Europe Silicone Market Size, Share, Trends & Growth Forecast Report – Segmented By Technology (Elastomer, Paper), End User, and Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic & Rest of Europe), Industry Analysis From 2026 to 2034

Market Size, 2025

$6.14 BnMarket Estimate, 2026

$6.47 BnMarket Forecast, 2034

$9.83 BnCAGR, 2026–2034

5.37%Europe Silicone Market Report Summary

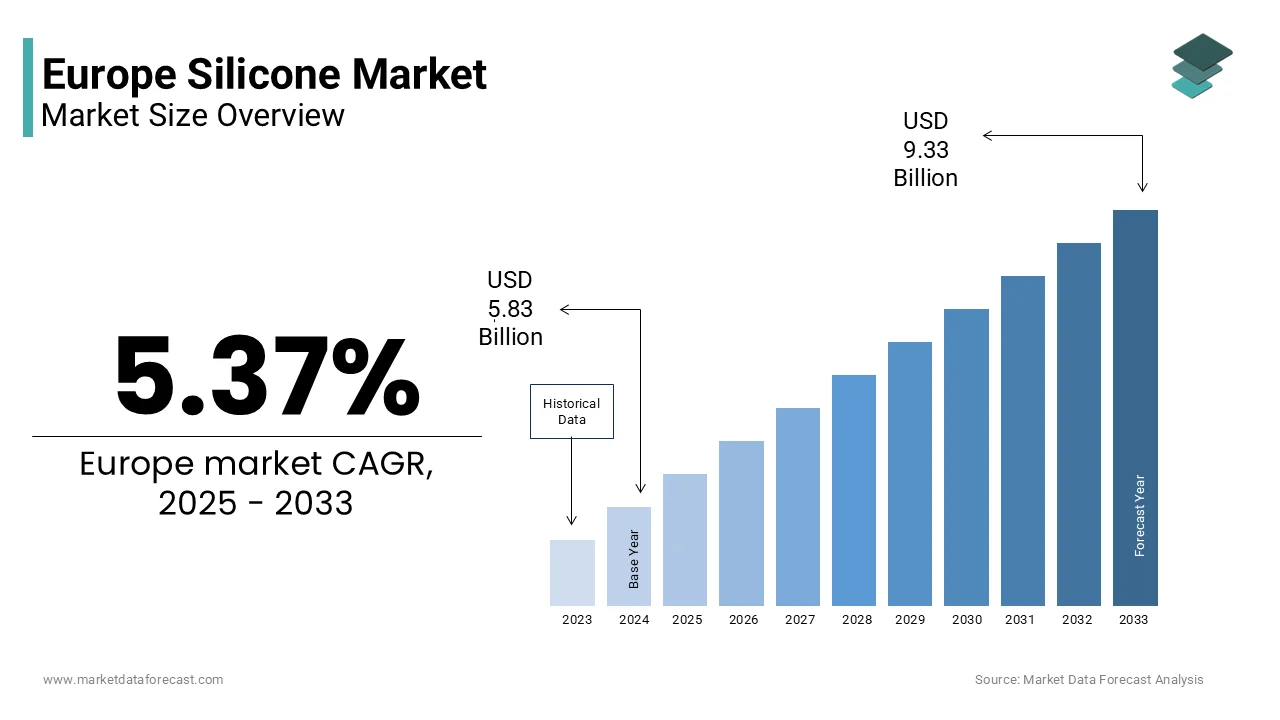

The Europe silicone market was valued at USD 6.14 billion in 2025, is estimated to reach USD 6.47 billion in 2026, and is projected to reach USD 9.83 billion by 2034, growing at a CAGR of 5.37% during the forecast period. Market growth is driven by rising demand for high-performance and durable materials across construction, automotive, electronics, and industrial applications. Increasing use of silicone-based sealants, adhesives, elastomers, and coatings due to their thermal stability, flexibility, and chemical resistance is further supporting market expansion. Additionally, growth in infrastructure development, renewable energy installations, and advanced manufacturing is reinforcing silicone consumption across Europe.

Key Market Trends

-

Germany emerged as the largest market, supported by strong industrial manufacturing, automotive production, and construction activity.

-

Western Europe continues to be a strong growth region, driven by infrastructure modernization and demand for energy-efficient building materials.

-

Increasing adoption of silicone elastomers in construction and industrial applications due to their durability, weather resistance, and long service life.

-

Rising use of silicone-based materials in green buildings, insulation, and sealants aligned with sustainability and energy efficiency goals.

-

Growing demand from electronics and automotive sectors for heat-resistant and high-purity silicone materials.

Segmental Insights

-

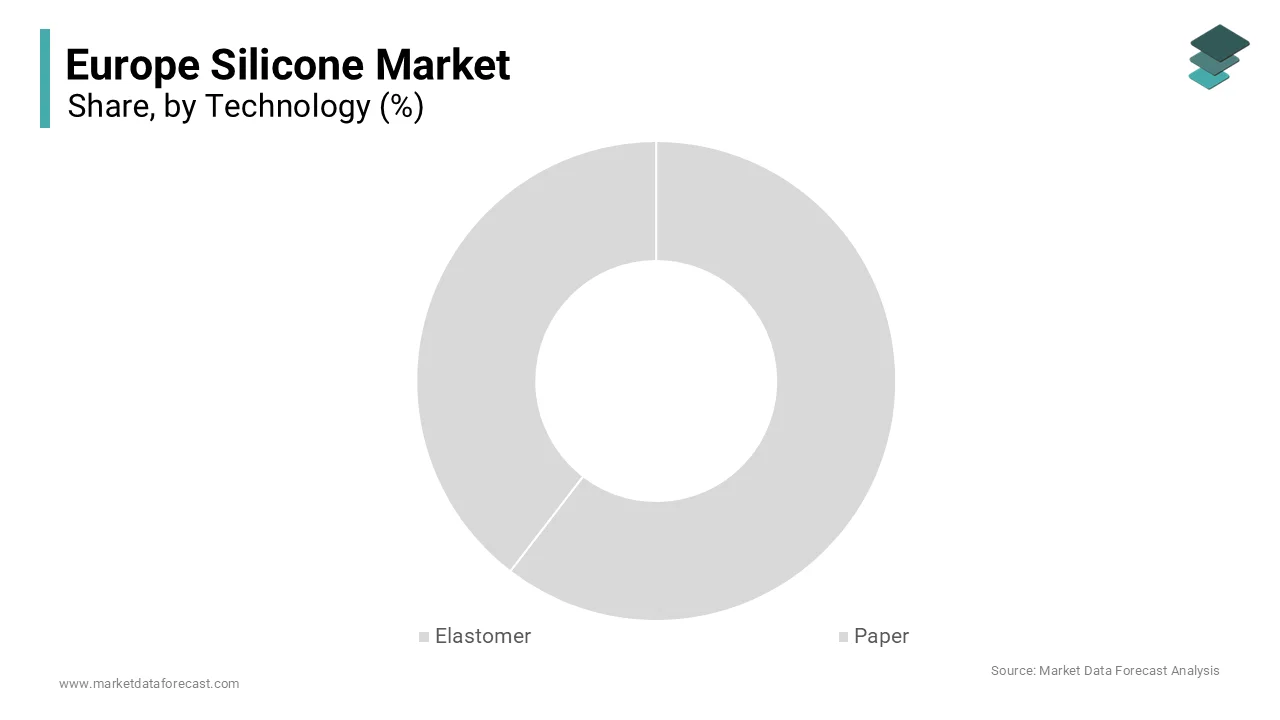

By technology, the elastomer segment dominated the Europe silicone market by occupying 2.5% of the market share in 2025, driven by widespread use in sealants, gaskets, adhesives, and flexible construction components.

-

By end user, the construction materials segment led the market by capturing 30.6% of the regional market share in 2025, supported by extensive use of silicone in sealants, waterproofing, insulation, and structural glazing applications.

Regional Insights

The European silicone market shows steady growth across major economies, supported by industrial activity and infrastructure development.

-

Germany dominated the market by commanding 23.5% of the regional market share in 2025, driven by its strong chemical manufacturing base and demand from construction and automotive industries.

-

France and the United Kingdom continue to witness stable demand, supported by renovation projects and industrial silicone applications.

-

Italy and Spain are emerging markets, driven by construction recovery and increasing use of advanced materials in manufacturing.

Competitive Landscape

The Europe silicone market is characterized by the presence of well-established global and regional chemical manufacturers with strong production capabilities and extensive product portfolios. Key players are focusing on capacity expansions, product innovation, and development of sustainable and high-performance silicone solutions. Strategic collaborations with construction, automotive, and electronics companies remain a key growth strategy. Prominent players operating in the European silicone market include Dow Inc., Wacker Chemie AG, Shin-Etsu Chemical Co., Ltd., Elkem ASA, Momentive Performance Materials Inc., Evonik Industries AG, KCC Corporation, Silchem Inc., H.B. Fuller Company, and Kaneka Corporation.

Europe Silicone Market Size

The Europe silicone market size was valued at USD 6.14 billion in 2025 and is projected to reach USD 9.83 billion by 2034 from USD 6.47 billion in 2026, growing at a CAGR of 5.37%.

The silicon is foundational materials for the semiconductor construction automotive and chemical industries. Silicon acts as an enabler for photovoltaic cells electric vehicle components and advanced electronics. According to Eurostat, the European Union imported approximately 85% of its silicon metal needs in 2022 highlighting a significant dependency on external suppliers primarily from Norway Brazil and China. The complex supply chain that transforms raw quartz into metallurgical grade silicon and subsequently into higher value added forms is elevating the growth of Europe silicon market. Regulatory frameworks such as the Critical Raw Materials Act aim to reduce this import reliance by boosting domestic production and recycling capabilities. The industry faces intense pressure to decarbonize production processes which are traditionally energy intensive. Consequently, the definition of the market now includes sustainability metrics alongside volume and value. The strategic importance of silicon has elevated it from a commodity to a geopolitical asset requiring coordinated policy interventions to secure supply chains and foster innovation in material efficiency.

MARKET DRIVERS

Expansion of Renewable Energy Infrastructure Drives Polysilicon Demand

The aggressive expansion of renewable energy infrastructure particularly solar photovoltaic installations is a major factor boosting the growth of Europe silicon market. Silicon is the fundamental material used in the manufacture of solar cells which convert sunlight into electricity. The European Union’s REPowerEU plan aims to accelerate the rollout of solar energy to reduce dependence on fossil fuels and enhance energy security. As per the SolarPower Europe association the EU installed 41.4 gigawatts of new solar capacity in 2022 representing a 47% increase compared to the previous year. This surge in installation rates directly correlates with an increased demand for high purity polysilicon. Governments across the continent are providing subsidies and incentives for both utility scale projects and residential rooftop installations. According to the International Energy Agency solar PV is set to become the largest source of electricity generation in Europe by 2027. This trajectory ensures a sustained and growing demand for silicon materials. Furthermore, the integration of solar panels into building materials and agricultural structures expands the application scope beyond traditional farms. The push for energy independence has made solar technology a strategic priority ensuring long term investment stability.

Surge in Electric Vehicle Production Boosts Semiconductor Grade Silicon

The rapid adoption of electric vehicles for semiconductor grade silicon, which is essential for power electronics and control systems is another attribute bolstering the growth of Europe silicon market. Electric vehicles require substantially more semiconductors than internal combustion engine vehicles due to the need for battery management systems inverters and advanced driver assistance systems. This shift necessitates a reliable supply of high purity silicon for the production of chips that manage power distribution and efficiency. Silicon carbide a compound derived from silicon is particularly valued for its ability to handle high voltages and temperatures in electric powertrains. According to the International Energy Agency the global stock of electric cars surpassed 26 million in 2022 with Europe being a key market. The European Green Deal mandates stricter emission standards encouraging automakers to accelerate electrification plans. This regulatory pressure combined with consumer preference for sustainable transport solutions sustains the upward trend in electric vehicle sales.

MARKET RESTRAINTS

High Energy Costs and Production Expenses Restrict Competitiveness

The high energy costs and production expenses, which undermine the competitiveness of domestic manufacturers is hampering the growth of Europe silicon market. Silicon production especially the conversion of quartz to metallurgical grade silicon is an extremely energy intensive process requiring substantial amounts of electricity. The recent energy crisis in Europe exacerbated by geopolitical tensions has led to volatile and elevated electricity prices. This spike in energy costs makes local production economically unviable compared to regions with cheaper energy sources such as China or Norway. Many European smelters have reduced output or temporarily closed operations to mitigate losses. According to the European Aluminum Association which also represents silicon producers the cost of energy accounts for up to 40% of total production costs. This financial burden discourages new investments in capacity expansion and threatens the survival of existing facilities. The lack of affordable and stable energy supplies forces companies to rely on imports thereby increasing supply chain vulnerability. Furthermore, the transition to green energy sources requires significant capital investment in infrastructure which adds to the operational costs.

Stringent Environmental Regulations Increase Compliance Burdens

The stringent environmental regulations are affecting operational flexibility and cost structures, which is primary factor hampering the growth of Europe silicon market. The production of silicon generates significant carbon emissions and waste products which are subject to strict regulatory oversight under the European Green Deal and the Industrial Emissions Directive. As per the European Environment Agency industrial facilities are required to implement best available techniques to minimize environmental impact which often involves costly upgrades to filtration and waste management systems. The Carbon Border Adjustment Mechanism further complicates the landscape by imposing tariffs on imports from countries with lower environmental standards potentially disrupting supply chains. According to the European Commission the goal of climate neutrality by 2050 requires all industrial sectors to drastically reduce their carbon footprints. Silicon producers must invest in cleaner technologies such as electric arc furnaces powered by renewable energy which require substantial capital expenditure. These regulatory pressures increase the overall cost of production and may lead to higher prices for end users. Additionally, the permitting process for new facilities or expansions is lengthy and complex delaying project timelines. Small and medium sized enterprises may lack the resources to comply with these rigorous standards leading to market consolidation.

MARKET OPPORTUNITIES

Development of Circular Economy and Recycling Initiatives

The development of circular economy principles and recycling initiatives to enhance sustainability and reduce import dependency is greatly influencing the growth of the Europe silicon market. Recycling silicon from end-of-life products, such as solar panels and electronic waste can provide a secondary source of high purity material. As per the International Renewable Energy Agency, the volume of solar panel waste is expected to reach 78 million tonnes globally by 2050 with Europe contributing a substantial share. Establishing efficient recycling infrastructure allows for the recovery of valuable silicon and other materials reducing the need for virgin raw material extraction. The European Union Waste Framework Directive encourages member states to improve recycling rates and develop closed loop systems. According to the European Commission, the Circular Economy Action Plan identifies electronics and batteries as key value chains for improvement. Innovations in hydrometallurgical and pyrometallurgical processes are making it increasingly feasible to recover silicon with high purity levels suitable for reuse in new applications. Companies that invest in recycling technologies can gain a competitive advantage by offering sustainable solutions to environmentally conscious customers. Furthermore, recycling reduces the environmental footprint associated with primary production aligning with corporate sustainability goals. Government funding and incentives for research and development in recycling technologies further support this opportunity.

Advancements in Silicon Carbide for High Performance Applications

The advancements in silicon carbide technology due to its superior performance in high power and high temperature applications is additionally levelling up the growth of Europe silicon market. Silicon carbide is a wide bandgap semiconductor that offers higher efficiency and durability compared to traditional silicon-based semiconductors. Europe is home to leading semiconductor manufacturers who are investing heavily in silicon carbide production facilities. The European Chips Act aims to strengthen the region's semiconductor ecosystem including the production of advanced materials like silicon carbide. According to the European Commission, the act mobilizes public and private investments to boost manufacturing capacity and innovation. The adoption of silicon carbide in electric vehicle inverters improves range and charging speed making it highly attractive to automakers. Additionally, its use in solar inverters enhances energy conversion efficiency. These applications drive demand for high quality silicon carbide substrates and epitaxial layers.

MARKET CHALLENGES

Supply Chain Vulnerability and Geopolitical Instability

The supply chain vulnerability and geopolitical instability, which threaten the consistent availability of raw materials is likely to restrict the growth of the Europe silicon market in coming years. Europe relies heavily on imports for silicon metal and polysilicon with limited domestic production capacity. Geopolitical tensions trade disputes and logistical disruptions can severely impact the flow of these critical materials. The conflict in Ukraine and subsequent sanctions have highlighted the risks of relying on single sources or unstable regions. According to the World Trade Organization, global supply chain disruptions have led to increased lead times and costs for industrial materials. This uncertainty makes it difficult for European manufacturers to plan production and meet customer demands. Diversifying supply sources is a complex and time consuming process requiring significant investment in new partnerships and infrastructure. Furthermore, the concentration of processing capabilities in a few countries exacerbates the risk of supply shocks.

Technological Complexity and Skill Shortages

The technological complexity and skill shortages, which hinder innovation and operational efficiency is also to inhibit the growth of Europe silicon market. The production and processing of silicon particularly for semiconductor applications require advanced technical expertise and specialized equipment. As per the European Centre for the Development of Vocational Training, there is a growing mismatch between the skills demanded by high tech industries and the available workforce in Europe. The shortage of engineers technicians and researchers with expertise in materials science and semiconductor manufacturing limits the industry's ability to innovate and scale up production. This skills gap is exacerbated by an aging workforce and insufficient training programs. According to the European Semiconductor Industry Association the industry needs to attract and retain talent to maintain its competitive edge globally. The complexity of silicon carbide and other advanced materials further increases the demand for specialized knowledge. Companies face difficulties in recruiting qualified personnel leading to delays in project implementation and increased labor costs. Additionally the rapid pace of technological change requires continuous upskilling of the existing workforce. Without adequate investment in education and training the industry risks falling behind in global competition.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 5.37% |

| Segments Covered | By Technology, End User, and Region |

| Various Analyses Covered | Global, Regional, & Country Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, and the Czech Republic |

| Market Leaders Profiled | Dow Inc., Wacker Chemie AG, Shin-Etsu Chemical Co., Ltd., Elkem ASA, Momentive Performance Materials Inc., Evonik Industries AG, KCC Corporation, Silchem Inc., H.B. Fuller Company, and Kaneka Corporation |

SEGMENTAL ANALYSIS

By Technology Insights

The elastomer segment was the largest by holding 52.4% of the Europe silicon market share in 2025 with the extensive use of silicone elastomers in automotive sealing gaskets and medical devices due to their thermal stability and flexibility. The automotive industry in Europe relies heavily on silicone rubber for engine components that must withstand high temperatures and harsh chemical environments. These materials offer superior resistance to aging and weathering compared to organic rubbers ensuring longer service life for vehicle components. In the healthcare sector, silicone elastomers are preferred for implants and tubing due to their biocompatibility and inert nature. As per the European Medical Device Industry the demand for medical devices continues to grow driven by an aging population and advanced healthcare infrastructure. Silicone’s ability to be sterilized without degradation makes it indispensable for surgical instruments and drug delivery systems. Furthermore the construction industry utilizes silicone sealants for glazing and joint sealing which are critical for energy efficient buildings.

The paper segment is projected to register a fastest CAGR of 6.8% during the forecast period with the increasing demand for silicone coated release papers in labeling and packaging applications. Release papers are essential for the production of self adhesive labels tapes and hygiene products where they prevent adhesives from sticking prematurely. The growth of the e commerce sector has spurred demand for pressure sensitive labels used in logistics and product identification. As per Eurostat the volume of parcel deliveries in the European Union increased significantly reflecting the boom in online retail which requires efficient labeling solutions. Silicone coated papers ensure smooth dispensing of labels in high speed automated printing and application processes. According to the European Label Forum the label industry is expanding due to stricter regulatory requirements for product information and branding. Additionally, the hygiene sector including diapers and feminine care products relies heavily on release liners made with silicone coatings.

By End User Insights

The construction materials segment held 35.4% of the Europe silicon market share in 2025 due to the widespread use of silicone sealants adhesives and protective coatings in building projects. Silicone based products are essential for weatherproofing insulation and glazing applications which are critical for energy efficient buildings. The European Union’s Energy Performance of Buildings Directive mandates higher energy efficiency standards driving the renovation of existing structures and the construction of new green buildings. According to study, the construction output in Europe is expected to grow steadily supported by public investment in infrastructure and housing. Silicone sealants provide durable airtight seals that prevent heat loss and moisture ingress enhancing the thermal performance of buildings. Furthermore, silicone coatings protect facades from environmental damage extending the lifespan of buildings and reducing maintenance costs. The versatility of silicones allows them to adhere to various substrates including glass metal and concrete making them ideal for modern architectural designs.

The electronics segment is expected to witness a fastest CAGR of 7.5% from 2026 to 2034 with the increasing miniaturization of electronic devices and the expansion of the semiconductor industry. Silicones are used as encapsulants thermal interface materials and conformal coatings to protect sensitive electronic components from heat moisture and mechanical stress. As per the European Semiconductor Industry Association, the demand for advanced packaging solutions is rising as devices become more powerful and compact. Silicone based thermal management materials are crucial for dissipating heat in high performance chips used in smartphones computers and automotive electronics. The proliferation of Internet of Things devices and 5G infrastructure further amplifies the need for reliable electronic protection. According to the International Data Corporation the number of connected devices in Europe is growing rapidly requiring robust materials to ensure operational reliability. Silicones offer excellent dielectric properties and stability over a wide temperature range making them ideal for these applications. The transition to electric vehicles also boosts demand for electronic components that require silicone protection.

REGIONAL ANALYSIS

Germany Silicon Market Analysis

Germany was the top performer of the Europe silicon market by occupying 26.3% of the share in 2025 due to its robust automotive and chemical industries. The country is home to major automobile manufacturers who extensively use silicone elastomers for sealing and insulation in vehicle production. According to the German Chemical Industry Association, the chemical sector including silicone production is a key pillar of the national economy benefiting from strong research and development capabilities. The presence of leading silicone manufacturers facilitates innovation in high performance materials for industrial applications. The construction sector in Germany also drives consumption through stringent energy efficiency regulations that require high quality sealants and insulation materials. Government initiatives promoting renewable energy and digitalization further support the adoption of silicon-based technologies in solar panels and electronics. The country’s focus on sustainability encourages the development of eco-friendly silicone formulations.

Italy Silicon Market Analysis

Italy silicon market growth is likely to witness prominent growth opportunities throughout the forecast period with the strong construction and personal care industry that utilizes significant volumes of silicone products. The construction sector in Italy drives demand for silicone sealants and adhesives used in renovation and new building projects. According to the National Institute of Statistics, the construction industry contributes substantially to the national GDP supporting the consumption of building materials. The personal care and cosmetics industry in Italy is renowned globally and relies on silicones for their sensory properties and stability in formulations. The automotive sector also contributes to market growth although to a lesser extent than Germany. Italian manufacturers focus on design and quality which aligns with the premium attributes of silicone materials. Regulatory compliance with European standards ensures the safety and environmental performance of silicone products.

France Silicon Market Analysis

France silicon market growth is likely to be driven by its aerospace automotive and construction sectors. The construction industry also contributes significantly through the renovation of residential and commercial buildings to improve energy efficiency. The country’s commitment to sustainability influences the development of bio based and recyclable silicone solutions. Major chemical companies in France invest in research to enhance the environmental profile of their products. The diverse industrial base ensures a steady demand for various silicone applications. France’s strategic focus on innovation and sustainability reinforces its market position.

United Kingdom Silicon Market Analysis

The United Kingdom silicon market growth is driven by its construction healthcare and personal care industries. The construction sector drives demand for silicone sealants and adhesives particularly in the context of building renovations and infrastructure projects. According to the Office for National Statistics, the construction industry remains a significant part of the UK economy supporting material consumption. The healthcare sector utilizes silicone elastomers for medical devices and implants benefiting from the country’s advanced medical infrastructure. The personal care industry also contributes through the formulation of cosmetics and hygiene products.

Spain Silicon Market Analysis

Spain silicon market growth is likely to grow with its construction tourism and automotive sectors. The construction industry is a primary driver due to ongoing infrastructure development and residential building projects. According to the National Statistics Institute of Spain, the construction sector has shown resilience and growth contributing to the demand for silicone sealants and coatings. The tourism industry supports the hospitality sector which requires durable and low maintenance materials for hotels and resorts. Silicone based products are preferred for their longevity and aesthetic appeal in such applications. The automotive industry in Spain also contributes to market growth through the production of vehicles that utilize silicone components. As per the Spanish Association of Automobile and Truck Manufacturers the country is a major vehicle producer in Europe. The personal care industry is expanding driven by domestic consumption and exports. Regulatory adherence to European standards ensures the quality and safety of silicone products.

COMPETITIVE LANDSCAPE

The competition in the Europe silicon market is characterized by the presence of established chemical giants and specialized producers who compete on technology sustainability and supply chain reliability. Market leaders leverage their integrated value chains to offer a broad range of silicon products from metallurgical grade to high purity polysilicon and specialty silicones. The shift towards sustainable and low carbon production methods has become a key differentiator as regulators impose stricter environmental standards. Companies are investing in green hydrogen and renewable energy to decarbonize their operations and gain a competitive edge. Innovation in application specific solutions for electronics automotive and construction sectors drives differentiation. Price volatility in raw materials and energy creates pressure on margins forcing companies to optimize operational efficiency. Consolidation through mergers and acquisitions is a common strategy to expand geographic reach and product portfolios. Supply chain resilience is critical given the region's dependency on imports.

KEY MARKET PLAYERS

Some of the notable key players in the European silicone market are

- Dow Inc.

- Wacker Chemie AG

- Shin-Etsu Chemical Co., Ltd.

- Elkem ASA

- Momentive Performance Materials Inc.

- Evonik Industries AG

- KCC Corporation

- Silchem Inc.

- H.B. Fuller Company

- Kaneka Corporation

Top Players in the Market

- Wacker Chemie AG is a leading global chemical company with a strong presence in the Europe silicon market through its comprehensive portfolio of polysilicon and silicone products. The company contributes significantly to the global market by supplying high purity polysilicon for solar applications and specialty silicones for various industries. Wacker actively invests in expanding its production capacities in Germany and the United States to meet growing demand. Recent actions include the optimization of its Burghausen site for sustainable silicone production and the development of bio-based silicone alternatives. The company focuses on energy efficiency and carbon reduction to align with European environmental standards. Wacker collaborates with customers to create innovative solutions for electronics construction and healthcare.

- Elkem ASA is a major international supplier of silicon based materials including silicon metal ferrosilicon and silicones with significant operations in Europe. The company plays a crucial role in the global market by providing essential materials for the aluminum steel and chemical industries. Elkem has been actively restructuring its business to focus on higher value added silicone products and sustainable solutions. Recent initiatives include the expansion of its silicone production facilities in France and the development of circular economy practices. The company invests in research and development to improve the environmental footprint of its operations. Elkem aims to become a leader in sustainable silicon solutions by leveraging its integrated value chain.

- Momentive Performance Materials Inc. is a global leader in silicone and quartz solutions with a substantial footprint in the Europe silicon market. The company provides a wide range of silicone elastomers fluids and resins for diverse applications including automotive aerospace and healthcare. Momentive contributes to the global market through its extensive distribution network and innovative product offerings. Recent actions include the launch of new high performance silicone formulations and investments in digitalization to enhance customer service. The company focuses on sustainability by developing recyclable silicone products and reducing emissions in its manufacturing processes. Momentive collaborates with industry partners to address complex material challenges. These efforts improve its market relevance and operational efficiency.

Top Strategies Used by the Key Market Participants

Key players in the Europe silicon market prioritize vertical integration to secure raw material supplies and control production costs amidst volatile energy prices. Companies invest heavily in research and development to create sustainable and bio based silicone alternatives that comply with strict environmental regulations. Expansion into high value added segments such as electronics and healthcare allows firms to diversify revenue streams and reduce dependence on commodity markets. Strategic partnerships with downstream manufacturers facilitate the development of customized solutions for specific applications. Manufacturers focus on enhancing energy efficiency in production processes to lower carbon footprints and meet sustainability goals. Digitalization of supply chains improves transparency and responsiveness to market changes. Investment in recycling technologies supports circular economy objectives and reduces waste.

MARKET SEGMENTATION

This research report on the European silicone market has been segmented and sub-segmented based on categories.

By Technology

- Elastomer

- Paper

By End User

- Transportation

- Construction Materials

- Electronics

- Healthcare

- Industrial Processes

- Personal Care and Consumer Products

- Other End-User Industries

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

1. What is driving the growth of the Europe silicone market?

Growth is driven by rising demand from construction, automotive, electronics, healthcare, and renewable energy sectors, supported by durability and thermal stability advantages.

2. Which countries dominate the Europe silicone market?

Germany leads due to strong industrial manufacturing, while France and the UK contribute significantly through construction, healthcare, and automotive applications.

3. What are the major types of silicone used in Europe?

Major types include elastomers, fluids, resins, and gels, with elastomers holding the largest share due to their flexibility and durability.

4. Which application segment holds the largest market share?

Construction is the largest application segment, driven by extensive use of silicone sealants, adhesives, and coatings

5. How does the automotive industry impact silicone demand in Europe?

The automotive sector uses silicones in gaskets, hoses, insulation, and electric vehicle components for heat resistance and longevity.

6. What role does healthcare play in the Europe silicone market?

Healthcare demand is supported by medical-grade silicones used in implants, catheters, tubing, and wearable medical devices.

7. How is the electronics industry contributing to market growth?

Silicones are widely used for insulation, encapsulation, and thermal management in semiconductors and electronic components.

8. How do regulations affect the Europe silicone market?

EU regulations such as REACH influence product formulations, manufacturing processes, and raw material sourcing.

9. What are the key challenges faced by the Europe silicone market?

Key challenges include fluctuating raw material prices and strict environmental and regulatory compliance requirements.

10. Which end-use industry is expected to grow at the fastest rate?

Electronics and renewable energy applications are expected to witness the fastest growth due to technological advancements.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com