Europe Robotics Market Size, Share, Trends, & Growth Forecast Report By Type (Mobile Robotics, Static Robotics, Others), Component, Application and Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic and Rest of Europe), Industry Analysis From 2026 to 2034

Europe Robotics Market Report Summary

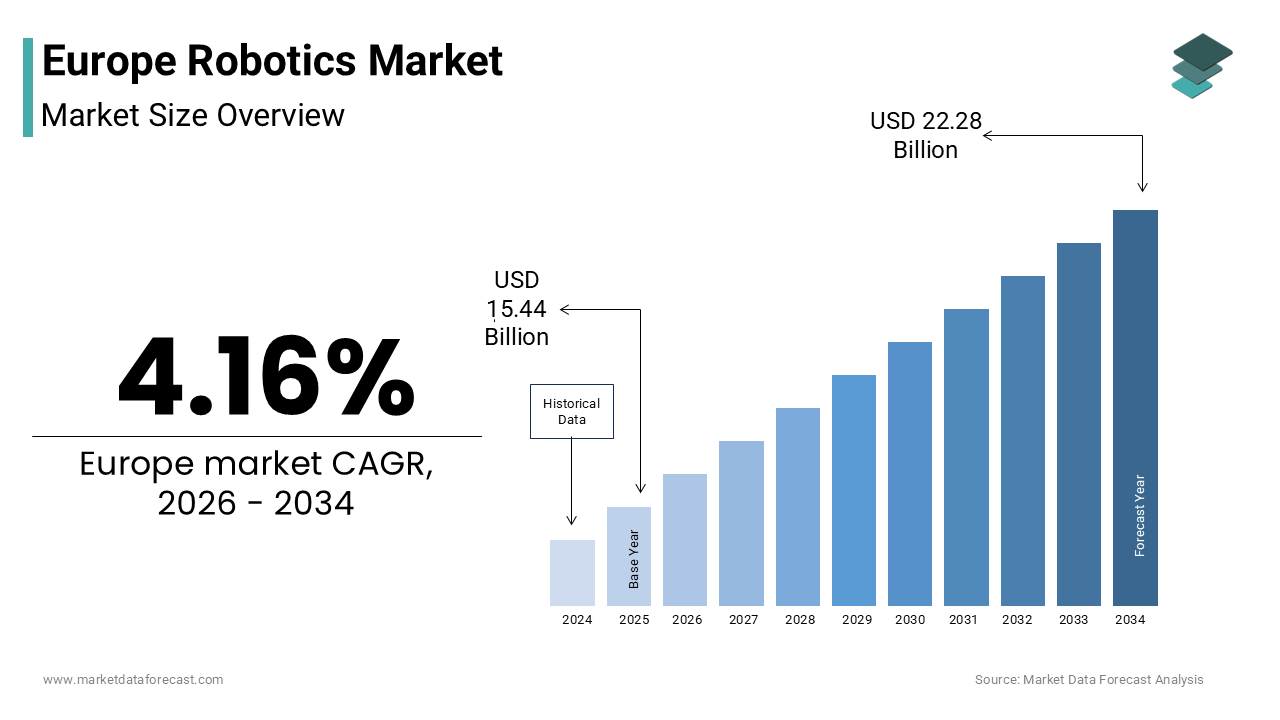

The Europe robotics market was valued at USD 15.44 billion in 2025, is estimated to reach USD 16.08 billion in 2026, and is projected to reach USD 22.28 billion by 2034, growing at a CAGR of 4.16% during the forecast period from 2026 to 2034. The growth of the Europe robotics market is driven by acute labor shortages across manufacturing, logistics, healthcare, and agriculture, alongside the European Union’s strategic push toward technological sovereignty and resilient supply chains. Rising automation adoption in automotive production, rapid expansion of autonomous mobile robots (AMRs) in logistics, and increasing deployment of collaborative robots (cobots) are further strengthening market demand. Additionally, demographic pressures such as an aging workforce are accelerating robotics integration across both industrial and service sectors.

Key Market Trends

- Rising adoption of collaborative robots (cobots) in SME manufacturing environments.

- Rapid expansion of autonomous mobile robots (AMRs) in warehouses and fulfillment centers.

- Increasing investment in AI-powered robotics and machine vision systems.

- Growing deployment of robots in precision agriculture and healthcare applications.

- Emergence of Robotics-as-a-Service (RaaS) models to reduce upfront capital barriers.

Segmental Insights

-

Based on type, the static robotics segment led the market by accounting for 60.6% of the regional market share in 2025, driven by strong demand from automotive and industrial manufacturing lines.

-

The mobile robotics segment is projected to grow at the fastest CAGR of 19.5% during the forecast period due to increased warehouse automation and flexible intralogistics solutions.

-

Based on component, the sensors segment dominated the market with 29.2% share in 2025, owing to rising demand for safety, perception, and environmental awareness in both industrial and collaborative robots.

-

Based on application, the automotive segment held the leading position with 33.9% share in 2025, supported by high robot density in welding, painting, and assembly operations.

Regional Insights

The Europe robotics market demonstrates strong regional concentration in industrially advanced economies with high robot density and manufacturing strength.

-

Germany led the market with 29.2% share in 2025, supported by its Industrie 4.0 strategy and strong automotive manufacturing ecosystem.

-

Italy secured the second-leading share, driven by robotics adoption across packaging, food processing, and SME-driven machinery sectors.

-

France is expected to witness promising growth fueled by state-backed industrial policy and aerospace automation initiatives.

-

Sweden is advancing through strong industrial automation players and healthcare robotics adoption.

-

The United Kingdom is registering steady growth, particularly in AI-driven robotics, medical robotics, and agri-tech innovation.

Competitive Landscape

The Europe robotics market is characterized by strong competition among established industrial automation leaders and emerging specialized robotics firms. Market leaders focus on expanding collaborative and mobile robotics portfolios, investing in AI-enabled vision and sensor integration, and strengthening local service networks. Strategic initiatives include partnerships under EU-funded research programs, expansion of RaaS models, and development of complete automation ecosystems combining hardware, software, and digital twin platforms. Competitive differentiation increasingly depends on integration capabilities, software intelligence, and after-sales support rather than hardware alone. Major players operating in the Europe robotics market include ABB Ltd., KUKA AG, Siemens AG, Vanderlande Industries B.V., Swisslog Holding AG, AutoStore Holdings Ltd., SSI Schaefer AG, KNAPP AG, Exotec SAS, and Robotnik Automation.

Europe Robotics Market Size

The Europe robotics market size was valued at USD 15.44 billion in 2025 and is anticipated to reach USD 16.08 billion in 2026 from USD 22.28 billion by 2034, growing at a CAGR of 4.16% during the forecast period from 2026 to 2034.

Robotics includes the development, deployment, and integration of programmable machines designed to automate physical tasks across industrial, commercial, and increasingly, personal domains. This market is a critical enabler of the continent’s strategic objectives in manufacturing competitiveness, economic resilience, and societal well-being. Its scope ranges from traditional industrial manipulators on factory floors to sophisticated collaborative robots (cobots), autonomous mobile robots (AMRs) in logistics, and service robots in healthcare and agriculture. A defining non-market statistic underpinning this sector is Europe’s acute demographic challenge. According to Eurostat, the old age dependency ratio in the EU is projected to rise significantly in the coming decades, which is creating structural pressure to automate tasks in eldercare, logistics, and manufacturing to offset a shrinking workforce. As per the European Commission, the EU’s manufacturing sector contributes a notable share to its gross domestic product, underscoring the existential importance of industrial automation for maintaining global competitiveness in an era of rising labor costs and supply chain volatility.

MARKET DRIVERS

Severe Labor Shortages Across Key Economic Sectors Drive Automation Adoption

The pervasive and worsening shortage of skilled and unskilled labor across its core industries is one of the major factors driving the robotics market growth in Europe. From manufacturing and logistics to agriculture and healthcare, employers are struggling to fill vacancies, a crisis exacerbated by an aging population and restrictive immigration policies in many countries. In the industrial sector, this gap is particularly acute for repetitive, physically demanding, or hazardous roles. As per the German Association of Chambers of Industry and Commerce (DIHK), many German manufacturers reported that a lack of skilled workers was a major constraint on their production capacity. This labor deficit has transformed robotics from a productivity enhancer into a necessity for operational continuity. Companies are now deploying robots not just to be more efficient, but simply to keep their production lines running and their warehouses functioning, making automation a direct response to a fundamental economic bottleneck.

EU’s Strategic Push for Technological Sovereignty and Resilient Supply Chains

A powerful macro level driver is the European Union’s concerted policy effort to achieve greater technological sovereignty and build resilient, secure supply chains. The disruptions caused by global events have laid bare the continent’s dependence on external suppliers for critical technologies. In response, the EU has launched initiatives like the European Chips Act and the Alliance for Robotics to foster a homegrown robotics ecosystem. This top-down support provides crucial funding for R&D and creates a favorable environment for public private partnerships. As per Horizon Europe, billions of euros have been allocated to projects focused on AI-enabled robotics for manufacturing and healthcare. This strategic imperative is compelling European companies to prioritize local or regional robotics solutions, not only to mitigate geopolitical risks but also to align with a broader political vision of a self-reliant, high-tech European industrial base, thereby creating a stable and growing demand for domestically developed and produced robotic systems.

MARKET RESTRAINTS

High Initial Investment and Complex Integration Costs Deter SMEs

A significant restraint on the widespread adoption of robotics, particularly among small and medium-sized enterprises (SMEs), is the formidable barrier of high upfront capital expenditure and the complexity of system integration. While the long-term return on investment can be substantial, the initial cost of purchasing a robot, along with the necessary safety infrastructure, software, and engineering services for integration into existing workflows, can be prohibitively expensive for smaller firms with limited capital budgets. As per the European DIGITAL SME Alliance, many of its members cited high acquisition and integration costs as the primary reason for not adopting robotics. This financial and technical hurdle confines advanced automation primarily to large corporations, leaving a vast swathe of the European industrial landscape unable to access the benefits of automation, thereby slowing the overall pace of technological diffusion and productivity growth across the continent.

Fragmented Regulatory Landscape and Lack of Harmonized Safety Standards

The Europe robotics market faces a critical restraint in the form of a fragmented and evolving regulatory environment. While the EU provides a broad framework, the interpretation and implementation of safety standards for robots, especially collaborative and mobile robots operating alongside humans, can vary significantly between member states. This lack of harmonization creates uncertainty for manufacturers and end users alike, complicating the design, certification, and cross-border deployment of robotic systems. Navigating this patchwork of national regulations increases time to market and compliance costs. As per a European robotics industry group study, the average time required to certify a new collaborative robot for sale across all major EU markets is significantly longer than in a single, unified regulatory zone. This regulatory friction acts as a brake on innovation and market expansion, particularly for startups and smaller integrators who lack the resources to manage complex compliance processes.

MARKET OPPORTUNITIES

Expansion of Robotics into Precision Agriculture and Sustainable Farming

A major opportunity for the Europe robotics market lies in the rapid adoption of agricultural robots to address the dual challenges of labor scarcity and the EU’s ambitious environmental goals under the Farm to Fork strategy. The continent’s agricultural sector is under intense pressure to reduce its reliance on chemical inputs while maintaining productivity. This has created fertile ground for robotic solutions such as autonomous weeding robots that use computer vision to mechanically remove weeds, eliminating the need for herbicides, and robotic harvesters that can pick delicate fruits with minimal waste. As per the European Commission’s Common Agricultural Policy, subsidies are available for investments in precision farming technologies. According to a European agri-tech association, the market for agricultural robots in the EU has shown strong growth, driven by a new generation of tech-savvy farmers seeking sustainable and efficient ways to manage their operations in an increasingly regulated and competitive environment.

Growth of Robotics as a Service (RaaS) Model for Democratizing Access

The emergence of the Robotics as a Service (RaaS) business model presents a transformative opportunity for the Europe robotics market to overcome the primary barrier of high capital costs. Instead of a large upfront purchase, customers can subscribe to robotic capabilities on a monthly or usage-based fee, which typically includes maintenance, software updates, and technical support. This model dramatically lowers the entry point for SMEs and allows businesses to scale their automation needs flexibly. In the logistics sector, for example, companies can deploy fleets of AMRs for seasonal peaks without a major capital commitment. As per a European venture capital firm specializing in deep tech, RaaS contracts have accounted for a notable share of new robotic deployments in the EU’s warehousing sector, with projections of further growth in the coming years. This shift from a product to a service paradigm is democratizing access to advanced automation and unlocking a vast new customer base that was previously priced out of the market.

MARKET CHALLENGES

Critical Shortage of Robotics Engineers and Skilled Integrators

One of the most pressing challenges facing the Europe robotics market is the severe shortage of professionals with the specialized skills required to program, deploy, and maintain advanced robotic systems. The demand for robotics engineers, mechatronics specialists, and system integrators far outstrips the supply from European universities and vocational programs. As per the European Federation of Robotics, the continent is expected to face a significant shortfall of qualified robotics professionals in the near future. This human capital gap creates a bottleneck that slows down project implementation, increases integration costs, and limits the ability of end users to fully exploit the potential of their robotic investments. Without a concerted effort to expand STEM education and create clear career pathways in robotics, this skills deficit will remain a fundamental constraint on the market’s ability to scale and deliver on its promised productivity gains.

Ethical and Societal Concerns Regarding Job Displacement and AI Autonomy

The Europe robotics market operates within a unique socio-political context where ethical considerations and public perception play a decisive role. There is persistent concern among citizens, labor unions, and policymakers about the potential for widespread job displacement due to automation. This apprehension is amplified by the increasing autonomy of robots powered by artificial intelligence, raising questions about decision-making, accountability, and safety. As per the European Parliament’s ongoing work on the AI Act, specific provisions for high-risk robotic applications reflect this cautious approach. These societal debates can lead to more stringent regulations, public resistance to certain applications, and a slower pace of adoption, particularly in sensitive areas like social care or public spaces. Navigating this complex ethical landscape requires manufacturers to engage in transparent dialogue and demonstrate that robotics is a tool for augmenting human labor rather than replacing it, a challenge that is as much cultural as it is technological.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 4.16% |

| Segments Covered | By Type, Component, Application and Region |

| Various Analyses Covered | Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

| Countries Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, the Netherlands, Turkey, the Czech Republic, and the Rest of Europe. |

| Market Leaders Profiled | ABB Ltd., KUKA AG, Siemens AG, Vanderlande Industries B.V., Swisslog Holding AG, AutoStore Holdings Ltd., SSI Schaefer AG, KNAPP AG, Exotec SAS, and Robotnik Automation. |

SEGMENTAL ANALYSIS

By Type Insights

The static robotics segment held the dominant position in the Europe robotics market in 2025 by accounting for 60.6% of the regional market share. The dominance of static robotics segment in the European market is attributed to its foundational role in Europe’s industrial manufacturing base. Industrial articulated arms and SCARA robots are deeply entrenched in high-volume production lines across automotive and electronics sectors, performing welding, painting, assembly, and palletizing with unmatched speed and precision. As per the International Federation of Robotics, Europe continues to install large numbers of industrial robots, with the majority being stationary units deployed in automotive manufacturing. This ongoing investment by Europe’s industrial giants ensures a stable demand stream for static robotic systems, solidifying their position as the market’s core.

The mobile robotics segment is a promising segment and is estimated to expand at a CAGR of 19.5% over the forecast period owing to the urgent need to automate material handling in warehouses and factories facing labor shortages. Autonomous Mobile Robots (AMRs), equipped with advanced sensors and AI, can navigate dynamic environments without fixed infrastructure, making them highly flexible compared to traditional AGVs. As per a European retail logistics report, fulfillment centers across Western Europe have increasingly adopted fleets of AMRs, with deployments doubling in recent years. This shift toward mobile, adaptable solutions is transforming intralogistics and fueling rapid demand for this segment.

By Component Insights

The sensors segment led the market by commanding for the highest share of 29.2% of the European market share in 2025. The dominance of the sensors segment in the European market is driven by their role as the primary interface between robots and the physical environment makes them indispensable. From proximity sensors on industrial arms to LiDAR arrays on AMRs, sensors provide the critical data enabling perception, safety, and precision. The rise of collaborative robots has further amplified demand, requiring dense arrays of force torque sensors and safety scanners. As per the European Photonics Industry Consortium, the average number of sensors per industrial robot has increased significantly since 2020, driven by the need for greater environmental awareness and adaptive control.

The vision systems segment is anticipated to register a CAGR of 22.6% over the forecast period. Machine vision enables robots to perform complex, non-repetitive tasks such as bin picking, quality inspection, and precision agriculture. High-resolution 3D cameras combined with AI-powered image recognition are revolutionizing warehouse automation and industrial applications. As per a European machine vision trade association, adoption of 3D vision in robotics has grown rapidly, supported by falling costs and improved processing power. This accessibility is driving widespread uptake and accelerating market expansion.

By Application Insights

The automotive segment led the European robotics market in 2025 with 33.9% of the European market share. Automotive manufacturing requires thousands of precise assembly steps, making robots indispensable for welding, painting, and assembly. Europe’s automotive giants such as Volkswagen, Stellantis, and BMW operate some of the most automated production networks globally. As per the European Automobile Manufacturers Association, the EU produced millions of motor vehicles in 2023, directly translating into continuous demand for industrial robots. This deep integration ensures automotive remains the largest and most stable application market for robotics in Europe.

The logistics segment is the fastest-growing application and is expected to witness a CAGR of 22.8% over the forecast period. The e-commerce expansion, labor scarcity, and supply chain resilience needs are contributing to the expansion of the logistics segment in the European market. Automated guided vehicles and AMRs are increasingly deployed in fulfillment centers and distribution hubs. As per a European logistics technology group, robot deployments in warehouses have grown significantly, with e-commerce giants and third-party logistics providers leading investments. This surge in automation is reshaping supply chains, making logistics a high-volume, innovation-driven growth engine for the robotics market.

REGIONAL ANALYSIS

Germany Robotics Market Analysis

Germany was the undisputed leader in the European robotics market in 2025 with 29.2% of the regional market share. The leading position of Germany in the European robotics market is driven by the renowned “Industrie 4.0” initiative and its role as Europe’s manufacturing powerhouse. German companies are at the forefront of deploying advanced automation in automotive, machinery, and chemical production. As per the International Federation of Robotics, Germany has the highest robot density in Europe, underscoring its deep industrial commitment to automation. With a strong domestic robotics industry led by firms like KUKA, Germany has built a self-reinforcing ecosystem that drives continuous innovation and adoption, making it the central engine of the continental market.

Italy Robotics Market Analysis

Italy secured second leading share of the European robotics market in 2025 owing to its diverse and innovative SME sector, particularly in specialized machinery for packaging, ceramics, and food processing. Italian manufacturers, known for flexibility and craftsmanship, increasingly adopt robotics to maintain competitiveness in high-mix, low-volume production. As per the Italian Robotics and Automation Association, many member companies integrated robotics into their solutions in 2023. This export-oriented industrial base ensures steady demand for collaborative and flexible robotic systems, positioning Italy as a vital hub for agile automation.

France Robotics Market Analysis

France is estimated to witness a promising CAGR in the European robotics market over the forecast period. The strong state-supported industrial policy and a focus on aerospace, nuclear energy, and rail transport are supporting the robotics market growth in France. The French government’s “France 2030” investment plan has allocated significant funding to reindustrialization and technological sovereignty, with robotics as a key pillar. As per the French National Centre for Scientific Research, public-private partnerships in robotics received substantial funding in 2023. This top-down support, combined with a growing startup ecosystem in Paris and Toulouse, is fostering innovation in both industrial and service robotics, creating a dynamic and well-funded market.

Sweden Robotics Market Analysis

Sweden is predicted to account for a notable share of the European robotics market over the forecast period. Its foundation lies in world-class engineering in automotive and telecommunications, supported by a strong social welfare model that embraces technology to address demographic challenges. Companies like ABB and Volvo are global leaders in industrial automation and drive domestic demand. A crucial factor is Sweden’s proactive use of technology to solve societal issues, such as eldercare, with government-funded pilot projects for service robots in healthcare facilities. Sweden’s leadership in 5G infrastructure also provides the connectivity needed for advanced mobile and collaborative robots, creating fertile ground for innovation in both industrial and service applications.

United Kingdom Robotics Market Analysis

The United Kingdom is expected to register a healthy CAGR in the European market over the forecast period owing to its leadership in artificial intelligence, strong university research base, and vibrant startup scene in London and Cambridge. While traditional manufacturing has declined, the UK excels in high-value applications of robotics. A key driver is investment in medical and surgical robotics, with hospitals being early adopters of systems like the da Vinci platform. As per Innovate UK, hundreds of millions of pounds were awarded to robotics and AI projects in 2023, with a significant portion focused on healthcare and agri-tech. This emphasis on software-driven, cutting-edge robotics gives the UK market a unique and forward-looking character within Europe.

COMPETITIVE LANDSCAPE

The competitive environment in the Europe robotics market is characterized by the dominance of a few global industrial giants who compete on technology, reliability, and service infrastructure. The rivalry is intense but largely centred on the industrial segment, where companies like ABB, KUKA, and FANUC leverage their decades of experience and deep integration into European manufacturing ecosystems. While these leaders hold a strong position, they face increasing competition from specialized European startups in emerging fields like mobile robotics and agricultural automation. The market is not fragmented at the high end, but it is highly dynamic, with competition shifting from hardware to software and service capabilities. Success is increasingly determined by a company’s ability to offer complete, easy to deploy solutions and robust after sales support, rather than just the robot itself, creating a high barrier to entry for new players without a strong service footprint.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the Europe Robotics Market include

- ABB Ltd.

- KUKA AG

- Siemens AG

- Vanderlande Industries B.V.

- Swisslog Holding AG

- AutoStore Holdings Ltd.

- SSI Schaefer AG

- KNAPP AG

- Robotnik Automation

- Exotec SAS

Top Players in the Market

ABB Ltd

ABB Ltd, a Swiss based multinational, is a global powerhouse in industrial automation and robotics with its European operations serving as the heart of its innovation and manufacturing. The company is a pioneer in both industrial articulated robots and collaborative robots, offering a comprehensive portfolio that serves the automotive, electronics, and logistics sectors across the continent. ABB’s contribution to the global market is its leadership in robot software and digital integration, particularly its RobotStudio offline programming platform. To strengthen its European position, ABB has heavily invested in its “Factory of the Future” concept, launching new cobot models with enhanced AI capabilities and expanding its network of application centers to provide localized support and training for European manufacturers seeking to automate.

KUKA AG

KUKA AG, a German engineering company and now a wholly owned subsidiary of China’s Midea Group, remains a quintessential European robotics champion with a deep legacy in automotive manufacturing automation. Headquartered in Augsburg, KUKA is renowned for its high precision industrial robots and its innovative mobile robotic platforms under the KMP series. Its global contribution lies in its expertise in system integration for complex production lines. In Europe, KUKA has strategically focused on diversifying beyond its traditional automotive base into sectors like e commerce logistics and healthcare. Recent actions include the development of it’s ready to use robotic cells for SMEs and significant investment in its R&D center in Germany to advance its AI and vision guided robotics technologies for the European market.

FANUC Europe Corporation S.A.

FANUC Europe, the regional arm of the Japanese robotics giant, is a dominant force in the European industrial robotics landscape, known for its extreme reliability, long service life, and extensive service network. The company provides a wide range of CNC systems and industrial robots that are the backbone of many European factories, particularly in the automotive and general machinery industries. FANUC’s global contribution is its vertically integrated manufacturing model, which ensures consistent quality and performance. To fortify its European standing, FANUC has been aggressively expanding its European headquarters in Luxembourg and its network of technical support centers. The company has also launched a series of user-friendly collaborative robots and partnered with European system integrators to develop industry specific automation solutions that address the unique needs of the local market.

Top Strategies Used by the Key Market Participants

Key players in the Europe robotics market are primarily focused on developing user friendly and easily integrable robotic solutions to cater to the vast small and medium enterprise sector. They invest heavily in software and digital platforms to enable remote monitoring, predictive maintenance, and seamless integration with existing factory IT systems. A core strategy involves expanding their portfolio of collaborative robots and mobile platforms to address the growing demand for flexible automation in logistics and non-automotive industries. Companies also prioritize building extensive local support and training networks to overcome the skills gap and build customer confidence. Furthermore, they are actively engaging in public private partnerships and EU funded research projects to align their R&D with the continent’s strategic goals for technological sovereignty and sustainable manufacturing.

MARKET SEGMENTATION

This research report on the Europe Robotics Market has been segmented and sub-segmented based on the following categories.

By Type

- Mobile Robotics

- Static Robotics

- Others

By Component

- Sensors

- Actuators

- Control Units

- Vision Systems

- Brake Systems

- Others

By Application

- Electronics

- Agriculture

- Military & Defense

- Medical & Healthcare

- Automotive

- Logistics

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

What is the Europe Robotics Market?

It refers to the development, deployment, and commercialization of industrial, service, and collaborative robots across European industries.

What are the major types of robots used in Europe?

Industrial robots, service robots, collaborative robots (cobots), autonomous mobile robots (AMRs), and medical robots are the primary categories.

What factors are driving robotics adoption in Europe?

Labor shortages, rising production costs, automation demand, Industry 4.0 initiatives, and AI integration are key growth drivers.

Which industries are the largest adopters of robotics in Europe?

Automotive, manufacturing, logistics, healthcare, electronics, and food & beverage industries lead adoption.

Why is the automotive sector important for robotics demand?

Automotive manufacturing relies heavily on robotic automation for welding, painting, assembly, and quality inspection processes.

How is Industry 4.0 influencing the robotics market?

Smart factories, IoT integration, and data-driven automation systems are increasing robotic deployment in European production facilities.

What role do collaborative robots (cobots) play in Europe?

Cobots work safely alongside humans, making them ideal for SMEs and flexible manufacturing environments.

How are autonomous mobile robots (AMRs) impacting logistics?

AMRs improve warehouse automation, material handling efficiency, and last-mile delivery operations.

Which countries lead the Europe Robotics Market?

Germany, France, Italy, the United Kingdom, and Nordic countries are major robotics adopters.

What challenges does the Europe Robotics Market face?

High initial investment costs, integration complexity, cybersecurity risks, and skilled labor shortages are key challenges.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com