Europe Stationary Catalytic Systems Market Size, Share, Trends, & Growth Forecast Report By Technology (Selective catalytic reduction and Oxidation catalyst), Application, Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic & Rest of Europe), Industry Analysis From 2026 to 2034

Europe Stationary Catalytic Systems Market Size

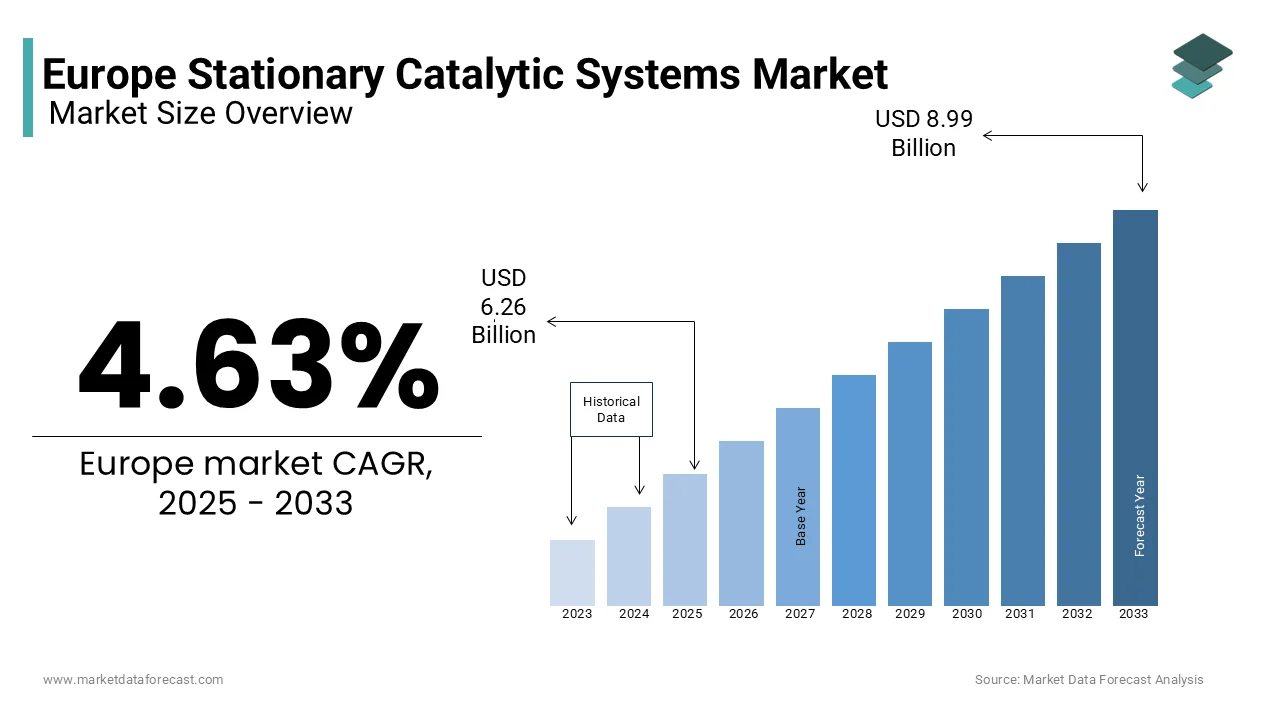

The Europe stationary catalytic systems market was worth USD 5.98 billion in 2024. The European market is expected to reach USD 8.99 billion by 2033 from USD 6.26 billion in 2025, growing at a CAGR of 4.63% from 2025 to 2033.

Stationary catalytic systems such as include selective catalytic reduction (SCR) and catalytic oxidizers are designed to mitigate pollutants such as nitrogen oxides (NOx), volatile organic compounds (VOCs), and carbon monoxide (CO) emitted by stationary sources like power plants, refineries, chemical facilities, and waste incinerators. These systems utilize catalysts, often composed of precious metals or metal oxides, to accelerate chemical reactions that break down pollutants into less harmful substances. According to the European Environment Agency, industrial emissions account for approximately 25% of total NOx emissions in the EU, underscoring the critical need for advanced emission control technologies.

The market growth in Europe is driven by stringent EU regulations, including the Industrial Emissions Directive (IED), which mandates industries to adopt best available techniques (BAT) for emission reduction. Countries like Germany and Sweden are leading adopters due to their robust industrial sectors and commitment to sustainability. According to the German Federal Ministry for Economic Affairs, over 60% of large-scale industrial facilities in Germany have integrated SCR systems to comply with NOx limits. As Europe accelerates its transition to a low-carbon economy, the demand for efficient and durable catalytic systems is expected to surge, reinforcing their importance in achieving emission reduction targets and fostering cleaner industrial operations.

MARKET DRIVERS

Stringent Environmental Regulations and Emission Standards

The European stationary catalytic systems market is significantly driven by stringent environmental regulations aimed at curbing industrial emissions. The European Environment Agency states that industrial activities contribute approximately 25% of total nitrogen oxide (NOx) emissions in the EU, prompting the implementation of the Industrial Emissions Directive (IED). This directive mandates industries to adopt best available techniques (BAT) for emission reduction, including catalytic systems. According to the German Federal Ministry for Economic Affairs, over 60% of large-scale industrial facilities in Germany have integrated selective catalytic reduction (SCR) systems to comply with NOx limits. Additionally, Eurostat reports that investments in emission control technologies have increased by 15% annually since 2020, driven by regulatory compliance. These policies are critical in fostering the adoption of catalytic systems, ensuring industries meet sustainability goals while reducing their environmental footprint.

Growing Focus on Sustainable Industrial Practices

The growing emphasis on sustainable industrial practices across Europe is further influencing the development of the European market. It is fueled by the EU’s Green Deal and net-zero emissions targets. As per the International Energy Agency, industries are increasingly adopting catalytic oxidizers and SCR systems to reduce volatile organic compounds (VOCs) and carbon monoxide (CO) emissions by up to 90%. Sweden’s Environmental Protection Agency notes that Swedish industries have reduced VOC emissions by 40% since 2015 through the integration of advanced catalytic systems. Furthermore, the European Investment Bank reports that funding for green industrial technologies has risen by 20% annually, supporting the transition to cleaner processes. As industries strive to align with Europe’s decarbonization goals, the demand for stationary catalytic systems is expected to grow, reinforcing their role in achieving energy-efficient and environmentally sustainable operations.

MARKET RESTRAINTS

High Initial Investment and Maintenance Costs

A major limitation in the European stationary catalytic systems market is the high upfront cost and continuous maintenance expenses of these systems. The International Energy Agency reports that installing a selective catalytic reduction (SCR) system can cost between €500,000 and €2 million, depending on the scale and complexity of the industrial facility. Additionally, according to the Eurostat, maintenance expenses for catalytic systems, including catalyst replacement, account for up to 20% of the total operational costs annually. These financial barriers are particularly challenging for small and medium-sized enterprises (SMEs), which represent a substantial portion of Europe’s industrial base. The German Federal Ministry for Economic Affairs notes that nearly 40% of SMEs delay adopting advanced emission control technologies due to budget constraints. This cost burden limits the widespread adoption of catalytic systems, despite their environmental benefits.

Limited Availability of Precious Metals for Catalysts

Another major restraint is the limited availability and rising costs of precious metals, such as platinum, palladium, and rhodium, which are critical components of catalytic systems. The European Environment Agency states that global supply chain disruptions have caused prices of these metals to surge by over 30% since 2020, impacting the affordability of catalyst production. Furthermore, the Swedish Environmental Protection Agency revealed that Europe relies heavily on imports for these materials, making the market vulnerable to geopolitical uncertainties. The scarcity of these resources also raises concerns about long-term sustainability. As industries face challenges in sourcing cost-effective catalysts, the development and deployment of alternative materials or technologies become imperative to ensure the continued growth and viability of the stationary catalytic systems market.

MARKET OPPORTUNITIES

Advancements in Catalyst Technology and Material Innovation

Advancements in catalyst technology and the creation of alternative materials represent a substantial opportunity for the European stationary catalytic systems market. The European Environment Agency found that research into non-precious metal catalysts, such as base metal oxides, could reduce system costs by up to 40%, making them more accessible for small and medium-sized enterprises (SMEs). Additionally, the International Energy Agency reports that innovations in nano-catalysts have improved efficiency by 25%, enabling industries to achieve higher emission reductions with smaller systems. Germany’s Federal Ministry for Economic Affairs notes that investments in R&D for sustainable catalysts have increased by 15% annually since 2020, driven by EU funding programs like Horizon Europe. These technological breakthroughs not only address cost and resource constraints but also align with Europe’s broader sustainability goals, positioning the market for long-term growth.

Rising Demand for Retrofitting Existing Industrial Facilities

Another key opportunity is the growing demand for retrofitting existing industrial facilities with advanced catalytic systems to comply with stricter emission standards. Eurostat reports that over 60% of industrial plants in Europe are over 20 years old, creating a substantial retrofitting market. The Swedish Environmental Protection Agency states that retrofitting SCR systems can reduce NOx emissions by up to 90%, significantly improving air quality. Furthermore, according to the European Investment Bank, governments across Europe have allocated over €1 billion annually in subsidies and low-interest loans for industrial emission control projects. This financial support, coupled with the EU’s push for decarbonization, creates a favorable environment for manufacturers and service providers to capitalize on retrofitting initiatives, driving both innovation and market expansion in the stationary catalytic systems sector.

MARKET CHALLENGES

Limited Awareness and Technical Expertise Among End Users

Limited awareness and technical expertise among end users, particularly small and medium-sized enterprises (SMEs) is a significant challenge in the European stationary catalytic systems market. The European Environment Agency stated that nearly 45% of SMEs lack sufficient knowledge about the benefits and operational requirements of catalytic systems, leading to hesitancy in adoption. Additionally, Eurostat reports that only 30% of industrial workers in Europe have received training on advanced emission control technologies, creates a skills gap that hinders proper installation and maintenance. The German Federal Ministry for Economic Affairs notes that improper handling or operation of these systems can reduce their efficiency by up to 20% increases operational risks and costs. This lack of awareness and technical know-how poses a barrier to market growth emphasizing the need for targeted education and training programs to bridge the knowledge gap.

Supply Chain Vulnerabilities for Critical Raw Materials

The vulnerability of supply chains for critical raw materials, such as platinum, palladium, and rhodium, which are essential for manufacturing catalysts are challenging the progress of this market. The Swedish Environmental Protection Agency states that Europe imports over **90% of these precious metals, making the market highly susceptible to geopolitical tensions and price volatility. The International Energy Agency reports that global supply chain disruptions have caused prices of these materials to increase by 35% since 2020, impacting production costs. Furthermore, the European Environment Agency warns that reliance on imported materials undermines the long-term sustainability of the market. As industries struggle to secure cost-effective and reliable supplies, there is an urgent need to develop alternative materials or recycling technologies to mitigate these risks and ensure the continued growth of the stationary catalytic systems market.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 4.63% |

| Segments Covered | By Technology, Application, and Country |

| Various Analyses Covered | Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

| Countries Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, and Rest of Europe |

| Market Leaders Profiled | Agriemach, Babcock & Wilcox, CECO Environmental, Cormetech, DCL International, Ducon, Environmental Energy Services, GE Vernova, Hug Engineering, Johnson Matthey, Kwangsung, MAN Energy Solutions, McGill AirClean, Mitsubishi Heavy Industries, Thermax, and Yara International. |

SEGMENTAL ANALYSIS

By Technology Insights

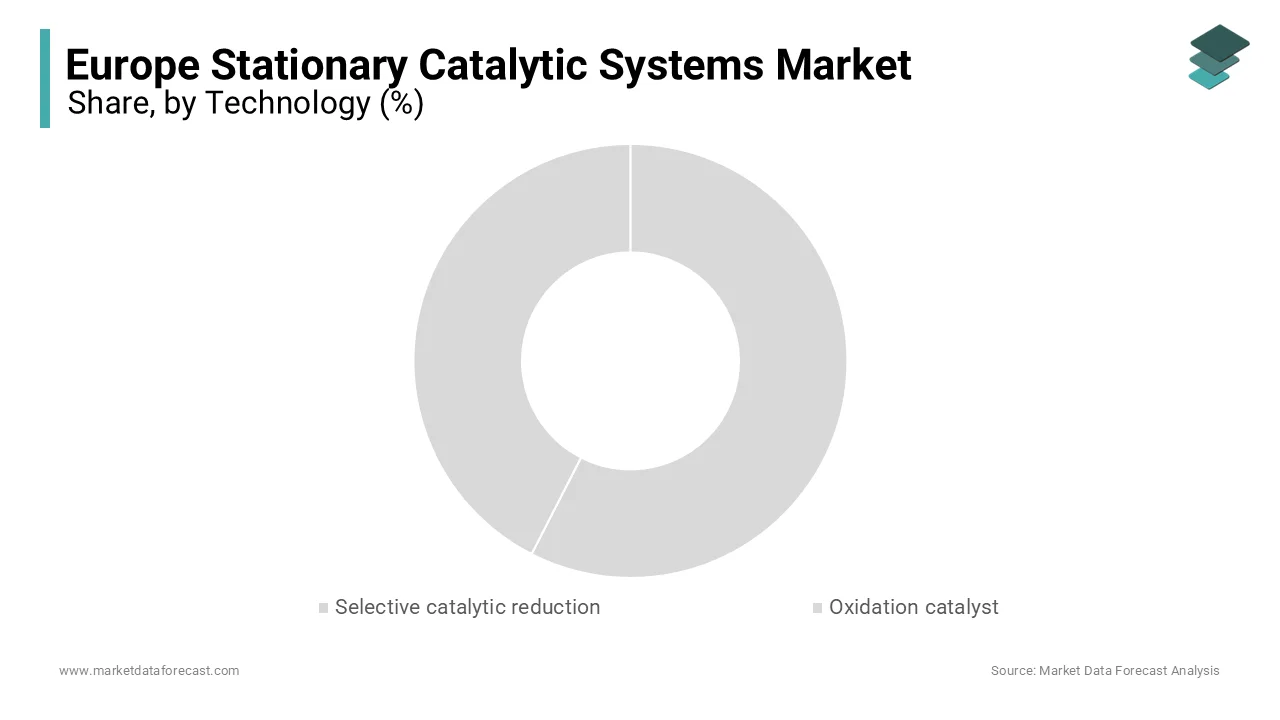

The selective Catalytic Reduction (SCR) segment commanded the European stationary catalytic systems market with a share of 60.5% in the European market in 2025. The unparalleled efficiency in reducing nitrogen oxides (NOx) emissions by up to 90% making it indispensable for industries like power generation and refining which is propelling the growth of this segment. The German Federal Ministry for Economic Affairs found that over 70% of large-scale industrial facilities in Germany rely on SCR systems to comply with stringent EU emission standards. With NOx being a major contributor to air pollution, SCR's role in achieving regulatory compliance and supporting Europe’s decarbonization goals underscores its critical importance.

The Oxidation catalysts segment is predicted to witness the highest CAGR of 7.2% from 2026 to 2034. The increasing demand for solutions to mitigate volatile organic compounds (VOCs) and carbon monoxide (CO) emissions, particularly in waste management and manufacturing is driving the growth of this segment. The Swedish Environmental Protection Agency notes that oxidation catalysts reduce VOC emissions by up to 85% and is aligning with EU air quality directives. As industries adopt sustainable practices, this segment is gaining traction for its cost-effectiveness and ability to address specific pollutants, making it vital for achieving cleaner industrial operations and meeting environmental targets.

By Application Insights

The Power plants segment led the European stationary catalytic systems market by holding 25.7% of the total market share in 2025. This dominance is driven by their significant contribution to nitrogen oxide (NOx) emissions, which account for nearly 30% of industrial air pollution in Europe. The German Federal Ministry for Economic Affairs stated that SCR systems reduce NOx emissions from power plants by up to 90%, ensuring compliance with the Industrial Emissions Directive (IED). With coal and gas-fired plants still prevalent, catalytic systems are critical for mitigating environmental impact while supporting Europe’s transition to cleaner energy sources.

The marine segment is expected to exhibit a noteworthy CAGR of 8.5% from 2026 to 2034. This growth is fueled by IMO 2020 regulations which mandate stricter sulfur and NOx emission limits. The Swedish Environmental Protection Agency notes that catalytic systems reduce maritime pollution by up to 80%, aligning with Europe’s focus on cleaner seas. As shipping companies adopt these technologies to comply with environmental standards, the marine segment is becoming vital for reducing emissions from one of Europe’s most polluting industries, underscoring its importance in achieving broader sustainability goals.

REGIONAL ANALYSIS

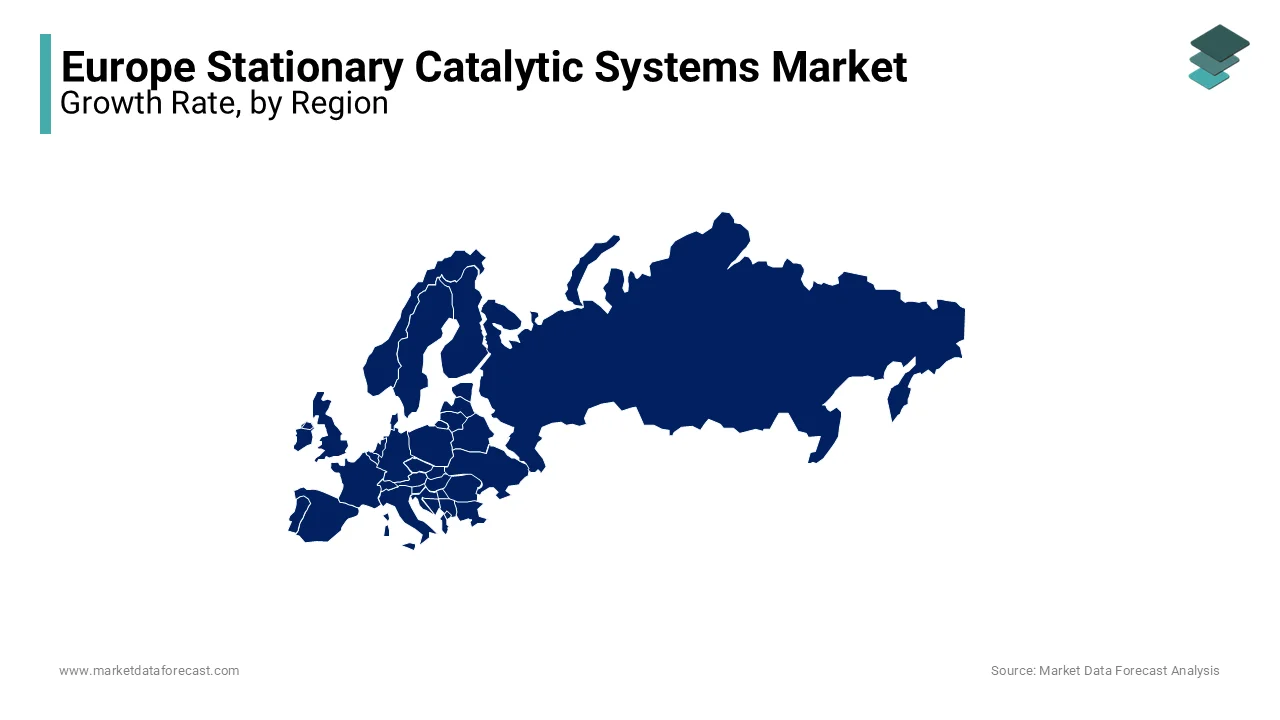

Germany dominated the Europe stationary catalytic systems market with a substantial share of 28.8% in 2024. This position in the market is linked to its strong industrial infrastructure, strict emission control regulations, and significant investments in renewable energy projects. The country’s focus on sustainability and green technologies has further bolstered its position. These factors have positioned Germany as a hub for innovation and adoption of catalytic systems.

France is predicted to have a CAGR of 4.9% during the forecast period. The French government’s initiatives to promote clean energy solutions and advancements in chemical manufacturing industries have been pivotal. France’s emphasis on reducing carbon footprints and adopting eco-friendly technologies has propelled its growth in this sector.

The United Kingdom have grown notably with Strategic Sustainability Efforts. The UK’s commitment to improving air quality through stringent policies and robust R&D activities has been instrumental in its success. The nation’s focus on sustainable practices and technological advancements has strengthened its position in the stationary catalytic systems market.

KEY MARKET PLAYERS

The major players in the European stationary catalytic systems market include

- Agriemach

- Babcock & Wilcox

- CECO Environmental

- Cormetech

- DCL International

- Ducon

- Environmental Energy Services

- GE Vernova

- Hug Engineering

- Johnson Matthey

- Kwangsung

- MAN Energy Solutions

- McGill AirClean

- Mitsubishi Heavy Industries

- Thermax

- Yara International

MARKET SEGMENTATION

This research report on the Europe stationary catalytic systems market is segmented and sub-segmented into the following categories.

By Technology

- Selective catalytic reduction

- Oxidation catalyst

By Application

- Power plants

- Chemical & petrochemical

- Cement

- Metal

- Marine

- Manufacturing

- Others

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

Which industries are the largest consumers of stationary catalytic systems in Europe?

The major industries using stationary catalytic systems in Europe include power generation, chemicals, cement, metal processing, and oil & gas.

What are the key factors driving the demand for stationary catalytic systems in Europe?

Stricter environmental regulations, increasing industrial emissions, and the need for sustainable energy production are the primary factors driving demand.

What are the latest technological advancements in stationary catalytic systems?

Recent advancements include high-efficiency catalysts, hybrid catalyst systems, and AI-based monitoring solutions for optimizing performance and reducing maintenance costs.

What is the future outlook for the stationary catalytic systems market in Europe?

The market is expected to grow steadily due to increasing environmental concerns, regulatory pressure, and the adoption of cleaner industrial processes.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com