Europe Scaffolding Market Size, Share, Trends, & Growth Forecast Report By Type( Supported Scaffolding, Suspended Scaffolding, Rolling Scaffolding), Material, Application and Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic and Rest of Europe), Industry Analysis From 2026 to 2034

Market Size, 2025

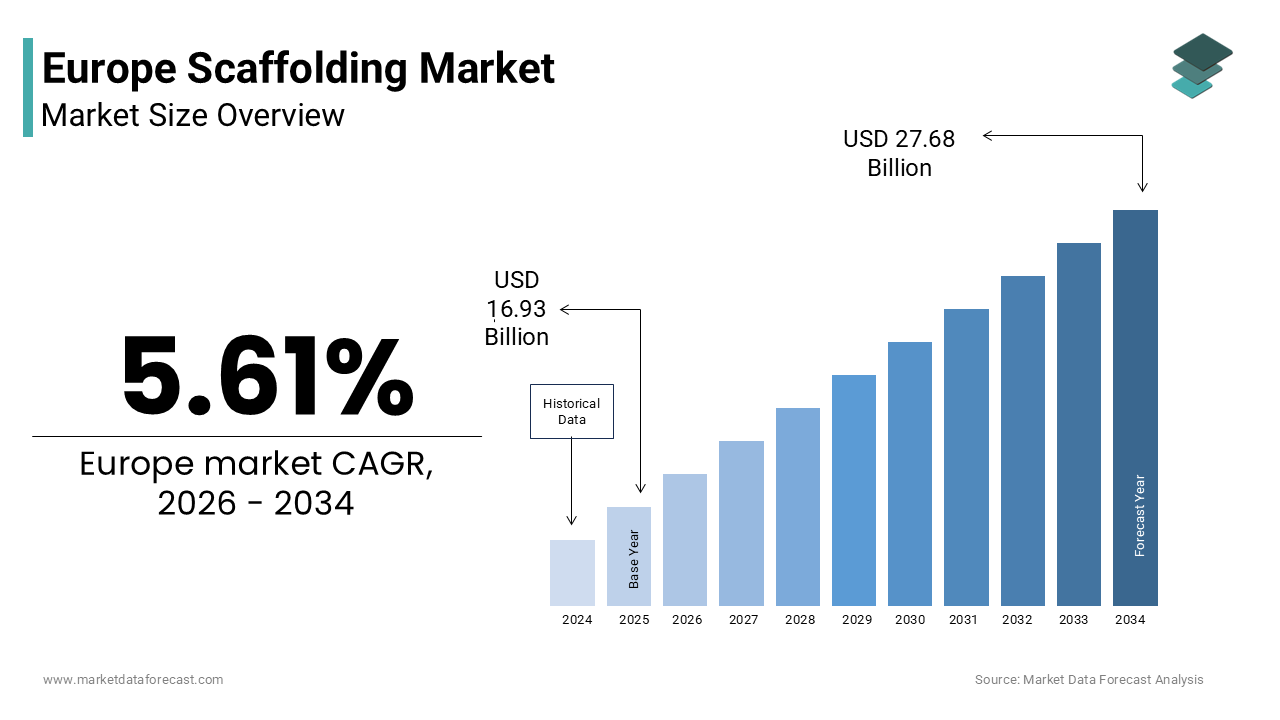

$16.93 BnMarket Estimate, 2026

$17.88 BnMarket Forecast, 2034

$27.88 BnCAGR, 2026–2034

5.61%Europe Scaffolding Market Report Summary

The Europe scaffolding market was valued at USD 16.93 billion in 2025, is estimated to reach USD 17.88 billion in 2026, and is projected to reach USD 27.68 billion by 2034, growing at a CAGR of 5.61% during the forecast period from 2026 to 2034. The growth of the Europe scaffolding market is driven by large-scale façade renovation programs, infrastructure modernization projects, and stringent occupational safety regulations emphasizing certified temporary access structures. Increasing adoption of modular scaffolding systems designed for rapid assembly, reusability, and compliance with EN 12811 safety standards is further fueling market growth. Moreover, urban densification, integration of digital planning tools such as BIM for scaffold design, and growing preference for lightweight aluminum systems are strengthening scaffolding demand across residential, commercial, and industrial construction activities throughout Europe.

Key Market Trends

-

Rising demand for scaffolding systems driven by Europe’s Renovation Wave Strategy promoting building energy efficiency upgrades and façade restoration.

-

Increasing adoption of modular and lightweight aluminum scaffolding solutions enabling faster assembly and improved worker ergonomics.

-

Growing integration of BIM-enabled scaffold planning tools supporting precise configuration, material optimization, and clash detection.

-

Expanding use of scaffolding across transport infrastructure, bridge rehabilitation, and large-scale public works projects.

-

Strengthening focus on worker safety and compliance with stringent European construction safety regulations driving certified system scaffold adoption.

Segmental Insights

- Based on material, the steel scaffolding segment was the largest and held a significant share of the Europe scaffolding market in 2025. The segment’s dominance is attributed to high load-bearing capacity, durability, and suitability for heavy-duty construction, infrastructure, and industrial maintenance applications.

- Based on type, the supported scaffolding segment accounted for a prominent share of the Europe scaffolding market in 2025. Supported systems remain widely preferred due to structural stability, versatility across building heights, and compatibility with diverse construction and façade maintenance requirements.

- Based on application, the commercial segment was the largest, capturing 48.3% of the Europe scaffolding market share in 2025. Frequent façade maintenance, renovation mandates, and expansion of commercial real estate infrastructure continue to drive sustained scaffolding demand within this segment.

Regional Insights

The Europe scaffolding market is demonstrating steady expansion across major economies, supported by renovation initiatives, infrastructure investment, and strong regulatory emphasis on construction safety.

-

Germany was the largest contributor to the Europe scaffolding market, driven by extensive renovation programs, advanced construction technology adoption, and a strong domestic scaffolding manufacturing base.

-

France and Italy continue to perform strongly, supported by historic building restoration requirements, urban redevelopment projects, and government-backed energy retrofit initiatives.

-

The United Kingdom demonstrates stable demand, fueled by infrastructure upgrades, transport maintenance activities, and strict safety compliance requirements.

-

Nordic and Central European markets are witnessing gradual growth, supported by modernization of construction practices and increasing adoption of modular and digital scaffolding solutions.

Competitive Landscape

The Europe scaffolding market is characterized by the presence of established engineering firms, rental specialists, and modular system innovators competing on safety compliance, modular design capability, and digital integration features. Leading companies are focusing on lightweight materials, BIM-compatible scaffold solutions, and rental-based service models to enhance operational flexibility and lifecycle efficiency. Strategic partnerships with construction contractors, investments in smart scaffold technologies, and alignment with circular economy principles are strengthening competitive positioning across the region. Prominent players in the Europe scaffolding market include PERI Group, Altrad Group, ULMA Construction, BrandSafway, Wilhelm Layher GmbH & Co. KG, Atlantic Pacific Equipment (AT-PAC) LLC, ADTO Group, MJ-Gerüst GmbH, Waco International, Doka GmbH, Bilfinger SE, HAKI AB, Scafom-Rux, and Hünnebeck.

Europe Scaffolding Market Size

The Europe scaffolding market size was valued at USD 16.93 billion in 2025 and is anticipated to reach USD 17.88 billion in 2026 from USD 27.68 billion by 2034, growing at a CAGR of 5.61% during the forecast period from 2026 to 2034.

Scaffolding refers to a temporary support structure or system used to help complete a task that would otherwise be difficult or impossible. Unlike generic work platforms, modern European scaffolding is engineered to meet stringent safety, load-bearing, and wind-resistance standards under EN 12811 and national regulations. These systems are increasingly designed for rapid assembly, reusability, and integration with digital planning tools to enhance site efficiency. According to Eurostat, production in the EU construction sector in 2024 showed signs of stagnation, with a 2.0% decrease in construction output in September 2024 compared to the previous year, suggesting a cautious market rather than a consistent boom. Despite this, the high prevalence of specialized construction work ensures a steady demand for professional, certified scaffolding systems. Furthermore, as per research, falls from height remain the leading cause of fatal accidents in construction, accounting for a portion of all occupational fatalities, thereby reinforcing regulatory emphasis on certified scaffolding systems. The market is also shaped by urban densification, which necessitates compact, high-rise compatible scaffolds for façade renovation in historic city centers. Consequently, scaffolding in Europe functions not merely as a temporary structure but as a critical safety and productivity enabler in the continent’s evolving built environment.

MARKET DRIVERS

Large Scale Urban Façade Renovation and Energy Efficiency Mandates

The region’s aggressive building renovation agenda, driven by climate policy and aging infrastructure, is a big engine for the growth of the Europe scaffolding market. The EU’s Renovation Wave Strategy intends to significantly accelerate the annual frequency of building energy upgrades, prioritizing extensive envelope improvements like insulation and window replacements that necessitate the use of external access equipment. According to European authorities, a vast majority of existing structures fail to meet modern energy standards, prompting national initiatives like Germany’s efficiency programs to fund a high volume of building envelope improvements. In historic urban centers such as Paris, Rome, and Prague, strict heritage preservation laws mandate non invasive access methods, favoring modular system scaffolds that minimize structural contact. Municipal authorities in Paris have designated substantial financial resources to support the aesthetic and thermal restoration of historic residential blocks, leading to a consistent demand for professional scaffolding installations across the city. This wave of mandated urban renewal ensures sustained, high volume demand for adaptable, code compliant scaffolding systems across Europe’s dense metropolitan corridors.

Infrastructure Modernization and Public Investment in Transport Projects

Significant public investment in transport and civil infrastructure is further propelling the expansion of the Europe scaffolding market. This is amplifying scaffolding requirements across the region. The European Investment Bank is prioritizing 2025 financing for climate-action-oriented transport infrastructure and cross-border connectivity, with a focus on rail electrification. For instance, the Brenner Base Tunnel project in the Alps utilizes custom suspended scaffolds for interior lining work at depths exceeding 1000 meters. Similarly, Network Rail utilizes specialized access equipment for maintaining overhead lines to improve safety across its rail network. Infrastructure projects, particularly bridge and viaduct repairs, are significant drivers of demand for modular scaffolding systems that increase productivity in European construction. The EU is pushing toward climate-resilient infrastructure under the Connecting Europe Facility. In this context, scaffolding remains indispensable for enabling the safe, precise, and efficient execution of large-scale public works across diverse geographies and structural complexities.

MARKET CHALLENGES

Stringent Safety Regulations and Certification Burdens

Rigorous and fragmented safety certification requirements across member states causes operational problems that restrict the growth of the Europe scaffolding market. While EN 12811 provides baseline design standards, countries impose supplementary rules. These rules affect load testing, wind resistance, and assembly protocols. German scaffolding safety rules require structural verification for non-standard, higher structures, while French regulations emphasize compliance with European standards for platform, including slip-resistance, to prevent fall accidents. Stricter safety regulations and documentation requirements in the European construction sector are increasing overall project costs and extending the time needed for scaffolding setup. German engineering firms are reporting a decline in production and orders due to a weak domestic market and high bureaucratic hurdles. Moreover, studies suggests that improper assembly remains a significant cause of scaffold accidents, leading to increased safety focus on training and stricter, albeit cost-increasing, inspection protocols. These enhanced safety measures simultaneously raise entry barriers and compress margins, particularly for smaller firms with limited compliance expertise.

Volatility in Steel Prices and Raw Material Supply Chains

Fluctuating hot rolled steel coil prices pose a major threat to the expansion of the European scaffolding market. These prices constitute a notable share of raw material costs for tubular and frame systems. Eurofer reported that imports maintained a high share of total apparent consumption in early 2025, which, combined with high energy costs, kept pressure on European steel manufacturers. This volatility directly impacts pricing stability. Scaffold tube prices have faced upward pressure due to manufacturing material cost inflation and high energy costs. Small to mid-sized manufacturers frequently struggle to manage raw material price volatility due to a lack of hedging tools, forcing them to adjust selling prices or reduce margins. Additionally, the EU’s Carbon Border Adjustment Mechanism adds indirect levies on imported steel billets, complicating sourcing strategies. Manufacturers have reported that significant material cost increases have outpaced their ability to raise prices, causing a squeeze on profitability. This external fragility not only squeezes profitability but also discourages long term investment in new product development, posing a systemic challenge to market resilience and innovation capacity.

MARKET OPPORTUNITIES

Adoption of Modular and Lightweight Aluminum Scaffolding Systems

The shift toward modular aluminum scaffolding paves the way to address urban space constraints and labor shortages across the region, which is anticipated to boost the growth of the Europe scaffolding market. Unlike traditional steel systems, aluminum scaffolds weigh less, enabling faster manual assembly and reducing the need for cranes in dense city centers. According to sources, European demand for aluminum scaffolding is experiencing a recovery, particularly in Northern European markets that prioritize lightweight, modular solutions for sustainable construction and renovation projects. Companies like Layher and PERI have introduced plug and play components that cut setup time compared to tube and coupler alternatives. Lightweight aluminum scaffolding is widely recognized as reducing the physical exertion required for manual handling, transport, and assembly compared to traditional steel, contributing to a lower risk of fatigue-related musculoskeletal injuries for workers. Furthermore, their full recyclability aligns with the EU Circular Economy Action Plan, which encourages reusable construction products. Lightweight modular systems are transforming European construction, providing a sustainable, human-centered alternative to traditional methods amid accelerating urban projects and skilled labor shortages.

Integration of Digital Planning and BIM-Enabled Scaffold Design

The convergence of scaffolding with Building Information Modeling and digital twin technologies is opening new efficiencies in planning, logistics, and safety compliance, which is expected to fuel the expansion of the Europe scaffolding market. Leading providers now offer BIM libraries that allow engineers to simulate scaffold configurations directly within architectural models, identifying clashes and optimizing material use before deployment. European Commission directives and national policies increasingly require Building Information Modeling (BIM) on public projects, which is accelerating the adoption of digital tools for temporary structures like scaffolding. The use of PERI's VARIOKIT system with 3D modeling and BIM allows for improved planning and precise component scheduling, which reduces on-site material waste during complex retrofitting projects. Similarly, ULMA's utilization of BIM-integrated systems on major infrastructure works like metro stations has been shown to improve the efficiency of engineering reviews and project planning. The Digital Europe Programme (2021-2027) provides funding to support the deployment of digital technologies, including AI, cloud, and data tools, aimed at strengthening digitalization across industries, including construction. This integration transforms scaffolding from a physical commodity into a data driven service, enhancing precision, reducing rework, and strengthening alignment with Europe’s broader vision for intelligent, resource efficient construction.

MARKET CHALLENGES

Fragmented National Standards for High Rise and Wind Load Performance

Disparities in national interpretations of wind load and high rise scaffold standards create significant technical and commercial friction, which negatively impacts the growth of the Europe scaffolding market. EN 12811 defines general stability criteria. However, countries apply divergent safety factors and testing methodologies for tall structures. For example, European countries, including the UK and Italy, adhere to specific national deviations for structural validation of scaffolding under wind and load conditions based on Eurocode standards, rather than a single, universal mandate. Divergent national annexes to European standards for scaffolding wind resistance create inconsistencies, resulting in additional engineering analyses for cross-border projects. Cross-border contractors in Europe experience increased costs and reduced productivity due to divergent national compliance, documentation, and safety regulations. This fragmentation delays time to market, inflates design expenses, and discourages pan European bidding, particularly for SMEs lacking in house structural engineers. Europe’s scaffolding sector is currently facing a regulatory patchwork that impedes scalability and competitiveness. This will continue until deeper alignment is achieved through initiatives like the Single Market Enforcement Action Plan.

Shortage of Certified Scaffold Erectors and Assemblers

The acute shortage of trained and certified erectors is among the major factors inhibiting the expansion of the Europe scaffolding market. This shortage is particularly severe for complex system scaffolds used in high-rise and industrial settings. The European construction sector is experiencing significant, widespread labor shortages across many Member States, with high demand for skilled professionals causing intensified recruitment difficulties for specialized craft roles. A large number of construction contractors across Europe are reporting project delays driven by significant shortages of qualified personnel, which are causing longer wait times for specialized work teams in urban areas. Vocational education pipelines have failed to keep pace. The availability of specialized training for scaffolding assembly in European vocational schools is limited, with some industry reports suggesting a shortage of formalized education programs to address the growing demand for certified scaffolding workers. This skills mismatch inflates labor costs, certified erectors earn more than general laborers, and increases safety risks from improper assembly. Without coordinated upskilling initiatives aligned with EN 12811 competencies, this human capital gap will continue to undermine project timelines. Furthermore, it will negatively impact safety outcomes and overall market efficiency across Europe.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 5.61% |

| Segments Covered | By Type, Material, Application and Region |

| Various Analyses Covered | Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

| Countries Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, the Netherlands, Turkey, the Czech Republic, and the Rest of Europe. |

| Market Leaders Profiled | PERI Group, Altrad Group, ULMA Construction, BrandSafway, Wilhelm Layher GmbH & Co. KG, Atlantic Pacific Equipment (AT-PAC), LLC, ADTO Group, MJ-Gerüst GmbH, Waco International, Doka GmbH, Bilfinger SE, HAKI AB, Scafom-Rux, and Hünnebeck. |

SEGMENTAL ANALYSIS

By Material Insights

The steel scaffolding segment held the majority share of the Europe scaffolding market in 2025. The supremacy of the segment is attributed to its unmatched load bearing capacity, durability, and cost effectiveness for large scale and long duration projects. Steel tube and coupler scaffolding is frequently utilized for high-rise and heavy industrial construction because, when engineered, it offers high strength and versatility for supporting significant live loads. Steel scaffolding is a preferred, heavily used, and durable material for large-scale infrastructure projects, such as bridges and industrial plants, owing to its high strength, ability to withstand significant loads, and suitability for complex, high-exposure environments. In Germany, safety regulations (DGUV) mandate rigorous, standardized structural validation for scaffolding to ensure safety in construction, with steel being a common, durable choice for high-rise access. Additionally, the established recycling infrastructure, a significant portion of construction steel is recovered post use, enhances its sustainability profile. The widespread availability of certified fabricators and rental fleets across Europe further cements steel as the backbone of professional scaffolding operations, particularly in sectors where safety and reliability outweigh weight considerations.

The aluminum scaffolding segment is anticipated to witness the fastest CAGR of 7.9% during the forecast period due to demand for lightweight, rapid assembly solutions in urban renovation and confined spaces. Weighing less than steel equivalents, aluminum systems reduce manual handling injuries and eliminate the need for cranes in dense city centers. Musculoskeletal disorders are a primary work-related health problem in the European construction sector, leading contractors to adopt lighter, more ergonomic materials to reduce physical strain. In historic districts like Amsterdam’s Canal Ring and Prague’s Old Town, municipal regulations favor non invasive aluminum frames that minimize facade contact. Aluminum scaffolds are generally recognized in the industry to offer faster setup times and reduced worker fatigue compared to traditional steel, due to their lower weight. Driven by the EU Renovation Wave Strategy, demand for lightweight aluminum scaffolding systems is rising for facade refurbishment projects. Aluminum is becoming the preferred choice for agile, human-centered access in Europe’s evolving urban landscape. This shift is driven by the material’s full recyclability and its compatibility with modular design.

By Type Insights

The supported scaffolding segment dominated the Europe scaffolding market and accounted for a substantial share in 2025. The dominance of the segment is driven by its versatility, stability, and compliance with EN 12811 standards for ground-based access across residential, commercial, and industrial sites. Comprising vertical standards, horizontal ledgers, and transoms, supported systems can be erected to heights exceeding 50 meters with proper bracing, making them indispensable for high rise construction and façade restoration. Building renovation across major European markets frequently employs supported scaffolding due to its ability to conform to complex structural shapes. German safety regulations enforce stricter access and stability requirements as scaffolding height increases, ensuring these structures remain safe in highly controlled work environments. Rental companies maintain vast inventories of modular frame and system scaffolds, enabling rapid deployment for seasonal peaks such as spring cladding upgrades. This combination of structural reliability, regulatory acceptance, and logistical scalability ensures supported scaffolding remains the default choice for the majority of European construction and maintenance tasks.

The rolling scaffolding segment is likely to experience the fastest CAGR of 8.3% between 2026 and 2034 owing to demand for mobile, repositionable access in interior fit outs, warehouse maintenance, and retail refurbishment. Unlike fixed systems, rolling towers feature lockable casters and guardrails, enabling safe relocation without disassembly, critical for projects requiring frequent position changes. Interior contractors have experienced improved labor efficiency and faster installation times for ceiling work and lighting retrofits by utilizing modern, mobile scaffolding solutions. Rolling towers are frequently used in Dutch office renovations to provide swift, non-disruptive access to HVAC systems during energy efficiency upgrades. The adoption of composite materials in scaffolding has decreased unit weight, leading to enhanced portability and ease of maneuvering in constrained areas. Modular construction and just-in-time interior finishing are on the rise. Because of this, rolling scaffolds are becoming essential tools for agile, low-disruption workflows across Europe’s service-oriented economy.

By End User Insights

The commercial end user segment was the largest segment in the Europe scaffolding market and captured a 48.3% share in 2025. The prominence of the segment is supported by the scale and frequency of façade maintenance, window replacement, and cladding upgrades across office towers, shopping centers, and hospitality properties. The European Commission’s Renovation Wave strategy and updated EPBD directives are driving increased renovation rates for the lowest-performing commercial buildings across Europe by 2030, creating sustained demand for exterior scaffolding. Strict safety regulations regarding building maintenance in major European cities create recurring demand for facade inspection and cleaning, often necessitating the use of scaffolding, particularly to address safety risks from deterioration. A significant, consistent volume of façade maintenance projects occurs in Paris, frequently requiring scaffolding for multiple weeks for repairs, cleaning, and painting. Additionally, the rapid expansion of logistics and e-commerce fulfillment centers across Europe continues to drive demand for interior scaffolding to support roofing, cladding, and racking system installations. This blend of regulatory mandates, asset management cycles, and infrastructure growth ensures the commercial segment remains the cornerstone of scaffolding utilization across Europe.

The industrial end user segment is on the rise and is expected to be the fastest growing segment in the market by witnessing a CAGR of 9.1% over the forecast period. The swift expansion of the segment is fuelled by infrastructure modernization, energy transition projects, and stringent safety protocols in complex environments. Industrial facilities, including refineries, power plants, and chemical processing units, require specialized scaffolding that meets ATEX explosion proof standards and supports heavy tooling at height. The European Investment Bank significantly increased financing for energy infrastructure in 2025, supporting the transition with investments in hydrogen, battery production, and grid improvements. Chemical and technology companies in Germany are enhancing safety during reactor maintenance by implementing modular scaffolding systems that incorporate fall protection The European Agency for Safety and Health at Work mandates that all industrial scaffolds undergo third party load testing, favoring engineered solutions from certified providers. Europe is accelerating its decarbonization agenda. Consequently, industrial scaffolding is becoming a critical enabler of safe, compliant, and efficient execution in high-risk technical environments.

REGIONAL ANALYSIS

Germany Scaffolding Market Analysis

Germany dominated the Europe scaffolding market and accounted for a 24.7% share in 2025. The growth of German market is credited to its massive construction volume and stringent safety regulations that mandate high-quality access solutions. Modular system scaffolding is strongly preferred over traditional tube and fitting methods in this region. This reflects a, industry-wide focus on efficiency and worker safety. A key driving factor is the extensive energy retrofitting program known as the Building Energy Act, which requires millions of existing structures to be upgraded with insulation and new facades, creating sustained demand for exterior access systems. Data from the German Construction Industry Federation indicates that the renovation sector accounted for a notable share of total construction output in 2024, directly fueling the need for reliable scaffolding structures. Furthermore, the severe shortage of skilled labor has accelerated the adoption of lightweight and easy-to-assemble systems that reduce erection time and physical strain on workers. As per reports from the Federal Institute for Occupational Safety and Health, compliance with rigorous fall protection standards has made system scaffolding the default choice for a considerable share of commercial projects. The presence of major domestic manufacturers like PERI and Doka ensures a continuous supply of innovative products tailored to local regulatory requirements. This combination of regulatory pressure, renovation mandates, and technological leadership solidifies Germany's position as the dominant force in the regional landscape.

United Kingdom Scaffolding Market Analysis

The United Kingdom was the next prominent country in the Europe scaffolding market and captured a share of 17.9% in 2025. This position of the UK market is attributed to its unique reliance on tube and fitting scaffolding which offers unparalleled flexibility for complex heritage structures and dense urban environments. The country’s market has a robust rental ecosystem where major hire companies dominate the supply chain, catering to both large infrastructure projects and small residential repairs. The government's commitment to massive infrastructure projects, including significant transport and housing investments via the National Infrastructure Strategy, drives the need for extensive temporary access solutions. Studies reveal that the sector faces a critical skills gap, prompting a shift towards prefabricated scaffold components that can be installed quickly by smaller crews. The strict enforcement of the Work at Height Regulations 2005 continues to drive demand for certified equipment and regular inspection services, ensuring a steady revenue stream for service providers. Reports from the National Access & Scaffolding Confederation show that the renovation and maintenance sector is the largest end-user of scaffolding services. The focus on refurbishing the existing building stock remains the primary driver of national scaffolding activity. Additionally, the resurgence of new housing starts following planning reforms has boosted demand for residential scaffolding packages. As research, the trend toward digital monitoring of scaffold integrity using IoT sensors is gaining traction among top-tier contractors, enhancing safety and operational efficiency across the country.

France Scaffolding Market Analysis

France is also a key player in the Europe scaffolding market by serving as a critical hub for large-scale public works and nuclear facility maintenance projects. This region's market features a balance of standard system scaffolding and specialized, heavy-duty industrial solutions. One of the major growth factors is the ambitious national renovation wave aimed at improving the energy efficiency of public buildings and private homes, supported by significant state subsidies like MaPrimeRénov. The nuclear energy sector also contributes uniquely to the market, as the periodic maintenance and life-extension programs for the country's fleet of reactors necessitate highly engineered scaffolding systems capable of withstanding harsh environments. According to the Ministry of Ecological Transition, the national push for sustainable construction has increased the popularity of aluminum scaffolding. Its durability and recyclability make it a preferred choice for companies aiming to reduce their environmental impact. Furthermore, the strict adherence to European safety standards EN 12811 ensures that only certified equipment is used on French job sites, driving consolidation among suppliers who can guarantee compliance. As per sources, the rental landscape continues to grow as contractors prefer to avoid capital expenditure on assets that require significant storage and maintenance, reinforcing the dominance of major rental houses in the national supply chain.

Italy Scaffolding Market Analysis

Italy is moving ahead steadily in the Europe scaffolding market. It is renowned for its specialized demand driven by the preservation of historical monuments and a vibrant residential construction sector. The market is distinct because it demands bespoke scaffolding solutions designed to protect delicate, centuries-old facades while accommodating the irregular, complex architecture of historic city centers. A key driving factor is the Superbonus tax incentive scheme, which, despite recent modifications, has left a legacy of extensive building rehabilitation projects that continue to drive demand for access equipment through 2024 and beyond. Statistics from the Italian National Institute of Statistics (ISTAT) show that the renovation sector continues to represent a major portion of total construction activity. This sustained focus on modernizing existing stock drives a high and consistent volume of scaffolding rentals and sales. The tourism industry also plays a crucial role, as constant maintenance of historical sites and churches requires delicate and often visually unobtrusive scaffolding systems. Observations from the National Association of Builders (ANCE) indicate a growing demand for lightweight aluminum scaffolding systems. Contractors are increasingly favoring these materials to minimize structural loads when working on older, fragile heritage buildings. Furthermore, the seismic retrofitting of buildings in earthquake-prone regions has created a niche market for heavy-duty shoring and access combinations. Studies emphasize that regulations promoted by industry bodies have made the integration of safety nets and debris containment systems effectively mandatory on urban sites. This requirement adds value to standard scaffolding packages and drives local manufacturers to innovate better containment solutions.

Spain Scaffolding Market Analysis

Spain is likely to grow significantly in the Europe scaffolding market from 2026 and 2034 by functioning as a dynamic growth market fueled by a recovery in residential construction and massive investments in renewable energy infrastructure. The market status in this region is defined by a rapid shift from traditional methods to modern system scaffolding as international contractors bring advanced practices to large-scale solar and wind farm projects. A major driving factor is the National Integrated Energy and Climate Plan, which mandates the installation of gigawatts of new renewable capacity, requiring extensive scaffolding for the construction of solar panel mounting structures and wind turbine maintenance. A study indicates that non-residential construction activity is expanding, largely driven by a surge in renewable energy projects and public infrastructure upgrades. The coastal tourism sector also drives seasonal demand for scaffolding related to hotel renovations and beachfront promenade repairs, creating a cyclical but predictable market pattern. According to the Ministry of Transport, Mobility and Urban Agenda, the national push for urban regeneration in major cities like Madrid and Barcelona has created a strong demand for specialized facade access systems. These projects require equipment that can strictly comply with modern safety and accessibility norms. Furthermore, the increasing adoption of rental models by small and medium-sized enterprises helps mitigate high initial costs, expanding the addressable market. Research suggests that the emphasis on worker safety and updated national regulations is reducing the use of non-compliant, legacy equipment. This trend favors established rental companies with certified, up-to-date fleets over smaller, informal operators.

COMPETITIVE LANDSCAPE

The competition in the Europe scaffolding market is characterized by a blend of established engineering houses, regional rental specialists, and agile digital enablers vying for dominance across residential, commercial, and industrial segments. Global leaders leverage decades of structural expertise and integrated digital platforms to offer certified, high rise compatible systems, while smaller firms compete through localized service, rapid delivery, and cost efficiency. Intense rivalry centers on safety compliance, weight reduction, and digital integration, particularly as urban renovation projects demand faster, lighter, and smarter access solutions. Regulatory fragmentation—especially in wind load and high rise certification—creates uneven playing fields that favor companies with robust engineering resources. Simultaneously, the shift from ownership to rental models is reshaping customer expectations toward full service provision and lifecycle support. This multifaceted environment rewards technical excellence, policy alignment, and user centric innovation, making the market both highly competitive and rich with opportunity for differentiated value creation rooted in safety, sustainability, and digital intelligence

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the Europe scaffolding market include

- PERI Group

- Altrad Group

- ULMA Construction

- BrandSafway

- Wilhelm Layher GmbH & Co. KG

- Atlantic Pacific Equipment (AT-PAC), LLC

- ADTO Group

- MJ-Gerüst GmbH

- Waco International

- Doka GmbH

- Bilfinger SE

- HAKI AB

- Scafom-Rux

- Hünnebeck

Top Players in the Europe Scaffolding Market

PERI Group

PERI Group is a German engineering leader in formwork and scaffolding systems with extensive operations across Europe and global influence in high rise and infrastructure projects. The company specializes in modular aluminum and steel scaffolding engineered for rapid assembly, safety, and integration with digital planning tools. It also expanded its rental fleet with smart scaffolds embedded with load sensors and tilt detectors to enhance real time safety monitoring on construction sites. Through partnerships with major contractors like Vinci and Skanska, PERI delivers customized solutions for urban renewal and industrial maintenance across the EU. These initiatives reinforce its global reputation for innovation while strengthening its leadership in Europe’s digitizing and sustainability driven scaffolding landscape.

Layher GmbH & Co KG

Layher is a renowned German manufacturer of modular scaffolding systems, celebrated for its Allround Scaffolding platform used in historic restoration, industrial plants, and stadium construction across Europe. The company combines precision engineering with lightweight aluminum alloys to deliver structures that meet stringent EN 12811 standards while reducing manual handling risks. It also enhanced its digital planning suite to enable clash detection and automated component lists within Revit and ArchiCAD environments. By prioritizing material efficiency, heritage compatibility, and digital interoperability, Layher strengthens its position as a trusted partner for complex urban and cultural projects while exporting its engineering excellence to global markets.

ULMA Construction

ULMA Construction, headquartered in Spain, is a key innovator in integrated scaffolding and formwork solutions serving commercial, industrial, and infrastructure sectors across Southern and Central Europe. The company emphasizes speed, safety, and sustainability through its modular frame systems designed for high wind resistance and rapid deployment. It also partnered with public housing authorities in Portugal and Italy to support façade energy retrofit programs under the EU Renovation Wave Strategy. By combining lean logistics, digital traceability, and policy aligned solutions, ULMA enhances productivity and regulatory compliance for contractors navigating Europe’s evolving construction landscape

Top Strategies Used by the Key Market Participants

Key players in the Europe scaffolding market pursue several strategic imperatives to maintain competitiveness and align with regional priorities. First they invest in modular and lightweight aluminum systems to reduce manual handling injuries and accelerate assembly in dense urban environments. Second they integrate digital tools such as BIM libraries QR code tracking and load sensors to enhance planning accuracy safety monitoring and compliance. Third they adopt circular economy principles through use of recycled materials design for disassembly and closed loop rental models. Fourth they expand service offerings including engineering support training and on site supervision to strengthen customer retention and project success. Fifth they align product development with EU policy frameworks such as the Renovation Wave Strategy and Energy Performance of Buildings Directive to capture public and commercial retrofit demand. These strategies collectively enable companies to differentiate beyond hardware and respond effectively to Europe’s unique regulatory technological and sustainability landscape.

RECENT MARKET DEVELOPMENTS

- In March 2025, PERI Group launched its updated VARIOKIT scaffolding system with BIM enabled components that reduce material waste by twenty two percent in European façade retrofit projects.

- In October 2024, Layher GmbH introduced its EcoFrame series made from ninety five percent recycled aluminum to align with EU circular economy regulations and reduce environmental impact.

- In February 2025, ULMA Construction rolled out its SmartScaffold platform featuring QR coded components for real time inventory and compliance tracking on construction sites across Europe.

- In July 2024, PERI expanded its rental fleet with smart scaffolds embedded with load sensors and tilt detectors to enhance real time safety monitoring on high risk job sites.

- In May 2025, Layher enhanced its digital planning suite to enable automated component lists and clash detection within Revit and ArchiCAD for European architectural and engineering firms.

MARKET SEGMENTATION

This research report on the Europe Scaffolding Market has been segmented and sub-segmented based on the following categories.

By Type

- Supported Scaffolding

- Suspended Scaffolding

- Rolling Scaffolding

By Material

- Steel

- Aluminum

- Wood

- Others

By Application

- Construction Industry

- Electrical Maintenance

- Temporary Stage

- Others

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

What is scaffolding used for in Europe?

Scaffolding is used to provide temporary structural support and safe working platforms for construction, maintenance, and repair activities.

What is driving the growth of the Europe scaffolding market?

Market growth is driven by increasing construction activities, infrastructure modernization projects, and rising renovation and maintenance work across Europe.

What are the main types of scaffolding used in Europe?

Supported scaffolding, suspended scaffolding, and rolling scaffolding are the primary types widely used.

Which materials are commonly used in scaffolding systems?

Steel, aluminum, wood, and composite materials are commonly used due to their strength and durability.

Which industries primarily use scaffolding solutions?

Construction, industrial maintenance, shipbuilding, energy, and event staging industries are major users.

How does aluminum scaffolding benefit construction projects?

Aluminum scaffolding is lightweight, corrosion-resistant, and easy to assemble, making it suitable for mobile and short-term applications.

What safety regulations affect scaffolding use in Europe?

European construction safety standards and occupational health regulations govern scaffolding design, installation, and operation.

.What role does scaffolding play in industrial maintenance?

Scaffolding enables safe access to elevated equipment and structures during inspection, repair, and maintenance operations.

What challenges affect the Europe scaffolding market?

High labor costs, strict safety compliance requirements, and raw material price fluctuations are key challenges.

Which countries are major scaffolding markets in Europe?

Germany, the UK, France, Italy, and Spain represent major regional markets.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com