Europe Soil Moisture Monitoring System Market Size, Share, Trends, COVID-19 Impact & Growth Forecast Report, Segmented By Type, Application, And By Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic and Rest of Europe), Industry Analysis From 2025 to 2033

Europe Soil Moisture Monitoring System Market Size

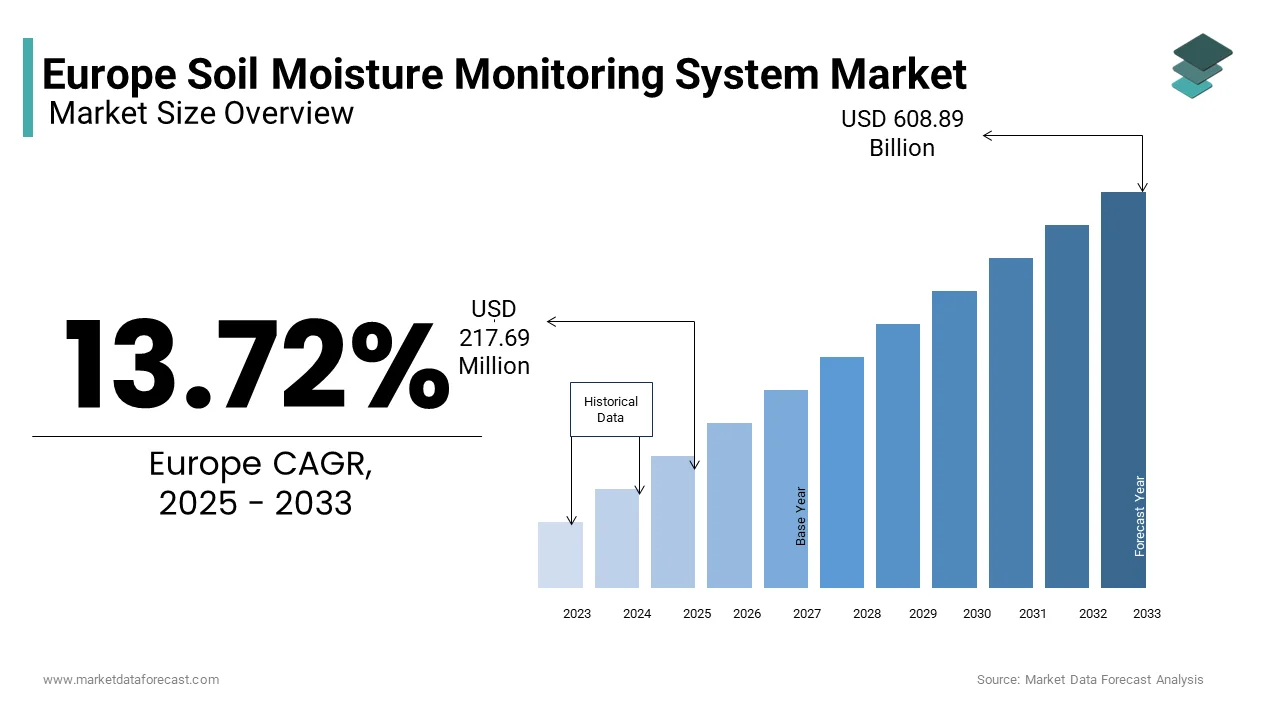

The Europe soil moisture monitoring system market was valued at USD 191.43 million in 2024 and is anticipated to reach USD 217.69 million in 2025 to USD 608.89 million by 2033, growing at a CAGR of 13.72% during the forecast period from 2025 to 2033.

The soil moisture monitoring systems utilize sensors such as time-domain reflectometry (TDR), capacitance probes, and remote sensing devices to provide real-time data on soil moisture levels. The growing emphasis on sustainable agriculture, climate resilience, and efficient water resource management has led to increased adoption across the continent.

In recent years, European countries have faced heightened challenges related to water scarcity and changing precipitation patterns. According to the European Environment Agency (EEA), approximately 11% of Europe’s land area and 17% of its population are affected by water stress, particularly in southern and eastern regions. Moreover, the European Commission’s Green Deal and Farm to Fork Strategy emphasize precision agriculture and reduced chemical input usage, reinforcing the importance of accurate soil moisture data. As per Eurostat, over 40% of total water abstraction in the EU is used for agriculture, making optimized irrigation essential.

MARKET DRIVERS

Increasing Agricultural Demand for Water Efficiency Amid Climate Change

The escalating need for water-efficient agricultural practices due to climate change and shifting weather patterns is amplifying the growth of the Europe Soil Moisture Monitoring System Market. Prolonged droughts, irregular rainfall, and rising temperatures have significantly impacted crop yields and irrigation reliability across several European regions. Farmers are increasingly adopting soil moisture monitoring systems to optimize irrigation schedules, reduce water waste, and enhance crop productivity. A study by Wageningen University revealed that farms using sensor-based irrigation techniques achieved up to 30% reduction in water consumption without compromising yield outcomes. Additionally, the European Union’s Common Agricultural Policy (CAP) encourages sustainable water use through subsidies and advisory services. As reported by the European Commission, over €10 billion was allocated under CAP's second pillar between 2023 and 2027 to support climate-smart farming initiatives, including precision irrigation tools.

Integration of Precision Agriculture and Smart Farming Technologies

The rapid integration of precision agriculture and smart farming technologies across Europe is another key driver of the Soil Moisture Monitoring System Market. Farmers are increasingly relying on digital tools to enhance decision-making, improve resource allocation, and increase operational efficiency. Soil moisture monitoring plays a central role in this transformation by providing real-time data that supports automated irrigation, variable rate fertilization, and predictive analytics.

According to the European Association of Agricultural Economists, over 35% of medium to large-scale farms in Western Europe had adopted some form of precision agriculture technology by 2023. Countries such as the Netherlands, Denmark, and the UK lead in adoption rates due to strong rural broadband infrastructure and government-backed innovation programs. The Horizon Europe initiative has funded numerous agri-tech projects integrating soil moisture data into AI-driven farm management platforms. Major agritech companies like Lely, John Deere Europe, and Bosch have introduced integrated sensor systems that communicate directly with autonomous machinery, enhancing precision in field operations. Additionally, the European Space Agency (ESA) has expanded its Copernicus program to include high-resolution soil moisture mapping via satellite, supporting both commercial and public sector applications.

MARKET RESTRAINTS

High Cost of Advanced Monitoring Systems for Small and Medium-Sized Farms

High costs remain a major barrier to widespread adoption among small and medium-sized farms across Europe is restraining the growth of the Europe Soil Moisture Monitoring System Market. The initial investment required for comprehensive monitoring setups, including sensors, telemetry units, cloud software, and installation,n can exceed €10,000 per farm, according to a report by the European Agricultural Machinery Industry Association (CEMA). Ongoing maintenance and subscription fees for data analytics platforms further add to the cost structure. Moreover, disparities in funding availability across EU member states contribute to uneven adoption rates. Although countries like Germany and the Netherlands offer robust subsidy programs, others such as Romania and Bulga, ria limited financial support for precision agriculture tools.

Limited Awareness and Technical Expertise Among Rural Farmers

The limited awareness and technical expertise among rural farmers regarding the benefits and operation of these systems are also hindering the growth of the Europe Soil Moisture Monitoring System Market. According to a survey conducted by the European Network for Rural Development (ENRD), less than 25% of surveyed farmers in Central and Eastern Europe were familiar with precision agriculture technologies, including soil moisture monitoring. Many agricultural advisory bodies struggle to keep pace with technological advancements, resulting in insufficient hands-on support for farmers transitioning to digital tools. Language barriers and regional disparities in digital literacy also hinder adoption. Educational materials and software interfaces are often available only in English or major national languages, posing difficulties for non-English-speaking farmers. Additionally, internet connectivity remains inconsistent in certain rural areas, impeding access to cloud-based monitoring solutions.

MARKET OPPORTUNITIES

Expansion of Government Subsidies and Sustainability Programs

The expansion of government subsidies and sustainability-focused agricultural programs aimed at promoting resource-efficient farming practices is creating new opportunities for the growth of the Europe Soil Moisture Monitoring System Market. The European Union has prioritized climate resilience and water conservation through initiatives such as the Common Agricultural Policy (CAP), the Green Deal, and the Farm to Fork Strategy. These policies encourage farmers to adopt precision irrigation technologies, including soil moisture monitoring systems, by offering financial incentives and technical support. Under the CAP Strategic Plans for 2023–2027, the European Commission has allocated over €9 billion to support sustainable farming practices, including investments in digital agriculture and irrigation efficiency. Several member states, including Germany, France, and the Netherlands, have introduced national-level grants that cover up to 60% of the cost of installing soil moisture sensors and related infrastructure. Additionally, cross-border collaborations such as the Danube Water Program and the Mediterranean Irrigation Initiative are fostering knowledge exchange and technology transfer among EU and non-EU countries.

Integration with Artificial Intelligence and Predictive Analytics Platforms

The integration of soil moisture monitoring systems with artificial intelligence (AI) and predictive analytics platforms presents a transformative opportunity for the Europe market. Modern agricultural operations increasingly rely on data-driven insights to optimize irrigation, manage soil health, and forecast yield outcomes. AI-powered platforms combine real-time soil moisture readings with satellite imagery, weather forecasts, and historical agronomic data to generate highly accurate recommendations for farmers. Several European agritech startups and established firms are developing AI-enhanced soil monitoring solutions. Companies such as Arable, Teralytic, and Sentek Europe have introduced platforms that leverage machine learning algorithms to analyze soil moisture fluctuations and predict irrigation needs with greater precision. According to a report by the European Innovation Partnership for Agricultural Productivity and Sustainability (EIP-AGRI), AI-integrated monitoring systems can improve water-use efficiency by up to 40%, reducing both operational costs and environmental impact. Furthermore, research institutions such as Wageningen University and ETH Zurich are collaborating with industry players to refine AI models for diverse soil types and climatic conditions across Europe. The European Commission has also supported these innovations through Horizon Europe funding, encouraging the development of next-generation digital farming tools.

MARKET CHALLENGES

Variability in Sensor Accuracy Across Different Soil Types and Climatic Conditions

The variability in sensor accuracy across different soil types and climatic conditions is acting as a barrier for the growth of the Europe Soil Moisture Monitoring System Market. Europe’s diverse landscape includes sandy soils in the Netherlands, loamy fields in Germany, and clay-rich terrains in parts of France and Italy. Each of these soil compositions affects how moisture is retained and measured, influencing the reliability of sensor readings. According to the European Geosciences Union (EGU), discrepancies of up to 12% have been observed in soil moisture measurements when identical sensors are deployed in varying soil textures. Temperature fluctuations, organic matter content, and salinity levels further complicate sensor performance, necessitating frequent recalibration and site-specific adjustments. Field studies conducted by the Joint Research Centre (JRC) of the European Commission revealed that standard calibration protocols do not adequately account for regional differences in soil properties, which is leading to inconsistencies in data interpretation.

Interoperability Issues Between Monitoring Devices and Farm Management Software

Interoperability is also one of the challenging factors for the growth of the Europe Soil Moisture Monitoring System Market in 2024. Farmers today deploy a variety of digital technologies—from GPS-guided tractors to nutrient management apps but often encounter difficulties consolidating soil moisture data with these platforms. According to a white paper published by the European Agricultural Machinery Association (CEMA), fewer than 30% of commercially available soil moisture sensors offer universal compatibility with leading farm data platforms such as Farm Management Web (FMWeb) or Ag Leader. Efforts are underway to standardize agricultural data exchange through initiatives like the Open Ag Data Alliance (OADA) and the AgGateway consortium, but widespread adoption remains slow. As per the European Commission’s Directorate-General for Agriculture and Rural Development, achieving full interoperability could take another five to seven years.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| CAGR | 13.72% |

| Segments Covered | By Type, Application, And By Country |

| Various Analyses Covered | Global, Regional & Country Level Analysis; Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic & Rest of Europe |

| Market Leaders Profiled | Stevens Water Monitoring Systems, Hebei Fei Meng Electric Technology, Campbell Scientific, China Huayun Group, McCrometer, Isaacs & Associates, Eco-Drip, Lindsay. |

SEGMENTAL ANALYSIS

By Type Insights

The granular matrix sensors system segment was accounted for holding a dominant share of the Europe Soil Moisture Monitoring System Market in 202,4 with its compatibility with diverse soil types and moisture conditions Unlike tensiometers that are limited to specific moisture ranges or FullStop systems that require complex setup, granular matrix sensors function effectively across a broad spectrum of soil textures and moisture levels. According to the European Environment Agency (EEA), over 55% of cultivated land in Europe consists of loamy and sandy soils, where granular matrix sensors deliver consistent readings without frequent recalibration. Another major factor fueling growth is integration with IoT-based farm management platforms. Leading agritech firms like Arable and Teralytic have embedded granular matrix sensors into wireless networks that provide real-time data to cloud-based analytics tools.

The fullStop system segment is swiftly emerging with a CAGR of 14.3% in the coming years, with the rising investment in greenhouse and controlled-environment agriculture (CEA. FullStop systems are particularly well-suited for hydroponic and vertical farming setups due to their ability to detect minute changes in soil moisture and prevent overwatering, which can lead to root diseases. Additionally, technological advancements in wireless connectivity and automated feedback loops have enhanced the usability of FullStop systems. Companies such as Sentek Europe and Delta-T Devices have introduced versions equipped with Bluetooth and LoRaWAN capabilities, allowing seamless integration with farm automation systems.

By Application Insights

The agriculture segment was the largest by occupying 54.3% of the Europe Soil Moisture Monitoring System Market share in 2024, with the increasing pressure on farmers to enhance water-use efficiency amid growing drought frequency. According to the European Drought Observatory, more than 40% of Europe experienced moderate to extreme drought conditions in 2023, which is prompting growers to adopt real-time soil moisture tracking as a means of conserving water resources. The expansion of precision agriculture technologies across large-scale commercial farms is propelling the growth of the Europe Soil Moisture Monitoring System Market. The European Commission reports that over 30% of EU farms now utilize some form of precision agriculture tool, including soil moisture sensors, to guide decision-making. Additionally, government incentive programs such as Germany’s Digital Agriculture Strategy and the Netherlands’ Smart Agri program support the adoption of these technologies.

The environmental protection segment is likely to exhibit a CAGR of 13.6% from 2025 to 2033. A key catalyst for this expansion is the rising focus on wildfire risk mitigation and forest health monitoring, particularly in drought-prone regions like southern France, northern Italy, and parts of Spain. According to the European Forest Institute, more than 7 million hectares of forest were affected by wildfires in Europe between 2020 and 2023, with the urgent need for early warning systems based on accurate soil moisture data. Environmental agencies and research institutions are deploying soil moisture sensors to assess fire danger levels and improve predictive modeling.

COUNTRY ANALYSIS

Germany

Germany was the largest contributor in the Europe Soil Moisture Monitoring System Market by holding 21.3% of stthearshare 2024. The rapid adoption of precision agriculture technologies in major crop-producing regions such as Bavaria and Lower Saxony is solely escalating the growth of the Europe Soil Moisture Monitoring System Market. According to the German Federal Ministry of Food and Agriculture, over 35% of farms had integrated precision agriculture tools by 2023, with soil moisture monitoring systems playing a central role in irrigation scheduling and crop health assessments. The availability of federal incentives, such as the Digital Agriculture Support Program, has further encouraged farmers to invest in sensor-based technologies. Additionally, the intensifying frequency of droughts and heatwaves has heightened demand for real-time soil moisture data. The German Weather Service (DWD) reported that in 2023, nearly 65% of the country was experiencing drought conditions in eastern and central regions. In response, regional agricultural boards have expanded their irrigation advisory services, incorporating real-time sensor data into decision-making processes.

France

France was positioned second with 16.2% of the Europe Soil Moisture Monitoring System Market share in 2024. While smaller in scale compared to Germany, France’s market is gaining momentum due to rising concerns over drought impacts, evolving agricultural policies, and increasing investments in smart farming technologies. The adoption is the recurrent drought conditions affecting major agricultural zones such as Aquitaine, Languedoc-Roussillon, and Provence-Alpes-Côte d'Azur, which collectively produce over 40% of France’s field crops, according to INRAE (French National Research Institute for Agriculture, Food and Environment). The French government’s active support through funding programs and agricultural modernization initiatives is gearing up the growth of the Europe Soil Moisture Monitoring System Market.

Italy

ItaThe ly Soil Moisture Monitoring System Market was positioned second with 12.3% of share in 2024. The persistent drought conditions are affecting major agricultural regions such as Lombardy, Emilia-Romagna, and Veneto, which together account for over 30% of Italy’s agricultural output according to the Italian National Institute of Statistics (ISTAT). Additionally, Italy’s participation in the European Union’s Common Agricultural Policy (CAP) has facilitated funding for digital agriculture and precision irrigation initiatives. Under the CAP Strategic Plan for Italy, over €900 million has been allocated between 2023 and 2027 to support sustainable water management and smart farming technologies.

Netherlands

The Netherlands Soil Moisture Monitoring System Market growth is propelled by the presence of high-tech greenhouse farming and export-oriented horticulture. Additionally, the strong presence of agritech startups and global agri-food corporations has fostered a favorable ecosystem for innovation in soil moisture monitoring. Companies such as Lely, Netafim, and Harkam have developed cutting-edge sensor technologies tailored for intensive farming applications. Furthermore, the Netherlands’ extensive network of agricultural knowledge institutes supports ongoing R&D in sensor calibration, data analytics, and AI-driven irrigation optimization.

Spain

The Spa in the Soil Moisture Monitoring System Market is escalating with the persistent water scarcity issues, increasing reliance on irrigated agriculture, and growing government support for sustainable farming practices. Additionally, national water management policies and EU-funded programs are encouraging the adoption of sensor-based irrigation systems. Under the Spanish Hydrological Planning Framework, over €500 million has been allocated between 2023 and 2027 to modernize irrigation infrastructure and promote water-saving technologies. Agritech companies and research institutions such as the Institute for Sustainable Agriculture (IAS-CSIC) are actively involved in developing region-specific soil moisture monitoring solutions.

KEY MARKET PLAYERS

Stevens Water Monitoring Systems, Hebei Fei Meng Electric Technology, Campbell Scientific, China Huayun Group, McCrometer, Isaacs & Associates, Eco-Drip, Lindsay. These are some of the market players dominating the Europe soil moisture monitoring systems market.

Top Players In The Market

One of the leading companies in the Europe Soil Moisture Monitoring System Market is Campbell Scientific, recognized for its high-quality environmental monitoring equipment. The company provides durable and precise soil moisture sensors widely used in agricultural, hydrological, and climate research applications. Campbell Scientific plays a vital role in supporting scientific studies and large-scale irrigation projects across Europe, contributing to global advancements in climate resilience and water resource management.

Another key player is Sentek Technologies, which is known for its innovative multi-depth soil moisture probes that offer accurate insights into soil water dynamics. Sentek’s solutions are extensively adopted in precision agriculture, helping European farmers optimize irrigation practices and improve crop yields. Their technology has been instrumental in promoting sustainable farming methods globally in regions facing water scarcity and changing climatic conditions.

Delta-T Devices is also a major contributor to the market, offering advanced soil moisture monitoring systems tailored for both field agriculture and scientific research. The company emphasizes reliability, ease of integration, and long-term performance, making its products popular among researchers, agronomists, and farm managers. Delta-T Devices continues to influence global trends in soil health monitoring and smart irrigation through continuous innovation and technical support.

Top Strategies Used By Key Market Participants

Key players in the Europe Soil Moisture Monitoring System Market are leveraging product innovation and technological integration to enhance functionality and usability. Companies are embedding IoT capabilities, wireless connectivity, and cloud-based analytics into their monitoring systems to provide real-time actionable insights for farmers and researchers.

Another major strategy involves strategic partnerships and collaborations with agricultural institutions and government agencies. Companies can align product development with user needs while also expanding awareness and adoption among end-users by working closely with research organizations and extension services.

Additionally, firms are emphasizing customer education and technical support programs to improve accessibility and ease of use. Training initiatives, digital platforms, and on-field demonstrations help bridge knowledge gaps, especially among small and mid-sized farms, by ensuring broader market penetration and long-term customer retention.

COMPETITION OVERVIEW

The competition in the Europe Soil Moisture Monitoring System Market is marked by a dynamic mix of established industry leaders and agile emerging players striving to capture a larger share through differentiation in technology, application adaptability, and service excellence. As demand for precision agriculture and environmental monitoring grows, companies are intensifying efforts to develop more accurate, durable, and scalable solutions tailored to diverse soil types and climatic conditions. While dominant firms leverage their brand reputation and extensive distribution networks, newer entrants are gaining traction through niche product portfolios and agile R&D strategies. The market landscape is also shaped by strategic collaborations, mergers, and acquisitions aimed at enhancing technical capabilities and geographic reach. Additionally, the increasing emphasis on sustainability and resource efficiency has prompted vendors to focus on interoperability with farm automation systems, further intensifying competitive dynamics.

RECENT HAPPENINGS IN THE MARKET

- In February 2024, Campbell Scientific launched an enhanced line of low-power, wireless soil moisture sensors designed for remote deployment in agricultural and ecological research settings, which improves data accuracy and transmission reliability.

- In May 2024, Sentek Technologies expanded its presence in Southern Europe by establishing a regional office in Spain that aimed at strengthening customer support and facilitating faster deployment of monitoring systems for local farmers and agritech partners.

- In July 2024, Delta-T Devices introduced a new calibration service tailored specifically for European soil types by enhancing sensor performance and reliability across different agricultural zones and climatic conditions.

- In October 2024, Arable partnered with a leading European agronomy institute to integrate its all-in-one soil and weather monitoring device into national irrigation advisory programs, which is increasing adoption among public and private sector users.

- In December 2024, Teralytic unveiled a modular soil moisture and nutrient sensing system compatible with existing farm automation platforms by enabling seamless integration for precision irrigation and fertilization planning across Europe.

MARKET SEGMENTATION

This research report on the Europe soil moisture monitoring system market is segmented and sub-segmented into the following categories.

By Type

- Granular Matrix Sensors System

- FullStop System

- Tensiometers System

By Application

- Environmental protection

- Agriculture

- Sandstorm Warning

- Others

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

What is a soil moisture monitoring system?

It’s a device or network that measures the water content in soil to help farmers, researchers, and land managers make informed irrigation and cultivation decisions. These systems use sensors placed at various depths to provide real-time or periodic moisture data.

Why is this market growing in Europe?

Increasing water scarcity, strict EU environmental regulations, and the push for sustainable farming are driving adoption across the region. Farmers are turning to precision agriculture to reduce waste and comply with resource efficiency standards.

Which countries in Europe are leading in adoption?

Germany, France, Italy, and the Netherlands are at the forefront due to advanced agricultural infrastructure and strong government support for smart farming. Nordic countries are also investing, especially in research and climate-resilient practices.

How do these systems benefit farmers?

They prevent over-irrigation, save water and energy costs, and improve crop yields by ensuring optimal soil conditions. Farmers gain better control over their operations, especially during dry summers or in drought-prone areas

What types of soil moisture sensors are commonly used?

Capacitive and tensiometric sensors are most popular for their accuracy and durability in different soil types. Some systems also integrate resistive or neutron probe-based technologies for specialized applications.

Are wireless and IoT-based systems common?

Yes, many modern systems use wireless connectivity and cloud platforms to send data directly to smartphones or farm management software. This allows remote monitoring and faster response, especially on large or multiple plots.

How do government policies support this market?

The EU’s Common Agricultural Policy (CAP) and Green Deal encourage efficient water use and digital farming tools through funding and incentives. National programs in several countries also subsidize sensor installations for small and medium farms.

What challenges do users face?

High initial costs, lack of technical knowledge, and inconsistent internet access in rural areas can slow adoption. Some farmers also struggle with interpreting data without proper training or support.

Can these systems help with climate adaptation?

Absolutely—they help farmers respond to changing rainfall patterns and prolonged dry spells by providing timely insights into soil conditions. This supports better planning and resilience against extreme weather.

What’s the future of soil moisture monitoring in Europe?

Expect wider integration with AI-driven farm platforms, increased use of satellite-assisted ground sensors, and growth in rental or subscription-based service models. The focus will remain on sustainability, automation, and ease of use.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com