Europe Security Tokens Market Size, Share, Growth, Trends, And Forecasts Report, Segmented By By Offering, Type, Application, End-User And By Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic & Rest of Europe), Industry Analysis From 2026 to 2034

Europe Security Tokens Market Report Summary

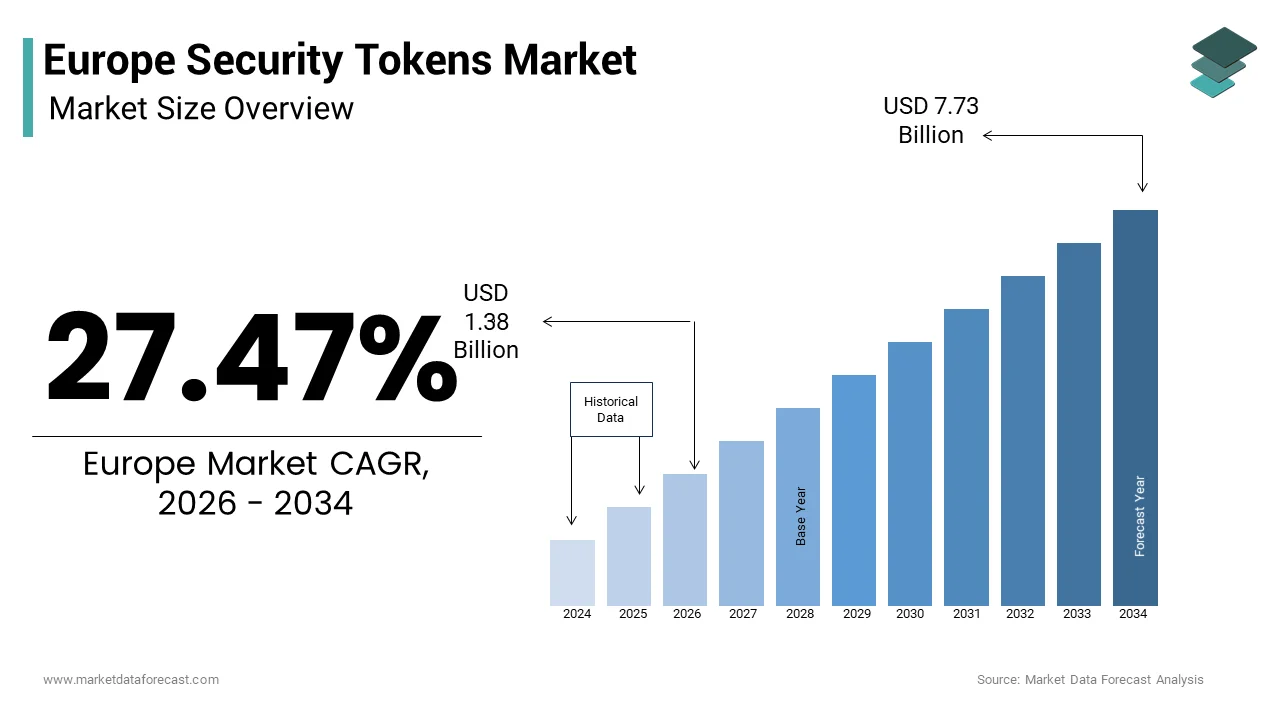

The Europe security tokens market was valued at USD 1.08 billion in 2025 and is estimated to reach USD 1.38 billion in 2026, eventually expanding to USD 7.73 billion by 2034, growing at a CAGR of 27.47% during the forecast period from 2026 to 2034. The market is witnessing rapid expansion due to the increasing adoption of blockchain technology in financial services, rising demand for tokenized securities, and the growing need for transparent and efficient capital market infrastructure. Security tokens are gaining traction across Europe as they enable fractional ownership, improved liquidity, and regulatory-compliant digital asset trading. Additionally, supportive regulatory frameworks, institutional participation, and the emergence of regulated digital asset exchanges are further accelerating the growth of the security tokens market in the region.

Key Market Trends

- Growing adoption of blockchain-based tokenization to digitize traditional assets such as equities, real estate, and bonds.

- Increasing institutional participation in digital asset markets, particularly from banks, asset managers, and fintech firms.

- Expansion of regulated digital asset exchanges and trading platforms to support compliant security token offerings (STOs).

- Rising demand for fractional ownership models, enabling investors to access high-value assets with smaller investments.

- Supportive regulatory developments across European countries encouraging innovation in tokenized financial securities.

Segmental Insights

By Offering

The platform segment dominated the Europe security tokens market and accounted for 55.2% of the market share in 2025. The strong position of this segment is attributed to the growing demand for blockchain-based issuance, management, and trading platforms that enable companies to launch and manage security token offerings while ensuring regulatory compliance.

By Type

The equity tokens segment held the largest share of 42.7% in 2025. Equity tokens are widely adopted due to their ability to represent ownership in companies through blockchain-based digital assets, providing investors with enhanced liquidity, transparency, and streamlined settlement processes.

By End User

The financial institutions segment led the market with 58.6% share in 2025. Banks, investment firms, and asset managers are increasingly exploring security tokens to modernize capital markets, reduce transaction costs, and enable faster cross-border asset transfers.

Regional Insights

The Europe security tokens market is expanding steadily as countries adopt progressive regulatory frameworks and blockchain innovation initiatives.

- Germany was the leading contributor, accounting for 24.8% of the Europe security tokens market share in 2025, supported by strong fintech ecosystems and regulatory initiatives that encourage digital asset innovation.

- France held 18.4% market share in 2025, driven by government-backed fintech development programs and growing institutional interest in blockchain-based securities.

- Switzerland remains a key hub for tokenization due to its reputation as “Crypto Valley”, supported by a flexible legal framework and strong blockchain startup ecosystem.

- The United Kingdom is witnessing steady growth as financial institutions and fintech companies expand their involvement in digital asset trading and tokenization initiatives.

- The Netherlands is expected to experience notable growth over the forecast period, supported by its strong digital infrastructure and increasing blockchain adoption in financial services.

Competitive Landscape

The Europe security tokens market is highly dynamic, with blockchain technology firms, fintech companies, and digital asset exchanges competing to develop advanced tokenization platforms and regulated trading ecosystems. Companies are focusing on regulatory compliance, interoperability, and secure blockchain infrastructure to support large-scale tokenized asset markets. Strategic collaborations with financial institutions and exchanges are also strengthening the growth of security token offerings across Europe.

Prominent players in the Europe security tokens market include Polymath, Societe Generale Forge, Deutsche Boerse Group, SIX Digital Exchange, tZERO, Securitize, Harbor, Swarm, TokenSoft, Securrency, Blockstream, Smartlands, Neufund, DigiShares, STO Global-X, Tokeny Solutions, Bitbond, OpenFinance Network, Fusang, INX Limited, STOKR, TokenMarket, and Lykke.

Europe Security Tokens Market Size

The Europe security tokens market size was valued at USD 1.08 billion in 2025 and is anticipated to reach USD 1.38 billion in 2026 to reach from USD 7.73 billion by 2034, growing at a CAGR of 27.47% during the forecast period from 2026 to 2034.

Current Introduction of the Europe Security Tokens Market

A security token is a blockchain-based digital asset that represents legal ownership of a real-world financial asset. Unlike utility tokens that grant access to services, security tokens in Europe represent legal ownership rights and are subject to the rigorous oversight of the Markets in Financial Instruments Directive Two and the newly implemented Markets in Crypto Assets Regulation. According to the European Fund and Asset Management Association, the European investment management sector oversees approximately thirty three trillion euros in assets, providing a massive underlying value pool for potential tokenization initiatives. Top-level decision-makers in European finance have moved beyond testing digital asset technology and now view its implementation as a vital component of their long-term business strategy. The European Commission has actively fostered this environment through the Distributed Ledger Technology Pilot Regime, which allows authorized market infrastructures to test settlement frameworks for tokenized securities under temporary regulatory exemptions. According to data from the European Banking Authority, more than fifteen European member states have already passed national laws enabling electronic securities registers or blockchain based custody solutions. The European Central Bank has further strengthened this foundation by advancing the digital euro project, with pilot phases concluding in two thousand twenty five to support programmable settlement. This unique convergence of strict investor protection laws and proactive technological infrastructure positions Europe as a global leader in developing a legally certain and technologically advanced market for digital securities.

MARKET DRIVERS

Regulatory Clarity Through MiFID Two And MiCA Harmonisation Drives Institutional Participation

Established securities regulations are now converging with emerging digital asset frameworks, which accelerates the growth of the Europe security tokens market. This alignment creates a compelling demand for security tokens among European institutional investors who want compliant exposure to blockchain efficiencies. According to the European Securities and Markets Authority, the Markets in Crypto Assets Regulation, which became fully applicable in December two thousand twenty four, establishes clear boundaries between regulated security tokens and other crypto assets, significantly reducing legal ambiguity for asset managers. Clearer rules are driving a significant number of European investment managers to move toward launching digital versions of their funds, as they can now operate within a recognized and stable legal environment. The DLT Pilot Regime, operational across all twenty seven member states, permits trading venues to settle tokenised securities with reduced intermediary layers, potentially lowering transaction costs by up to thirty percent according to European Central Bank efficiency modelling. Institutional demand intensifies as tokenisation enables fractional ownership of previously illiquid assets such as private equity stakes or commercial real estate, democratising access for pension funds with strict diversification mandates. According to data from the Association for Financial Markets in Europe, cross border securities settlement in Europe currently averages two days, whereas tokenised instruments on distributed ledgers can achieve near instantaneous finality, addressing a critical operational pain point for institutional portfolios. This regulatory enabled efficiency gain, combined with enhanced transparency through immutable transaction records, aligns with European institutional investors' escalating environmental social and governance reporting obligations, creating sustained demand for security token infrastructure that embeds compliance logic directly into asset programmability.

Operational Efficiency Gains Through Automated Settlement And Compliance Attract Market Infrastructure Investment

European financial institutions increasingly prioritise security tokens for their capacity to automate post-trade processes through smart contract functionality, which fuels the expansion of the European security token market. This shift directly addresses persistent cost pressures in securities settlement and regulatory reporting. According to the Bank for International Settlements, European securities settlement infrastructure processes over one hundred trillion euros annually, with manual reconciliation and intermediary fees representing significant operational overhead. As per analysis from the European Central Bank, tokenised securities settled on distributed ledgers can reduce settlement times from the current T plus two standard to near real time finality, potentially freeing up collateral worth billions of euros currently tied in settlement cycles. The automation of compliance obligations through programmable tokens offers further efficiency; for instance, investor eligibility checks, withholding tax calculations, and position limits can be embedded directly into token transfer logic. A significant portion of the money spent running investment funds in Europe goes toward manually double-checking records, a process that digital ledger technology could largely automate. Institutional adoption accelerates as major custodians including BNP Paribas Securities Services and Euroclear invest in blockchain compatible infrastructure, with over seven major European financial institutions participating in the deuss blockchain initiative for small and medium enterprise bond issuance. As per Roland Berger research, tokenisation could reduce end to end issuance costs for mid cap corporate bonds by up to forty percent through disintermediation of traditional underwriting and settlement layers. This compelling efficiency narrative, validated by central bank research and institutional pilot results, sustains robust demand for security token solutions that deliver measurable operational improvements while maintaining full regulatory compliance within the European financial services framework.

MARKET RESTRAINTS

Regulatory Fragmentation Across Member States Creates Compliance Complexity For Cross Border Issuance

European Union-level initiatives aimed at harmonizing DLT are undermined by divergent national implementations, which constrain the growth of the Europe security tokens market. Consequently, security token issuers targeting pan-European distribution face significant compliance overhead. The European market for digital securities is currently divided among numerous country-specific legal systems, each imposing its own technical and administrative rules for how investments are officially recorded. As per analysis from Clifford Chance legal advisors, a security token issuer seeking distribution across Germany, France, and Luxembourg must navigate three separate regulatory regimes: Germany's Electronic Securities Act requiring BaFin licensed registrars, France's DEEP framework mandating reversibility planning, and Luxembourg's iterative Blockchain Laws imposing substance over form custody principles. This fragmentation increases time to market and legal costs substantially. The cost of ensuring that a digital investment fund meets the diverse legal requirements of multiple European countries is substantially higher than the cost of launching that same fund in just one country. The absence of harmonised technical standards for token interoperability further complicates secondary market liquidity, as tokens issued on one national ledger often cannot be seamlessly transferred to trading venues operating under another member state's framework. Small and medium-sized businesses in Europe often find that the expensive legal hurdles of offering digital securities in multiple countries make the technology too costly to use for their smaller funding rounds. The current fragmentation of national implementation guidelines restrains market scale and limits necessary network effects for European security tokens. This situation will persist until the European Securities and Markets Authority achieves greater regulatory convergence.

Legacy Infrastructure Integration Challenges Impede Scalable Adoption Among Traditional Financial Institutions

European financial institutions face substantial technical and operational hurdles when integrating tokenised securities with existing core banking and custody systems, which inhibits the expansion of the Europe security tokens market. This integration creates friction that slows institutional adoption of security tokens. The vast majority of Europe's largest banks are still running their most critical accounting and settlement tasks on decades-old computer systems that were never designed to talk to modern digital ledger technologies. Trying to connect new digital investment records to old-fashioned cash payment systems creates a complicated middle layer that significantly raises the chance of technical errors or processing delays during the early stages of adoption. The challenge intensifies with cash on chain requirements. Furthermore, legacy risk management systems often cannot process the real time valuation data generated by tokenised assets trading on twenty four seven markets, creating compliance gaps for institutions subject to strict intraday exposure limits. Upgrading the technical foundations of a bank to handle digital securities is so expensive that it is currently preventing many smaller and medium-sized European financial firms from entering the market. European regulators have yet to provide clearer pathways for hybrid settlement models and legacy system interoperability standards. However, until they do, these integration challenges will continue to restrain the pace of institutional security token adoption across the European financial services landscape.

MARKET OPPORTUNITIES

Expansion Of Tokenised Private Market Assets Creates New Liquidity Pathways For Institutional Portfolios

The tokenization of private market assets, including private equity, venture capital, and commercial real estate, offers a transformative opportunity for European institutional investors and the Europe security tokens market. These investors can now seek enhanced liquidity and portfolio diversification within regulated frameworks. European institutional investors are steadily increasing their exposure to private markets, though these investments remain a smaller portion of their total holdings compared to public stocks and bonds due to their long-term nature and lack of immediate liquidity. Security tokens enable fractional ownership and programmable transfer restrictions that can create compliant secondary markets for these illiquid assets, potentially unlocking billions in trapped capital. Industry experts predict that turning private company shares into digital tokens will soon enable a multi-billion euro resale market, provided that lawmakers create uniform rules for how these digital assets are traded. The opportunity extends to small and medium enterprise financing. The European Union is mobilising massive amounts of capital to lead in new technologies, while simultaneously exploring how digital bonds can help smaller companies access cheaper funding than traditional bank loans. Institutional demand intensifies as tokenisation enables dynamic portfolio rebalancing. : Financial experts believe that if pension funds could see the true value of their private investments more frequently, they could manage their money more effectively and potentially increase their overall profits. Furthermore, environmental social and governance criteria can be embedded directly into token smart contracts, allowing institutional investors to automate impact reporting and ensure ongoing compliance with sustainable finance disclosure regulations. This convergence of liquidity enhancement, cost reduction, and regulatory technology positions tokenised private markets as a high growth opportunity segment within the European security tokens ecosystem.

Digital Euro Integration Enables Seamless On Chain Settlement For Tokenised Securities

The European Central Bank’s anticipated launch of a digital euro creates a foundational opportunity for security tokens to achieve fully on-chain settlement, which is anticipated to drive the expansion of the Europe security tokens market. This would eliminate the friction of bridging between distributed ledgers and traditional payment systems. The European Central Bank has completed its major research and initial testing phases, establishing the technical rules that would allow a digital currency to automatically settle complex financial trades even without a constant internet connection. Industry experts find that using a digital version of central bank money to pay for investments can almost entirely remove the risk of one party failing to deliver their side of a deal, as the payment and the asset transfer happen at the exact same moment. The opportunity extends to cross border efficiency. Sending and settling investments across European borders currently involves high fees from a chain of different banks, but a unified digital currency could bypass these middlemen to make international transactions much cheaper. Institutional adoption accelerates as tokenised funds gain the ability to execute intraday redemptions with finality, a capability particularly valuable for money market funds managing corporate treasury liquidity. Investment experts predict that within the next few years, a significant portion of Europe's short-term savings will be held in digital formats, allowing investors to move their money instantly at any time of day. Furthermore, the digital euro's compliance. This convergence of central bank digital currency development and security token innovation positions Europe to lead in building the next generation of financial market infrastructure.

MARKET CHALLENGES

Interoperability Gaps Between Distributed Ledger Platforms Fragment Secondary Market Liquidity

The absence of standardised technical protocols for cross platform token transfers creates significant liquidity fragmentation in the European security tokens market. This restrains secondary trading volumes and price discovery efficiency. The European digital asset landscape is currently built on many different and competing technical foundations, making it difficult to establish a single standard for how these investments are created and verified. Because different digital trading platforms in Europe cannot "talk" to each other directly, moving an investment from one system to another requires complex workarounds that add risk and slow down the process. The liquidity impact is material. While many new digital investments are being created, very few are actually being resold later because the technology is too fragmented to bring enough buyers and sellers together in one place. Institutional investors face additional complexity in portfolio management. Investment firms are finding that managing several different types of digital ledgers at once actually requires more manual record-keeping and time-consuming double-checks than the older systems they were meant to replace. Furthermore, the absence of common standards for token metadata and corporate action processing impedes automated compliance monitoring, a critical requirement for European institutional portfolios subject to stringent reporting obligations. European standardisation bodies, such as the European Committee for Standardisation, must first establish unified protocols for token interoperability. Until then, fragmentation will continue to constrain the development of deep and liquid secondary markets for security tokens across the European Union.

Evolving Regulatory Perimeter For Decentralised Finance Creates Uncertainty For Tokenised Asset Protocols

The rapid evolution of decentralized finance protocols introduces regulatory ambiguity for the region’s security tokens interacting with lending, market making, or yield mechanisms, which slows down the expansion of the Europe security tokens market. This creates significant compliance uncertainty for institutional participants. The decentralised finance ecosystem is becoming increasingly interconnected across various digital ledgers, creating challenges for regulators who must monitor activities that span multiple jurisdictions and technical frameworks. Asset managers are facing more complex due diligence requirements when dealing with digital assets, as they must now account for the legal and operational risks associated with the underlying technology protocols in addition to standard security laws. The regulatory challenge intensifies with cross chain composability. Uncertainty regarding the implementation of new digital asset frameworks has led some financial institutions to postpone the rollout of blockchain-based investment vehicles while they wait for clearer compliance standards. Institutional investors face heightened due diligence burdens. Furthermore, the absence of clear guidelines on liability allocation when smart contract vulnerabilities cause losses in decentralised environments creates legal uncertainty that discourages institutional participation. European regulators have yet to provide explicit frameworks for the interaction between regulated security tokens and decentralized finance infrastructure. This uncertainty will continue to restrain institutional adoption and limit the innovation potential of the European market.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 27.47% |

| Segments Covered | By Offering, Type, Application, End-User, and Country |

| Various Analyses Covered | Global, Regional, and Country Level Analysis, Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, the Czech Republic, and the Rest of Europe |

| Market Leaders Profiled | Polymath, Societe Generale Forge, Deutsche Boerse Group, SIX Digital Exchange, tZERO, Securitize, Harbor, Swarm, TokenSoft, Securrency, Blockstream, Smartlands, Neufund, DigiShares, STO Global-X, Tokeny Solutions, Bitbond, OpenFinance Network, Fusang, INX Limited, STOKR, TokenMarket, Lykke |

SEGMENTAL ANALYSIS

By Offering Insights

The platform segment captured the majority share of 55.2% of the Europe security tokens market in 2025. The prominence of the segment is attributed to the foundational necessity of robust technological infrastructure before any service layer can be effectively deployed. European financial institutions prioritize the acquisition and licensing of secure issuance and trading platforms to ensure compliance with the stringent requirements of the Markets in Crypto Assets Regulation and the Distributed Ledger Technology Pilot Regime. Big force shaping the platform segment is the urgent requirement for infrastructure that natively embeds regulatory logic into the asset lifecycle. European crypto-asset service providers are now required to meet significantly higher operational and investor protection standards under a harmonized regulatory framework. Financial institutions are increasingly adopting third-party tokenization platforms to quickly gain access to compliant, ready-to-use digital asset infrastructure. The complexity of complying with varying national laws across the twenty seven member states forces institutions to rely on pre validated platforms rather than building proprietary solutions from scratch. Leveraging established, third-party DLT platforms significantly accelerates the speed-to-market for financial institutions implementing tokenized services compared to building in-house. This speed to market advantage is critical as issuers race to capitalize on the Digital Finance Strategy incentives. Furthermore, platforms offering multi chain interoperability are seeing heightened demand. Institutional demand is rapidly shifting towards tokenization solutions that offer interoperability between different ledger types (permissioned and public) while ensuring a single, authoritative record of ownership. This structural dependency on compliant, ready to deploy technology ensures the platform segment retains its leading market position. A further reason for this growth is the substantial capital investment required to establish secure digital custody capabilities, which are integral to modern issuance platforms. The preference shifts spending toward comprehensive platforms that bundle issuance, trading, and custody into a single regulated environment. The cost of developing such secure environments internally is prohibitive for most mid sized firms. Consequently, institutions opt for platform licenses that spread these costs across multiple users. This economic reality solidifies the platform segment as the primary revenue generator in the market ecosystem.

The service segment is predicted to witness the highest CAGR of 28.5% during the forecast period due to the increasing complexity of the tokenized asset lifecycle, which necessitates specialized advisory, legal, and marketing support beyond the capabilities of standard software platforms. As the market matures from pilot phases to full scale production, the demand for human expertise to navigate regulatory nuances and structure complex deals is outpacing the demand for pure technology. The rapid expansion of the service segment is mainly fueled by the intricate legal structuring required to tokenize diverse asset classes under the evolving European regulatory framework. Legal, tax, and regulatory uncertainty remains high across European jurisdictions regarding security token classification, requiring manual, bespoke legal advice. Despite regulatory, pan-European initiatives to harmonize distributed ledger technology (DLT) in financial markets, the need for localized legal advice across member states remains high. The complexity is further compounded by the need to draft smart contract legal wrappers that align code with contractual obligations. Tokenized asset documentation requires significant customization compared to traditional, standardized financial documentation due to novel legal risks involving technology and settlement finality. This trend is intensifying as real world assets like commercial real estate and private equity enter the market. Tokenizing real estate assets continues to require a multidisciplinary approach due to the complex, parallel, and disparate regulations governing property and financial instruments. The demand for highly specialized legal and technical consulting expertise in tokenization continues to put upward pressure on professional service costs. This reliance on specialized knowledge ensures the service segment will outpace platform sales in percentage growth terms. In addition, this segment is supported by the growing need for targeted investor education and marketing campaigns to bridge the trust gap between traditional investors and digital assets. The regulatory environment also mandates clear communication. This has created a booming niche for marketing agencies and communication firms specializing in fintech compliance. Furthermore, the rise of decentralized finance integration requires issuers to educate investors on wallet management and private key security. The service sector is experiencing sustained double-digit growth as the market moves toward mass adoption. This is because the ability to communicate value and safety has become a key differentiator for issuers who realize technology alone is not enough for subscription success.

By Type Insights

The equity tokens segment dominated the Europe security tokens market and accounted for a 42.7% share in 2025. The dominance of the segment is driven by the strong alignment between tokenized equity structures and the deep venture capital and private equity ecosystems prevalent in Europe, particularly in technology and green energy sectors. The ability to fractionalize ownership in high growth private companies appeals strongly to the region's sophisticated investor base seeking early stage exposure with improved liquidity options. The dominance of equity tokens is fundamentally driven by Europe's robust venture capital landscape, which is increasingly adopting tokenization to solve liquidity constraints for early stage investors. European venture capital fundraising has significantly matured over the last decade, reaching historic highs but remains well below the hundred-billion-euro threshold for annual capital raised. Large European startups and unicorns are increasingly evaluating blockchain technologies for efficiency gains in post-trading and cap table management, though widespread execution of tokenized equity rounds is not yet the industry standard.

The traditional lock up periods in private equity, often lasting seven to ten years, are a significant pain point that equity tokens address by enabling secondary trading on regulated multilateral trading facilities. Venture capital and private equity holding periods have historically lengthened as companies stay private longer, though emerging secondary market technologies are being developed with the intent to provide earlier liquidity. This liquidity premium makes equity tokens highly attractive for founders and early backers. Furthermore, the regulatory clarity provided by the MiFID Two framework for shares simplifies the issuance process for corporate equity compared to more complex debt structures. Major European exchanges are successfully launching digital market infrastructures to facilitate tokenization, but traditional equity issuances and established exchange-traded products continue to dominate total market volume. This strong correlation between the vibrant startup ecosystem and the need for liquidity cements equity tokens as the market leader. Also, this segment is boosted by the democratization of access to private market returns through fractional ownership, a capability highly valued in the European wealth management sector. Equity tokens allow these assets to be divided into fractions as small as one thousand euros, opening the asset class to a wider demographic of investors. The programmability of equity tokens also facilitates automated dividend distributions and voting rights execution, enhancing the administrative efficiency for issuers managing large numbers of small shareholders. This efficiency gain encourages more companies to choose equity tokenization over traditional share registries. Additionally, the alignment with Environmental Social and Governance goals is stronger in equity tokens. These combined benefits of accessibility, efficiency, and transparency ensure equity tokens remain the preferred instrument for capital formation in Europe.

The asset backed tokens segment is estimated to register the fastest CAGR of 32.4% from 2026 to 2034 owing to the immense opportunity to tokenize illiquid real world assets such as real estate, commodities, and infrastructure projects, which represent a vastly larger store of value than the equity or debt markets alone. The drive to unlock liquidity in these traditionally stagnant asset classes is reshaping the European investment landscape. The top factor for this segment is the tokenization of commercial and residential real estate, a sector where Europe holds trillions in illiquid value. : The European commercial property sector is currently experiencing a period of low transaction volume and significant valuation adjustments, primarily driven by high interest rates and the resulting gap between buyer and seller price expectations. Tokenization is being adopted as a tool to fractionalize high-value assets and streamline settlement processes, aiming to make real estate investment more accessible to a broader range of investors through digital infrastructure. Germany and France are leading the European market in establishing regulatory frameworks for digital securities, which has spurred significant growth in domestic tokenized real estate projects compared to other regional markets. The ability to fractionalize high value properties allows investors to diversify across geographies and asset types with unprecedented ease. European asset managers are showing strong interest in blockchain technology, with a significant portion of firms currently in the research or pilot phase for launching tokenized fund structures to increase operational efficiency. Furthermore, the transparency of blockchain ledgers provides immutable records of property titles and rental income flows, addressing historical issues of opacity in real estate investing. European land registries are investigating blockchain to create more transparent and immutable property records, though full integration into national legal systems remains a long-term goal dependent on legislative reform. This compelling value proposition of liquidity, accessibility, and transparency is driving the asset backed segment to outpace all other token types in growth rate. Additionally, the segment is helped by the increasing tokenization of infrastructure projects and commodities to meet the surging demand for Environmental Social and Governance compliant investments. The programmability of these tokens allows for automated distribution of yields generated from energy production or commodity sales, providing a transparent and verifiable income stream. In the infrastructure space, tokenization enables the bundling of small scale projects, such as solar rooftops, into investable portfolios that were previously too small for institutional funds. This alignment with the continent's sustainability agenda, combined with the operational efficiencies of digital settlement, positions asset backed tokens as the highest growth frontier in the European security tokens market.

By End User Insights

The financial institutions segment led the Europe security tokens market and held a 58.6% share in 2025 because of the heavy regulatory oversight and capital resources that banks, asset managers, and custodians possess, allowing them to lead the adoption of tokenization for internal efficiency gains and new product creation. Their role as gatekeepers of capital and compliance makes them the primary drivers of market volume. The leading position of financial institutions is heavily influenced by the pressing need to comply with increasingly complex regulatory reporting requirements while reducing operational costs. Regulatory compliance costs for European banks have risen steadily due to complex reporting requirements, leading to significant investment in automated regulatory technology to manage these massive financial burden. European regulators are actively integrating blockchain into central bank operations to modernize settlement systems, while traditional reporting frameworks continue to evolve toward more data-driven, rather than DLT-based, automated models. Tokenized assets provide an immutable audit trail that simplifies the verification of holdings and transaction history for supervisors. Furthermore, the Markets in Crypto Assets Regulation explicitly designates credit institutions and authorized investment firms as the primary entities permitted to offer crypto asset services, effectively channeling market activity through established financial players. Traditional European financial institutions are gradually entering the digital asset space through targeted partnerships and niche service offerings, though the market for licensed crypto services is still predominantly led by specialized digital-first companies. This regulatory moat prevents non financial entities from dominating the market. Additionally, the need for efficient collateral management in repo markets drives adoption. The tokenization of high-quality liquid assets is enabling real-time collateral movement across borders, significantly reducing the time assets spend "in transit" and allowing for more precise management of global liquidity pools. This combination of regulatory pressure and operational incentive ensures that financial institutions remain the central actors in the security tokens ecosystem. Beyond compliance, the drive for product innovation and new fee streams is a critical factor cementing the dominance of financial institutions, particularly asset managers. Tokenized funds offer a unique value proposition by enabling daily liquidity for alternative assets and lowering minimum investment thresholds, attributes that attract fresh capital. The ability to program fee structures directly into smart contracts also ensures accurate and timely revenue recognition. Major European players like Societe Generale and Deutsche Bank have already launched tokenized deposit and fund products, setting a precedent for the industry. The strategic imperative to modernize product offerings and capture new market segments ensures that financial institutions will continue to dictate the pace and direction of the Europe security tokens market.

The retail investors segment is anticipated to witness the fastest CAGR of 29.8% over the forecast period owing to the democratization of investment opportunities previously reserved for the wealthy, facilitated by user friendly digital platforms and the rising financial literacy regarding digital assets among the European population. The rapid growth of retail participation is mainly supported by the ability of security tokens to lower minimum investment thresholds for high value alternative assets like private equity and commercial real estate. European mass affluent investors are increasingly looking for ways to diversify into private markets, though high entry barriers and a lack of tailored digital products currently keep much of their wealth in traditional cash deposits. The technology for fractionalizing high-value assets is maturing, offering a pathway to lower investment minimums and broader retail participation in traditionally exclusive asset classes. Household financial wealth in Europe has seen a steady recovery and growth following recent market volatility, with the majority of assets held in equity, investment funds, and bank deposits. The rise of neo brokerage platforms offering seamless access to security tokens has further accelerated this trend. The European fintech sector is undergoing a period of consolidation, with capital concentrating in established firms while new retail adoption of advanced blockchain-based securities remains in an early, steady growth phase rather than a sudden doubling. Furthermore, the transparency of blockchain technology appeals to younger investors who demand visibility into their holdings. Younger investors are leading the shift toward digital-first investment platforms and alternative assets, driven by a preference for mobile accessibility and a greater willingness to navigate emerging technology environments. This generational shift in investment preferences, combined with the removal of financial barriers, is propelling the retail segment to become the fastest growing component of the market. A major factor that aids this segment is the promise of enhanced liquidity and access to secondary markets for assets that were historically illiquid. The integration of security tokens with familiar trading interfaces allows retail investors to manage portfolios with the same ease as public equities. Moreover, the programmability of tokens allows for features like automated dividend reinvestment, which appeals to long term retail savers. This convergence of liquidity access, user experience improvements, and regulatory support for retail protection creates a fertile environment for the exponential growth of retail involvement in the security tokens market.

COUNTRY ANALYSIS

Germany Security Tokens Market Analysis

Germany was the top performer in the Europe security tokens market and occupied a 24.8% share in 2025. The supremacy of the German markets is driven by its proactive legislative framework and robust industrial base. The country's position is anchored by the Electronic Securities Act enacted in two thousand twenty one, which legally equates digital securities with traditional paper instruments, providing unparalleled legal certainty for issuers. Germany has established one of the most rigorous and clear licensing frameworks for digital asset custody in the world, leading to a steady increase in the number of traditional and fintech firms successfully meeting high regulatory standards. The German market is uniquely driven by the "Mittelstand" or small and medium enterprises sector, which faces significant financing challenges and views tokenization as a viable alternative to bank loans. The German startup ecosystem is increasingly exploring blockchain-based financing as a way to diversify capital sources, though traditional equity and debt rounds continue to represent the overwhelming majority of funding transactions. The presence of major global exchanges like Deutsche Boerse, which operates the Digital Exchange for institutional crypto trading, further solidifies Germany's hub status. Frankfurt is leveraging its status as a leading financial centre to build a robust digital market infrastructure, attracting major institutions to pilot tokenized settlement and post-trade services. The government's continued support through the Blockchain Strategy of the Federal Government ensures that regulatory sandboxes remain open for innovation. Germany’s state-owned development bank is actively leading by example in the capital markets, using its own bond issuances to test and validate the legal and technical viability of blockchain-based securities. This combination of clear laws, strong institutional infrastructure, and government backing ensures Germany maintains its top ranking in the regional market.

France Security Tokens Market Analysis

France followed closely in the Europe security tokens market and captured a 18.4% share in 2025. The expansion of the French market is propelled by its comprehensive regulatory regime known as the Visas for Digital Assets Service Providers and the optional visa for security token offerings. The French market known for a strong state led initiative to position Paris as a global fintech hub, leveraging the Autorite des Marches Financiers to provide fast track approval for compliant projects. A key driving factor is the "Deep" framework which allows for the direct registration of financial minibonds on distributed ledgers, bypassing traditional notaries and significantly reducing issuance costs. The presence of major banking groups like Societe Generale, which issued the first covered bond on a public blockchain, demonstrates the deep integration of tokenization into the mainstream financial system. Furthermore, the French government's "France 2030" investment plan allocates substantial resources to digital innovation, including blockchain infrastructure for capital markets. This strategic alignment of regulatory innovation, banking leadership, and state support propels France to the forefront of the European landscape.

Switzerland Security Tokens Market Analysis

Switzerland held a noteworthy share of the Europe security tokens market by leveraging its reputation as a global crypto valley and its flexible legal framework adapted for digital assets. Although not an EU member, Switzerland's proximity and regulatory compatibility make it a critical player in the broader European ecosystem. The country's growth is also driven by the DLT Act which came into force in two thousand twenty one, creating a dedicated license category for DLT trading facilities that can trade and settle tokenized securities simultaneously. The canton of Zug, known as Crypto Valley, serves as the epicenter for this activity, housing hundreds of blockchain companies and foundations. The stability of the Swiss Franc and the country's political neutrality attract international issuers seeking a safe harbor for tokenization projects. The SIX Digital Exchange operates as a fully regulated digital asset exchange, providing institutional grade liquidity that is unmatched in the region. This unique blend of legal clarity, financial stability, and specialized infrastructure sustains Switzerland's high market standing.

United Kingdom Security Tokens Market Analysis

The United Kingdom witnessed a steady expansion in the Europe security tokens market. Despite leaving the EU, the UK remains a pivotal market due to the Financial Conduct Authority's proactive engagement with the industry through its regulatory sandbox and the development of a distinct digital securities regime. It relies on its historic strength as a global financial center and its agile regulatory approach post Brexit. The dominance of the UK market is driven by the depth of its institutional investor base, particularly in London, which manages trillions in assets and is eager to adopt tokenization for efficiency. The Bank of England's work on the Digital Securities Sandbox provides a controlled environment for testing settlement models using central bank money, a critical feature for institutional adoption. Furthermore, the UK's strong legal system based on common law provides a familiar and trusted framework for complex financial contracts involving smart assets. This combination of regulatory agility, deep capital pools, and legal certainty ensures the UK remains a top tier market despite its separation from the EU single market.

Netherlands Security Tokens Market Analysis

The Netherlands is predicted to grow in the Europe security tokens market over the forecast period due to its advanced digital infrastructure and progressive stance on blockchain integration within its civil law system. The Dutch market is also fuelled by the seamless integration of tokenization into its existing robust financial ecosystem, supported by the Authority for the Financial Markets which provides clear guidance on the qualification of crypto assets. A key factor is the collaboration between major banks like ING and ABN AMRO, who are actively developing tokenized deposit and bond platforms to serve corporate clients. The presence of Euroclear's significant operations in Amsterdam also facilitates the bridging of traditional and digital settlement systems. The Dutch legal system's adaptability was demonstrated by the court recognition of smart contracts as binding agreements, providing legal certainty for issuers. This forward looking regulatory environment combined with strong institutional participation secures the Netherlands' place among the top five markets.

COMPETITIVE LANDSCAPE

The competition in the Europe security tokens market is characterized by a dynamic interplay between established financial incumbents and agile technology driven newcomers vying for dominance in the emerging digital asset landscape. Traditional banks and stock exchanges leverage their extensive regulatory licenses and deep client relationships to offer trusted tokenization services while facing pressure to modernize their legacy infrastructure rapidly. Simultaneously specialized fintech firms and blockchain native companies compete by providing innovative technological solutions and superior user experiences that appeal to digitally savvy investors and issuers. The competitive intensity increases as players strive to secure first mover advantages in key sectors such as real estate tokenization and private equity digitization where regulatory clarity is improving. Strategic differentiation often hinges on the ability to offer seamless interoperability between various blockchain networks and traditional settlement systems ensuring liquidity and operational efficiency. As the regulatory framework under Markets in Crypto Assets Regulation matures the battle for market leadership will likely shift towards scalability and the breadth of asset classes supported by each platform provider.

KEY MARKET PLAYERS

A dominating players are in this Europe security tokens market are

- Polymath

- Societe Generale Forge

- Deutsche Boerse Group

- SIX Digital Exchange

- tZERO

- Securitize

- Harbor

- Swarm

- TokenSoft

- Securrency

- Blockstream

- Smartlands

- Neufund

- DigiShares

- STO Global-X

- Tokeny Solutions

- Bitbond

- OpenFinance Network

- Fusang

- INX Limited

- STOKR

- TokenMarket

- Lykke

Top Players In The Market

- Societe Generale Forge stands as a pioneering subsidiary of the French banking giant Societe Generale and serves as a dedicated digital asset issuer and service provider. The entity has successfully bridged traditional finance with blockchain technology by issuing the first covered bond on a public blockchain and launching multiple tokenized funds. Its contribution to the global market involves setting benchmarks for regulatory compliance within the European Union framework while demonstrating the viability of institutional grade digital assets. Recent actions include the expansion of its OB2T stablecoin for wholesale central bank digital currency settlements and partnerships with major asset managers to tokenize private debt instruments. By leveraging its banking license and deep expertise in securities law, the firm continues to validate the security token model for large scale institutional adoption across Europe and beyond.

- Deutsche Boerse Group operates as a critical infrastructure provider through its Digital Exchange known as D7 which offers a regulated marketplace for digital assets including security tokens. The group plays a vital role in the global market by integrating distributed ledger technology into existing post trade infrastructure to ensure seamless interoperability between traditional and digital securities. Its recent strategic moves involve enhancing the D7 platform with advanced custody solutions and expanding its range of tokenized money market funds to meet rising institutional demand. By collaborating with major banks and fintech firms, Deutsche Boerse ensures that its ecosystem supports the full lifecycle of security tokens from issuance to settlement. This comprehensive approach solidifies its position as a foundational pillar for the European digital finance landscape and influences global standards for exchange operated token platforms.

- SIX Digital Exchange based in Switzerland functions as a fully regulated financial market infrastructure that enables the trading and settlement of digital assets using distributed ledger technology. The exchange contributes significantly to the global market by proving that a complete value chain for digital securities can operate within a strict regulatory environment while maintaining atomic settlement capabilities. Recent initiatives include the successful migration of traditional bonds onto its digital platform and the launch of new tokenized fund structures that offer intraday liquidity to investors. By fostering partnerships with international custodians and issuers, SIX Digital Exchange expands the reach of Swiss based digital asset services to a broader European audience. Its continuous innovation in settlement finality and smart contract integration sets a high standard for security token exchanges worldwide and drives the evolution of capital market infrastructure.

Top Strategies Used By Key Market Participants

Key players in the Europe security tokens market primarily employ strategic partnerships and collaborations to integrate blockchain technology with legacy financial systems effectively. Major institutions frequently engage in joint ventures with fintech startups to accelerate product development and leverage specialized technical expertise without building solutions from scratch. Another prevalent strategy involves obtaining multiple regulatory licenses across different European jurisdictions to facilitate cross border distribution and ensure compliance with varying national laws. Companies also focus heavily on developing proprietary custody solutions that meet the stringent security requirements of institutional investors while supporting diverse blockchain protocols. Furthermore, market participants actively invest in educational initiatives and industry working groups to shape emerging regulations and promote standardization of token formats. These collective efforts aim to build trust among traditional investors and create a robust ecosystem capable of scaling tokenized asset adoption throughout the region.

MARKET SEGMENTATION

This research report on the Europe security tokens market is segmented and sub-segmented into the following categories.

By Offering

- Platform

- Service

By Type

- Equity Tokens

- Debt Tokens

- Utility Tokens

- Asset-backed Tokens

By Application

- Trading

- Payment

- Investment

- Compliance

- Others

By End-User

- Financial Institutions

- Retail Investors

- Enterprises

- Others

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

What are security tokens in the European financial market?

Security tokens are blockchain-based digital assets that represent ownership of real-world assets such as equities, bonds, or real estate and comply with financial regulations.

What factors are driving the growth of the Europe security tokens market?

Increasing adoption of blockchain technology, demand for digital asset investment, and supportive regulatory frameworks are key growth drivers.

How do security tokens differ from traditional cryptocurrencies?

Security tokens represent regulated financial assets and provide investor rights, while cryptocurrencies mainly function as digital currencies without ownership claims.

Which industries are adopting security tokens in Europe?

Financial services, real estate, venture capital, and asset management sectors are actively adopting security tokens for digital fundraising and asset tokenization.

How does blockchain technology support the security tokens market?

Blockchain enables transparent, secure, and efficient recording of transactions while reducing intermediaries in financial asset trading.

Which European countries are leading the security tokens market?

Germany, Switzerland, the United Kingdom, and France are key markets due to progressive digital asset regulations and fintech innovation.

What advantages do security tokens offer to investors?

Security tokens provide increased liquidity, fractional ownership of assets, faster settlement processes, and improved transaction transparency.

What challenges affect the Europe security tokens market?

Regulatory uncertainties, lack of standardized frameworks, and limited investor awareness can slow market adoption.

How are financial institutions responding to the rise of security tokens?

Many banks and fintech companies are exploring tokenized assets, blockchain trading platforms, and digital securities issuance.

What is the future outlook for the Europe security tokens market?

The market is expected to expand as blockchain adoption increases and regulatory frameworks for digital securities continue to mature across Europe.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com