductors, optical fibers, and electronic components is driving the growth of the electronics and semiconductor segment in the European market. Quartz is essential for producing crucibles, tubes, and wafers used in silicon processing and chip fabrication. The strategic push by the European Union to strengthen its semiconductor sovereignty has led to significant investments in local production capabilities. As per policy announcements, the European Chips Act aims to mobilize billions in public and private investments to boost chip manufacturing. This initiative is expected to create a robust demand for specialized quartz materials required in fabrication plants. Additionally, the proliferation of fifth-generation telecommunications networks and Internet of Things devices has increased the need for advanced electronic components. These technologies rely on high-performance semiconductors, which in turn depend on high-purity quartz. According to industry forecasts, the European semiconductor market is expected to grow annually, driven by automotive and industrial applications. The transition to electric vehicles and smart manufacturing also contributes to this growth. The requirement for miniaturization and higher efficiency in electronic devices necessitates the use of high-quality quartz substrates. These technological and policy-driven factors position the electronics and semiconductor segment for exceptional expansion in the coming years.

COUNTRY LEVEL ANALYSIS

Germany Quartz Market Analysis

Germany accounted for the leading share of 23.5% of the European market in 2025. The country's dominant position is primarily attributed to its robust construction industry and strong manufacturing base for high-tech applications. Germany is a leader in engineering and industrial production, which drives the demand for both engineered quartz surfaces and high-purity quartz for semiconductor and optical applications. The construction sector in Germany is characterized by a high rate of renovation and modernization of existing buildings. According to statistical data, the German construction industry generated significant revenues in 2024, with a large portion allocated to interior finishing materials. The preference for high-quality and durable materials in German homes and commercial spaces favors the adoption of quartz products. Additionally, Germany is a hub for semiconductor research and production, with several major fabs operating in the country. The government's support for the European Chips Act has led to new investments in semiconductor facilities, which require high-purity quartz components. According to industry reports, Germany accounts for a substantial portion of the European semiconductor equipment market, which indirectly boosts quartz demand. The presence of leading quartz manufacturers and distributors in Germany ensures a well-developed supply chain. The country's focus on sustainability has also encouraged the use of eco-friendly quartz products in green building projects. These factors collectively sustain Germany's leading position in the Europe quartz market.

Italy Quartz Market Analysis

Italy occupied the second-largest share of the European quartz market in 2025. The country is renowned for its design excellence and strong tradition in stone processing, which extends to engineered quartz production. Italy is home to some of the world's leading quartz surface manufacturers who export globally. The domestic market is driven by a strong culture of interior design and renovation. Italian consumers place a high value on aesthetics and quality, which aligns with the premium positioning of quartz products. As per industry data, the Italian stone and ceramic sector, including engineered quartz, reported high export values in 2024, highlighting its global competitiveness. The tourism and hospitality sectors are also significant drivers of demand for quartz surfaces in hotels and restaurants. The restoration of historic buildings often incorporates modern materials like quartz for functional areas while preserving architectural heritage. According to tourism statistics, Italy welcomed a high volume of international tourists in 2024, leading to increased investment in hospitality infrastructure. This influx supports the demand for durable and stylish interior materials. Furthermore, Italy has a growing semiconductor industry, with new fabrication plants planned under the European Chips Act. These developments will increase the demand for high-purity quartz in the coming years. The combination of design leadership, manufacturing strength, and tourism-driven construction sustains Italy's strong market position.

France Quartz Market Analysis

France is estimated to hold a promising share of the European quartz market during the forecast period. The market in France is driven by an active construction sector and a strong emphasis on architectural innovation. Paris and other major cities are undergoing significant urban renewal projects, which incorporate modern materials, including quartz. The French government's initiatives to improve energy efficiency in buildings have led to widespread renovation activities. As per construction reports, the renovation market in France maintains a high annual valuation, providing a steady demand for interior materials. Quartz surfaces are popular in French kitchens and bathrooms due to their elegance and ease of maintenance. The country also has a growing luxury retail and hospitality sector, which uses quartz for high-end interiors. According to retail data, luxury goods sales in France increased in 2024, supporting the demand for premium store fittings. Additionally, France is investing in its semiconductor industry, with plans to expand production capacity. The government's support for technological sovereignty includes funding for chip manufacturing, which will drive demand for high-purity quartz. As per industry announcements, several semiconductor projects are underway in France, supported by European funds. The presence of major quartz distributors and a strong design community further enhances market growth. These factors contribute to France's significant share in the regional quartz market.

Spain Quartz Market Analysis

Spain is predicted to showcase a healthy CAGR in the European quartz market over the forecast period. The Spanish market is characterized by a strong construction industry and a vibrant tourism sector. The country is a major producer of natural stone and has developed a robust engineered quartz manufacturing industry. Spanish quartz brands are well known internationally for their design and quality. Domestically, the demand for quartz is driven by residential construction and renovation. As per housing data, new home sales in Spain increased in 2024, reflecting a recovering property market. The popularity of open plan living and modern kitchens has boosted the adoption of quartz countertops. The tourism industry is a key driver of commercial construction, with hotels and resorts frequently using quartz for its durability and aesthetic appeal. According to tourism statistics, Spain received a massive volume of international visitors in 2024, making it one of the most visited countries in the world. This high volume of tourists necessitates continuous investment in hospitality infrastructure. Additionally, Spain is emerging as a hub for renewable energy production, particularly solar power. The growth in solar panel manufacturing increases the demand for fused quartz crucibles. As per energy reports, Spain aims to significantly increase solar capacity by 2030, supporting the quartz market. These diverse drivers sustain Spain's prominent position in the Europe quartz market.

United Kingdom Quartz Market Analysis

The United Kingdom is expected to exhibit a notable share of the European quartz market over the forecast period. The UK market is driven by a mature construction sector and a strong preference for home improvement. Despite economic challenges, the renovation market remains resilient, with homeowners investing in kitchen and bathroom upgrades. Quartz surfaces are highly popular in the UK due to their durability and wide range of designs. As per construction data, the UK repair, maintenance, and improvement sector reached a high valuation in 2024. The housing stock in the UK is aging, which necessitates regular updates and modernization. The trend towards open plan living has increased the demand for large format quartz slabs for islands and worktops. The commercial sector also contributes to demand, with offices and retail spaces using quartz for interior finishes. The UK has a strong design community that influences material choices in high-end projects. Additionally, the UK is focusing on developing its semiconductor industry, with government support for new fabrication facilities. These initiatives will create future demand for high-purity quartz. According to industry analysis, the UK semiconductor strategy aims to increase domestic production capacity, which will benefit the quartz market. The presence of established distributors and a knowledgeable consumer base supports market growth. These factors maintain the UK's significant share in the Europe quartz market.

COMPETITIVE LANDSCAPE

The competition in the Europe quartz market is characterized by intense rivalry among established multinational corporations and emerging regional players. Market participants compete primarily on product quality, design innovation,n and sustainability credentials. The presence of numerous brands offering similar aesthetic options leads to price sensitivity in certain segments, particularly for standard collections. However, our premium brands differentiate themselves through exclusive designs,gns advanced technologies,gies and superior customer service. The barrier to entry remains moderate due to the capital-intensive nature of manufacturing facilities and the need for established distribution networks. Regulatory compliance regarding environmental standards and occupational health safety adds complexity to operations,s influencing competitive dynamics. Companies are increasingly focusing on circular economy principles to align with European Union policies and consumer preferences. This shift towards sustainability creates opportunities for innovation but also requires significant investment in research and development. Strategic alliances with construction firms and interior designers play a vital role in securing project specifications. The market also faces competition from alternative materials such as porcelain and compact laminate, which offer comparable benefits. Consequently, many manufacturers must continuously innovate and adapt to changing market trends to maintain relevance. The fragmented nature of the market in some regions allows niche players to thrive by catering to specific local preferences. Overall, the competitive landscape is dynamic and driven by technological advancement and regulatory pressures.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the global europe quartz market include

- Sibelco Group

- Imerys S.A.

- The Quartz Corporation

- Covia Holdings LLC

- Momentive Technologies

- Heraeus Holding GmbH

- Saint-Gobain S.A.

- Kyocera Corporation

- Murata Manufacturing Co., Ltd.

- Tosoh Corporation

- Jiangsu Pacific Quartz Co., Ltd.

- Russian Quartz LLC

TOP LEADING PLAYERS IN THE MARKET

- Cosentino Group stands as a pivotal entity in the Europe quartz market,t renowned for its Silestone brand, nd which has become synonymous with high-quality engineered stone surfaces. The company operates extensive production facilities across Spain and maintains a robust global distribution network that ensures widespread availability of its products. Cosentino actively invests in sustainable manufacturing practices, including water recycling systems and renewable energy usage, to align with European environmental standards. Recent strategic initiatives include the launch of new collections featuring recycled materials and advanced antimicrobial technologies. These innovations cater to the growing consumer demand for hygienic and eco-friendly interior solutions. The company also focuses on digital tools for designers and architects to enhance customer engagement and streamline the selection process. By prioritizing sustainability and design excellence, Cosentino strengthens its brand loyalty and competitive edge in the premium segment of the market while expanding its footprint in emerging economies through targeted marketing campaigns and partnerships with local distributors.

- Caesarstone Ltd. is a leading innovator in the engineered quartz surface industry with a significant presence in the European market. The company is celebrated for its pioneering role in developing quartz surfaces and continues to drive innovation through extensive research and development efforts. Caesarstone offers a diverse portfolio of colors and textures that mimic natural stone while providing superior durability and low maintenance benefits. In recent years, the company has focused on enhancing its supply chain efficiency and expanding its production capacity to meet rising global demand. Strategic collaborations with prominent architects and interior designers have helped Caesarstone maintain its reputation for aesthetic excellence. The company has also implemented stringent quality control measures to ensure consistent product performance. Caesarstone actively promotes sustainability by incorporating recycled content into its products and reducing carbon emissions during manufacturing. These efforts resonate with environmentally conscious consumers and regulatory bodies in Europe. By leveraging its brand heritage and commitment to innovation,n Caesarstone solidifies its position as a preferred choice for residential and commercial projects worldwide.

- Compac Superficies is a distinguished manufacturer of engineered quartz surfaces based in Spain with a strong influence on the Europe quartz market. The company is recognized for its technological advancements and commitment to producing high-performance materials that meet the rigorous demands of modern architecture. Compac utilizes proprietary technology to create surfaces with exceptional resistance to stains,s scratches, es and heat. The company has recently expanded its product range to include ultra compact surfaces and large format sla, bs which are ideal for both indoor and outdoor applications. Compac places a strong emphasis on sustainability by implementing circular economy principles in its production processes. This includes the use of recycled materials and the reduction of waste generation. The company also engages in continuous improvement of its manufacturing efficiency to minimize environmental impact. Compac collaborates with international design studios to create exclusive collections that reflect contemporary trends. These strategic moves enhance its appeal to discerning customers and professionals. By focusing on innovation and sustainability, Compac reinforces its leadership in the engineered stone sector and contributes significantly to the global market dynamics.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Key players in the Europe quartz market primarily employ product innovation and sustainability initiatives to maintain a competitive advantage. Companies invest heavily in research and development to create unique designs and enhanced functional properties such as antimicrobial surfaces and improved durability. This differentiation strategy appeals to discerning consumers seeking premium aesthetics and performance. Another major strategy involves vertical integration, where manufacturers control the supply chain from raw material sourcing to distribution. This approach ensures quality consistency and cost efficiency while mitigating supply chain risks. Strategic partnerships with architects, designers, and builders are crucial for market penetration and brand visibility. These collaborations facilitate the specification of quartz products in high-profile projects. Expansion into digital platforms enables companies to reach broader audiences through virtual showrooms and design tools. Sustainability is increasingly central to corporate strategies, with firms adopting eco-friendly manufacturing processes and recycled content. Compliance with stringent European environmental regulations drives these green initiatives. Additionally, companies focus on geographic expansion by establishing local production facilities or distribution centers to reduce logistics costs and improve service delivery. These multifaceted strategies collectively strengthen market positions and long-term growth in the competitive landscape.

MARKET SEGMENTATION

This research report on the europe quartz market is segmented and sub-segmented into the following categories.

By Type

- Quartz Surface and Tile

- Fused Quartz Crucibles

- Quartz Glass

- Other Quartz Products

By End-User Industry

- Building and Construction

- Electronics and Semiconductor

- Solar Energy

- Optical and Lighting

- Other Industries

By Country

- Germany

- Italy

- France

- Spain

- United Kingdom

- Rest of Europe

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com