Europe Rigid Plastic Packaging Market Size, Share, Trends & Growth Forecast Report, Segmented By Product Type (Bottles and Jars, Trays and Containers, Caps and Closures, Intermediate Bulk Containers), Material, End Use Industry And Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic & Rest Of Europe) - Industry Analysis From (2025 To 2033)

Europe Rigid Plastic Packaging Market Size

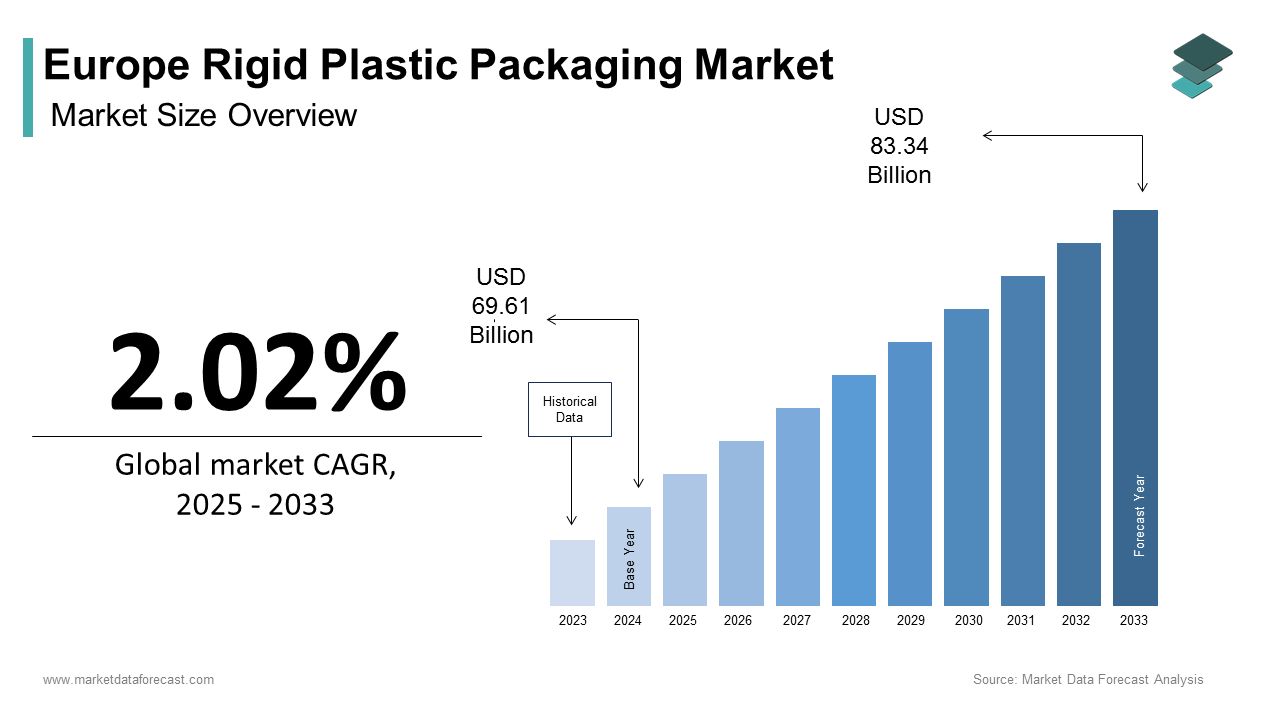

The Europe rigid plastic packaging market size was calculated at USD 69.61 billion in 2024 and is anticipated to reach USD 83.34 billion by 2033, from USD 71.02 billion in 2025, growing at a CAGR of 2.02% during the forecast period.

The rigid plastic packaging is non-flexible containers and closures made from polymers such as polyethylene terephthalate (PET), high-density polyethylene (HDPE), polypropylene (PP), and polystyrene (PS), used for food, beverages, pharmaceuticals, personal care, and household products. These packages maintain structural integrity under handling and storage, offering barrier protection, transparency, and design versatility. According to the European Environment Agency, over 14 million metric tons of rigid plastic packaging enter the EU waste stream annually, with packaging accounting for nearly 40% of total plastic consumption in the region.

MARKET DRIVERS

Mandatory Recycled Content Requirements Accelerate Circular Material Adoption

The European Union’s binding targets for post-consumer recycled content are fundamentally reshaping material sourcing and design in rigid plastic packaging, which is a major factor prompting the growth of Europe's rigid packaging market. According to the European Commission’s Packaging and Packaging Waste Regulation, all PET beverage bottles must contain at least 30% recycled content by 2030, rising to 65% by 2040. Beverage giants like Coca-Cola Europacific Partners now use 100% rPET in bottles across Sweden and Finland, as verified by national environmental agencies. The result is a structural shift from virgin to circular polymers, not driven by consumer preference alone but by legal obligation, which is making recycled content a baseline requirement rather than a premium differentiator in the rigid packaging value chain.

Growth of E Commerce and Premiumization Demand Enhanced Protective and Aesthetic Packaging

The expansion of online retail and rising consumer expectations for product presentation are escalating the growth of the Europe rigid plastic packaging market. In the food sector, ready-to-eat meal kits rely on thermoformed PP trays with secure lidding to maintain freshness and microwave safety. As per GfK’s 2024 Home Care Tracker, some European shoppers associate opaque or textured rigid containers with higher product efficacy, particularly in skincare and detergents. Additionally, the shift toward single-serve and portion-controlled formats in urban households favors rigid containers for their precision and resealability. This integration of logistics necessity and sensory branding elevates rigid plastic from mere containment to a strategic touchpoint in the digital and physical consumer journey.

MARKET RESTRAINTS

Strict Single-Use Plastic Bans Eliminate Key Product Categories and Disrupt Legacy Designs

The EU Single Use Plastics Directive has removed entire segments of rigid packaging with significant reformulation and redesign pressures for manufacturers, which is expected to hamper the growth of the Europe rigid plastic packaging market. According to the European Commission, food containers made of expanded polystyrene (EPS), commonly used for takeaway meals, are prohibited as of 2024, with non-compliant products barred from sale across all member states. Similarly, rigid PP and PS cutlery, stirrers, and balloon sticks are banned regardless of recyclability. Companies that failed to anticipate these changes faced inventory write-offs and supply chain delays. This regulatory pruning eliminates low-value, high-waste formats but compels innovation in compliant rigid designs that balance functionality with environmental responsibility.

Inconsistent National Recycling Infrastructure Undermines Collection and Reuse Targets

The EU packaging laws effectiveness of rigid plastic recovery varies dramatically across member states due to fragmented waste management systems. The inconsistent national recycling infrastructure undermines collection and reuse targets, which is also hindering the growth of the European rigid plastic packaging market. In Southern Europe, contamination rates in collected streams often exceed 25% due to inadequate rinsing and mixed material disposal, by reduces the yield of food-grade rPET. Producers face a paradox where they are mandated to use recycled content but cannot reliably source sufficient high-quality material. This infrastructure gap threatens the feasibility of EU recycling targets and increases compliance costs for multinationals operating across diverse national landscapes.

MARKET OPPORTUNITIES

Innovation in Mono Material Rigid Packaging Enhances Recyclability and Brand Compliance

The packaging designers are increasingly shifting to mono-material rigid structures to overcome the recyclability limitations of multi-layer composites. This factor is solely to create new opportunities for the growth of Europe's rigid plastic packaging market. According to the European Organisation for Packaging and the Environment, new rigid packaging launches in 2024 will use single polymer systems such as all PP or all PET instead of traditional combinations like PET/PE or PS/Aluminum. Amcor introduced a 100% PP yogurt pot with an integrated sealant layer that passes recyclability tests in existing streams as verified by PRE’s RecyClass certification. Alpla developed a mono PET bottle for liquid detergents that replaces HDPE triggers with molded PET alternatives. As per CEFLEX guidelines, mono-material designs increase recovery rates by up to 35% compared to laminated formats. Retailers like Carrefour and Tesco now prioritize mono-material SKUs in private label ranges to meet their own sustainability pledges.

Expansion of Reusable Rigid Packaging Systems Supported by EU Policy and Retail Pilots

The reusable rigid containers are gaining traction as a viable alternative to single-use models under the EU’s push for packaging reuse, which is aimed at bolstering the growth of Europe's rigid plastic packaging market. According to the European Commission’s 2024 Reuse Roadmap, member states must implement systems for beverages, food, and takeaway by 2026 with binding targets for 2030. Similarly, Loop by TerraCycle partners with Carrefour in France and Kroger in the Netherlands to offer premium products in durable PP tubs collected, cleaned and refilled. Major brands, including Nestlé and Danone, are investing in returnable bottle infrastructure to comply with upcoming mandates.

MARKET CHALLENGES

Food Grade Recycled Resin Shortages Constrain Compliance with Regulatory Mandates

The shortfall in food-grade recycled polymers like rPET and rPP suitable for direct food contact is a challenge for the growth of Europe's rigid plastic packaging market. According to the European Food Safety Authority, only 12 recycling facilities in the EU held approval for producing food-compliant rPET in 2024, with total capacity capped at 650000 metric tons annually. This gap forces brands to rely on mass balance or imported resins, which lack traceability and face scrutiny under the EU Green Claims Directive. Mechanical recycling alone cannot meet demand due to degradation after multiple cycles, prompting investment in advanced methods like depolymerization.

Consumer Misperceptions About Plastic Recyclability Hinder Behavioral Change and Sorting Accuracy

The public confusion over which rigid plastic packages are truly recyclable continues to contaminate waste streams and reduce recovery efficiency is additionally degrading the growth of Europe's rigid plastic packaging market. According to a 2024 Eurobarometer survey, EU citizens believe all plastic packaging placed in recycling bins is automatically recycled regardless of type or cleanliness. Only PET bottles and HDPE containers achieve consistent recycling rates, while colored PP tubs and black PS trays are often rejected due to sorting limitations. This misconception is exacerbated by inconsistent labeling, such as the “chasing arrows” symbol, which implies recyclability even for non-collected formats.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| CAGR | 2.02% |

| Segments Covered | By Product Type, Material, End Use Industry, and Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, and the Czech Republic |

| Market Leaders Profiled | Amcor plc, Berry Global Inc., ALPLA Group, RPC Group (Berry Global), Sonoco Products Company, Silgan Holdings, Greiner Packaging, DS Smith Plastics, Plastipak Holdings, Paccor, Huhtamaki, Coveris, AptarGroup |

SEGMENTAL ANALYSIS

By Product Type Insights

The bottles and jars segment accounted in holding 42.3% of the Europe rigid plastic packaging market share in 2024 due to their universal application across beverages, food, personal care, and pharmaceuticals, where product visibility, dosage control, and barrier protection are essential. According to a recent survey, over 85 billion plastic bottles are placed on the EU market annually, with PET accounting for 78% of beverage containers. The European Commission’s Single Use Plastics Directive has accelerated the adoption of refillable and recycled content bottles, with Germany and Sweden achieving collection rates above 90% through deposit return systems as verified by national environmental agencies. Additionally, the rise of functional beverages such as protein shakes and plant-based milks relies on HDPE and PP bottles with resealable caps for on-the-go consumption. This combination of regulatory alignment, consumer familiarity, and functional versatility ensures bottles and jars remain the cornerstone of rigid packaging in Europe.

The caps and closures segment is anticipated to grow with a significant CAGR of 8.6% during the forecast period, with the innovations in child safety, tamper evidence, and dispensing functionality across healthcare and household sectors. Beverage brands like Coca-Cola and PepsiCo have rolled out tethered HDPE closures across all EU markets, with over 20 billion units deployed annually. The integration of recycled content into closures now exceeds 50% in leading brands, which further aligns with circular economy goals.

By Material Insights

The Polyethylene terephthalate (PET) segment was the largest by holding a significant share of the Europe rigid plastic packaging market in 2024 due to its exceptional clarity, strength-to-weight ratio, and established recycling infrastructure. The material’s gas barrier properties make it ideal for carbonated drinks, juices, and edible oils, preserving shelf life without secondary packaging. Advanced recycling technologies such as enzymatic depolymerization are further enhancing food-grade rPET supply with Carbios' commissioning of Europe’s first industrial-scale plant in France in 2024.

The polypropylene segment is likely to grow with an anticipated CAGR of 6.7% in next coming years with its versatility in food containers, healthcare packaging, and reusable systems. According to the European Food Safety Authority, over 40 new PP recycling facilities received food contact approval in 2024, enabling broader use of rPP in yogurt pots, ready meal trays, and medicine bottles. Additionally, the EU’s push for mono-material packaging has elevated PP as a replacement for multi-layer composites in dairy and sauces.

By End-User Industry Insights

The food industry segment held 38.2% of the Europe rigid plastic packaging market share in 2024 due to stringent hygiene requirements, portion control demands, and the need for extended shelf life in perishable categories. According to the European Food Safety Authority, over fresh meat, poultry, and ready-to-eat meals are packaged in rigid PP or PET trays with modified atmosphere technology to inhibit microbial growth. Supermarkets across the EU now mandate recyclable mono material trays, with Carrefour eliminating black plastic trays in 2023 after sorting facilities flagged them as non-detectable.

The cosmetics and personal care sector is likely to grow with an anticipated CAGR of 10.2% in next coming years, with the premiumization, sustainability branding, and e-commerce logistics. Over 80% of new skincare launches in 2024 used airless pump bottles or opaque PET jars to protect active ingredients from light and oxidation. Brands like L’Oréal and Natura have committed to 100% reusable, recyclable, or compostable packaging by 2025, with rigid formats leading the transition through mono-material PP and rPET designs. E-commerce growth has amplified demand for durable containers, with 92% of online beauty brands using rigid bottles to prevent leakage during transit, as per the European E Commerce Association.

REGIONAL ANALYSIS

Germany Rigid Plastic Packaging Market Analysis

Germany was the top performer of the Europe rigid plastic packaging market with its advanced recycling infrastructure, stringent environmental regulations, and powerful manufacturing base. According to a study, over 95% of PET bottles are collected through the nationwide deposit system, with 98% of households participating as per the German Environment Agency. The country hosts leading converters like ALPLA and Greiner Packaging, which supply mono material trays and rPET bottles to global brands. Germany’s Circular Economy Act mandates that all packaging placed on the market be recyclable by 2025, driving rapid adoption of design for recycling principles. The nation also leads in reusable systems, with over 300 supermarkets participating in standardized HDPE container networks for dairy and juices.

France Rigid Plastic Packaging Market Analysis

France was positioned second in the European rigid plastic packaging market, distinguished by its aggressive anti-waste legislation and leadership in advanced recycling. According to the French Ministry of Ecological Transition, the Anti-Waste Law for a Circular Economy bans single-use plastic packaging for fruits and vegetables and mandates 100% recyclable packaging by 2025. The country pioneered industrial-scale enzymatic PET recycling with Carbios commissioning the world’s first commercial plant in Clermont-Ferrand in 2024, producing food-grade rPET from colored and opaque waste.

United Kingdom Rigid Plastic Packaging Market Analysis

The United Kingdom rigid plastic packaging market growth is likely to be driven by the characterized by strong retailer influence and post-Brexit regulatory autonomy. According to the UK Department for Environment, Food and Rural Affairs, the Plastic Packaging Tax introduced in 2022 levies 210 pounds per metric ton on packaging with less than 30% recycled content, driving rapid reformulation across sectors. Major retailers like Tesco and Sainsbury’s have eliminated black plastic trays and committed to 100% recyclable rigid packaging by 2025. The UK also hosts Europe’s largest chemical recycling pilot by Recycling Technologies, converting mixed plastic waste into feedstock for new rigid containers.

Italy Rigid Plastic Packaging Market Analysis

Italy's rigid plastic packaging market growth is likely to grow with its strong food and beverage culture and advanced converting industry. According to the Italian National Institute of Statistics, over 1.2 million metric tons of rigid plastic packaging were consumed in 2024, with olive oil, wine, and ready meals representing key applications. The country’s CONAI system achieves a 72% collection rate for rigid plastics through producer-funded recovery as per the Italian Ministry of Ecological Transition. Additionally, Italy is a pioneer in reusable glass and plastic systems for water, with Sanpellegrino deploying returnable PET bottles across 80% of its domestic portfolio.

COMPETITION OVERVIEW

Competition in the Europe rigid plastic packaging market is intense and multifaceted, involving global giants, regional specialists, and agile innovators. Large players like Amcor and ALPLA compete on scalable technology and circular infrastructure, while European converters such as Greiner and RPC Group differentiate through localized service and regulatory expertise. This regulatory pressure has shifted competition from cost and aesthetics to sustainability credentials and compliance readiness. Innovation now centers on mono-material structures, reusable formats, and digital watermarking for sorting. At the same time, inconsistent national recycling systems create operational complexity for multinationals. The most successful companies combine material science with policy foresight and close brand collaboration to navigate this dynamic landscape where environmental performance is as critical as functional reliability.

KEY MARKET PLAYERS

A few major players of the Europe rigid plastic packaging market include

- Amcor plc

- Berry Global Inc

- ALPLA Group

- RPC Group (Berry Global)

- Sonoco Products Company

- Silgan Holdings

- Greiner Packaging

- DS Smith Plastics

- Plastipak Holdings

- Paccor

- Huhtamaki

- Coveris

- AptarGroup

Top Strategies Used by the Key Market Participants

Key players in the Europe rigid plastic packaging market prioritize mono-material design to enhance recyclability and comply with Extended Producer Responsibility schemes. They invest in expanding food-grade recycled resin capacity through mechanical and advanced recycling partnerships. Companies develop reusable and refillable rigid systems to align with EU reuse targets and retailer sustainability pledges. They collaborate with brands on lightweighting and design for recycling to reduce material use and improve sortation efficiency. Additionally, firms localize production to shorten supply chains and meet national regulatory requirements. These strategies collectively address the dual imperatives of functionality and circularity in a highly regulated and competitive environment.

Leading Players in the Market

ALPLA Group

ALPLA Group is a leading European producer of rigid plastic packaging headquartered in Austria with operations across 46 countries. The company specializes in PET bottles, HDPE containers, and reusable packaging systems for the food, beverage, and personal care sectors. It also launched a mono-material PP yogurt pot certified recyclable by RecyClass. These initiatives reinforce ALPLA’s global leadership in circular packaging solutions while supporting EU regulatory compliance and brand sustainability goals worldwide.

Amcor plc

Amcor plc is a multinational packaging giant with a strong European footprint in rigid plastic containers for pharmaceuticals, food, and specialty products. The company leverages its global R&D network to develop high-barrier recyclable formats, including all PP medical packaging and lightweight PET bottles. It also partnered with major retailers to implement reusable container pilots in the UK and France. These actions position Amcor as a solutions-driven partner in Europe’s transition toward circular and functional rigid packaging.

Greiner Packaging

Greiner Packaging is a key European manufacturer of rigid plastic packaging based in Austria, with a focus on thermoformed trays, containers, and reusable systems. The company serves the food, healthcare, and industrial sectors with products designed for recyclability and resource efficiency. In 2024, Greiner commissioned a new production line in the Czech Republic dedicated to rPP trays containing 50% recycled content. It also launched the GreenLine range of mono material PET and PP containers, compliant with EU design for recycling guidelines.

MARKET SEGMENTATION

This research report on the Europe rigid plastic packaging market has been segmented and sub-segmented based on product type, material, end-use industry, and region.

By Product Type

- Bottles and Jars

- Trays and Containers

- Caps and Closures

- Intermediate Bulk Containers

By Material

- Polyethylene (PE)

- Polyethylene Terephthalate (PET)

- Polypropylene (PP)

By End Use Industry

- Food

- Beverage

- Healthcare

- Cosmetics and Personal Care

By Region

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

1. What materials are commonly used in rigid plastic packaging?

Key materials include PET, PP, HDPE, LDPE, PVC, and PS

2. Which end-use industries drive the demand for rigid plastic packaging in Europe?

Major industries include food & beverages, pharmaceuticals, personal care & cosmetics, household care, and industrial products.

3. What factors are driving the growth of the market?

Drivers include rising packaged food consumption, convenience packaging demand, lightweight packaging advantages, recyclability initiatives, and growth in the pharma & personal care sectors.

4. What challenges does the market face?

Major challenges include environmental concerns, strict EU regulations on plastics, recycling limitations, and competition from sustainable packaging alternatives.

5. Which countries lead the rigid plastic packaging market in Europe?

Germany, the UK, France, Italy, and Spain are major markets due to strong manufacturing and consumer goods industries.

6. What are the key trends in the European rigid plastic packaging market?

Trends include lightweighting, use of recycled plastics (rPET, rPP), bio-based plastics, smart packaging, and increased focus on circular economy goals.

7. Who are the major players in the market?

Amcor plc, Berry Global Inc., ALPLA Group, RPC Group, Silgan Holdings, Greiner Packaging, Plastipak Holdings, Paccor, Huhtamaki, Coveris, AptarGroup.

8. What types of rigid plastic packaging are most commonly used?

Bottles, containers, jars, tubs, trays, cans, and closures/caps.

9. Which polymer type dominates the market?

PET and HDPE dominate due to widespread use in food, beverage, and household packaging.

10. What is the market outlook for the next few years?

The market is expected to grow steadily due to rising packaging innovation, recyclability initiatives, increasing consumption of packaged goods, and strong demand from the personal care and pharma sectors.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com