Europe Recycled Carbon Fiber Market Size, Share, Trends & Growth Forecast Report – Segmented By Type (Milled, Chopped), Source, Manufacturing Process, End-use Industry, and Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic & Rest of Europe), Industry Analysis From 2025 to 2033

Europe Recycled Carbon Fiber Market Size

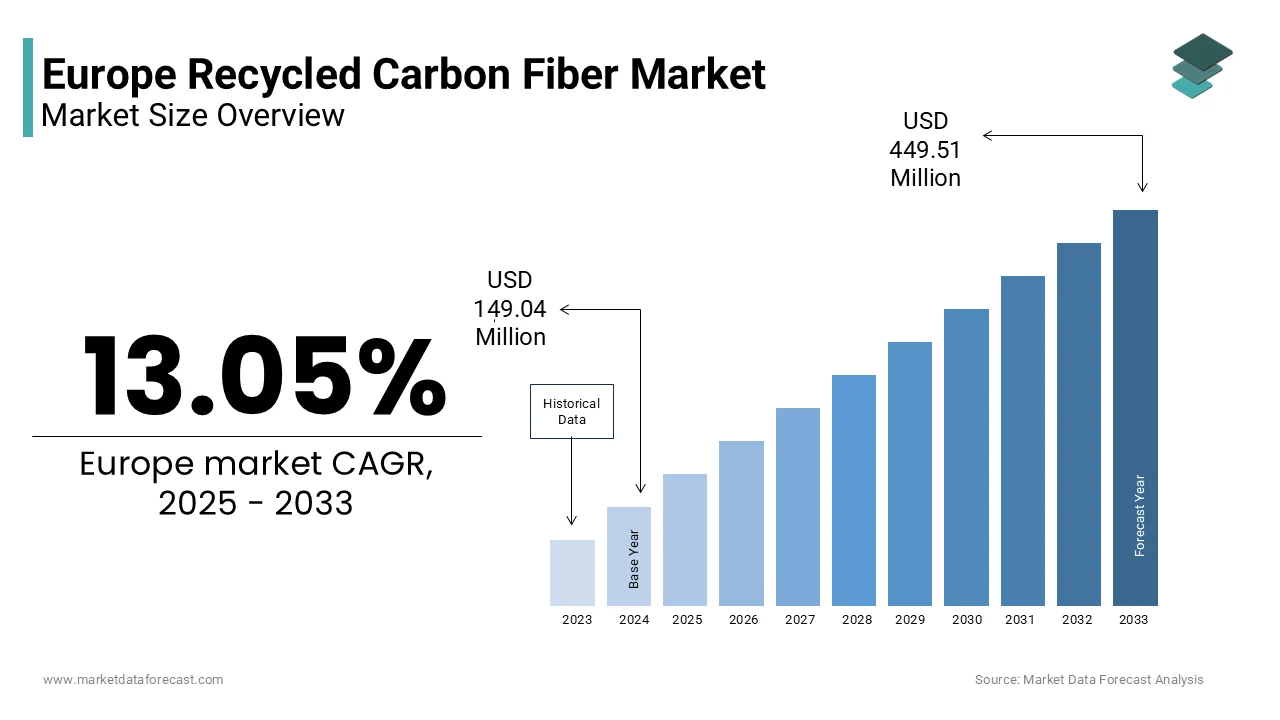

The Europe recycled carbon fiber market size was valued at USD 149.04 million in 2024 and is projected to reach USD 449.51 million by 2033 from USD 168.49 million in 2025, growing at a CAGR of 13.05%.

The recycled carbon fiber is recovered carbon fiber materials derived primarily from thermoset composite scrap, such as aerospace offcuts and end-of-life wind turbine blades, which are processed through pyrolysis or solvolysis to yield reusable fibers with retained mechanical properties. The European Environment Agency emphasises that recycling one kilogram of carbonfibrer saves approximately 150 megajoules of energy, compared to a virgin product,, ion equivalent to avoiding 35 kilograms of CO₂ emissions. Regulatory frameworks such as the EU Circular Economy Action Plan and the End-of-Life Vehicles Directive increasingly mandate material recovery and restrict landfilling of composite waste. Under the European Green Deal, the European Chemicals Agency is also reviewing resin formulations to enhance future recyclability.

MARKET DRIVERS

Stringent EU Circular Economy and Landfill Diversion Mandates

The European Union’s regulatory push to minimise industrial waste and promote material circularity is a primary driver for the growth of Europe's recycled carbonfibrer market. In parallel, the EU Circular Economy Action Plan identifies carbon fiber reinforced polymers as a priority stream for circular innovation. Germany’s Circular Economy Act and France’s Anti Waste Law impose escalating landfill taxes reaching 85 euros per ton in 2024 by making disposal economically unviable for manufacturers. Companies like Airbus and Vestas are contractually obligated to manage end-of-life composites, creating guaranteed feedstock streams for recyclers. This regulatory ecosystem transforms waste from a liability into a resource, directly fueling investment in recycling infrastructure and market development for recovered fibers.

Growing Demand for Lightweight Sustainable Materials in Automotive and Consumer Goods

The European automotive and industrial manufacturers are increasingly integrating recycled carbon fiber into components to meet corporate decarbonization targets and consumer sustainability expectations. The growing demand for lightweight, sustainable materials in automotive and consumer goods is an additional factor prompting the growth of the European recycled carbon fiber market. BMW’s iVision Circular concept car, for instance, uses 100% recycled carbon fiber in its cabin structure, showcasing feasibility at scale. Additionally, the European Battery Regulation requires battery enclosures to incorporate recyclable materials by 2027, further expanding the addressable market.

MARKET RESTRAINTS

Inconsistent Fiber Quality and Limited Standardization Across Recycling Processes

The performance variability of recycled carbon fiber is a technical barrier to widespread adoption in high-integrity applications. The inconsistent fiber quality and limited standardisation across the recycling process are restricting the growth of the European recycled carbon market. Unlike virgin carbon fiber, which adheres to ISO 10119 standards for modulus and tensile properties, recycled fiber lacks harmonised certification across the EU. The European Committee for Standardisation has initiated work on EN specifications for recycled carbon fiber, but no binding standards exist as of 2024. Consequently, aerospace and structural automotive applications remain inaccessible despite strong sustainability incentives.

Limited and Fragmented Collection Infrastructure for End-of-Life Composite Waste

The absence of a coordinated and economically viable collection system for carbon fiber reinforced polymer waste severely constrains feedstock availability, which is additionally to hamper the growth of the European recycled carbon fiber market. According to the European Environment Agency, fewer than 12 specialised composite recycling facilities operate in the EU, with most concentrated in Germany, the UK and Sweden. Aerospace scrap is better managed but often exported outside the EU for recycling due to higher processing costs domestically.

MARKET OPPORTUNITIES

Integration into Wind Energy Blade Circular Economy Initiatives

The decommissioning of first-generation wind turbines is amplifying the growth of Europe's recycled carbon fiber market. According to the European Wind Energy Association, over 25,000 metric tons of carbon fiber reinforced blades will reach the end of life annually by 2030 as early installations from the 2000s retire. Companies like Siemens Gamesa and Vestas have committed to 100% recyclable blade designs by 2030 and are partnering with recyclers such as ELG Carbon Fibre and CFK Valley to establish closed-loop systems. The recovered fibers are already being reused in injection-moulded automotive parts and construction profiles.

Advancement of Solvolysis and Emerging Recycling Technologies

Next-generation chemical recycling methods like solvolysis and fluidised bed processing are unlocking higher quality and more consistent recycled carbon fiber, expanding its applicability. The advancement of solvolysis and emerging recycling technologies is another attribute prompting the growth of the European recycled carbon fiber market. As per the Joint Research Centre, solvolysis preserves up to 95% of the original fiber tensile strength and enables clean resin recovery. European innovators are leading this shift with the UK-based company Bcomp and Germany’s CFK Valley piloting commercial solvolysis lines under EU Innovation Fund grants. These advanced processes also align with REACH regulations by avoiding hazardous emissions associated with thermal methods.

MARKET CHALLENGES

High Processing Costs and Unfavorable Economics Relative to Virgin Fiber

Recycled carbon fiber remains approximately 20 to 30% more expensive than standard virgin carbon fiber on a per kilogram basis for equivalent performance grades is a barrier for the growth of the Europe recycled carbon fiber market. Virgin fiber prices have also declined due to scale from global producers like Toray and SGL, while recycled fiber lacks similar economies of scale. Public procurement rules rarely mandate recycled carbon fiber, unlike metals or plastics, limiting demand pull.

Lack of Downstream Market Acceptance in High-Value Engineering Applications

The recycled carbon fiber continues from engineers and certification bodies in performance sectors is challenging the growth of the European recycled carbon fiber market. As per the European Aviation Safety Agency, no commercial aircraft currently uses recycled carbon fiber in primary or secondary structures due to unresolved questions around fatigue life impact resistance and long-term durability. Similarly, the European Automotive Certification Body does not recognise recycled carbon fiber in crash-relevant components without extensive and costly validation testing. OEMs also worry about supply continuity. Recycled fiber production is still batch based and not yet available in continuous tow formats required for automated fiber placement.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| CAGR | 13.05% |

| Segments Covered | By Type, Source, Manufacturing Process, End Use Industry, and Region |

| Various Analyses Covered | Global, Regional, & Country Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, and the Czech Republic |

| Market Leaders Profiled | ELG Carbon Fibre Ltd (UK), SGL Carbon (Germany), Procotex Corporation SA (Belgium), Gen 2 Carbon Limited (UK), Fairmat (France), carboNXT GmbH (Germany), CFK Valley Stade Recycling GmbH & Co. KG (Germany), and Extracthive (Europe) |

SEGMENTAL ANALYSIS

By Type Insights

The chopped recycled carbon fiber segment held a significant share of the European recycled carbon fiber market in 2024, with its compatibility with high-volume thermoplastic processing techniques such as injection moulding and compression moulding, which are widely used in automotive and consumer goods manufacturing. Chopped fibers typically range from 3 to 12 millimetres in length offering a balance between mechanical reinforcement and processability in polymer matrices like polyamide and polypropylene. Additionally, chopped fiber production is more energy efficient than milled variants as it avoids intensive grinding steps that degrade fiber strength. Major recyclers, including ELG Carbon Fibre and CFK Valle, operate dedicated chopping lines integrated with pyrolysis plants, ensuring consistent length distribution.

The milled segment is expected to grow at the fastest CAGR of 11.2% throughout the forecast period, with its unique role as a functional additive in high-performance coatings, adhesives and 3D printing filament, where micron-scale particles enhance conductivity, stiffness and thermal stability. The European Coatings Federation notes that demand for conductive automotive primers using milled carbon fiber increased by 34% in 2023 as electric vehicle manufacturers seek electromagnetic interference shielding for battery enclosures without adding metal weight. Furthermore, milled fiber is increasingly used in syntactic foams for marine buoyancy modules where its low density and compressive strength outperform traditional glass microspheres. The European Commission’s Horizon Europe program has funded three pilot projects since 2022 to optimise milling parameters for consistent particle morphology.

By End Use Industry Insights

The automotive and transportation segment held 47.3% of the European recycled carbon fiber market share in 2024, with the stringent EU vehicle CO₂ emission targets and corporate sustainability mandates that drive lightweighting with circular materials. BMW, Mercedes-Benz Benz and Stellantis have all integrated recycled carbon fiber into interior and underbody components, with BMW’s i series using over 120 kilograms per vehicle in non-structural parts. Commercial vehicle manufacturers like Daimler Truck are also adopting the material for cab panels and fairings to improve fuel efficiency. Additionally, the End of Life Vehicles Directive’s 95% recovery target creates a future circular loop as today’s vehicles become tomorrow’s feedstock.

The industrial applications segment is expected to grow at the fastest CAGR of 13.5% throughout the forecast period, with the high-performance composite components in machinery, robotics and renewable energy infrastructure. As per the European Robotics Association, 38% of collaborative robot arms now incorporate recycled carbon fiber reinforced polymers in joints and housings to reduce inertia and improve energy efficiency. Additionally, the EU’s Critical Raw Materials Act encourages the substitution of imported carbon fiber with domestic recycled content in industrial equipment.

REGIONAL ANALYSIS

Germany Market Analysis

Germany was the top performer of the European recycled carbon fiber market by holding 28.3% of the share in 2024, with its advanced automotive industry, strong recycling infrastructure, and proactive circular economy policies. Over 90% of Germany’s premium automakers, including BMW, Mercedes-Benz Benz and Audi, have contractual agreements with recyclers like CFK Valley and SGL Carbon for closed-loop fiber recovery. The German government’s Circular Economy Act mandates industrial waste recycling rates of 70% by 2025 accelerating investment in pyrolysis and solvolysis facilities. Germany also hosts Europe’s most developed composite scrap collection network with over 45 certified take-back points for aerospace and automotive offcuts. The Fraunhofer Institute for Chemical Technology operates pilot lines for advanced recycling and provides third-party validation of fiber properties, enhancing market trust.

United Kingdom Market Analysis

The United Kingdom recycled carbon fiber market held 19.2% of the share in 2024, with EU environmental standards and continues to lead in aerospace recycling and advanced manufacturing. Companies like BAE Systems and Rolls-Royce partner with UK-based recyclers such as Adesso and ELG Carbon Fibre to recover aerospace scrap under the Sustainable Aviation Strategy. The UK also hosts Europe’s first commercial solvolysis plant operated by Bcomp in collaboration with the University of Nottingham, enabling high-quality fibre recovery from epoxy matrices. Furthermore, Innovate UK has funded 12 projects since 2022 focused on recycled carbon fiber applications in wind energy and construction.

France Market Analysis

France's recycled carbon fiber market growth is likely to grow with its aerospace leadership and national circular economy commitments. Airbus’s facilities in Toulouse and Saint Nazaire generate significant carbon fiber scrap, which is processed domestically through partnerships with recyclers like Carbios and Valdelia. The French Anti Waste Law prohibits landfilling of industrial composites and requires producers to finance end-of-life management, creating stable feedstock streams. Additionally, the automotive industry, led by Stellantis and Renault, is integrating recycled fibre into electric vehicle platforms under the France 2030 investment plan, which allocated 1.2 billion euros to sustainable mobility materials.

Italy Market Analysis

Italy's recycled carbon fiber market growth is likely to grow with the speciality automotive and luxury goods sectors, where lightweight high-performance materials enhance product value. Companies like Ferrari, Lamborghini and Ducati use recycled carbon fiber in non-structural interior and body components under their sustainability charters. Italy also leads in consumer applications with high-end fashion and eyewear brands such as Luxottica, incorporating recycled fiber into frames and accessories to meet EU green labelling requirements. The National Recovery and Resilience Plan allocated 200 million euros to advanced materials innovation, including composite recycling infrastructure in Emilia Romagna and Lombardy.

COMPETITIVE LANDSCAPE

KEY MARKET PLAYERS

Some of the notable key players in the European recycled carbon fibre market are

- ELG Carbon Fibre Ltd (UK)

- SGL Carbon (Germany)

- Procotex Corporation SA (Belgium)

- Gen 2 Carbon Limited (UK)

- Fairmat (France)

- carboNXT GmbH (Germany)

- CFK Valley Stade Recycling GmbH & Co. KG (Germany)

- Extracthive (Europe)

TOP STRATEGIES USED BY THE KEY MARKET PLAYERS

Key players in the European recycled carbon fiber market focus on securing stable feedstock through partnerships with aerospace, automotive and wind energy OEMs to establish closed-loop take-back systems. Companies invest in advanced recycling technologies such as solvolysis and fluidised bed processing to improve fiber quality and expand into higher value applications. Strategic collaborations with research institutes and certification bodies aim to develop standardised testing protocols and design allowables to build engineering confidence. Product diversification into milled, chopped, and continuous formats enables penetration across injection moulding, 3D printing and compression moulding segments. Additionally, firms pursue environmental validation through life cycle assessments and compliance with EU green labelling schemes to meet corporate sustainability procurement requirements.

COMPETITION OVERVIEW

The European recycled carbon fiber market features a nascent yet intensifying competitive landscape defined by technological differentiation, feedstock access and regulatory alignment rather than price competition. A handful of specialised recyclers dominate the space, supported by strong ties to aerospace and automotive OEMs who act as both waste suppliers and end users. Competitioncentress on fiber consistency, process scalability, and certification for semi-structured applications where virgin fiber still prevails. The market is highly innovation-driven with players racing to commercialise solvolysis and other chemical recycling methods that preserve fibre properties better than traditional pyrolysis. National circular economy policies create uneven advantages, with German, UK and French companies benefiting from supportive grants and waste regulations. Barriers to entry remain high due to capital intensity, regulatory compliance and the need for long-term offtake agreements.

TOP PLAYERS IN THE MARKET

- ELG Carbon Fibre Ltd is a UK-based global pioneer in carbon fiber recycling and a key player in the European recycled carbon fiber market. The company operates the world’s first large-scale commercial carbon fiber recycling facility in Coseley, England, utilising pyrolysis to recover high-quality fibres from aerospace and industrial scrap. ELG supplies milled and chopped recycled carbon fiber to automotive consumer goods and industrial clients across Europe and North America. To strengthen its position, the company has partnered with major aerospace OEMs including Boeing and GKN Aerospace,ce to establish closed-loop take-back systems.

- CFK Valley Stade Recycling is a Germany-based leader in recycled carbon fiber innovation operating within the broader CFK Valley ecosystem that connects industry research and government stakeholders. The company specialises in recovering carbon fiber from aerospace prepeg offcuts and end-of-life components using both pyrolysis and emerging solvolysis techniques. It supplies tailored fiber formats to automotive and industrial customers seeking circular material solutions. CFK Valley has reinforced its market presence by collaborating with the German Aerospace Centre and Fraunhofer Institutes to develop standardised testing protocols for recycled fiber performance.

- SGL Carbon SE is a German multinational with a strategic focus on sustainable carbon materials, including recycled carbon fiber for automotive and industrial applications. The company integrates recycled fiber into its SIGRAFIL portfolio, offering compound solutions for injection moulding and extrusion processes. SGL works closely with premium automakers like BMW and Mercedes-Benz to develop lightweight interior and underbody parts that meet both mechanical and circularity requirements. To enhance its recycling capabilities, SGL has invested in digital material passports and traceability systems aligned with EU battery and vehicle regulations.

MARKET SEGMENTATION

This research report on the Europe recycled carbon fiber market has been segmented and sub-segmented based on categories.

By Type

- Chopped

- Milled

By Source

- Automotive Scrap

- Aerospace Scrap

- Other Sources

By Manufacturing Process

- Mechanical

- Thermal

- Chemical

By End-Use Industry

- Automotive & Transportation

- Consumer Goods

- Sporting Goods

- Industrial

- Aerospace & Defense

- Marine

- Other End-use Industries

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

1. What is the Europe recycled carbon fiber market?

The Europe recycled carbon fiber market focuses on producing carbon fibers recovered from waste composites through processes like pyrolysis and solvolysis for reuse in various industries.

2. What is driving the growth of recycled carbon fiber in Europe?

Growth is driven by sustainability policies, rising carbon fiber waste, automotive lightweighting demand, and increasing adoption of circular economy practices.

3. Which industries widely use recycled carbon fiber in Europe?

Key users include automotive, aerospace, construction, consumer electronics, sports equipment, and renewable energy sectors.

4. What are the main benefits of recycled carbon fiber?

It offers high strength-to-weight ratio, lower material cost, reduced environmental impact, and suitability for lightweight applications.

5. Which countries in Europe lead the recycled carbon fiber market?

Germany, the UK, France, and Italy are among the top contributors due to strong industrial and automotive bases.

6. What recycling technologies are used for carbon fiber in Europe?

Common technologies include pyrolysis, solvolysis, mechanical recycling, and fluidized bed processes.

7. What challenges does the Europe recycled carbon fiber market face?

Challenges include high recycling costs, quality variations, limited large-scale production, and lack of standardized regulations.

8. Which segment accounts for the largest demand for recycled carbon fiber?

The automotive sector accounts for the largest demand due to lightweighting initiatives and emission reduction goals.

9. Is recycled carbon fiber as strong as virgin carbon fiber?

Recycled carbon fiber retains 90–95% of its mechanical properties, making it suitable for many structural and non-structural applications.

10. How does government regulation impact the market?

Strict EU sustainability regulations and waste management policies boost adoption of carbon fiber recycling solutions.

11. What forms of recycled carbon fiber are available in Europe?

Products include milled fibers, chopped fibers, non-woven mats, and pellets for compounding.

12. What is the future outlook for the Europe recycled carbon fiber market?

The market is expected to grow steadily due to rising sustainability goals, increasing composite waste, and expanding adoption across automotive, aerospace, and construction industries.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com