Europe Sparkling Water Market Size, Share, Trends, & Growth Forecast Report By Type (Natural/Mineral, Caffeinated), Packaging and Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic and Rest of Europe), Industry Analysis From 2026 to 2034

Europe Sparkling Water Market Report Summary

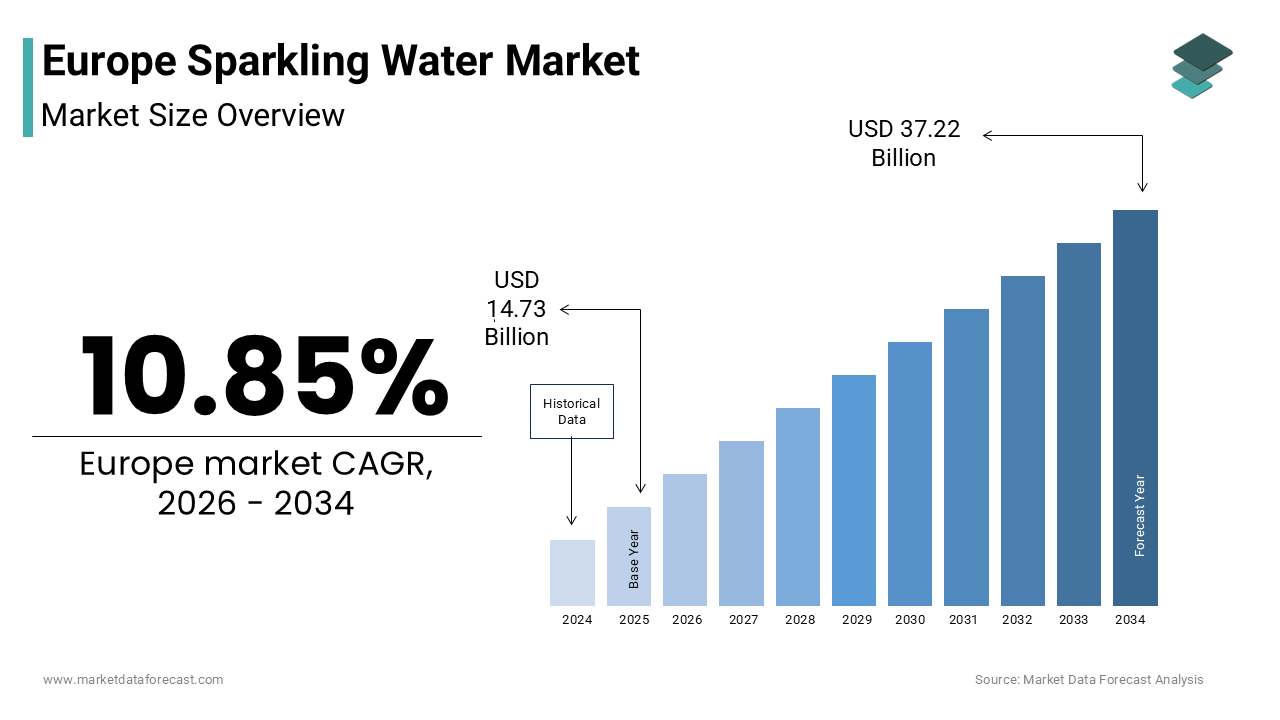

The Europe sparkling water market was valued at USD 14.73 billion in 2025, is estimated to reach USD 16.33 billion in 2026, and is projected to reach USD 37.22 billion by 2034, growing at a CAGR of 10.85% during the forecast period from 2026 to 2034. The growth of the Europe sparkling water market is driven by rising consumer preference for low-sugar beverage alternatives, strong cultural consumption habits in Central and Southern Europe, and increasing premiumization of naturally carbonated mineral waters. Expanding urban wellness trends, growth in alcohol-free social experiences, and innovation in flavored and functional sparkling beverages are further accelerating demand across European countries.

Key Market Trends

- Strong consumer shift toward zero-sugar and clean-label beverages replacing traditional soft drinks.

- The rising popularity of premium natural mineral sparkling water in wellness cafés and fine dining.

- Increasing adoption of canned formats due to sustainability perceptions and portability.

- Expansion of functional and caffeinated sparkling water targeting health-conscious consumers.

- Growth of sober-curious lifestyle trends is boosting sparkling water consumption in nightlife settings.

Segmental Insights

-

Based on type, the natural and mineral sparkling water segment held a prominent share of the Europe sparkling water market in 2024, supported by strong consumer trust in naturally sourced carbonation and clean-label positioning.

-

The caffeinated sparkling water segment is projected to witness the fastest CAGR during the forecast period due to increasing demand for low-calorie energy alternatives.

-

Based on packaging, the bottled segment dominated the market in 2024, driven by established dining culture, strong carbonation retention, and premium brand positioning.

-

The canned segment is expected to grow at the fastest rate owing to high recycling rates, urban on-the-go consumption, and eco-friendly perceptions among younger consumers.

Regional Insights

The Europe sparkling water market demonstrates strong regional variations influenced by culture, health awareness, and climate.

-

Germany led the Europe sparkling water market with a 28.3% share in 2024, driven by deeply rooted consumption habits and widespread availability of naturally carbonated mineral water.

-

Italy accounted for 19.2% of the market share in 2024, supported by strong gastronomic traditions and extensive mineral spring resources.

-

France maintains a premium market position through terroir-driven branding and substitution away from sugary beverages.

-

The United Kingdom is witnessing rapid growth as health policies and sugar taxes encourage consumers to shift toward sparkling water.

-

Spain is emerging as a high-growth market fueled by tourism, warmer climate conditions, and increasing adoption of flavored sparkling variants.

Competitive Landscape

The Europe sparkling water market is characterized by strong competition between heritage mineral water brands, multinational beverage companies, and innovative functional beverage startups. Leading companies focus on premium positioning, sustainability initiatives, packaging innovation, and expansion into alcohol-free social occasions. Major players operating in the Europe sparkling water market include Nestlé S.A., Danone S.A., PepsiCo Inc., The Coca-Cola Company, Sanpellegrino S.p.A., Gerolsteiner Brunnen GmbH & Co. KG, Ferrarelle Società Benefit S.p.A., Highland Spring Group, CG Roxane LLC (Crystal Geyser), and Vichy Catalan Corporation.

Europe Sparkling Water Market Size

The Europe sparkling water market size was valued at USD 14.73 billion in 2025 and is anticipated to reach USD 16.33 billion in 2026 from USD 37.22 billion by 2034, growing at a CAGR 10.85% during the forecast period from 2026 to 2034.

The sparkling water is a carbonated water that may be naturally sourced from mineral springs or artificially infused with carbon dioxide, often consumed as a non-alcoholic beverage alternative. The category includes plain sparkling water, flavored variants without added sugar, and premium mineral waters with naturally occurring carbonation. European consumers increasingly view sparkling water as a health-conscious substitute for sugary soft drinks by aligning with broader dietary shifts toward reduced sugar intake and clean label preferences. As per Eurostat, over 60% of adults in the European Union reported actively limiting their consumption of sugar sweetened beverages in 2023. According to the European Food Safety Authority, daily per capita water consumption across the EU averaged 1.8 liters in 2024, with carbonated water accounting for a growing share particularly in Southern and Central Europe. Germany, Italy, and France, collectively represent more than half of the region’s sparkling water volume consumption, driven by long standing cultural preferences and widespread retail availability.

MARKET DRIVERS

Health-Conscious Consumer Shift Toward Low Sugar Alternatives

The consumers are abandoning sugar laden soft drinks of healthier hydration options, with sparkling water of this behavioral transformation is driving the growth of Europe sparkling water market. According to the European Commission’s Special Eurobarometer on Food Safety published in 2023, 68% of EU citizens expressed concern about excessive sugar in their diets, prompting a measurable decline in regular soda purchases. Data from the World Health Organization Regional Office for Europe indicates that average per capita sugar consumption from beverages fell by 12% between 2019 and 2024, coinciding with a 23% rise in retail sales of unsweetened sparkling water across the EU. In Germany, the Federal Ministry of Food and Agriculture reported that households purchased sparkling water at least once a week in 2025 for cola type drinks. This trend is especially pronounced among urban millennials and Gen Z consumers who prioritize ingredient transparency and metabolic health. Retailers such as Carrefour and Edeka have responded by expanding shelf space for zero calorie carbonated water, often positioning it alongside functional beverages rather than traditional soft drinks.

Cultural Entrenchment of Carbonated Water in Daily Consumption Habits

The ingrained element of culinary and social routines is creating a durable foundation is additionally leveraging the growth of Europe sparkling water market. According to the German Mineral Water Association, over 70% of all bottled water consumed in Germany in 2024 was carbonated, a figure unmatched by any other major economy globally. Similarly, in Italy, the National Institute of Statistics noted that 58% of households regularly purchase naturally sparkling mineral water, often served during meals in restaurants and homes alike. This cultural normalization extends beyond domestic use, in Austria and Hungary, public fountains dispensing naturally carbonated spring water remain common in cities like Vienna and Budapest. As per a 2025 survey by the European Hydration Institute, consumers in Central and Southern Europe are three times more likely than their Northern counterparts to prefer carbonated over still water, citing sensory satisfaction and perceived digestive benefits. Such deeply rooted habits reduce susceptibility to short term market fluctuations and create a baseline demand that transcends marketing trends.

MARKET RESTRAINTS

Environmental Concerns Surrounding Single Use Plastic Packaging

The environmental footprint of its predominant packaging formats, particularly single use plastic bottles is majorly restricting the growth of Europe sparkling water market. According to the European Environment Agency, PET bottles accounted for nearly 40% of all plastic beverage containers placed on the EU market in 2024, with sparkling water brands contributing significantly due to higher internal pressure requirements that limit lightweighting options. The European Commission’s Circular Economy Action Plan mandates that all plastic bottles contain at least 30% recycled content by 2030, yet industry data from Plastics Europe shows that only 22% of PET used in carbonated water bottles met this threshold in 2025, primarily due to technical constraints in maintaining carbonation integrity with high rPET content. Moreover, a 2024 study by the Helmholtz Centre for Environmental Research found that carbonated beverage containers have a lower recycling yield than still water bottles because pressurized containers are more frequently discarded improperly or damaged during collection. These challenges are amplified by evolving Extended Producer Responsibility regulations, which now require manufacturers to bear full financial responsibility for end-of-life management. Consequently, brands face rising compliance costs and reputational risks, particularly in environmentally conscious markets like Sweden and the Netherlands, where municipal bans on single use plastics in public institutions are increasingly common.

Intensifying Competition from Emerging Functional Hydration Alternatives

The competitive displacement from a new wave of functional hydration beverages that offer added nutritional benefits beyond effervescence and taste is also hampering the growth of Europe sparkling water market. According to Euromonitor International, sales of functional sparkling drinks, such as those fortified with electrolytes, vitamins, or adaptogens grew by 34% in Western Europe between 2022 and 2025, while plain sparkling water growth slowed to 9% over the same period. Brands like Isostar and San Benedetto have launched vitamin enriched sparkling waters targeting fitness and wellness-oriented consumers, directly encroaching on traditional sparkling water users. As per the European Consumer Organisation BEUC, 47% of consumers aged 18 to 35 now consider “added functional benefits” a key factor when choosing non-alcoholic beverages, a metric that rose sharply after the pandemic heightened health awareness. Additionally, kombucha and fermented sparkling teas, though niche, recorded a 28% annual growth rate in France and Germany according to national food observatories, appealing to consumers seeking gut health advantages. This diversification fragments the market, compelling legacy sparkling water producers to either innovate beyond basic carbonation or risk brand erosion. The challenge is particularly acute for private label offerings, which lack the R&D capacity to rapidly integrate functional ingredients while maintaining clean label claims, thereby ceding ground to agile specialty brands.

MARKET OPPORTUNITIES

Expansion of Premium Naturally Sparkling Mineral Water in Urban Wellness Channels

The premiumization of naturally carbonated mineral water through specialized retail and hospitality channels that cater to health and sustainability minded urban consumers, which is anticipated to create new opportunities for the growth of Europe sparkling water market. According to the Italian Ministry of Economic Development, exports of premium Italian sparkling mineral waters, such as Acqua Panna and San Pellegrino grew by 18% in value terms across the EU in 2024, driven by demand from high end restaurants, boutique hotels, and organic grocery chains. In France, the Syndicat des Eaux Minerales reported that sales of glass bottled naturally sparkling water in Parisian wellness cafes and yoga studios increased by 41% between 2023 and 2025, reflecting a convergence of hydration, aesthetics, and ethical consumption. These venues emphasize terroir, geological origin, and trace mineral content attributes that resonate with consumers willing to pay a 30 to 50% price premium over standard sparkling water. The trend is further supported by EU regulations that strictly define “natural mineral water,” by ensuring authenticity and differentiating it from artificially carbonated alternatives.

Strategic Integration into Alcohol Free Social and Nightlife Experiences

The rapid growth of the sober curious movement presents a compelling avenue for sparkling water brands to position themselves as sophisticated, non-alcoholic alternatives in social settings traditionally dominated by beer and cocktails. The strategic integration into alcohol free social and nightlife experiences is additionally fuelling the growth of Europe sparkling water market. According to the UK’s Office for National Statistics, 29% of adults aged 16 to 34 identified as non-drinkers or occasional drinkers in 2025, up from 21% in 2019. This shift has the rise of alcohol-free bars and mocktail menus across cities like Berlin, Barcelona, and Amsterdam, where premium sparkling water serves as a foundational mixer. In Spain, the National Observatory on Youth and Alcohol reported that 44% of university students, now choose sparkling water with lime or mint as their default drink in nightclubs, signaling a cultural pivot away from peer pressured drinking. Beverage service providers such as Coca Cola HBC and Refresco have responded by developing bar specific sparkling water formats with enhanced fizz retention and elegant glassware compatibility.

MARKET CHALLENGES

Volatility in Natural Carbon Dioxide Supply Chains

The increasing instability in the supply of food grade carbon dioxide, a byproduct of industrial processes, such as ammonia production and ethanol fermentation is certainly a major factor to decline growth of Europe sparkling water market. According to the European Industrial Gases Association, two major CO₂ production facilities in the Netherlands and Poland underwent unscheduled shutdowns in early 2025 due to energy cost surges, triggering regional shortages that forced several bottlers to temporarily halt production. In 2022, a similar crisis led to a 30% spike in CO₂ prices across the EU, squeezing margins for small and mid-sized sparkling water producers lacking long term supply contracts. Unlike still water, carbonated products cannot be stored or distributed without consistent CO₂ injection during bottling, rendering inventory buffers ineffective. While some companies are investing in on site carbon capture systems, the European Commission estimates that less than beverage plants had such infrastructure as of 2025 due to high capital costs. This dependency on external, energy linked CO₂ sources introduces systemic fragility that could intensify with ongoing decarbonization policies affecting traditional industrial emitters.

Regulatory Fragmentation in Flavored Sparkling Water Labeling Across EU Member States

The inconsistent regulatory interpretations regarding the labeling of flavored variants, particularly concerning the use of natural flavors, sweeteners, and nutritional claims is also acting as a barrier for the growth of Europe sparkling water market. Although, the EU harmonized food labeling under Regulation EC No 1169/2011, national authorities retain discretion in enforcing definitions of terms like “naturally flavored” or “no added sugar.” According to the European Consumer Organisation BEUC, a 2024 audit revealed that identical sparkling water products were labeled differently in France, Germany, and Sweden, leading to consumer confusion and compliance burdens for pan European brands. For instance, Germany’s Federal Office of Consumer Protection requires explicit disclosure if carbonation is artificial, whereas Italy permits generic “sparkling water” labeling regardless of CO₂ source. The European Food Safety Authority tightened its stance in 2025 on the use of stevia and monk fruit extracts in beverages marketed as “natural,” prompting reformulations for over 60 brands operating in Benelux countries. As per the Confederation of the Food and Drink Industries of the EU, these divergences increase legal risk and force companies to maintain multiple SKUs for the same product, raising operational costs by an estimated 8 to 12%.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 10.85% |

| Segments Covered | By Type, Packaging and Region |

| Various Analyses Covered | Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

| Countries Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, the Netherlands, Turkey, the Czech Republic, and the Rest of Europe. |

| Market Leaders Profiled | Nestlé S.A., Danone S.A., PepsiCo Inc., The Coca-Cola Company, Sanpellegrino S.p.A., Gerolsteiner Brunnen GmbH & Co. KG, Ferrarelle Società Benefit S.p.A., Highland Spring Group, CG Roxane LLC (Crystal Geyser), and Vichy Catalan Corporation. |

SEGMENTAL ANALYSIS

By Type Insights

The natural and mineral sparkling water segment held a prominent share of the European sparkling water market in 2024 from deep rooted consumer trust in naturally sourced carbonation and strict EU regulatory definitions that protect the authenticity of natural mineral water. According to the European Commission’s Directorate General for Health and Food Safety, over 95% of consumers in Germany and Italy associate “natural sparkling water” with purity and digestive wellness, a perception reinforced by decades of cultural consumption. The German Mineral Water Association reported that in 2024, 73% of all bottled water sold in Germany was naturally carbonated mineral water, far exceeding artificially carbonated alternatives. Similarly, in France, the Syndicat des Eaux Minerales stated that natural sparkling waters accounted for premium bottled water sales in 2025, driven by terroir based branding and geological origin storytelling. Unlike caffeinated variants, which face scrutiny over stimulant content, natural mineral waters benefit from exemption from sugar taxes and clean label positioning. The European Food Safety Authority reaffirmed in 2024 that naturally carbonated waters require no additives, aligning with rising demand for ingredient simplicity. These structural and perceptual advantages ensure the segment’s continued hegemony across both retail and food service channels.

The caffeinated sparkling water segment is expected to grow at a fastest CAGR of 14.2% from 2025 to 2033 owing to the converging trends in functional beverage innovation, energy drink fatigue, and emand for low calorie stimulants among urban professionals. According to Euromonitor International, caffeinated sparkling water sales in Western Europe surged by 31% in 2024 alone, with brands like Bubly Boost and AHA gaining traction in the UK and Netherlands. As per the European Soft Drinks Association, 38% of adults aged 25 to 40 now seek alternatives to traditional energy drinks due to concerns about sugar and artificial ingredients, creating a receptive audience for lightly caffeinated sparkling options containing 30 to 50 milligrams per can comparable to a cup of green tea. In Sweden, the National Food Agency recorded a 45% year on year increase in new product launches featuring natural caffeine from green coffee bean or guarana in carbonated water formats. Retailers such as Tesco and Albert Heijn have dedicated shelf space to this emerging category, often placing it alongside sports and wellness beverages rather than soft drinks.

By Packaging Insights

The bottled packaging segment was accounted in capturing a significant share of the Europe sparkling water market in 2024 with the consumer familiarity, superior carbonation retention, and the entrenched role of glass and PET bottles in European dining culture. According to the European Container Glass Federation, over 60% of restaurants and cafes in Italy and France exclusively serve sparkling water in glass bottles, reinforcing perceptions of quality and authenticity. The German Packaging Institute noted that household sparkling water purchases in 2024 were in one liter or larger PET bottles, reflecting bulk consumption habits in Central Europe. Additionally, bottling infrastructure for carbonated water is mature and optimized, with over 85% of Europe’s mineral water sources directly linked to bottling plants, minimizing logistics costs. Retailers also favor bottles for their shelf stability and brand visibility, with premium labels like Perrier and San Pellegrino leveraging iconic bottle designs as key marketing assets.

The canned sparkling water segment is projected to grow at a CAGR of 16.8% from 2025 to 2033 owing to the portability, sustainability perceptions among younger demographics, and alignment with on the go consumption patterns in urban centers. According to Metal Packaging Europe, aluminum can recycling rates in the EU reached 76% in 2024, significantly higher than the 52% average for PET bottles by making cans a preferred choice for eco conscious millennials. In the UK, the Waste and Resources Action Programme reported that 57% of consumers aged 18 to 30 believe aluminum cans are more environmentally friendly than plastic, even when accounting for production emissions. The format’s rise is also tied to distribution expansion; vending machines, gyms, and convenience stores, which account for over 40% of impulse beverage purchases in cities like Amsterdam and Barcelona favor cans for their durability and stackability. Furthermore, aluminum’s superior barrier properties help maintain fizz longer than lightweight PET, addressing a key consumer complaint.

REGIONAL ANALYSIS

Germany Sparkling Water Market Analysis

Germany was the top performer of the Europe sparkling water market by holding 28.3% of share in 2024 owing to its unparalleled cultural integration of carbonated water into daily life. Sparkling water is not merely a beverage but a dietary norm, with the average German consuming over 100 liters annually. According to the German Mineral Water Association, 92% of households purchase sparkling mineral water regularly, and over 70% of all bottled water consumed is carbonated, a global outlier. The market thrives on a dense network of regional spring sources, with more than 500 licensed mineral water producers ensuring local availability and brand loyalty. Regulatory support also plays a role; Germany enforces strict labeling laws that differentiate natural carbonation from artificial, bolstering consumer trust. Retailers like Aldi and Lidl dedicate entire aisles to domestic sparkling water brands, often priced competitively against tap water alternatives. Urbanization has not diluted this preference; even in Berlin and Munich, sparkling water remains the default table beverage in both casual and fine dining establishments with its socio cultural embeddedness.

Italy Sparkling Water Market Analysis

Italy was ranked second by holding 19.2% of the European sparkling water market share in 2024 with the heritage of natural mineral springs and gastronomic traditions. Sparkling water is inseparable from Italian meals, with restaurants routinely serving it alongside still water as a standard offering. According to the Italian Ministry of Agricultural, Food and Forestry Policies, Italy hosts over 400 certified natural mineral water sources, many of which produce naturally effervescent water such as those in the Alps and Apennines. The National Institute of Statistics reported that 63% of Italian households consumed sparkling mineral water at least three times per week in 2024, with premium brands like Acqua Panna and Levissima leading volume sales. The “made in Italy” narrative extends to water, with consumers associating geological origin with health benefits and taste refinement. Unlike Northern Europe, where flavored variants gain ground, Italian consumers overwhelmingly prefer unflavored, naturally carbonated options, preserving market stability.

France Sparkling Water Market Analysis

France sparkling water market growth is likely to grow with the premium positioning and strong brand equity in natural mineral water. French consumers exhibit a marked preference for terroir driven products, with sparkling waters like Perrier and Badoit enjoying iconic status both domestically and internationally. The French Agency for Food, Environmental and Occupational Health & Safety confirmed that natural mineral waters are exempt from added ingredient labeling, reinforcing their clean image. Urban centers like Paris and Lyon have seen a rise in artisanal sparkling water bars, where sommelier style water pairings complement gourmet dining, an extension of France’s culinary sophistication. Moreover, the government’s Nutri Score system indirectly favors sparkling water by penalizing sugary drinks, accelerating substitution effects. France’s blend of regulatory clarity, cultural prestige, and export prowess solidifies its pivotal role in shaping European sparkling water preferences.

United Kingdom Sparkling Water Market Analysis

The United Kingdom holds the fourth position in the Europe sparkling water market with a 9% share in 2025, characterized by rapid innovation and shifting health consciousness post Brexit. While historically a still water market, the UK has witnessed a dramatic pivot toward sparkling formats, especially among younger demographics seeking soda alternatives. According to the UK’s Food Standards Agency, retail sales of unsweetened sparkling water grew by 27% between 2022 and 2024, outpacing all other non-alcoholic segments. This shift is amplified by the government’s Soft Drinks Industry Levy, which incentivized manufacturers to eliminate sugar and reposition carbonated water as a guilt free indulgence. Brands like Belvoir and Franklin & Sons have capitalized on this by launching British sourced sparkling waters with subtle botanical infusions, appealing to localism and clean label trends. Supermarkets such as Sainsbury’s and Waitrose have expanded sparkling water sections by 40% since 2023, often placing them near ready to drink cocktails and mocktails. Although natural mineral water imports dominate premium shelves, domestic production is rising, with new bottling facilities opening in Wales and the Lake District.

Spain Sparkling Water Market Analysis

Spain sparkling water market growth is fueled by tourism, urbanization, and rising health awareness. Traditionally a still water market, Spain has seen a notable uptick in sparkling water consumption, particularly in coastal regions and major cities like Madrid and Barcelona. According to Spain’s Ministry of Consumer Affairs, sparkling water sales increased by 19% in 2024, the highest annual growth in Southern Europe. Tourism plays a pivotal role with over 85 million international visitors in 2024, hotels and beach clubs routinely serve sparkling water as a premium alternative to soda, normalizing its use among locals. Domestic brands like Font Vella and Lanjaron have invested heavily in flavored sparkling variants using Mediterranean citrus, resonating with younger consumers. Additionally, Spain’s hot climate increases daily fluid intake needs, and sparkling water’s refreshing effervescence offers sensory appeal beyond plain hydration. Retail chains such as Mercadona have introduced private label sparkling waters in both glass and can formats, improving accessibility.

COMPETITIVE LANDSCAPE

Competition in the Europe sparkling water market is characterized by a blend of heritage brands and agile newcomers vying for consumer loyalty in a landscape shaped by health consciousness sustainability demands and cultural preferences. Established players like Nestle Waters Sanpellegrino and Danone dominate through geological exclusivity brand legacy and extensive distribution networks while regional bottlers maintain strong local footholds particularly in Germany and Italy. New entrants focus on functional enhancements eco-friendly packaging and direct to consumer models to disrupt traditional retail pathways. The rivalry intensifies in premium segments where terroir storytelling and gastronomic alignment serve as key differentiators. Simultaneously private label offerings from major retailers exert price pressure especially in value-oriented markets. Regulatory scrutiny around labeling carbonation sources and environmental compliance further raises operational stakes.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the Europe Sparkling Water Market include

- Nestlé S.A.

- Danone S.A.

- PepsiCo Inc.

- The Coca-Cola Company

- Sanpellegrino S.p.A.

- Gerolsteiner Brunnen GmbH & Co. KG

- Ferrarelle Società Benefit S.p.A.

- Highland Spring Group

- CG Roxane LLC (Crystal Geyser)

- Vichy Catalan Corporation

Top Players in the Market

Nestle Waters

Nestle Waters is a pivotal force in the Europe sparkling water market through its iconic brand Perrier which has become synonymous with premium naturally carbonated mineral water. The company leverages its deep geological sourcing rights in Vergeze France and maintains strict adherence to natural carbonation processes. In recent years Nestle Waters has intensified sustainability initiatives including transitioning to 100% recycled PET bottles across its European sparkling portfolio by 2025 and investing in water stewardship programs at source sites. It has also expanded distribution in urban wellness channels and introduced limited edition flavor infusions using natural essences to attract younger consumers without compromising its clean label identity.

Sanpellegrino S.p.A

Sanpellegrino S.p.A a subsidiary of Nestle operates as a standalone entity in Italy and holds cultural significance through its namesake San Pellegrino brand. The company controls one of Europe’s oldest and most renowned mineral springs in the Lombardy region and exports its sparkling water to over 150 countries. To reinforce its premium positioning Sanpellegrino has partnered with Michelin starred restaurants across Europe and launched glass bottle refill programs in high end hospitality venues. Recent actions include modernizing bottling facilities with AI driven quality control systems and launching a digital traceability platform that allows consumers to verify the origin and mineral composition of each bottle.

Danone

Danone operates its sparkling water business under the Badoit and Volvic brands with a strong presence in France and expanding reach in Benelux and Iberia. Badoit sourced from Saint Galmier is marketed as a gastronomic sparkling water often paired with fine dining experiences. Danone has prioritized circular economy commitments by tripling its use of food grade recycled plastic in sparkling water bottles since 2023 and piloting aluminum can formats for Badoit in select urban markets. The company also collaborates with European culinary institutes to promote sparkling water as an essential element of mindful eating reinforcing its role beyond mere hydration.

MARKET SEGMENTATION

This research report on the Europe Sparkling Water Market has been segmented and sub-segmented based on the following categories.

By Type

- Natural/Mineral

- Caffeinated

By Packaging

- Bottled

- Canned

- Other

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

What is the Europe Sparkling Water Market?

The Europe sparkling water market refers to the production, distribution, and consumption of carbonated water products across European countries, including plain and flavored variants sold through retail and foodservice channels.

What is driving consumer demand for sparkling water in Europe?

Growing health awareness, reduced sugar consumption, and preference for premium hydration options are major factors increasing demand for sparkling water across Europe.

How is flavored sparkling water influencing market growth?

Flavored sparkling water is attracting younger consumers and expanding the category beyond traditional mineral water, supporting faster market expansion.

Which distribution channels are important in the Europe sparkling water market?

Supermarkets and hypermarkets dominate sales, while online retail and convenience stores are rapidly growing due to changing shopping habits.

How do lifestyle trends impact sparkling water consumption in Europe?

Fitness culture, wellness movements, and clean-label preferences encourage consumers to replace sugary sodas with sparkling water.

What role does packaging innovation play in the market?

Brands are introducing recyclable cans, glass bottles, and sustainable packaging solutions to meet environmental expectations and improve brand image.

What challenges are faced by sparkling water manufacturers in Europe?

Key challenges include high production costs, strict regulations, and strong competition from energy drinks, flavored water, and functional beverages.

Which age group consumes the most sparkling water in Europe?

Young adults and urban consumers represent a significant share due to their preference for healthier and trendy beverage choices.

How is innovation shaping the Europe sparkling water market?

Manufacturers are introducing functional sparkling water with added vitamins, natural extracts, and zero-calorie formulations to attract new customers.

What is the long-term outlook for the Europe sparkling water market?

The market is expected to experience steady growth driven by sustainability trends, premiumization, and increasing awareness of healthy hydration.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com