Europe Structured Cabling Market Size, Share, Trends & Growth Forecast Report – Segmented By Product Type (Copper (Copper Cable, Copper Connectivity), Fiber (Fiber Cable (Single-Mode & Multi-Mode), Fiber Connectivity)), Application, and Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic & Rest of Europe), Industry Analysis From 2025 to 2033

Europe Structured Cabling Market Report Summary

The Europe structured cabling market was valued at USD 13.01 billion in 2024, is estimated to reach USD 13.96 billion in 2025, and is projected to grow to USD 24.55 billion by 2033, expanding at a CAGR of 7.31% from 2025 to 2033. Market growth is driven by the rapid expansion of data centers, increasing digital transformation across enterprises, rising adoption of high-speed communication networks, and the growing need for scalable IT infrastructure. Additionally, advancements in PoE technologies, cloud computing growth, and the rising demand for intelligent building systems are accelerating the adoption of structured cabling solutions across Europe.

Key Market Trends

- Increasing demand for high-speed network infrastructure due to cloud computing, IoT adoption, and enterprise digitalization.

- Growing deployment of fiber-rich networks in hyperscale and colocation data centers.

- Rising preference for modular, easy-to-upgrade cabling systems in smart buildings and industrial automation.

- Adoption of PoE-enabled cabling solutions supporting IP-based devices such as CCTV, VoIP systems, and access controls.

- Strong push toward energy-efficient, sustainable cabling designs across Europe to meet regulatory and corporate ESG goals.

Segmental Insights

- Based on product type, the copper cabling was the largest segment, accounting for 59.5% of the Europe structured cabling market share in 2024, driven by its cost-effectiveness, durability, and widespread use in enterprise LANs.

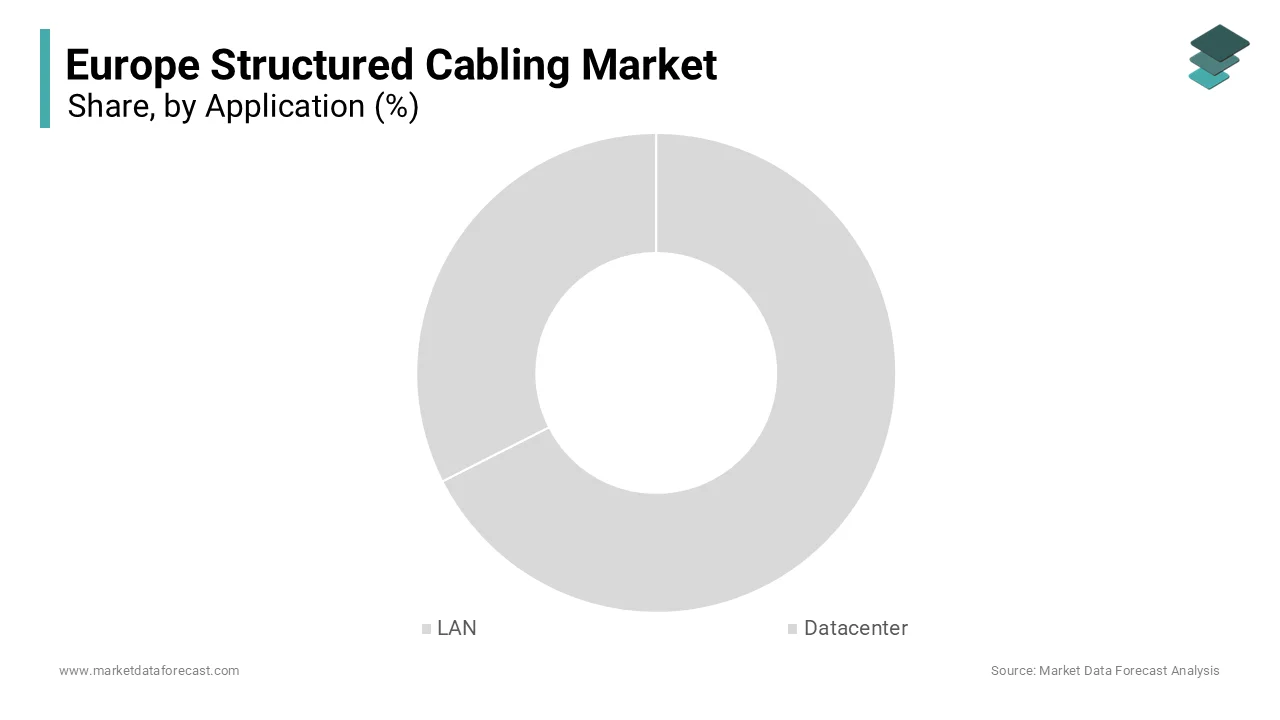

- Based on application, the LAN applications dominated the market with 58.5% share in 2024, supported by extensive enterprise networking needs and increasing data traffic within commercial buildings.

Regional Insights

The European structured cabling market continues to expand across major economies due to strong ICT investments, advanced telecom infrastructure, and increasing cloud adoption.

- Germany was the largest market, holding 23.5% of the regional share in 2024, supported by strong industrial digitalization, data center expansion, and robust manufacturing-driven IT infrastructure needs.

- Other key contributors include France, the United Kingdom, and the Netherlands, where smart city initiatives and hyperscale data center deployments are boosting structured cabling demand.

Competitive Landscape

The Europe structured cabling market is moderately consolidated, with leading players focusing on advanced cabling solutions, fiber innovations, sustainability improvements, and strategic partnerships with data center operators and enterprises. Key companies are enhancing their product portfolios through high-performance cabling, intelligent connectivity solutions, and end-to-end network infrastructure offerings.

Prominent players in the Europe structured cabling market are Nexans, Belden Inc., Legrand SA, CommScope Holding Co. Inc., Corning Inc., Furukawa Electric Co. Ltd., Siemens AG, ABB Ltd., and Schneider Electric SE

Europe Structured Cabling Market Size

The Europe structured cabling market size was valued at USD 13.01 billion in 2024 and is projected to reach USD 24.55 billion by 2033 from USD 13.96 billion in 2025, growing at a CAGR of 7.31%.

Structured cabling is standardized network infrastructure solution that support data voice and multimedia transmission across commercial institutional and industrial buildings through organized copper and fiber optic pathways. Unlike ad hoc wiring systems, structured cabling adheres to international standards such as ISO/IEC 11801 and EN 50173 to ensure scalability interoperability and long-term performance in evolving digital environments. This infrastructure serves as the physical backbone for enterprise networks smart building controls and data center interconnects. According to the European Commission, the Energy Performance of Buildings Directive requires new non-residential buildings in the EU to integrate digital readiness assessments, which is mandating minimum connectivity infrastructure such as category 6A or higher cabling. According to Eurostat, Europe added millions of square meters of new office and data center floor space in 2023, which is driving foundational cabling demand. Furthermore, the European Telecommunications Standards Institute has accelerated adoption of single pair Ethernet cabling for industrial IoT applications, aligning structured cabling with Industry 5.0 objectives. In this context, structured cabling transcends mere connectivity to become a strategic enabler of energy efficiency, digital sovereignty and cyber-physical integration across the European built environment.

MARKET DRIVERS

Mandatory Digital Infrastructure Regulations Drive Adoption

The implementation of stringent building regulations across Europe has made structured cabling a compulsory element in new construction and major renovation projects, which is primarily driving the growth of the structured cabling market. The European Union’s revised Energy Performance of Buildings Directive which came into full effect in 2023 requires all new non-residential buildings to achieve a “digital readiness score” that includes provisions for high-speed in-building connectivity infrastructure. According to the European Commission, this score mandates at least category 6A copper cabling or OM4 multimode fiber to each workstation enabling gigabit-capable networks. In Germany, the federal Digital Building Ordinance enacted in January 2024 requires all public buildings over 1000 square meters to install structured cabling certified under DIN EN 50173-1 with traceable test documentation. Similarly, France’s RE2020 environmental regulation ties building permits to digital infrastructure compliance, including structured pathways for future proofing. For instance, a majority of recent commercial construction projects in Western Europe have included structured cabling as a core specification rather than an optional add-on. This regulatory shift transforms cabling from a discretionary IT expense into a civil engineering requirement thereby embedding long-term demand into Europe’s urban development fabric.

Expansion of Hyperscale and Edge Data Centers

The accelerating data center builds out particularly in hyperscale and edge computing segments has intensified demand for high performance structured cabling systems capable of supporting 100 gigabit and beyond Ethernet speeds, which is further boosting the regional market growth. According to industry reports, over 200 new data halls were commissioned across the EU in 2023 with Ireland, the Netherlands and Sweden emerging as key hubs due to favorable renewable energy access. Each hyperscale facility typically deploys extensive structured fiber links and copper drops requiring stringent channel loss budgets and modular patching architectures. According to the European Data Centre Association, new facilities increasingly adopt OM5 wideband multimode fiber and category 8 copper to support AI workloads and high-frequency trading which demand sub-microsecond latency. Furthermore, the rise of edge data centers located within urban cell towers or retail facilities necessitates compact high-density cabling solutions such as pre-terminated trunk cables and modular cassette systems. Telefónica’s 2024 edge rollout in Spain involved hundreds of micro data centers, each requiring structured fiber connections compliant with EN 50173-4. This dual momentum of cloud scale and edge proximity ensures sustained and technically advanced cabling deployment across the region.

MARKET RESTRAINTS

Skilled Labor Shortage in Certified Installation

A critical shortage of network cabling technicians certified to international standards is constraining the timely and compliant deployment of structured cabling projects across Europe, which is hampering the structured cabling market in Europe. Across the EU, fewer than 30,000 professionals currently hold valid BICSI or ETA certification for structured cabling installation, despite an estimated annual demand for more than 65,000 qualified personnel. This gap is most acute in Central and Eastern Europe where data center and 5G infrastructure projects are expanding rapidly but local training pipelines remain underdeveloped. The German Chamber of Commerce reported in 2023 that a majority of IT infrastructure contractors experienced project delays due to inability to staff certified cable installers, which is leading to significant cost overruns. Moreover, improper termination or testing of category 6A links can cause alien crosstalk that degrades 10GBASE-T performance, which is a risk that deters building owners from using non-certified labor. Although initiatives like the EU Digital Skills and Jobs Platform have trained thousands of technicians since 2022, the certification process remains lengthy and expensive. Until vocational education systems integrate structured cabling competencies, this human capital deficit will continue to bottleneck market execution.

Fragmented National Standards and Compliance Requirements

Divergent national interpretations of European cabling standards create regulatory uncertainty and increase compliance costs for pan European structured cabling projects, which is further hindering the regional market growth. While the European Committee for Electrotechnical Standardization publishes EN 50173 as a harmonized framework individual member states impose supplementary requirements that complicate cross border deployments. According to the European Cabling Association, France mandates additional fire retardancy testing under NF C 15-100 for all indoor cables, while Germany requires separate electromagnetic compatibility validation under VDE 0800 for industrial sites. In Sweden, all public sector cabling must use locally sourced copper with traceable origin documentation, which is a stipulation not found in EU directives. These discrepancies force multinational integrators to maintain multiple cable inventories and test protocols, which is increasing lead times significantly. Furthermore, the lack of mutual recognition for cable certification bodies means a link tested and approved in Italy may require re-verification in Poland. This regulatory fragmentation undermines the single market principle and inflates total cost of ownership for digital infrastructure.

MARKET OPPORTUNITIES

Integration with Smart Building Management Systems

The convergence of IT networks and operational technology in smart buildings is a significant opportunity for European structured cabling market. Modern European office and healthcare facilities increasingly deploy Power over Ethernet powered sensors actuators and controllers for lighting HVAC and security all requiring standardized cabling pathways. According to the European Smart Buildings Coalition, a majority of new commercial buildings in the EU now use a single structured cabling plant to carry both data and low voltage power, which is reducing conduit clutter and maintenance complexity. The European Standard EN 50173-6 published in 2023 specifically addresses cabling for building automation systems, recommending category 6A for PoE++ applications delivering up to 90 watts per port. In the Netherlands, the BENG sustainability certification awards bonus points for unified cabling that enables real-time energy monitoring through connected meters and occupancy sensors. For instance, Siemens Smart Infrastructure reported in 2024 that its integrated campus deployments in Frankfurt and Barcelona reduced cabling material use significantly through consolidated pathways. This trend toward infrastructure convergence positions structured cabling as the central nervous system of intelligent built environments.

Growth of Industrial Ethernet in Manufacturing Facilities

The adoption of Industrial Ethernet protocols such as PROFINET EtherNet/IP and TSN in European factories is creating robust demand for ruggedized structured cabling designed for harsh electromagnetic and mechanical environments, which is another notable opportunity for the European structured cabling market. For instance, a majority of new production lines installed in the EU in 2023 utilized Ethernet-based control networks replacing legacy fieldbuses to enable real-time data exchange with enterprise systems. These applications require industrial-grade category 5e or 6A cables with shielding braid armor and oil-resistant jackets certified under IEC 60529 for IP67 ingress protection. According to the German Mechanical Engineering Industry Association, Industry 5.0 initiatives emphasize human-machine collaboration which relies on deterministic network performance only achievable through properly installed structured cabling. In 2024 BMW’s plant in Munich deployed extensive M12 X-coded fiber and copper cabling to connect thousands of sensors and robotic arms on its EV assembly line. Similarly, Schneider Electric’s Smart Factory in Poland uses pre-terminated industrial patch cords to reduce machine commissioning time significantly. This migration to Ethernet-based automation transforms structured cabling from an office utility into a mission-critical industrial asset.

MARKET CHALLENGES

Supply Chain Volatility for Critical Raw Materials

Fluctuations in the availability and pricing of copper aluminum and specialty polymers have introduced significant cost and scheduling risks into the European structured cabling supply chain, which is primarily challenging the growth of the European structured cabling market. Copper constitutes a significant share of the material cost in category 6A cables and its price on the London Metal Exchange rose notably between January and September 2023, according to the International Copper Study Group. This volatility is exacerbated by Europe’s dependence on imported refined copper with a large portion sourced from outside the EU as per the European Commission’s Raw Materials Information System. Simultaneously, global shortages of flame-retardant polyethylene compounds used in low smoke zero halogen jacketing have delayed cable deliveries by several weeks as confirmed by the European Wire and Cable Association in early 2024. These disruptions force contractors to lock in long-term pricing or substitute materials which may not meet EN 50575 fire safety classifications. Although recycling initiatives recover millions of metric tons of copper annually from end-of-life cables, this secondary supply cannot meet the surge in new construction and data center demand. Until material sourcing stabilizes, project economics and timelines will remain exposed to upstream commodity shocks.

Obsolescence Risk from Rapid Technological Evolution

The accelerating pace of network speed upgrades and cabling standard revisions creates a risk of premature infrastructure obsolescence that deters long term investment in structured cabling, which is further challenging the regional market expansion. Just five years after category 6A became mainstream, 40GBASE-T and 25GBASE-T applications now necessitate category 8 cabling with alien crosstalk performance far beyond previous norms. According to the European Telecommunications Standards Institute, the useful life of copper cabling in high-density data environments has shortened significantly due to bandwidth demands from AI and high-performance computing. In 2023, a major Dutch bank decommissioned a category 6A backbone installed in 2019 because it could not support 25-gigabit links to trading terminals as documented in its infrastructure audit. Similarly, the emergence of single pair Ethernet for IoT devices requires entirely new connector types such as IEC 63171-1, which are incompatible with traditional RJ45 jacks. This technological churn forces facility managers to choose between over-engineering with future-proof but costly solutions or accepting near-term upgrade cycles. Until cabling architectures adopt greater modularity and adaptability, this obsolescence pressure will constrain capital allocation and encourage minimalist deployments.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| CAGR | 7.31% |

| Segments Covered | By Product Type, Application, and Region |

| Various Analyses Covered | Global, Regional, & Country Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, and the Czech Republic |

| Market Leaders Profiled | Nexans, Belden Inc., Legrand SA, CommScope Holding Co Inc, Corning Inc, Furukawa Electric Co Ltd, Siemens AG, ABB Ltd, and Schneider Electric SE |

SEGMENTAL ANALYSIS

By Product Insights

The copper segment led the European structured cabling market by holding 59.5% of the European market share in 2024. Copper remains the dominant product type in the Europe structured cabling market due to its cost effectiveness compatibility with Power over Ethernet and widespread suitability for horizontal cabling in office and commercial environments. The vast majority of workstation connections across European enterprises rely on category 6 and 6A twisted pair cables which support gigabit and multi-gigabit speeds up to 100 meters without signal regeneration. According to the European Telecommunications Standards Institute, most new office buildings constructed in the EU in 2023 specified category 6A as the minimum standard for all work area outlets, which is enabling support for Wi-Fi 6E backhaul and desktop video conferencing. Furthermore, the European Commission’s Digital Building Passport initiative mandates that all public sector buildings integrate PoE-capable cabling to power LED lighting, occupancy sensors and access control systems with a single infrastructure. According to the German Federal Ministry of the Interior, federal building modernization program allocated hundreds of millions of euros specifically for copper cabling upgrades to meet EN 50173-2 standards in 2024. This regulatory and functional alignment ensures copper’s continued dominance despite advances in fiber optics.

The multimode fiber held 54.8% of the European structured cabling market in 2024. The dominance of the multimode fiber segment in the European market can be credited to its optimal balance of bandwidth reach and cost for intra building and data center applications. OM4 and OM5 laser-optimized multimode fibers support 100 gigabit Ethernet up to 150 meters and 400 gigabit up to 100 meters respectively, which is making them ideal for server-to-top-of-rack connections in enterprise and colocation facilities. For instance, a large majority of new on-premise data centers commissioned in Western Europe in 2023 deployed OM4 as the standard backbone medium. The cost per link for multimode remains significantly lower than single mode when factoring in transceiver expenses, as noted by the European Photonics Industry Consortium. Furthermore, the European Standard EN 50173-3 permits multimode fiber for backbone cabling in buildings up to 500 meters, which covers nearly all campus environments. Major banks in London and Frankfurt continue to specify OM4 for trading floor networks where low latency and proven reliability outweigh theoretical reach advantages of single mode. This economic and performance pragmatism secures multimode’s leadership within the fiber category.

The single mode fiber connectivity segment is anticipated to record a CAGR of 12.2% over the forecast period in the European market owing to the hyperscale data center expansion and metro network densification. Unlike multimode single mode supports unlimited bandwidth over distances exceeding 10 kilometers, which is making it essential for campus backbones inter data center links and 5G fronthaul. For instance, new hyperscale facilities in Ireland, the Netherlands and Sweden increasingly use single mode fiber exclusively for both backbone and horizontal runs to future-proof against 800 gigabit and 1.6 terabit Ethernet. The European Telecommunications Standards Institute’s 2024 update to EN 50173-4 mandates APC angled physical contact connectors for all single mode links to minimize reflectance, a requirement that has spurred redesign of patch panels and splice trays. Companies like Huber+Suhner and Rosenberger have introduced pre-terminated single mode trunk cables with factory-verified loss budgets under 0.2 decibels per mated pair as documented in their 2024 compliance dossiers. As Europe’s digital infrastructure scales in both density and speed, single mode connectivity becomes the critical enabler of optical network integrity.

By Application Insights

The LAN segment dominated the market by accounting for 58.5% of the regional market share in 2024. The dominance of LAN segment in the European market is attributed to the continuous rollout of digital workspaces smart offices and building automation systems across the commercial and public sectors. Every new workstation classroom or hospital room requires a minimum of two structured drops often more for VoIP phones video endpoints and IoT sensors. According to Eurostat, significant volumes of new non-residential floor space were completed in the EU in 2023 with typical office designs specifying multiple data outlets per 100 square meters as noted by the European Construction Federation. The European Commission’s Digital Decade targets require all EU households to have gigabit connectivity by 2030, which requires in-building cabling upgrades even in existing structures. In Germany, the federal DigitalPakt Schule initiative funded 6.5 billion euros between 2020 and 2024 to upgrade school connectivity and cabling. Similarly, France’s France Très Haut Débit plan supports digital infrastructure upgrades in public buildings. This pervasive need for endpoint connectivity across education, healthcare and enterprise ensures LAN remains the volume backbone of the structured cabling market.

The datacenter segment is estimated to record at a CAGR of 14.04% over the forecast period in the European market owing to the Europe’s aggressive cloud infrastructure build out renewable powered hyperscale facilities and regulatory push for data sovereignty. For instance, significant numbers of new data halls commissioned across the EU in 2023 with substantial investment in capacity expansion. Each large facility typically deploys extensive structured fiber links and copper drops requiring high-density modular architectures and rigorous loss budget management. The EU’s Data Act entered into force in 2024 to improve access to and use of data under European rules, which is supporting continued local data center expansion by major cloud providers in countries such as Sweden, Denmark and the Netherlands. In parallel, initiatives aligned with the European Green Deal and sector pacts promote increased renewable energy sourcing for new data centers, which is encouraging co-location near wind and hydro sites that demand robust long-reach cabling. As AI workloads drive adoption of 400G and 800G Ethernet, the need for OM5 and single mode structured pathways intensifies. This confluence of digital sovereignty, sustainability and performance requirements positions data centers as the high-growth engine of the structured cabling market.

REGIONAL ANALYSIS

Germany Market Analysis

Germany led the structured cabling market in Europe by holding 23.5% of the regional market share in 2024 owing to its strong industrial base stringent building codes and federal digitalization programs. As Europe’s largest economy, Germany added significant volumes of commercial office and industrial space in 2023, according to the Federal Institute for Research on Building, Urban Affairs and Spatial Development. The country’s DigitalPakt Schule and DigitalPakt Hochschule initiatives allocated billions of euros between 2020 and 2024 to modernize cabling infrastructure in tens of thousands of educational institutions, mandating category 6A or better. Furthermore, regulations require new non-residential buildings to integrate digital-ready cabling pathways compliant with DIN EN 50173. Major data center operators including Equinix and Global Switch have expanded Frankfurt’s “Data Center Alley” with multiple new facilities since 2022, each deploying extensive lengths of structured fiber. With a large pool of certified cabling contractors and a dense ecosystem of manufacturers like Reichle & De Massari, Germany maintains unmatched scale and technical depth in structured infrastructure deployment.

United Kingdom Market Analysis

The United Kingdom remains a high impact regional segment in the European structured cabling market owing to its mature enterprise sector thriving data center corridor and post Brexit emphasis on digital sovereignty. London’s Slough and Croydon clusters host a large concentration of data centers representing a significant share of Europe’s colocation capacity. The UK government’s Levelling Up Fund has allocated substantial funding to upgrade public sector infrastructure, including structured cabling in hospitals and local councils. Additionally, the National Health Service’s Digital Transformation Strategy emphasizes high-capacity connectivity for telemedicine and electronic records in new clinical facilities. The British Standards Institution has aligned BS 6701 with EN 50173-6 for building automation cabling, which is enabling unified PoE networks in smart campuses. Companies like Fujitsu and BT Deploy have executed large-scale cabling retrofits across government buildings using shielded high-performance systems. This blend of hyperscale cloud demand and public sector digitization sustains robust and diverse cabling consumption across the UK.

France Market Analysis

France occupied a strategic position in the European structured cabling market in 2024 through its centralized public investment digital inclusion policies and growing data center footprint. As per the French Agency for Digital Infrastructure, millions of households were connected to fiber to the home by 2023 with building internal cabling modernized under the “France Très Haut Débit” national plan. All new public buildings must comply with the RE2020 environmental regulation, which includes provisions related to digital readiness and in-building connectivity infrastructure. In 2024, the French Ministry of Education launched the “Plan Numérique pour l’Éducation” to equip thousands of schools with structured cabling supporting one device per student. Major cloud providers including OVHcloud and Amazon Web Services are expanding data center campuses in Paris and Marseille with significant investments since 2022. The French standard NF C 15 100 imposes additional fire safety requirements on indoor cables, which is driving adoption of low smoke zero halogen variants. This state-led digital infrastructure agenda ensures consistent and regulated cabling demand nationwide.

Netherlands Market Analysis

The Netherlands serves as Europe’s digital gateway with a disproportionately large structured cabling market driven by its data center density fiber optic backbone and progressive building regulations. Amsterdam and Eemshaven host hyperscale and enterprise data centers including facilities from Microsoft, Google and Meta. The country’s Energy Agreement for Sustainable Growth mandates that all new commercial buildings achieve an energy performance score that includes structured cabling for smart metering and HVAC control. The Dutch Standard NEN 1013 aligns with EN 50173 but adds requirements for electromagnetic compatibility in industrial zones like Rotterdam port. In 2024, the Ministry of the Interior launched the “Gemeenten Digitaal” program funding cabling upgrades to support digital citizen services. Companies like Proximus and Cegeka have deployed campus wide category 8 cabling in logistics hubs to support autonomous forklifts and real time inventory tracking. This fusion of cloud infrastructure logistics digitization and regulatory foresight makes the Netherlands a high intensity cabling market.

Sweden Market Analysis

Sweden emerges as a sustainability driven leader in the European structured cabling market leveraging abundant renewable energy favorable climate and strong public digital services. According to the Swedish Energy Agency, a large share of electricity used in Swedish data centers comes from low-carbon hydro and nuclear sources, which is attracting major cloud investments with multiple new facilities commissioned in 2023 near Stockholm and Umeå. The Swedish National Board of Housing, Building and Planning updated its building code in 2024 to strengthen in-building connectivity provisions with many projects specifying category 6A cabling and multiple outlets per room. The “Digital Sweden” national strategy funds modernization of school and hospital IT infrastructure including structured cabling for telehealth and remote learning. Major enterprises like Ericsson and ABB deploy industrial grade structured cabling in smart factories supporting real time machine data exchange via PROFINET. Additionally, Sweden’s cold climate reduces data center cooling loads allowing higher port density per rack which increases cabling requirements. This alignment of green energy digital policy and industrial innovation positions Sweden as a model for future oriented cabling deployment.

COMPETITIVE LANDSCAPE

KEY MARKET PLAYERS

Some of the notable key players in the Europe Structured cabling market are

-

Nexans

-

Belden Inc.

-

Legrand SA

-

CommScope Holding Co Inc

-

Corning Inc

-

Furukawa Electric Co Ltd

-

Siemens AG

-

ABB Ltd

-

Schneider Electric SE

TOP STRATEGIES USED BY THE KEY MARKET PLAYERS

Key players in the Europe structured cabling market pursue vertical integration by offering end to end solutions encompassing cables connectivity panels and intelligent monitoring software to ensure system compatibility and performance validation. They align product development with European regulatory frameworks such as the Energy Performance of Buildings Directive and Construction Products Regulation by embedding sustainability and digital readiness into cabling design. Companies invest in high density modular architectures to support data center scalability and AI driven network demands. Strategic partnerships with system integrators and hyperscalers secure long term deployment pipelines in cloud and edge computing segments. Additionally firms emphasize circular economy initiatives including copper recovery programs and halogen free material formulations to meet EU environmental compliance and enhance brand differentiation in a technically mature market.

COMPETITION OVERVIEW

The Europe structured cabling market features a mature yet dynamic competitive environment characterized by technological precision regulatory compliance and sustainability differentiation rather than price competition. Dominated by European engineering firms with global reach the landscape rewards long term certification adherence robust testing documentation and local technical support networks. Incumbents leverage decades of standards participation to influence EN and ISO specifications ensuring their architectures remain compliant by design. New entrants from Asia face barriers due to the EU’s Construction Products Regulation which mandates CE marking fire safety classification and performance declarations traceable to notified bodies. Innovation is concentrated in intelligent cabling with embedded sensors high density fiber solutions and single pair Ethernet for industrial IoT. The absence of commoditization allows premium pricing for systems that demonstrably reduce installation time ensure future proofing or support digital building passports. As Europe prioritizes data sovereignty energy efficiency and digital inclusion the competitive advantage increasingly lies with players who integrate physical infrastructure with digital asset management and circular material practices.

TOP PLAYERS IN THE MARKET

-

Legrand is a French multinational and a global leader in electrical and digital infrastructure with deep integration across the European structured cabling market. The company offers a comprehensive portfolio of copper and fiber cabling solutions under brands such as Ortronics and FTR, serving enterprise, data center and smart building segments. Legrand’s systems comply with EN 50173 and ISO/IEC 11801 standards and are widely specified in public sector and healthcare projects across Europe. In 2024 the company launched its new LX7 high density fiber connectivity platform optimized for 400G data center deployments and introduced AI ready copper solutions supporting multi gigabit PoE for intelligent workspaces. These innovations reinforce Legrand’s role in enabling Europe’s digital and energy transition strategies through future proof infrastructure.

-

Reichle & De Massari is a Swiss engineering company renowned for its precision structured cabling systems that combine Swiss manufacturing quality with advanced performance metrics. The company serves high demand sectors including finance, aviation and critical infrastructure across Europe with category 8 and OM5 solutions engineered for maximum signal integrity. R&M maintains a strong presence in hyperscale data center projects in Germany, the Netherlands and Sweden through its scalable Prime and FieldConnect platforms. In early 2024 R&M introduced its Smart Cabling System featuring embedded RFID and NFC tags for real time asset tracking and digital twin integration in line with EU digital building regulations. Its commitment to sustainability is demonstrated through halogen free materials and a carbon neutral manufacturing pledge, aligning with Europe’s green infrastructure mandates.

-

Nexans is a Paris based global cable manufacturer with a significant footprint in Europe’s structured cabling landscape through its LAN and datacom division. The company provides end to end solutions including high performance copper cables, fiber trunk assemblies and connectivity hardware for enterprise networks and cloud infrastructure. Nexans supplies major telecom operators, data center developers and public institutions across the continent with products certified under EN 50173 and CPR fire safety classifications. In 2024 Nexans expanded its LANX modular cabling range to support single pair Ethernet for industrial IoT and launched a circular economy program recovering and reprocessing copper from decommissioned cabling installations. These initiatives strengthen its position as a sustainable and technologically adaptive partner in Europe’s digital backbone development.

MARKET SEGMENTATION

This research report on the Europe structured cabling market has been segmented and sub-segmented based on categories.

By Product Type

-

Copper

-

Copper Cable

-

Copper Connectivity

-

Fiber

-

Fiber Cable (Single-mode & Multi-mode)

-

Fiber Connectivity

By Application

-

LAN

-

Datacenter

By Country

-

UK

-

France

-

Spain

-

Germany

-

Italy

-

Russia

-

Sweden

-

Denmark

-

Switzerland

-

Netherlands

-

Turkey

-

Czech Republic

-

Rest of Europe

Frequently Asked Questions

1. What is structured cabling and why is it important in Europe?

Structured cabling is an organized system of cables and hardware that supports data, voice, and video communication. It is essential in Europe due to growing digitalization, cloud adoption, and the need for reliable network infrastructure.

2. What are the main components of a structured cabling system?

A structured cabling system includes copper and fiber cables, patch panels, connectors, racks, cable management systems, and network hardware.

3. Which factors are driving the structured cabling market in Europe?

Key drivers include data center expansion, smart building development, IoT growth, and increasing enterprise demand for high-speed connectivity.

4. Which product types are widely used in European structured cabling?

Both copper and fiber optic solutions are widely used, with copper commonly preferred for LAN networks and fiber for high-speed, long-distance data transmission.

5. What applications rely heavily on structured cabling in Europe?

Applications include LAN networks, data centers, telecom facilities, industrial automation, and commercial buildings.

6. Why is copper cabling popular in European enterprise networks?

Copper cabling is cost-effective, easy to install, durable, and widely compatible with existing infrastructure, making it a preferred choice for many organizations.

7. How is fiber optic cabling influencing the market?

Fiber optic cabling is gaining momentum due to its high bandwidth, faster transmission, resistance to electromagnetic interference, and suitability for modern data centers.

8. What industries are major users of structured cabling in Europe?

Key industries include IT & telecom, banking, manufacturing, healthcare, retail, and transportation, all of which require robust digital connectivity.

9. How is the rise of smart buildings impacting structured cabling demand?

Smart buildings rely on interconnected systems such as security, lighting, HVAC, and IoT devices, all of which depend on structured cabling to enable efficient communication.

10. What role do data centers play in the structured cabling market?

Data centers require high-performance cabling systems to support cloud computing, storage, network scaling, and fast data processing, significantly boosting market demand.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com