Europe Safes and Vaults Market Research Report – Segmented By Type ( Electronic Safes, Biometric Safes ) Function Type ,Application, End User & Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic & Rest of EU) - Industry Analysis on Size, Share, Trends & Growth Forecast (2025 to 2033)

Europe Safes and Vaults Market Size

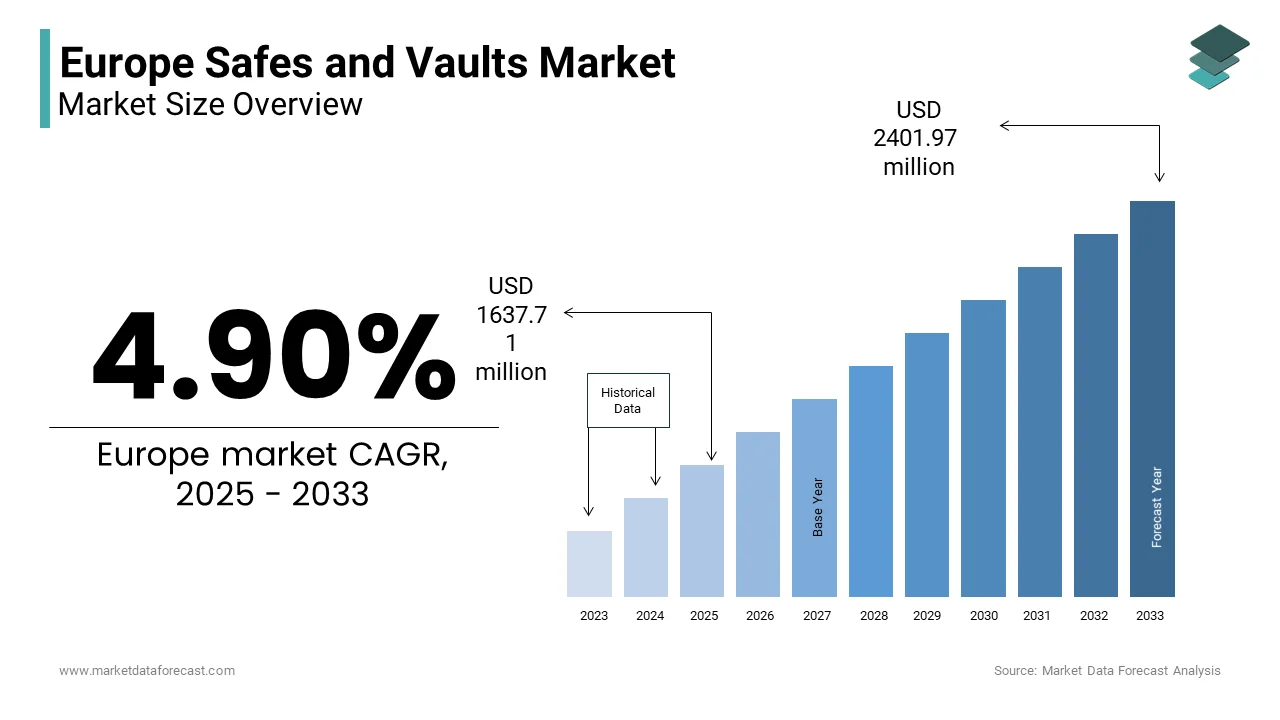

The Europe Safes and Vaults Market Size was valued at USD 1561.21 million in 2024. The Europe Safes and Vaults Market size is expected to have 4.90 % CAGR from 2025 to 2033 and be worth USD 2401.27 million by 2033 from USD 1637.71 million in 2025.

The Europe safes and vaults market covers a wide range of secure storage solutions designed for both residential and commercial applications. These include wall safes, floor safes, gun safes, data safes, vault doors, and high-security modular vault systems. The market is primarily driven by rising concerns over personal and corporate security, especially in light of increasing cyber-physical threats, financial frauds, and burglary incidents across urban centers. Unlike generic lock-and-key mechanisms, modern safes and vaults integrate advanced technologies such as biometric access control, digital keypads, time locks, and remote monitoring capabilities. In recent years, Europe has witnessed a surge in demand for high-security infrastructure, particularly in banking, retail, defense, and government sectors.

MARKET DRIVERS

Rising Crime Rates and Security Concerns Across Urban Centers

One of the primary drivers of the Europe safes and vaults market is the persistent rise in crime rates, particularly property crimes and burglaries in urban areas. This growing incidence of theft and break-ins has significantly heightened demand for secure storage solutions among households, small businesses, and financial institutions. Countries like France and Spain have seen a notable uptick in residential safe purchases, with online retailers reporting a notable year-over-year growth in sales since 2021. Moreover, the banking sector remains a critical consumer of high-end vault systems. This shift shows the institutional prioritization of physical security alongside digital safeguards.

Regulatory Mandates and Compliance Requirements in Sensitive Industries

Another significant driver of the Europe safes and vaults market is the imposition of strict regulatory mandates governing asset and information security across various industries. Governments and supranational bodies such as the European Commission have introduced stringent compliance frameworks that require financial institutions, defense organizations, and healthcare providers to maintain secure storage facilities for sensitive documents, valuables, and controlled substances. Also, under the European Firearms Directive, member states are required to ensure secure storage of firearms, compelling gun owners to invest in certified gun safes. Similarly, in the pharmaceutical industry, the Falsified Medicines Directive (FMD) requires secure storage of high-risk medications, prompting hospitals and pharmacies to upgrade their safe systems. These regulatory compulsions have not only expanded the customer base but also elevated product standards, encouraging manufacturers to develop safes and vaults with enhanced security features.

MARKET RESTRAINTS

High Initial Investment and Cost Sensitivity Among SMEs

Despite the growing demand for safes and vaults, one of the most prominent restraints in the Europe market is the high initial cost associated with premium security products. High-end safes and modular vault systems—especially those featuring biometric access, fireproofing, or tamper-proof locking mechanisms—often come with price tags that can exceed several thousand euros. This pricing structure poses a considerable barrier for small and medium-sized enterprises (SMEs), which constitute a substantial portion of potential buyers. Many SMEs operate under tight budget constraints and often prioritize operational expenditures over capital-intensive security upgrades. A 2023 survey conducted by the Federation of German Small and Medium Enterprises revealed that only a limited portion of surveyed SMEs had upgraded their existing safe systems in the past five years, citing cost as the primary deterrent. Furthermore, in economically volatile regions such as Eastern Europe, where inflationary pressures remain high, businesses are even more reluctant to allocate funds toward high-end security infrastructure.

Availability of Substandard and Non-Certified Products in the Secondary Market

A critical challenge impeding the Europe safes and vaults market is the proliferation of low-quality, non-certified products in the secondary and grey markets. Despite stringent regulations mandating compliance with European Committee for Standardization (CEN) norms such as EN 1143-1 for burglary resistance, many consumers—particularly in the residential segment—opt for cheaper, uncertified alternatives available through online platforms and local distributors. These substandard products not only compromise user safety but also distort market dynamics by undercutting genuine manufacturers. Such practices erode consumer trust in the efficacy of security products and reduce the incentive for legitimate companies to invest in research and development. Besides, enforcement of anti-counterfeiting laws remains inconsistent across EU member states, allowing these inferior products to persist in circulation.

MARKET OPPORTUNITIES

Integration of Smart Technologies in Safe and Vault Systems

A significant opportunity emerging in the Europe safes and vaults market is the integration of smart technologies into traditional security products. Manufacturers are increasingly incorporating IoT-enabled features such as remote access control, real-time monitoring, GPS tracking, and AI-based intrusion detection systems. This technological evolution aligns with the broader trend of digitization across home and commercial security ecosystems. According to a 2023 report, a notable percentage of new safe installations in Germany and the Netherlands included smart connectivity options, reflecting a growing consumer preference for integrated digital solutions. Moreover, the banking and logistics sectors are leading the adoption of smart vault systems that provide audit trails, automated locking schedules, and biometric verification logs. For example, ING Bank implemented cloud-connected vault management systems in 15 of its branch locations across Benelux in 2022, reducing manual intervention considerably and enhancing operational efficiency. Similarly, in the luxury retail sector, brands like Rolex and Cartier have begun deploying smart display safes equipped with RFID tagging and motion sensors to protect high-value inventory. Consumer interest in smart safes is also rising in the residential segment, particularly among millennials and tech-savvy homeowners. Online retailers such as Amazon and MediaMarkt have reported a significant year-on-year increase in smart safe sales since 2021.

Expansion of the Cash-in-Transit and Automated Teller Machine (ATM) Networks

The expansion of cash-handling infrastructure, particularly the Cash-in-Transit (CIT) services and ATM networks, presents a strong growth avenue for the Europe safes and vaults market. Despite the ongoing digital payment revolution, cash remains a dominant transaction mode in certain parts of Europe, especially in Southern and Eastern regions. Each of these ATMs requires secure internal safes and external vault protection to safeguard stored currency and prevent tampering or theft. Simultaneously, CIT operators have ramped up their fleet sizes and service frequencies to accommodate persistent demand for cash replenishment. In Poland alone, CIT revenues grew notably in 2023, as reported by the Polish Logistics and Security Institute, directly translating into higher procurement volumes for armored vehicles equipped with high-security safes. Furthermore, the implementation of stricter security regulations for CIT operations under the EU’s Payment Services Directive (PSD2) has compelled service providers to adopt advanced safe systems with encryption and tamper-detection capabilities.

MARKET CHALLENGES

Stringent Certification and Approval Processes Delay Product Launches

One of the foremost challenges facing the Europe safes and vaults market is the lengthy and complex certification process required for product approval. Manufacturers must adhere to rigorous standards set by the European Committee for Standardization (CEN), including EN 1143-1 for burglary resistance and EN 14450 for explosion-resistant safes. Obtaining certifications such as ECB-S (European Certification Board for Security Equipment) involves extensive testing procedures that can take anywhere from six months to two years, depending on the product category and complexity. According to the European Safe Association, delays in certification have caused some manufacturers to postpone product launches by up to nine months, affecting their ability to respond swiftly to changing market demands. Startups and smaller firms, in particular, face difficulties in navigating this regulatory landscape without adequate financial backing or technical expertise. Moreover, the lack of harmonized testing protocols across EU member states adds another layer of complexity.

Fluctuating Raw Material Prices Impacting Production Costs

Fluctuating raw material prices represent a significant challenge for manufacturers in the Europe safes and vaults market. Steel, aluminum, and high-grade alloys—key components in producing durable and secure safes—are subject to volatile pricing influenced by global supply chain disruptions, geopolitical tensions, and energy costs. Like, steel prices in Europe surged significantly in 2022 following Russia's invasion of Ukraine, which disrupted key supply routes and triggered sanctions on Russian exports. This volatility has placed immense pressure on manufacturers' profit margins, many of whom operate with thin cushions due to competitive pricing structures. Smaller manufacturers, lacking economies of scale, have been disproportionately affected, with several opting to reduce product lines or exit niche segments altogether. Furthermore, the transition toward lightweight yet high-strength materials for portable safes has introduced reliance on specialized metals like titanium and carbon fiber composites, which carry even greater price instability.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| CAGR | 4.90 % |

| Segments Covered | By Voltage Rating , Cooling Method,Phase Type,Mounting Type and Country. |

| Various Analyses Covered | Global, Regional, & Country Level Analysis; Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Country Covered | UK, Germany, Italy, France, Spain, Sweden, Denmark, Poland, Switzerland, Netherlands, Rest of Europe. |

| Market Leaders Profiled | CG Power & Industrial Solutions, Eaton, Elsewedy Electric, General Electric |

SEGMENT ANALYSIS

By Type Insights

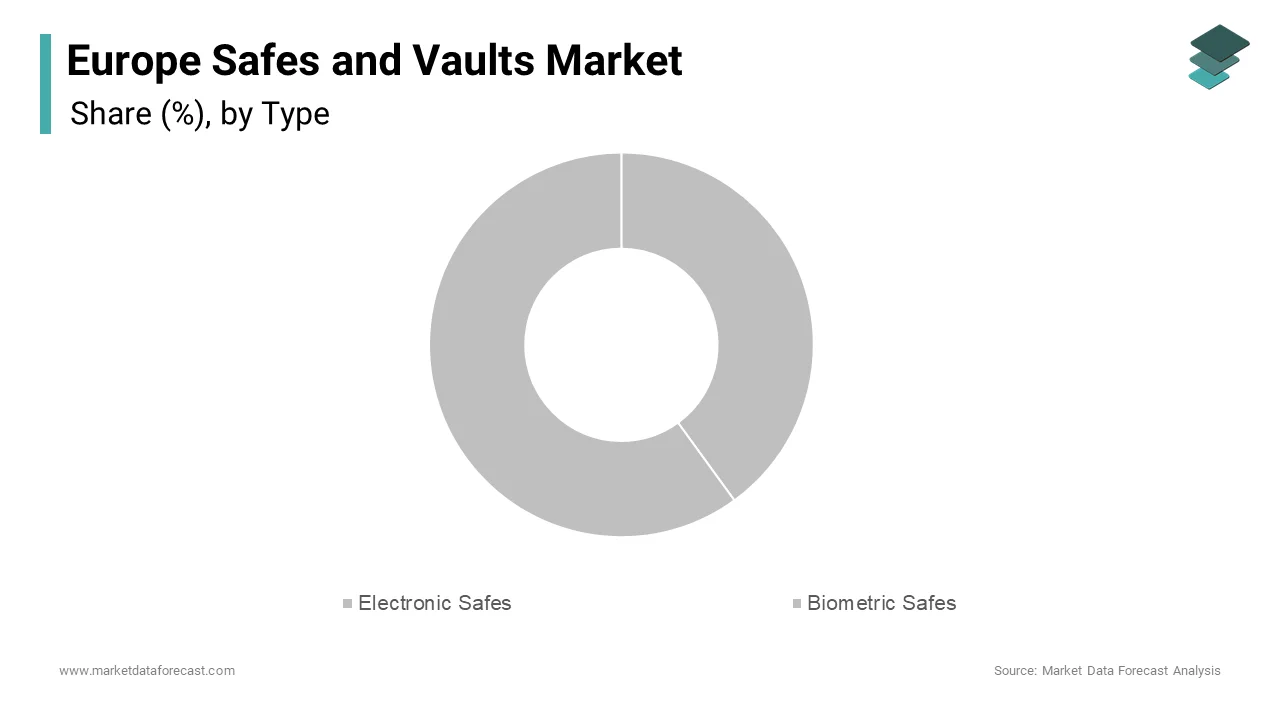

The electronic safes segment was the largest market share in the Europe safes and vaults market by accounting for a 43.3% of total revenue in 2024. This dominance is primarily driven by the growing preference for user-friendly access control systems that offer a balance between security and convenience. Unlike mechanical locks, which require physical keys or combinations, electronic safes utilize digital keypads, programmable codes, and sometimes remote monitoring capabilities—features that appeal to both residential and commercial users. The banking sector has also contributed significantly to this trend. Besides, small businesses are increasingly adopting electronic safes due to their ease of use and relatively lower cost compared to biometric alternatives.

Biometric safes represent the fastest-growing segment in the Europe safes and vaults market, projected to expand at a CAGR of 9.4% from 2025 to 2033. This rapid progress is fueled by increasing consumer demand for high-end authentication technologies that offer superior security through fingerprint scanning, facial recognition, and iris detection. These features make biometric safes particularly attractive to affluent homeowners, luxury retailers, and healthcare institutions seeking to protect high-value assets and sensitive documents. Moreover, technological advancements have reduced the cost gap between biometric and electronic safes, making them more accessible to a broader customer base.

By Function Type Insights

The vaults and vault doors constituted the biggest function type segment in the Europe safes and vaults market by holding an estimated market share of 37.2% in 2024. This influence is due to the critical role these systems play in securing high-risk environments such as banks, government institutions, military facilities, and large corporations. Vaults provide comprehensive protection against burglary, fire, and forced entry, making them indispensable in sectors where asset security is paramount. The defense sector is another major contributor, with countries like France and Italy investing heavily in reinforced vault infrastructure for ammunition and classified data storage. According to the European Defense Agency, defense-related vault procurement increased in 2022 , driven by modernization initiatives and geopolitical uncertainties. Moreover, financial institutions across the Benelux region have been retrofitting existing branches with upgraded vault doors featuring multi-factor authentication and real-time monitoring capabilities. In addition, regulatory mandates such as the ECB's guidelines on physical security have further solidified the demand for certified vault systems.

The gun safes and vaults are coming up as the swiftest expanding function type segment in the Europe safes and vaults market, registering a projected CAGR of 8.9% during the forecast period. This growth is primarily driven by tightening firearm storage regulations across several EU member states, particularly in response to rising concerns around gun violence and unauthorized access. Similarly, in Germany, the Federal Weapons Act requires all private firearms to be stored in approved safes, prompting widespread compliance-driven procurement. Beyond legal requirements, there has also been a notable rise in personal safety consciousness among European households, especially in urban areas experiencing increased crime rates.

By Application Insights

The commercial application segment spearheaded the Europe safes and vaults market by representing a 56.7% of total industry revenue in 2024. This is attributed to the extensive use of high-security safes and vaults in banking, retail, healthcare, logistics, and industrial sectors where asset protection is a core operational requirement. The retail sector has also seen significant investment in secure cash management solutions, with supermarket chains such as Carrefour and Rewe installing depository safes to streamline daily transactions and reduce exposure to theft. Furthermore, the logistics and courier services industry has expanded its use of commercial safes for transporting valuable goods, with companies like DHL and UPS adopting tamper-proof containers that comply with EN 1143-1 standards. Regulatory pressures, particularly in the pharmaceutical and defense industries, have also played a crucial role in driving demand.

The residential application segment is the quickly developing area in the Europe safes and vaults market, anticipated to grow at a CAGR of 7.6%. This is being propelled by rising personal wealth, increased home ownership, and a growing perception of vulnerability to break-ins and cyber-physical threats among private individuals. In the UK, where property crime remains a persistent concern, the British Home Security Association noted a increase in residential safe purchases in 2023 , particularly among homeowners in London and Manchester. Moreover, shifting consumer preferences toward smart home integration have spurred demand for connected residential safes. Additionally, higher disposable incomes in Nordic and Alpine regions have enabled affluent consumers to adopt premium gun and jewelry safes, further boosting market expansion.

By End User Insights

The banking sector remained the prominent end-user segment in the Europe safes and vaults market by capturing a 49.9% of total market value in 2024. This is caused by the sector’s intrinsic need for high-security infrastructure to safeguard cash reserves, confidential records, and transactional assets. Despite the rise of digital banking, physical cash handling remains a critical component of financial operations, particularly in Southern and Eastern Europe. Moreover, central banks and commercial institutions continue to invest in fortified vault systems for bullion storage and interbank transfers. Regulatory frameworks such as the ECB’s Physical Security Guidelines and the Basel Committee’s risk mitigation protocols have also intensified the demand for certified vault systems. Also, the proliferation of automated teller machines and cash-in-transit (CIT) services has created a parallel need for standardized, high-security safe compartments.

The non-banking sector is the fastest-growing end-user segment in the Europe safes and vaults market, projected to register a CAGR of 8.1%. This accelerated expansion is driven by expanding applications across diverse industries such as healthcare, defense, luxury retail, and private residences, where asset protection is becoming increasingly sophisticated and regulated. One of the primary contributors to this trend is the healthcare industry, particularly in the context of pharmaceutical storage. Hospitals and pharmacies across the EU are adopting high-security media safes and drug vaults to store controlled medications in compliance with the Falsified Medicines Directive (FMD). Similarly, the defense sector has ramped up procurement of specialized vaults for storing weapons, explosives, and classified intelligence. Additionally, luxury retailers such as Cartier and Rolex have deployed high-tech display safes in flagship stores across Paris and Milan to protect high-value merchandise from theft.

COUNTRY LEVEL ANALYSIS

Germany held the largest market share in the Europe safes and vaults market by accounting for a 22.1% of total regional revenue in 2024. The country's prominence is underpinned by its strong industrial base, stringent regulatory environment, and high levels of investment in banking and defense infrastructure. As a manufacturing hub for high-security products, Germany is home to leading companies such as Dormakaba, Hufschmied, and Burg Wächter, which drive innovation and export activity across Europe. Additionally, the defense industry has seen a resurgence in vault procurement. The residential segment is also growing, with a notable increase in home safe purchases since 2021, linked to rising property crime rates in urban centers like Berlin and Munich. Moreover, Germany’s implementation of strict firearm storage laws has boosted demand for certified gun safes, particularly in rural areas.

The United Kingdom is a strong demand amid post-brexit volatility. The country's market strength is shaped by economic uncertainty following Brexit, rising inflation, and a historically high incidence of property crimes, which have collectively driven demand for secure storage solutions. Additionally, the banking sector remains a key buyer, with institutions like Barclays and HSBC enhancing ATM security through next-generation cash safes. Post-Brexit trade disruptions have also influenced procurement strategies, with many firms opting for locally manufactured safes to avoid supply chain delays. Furthermore, the UK’s Firearms Act mandates the use of certified gun safes for licensed owners, contributing to steady demand in the residential segment.

France occupies a notable position in the Europe safes and vaults market. The country's market dynamics are primarily shaped by stringent regulatory requirements across banking, defense, and public administration sectors, which mandate the use of certified security solutions. The luxury retail sector, concentrated in Paris, has also emerged as a key adopter of high-tech display safes, with brands such as Louis Vuitton and Cartier deploying RFID-enabled units to protect high-value merchandise. Regulatory enforcement in the firearms sector has further bolstered demand.

Italy sees rising crime rates and traditional cash reliance fuel growth. The regional market is driven by persistently high cash usage, rising crime rates, and a robust retail sector that demands secure storage solutions. This has led to greater adoption of depository and wall safes among local merchants. Additionally, the banking sector remains a key investor. The defense and pharmaceutical industries have also contributed to market growth, with the Ministry of Health mandating the use of certified media safes for storing controlled substances.

Spain is supported by rising urbanization, expanding retail infrastructure, and growing awareness of personal and commercial security. The country has witnessed year-over-year increase in reported theft incidents between 2021 and 2023, prompting households and businesses alike to invest in secure storage solutions. The Spanish banking sector remains a key consumer, with BBVA and Banco Santander integrating advanced vault systems into new branch designs to comply with ECB security mandates. Additionally, the retail industry has seen a surge in demand for cash management safes, particularly among supermarket chains. Homeownership trends and rising disposable incomes in coastal regions like Barcelona and Valencia have also contributed to the residential segment’s expansion.

KEY MARKET PLAYERS AND COMPETITIVE LANDSCAPE

Companies playing a prominent role in the europe safes and vaults market are Gunnebo AB, ASSA ABLOY Group, dormakaba Group, Chubbsafes, Fichet-Bauche, Diebold Nixdorf, Godrej & Boyce Manufacturing Company Limited, Juwel Safes, Bordogna Group, Wittkopp Safe and Key Company, SMP Security Corporation, Burg-Wächter

The competition in the Europe safes and vaults market is characterized by a mix of established global players and niche regional manufacturers vying for dominance through differentiation in technology, product design, and service offerings. While large corporations leverage economies of scale and brand recognition to maintain market leadership, smaller firms focus on customization, specialized applications, and cost-effective solutions to capture segment-specific demand. The market remains highly fragmented, with intense rivalry observed particularly in countries like Germany, France, and the UK, where security consciousness is high and regulatory compliance stringent. Manufacturers are continuously innovating to integrate digital technologies such as biometrics and smart connectivity into traditional safe systems, aiming to align with evolving consumer preferences. Additionally, the emphasis on certification and adherence to European safety standards plays a crucial role in shaping competitive dynamics.

Top Players in the Market

Dormakaba Group

Dormakaba is a leading global provider of security solutions, with a strong presence in the European safes and vaults market. The company offers an extensive range of high-security products including electronic and biometric safes, modular vault systems, and secure access solutions for commercial and institutional clients. With its headquarters in Switzerland, Dormakaba combines advanced engineering with innovation to cater to diverse sectors such as banking, healthcare, and government institutions. Its reputation for reliability and compliance with international security standards makes it a preferred choice across Europe.

Hufschmied Sicherheitstechnik GmbH

Hufschmied is a German manufacturer renowned for producing premium-grade safes and vault systems tailored to both residential and commercial applications. Known for superior craftsmanship and cutting-edge technology, the company specializes in burglary-resistant and fireproof safes, gun safes, and customized vault doors. Hufschmied’s focus on precision engineering and product durability has earned it a strong foothold in the European market. It serves a wide customer base, from private individuals to banks and defense organizations, reinforcing its status as a key industry player.

Burg Wächter

Burg Wächter, headquartered in Germany, is one of Europe's most recognized brands in the field of security storage solutions. The company provides a comprehensive portfolio that includes mechanical and electronic safes, media safes, deposit safes, and high-security vault systems. Burg Wächter emphasizes innovation, design, and functionality, catering to both retail and institutional markets. Its commitment to quality and continuous product development has positioned it as a trusted name across Europe and beyond, contributing significantly to the growth and evolution of the regional safes and vaults sector.

Top strategies used by the key market participants

Product Innovation and Technological Integration

Leading players in the Europe safes and vaults market are increasingly investing in research and development to introduce technologically advanced products. Companies are integrating smart features such as biometric authentication, IoT-enabled remote monitoring, and AI-based intrusion detection into traditional safe designs. These innovations not only enhance security but also improve user experience, making them highly attractive to modern consumers.

Strategic Partnerships and Collaboration

To strengthen their market position and expand their reach, key manufacturers are forming strategic alliances with distributors, system integrators, and technology providers. These collaborations help companies offer bundled security solutions that combine safes with surveillance, access control, and alarm systems. Such partnerships enable firms to meet complex client demands while enhancing brand visibility across different end-user segments.

Expansion Through Acquisitions and Geographic Penetration

Major players are actively acquiring regional manufacturers and expanding their distribution networks across emerging markets within Europe. By establishing local production units and service centers, companies can reduce costs, improve response times, and tailor products to regional regulatory requirements. This strategy supports long-term market consolidation and enhances competitive advantage in a highly fragmented industry landscape.

RECENT HAPPENINGS IN THE MARKET

In March 2024, Dormakaba announced the launch of its new line of IoT-integrated biometric safes designed specifically for high-end residential and luxury retail applications across Europe. This move reflects the company’s commitment to merging advanced security features with smart home compatibility, enhancing its appeal among affluent consumers and upscale businesses seeking seamless integration with digital ecosystems.

In June 2023, Hufschmied Sicherheitstechnik expanded its manufacturing facility in Isny, Germany, to increase production capacity for modular vault systems and certified gun safes. The expansion was aimed at meeting growing demand driven by stricter firearm storage laws and rising institutional procurement, positioning the company to better serve both public and private sector clients across the continent.

In February 2024, Burg Wächter partnered with a leading cybersecurity firm to develop a new generation of encrypted digital locking systems for safes used in financial institutions and data centers. This collaboration underscores the company’s effort to address emerging threats by combining physical security with robust cyber protection, thereby strengthening its value proposition in critical infrastructure sectors.

In September 2023, a major European distributor of security equipment entered into a long-term supply agreement with a prominent safe manufacturer to exclusively distribute its ECB-S certified products across Southern Europe. This partnership was intended to consolidate market presence and ensure consistent product availability in regions experiencing heightened demand due to rising crime rates and regulatory mandates.

In May 2024, a leading provider of integrated security solutions acquired a niche French company specializing in high-security media safes for pharmaceutical and archival storage. This acquisition enabled the buyer to broaden its portfolio and tap into regulated sectors requiring compliance with EU directives on controlled substances and document preservation, reinforcing its position as a diversified security solutions provider.

MARKET SEGMENTATION

This research report on the europe safes and vaults market has been segmented and sub-segmented into the following categories.

By Type

- Electronic Safes

- Biometric Safes

By Function Type

- Vaults and Vault Doors

- Gun Safes and Vaults

By Application

- Commercial Application

- Residential Application

By End User

- Banking Sector

- Non-Banking Sector

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe.

Frequently Asked Questions

What factors are driving the growth of the safes and vaults market in Europe?

Key drivers include increasing crime rates, rising adoption of digital security solutions, growing awareness of home security, the expansion of the financial and banking sector, and the need for secure storage in commercial establishments like hotels, retail, and healthcare.

Which countries dominate the safes and vaults market in Europe?

Major markets include Germany, the United Kingdom, France, Italy, and Spain, with Germany leading due to its strong financial sector, advanced manufacturing capabilities, and high-security awareness.

What are the latest trends in the Europe safes and vaults market?

Key trends include smart safes with biometric authentication, IoT-enabled security systems, advanced fireproof and waterproof safes, and increasing integration of AI for predictive security management.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com