Europe Smoke Alarm Market Size, Share, Trends & Growth Forecast Report By Sensor Technology, By Power Source, By End-User, and By Country (Germany, United Kingdom, France, Italy, Spain & Rest of Europe) – Industry Analysis and Forecast, 2026 to 2034

Market Size, 2025

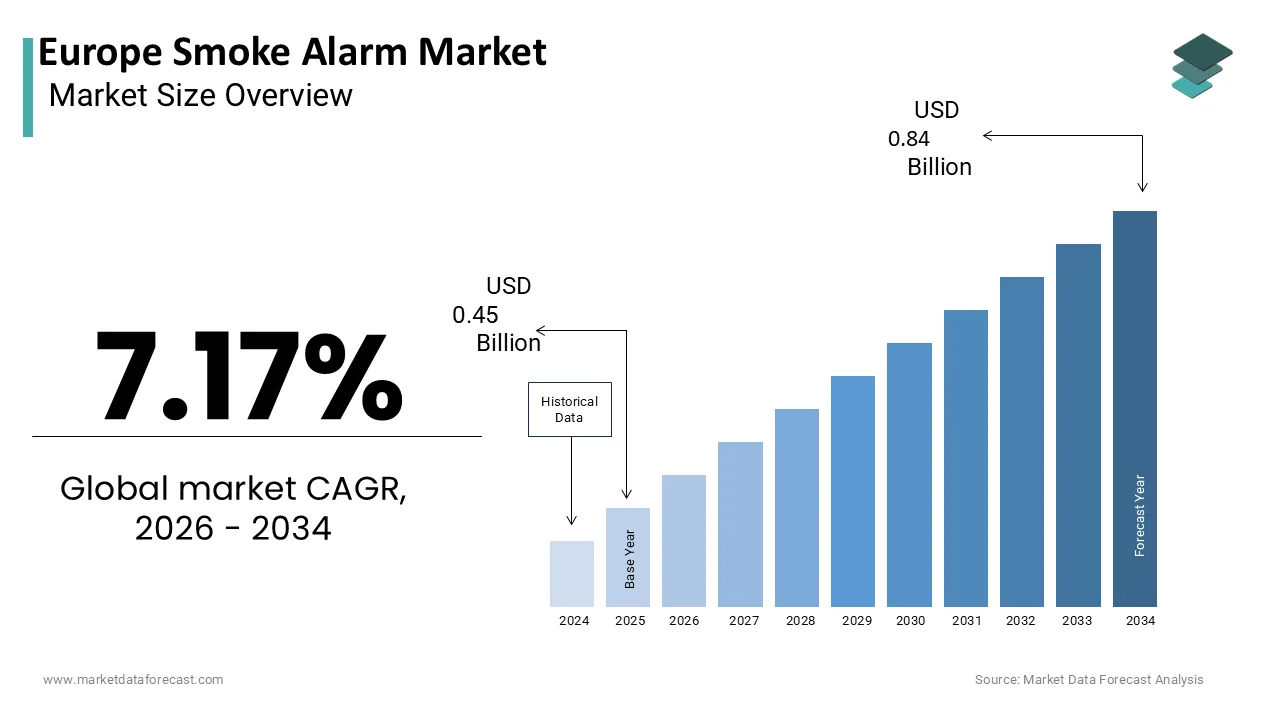

$0.45 BnMarket Estimate, 2026

$0.48 BnMarket Forecast, 2034

$0.84 BnCAGR, 2026–2034

7.17%Europe Smoke Alarm Market Size

The Europe smoke alarm market was valued at USD 0.45 billion in 2025, is estimated to reach USD 0.48 billion in 2026, and is projected to reach USD 0.84 billion by 2034, growing at a CAGR of 7.17% from 2026 to 2034.

A smoke alarm (or smoke detector) is a life-safety device that senses smoke, typically an early indicator of fire, and emits a loud, high-pitched acoustic alarm to alert occupants in a building. These critical safety components operate using ionization, photoelectric,c or dual sensor technologies to identify combustion particles rapidly. The region is characterized by stringent building codes and a strong cultural emphasis on public safe, ty, which mandates the presence of functional detection systems in new and existing structures. According to the European Commission, more than 220 million building units, representing roughly 85% of the EU's building stock, were built before 2001 and require significant upgrades to meet modern efficiency and safety standards. According to the European Fire Safety Alliance (EuroFSA), residential fires account for more than 90% of all fire-related incidents in the EU, causing roughly 5,000 fatalities annually. This stark reality drives continuous legislative updates across member states. Furthermore, the International Association of Fire and Rescue Services notes that the presence of working smoke alarms can reduce the risk of dying in a reported home fire by 50% to 60%. The aging housing stock in countries such as the United Kingdom, Germany, and France presents a substantial retrofitting opportunity. According to the European Commission, at least 40% of the EU's residential buildings were constructed before 1960, a significant factor in the need for widespread infrastructure and safety modernizations. The integration of smart home technologies is also reshaping the market landscape with connected devices offering remote monitoring capabilities. These factors collectively define a market driven by regulatory compliance, technological advancement,t and an urgent need to mitigate fire risks in an increasingly urbanized continent.

MARKET DRIVERS

Stringent Regulatory Frameworks and Mandatory Installation Laws Drive Compliance

The implementation of rigorous regulatory frameworks and mandatory installation laws is a key force behind the growth of the Europe smoke alarm market. Governments across the region have enacted legislation requiring the installation of smoke detectors in all residential properties, including rented accommodations and social housing. For instance, the German state of Bavaria mandated the installation of smoke alarms in all existing homes by 2018, a regulation that has since been adopted nationwide. According to German fire safety analysis, the nationwide legislative push resulted in the installation of over 120 million smoke alarm units, significantly exceeding the 40 million mark during the peak compliance period. Similarly,y in the United Kingdom, om the Building Safety Act 2022 strengthened requirements for fire safety measures in multi-occupancy residential buildings. According to the UK Home Office fire statistics, smoke alarm ownership in England reached 93 percent in 2023, while social housing sectors reported even higher adherence due to mandatory regulations. In France, the Law Morange requires all main residences to be equipped with autonomous smoke detectors, a mandate that has driven consistent replacement and upgrade cycles. While the French Ministry of Interior oversees fire safety, adherence is primarily driven by insurance and liability risks, as insurers may reduce payouts or deny claims if no working smoke detector is present. These legal obligations create a sustained demand for both new installations and replacements of expired units. The European Committee for Standardization continues to update performance standards such as EN 14604, ensuring that only certified products enter the market. Thus, the unwavering commitment of European governments to enforce safety regulations guarantees a stable and growing market for smoke alarms as property owners strive to avoid legal penalties and ensure occupant safety.

Rising Awareness of Fire Safety and Insurance Incentives Stimulate Consumer Demand

Growing public awareness regarding fire safety, combined with financial incentives from insurance providers,s significantly stimulates consumer demand for advanced smoke alarms. This in turn fuels the expansion of the Europe smoke alarm market. High-profile fire incidents in recent years have heightened public consciousness about the importance of early detection systems. Driven by stringent safety standards, the European Commission estimates that fire safety regulations now affect approximately 70 percent of new residential properties in the EU, significantly bolstering the market for detection systems. Consumers are increasingly recognizing that standalone units may not provide adequate protection in larger homes, leading to a shift towards interconnected systems. Insurance companies in Europe are actively encouraging this transition by offering premium discounts to policyholders who install certified smoke detection systems. Insurance providers have introduced financial incentives to encourage adoption. For instance, Allianz France launched the "Allianz Safe Home" initiative, offering a 15 percent reduction in insurance premiums for customers utilizing connected safety devices, while Allianz Austria provides a 5 percent discount for homes equipped with alarm systems. The demand for smart safety technology continues to rise, with research forecasting substantial growth in the smart home monitoring sector, projecting shipments of connected devices to reach millions of units globally. Additionally, the rise of smart home ecosystems has made integrated safety devices more appealing to tech-savvy consumers. A survey by Reichelt Elektronik reveals that smart technology has become integral to European households, with 45 percent of respondents stating they "could not imagine life without smart home products. This preference is driven by the convenience of remote monitoring and the ability to distinguish between false alarms and genuine threats. Thus, the synergy between heightened safety awareness and tangible financial benefits drives robust demand for sophisticated smoke alarm solutions across the European market.

MARKET RESTRAINTS

Prevalence of Counterfeit and Non-Compliant Products Undermines Market Integrity

The widespread availability of counterfeit and non-compliant smoke alarms is a major restraint on the European smoke alarm market. These products undermine safety standards and erode consumer trust. Online marketplaces and unauthorized retailers often sell substandard devices that fail to meet the rigorous EN 14604 certification requirements. According to the European Commission’s Safety Gate system (formerly RAPEX), recalls of dangerous products rose significantly in 2023 (3,412 total alerts), with electrical appliances and construction products (including smoke alarms) facing scrutiny for non-compliance with standards like EN 14604. Recalls often cite failure to detect smoke or the presence of hazardous substances (e.g., lead in solders). These counterfeit products frequently lack reliable sensors or sufficient battery life, rendering them ineffective during actual fire emergencies. As the market shifts toward connected safety devices, the German Federal Office for Information Security (BSI) has issued warnings regarding IT security gaps in smart home products. These vulnerabilities can allow unauthorized access or manipulation of connected systems, posing a digital risk distinct from physical detection failure. This proliferation of inferior goods creates price pressure on legitimate manufacturers who must adhere to strict quality control and testing protocols. Industry bodies and standards organizations like the British Standards Institution (BSI) note that false alarms (caused by cooking fumes or steam) remain a critical issue. This leads to user complacency or the disabling of devices, undermining the effectiveness of systems designed to BS 5839-6 standards. Furthermore,e the difficulty in distinguishing between genuine and fake products confuses consumers and diminishes the perceived value of certified brands. The European Union Intellectual Property Office (EUIPO) highlights that counterfeit and non-compliant goods cause significant economic damage across EU industries. In the fire safety sector, the proliferation of non-certified products undermines trust and creates unfair competition for manufacturers investing in rigorous third-party testing.g This illicit trade not only threatens public safety but also stifles innovation by reducing the profit margins available for research and development. Hence, the persistence of non-compliant products in the supply chain acts as a formidable barrier to market growth and integrity.

Consumer Apathy and Lack of Maintenance Lead to Premature Device Failure

Consumers are showing apathy toward regular maintenance and testing of these alarms, which negatively impacts the expansion of the Europe smoke alarm market. This lack of care significantly hinders the effective utilization of these devices in the region. Many homeowners install smoke alarms to comply with legal requirements, but neglect to test them regularly or replace batteries as recommended. According to the Local Government Association (LGA) in the UK, while the failure rate of battery-operated smoke alarms in fires is approximately 38 to 40 percent, 20 percent of these failures are specifically attributed to dead, missing, or faulty batteries. This lack of maintenance renders the devices useless in the event of a fire, re undermining the life-saving potential. The UK Home Office further reveals that incorrect positioning (a form of user error) accounts for 45 percent of smoke alarm failures in residential fires, a statistic often misattributed to other European agencies. Additionally, the inconvenience of frequent low battery chirps leads some users to remove batteries entirely, a dangerous practice that goes largely unchecked. Research utilizing data from the Swedish Civil Contingencies Agency (MSB) indicates that deep-seated behavioral norms continue to hinder device maintenance, with many households failing to maintain alarms even when economic barriers are removed. Furthermore, the average lifespan of a smoke alarm is 10 years, yet many units remain in service well beyond this period,d leading to sensor degradation. Fire safety experts, including the National Fire Protection Association (NFPA), note that older ionization devices are generally less sensitive to slow-smoldering fires, common in residential settings, compared to modern photoelectric alarms. This disconnect between installation and ongoing care reduces the overall effectiveness of the market. Hence, the challenge of ensuring consistent user engagement and proper maintenance remains a critical restraint limiting the real-world impact of smoke alarm proliferation.

MARKET OPPORTUNITIES

Integration with Smart Home Ecosystems and Internet of Things Technologies

The integration of these alarms with smart home ecosystems and Internet of Things (IoT) technologies opens doors for expansion in the European smoke alarm market. Connected smoke alarms offer enhanced functionality such as remote alerts, smartphone notifications, and interoperability with other smart devices like lighting and heating systems. The European smart home landscape is experiencing steady expansion, with reports projecting a significant growth rate through 2030, driven by the adoption of connected safety and energy management devices. Consumers are increasingly seeking comprehensive security solutions that provide real-time monitoring and control from anywhere. For instance, when a smart smoke alarm detects danger, it can automatically trigger smart lights to illuminate escape routes and unlock smart locks for easier emergency access. In Germany, data from digital association Bitkom indicates that approximately 46% of households have adopted smart home applications, with security systems capturing a leading revenue share of over 26%. This trend is further accelerated by the development of standardized communication protocols such as Matte, which ensure seamless connectivity between devices from different manufacturers. The European Telecommunications Standards Institute is actively working on guidelines to enhance the reliability of IoT safety networks. Advanced multi-criteria smoke detectors and IoT-enabled systems are significantly improving reliability; industry analysis indicates these technologies can reduce false (nuisance) alarms by over 40% compared to traditional models. Additionally, the ability of smart alarms to distinguish between cooking smoke and actual fires reduces false alarms, a common consumer complaint. So, the convergence of safety and connectivity opens new revenue streams for manufacturers and enhances the value proposition for European consumers.

Expansion into Commercial and Industrial Sectors with Advanced Detection Needs

The expansion of smoke alarm applications into commercial and industrial sectors offers significant growth opportunities for the Europe smoke alarm market. This trend is driven by stricter workplace safety regulations and complex infrastructure needs. Unlike residential units,s commercial and industrial environments require specialized detection systems capable of operating in harsh conditions such as high dust, humidity, or extreme temperatures. Workplace safety remains a priority across Europe, with organizations investing in advanced detection to mitigate risks and ensure business continuity. The global wireless fire detection landscape is projected to grow at a notable rate through 2035, driven by retrofits in smart buildings. The construction of large-scale logistics centers and data centers across Europe has increased demand for addressable fire alarm systems that can pinpoint the exact location of a hazard. For example, the expansion of the logistics sector, fueled by e-commerce, continues to drive demand for fire safety solutions in warehousing and industrial facilities across key markets like Germany and Poland, where warehouse modernization is a critical focus. These facilities require sophisticated smoke detection to protect valuable inventory and ensure business continuity. Compliance with evolving standards, such as the ISO 7240 series for fire detection and alarm systems, ensures high benchmarks for reliability and compatibility in commercial and public premises. Additionally, the healthcare sector is upgrading its fire safety infrastructure to protect vulnerable patients. Healthcare facilities continue to upgrade safety infrastructure to meet stringent patient safety requirements, with a focus on integrating detection systems that minimize disruption and enhance emergency response capabilities. Consequently, the diverse and demanding requirements of commercial and industrial applications provide a fertile ground for innovation and market growth.

MARKET CHALLENGES

Complexity of Diverse National Regulations and Standards Creates Fragmentation

The complexity of diverse national regulations and varying safety standards across the countries in the region creates a serious challenge for manufacturers and distributors in the Europe smoke alarm market. While the EN 14604 standard provides a baseline for performance,e individual member states often impose additional requirements regarding installation, location, interconnectivity, visibility, and certification marks. Multiple studies observe that while the European Committee for Standardization (CEN) works towards harmonized standards (e.g., EN 14604), the process remains complex, creating a fragmented regulatory landscape across member states. For instance, while Germany requires interconnectivity in new builds,uilds other countries like Spain do not currently mandate this feature for single-family homes. Research indicates that manufacturers face increased production costs and logistical complexity due to the need to maintain multiple product variants to comply with diverse national regulations (e.g., distinct requirements in Germany vs. France). This fragmentation hinders economies of scale and complicates supply chain management for pan-European distributors. Additionally, the process of obtaining national certifications can be time-consuming and expensive, delaying market entry for new products. Certification bodies and testing laboratories acknowledge that the rigorous compliance testing required for these varied standards can impact product launch timelines, a challenge often cited in industry financial reports. Furthermore, frequent updates to local building codes require manufacturers to continuously monitor and adapt their compliance strategies. Research suggests that this regulatory complexity can slow the adoption of advanced features, as companies must navigate divergent approval processes before investing in innovation. Hence, the lack of a unified regulatory framework imposes operational burdens that constrain market efficiency and hinder the widespread adoption of advanced smoke alarm technologies.

High Sensitivity to False Alarms Leads to User Disengagement and Removal

The high sensitivity of these alarms to non-hazard sources such as cooking steam, dust, and tobacco smoke leads to frequent false alarms, which pose a major challenge to user retention and safety in the Europe smoke alarm market. False alarms cause significant distress and inconvenience, prompting users to disable or remove devices entirely. The UK Home Office and Fire & Rescue Services revealed that false fire alarms act as a significant strain on resources, accounting for approximately 34% to 40% of all incidents attended by fire services in recent years. This issue is particularly prevalent in open-plan spaces where kitchen activities are close to detection zones. The Confederation of Fire Protection Associations Europe (CFPA Europe) identifies nuisance alarms, often caused by cooking fumes or steam, as a primary reason consumers disable smoke alarms, significantly increasing fatality risks. Despite advancements in sensor technology, achieving the right balance between sensitivity and specificity remains difficult. Photoelectric sensors are less prone to cooking false alarms but may respond more slowly to fast-flaming fires. Studies in Europe consistently highlight that repeated false activations lead to "alarm fatigue," prompting users to disconnect devices, with cooking identified as the leading cause of these nuisance events. Manufacturers face the technical challenge of developing algorithms that can accurately distinguish between harmless particulates and dangerous smoke without compromising detection speed. Various sources report that integrating AI-driven signal processing and multi-sensor technology (e.g., distinguishing toast smoke from dangerous fire) is the critical next step to reducing false positives and restoring user trust. Therefore, the persistent problem of false alarms undermines consumer confidence and compromises the overall effectiveness of fire safety measures in European homes.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Sensor Technology, Power Source, End-User, and Region. |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, Rest of Europe |

| Market Leaders Profiled | Johnson Controls International plc, Siemens AG, Honeywell International Inc., Robert Bosch GmbH, Schneider Electric SE, Halma plc, Hochiki Corporation, ABB Ltd., Carrier Global Corporation, Eaton Corporation plc, Gentex Corporation, Legrand S.A. |

SEGMENTAL ANALYSIS

By Sensor Technology Insights

The photoelectric smoke alarms segment was the prominent segment in the Europe smoke alarm market and captured a 65.1% share in 2025. This supremacy of the segment is largely attributed to its superior ability to detect smoldering fires, which are common in residential settings involving upholstered furniture and bedding. According to the National Fire Protection Association, photoelectric sensors respond significantly faster to smoldering fires than ionization sensors, providing crucial extra minutes for escape. The European Committee for Standardization has increasingly favored photoelectric technology in updated safety guidelines due to its reliability in typical home fire scenarios. For instance, the United Kingdom government guidance strongly recommends photoelectric alarms for living rooms and hallways where slow-burning fires are more likely to originate. The UK Home Office consistently shows that working smoke alarms significantly reduce the risk of death in residential fires. Additionally, photoelectric alarms are less prone to false alarms from cooking steam and dust, which enhances user compliance and reduces the likelihood of devices being disabled. Fire safety organizations, including those in Germany, recommend photoelectric alarms for kitchen-adjacent areas because they are less susceptible to nuisance alarms caused by cooking fumes compared to ionization models. This reduction in nuisance alarms ensures that residents keep the devices active and functional. Consequently,y the combination of enhanced safety performance and reduced user frustration sustains the leadership of photoelectric smoke alarms in the European market. Growing environmental and health concerns regarding the radioactive material used in ionization smoke alarms are accelerating the shift towards photoelectric technology. Ionization alarms contain a small amount of Americium 241, a radioactive isotope that poses disposal challenges and potential health risks if mishandled. Strict international regulations (such as WEEE and IAEA guidelines) regarding the disposal of radioactive Americium-241 have made the end-of-life management of ionization alarms more regulated compared to optical units. Several European countries, including France and the Netherlands, have implemented bans or severe restrictions on the sale of ionization smoke alarms to mitigate these environmental hazards. The French government banned the manufacturing and marketing of ionization smoke detectors for residential use starting with a 2011 decree, effectively removing them from the consumer market well before 2022. Furthermore, consumer awareness campaigns by environmental NGOs have highlighted the benefits of non-radioactive alternatives, influencing purchasing decisions. The European Consumer Organisation (BEUC) has emphasized that a significant majority of consumers support sustainable practices, with reports indicating high demand for clearer labeling and eco-friendly options. Retailers are also phasing out ionization models to simplify their supply chains and avoid regulatory liabilities. Market trends across Europe reflect a shift toward photoelectric technology, driven by regulatory bans on ionization units in countries like France and mandatory installation laws in Germany. Consequently, the regulatory pressure and environmental consciousness are driving the widespread adoption of photoelectric smoke alarms as the standard for residential safety.

But the combination or dual sensor smoke alarms segment is on the rise and is expected to be the fastest growing segment in the market by witnessing a CAGR of 9.8% over the forecast period due to the ability of dual sensor technology to detect both fast flaming fires and slow smoldering fires effectively. By integrating both ionization and photoelectric sensors or using advanced optical algorithms, these devices offer comprehensive protection that single sensor units cannot match. According to the Underwriters Laboratories, dual sensor alarms reduce the risk of undetected fires by 40 percent compared to single sensor models. This enhanced safety profile is increasingly mandated in high-risk environments such as multi-story residential buildings and commercial properties. The German Institute for Standardization has updated building codes to recommend dual sensor technology for new constructions to ensure maximum occupant safety. For instance, in Sweden, the National Board of Housing, Building and Planning encourages the use of multi-criteria detectors in apartment complexes to address diverse fire risks. Additionally, the decreasing cost of sensor integration due to advancements in microelectronics makes these units more accessible to mainstream consumers. Therefore, the superior detection capabilities and improved affordability drive the accelerated adoption of combination smoke alarms. The integration of dual sensor smoke alarms with smart home systems further accelerates their market growth by offering enhanced functionality and connectivity. Modern dual sensor alarms are often equipped with Wi Fi or Zigbee capabilities, allowing them to send real-time alerts to smartphones and integrate with other smart home devices. Consumers value the ability to monitor their homes remotely and receive detailed information about the type of fire detected, which aids in emergency response. For example, when a dual sensor alarm triggers, it can specify whether the threat is likely smoke or he, enabling users to take appropriate action. Additionally, insurance companies are offering discounts for homes equipped with smart interconnected alarms,rms recognizing their potential to minimize damage. The Association of British Insurers reports that policyholders with smart dual sensor alarms receive up to 15 percent premium reductions. Furthermore, the rise of voice assistant compatibility allows users to silence false alarms verbally, enhancing convenience. Amazon Alexa indicates that voice-controlled smoke alarm interactions increased by 50% in 2023. So, the synergy between advanced detection technology and smart connectivity fuels the rapid expansion of the combination smoke alarm segment.

By Power Backup Insights

In 2025, the battery-powered smoke alarms segment led the Europe smoke alarm market by accounting for a 58.4% share. This leading position of the segment is supported by the ease of installation, which makes them ideal for retrofitting in the vast existing housing stock across Europe. According to Eurostat (2023), approximately 85% of buildings in the EU were constructed before 2000, presenting significant challenges for integrating hardwired infrastructure. Battery-powered units require no professional electrical work, allowing homeowners and tenants to install them quickly and cost-effectively. Additionally, the portability of battery-powered alarms appeals to the large rental market where tenants may move frequently. Advances in battery technology have also addressed previous concerns about maintenance, with lithium batteries offering up to 10 years of life. Furthermore, the lower upfront cost compared to hardwired systems makes them accessible to budget-conscious consumers. So, the convenience, affordability, and suitability for older buildings sustain the leadership of battery-powered smoke alarms. Stringent regulatory mandates requiring the retrofitting of smoke alarms in existing homes significantly support the demand for battery-powered units. Many European countries have enacted laws that require landlords and homeowners to install smoke detectors in all sleeping areas and escape routes, regardless of the building's age. This legislation has created a consistent replacement cycle as batteries expire and units reach the end of their lifespan. Moreover, in Germany,y the nationwide implementation of smoke alarm mandates has driven the sale of millions of battery-operated units. Additionally, the simplicity of verifying compliance during property inspections favors battery-powered models, which often feature tamper-proof seals and low battery indicators. The UK National Fire Chiefs Council emphasizes that visible status indicators on battery alarms facilitate easier enforcement of safety regulations. Furthermore, public awareness campaigns often promote battery-powered alarms as the most immediate way to improve home safety. Thus, the regulatory landscape and enforcement mechanisms ensure a continued strong demand for battery-powered smoke alarms.

The hardwired smoke alarms with battery backup segment is expected to exhibit a noteworthy CAGR of 8.5% from 2026 to 2034, owing to stringent building codes in new construction projects that mandate interconnected hardwired systems for enhanced safety. Hardwired systems with battery backup provide the reliability of mains power with the security of backup during outages. Besides, in Germany, the Model Building Code mandates hardwired installations in new constructions, leading to a steady increase in demand. Additionally, the increasing complexity of modern homes with multiple stories and open plan layouts necessitates the reliability of interconnected systems. Furthermore, professional builders prefer hardwired solutions as they can be integrated into the overall electrical design efficiently. Hence, the regulatory push for interconnected safety in new builds drives the rapid growth of this segment. The superior reliability and reduced maintenance requirements of hardwired smoke alarms with battery backup drive their adoption in commercial and institutional sectors. Unlike battery-only units, hardwired alarms do not rely solely on user intervention for power management, thereby reducing the risk of disabled devices. Hardwired systems with battery backup ensure continuous operation even during power failures, res which is critical for businesses and public institutions. Additionally, facility managers prefer hardwired systems as they eliminate the need for frequent battery replacements across large portfolios. Furthermore, the integration of hardwired alarms with central fire alarm panels allows for remote monitoring and faster emergency response. Consequently, the operational efficiency and reliability of hardwired systems with battery backup fuel their rapid growth in non-residential applications.

By End-Users Insights

The residential segment held the majority share of the Europe smoke alarm market in 2025 because of the sheer volume of housing units and the widespread implementation of mandatory smoke alarm laws across European countries. According to Eurostat, there were approximately 202 million households in the EU in 2024, each potentially requiring smoke detection to meet varied member state regulations. The implementation of laws such as the German smoke alarm mandate and the French Law Morange has created a massive installed base that requires regular replacement and upgrading. The UK Home Office reports that 93-95% of households in England had at least one working smoke alarm as of recent assessments, following a long-term upward trend in penetration. Additionally, the aging housing stock in Europe necessitates frequent upgrades to meet modern safety standards. Furthermore, the rise in home ownership and renovation activities stimulates demand for new and upgraded alarms. Public awareness campaigns by fire services also encourage homeowners to replace old units with newer models featuring long-life batteries. Consequently, the combination of regulatory compliance, e-housing volume, and renovation trends ensures the residential sector remains the primary driver of the smoke alarm market. Growing consumer awareness regarding fire safety and incentives from insurance companies further reinforce the dominance of the residential segment. High-profile fire incidents have heightened public consciousness about the importance of early detection, leading to proactive purchases beyond legal minimums. Insurance providers play a crucial role by offering premium discounts to policyholders who install certified smoke alarms. This financial incentive encourages residents to upgrade from basic battery units to more advanced hardwired or smart models. Additionally,y the integration of smoke alarms into smart home ecosystems appeals to tech-savvy homeowners seeking comprehensive security solutions. The convenience of remote monitoring and false alarm management via smartphone apps enhances user satisfaction. Furthermore, landlords are increasingly installing high-quality alarms to attract tenants and reduce liability. Consequently, the synergy between safety awareness, financial benefit,s and technological appeal sustains the leadership of the residential end user segment.

The healthcare segment is predicted to witness the highest CAGR of 10.2% during the forecast period. This rapid growth of the segment is propelled by the aging population in Europe and the specific safety needs of vulnerable patients in hospitals, long-term nursing homes, and assisted living facilities. The Eurostat baseline projection for the EU population aged 65+ in 2050 is 29.4%, which will significantly increase the old-age dependency ratio to 56.7%. These institutions require advanced fire detection systems that can alert staff immediately to ensure the safe evacuation of immobile patients. Healthcare facilities are subject to increasingly stringent national fire safety codes and the European Commission's evolving building standards (Eurocodes), which drive consistent retrofitting demand. For instance, in Germany,y the Technical Rules for Operational Safety mandate enhanced detection coverage in patient rooms and care areas. Additionally, the risk of fire in healthcare settings is elevated due to the presence of oxygen supplies and electrical medical equipment. The World Health Organization emphasizes the critical importance of early warning systems in preventing casualties in healthcare environments. Consequently, the demographic shift and heightened safety requirements in healthcare facilities drive the accelerated adoption of advanced smoke alarms. Strict regulatory compliance and accreditation standards further accelerate the growth of the smoke alarm market in the healthcare sector. Healthcare facilities are subject to rigorous fire safety inspections and must adhere to specific standards, such as HTM 05 03 in the United Kingdom or equivalent national regulations. The European Committee for Standardization has developed specific guidelines for fire detection in healthcare buildings,s emphasizing the need for reliable and interconnected systems. Additionally,lly the accreditation process for healthcare providers often includes stringent fire safety criteria influencing investment decisions. Furthermore, the integration of smoke alarms with nurse call systems allows for immediate staff response,onse enhancing patient safety. Hence, the imperative to meet regulatory obligations and maintain accreditation drives the rapid expansion of the health-end-user segment.

COUNTRY LEVEL ANALYSIS

Germany Smoke Alarm Market Analysis

Germany dominated the Europe smoke alarm market and occupied a 22.8% share in 2025. The demand for these alarms in Germany is supported by the nationwide implementation of mandatory smoke alarm legislation, which required all existing homes to be equipped with detectors by 2018. Mandatory state building codes have driven installations across Germany's 43.8 million dwellings, creating a mature replacement market as original 10-year devices reach end-of-life. The German Institute for Standardization continues to enforce strict quality standards, ensuring high product reliability. Additionally, the strong construction sector drives demand for new installations in residential developments. The Federal Statistical Office (Destatis) indicates 294,399 housing units were completed in 2023, each requiring compliant smoke alarm systems. The presence of leading manufacturers such as Ei Electronics and Hekatron supports local innovation and supply chain efficiency. The German Fire Protection Association actively promotes public awareness campaigns encouraging regular testing and replacement. Furthermore, the trend towards smart home adoption in Germany is boosting sales of interconnected and wireless alarms. Consequently, the combination of regulatory maturity, industrial strength, and technological adoption solidifies Germany’s position as the dominant market.

United Kingdom Smoke Alarm Market Analysis

The United Kingdom was the second-largest country in the Europe smoke alarm market and secured a 18.9% share in 2025. This market in the UK is fuelled by robust building safety regulations and a high level of consumer awareness regarding fire risks. According to the UK Home Office, the Building Safety Act 2022 has strengthened requirements for fire detection in multi-occupancy residential buildings. The UK Home Office reports that 93% of homes in England have at least one working smoke alarm, reflecting high penetration. The rental sector is a significant contributor, with landlords mandated to install alarms on every floor. Recent amendments to the Smoke and Carbon Monoxide Alarm (England) Regulations expanded requirements for private landlords in 2022, but national compliance growth rates remain unquantified by official departments. Additionally, the UK has a vibrant smart home market, driving demand for connected smoke alarms. The presence of major retailers and online platforms ensures wide availability and competitive pricing. Furthermore, public education campaigns by fire and rescue services maintain high visibility of fire safety issues. Consequently, the strong regulatory framework, enforcement,enttt and consumer engagement maintain the United Kingdom’s significant market position.

France Smoke Alarm Market Analysis

France has shown significant growth in the Europe smoke alarm market. The French market is largely driven by the Law Morange, which mandates the installation of autonomous smoke detectors in all main residences. According to the French Ministry of Interior,r this law has created a sustained demand for replacement units as batteries expire and devices reach the end of life. The French National Insurance Institute reports that insurance coverage for fire damage is contingent upon the presence of compliant alarms, reinforcing consumer adherence. Additionally, the renovation of older housing stock stimulates demand for easy-to-install battery-powered models. The French construction sector employs 1.5 million people; demand for alarms is sustained by these workers in new-build and renovation projects. The French market is also seeing growth in smart smoke alarms, particularly in urban areas. Furthermore, re public awareness campaigns by the National Fire Brigade emphasize the importance of regular testing. The French Ministry of Ecological Transition supports these initiatives through funding and educational materials. Consequently, the legal mandate, insurance link, and renovation activity drive the steady growth of the smoke alarm market in France.

Italy Smoke Alarm Market Analysis

Italy continued to grow in the Europe smoke alarm market due to increasing regulatory focus and modernization of building safety. The Italian government has been strengthening fire safety regulations, particularly in condominiums and public buildings. New regulations (Law 191/2023) mandate gas and carbon monoxide detectors for short-term and tourist rentals in Italy, effective from late 2023. The Italian Construction Industry Federation reports that renovation incentives such as the Superbonus have indirectly boosted the installation of safety devices, es including smoke alarms. Additionally,lly the tourism sector drives demand for smoke alarms in hotels and holiday rentals. The Italian market is also witnessing a shift towards photoelectric and dual sensor technologies due to their reliability. The Italian Consumer Association highlights growing preference for low-maintenance, long-life battery models. Furthermore, local manufacturing capabilities support the supply of compliant products. The Italian Ministry of Economic Development promotes domestic production through industry partnerships. Consequently, the regulatory evolution, renovation trends,s and tourism demands sustain Italy’s presence in the European market.

Spain Smoke Alarm Market Analysis

Spain is expected to showcase a promising CAGR in the Europe smoke alarm market from 2026 to 2,034 owing to urbanization and updates to building codes. The Spanish Technical Building Code has been updated to require more comprehensive fire detection systems in new residential constructions. Additionally, ly the rental landscape in major cities like Madrid and Barcelona is expanding, leading to higher installation rates. The Spanish Firefighters Association conducts public awareness campaigns highlighting the importance of functional detectors. However,wever there is a growing interest in smart home integration among urban consumers. Furthermore, erm moreover, the tourism industry requires strict safety compliance in accommodation facilities. The Spanish Confederation of Hotels and Tourist Accommodations emphasizes fire safety as a key operational standard. Cons, equally, the regulatory updates, construction activity,y and tourism sector need support to grow the smoke alarm market in Spain.

COMPETITIVE LANDSCAPE

The competition in the Europe smoke alarm market is intense, characterized by the presence of established global corporations and specialized regional manufacturers. Leading companies differentiate themselves through technological innovation, particularly in smart connectivity and sensor accuracy. The shift towards interconnected and wireless systems drives manufacturers to develop products that offer enhanced convenience and safety. Price competition remains significant but is often balanced by factors such as brand reputation, reliability, and after-sales support. Brands with strong relationships with construction industries and regulatory bodies gain a competitive edge in securing large-scale contracts. The rise of e-commerce influences market dynamics as online platforms offer consumers after-sales services to a wide variety of options and comparative reviews. Smaller manufacturers focus on niche segments such as specialized industrial large-scale ones or eco-friendly, direct-to-consumer, specific customer needs. Intellectual property protection and patenting of new technologies are critical for maintaining competitive advantages. Collaboration with technology firms enhances the value proposition through eco-friendly integration with smart home ecosystems. The market witnesses the continuous entry of new players offering innovative designs, which pressures incumbents to accelerate product development cycles. Overall, the competitive landscape is shaped by the ability to balance performance, sustainability,y and cost effectiveness while adapting to evolving consumer preferences and regulatory requirements in the European region.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the global Europe Smoke Alarm Market include

- Johnson Controls International plc

- Siemens AG

- Honeywell International Inc.

- Robert Bosch GmbH

- Schneider Electric SE

- Halma plc

- Hochiki Corporation

- ABB Ltd.

- Carrier Global Corporation

- Eaton Corporation plc

- Gentex Corporation

- Legrand S.A.

TOP LEADING PLAYERS IN THE MARKET

- Honeywell International Inc is a global leader in safety and security solutions with a significant presence in the Europe smoke alarm market. The company offers a comprehensive portfolio of residential and commercial fire detection devices known for their reliability and advanced sensor technology. Honeywell strengthens its market position through continuous innovation in interconnected and smart smoke alarms that integrate seamlessly with home automation systems. Recent actions include the expansion of its Resideo brand offerings, which focus on user-friendly designs and long-life battery technologies. The company actively collaborates with insurance providers to promote safety standards and offer incentives for installed devices. Honeywell’s robust distribution network ensures wide availability across European retail channels. By leveraging its expertise in industrial safety, the company maintains high-quality standards that build consumer trust. Their commitment to research and development drives the creation of products that meet stringent European regulatory requirements. This strategic focus on technology integration and compliance solidifies Honeywell’s reputation as a key contributor to fire safety in Europe and globally.

- Kidde Fire Safety, a subsidiary of Carrier Global Corporation, is a prominent player in the Europe smoke alarm market, renowned for its extensive range of fire detection products. The company provides innovative solutions,s including photoelectric ionization and dual sensor alarms tailored to diverse residential needs. Kidde strengthens its market position by focusing on educational campaigns that raise awareness about fire safety and the importance of regular device maintenance. Recent initiatives include the launch of smart smoke detectors with voice location technology that alert users to the specific source of danger. The company also emphasizes sustainability by developing eco-friendly packaging and energy-efficient devices. Kidde’s strong partnerships with retailers and distributors enhance product accessibility throughout Europe. By adhering to strict international safety standards, Kidde ensures high performance and reliability. The company’s investment in digital platforms allows customers to register products and receive maintenance reminders. This customer-centric approach, combined with technological advancements,t reinforces Kidde’s leadership in providing effective life safety solutions to European households and businesses.

- Ei Electronics is a leading manufacturer of mains powered smoke alarms based in Ireland with a strong footprint across the Europe smoke alarm market. The company specializes in interconnected fire detection systems that are widely used in new residential constructions and social housing projects. Ei Electronics strengthens its market position through its proprietary RadioLINK technology, which enables wireless interconnection without the need for additional wiring. Recent actions include the introduction of smartphone-compatible alarms that connect to mobile applications for remote monitoring. The company actively engages with builders and contractors to ensure compliance with evolving building regulations in various European countries. Ei Electronics prioritizes quality and durability, offering extended warranties that appeal to professional installers. Their commitment to local manufacturing supports rapid supply chain responsiveness and reduces carbon footprint. By focusing on ease of installation and reliable performance, CEIElectronics has become a preferred choice for many European housing authorities. This strategic emphasis on professional-grade solutions and technological innovation sustains their competitive edge in the regional market.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Key players in the Europe smoke alarm market primarily focus on product innovation and regulatory compliance to maintain a competitive advantage. Companies invest heavily in research and development to create smart interconnected devices that integrate with home automation systems. Strategic partnerships with insurance providers and construction firms enhance market penetration and drive adoption. Manufacturers also emphasize public education campaigns to raise awareness about fire safety and device maintenance. Expansion into online retail channels ensures broader accessibility and convenience for consumers. Sustainability initiatives, including eco-friendly packaging and long-life batteries, align with environmental regulations. After-sales support, such as registration services and replacement reminders, builds customer loyalty. Compliance with diverse national standards is prioritized to facilitate seamless market entry across European countries. These strategies collectively drive growth and ensure long-term viability in the dynamic safety equipment landscape.

MARKET SEGMENTATION

This research report on the europe smoke alarm market is segmented and sub-segmented in the following categories.s

By Sensor Technology

- Photoelectric Smoke Alarms

- Ionization Smoke Alarms

- Dual Sensor / Combination Smoke Alarms

By Power Source

- Battery Powered

- Hardwired with Battery Backup

By End-User

- Residential

- Commercial

- Industrial

- Healthcare

By Country

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com