Europe Sentiment Analysis Market Size, Share, Trends, & Growth Forecast Report By Component (Service, Professional Services, Sentiment, Support and Maintenance Services), Deployment, Organization Size, Vertical and Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic and Rest of Europe), Industry Analysis From 2026 to 2034

Europe Sentiment Analysis Market Report Summary

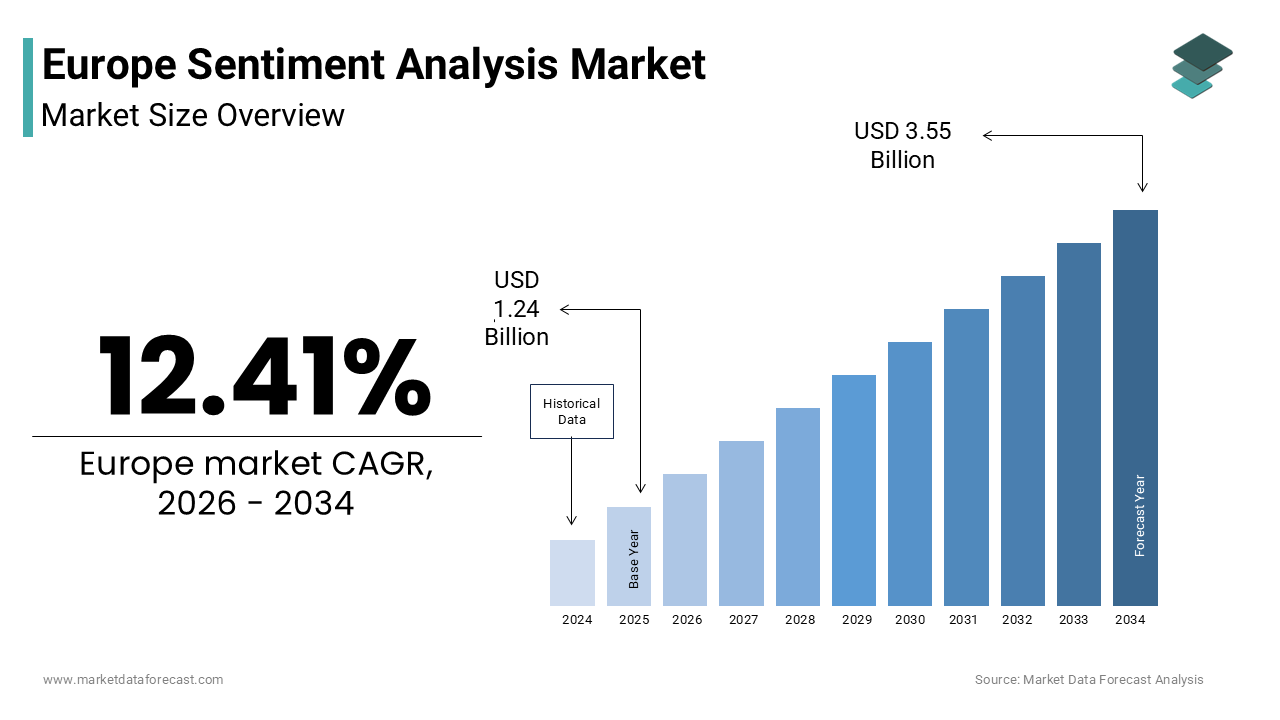

The Europe sentiment analysis market was valued at USD 1.24 billion in 2025, is estimated to reach USD 1.39 billion in 2026, and is projected to reach USD 3.55 billion by 2034, growing at a CAGR of 12.41% during the forecast period from 2026 to 2034. The growth of the Europe sentiment analysis market is driven by the rising importance of real-time customer feedback analysis, increasing use of artificial intelligence and natural language processing technologies, and the rapid growth of digital communication platforms across the region. The growing volume of user-generated content on social media, online review platforms, and digital customer service channels is further accelerating demand for sentiment analysis solutions. Moreover, the adoption of data-driven decision-making across industries such as retail, banking, and government is encouraging organizations to deploy advanced analytics tools to monitor public opinion, brand perception, and customer satisfaction.

Key Market Trends

-

Rising adoption of AI-driven sentiment analysis tools to monitor brand reputation and customer feedback across social media and digital platforms.

-

Increasing demand for real-time sentiment monitoring in sectors such as finance, retail, and public governance to support faster decision-making.

-

Growing integration of multilingual natural language processing technologies capable of analyzing multiple European languages and regional dialects.

-

Expansion of cloud-based sentiment analysis platforms that allow organizations to process large volumes of unstructured data efficiently.

-

Emergence of multimodal sentiment analysis combining text, voice, and visual inputs to provide deeper insights into consumer behavior.

Segmental Insights

- Based on component, the professional services segment was the largest and held 54.7% of the Europe sentiment analysis market share in 2025. The segment’s dominance is attributed to the need for customized deployment, model training, and consulting services to handle complex multilingual data and ensure regulatory compliance with European data protection laws.

- Based on organization size, the large enterprises segment accounted for a substantial share of the Europe sentiment analysis market in 2025. Large corporations generate enormous volumes of unstructured data through customer interactions, social media engagement, and digital transactions, making advanced sentiment analysis solutions essential for reputation management and strategic decision-making.

- Based on deployment and vertical, the cloud deployment model and BFSI sector together held a significant share of the Europe sentiment analysis market in 2025. Financial institutions rely heavily on sentiment analysis to monitor market sentiment, detect fraud risks, and analyze customer feedback in real time.

Regional Insights

The Europe sentiment analysis market is expanding across several countries due to increasing digitalization, strong artificial intelligence research ecosystems, and growing reliance on data-driven decision-making.

-

The United Kingdom dominated the Europe sentiment analysis market with 21.7% share in 2025, supported by its strong fintech sector, advanced AI research capabilities, and large volume of digital consumer data generated across industries.

-

Germany held 18.6% of the market share in 2025, driven by the adoption of data analytics technologies within manufacturing, automotive, and industrial sectors as part of the Industry 4.0 initiative.

-

France continues to expand its market presence due to government investments in artificial intelligence research and the global influence of French luxury and consumer brands that require sophisticated brand monitoring tools.

-

The Netherlands is witnessing steady growth due to its strong digital infrastructure and the presence of multinational companies that require multilingual sentiment analysis solutions for global markets.

-

Sweden is emerging as a growing market supported by strong investments in digital transformation and the widespread adoption of AI technologies across both public and private sectors.

Competitive Landscape

The Europe sentiment analysis market is characterized by intense competition between global technology providers and specialized analytics vendors. Companies are focusing on developing advanced multilingual natural language processing models, improving sarcasm and context detection capabilities, and ensuring compliance with strict European data protection regulations. Strategic partnerships with universities, AI research institutions, and cloud infrastructure providers are also helping companies expand their technological capabilities and improve analytical accuracy. Continuous innovation in real-time analytics, multimodal data analysis, and explainable AI solutions is shaping the competitive landscape of the market. Prominent players in the Europe sentiment analysis market include IBM Corporation, Oracle Corporation, SAP SE, Salesforce Inc., Adobe Inc., SAS Institute Inc., Brandwatch, Talkwalker, Meltwater, Clarabridge, Aylien Ltd., and Lexalytics Inc.

Europe Sentiment Analysis Market Size

The Europe sentiment analysis market size was valued at USD 1.24 billion in 2025 and is anticipated to reach USD 1.39 billion in 2026 from USD 3.55 billion by 2034, growing at a CAGR of 12.41% during the forecast period from 2026 to 2034.

Sentiment analysis (also known as opinion mining) is a Natural Language Processing (NLP) technique used to determine whether a piece of data is positive, negative, or neutral. This technology transcends simple positive or negative classification by interpreting nuance, sarcasm, and emotional intensity within diverse European languages to support strategic decision-making in finance, public policy, and corporate governance. The operational landscape is uniquely complex due to the linguistic fragmentation of the region, requiring solutions capable of processing over twenty official languages with high contextual accuracy. As per sources, messaging and email remain the cornerstone of digital life in the EU, with a steady shift toward instant messaging platforms over traditional communication methods. Furthermore, more people are using the internet to find information from public authorities. However, the active use of digital platforms to provide feedback or engage in policy debate remains a developing behavior. Social media usage has become a daily habit for a majority of Europeans, particularly among younger generations who use these platforms as their primary source of news and social interaction. This connectivity enables the continuous flow of public opinion data that organizations must analyze to maintain reputation and compliance. Unlike basic keyword tracking, modern sentiment analysis in Europe integrates deep learning models to understand cultural idioms and local dialects. The market thus functions as a critical intelligence layer for navigating the volatile digital public sphere while adhering to strict data privacy mandates under the General Data Protection Regulation.

MARKET DRIVERS

Escalating Demand for Real-Time Brand Reputation Management

The intensifying need for instantaneous brand reputation management serves as a primary growth enabler for the adoption of sentiment analysis solutions across European enterprises and the Europe sentiment analysis market as a whole. In an era where viral negative feedback can erode brand equity within hours, corporations require tools that detect shifts in public perception immediately rather than retrospectively. According to research, European consumers are becoming more ethically conscious, with a significant majority willing to withhold spending from brands that do not align with their social or environmental values. This high stakes environment forces companies to deploy advanced sentiment monitoring systems that scan millions of data points across forums, review sites, and social networks to identify emerging crises before they escalate. The ability to distinguish between isolated complaints and coordinated backlash allows marketing teams to deploy targeted responses rapidly. As per a study, retailers are increasingly adopting data-driven tools to monitor customer feedback in real-time, aiming to address service failures before they escalate on social platforms. The integration of these tools with customer relationship management systems enables automated escalation of critical issues to support teams, reducing resolution times significantly. Furthermore, the rise of influencer culture means that sentiment around specific endorsements must be tracked continuously to ensure alignment with brand values. This imperative to safeguard intangible assets drives sustained investment in sophisticated analytical platforms capable of delivering immediate, actionable intelligence.

Regulatory Mandates for Public Opinion Monitoring in Governance

Stringent regulatory frameworks are also a major factor boosting the expansion of the Europe sentiment analysis market. Additionally, the growing expectation for transparent governance drives public sector adoption of sentiment analysis. Government agencies are increasingly mandated to assess the societal impact of policies and legislation through systematic analysis of citizen feedback collected via digital consultation portals and social media. As per sources, local governments are moving toward "participatory governance" models, seeking more direct ways to involve citizens in decisions regarding the green and digital transitions. This shift toward data-driven policymaking ensures that legislative decisions reflect the genuine mood of the electorate rather than anecdotal evidence. The General Data Protection Regulation encourages the use of anonymized aggregate data, allowing authorities to analyze trends without compromising individual privacy. According to research, the use of AI and automation in public administration is being explored to help officials process thousands of unique citizen responses more quickly and accurately during large-scale consultations. Besides, the need to monitor disinformation campaigns and hate speech during election cycles has prompted electoral commissions to invest in advanced linguistic analysis capabilities. The ability to process vast volumes of multilingual input allows national governments to maintain social cohesion by addressing grievances proactively. This institutionalization of sentiment monitoring transforms it from a commercial luxury into a civic necessity, fueling robust market growth.

MARKET RESTRAINTS

Linguistic Fragmentation and Dialectical Complexity

The profound linguistic fragmentation and dialectical complexity across the European continent is a major limiting factor for the Europe sentiment analysis market growth. This affects the accuracy and scalability of sentiment analysis deployments. Unlike monolingual markets, Europe hosts numerous official languages and countless regional dialects, each with unique grammatical structures, idioms, and cultural contexts that challenge standard natural language processing models. As per the European Centre for Modern Languages, over 300 minority and regional languages are spoken across Europe, many of which lack sufficient annotated training data to build reliable sentiment algorithms. This scarcity leads to high error rates when analyzing content in less common languages, causing organizations to hesitate in deploying pan-European solutions. The nuance of sarcasm and irony varies significantly between cultures, such as the dry wit common in British English versus the expressive style of Southern European languages, often resulting in misclassification by generic models. According to a study, artificial intelligence tools struggle to interpret the nuances, slang, and grammar of regional speech, leading to less reliable insights for organizations operating outside of standardized national languages. Developing custom models for each linguistic variant requires substantial investment in data collection and expert annotation, which is prohibitive for many small and medium-sized enterprises. Universal models have yet to achieve high proficiency across all European tongues. Until they do, linguistic barriers will continue to limit the effective reach and reliability of sentiment analysis technologies.

Strict Data Privacy Regulations and Anonymization Requirements

The rigorous enforcement of data privacy regulations, such as the GDPR, serves as a significant hurdle to the Europe sentiment analysis market. It specifically limits the data collection practices necessary for training and operating sentiment analysis systems. The legal requirement to obtain explicit consent for processing personal data and the mandate to anonymize information strictly limit the volume of usable social media and communication data available for analysis. High-profile financial penalties for privacy violations are making European companies more hesitant to implement large-scale data processing projects without exhaustive legal vetting. Companies face significant legal risks when scraping public data if individuals have not explicitly consented to their posts being used for commercial analysis, leading to restricted datasets. The obligation to implement "privacy by design" means that vendors must build complex filtering mechanisms to strip personally identifiable information before any sentiment scoring occurs, increasing computational costs and latency. Uncertainties regarding how data can be moved and stored across borders are causing many organizations to pause their adoption of cloud-based analytics tools. Furthermore, cross-border data transfer restrictions complicate the use of global cloud-based analysis tools, forcing organizations to maintain fragmented local infrastructures. These regulatory hurdles increase the total cost of ownership and slow the deployment of comprehensive sentiment monitoring solutions.

MARKET OPPORTUNITIES

Integration of Multimodal Analysis for Holistic Insight

The integration of multimodal analysis capabilities opens up major possibilities for the growth of the Europe sentiment analysis market. This paves the way to move beyond text-only interpretation. By combining textual data with visual and audio inputs such as emojis, images, video tone, and voice inflection, providers can offer a far more accurate and holistic understanding of user sentiment. As per the European Association for Artificial Intelligence, the adoption of multimodal AI systems in customer experience management grew by 48% in 2025, driven by the need to capture non-verbal cues that text alone misses. This technology enables brands to detect frustration in a customer's voice during a call center interaction or interpret the sarcasm conveyed through a specific meme on social media. For instance, analyzing video reviews of products allows manufacturers to gauge genuine emotional reactions that written summaries might obscure. According to research from the Fraunhofer Institute, multimodal sentiment analysis improved prediction accuracy of consumer behavior by 28% compared to text-only models in European pilot studies. The opportunity lies in developing unified platforms that ingest data from diverse sources like TikTok videos, podcast transcripts, and image-heavy Instagram posts to create a 360-degree view of public opinion. As content consumption shifts increasingly toward video and audio formats in Europe, vendors who master multimodal processing will gain a decisive competitive edge by unlocking deeper layers of emotional intelligence.

Expansion of Hyper-Localised Cultural Context Engines

The development of hyper-localized cultural context engines offers a substantial opportunity for the Europe sentiment analysis market expansion. This growth is achieved by addressing the specific nuances of European regional identities. Rather than relying on broad national language models, vendors can create specialized engines trained on local slang, historical references, and cultural sensitivities unique to specific cities or regions. As per sources, there is a growing push to support digital tools that respect and preserve local cultural diversity, creating a favorable policy environment for such innovations. A system capable of distinguishing the specific sentiment markers used in Catalan versus Castilian Spanish or Bavarian versus Standard German would provide unparalleled accuracy for local businesses and municipalities. According to studies, demand for region-specific natural language processing APIs increased as enterprises sought to tailor marketing campaigns to micro-demographics. This granularity allows retailers to adjust promotions based on local moods or enables political parties to fine-tune messaging for specific constituencies. The opportunity resides in partnering with local universities and cultural institutions to curate high-quality training datasets that capture the essence of regional communication styles. Providers can command premium pricing and secure long-term contracts by solving the nuance problem for organizations requiring deep local insight. This approach effectively turns linguistic diversity from a barrier into a value proposition.

MARKET CHALLENGES

Prevalence of Sarcasm and Irony in Digital Communication

The pervasive use of sarcasm and irony in European digital communication is a serious impediment to the Europe sentiment analysis market. It undermines the accuracy of even advanced sentiment analysis algorithms. European cultures, particularly in the United Kingdom, Ireland, and parts of Scandinavia, frequently employ dry humor and understatement where literal meanings contradict intended sentiments, confusing standard polarity classifiers. As per research, a notable share of informal online comments in Northern Europe contain ironic elements that are routinely misidentified as positive or neutral by current AI models. This misclassification leads to flawed insights where genuine criticism is overlooked or praise is misinterpreted, potentially causing strategic blunders for brands relying on automated reports. The challenge is compounded by the evolution of internet slang and memes, which often rely on contextual knowledge that machines struggle to acquire without extensive cultural training. According to a study, state-of-the-art models still fail to detect sarcasm correctly in a considerable portion of cases involving complex sentence structures. Overcoming this requires massive datasets labeled specifically for irony and the development of context-aware neural networks that can analyze conversation history and user profiles. Algorithms cannot yet reliably decode these subtle linguistic devices. Consequently, the risk of erroneous sentiment scoring remains a significant hurdle for widespread trust and adoption.

High Computational Costs for Real-Time Multilingual Processing

The exorbitant computational costs associated with processing vast streams of multilingual data in real time pose a severe challenge to the scalability and profitability of sentiment analysis services in the region, and the Europe sentiment analysis market. Analyzing text across dozens of languages simultaneously requires immense processing power and sophisticated infrastructure, leading to high operational expenses that are difficult to pass on to price-sensitive customers. As per various sources, the energy consumption and server costs for running large language models across multiple European languages increased due to rising electricity prices and hardware shortages. Small and medium-sized enterprises often find the subscription fees for enterprise-grade multilingual sentiment tools prohibitive, limiting the market to large corporations with deep pockets. The latency introduced by translating and analyzing diverse languages in real time can also degrade the user experience, making instant crisis detection difficult. According to data from the Cloud Infrastructure Service Providers in Europe, the cost of GPU resources required for deep learning inference in multiple languages remains a primary barrier for startups entering the space. Furthermore, maintaining up-to-date models for rapidly evolving slang in twenty-plus languages requires continuous retraining, adding to the financial burden. Balancing the need for comprehensive linguistic coverage with economic viability remains a delicate act that constrains market penetration and innovation speed.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 12.41% |

| Segments Covered | By Component, Deployment, Organization Size, Vertical and Region. |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Country Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, the Netherlands, Turkey, the Czech Republic, and the Rest of Europe. |

| Market Leaders Profiled | IBM Corporation, Oracle Corporation, SAP SE, Salesforce Inc., Adobe Inc., SAS Institute Inc., Brandwatch, Talkwalker, Meltwater, Clarabridge, Aylien Ltd., and Lexalytics Inc. |

SEGMENTAL ANALYSIS

By Component Insights

The professional services segment dominated the Europe sentiment analysis market and accounted for a 54.7% share in 2025. The dominance of the segment is primarily driven by the critical need for customized implementation and strategic consulting to navigate the complex linguistic and regulatory landscape of the European continent. A key factor is the necessity for bespoke model training that accounts for regional dialects, cultural nuances, and industry-specific terminology which off-the-shelf software cannot address effectively. As per research, a notable share of European enterprises in 2025 required extensive professional consulting to integrate sentiment analysis tools with their legacy customer relationship management systems while ensuring General Data Protection Regulation compliance. Furthermore, the scarcity of internal expertise in natural language processing forces organizations to rely on external specialists for data annotation, algorithm tuning, and workflow orchestration. According to studies, companies that engaged professional services for deployment saw a higher accuracy rate in sentiment classification compared to those attempting self-implementation. The complexity of merging multilingual data streams from diverse sources such as social media, call centers, and email necessitates a hands-on approach that only specialized service providers can deliver. This reliance on expert guidance for successful adoption solidifies professional services as the primary revenue generator in the market component landscape.

The support and maintenance services segment is anticipated to witness the fastest CAGR of 18.3% during the forecast period due to the dynamic nature of language and the continuous evolution of online communication styles which require constant model updates and performance monitoring. A major driving factor is the escalating threat of adversarial attacks and data drift where shifting slang or new sarcasm patterns degrade model accuracy over time if not actively managed. Additionally, the stringent requirements for system uptime and data security under European cyber resilience acts compel organizations to subscribe to comprehensive support packages that offer real-time troubleshooting and security patching. According to a study, numerous large European firms increased their budget for AI system maintenance in 2025 to mitigate risks associated with biased or outdated algorithms. The need to continuously ingest fresh data to keep pace with trending topics and emerging crises ensures a recurring demand for maintenance expertise. This shift from one-time implementation to ongoing operational stewardship propels the support and maintenance segment to outpace other components in growth velocity.

By Organization Size Insights

The large enterprises segment led the Europe sentiment analysis market and captured a substantial share in 2025 because of the massive volume of unstructured data generated by multinational operations across multiple countries and the substantial financial resources available to invest in advanced analytical infrastructure. A further reason for this growth is the critical imperative for global brand reputation management and risk mitigation, where even minor sentiment shifts can impact stock prices and regulatory standing. As per sources, the top 500 corporations in Europe collectively process billions of customer interactions annually, creating an immense demand for scalable sentiment analysis platforms capable of handling big data workloads. Furthermore, large organizations face stricter regulatory scrutiny regarding consumer protection and fair trading practices, necessitating sophisticated tools to monitor compliance and detect potential issues proactively. The ability to integrate these tools with existing enterprise resource planning and business intelligence ecosystems provides a holistic view of organizational health that smaller entities rarely require. This combination of data scale, regulatory pressure, and strategic necessity ensures that large enterprises remain the primary revenue source for sentiment analysis vendors across the continent.

The small and medium enterprises segment is likely to experience the fastest CAGR of 16.9% over the forecast period. This accelerated growth is mainly attributed to the democratization of artificial intelligence through cloud-based software as a service models that lower entry barriers for smaller players. A significant driving factor is the increasing recognition among SMEs that understanding customer feedback is vital for survival in a competitive digital marketplace where agility and responsiveness are key differentiators. As per research, many SMEs in Europe adopted affordable sentiment analysis tools in 2025 to enhance their social media marketing strategies and improve customer retention rates. Additionally, the rise of e-commerce platforms and digital storefronts has empowered smaller retailers to compete with giants by leveraging data-driven insights to personalize user experiences. The availability of pre-trained models for major European languages eliminates the need for costly custom development, making advanced analytics accessible to businesses with limited IT budgets. This alignment of affordable technology with the urgent need for customer-centricity drives the exceptional growth trajectory of the SME segment.

By Deployment and Vertical Insights

The cloud deployment mode and the Banking Financial Services and Insurance segments together held the majority share of the Europe sentiment analysis market in 2025. The supremacy of the segment is credited to the urgent need for financial institutions to monitor real-time market sentiment, detect fraud, and ensure regulatory compliance amidst volatile economic conditions. A further key factor is the capability of cloud platforms to provide the elastic computing power required to process millions of transactional comments and news feeds instantly without heavy upfront infrastructure investment. Furthermore, the strict capital adequacy requirements encourage banks to adopt operational expenditure models offered by cloud vendors rather than sinking capital into on-premise hardware. According to studies, insurers utilizing cloud sentiment tools reduced their claims processing time by automatically prioritizing cases based on customer emotional distress levels. The ability to rapidly scale resources during market crises or product launches makes cloud deployment indispensable for the fast-paced BFSI sector. This synergy of scalability, cost-efficiency, and critical risk management needs solidifies the leadership of the cloud-based BFSI segment.

The healthcare and life sciences vertical segment is on the rise and is expected to be the fastest growing segment in the market by witnessing a CAGR of 19.5% from 2026 to 2034. This rapid expansion is fueled by the increasing emphasis on patient-centric care and the need to analyze vast amounts of unstructured clinical data and patient feedback to improve treatment outcomes. A major driving factor is the post-pandemic surge in digital health platforms and telemedicine services which generate enormous volumes of patient reviews, forum discussions, and social media conversations regarding drug efficacy and side effects. As per research, the volume of adverse event reports sourced from social media and digital channels increased in 2024, necessitating automated sentiment tools for pharmacovigilance. Additionally, pharmaceutical companies are leveraging sentiment analysis to monitor brand perception and identify unmet medical needs by analyzing patient communities and advocacy group discussions. The ability to extract actionable insights from patient narratives helps providers tailor communication strategies and enhance adherence to treatment plans. This convergence of regulatory encouragement, digital health adoption, and the drive for personalized medicine propels the healthcare sector to outpace all other verticals in growth velocity.

SEGMENTAL ANALYSIS

United Kingdom Sentiment Analysis Market Analysis

The United Kingdom was the top performer in the Europe sentiment analysis market and accounted for a 21.7% share in 2025. The dominance of the UK market is driven by the robust presence of the London Stock Exchange and major financial institutions that rely heavily on real-time sentiment data for algorithmic trading and risk management. The nation serves as the undisputed hub for artificial intelligence research and fintech innovation, driven by a dense concentration of world-leading universities and a supportive government strategy for digital technologies. As per sources, the UK is seeing massive private capital inflows into AI infrastructure and datacentres, solidifying its position as a global leader in AI development and research. Furthermore, the mature e-commerce sector and the influential British media landscape generate vast amounts of consumer data that fuel the demand for advanced analytics. The UK's AI startup ecosystem is expanding beyond London into regional hubs, creating a widespread network of innovation across various technical specialties. The early adoption of generative AI and large language models by British corporations further cements its leadership, as organizations strive to gain deeper insights from unstructured data. This confluence of financial clout, academic excellence, and technological maturity ensures the United Kingdom remains the dominant force in the European landscape.

Germany Sentiment Analysis Market Analysis

Germany followed closely in the Europe sentiment analysis market and held a 18.6% share in 2025. The growth of the German market is fuelled by the "Industry 4.0" initiative which encourages the use of data analytics to optimize production processes and understand customer feedback on complex engineering products. The market status in Germany is defined by its powerful industrial base and the systematic integration of AI into manufacturing and automotive sectors to monitor supply chain sentiments and brand reputation. As per studies, German industry is facing a widening gap in AI adoption, as geopolitical uncertainties lead some sectors to prioritize cost-cutting over technological innovation. Additionally, the strict regulatory environment regarding product safety and consumer rights compels German manufacturers to employ rigorous monitoring tools to detect potential issues early. Automakers are increasingly focused on consumer-centric technology and autonomous driving features to remain competitive in the global shift toward climate-neutral mobility. The strong tradition of engineering precision extends to software solutions, driving demand for high-accuracy models capable of handling technical jargon. This blend of industrial might, regulatory rigor, and technological discipline drives the sustained prominence of Germany in the market.

France Sentiment Analysis Market Analysis

France maintains a notable share of the Europe sentiment analysis market due to its strategic national AI plan and a thriving luxury goods sector. The market status in France is characterized by a strong emphasis on preserving linguistic sovereignty while adopting advanced technologies to analyze French and Francophone content globally. A further key factor is the government's "France 2030" investment plan which allocates significant funds to develop sovereign AI capabilities and reduce dependence on non-European tech giants. France is leveraging its "France 2030" programme to build significant local expertise in critical technologies like AI and quantum computing. Furthermore, the global influence of French luxury brands necessitates sophisticated sentiment monitoring to protect brand image across diverse international markets. The luxury sector is shifting its marketing focus toward micro-influencers and niche communities to maintain authenticity and brand prestige in a digital environment. The rich cultural output in cinema and literature also provides a unique dataset for training nuanced language models. This synergy of state support, brand prestige, and cultural depth solidifies France as a critical market node.

Netherlands Sentiment Analysis Market Analysis

The Netherlands witnessed a consistent growth in the Europe sentiment analysis market owing to the exceptional English proficiency and digital literacy of the Dutch population, which facilitates the rapid adoption of global AI tools and the testing of new multilingual algorithms. The market dynamics in the Netherlands are heavily influenced by its role as a digital gateway to Europe and a center for multinational headquarters that require cross-border sentiment insights. Additionally, the strong agri-food and logistics sectors utilize sentiment analysis to monitor global trade sentiments and consumer trends regarding sustainability and food safety. The collaborative ecosystem between universities, tech giants, and startups accelerates the deployment of cutting-edge solutions. This combination of infrastructural superiority, international orientation, and innovative spirit establishes the Netherlands as a key growth engine.

Sweden Sentiment Analysis Market Analysis

Sweden is predicted to grow in the Europe sentiment analysis market over the forecast period due to the national commitment to becoming a fully digital society, which has driven extensive investments in AI research and the development of ethical guidelines for algorithmic decision-making. The country serves as a leader in digital innovation and startup culture, distinguished by its early adoption of technology in both public and private sectors. As per the Swedish Agency for Digital Government, 90% of public agencies utilized some form of automated text analysis in 2025 to improve citizen services and policy formulation. Furthermore, the presence of global gaming and streaming giants headquartered in Stockholm generates massive volumes of user interaction data that require real-time sentiment processing to enhance user engagement. According to data from Business Sweden, the tech sector contributed 25% to the national GDP in 2024, with sentiment analysis playing a key role in product development cycles. The strong focus on transparency and explainable AI aligns with European values, making Swedish solutions highly attractive. This fusion of forward-thinking policy, digital-native industries, and ethical leadership propels Sweden's significant standing in the market.

COMPETITIVE LANDSCAPE

The competition in the Europe sentiment analysis market is intense and characterized by a dynamic rivalry between global technology giants and agile local specialists who compete on linguistic accuracy and regulatory compliance. Large multinational corporations leverage their extensive cloud ecosystems and broad product portfolios to offer integrated solutions while smaller firms differentiate themselves through deep expertise in specific European languages and cultural contexts. The battleground has shifted toward the ability to detect subtle nuances such as sarcasm and irony which are prevalent in many European communication styles and often confuse standard algorithms. Data privacy and sovereignty remain critical differentiators where vendors must prove their ability to keep data within European borders to win contracts from public sector and financial clients. Strategic alliances with local system integrators become essential for navigating the fragmented regulatory landscape across different nations. Customers increasingly demand explainable AI and bias mitigation features which forces competitors to constantly evolve their ethical frameworks and transparency reports. The market sees frequent collaborations as companies join forces to pool resources for developing large scale multilingual models that no single entity could build alone. Innovation in real time processing and multimodal analysis serves as a key frontier for gaining competitive advantage in this rapidly maturing sector.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the Europe Sentiment Analysis Market include

- IBM Corporation

- Oracle Corporation

- SAP SE

- Salesforce Inc.

- Adobe Inc

- SAS Institute Inc

- Brandwatch

- Talkwalker

- Meltwater

- Clarabridge

- Aylien Ltd.

- Lexalytics Inc.

Top Players in the Europe Sentiment Analysis Market

IBM Corporation

IBM Corporation stands as a global leader in artificial intelligence and data analytics with a profound impact on the Europe sentiment analysis market through its Watson AI platform. The company significantly contributes to the global landscape by providing advanced natural language processing capabilities that understand context and nuance across multiple European languages. Recently IBM strengthened its European position by expanding its cloud data centers in Germany and France to ensure strict compliance with local data sovereignty laws while offering low latency services. The firm actively collaborates with European financial institutions and government bodies to deploy custom sentiment models for risk management and public opinion monitoring. IBM continues to invest heavily in ethical AI frameworks to address bias in algorithmic decision making which is crucial for gaining trust in the region. Their strategic focus on hybrid cloud solutions allows clients to integrate sentiment analysis seamlessly with existing legacy systems. This commitment to security and customization solidifies their reputation as a premier provider of enterprise grade intelligence solutions worldwide.

SAP SE

SAP SE leverages its dominance in enterprise resource planning to embed sophisticated sentiment analysis directly into business workflows across Europe. The company contributes globally by enabling organizations to correlate customer sentiment data with sales inventory and supply chain metrics for holistic decision making. To strengthen its market position in Europe SAP recently launched industry specific clouds for retail and automotive that include pre trained sentiment models tailored to regional dialects and consumer behaviors. The firm has also integrated generative AI features into its Customer Experience suite allowing users to generate automated responses based on detected emotional tones. SAP frequently partners with European universities to advance research in multilingual natural language understanding ensuring their tools remain accurate across diverse linguistic landscapes. By focusing on real time integration within core business processes SAP empowers companies to act instantly on customer feedback. Their dedication to sustainability and data privacy aligns perfectly with European values driving widespread adoption among large corporations and public sector entities.

Microsoft Corporation

Microsoft Corporation capitalizes on its Azure cloud infrastructure and Dynamics 365 platform to deliver scalable sentiment analysis solutions tailored for the European market. The company contributes globally by offering accessible AI tools that democratize advanced text analytics for businesses of all sizes through its user friendly interfaces. Recent actions to bolster its market presence include the introduction of Azure AI Language updates that support deeper sentiment detection for over twenty European languages including rare dialects. Microsoft has also enhanced its Teams and Viva platforms with real time sentiment tracking to help managers gauge employee well being and engagement levels remotely. The firm actively engages with European regulators to shape policies on responsible AI usage ensuring its technologies meet stringent ethical standards. By integrating sentiment analysis into productivity tools Microsoft makes emotional intelligence a standard feature of daily work life. Their continuous investment in large language models and secure cloud environments ensures they remain at the forefront of innovation in the rapidly evolving European digital ecosystem.

Top Strategies Used by Key Market Participants

Key players in the Europe sentiment analysis market primarily employ strategic partnerships with local universities and research institutions to develop specialized models capable of understanding complex European dialects and cultural nuances. Companies frequently invest in expanding their cloud infrastructure within the European Union to ensure data residency compliance and reduce latency for real time processing needs. Product innovation remains a central strategy where vendors continuously integrate generative artificial intelligence to enhance context awareness and detect sarcasm or irony more accurately. Market participants also focus on vertical specialization by creating tailored solutions for highly regulated sectors like banking and healthcare to address specific compliance and risk management requirements. Acquiring niche startups with unique natural language processing capabilities allows larger firms to rapidly expand their linguistic coverage and technological depth. Offering flexible deployment options including hybrid and on premise solutions helps attract clients with strict data sovereignty concerns. Providing comprehensive professional services for custom model training and ongoing maintenance ensures high accuracy and long term customer retention.

MARKET SEGMENTATION

This research report on the Europe Sentiment Analysis Market has been segmented and sub-segmented based on the following categories.

By Component

- Service

- Professional Services

- Sentiment

- Support and Maintenance Services

By Deployment

- Cloud

- On-Premise

By Organization Size

- Small & Medium Enterprises (SMEs)

- Large Enterprises

By Vertical

- BFSI

- Retail

- Transportation & Logistics

- Education

- Media & Entertainment

- Healthcare & Life Sciences

- Others

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

What is the Europe Sentiment Analysis Market?

The Europe Sentiment Analysis Market involves tools and software that analyze opinions, emotions, and attitudes from digital text to help organizations understand public perception.

What factors are driving the growth of the Europe Sentiment Analysis Market?

Increasing use of social media, rising demand for customer experience management, and advancements in artificial intelligence are key growth drivers.

Which industries use sentiment analysis solutions in Europe?

Industries such as BFSI, healthcare, retail, IT and telecom, media and entertainment, and government widely use sentiment analysis solutions.

What are the main components of sentiment analysis solutions?

Sentiment analysis solutions typically include software platforms, analytics tools, and professional services.

How does sentiment analysis help businesses in Europe?

It helps businesses understand customer feedback, monitor brand reputation, and improve products and services.

What technologies support sentiment analysis systems?

Technologies such as natural language processing (NLP), machine learning, text analytics, and artificial intelligence support sentiment analysis systems.

What type of data is used in sentiment analysis?

Sentiment analysis uses data from social media posts, customer reviews, emails, surveys, blogs, and online forums.

What are the key applications of sentiment analysis in Europe?

Applications include social media monitoring, brand management, customer service optimization, and market research.

What deployment models are available in the Europe Sentiment Analysis Market?

Solutions are generally deployed through cloud-based platforms and on-premises systems.

What challenges are faced in the Europe Sentiment Analysis Market?

Challenges include language diversity across Europe, data privacy regulations, and difficulty in analyzing sarcasm or complex expressions.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com