Europe Rubella Vaccine Market Size, Share, Trends & Growth Forecast Report By End User and By Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic & Rest of Europe) – Industry Analysis and Forecast, 2026 to 2034

Europe Rubella Vaccine Market Size

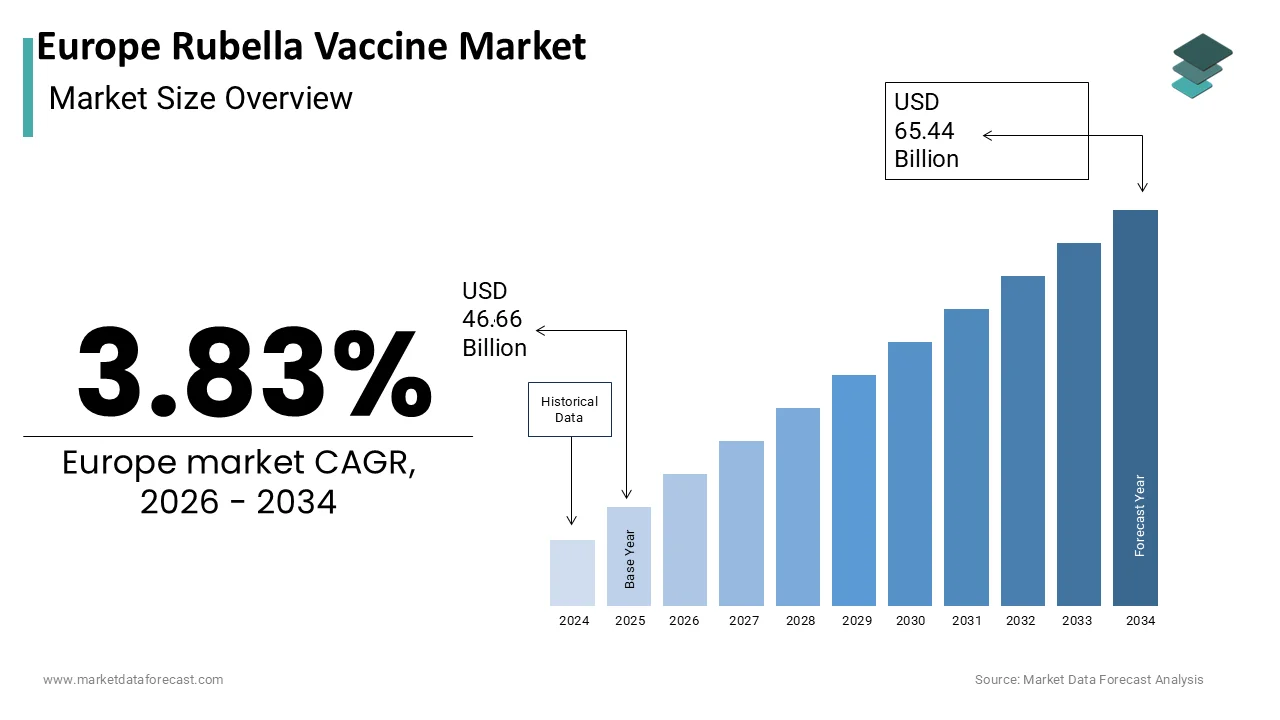

The europe rubella vaccine market size was valued at USD 46.66 billion in 2025, is expected to have a 3.83 % CAGR from 2026 to 2034 and be worth USD 65.44 billion by 2034 from USD 48.45 billion in 2026.

Rubella vaccine refers to immunization products designed to prevent rubella infection, a contagious viral disease that poses severe risks during pregnancy, including congenital rubella syndrome, which can cause deafness, cataracts, heart defects, and developmental delays in newborns. In Europe, rubella vaccination is universally delivered through combined mea, mumps, rubella, or measles, mumps, rubella, varicella vaccines as part of national childhood immunization programs. Never, maintaining elimination requires continuous immunization efforts as immunity gaps in adolescents and young adults remain a concern. The European Medicines Agency oversees centralized approval of rubella-containing vaccines, ensuring consistent safety and efficacy standards across the European Union. Congenital rubella syndrome is now rare in Europe due to vaccination, and the market is primarily driven by routine pediatric schedules, catch-up campaigns, and public health mandates rather than outbreak response.

MARKET DRIVERS

Universal National Immunization Programs Ensure Sustained Vaccine Demand

Mandatory and publicly funded childhood immunization schedules across all European countries drive the growth of the Europe rubella vaccine market. According to the European Centre for Disease Prevention and Control, every European Union member state includes two doses of the MMR vaccine in its national immunization program. In 2023, twenty-six out of thirty-one European countries reported first-dose MMR coverage exceeding ninety percent among two-year-olds, demonstrating strong programmatic adherence. Countries like Portugal maintain coverage above ninety-six percent through school entry requirements and integrated electronic immunization registries that flag missed doses. The United Kingdom’s National Health Service provides MMR vaccines free of charge at general practitioner clinics and school-based sessions. Furthermore, the European Commission’s Joint Action on Vaccination encourages cross-border coordination to harmonize schedules and address immunity gaps in mobile populations. This institutionalized public health infrastructure transforms rubella vaccination from a discretionary health choice into a routine civic norm, ensuring consistent uptake and market stability.

Risk of Congenital Rubella Syndrome Drives Preventive Policy Emphasis

The consequences of rubella infection during early pregnancy continue to emphasize Europe’s unwavering commitment to high vaccination coverage, which in turn propels the expansion of the Europe rubella vaccine market. According to the World Health Organization, a rubella infection in the first trimester carries up to a ninety percent risk of congenital rubella syndrome. National health agencies respond with targeted serosurveys. France mandates rubella immunity testing during early prenatal care and offers immediate vaccination postpartum if needed. These measures reflect a precautionary public health principle where even minimal risk of fetal harm justifies population-wide prevention. Consequently, rubella vaccination remains non-negotiable in European health policy, sustaining demand for safe and effective vaccines across generations.

MARKET RESTRAINTS

Vaccine Hesitancy and Misinformation Affect Coverage Consistency

Persistent vaccine hesitancy fueled by misinformation poses a restraint on the Europe rubella vaccine market. The Vaccine Confidence Project's August 2023 report noted that while vaccine confidence in some EU member states declined between 2018 and 2022, especially among younger adults, other countries saw improvements. In 2023, Romania reported MMR first-dose coverage of only eighty-two percent among two-year-olds. Outbreaks follow these immunity gaps. According to the ECDC, there were 3,973 measles cases reported in the EU/EEA in 2023, not over two thousand. Public health authorities struggle to counter emotionally charged misinformation with technical data, leading to localized vulnerability that threatens regional elimination status and complicates supply planning.

Limited Standalone Rubella Vaccine Availability Constricts Targeted Use

The near exclusive use of combined MMR or MMRV vaccines restricts the availability of monovalent rubella formulations by limiting flexibility in specific clinical or public health scenarios, which hampers the expansion of the Europe rubella vaccine market. This poses challenges when only rubella immunity is lacking, such as in seronegative women of childbearing age who may have contraindications to live measles or mumps components. Furthermore, global shortages of MMR vaccines, as occurred in 2021 due to manufacturing delays, directly impact rubella protection even when rubella-specific demand is high. This lack of formulation diversity reduces public health agility and exposes the system to supply chain risks beyond rubella-specific factors.

MARKET OPPORTUNITIES

Integration with Regional Measles Elimination Initiatives Enhances Program Reach

The strategic alignment of rubella control with broader measles elimination efforts across the region creates synergistic possibilities for vaccine delivery and surveillance, which provides new opportunities for the Europe rubella vaccine market. According to the World Health Organization Regional Office for Europe, the measles rubella initiative provides a unified framework for joint outbreak response and data sharing. In 2023, following an increase in measles cases, the ECDC recommended catch-up vaccination campaigns to address immunity gaps. These integrated campaigns achieve higher efficiency by leveraging shared cold chain logistics training and communication materials. Furthermore, electronic immunization registries in countries like Denmark and Estonia automatically flag individuals missing either measles or rubella doses, enabling precise recall systems. The European Commission's joint procurement mechanism, now governed by the Regulation on serious cross-border health threats, is primarily used for acquiring medical countermeasures during major health crises. Public health systems embed rubella within a larger elimination architecture to amplify imp, act, reduce duplication, and ensure the disease remains prioritized even as its standalone incidence declines.

Expansion of Preconception Care Programs Creates New Vaccination Pathways

The growing emphasis on preconception health in European maternal care systems opens fresh prospects for the Europe rubella vaccine market. According to sources, a growing number of European countries have made rubella immunity screening a routine part of preconception or early prenatal healthcare visits. As per research, studies from Norway indicate that incorporating these screenings within family planning services has significantly improved vaccination coverage among women lacking immunity compared to less structured approaches. These proactive strategies address the important window before pregnancy when vaccination is safe and effective. Reproductive health services increasingly adopt life course approaches. Rubella vaccination transitions from a childhood-only intervention to a lifelong component of women’s preventive care.

MARKET CHALLENGES

Supply Chain Fragility Due to Limited Global Manufacturers

Extreme concentration in global manufacturing challenges the growth of the Europe rubella vaccine market. The oligopolistic structure creates systemic risk. Unlike therapeutic drugs, vaccine production cannot be rapidly scaled due to complex biological processes and stringent batch testing requirements. This manufacturing barrier leaves national immunization programs exposed to external disruptions with no alternative suppliers available within the EU. Until regional production capacity is diversified, Europe remains dependent on a fragile global supply chain.

Waning Immunity in Young Adult Cohorts Threatens Elimination Status

Region faces emerging susceptibility among young adults due to waning immunity and historical gaps in second dose uptake, which slows down the expansion of the Europe rubella vaccine market. The issue stems from suboptimal second-dose coverage in the early 2000s when several countries had not yet implemented two-dose policies. Aging individuals may not seek booster doses because of the perception that rubella has been eradicated. Proactive seroscreening and catch-up vaccination are needed to prevent this silent immunity gap from reigniting endemic transmission, affecting decades of elimination progress, and destabilizing vaccine demand forecasting.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By End-User and Region. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, and the Rest of Europe |

| Market Leaders Profiled | Merck & Co., Inc., GlaxoSmithKline Plc, Chiron Corporation (Novartis), Sanofi-Aventis, Serum Institute of India, Astellas Pharma Inc., AstraZeneca Plc (Medimmune, LLC), CSL Limited, Pfizer Inc., Berna Biotech (Crucell). |

SEGMENTAL ANALYSIS

By End User Insights

The pediatric rubella vaccination segment led the Europe rubella vaccine market by accounting for a substantial share in 2025. The dominance of the pediatric rubella vaccination segment is propelled by mandatory public health policies that integrate rubella prevention into routine early childhood care across all European Union member states. The United Kingdom’s National Health Service delivers over one million MMR doses annually to children through general practitioner networks and school programs. Similarly, Germany’s Standing Committee on Vaccination mandates MMR as a prerequisite for daycare enrollment, strengthening compliance. The pediatric segment benefits from centralized procurement, stable funding, and electronic immunization registries that automatically track and recall missed doses. This institutionalized delivery model, combined with decades of public trust in childhood vaccination, strengthens pediatrics as the overwhelming core of rubella vaccine utilization in Europe.

The adult rubella vaccination segment is predicted to witness the highest CAGR of 7.9% from 2025 to 2033 due to targeted preconception health strategies and serosurveillance initiatives. Unlike pediatric vaccination, which is universal, adult vaccination focuses on women of childbearing age who lack immunity, identified through routine gynecological or prenatal screening. France mandates rubella immunity verification during the first prenatal visit and provides free catch-up vaccination after delivery. Adult rubella vaccination transitions from reactive to proactive, which drives sustained growth in a niche but vital segment, as reproductive health services increasingly adopt life course approaches.

COUNTRY LEVEL ANALYSIS

Germany Market Analysis

Germany was the top performer in the Europe rubella vaccine market by occupying 20.7% share in 2025. The dominance of Germany is primarily driven by its robust public health infrastructure and stringent immunization mandates. The country’s Standing Committee on Vaccination recommends two doses of the MMR vaccine, with the first at eleven to fourteen months and the second between fifteen and twenty-three months. A pivotal driver is the 2020 Measles Protection Act, which requires proof of MMR vaccination for all children attending daycare or school and for staff in medical and community facilities, directly expanding demand beyond routine pediatrics. Germany also operates a nationwide electronic immunization registry that enables real-time monitoring and recall of missed doses. The Paul Ehrlich Institute ensures rapid batch release and safety surveillance, maintaining public confidence. Apart from these, Germany’s federal structure allows states like Bavaria and North Rhine-Westphalia to fund supplementary catch-up campaigns targeting adolescents and young adults. These layered policy and operational mechanisms sustain Germany’s dominance in both volume and programmatic rigor.

United Kingdom Market Analysis

The United Kingdom is the second largest in the Europe rubella vaccine market by capturing 17.7% share in 2025. The growth of the United Kingdom is propelled by its integrated National Health Service delivery model and historical commitment to rubella elimination. The NHS provides MMR vaccines free of charge at general practitioner clinics, with the first dose administered at twelve months and the second at three years and four months. A unique driver is the inclusion of rubella immunity checks in preconception care pathways across all four nations; postpartum MMR vaccination is routinely offered to seronegative mothers before hospital discharge. This data-driven approach ensures continuous adaptation of vaccination strategies beyond childhood schedules.

France Market Analysis

France grew steadily in the Europe rubella vaccine market due to its comprehensive maternal and child health framework and mandatory vaccination policies. An important differentiator is France’s systematic integration of rubella screening into prenatal care. France also maintains a national immunization registry that links maternity hospitals with primary care providers to ensure follow-up. Regional health agencies in Île de France and Provence-Alpes-Côte d’Azur run targeted campaigns for migrant and underserved communities where coverage gaps persist. These coordinated clinical and public health measures support France’s high and sustained vaccine utilization.

Italy Market Analysis

Italy witnessed moderate expansion in the Europe rubella vaccine market, with its position shaped by recent policy reforms and persistent regional disparities. The 2017 Lorenzin Law made ten vaccines, including MMR, mandatory for school enrollment, reversing years of declining coverage. However, immunity gaps remain among young adults who missed vaccination during the low coverage era of the early 2000s. Italy addresses this through regional initiatives. The National Transplant Center also mandates rubella immunity verification for female organ donors, creating another vaccination touchpoint. These adaptive strategies reflect Italy’s transition from crisis response to sustained elimination maintenance.

Spain Market Analysis

Spain is likely to grow in the Europe rubella vaccine market from 2025 to 2033, owing to decentralized regional health management and strong maternal health integration. Each of Spain’s seventeen autonomous communities manages its own immunization schedule, though all align with the national recommendation of MMR at twelve months and three to four years. A key driver is the universal inclusion of rubella serology in the first prenatal visit across all regions. Spain also runs targeted campaigns for Roma and migrant communities through mobile clinics in Madrid and Barcelona. This blend of regional autonomy and national coordination ensures consistent rubella protection while addressing localized vulnerabilities.

COMPETITIVE LANDSCAPE

The competition in the Europe Rubella Vaccine Market is characterized by the presence of established pharmaceutical companies that dominate supply through proven combination vaccines. These companies compete primarily on product reliability, regulatory compliance, and consistent delivery to national immunization programs. While the number of direct competitors remains limited due to high regulatory barriers and complex manufacturing requirements, the market sees intense focus on operational excellence and public health partnerships. Companies differentiate themselves through investments in production scalability, cold chain management, and digital health tools that support vaccination campaigns. The European regulatory enenvironmentoverned by the European Medicines Agency, ensures stringent quality control, further consconsolidatesket among experienced players. Competition also extends to securing government tenders and maintaining strong relationships with ministries of health across member states. Overall, the market remains stable with competition centered on service quality, supply chain resilience, and alignment with public health priorities rather than price alone.

KEY MARKET PLAYERS

Key players operating in the europe rubella vaccine market profiled in this report are

- Merck & Co., Inc.

- GlaxoSmithKline Plc

- Chiron Corporation (Novartis)

- Sanofi-Aventis

- Serum Institute of India

- Astellas Pharma Inc.

- AstraZeneca Plc.

- (Medimmune, LLC.)

- CSL Limited

- Pfizer Inc.

- Berna Biotech (Crucell).

TOP LEADING PLAYERS IN THE MARKET

- GlaxoSmithKline is a leading contributor to the Europe Rubella Vaccine Market through its widely used MMR vaccine, which protects against measles,les m, and rubella. The company maintains a strong presence by ensuring a consistent vaccine supply and collaborating with public health agencies across European countries. It also participates in government immunization programs and supports awareness campaigns to increase vaccination coverage. These initiatives demonstrate its commitment to public health and strengthen its role as a dependable vaccine supplier in both European and global markets.

- Merck Sharp and Dohme plays a significant role in the Europe Rubella Vaccine Market by offering its MMR II vaccine, which is approved for use in multiple European nations. The company actively engages with regulatory bodies to maintain product compliance and ensure timely availability. Merck has recently focused on digital health integration by partnering with healthcare platforms to improve vaccine tracking and patient outreach. It also supports training programs for healthcare professionals to promote proper vaccine administration. These efforts have strengthened its operational footprint and enhanced trust among public health systems across Europe and beyond.

- Sanofi contributes to the Europe Rubella Vaccine Market primarily through its combination vaccines that include rubella protection as part of routine childhood immunization schedules. The company collaborates closely with national health authorities to align its supply with immunization targets. It also invests in research to explore next-generation vaccine technologies and improve immunogenicity. Through these actions, Sanofi demonstrates a proactive approach to maintaining vaccine access and supporting global immunization goals.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Key players in the Europe Rubella Vaccine Market employ several strategic approaches to maintain and enhance their competitive edge. These include strengthening manufacturing infrastructure to ensure a consistent vaccine supply and meet regulatory standards across diverse European countries. Companies actively collaborate with government health agencies and participate in national immunization programs to secure long-term contracts and public trust. Investment in research and development enables innovation in vaccine formulation and delivery methods. Apart from these, firms focus on expanding distribution networks through partnerships with logistics providers to maintain cold chain integrity. Digital health integration is another emerging strategy involving electronic immunization registries and mobile health platforms to improve vaccination tracking and coverage rates across the region.

MARKET SEGMENTATION

This research report on the europe rubella vaccine market has been segmented and sub-segmented into the following categories.

By End User

- Pediatric Rubella Vaccine

- Adult Rubella Vaccine

- Traveler Rubella Vaccine

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

1. Which countries contribute most to the Europe Rubella Vaccine Market?

Leading countries in the Europe Rubella Vaccine Market include Germany, the UK, France, Italy, and Spain,

with Italy showing the highest growth due to strong immunization programs and healthcare spending.

2. Who are the top companies operating in the Europe Rubella Vaccine Market?

Major players in the Europe Rubella Vaccine Market are Merck & Co., GlaxoSmithKline, Sanofi-Aventis, and Serum Institute of India,

well known for their research and reliable vaccine supply networks.

3. What are the major growth factors for the Europe Rubella Vaccine Market?

Government vaccination campaigns, public-private partnerships, and improved healthcare access

are the leading factors boosting the Europe Rubella Vaccine Market growth.

4. What challenges impact the Europe Rubella Vaccine Market?

The main challenges include vaccine hesitancy in a few regions, affordability disparities across Eastern Europe, and supply chain management issues in remote areas.

5. What vaccine types are included in the Europe Rubella Vaccine Market?

The Europe Rubella Vaccine Market includes monovalent rubella vaccines and combined MMR vaccines,

with tetravalent vaccine variants growing rapidly.

6. How is government policy influencing the Europe Rubella Vaccine Market?

Policies such as compulsory immunization for school enrollment and strong EU funding programs

have significantly encouraged the use of rubella vaccines in Europe.

7. What is the forecast period for Europe Rubella Vaccine Market growth?

The Europe Rubella Vaccine Market forecast spans 2025–2033,

with steady growth supported by R&D, new vaccine approvals, and high uptake rates.

8. Which age group drives most demand in the Europe Rubella Vaccine Market?

Pediatric patients and child immunization programs represent the largest demand segment, Though adult booster campaigns are gaining traction.

9. What role does congenital rubella awareness play in this market?

Awareness about congenital rubella syndrome prevention contributes to market expansion, as early immunization efforts reduce infections in newborns.

10. How are technological advancements shaping the Europe Rubella Vaccine Market?

New vaccine formulations, improved storage systems, and delivery innovations

are helping enhance vaccine safety and coverage rates in Europe.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com