Europe Sulfuric Acid Market Size, Share, Trends, & Growth Forecast Report By Application (Fertilizers, Chemical Manufacturing, Metal Processing, Textile Paper & Pulp Automotive, Others), Technology, End-User and Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic and Rest of Europe), Industry Analysis From 2025 to 2033

Europe Sulfuric Acid Market Report Summary

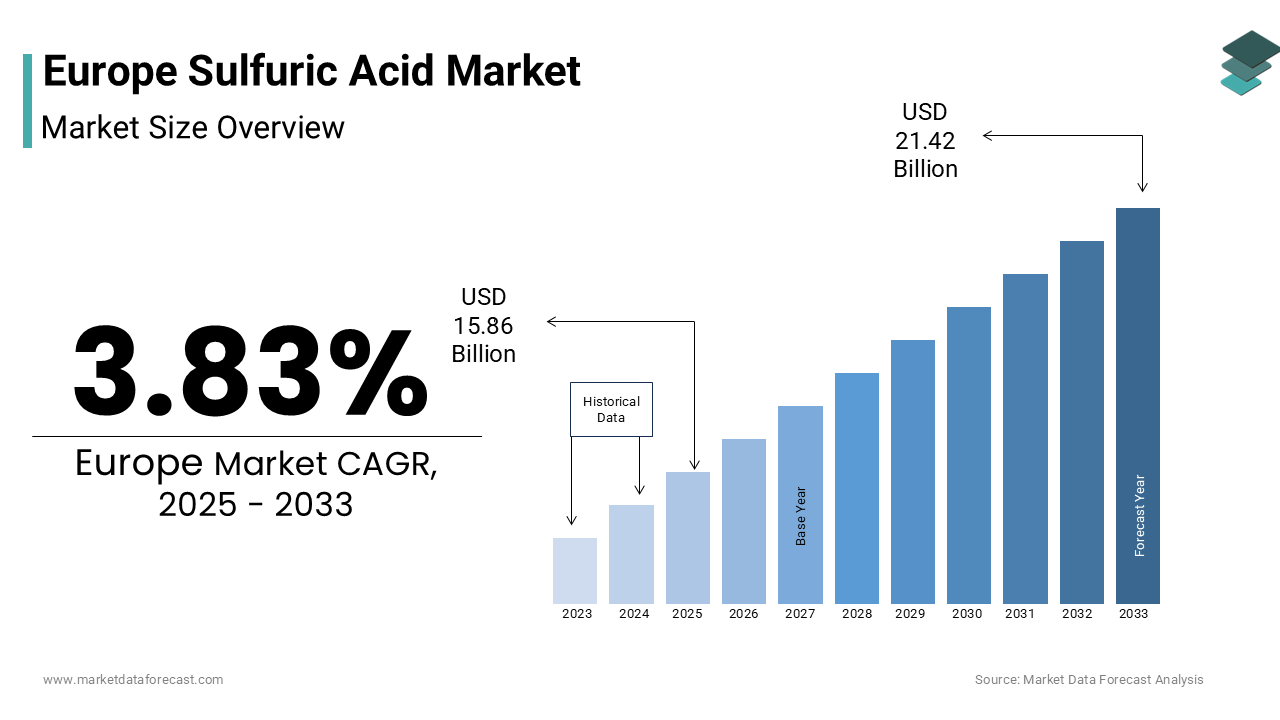

The Europe sulfuric acid market was valued at USD 15.27 billion in 2024, is estimated to reach USD 15.86 billion in 2025, and is projected to reach USD 21.42 billion by 2033, growing at a CAGR of 3.83% during the forecast period from 2025 to 2033. The growth of the Europe sulfuric acid market is primarily driven by sustained demand from fertilizer manufacturing, expanding non-ferrous metal processing, and the increasing role of sulfuric acid in battery materials and circular economy applications. Sulfuric acid remains a cornerstone industrial chemical in Europe, supporting agriculture, metallurgy, chemical synthesis, and wastewater treatment. Despite broader declines in chemical production volumes due to regulatory and economic pressures, sulfuric acid retains strategic importance as a byproduct of metal smelting and as an enabler of resource efficiency under the EU’s circular economy and decarbonization frameworks.

Key Market Trends

- Continued dominance of fertilizer production as the largest consumer of sulfuric acid across Europe.

- Rising utilization of sulfuric acid in non-ferrous metal refining and battery material purification.

- Increasing recovery and reuse of sulfuric acid in alignment with EU circular economy mandates.

- Growing demand from battery recycling and critical raw material recovery operations.

- Gradual shift toward localized production to mitigate sulfur feedstock and transport risks.

Segmental Insights

- Based on application, the fertilizers segment dominated the Europe sulfuric acid market by accounting for 62.7% of the market share in 2024. This dominance is attributed to sulfuric acid’s indispensable role in converting phosphate rock into phosphoric acid, which is essential for producing phosphate-based fertilizers. Europe’s intensive agricultural systems, food security priorities, and continued reliance on mineral fertilizers ensure structurally stable demand for sulfuric acid despite long-term efficiency and sustainability initiatives.

- The metal processing segment is projected to register the fastest CAGR of 5.2% from 2025 to 2033. Growth in this segment is driven by increasing demand for refined copper, nickel, and zinc used in electric vehicles, renewable energy infrastructure, and battery manufacturing. Sulfuric acid is extensively used in hydrometallurgical leaching and purification processes, while EU policies supporting domestic refining of critical raw materials further accelerate demand from this segment.

Regional Insights

The Europe sulfuric acid market demonstrates strong regional concentration aligned with industrial clusters and metallurgical activity.

- Germany was the largest contributor, holding 18.5% of the Europe sulfuric acid market share in 2024, supported by its dense network of chemical manufacturers, fertilizer producers, and integrated metal smelting facilities.

- Poland followed closely, accounting for 14.2% of the market share, driven by large-scale copper smelting operations and strong domestic fertilizer production.

- France remains a key market due to its advanced chemical sector, phosphate fertilizer manufacturing, and growing battery materials ecosystem.

- The Netherlands plays a critical role as a logistics and processing hub, leveraging major ports and circular chemistry initiatives.

- Sweden is emerging as a high-growth market, supported by sustainable metallurgy and expanding battery recycling capacity powered by low-carbon energy sources.

Competitive Landscape

The Europe sulfuric acid market is moderately competitive and characterized by a mix of integrated chemical producers, fertilizer manufacturers, and non-ferrous metal refiners. Competition is shaped less by pricing and more by supply reliability, regulatory compliance, logistics efficiency, and sustainability credentials. Large players benefit from vertical integration and byproduct sulfuric acid generation from smelting operations, while smaller suppliers focus on high-purity and specialty grades for advanced industrial applications. Investments in acid regeneration, circular production models, and secure feedstock sourcing are key strategic priorities. Prominent players in the Europe sulfuric acid market include BASF SE, LANXESS AG, Akzo Nobel N.V., Nouryon, Arkema S.A., Solvay S.A., INEOS Group, Grupa Azoty S.A., Aurubis AG, and Boliden Group.

Europe Sulfuric Acid Market Size

The europe sulfuric acid market size was valued at USD 15.27 billion in 2024 and is anticipated to reach USD 15.86 billion in 2025 from USD 21.42 billion by 2033, growing at a CAGR of 3.83% during the forecast period from 2025 to 2033.

Sulfuric acid H2SO4 is the world's most consumed industrial chemical. It serves as a foundational reagent in fertilizer production, metal processing, chemical synthesis, and wastewater treatment. The European sulfuric acid landscape is closely interlinked with the region’s metallurgical and agricultural sectors, both of which dictate consumption patterns and logistical dynamics. According to Eurostat data from 2023, the production and consumption of industrial chemicals in the EU generally experienced a significant decline, marking a multi-year downward trend in line with broader economic and regulatory factors. This decrease was observed across both hazardous and non-hazardous categories, with the production of chemicals hazardous to the environment reaching a new minimum for the entire reporting period. As per sources, a significant portion of the region's sulfuric acid supply, widely reported in industry sources, is derived as a byproduct of non-ferrous metal smelting, particularly from copper and zinc operations in countries like Poland, Germany, and Finland. The European Chemicals Agency (ECHA) generally endorses practices that align with the EU's circular economy mandates, promoting the recovery and reuse of materials, which is an increasingly embedded mechanism within the chemical industry's production chains due to stringent environmental regulations. This positioning reinforces sulfuric acid not merely as a commodity but as a critical enabler of resource efficiency within Europe’s broader industrial decarbonization strategy.

MARKET DRIVERS

Fertilizer Manufacturing Continues to Anchor Regional Sulfuric Acid Consumption

The production of phosphate-based fertilizers remains the primary driver of the Europe sulfuric acid market. This is driven by the continent’s sustained agricultural output and food security priorities. Sulfuric acid is essential in converting phosphate rock into water soluble phosphoric acid, a key ingredient in compound fertilizers such as diammonium phosphate and superphosphates. According to multiple sources, European demand for phosphate fertilizers remains vital for agricultural productivity, necessitating a stable supply of sulfuric acid to sustain the manufacturing of these essential soil nutrients. As per data from the European Commission’s Directorate General for Agriculture and Rural Development, arable land in the EU covers approximately 98.1 million hectares in 2020, with intensive cropping systems in France, Germany, and Poland requiring regular soil nutrient replenishment. The production of phosphate-based fertilizers in Europe is overwhelmingly dependent on chemical digestion processes that utilize sulfuric acid to convert raw phosphate rock into plant-available nutrients. In addition, geopolitical disruptions in natural gas supply chains since 2022 have elevated the strategic importance of domestically sourced fertilizers, thereby reinforcing demand for sulfuric acid despite cost pressures. This structural linkage between crop nutrition and sulfuric acid ensures persistent baseline consumption that remains largely insulated from short term economic volatility.

Expansion of Non Ferrous Metal Smelting Sustains Sulfuric Acid Demand

Robust non-ferrous metal industry in the region, particularly in copper, nickel, and zinc refining, serves as a dual source and consumer of sulfuric acid by creating a self-reinforcing industrial loop. This also fuels the expansion of the Europe sulfuric acid market. During the smelting of sulfide ores, sulfur dioxide is released and subsequently converted into sulfuric acid through contact process technology. This captive production is then either reused within metallurgical circuits or supplied to adjacent chemical industries. The European Union's copper refining output is consistently substantial, maintaining a stable level in response to ongoing demand from sectors like electrical engineering and infrastructure. Moreover, the majority of copper smelters in Europe utilize integrated sulfuric acid plants, which collectively produce a significant amount of the acid byproduct each year. In some facilities, such as those in Finland and Poland, the utilization of the sulfuric acid byproduct is so efficient that the excess can be sold commercially to other entities. The European Battery Alliance’s push for localized battery material production further bolsters this dynamic, as nickel and cobalt sulfate purification for cathode manufacturing requires high purity sulfuric acid. Thus, the metallurgical sector not only reduces Europe’s reliance on imported acid but also enhances supply chain resilience in critical mineral processing.

MARKET RESTRAINTS

Stringent Environmental Regulations Impose Operational Constraints

The European sulfuric acid sector faces mounting pressure from evolving environmental legislation that governs emissions, storage, and transportation of highly corrosive substances, and thereby hampers the growth of the Europe sulfuric acid market. As per research, sulfuric acid's classification under regulatory guidelines indicates that the substance may cause severe skin burns and eye damage, necessitating rigorous handling protocols. The Industrial Emissions Directive requires integrated pollution prevention and control permits for all major acid producing facilities, mandating continuous monitoring of sulfur dioxide and acid mist releases. According to sources, a number of facilities within the European Union that work with the substance were subjected to enhanced emission audits. Transport restrictions under the European Agreement Concerning the International Carriage of Dangerous Goods by Road have further complicated logistics, particularly in densely populated regions such as the Benelux and Rhine River corridor. Compliance expenditures for producers of sulfuric acid have seen an increase, driven primarily by investments in upgrades to equipment and waste neutralization systems. These regulatory layers, while essential for environmental protection, elevate production costs and discourage new entrants, and thereby limit market fluidity and innovation in acid handling technologies.

Volatility in Sulfur Feedstock Availability Disrupts Production Continuity

The region’s sulfuric acid manufacturing is heavily dependent on molten sulfur, a factor that further restrains the expansion of the Europe sulfuric acid market. This feedstock's supply is intrinsically tied to global oil and gas desulfurization activities. The European Union significantly depends on international markets for its elemental sulfur supply due to limited domestic deposits. Changes in global crude oil refining have restricted sulfur availability, posing difficulties for European acid producers who rely on imported resources. This high dependency on foreign imports makes the regional acid production chain vulnerable to international instability and logistics disruptions. The closure of several North Sea refineries between 2020 and 2023 further eroded domestic sulfur availability, forcing acid plants in the Netherlands and Italy to secure long term contracts at premium rates. As per market analyses, sulfur prices faced significant fluctuations in 2023, with values initially softening due to weak industrial demand before recovering later in the year as phosphate fertilizer production stabilized. This feedstock fragility not only elevates input costs but also constrains the ability of European producers to respond dynamically to shifts in downstream demand, particularly in time sensitive sectors such as agriculture and mining.

MARKET OPPORTUNITIES

Circular Economy Initiatives Unlock New Demand in Battery Recycling

The rapid expansion of lithium-ion battery recycling in the region creates a pathway for growth of the Europe sulfuric acid market. This is particularly true in the hydrometallurgical recovery of critical metals such as nickel, cobalt, and lithium. As per research, the volume of spent electric vehicle batteries is expected to grow significantly over the coming years as electrification trends continue. Sulfuric acid serves as a primary leaching agent in these processes, enabling selective dissolution of metal sulfates under controlled pH and temperature conditions. According to multiple sources, mandated recovery efficiency targets for specific battery metals are driving an increased dependency on high-purity acid streams during the recycling process. Facilities such as Northvolt’s Revolt plant in Sweden and Umicore’s Hoboken operation in Belgium already integrate sulfuric acid based circuits to meet these targets. The integration of recycled materials into the battery supply chain suggests a corresponding increase in the overall consumption of acids. This symbiotic relationship between circular battery economies and acid chemistry not only diversifies end use applications but also aligns with the EU’s strategic autonomy goals in critical raw materials.

Green Hydrogen Infrastructure Development Spurs Sulfuric Acid Utilization in Electrolyte Purification

Emerging green hydrogen projects across the region are indirectly enabling demand for high purity sulfuric acid in the pre-treatment of water, which is expected to fuel the expansion of the Europe sulfuric acid market. This demand extends to electrolyte systems used in proton exchange membrane electrolyzers. Although sulfuric acid is not a direct component of the electrolysis reaction, it plays a critical role in ion exchange resin regeneration and feedwater demineralization to prevent membrane fouling. The development of a large-scale hydrogen pipeline network is being pursued by a number of countries across Europe to facilitate the transport of hydrogen. Estimates suggest this planned infrastructure could support a significant volume of annual hydrogen production. Electrolyzer systems, which are essential for producing clean hydrogen, require specific volumes of a key conditioning agent during their initial setup and subsequent upkeep. The cumulative demand for this conditioning agent is becoming increasingly relevant given the substantial amount of new electrolyzer capacity that has received official approval for development. Overall, as hydrogen projects progress from the planning phase to deployment, the logistics of necessary operational resources present an important consideration for supply chains. Some companies have already formalized supply agreements with European acid producers to secure qualified reagents. This evolving nexus between clean hydrogen deployment and acid chemistry represents a novel, technology driven demand stream that transcends traditional industrial paradigms.

MARKET CHALLENGES

Energy Intensity of Production Raises Decarbonization Compliance Costs

The manufacturing of sulfuric acid via the contact process is inherently energy intensive, and requires sustained high temperatures for sulfur combustion and catalytic oxidation stages to ultimately slow down the growth of the Europe sulfuric acid market. Facilities that produce sulfuric acid typically utilize a certain range of thermal energy per metric ton produced, derived from conventional energy sources like natural gas or grid electricity, according to various studies. There is increasing pressure on producers of sulfuric acid to transition away from carbon-intensive thermal inputs in response to evolving environmental policies. In addition, the reported emissions from these facilities are subject to regulation and associated financial implications. Industry estimates suggest an increase in investment to meet compliance requirements through modifications to current processes, such as integrating waste heat recovery systems or exploring alternative fuels. These financial burdens disproportionately affect smaller or standalone producers lacking the scale to absorb transition costs, and thereby threaten operational viability and regional supply balance.

Cross Border Transport Restrictions Heighten Supply Chain Fragmentation

The movement of sulfuric acid across European jurisdictions is increasingly constrained by divergent national regulations governing the transport of dangerous goods, and consequently impedes the expansion of the Europe sulfuric acid market. This creates logistical bottlenecks that impede market integration. A notable amount of a specific chemical consumed in a certain region crosses at least one international boundary before reaching its intended destination. Varying documentation requirements in key countries can lead to delays in product movement and contribute to increased operational costs. Movement of certain materials along roadways is not permitted during specific community events or busy periods in several areas. These rules result in delivery periods having the potential to fluctuate significantly between adjacent regions. A major inland transport route has experienced periods of movement limitations due to environmental conditions. These limitations have an effect on the smooth flow of materials to key industrial areas Furthermore, the European Agency for Safety and Health at Work mandates specialized driver training and vehicle certification that are not mutually recognized across all EU states, adding administrative friction. These fragmented regulatory layers not only increase lead times but also incentivize localized production, which affects economies of scale and raising end user prices in peripheral markets such as the Balkans and Baltics.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| CAGR | 3.83% |

| Segments Covered | By Application and Region. |

| Various Analyses Covered | Global, Regional, and Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | United Kingdom, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, the Netherlands, Turkey, and the Czech Republic. |

| Market Leaders Profiled | BASF SE, LANXESS AG, Akzo Nobel N.V., Nouryon, Arkema S.A., Solvay S.A., INEOS Group, Grupa Azoty S.A., Aurubis AG, and Boliden Group |

SEGMENTAL ANALYSIS

By Application Insights

The fertilizers segment dominated the Europe sulfuric acid market by accounting for a 62.7% share in 2024. The dominance of the fertilizers segment is driven by sulfuric acid’s irreplaceable role in producing phosphate-based fertilizers, which are essential for maintaining soil fertility across the continent’s intensive agricultural systems. Sulfuric acid is used to treat phosphate rock through a process known as acidulation, yielding phosphoric acid, a precursor to monoammonium phosphate and triple superphosphate. According to research, European Union (EU) agriculture consistently applies phosphate fertilizers, from both mineral and organic sources, to sustain crop yields across a substantial area of farmland. Mineral phosphate consumption in the EU has seen a general decline over time, although it remains a necessary input. The European Commission’s Farm to Fork Strategy continues to emphasize food security amid geopolitical supply chain disruptions, reinforcing domestic fertilizer production. Besides, Phosphorus is recognized as a finite and dwindling resource essential for agricultural production, and its efficient use and recovery from secondary sources are significant areas of focus within the EU's agricultural and environmental policies. These intertwined agronomic and policy driven factors ensure that the fertilizers segment remains structurally anchored as the primary consumer of sulfuric acid in Europe.

The metal processing segment is estimated to register the fastest CAGR of 5.2% between 2025 and 2033. The rapid growth of the metal processing segment is propelled by rising demand for refined copper, nickel, and zinc, metals critical to the region’s clean energy and electric vehicle transitions. Sulfuric acid is extensively used in leaching, purification, and electrowinning operations, particularly in hydrometallurgical recovery circuits. Several European copper processing facilities manage emissions and support related activities by using integrated acid management systems. Across Europe, the demand for materials used in battery manufacturing is projected to increase significantly, which will necessitate an expansion in the supply of high-purity processing agents. The recovery rates for common industrial metals within European processing operations have reached substantial levels, with both processes relying on acid-based leaching methods. Furthermore, the EU Critical Raw Materials Act designates nickel, cobalt, and copper as strategic materials, incentivizing domestic refining capacity. This policy industrial synergy, combined with circular economy mandates, positions metal processing as the most dynamically expanding sulfuric acid application in Europe.

REGIONAL ANALYSIS

Germany Sulfuric Acid Market Analysis

Germany led the Europe sulfuric acid market and captured a 18.5% share in 2024 because of its status as the continent’s foremost industrial and chemical manufacturing hub. The country’s sulfuric acid demand is driven by a dense network of fertilizer producers, metal refiners, and specialty chemical plants concentrated in the Rhine Ruhr and Baden Württemberg regions. The chemical sector consumed a significant quantity of sulfuric acid during the specified period, utilized by several key industrial players. A single large copper processing facility produces a substantial volume of this acid as a byproduct each year, which is then largely recycled within the operation or distributed locally. A strategic focus on increasing battery manufacturing capacity across the nation has led to a heightened requirement for acid in the purification of essential metals like nickel and cobalt. Furthermore, national regulations promoting the regeneration of waste acid have contributed to a decrease in the amount of primary acid imported from other countries. This blend of industrial scale, regulatory foresight, and technological integration solidifies Germany’s leadership in the European sulfuric acid landscape.

Poland Sulfuric Acid Market Analysis

Poland followed closed in the Europe sulfuric acid market and held a share of 14.2% in 2024. The demand for sulfuric acid is credited to its dominant position in non-ferrous metal production and phosphate fertilizer manufacturing. The country is home to KGHM Polska Miedź, one of the world’s largest copper and silver producers, which operates integrated sulfuric acid plants at its Legnica and Głogów smelting complexes. Poland's production of sulfuric acid has been consistently strong, with a significant majority generated as a byproduct of copper refining. The output of domestic phosphate fertilizer production is high, a sector that relies on a consistent acid supply for use on agricultural land. Furthermore, national recovery plans are funding critical raw material processing, including the expansion of certain metal refining capacities in Lower Silesia. The nation demonstrates a very high self-sufficiency ratio for sulfuric acid, which helps to minimize import dependency and enhance overall supply chain resilience. This dual foundation in metallurgy and agriculture, supported by state backed industrial modernization, underpins Poland’s robust position in the regional acid market.

France Sulfuric Acid Market Analysis

France is also a significant player in the Europe sulfuric acid market, with its advanced chemical industry and expanding battery material ecosystem. The country’s sulfuric acid consumption is concentrated in Grand Est and Normandy, where major players operate large scale phosphate and specialty chemical facilities. The nation's consumption of sulfuric acid shows a significant portion is dedicated to the production of fertilizers, followed by metal processing activities. The country is able to support its domestic acidulation needs through a consistent supply of source rock from a single active phosphate mine. In the battery value chain, the use of sulfuric acid experienced considerable growth within the year. Moreover, France’s transport regulations under the ADR framework are among the most standardized in the EU, facilitating efficient acid logistics across Western Europe. These synergies between legacy chemical infrastructure and next generation electrochemical manufacturing sustain France’s top tier market position.

The Netherlands Sulfuric Acid Market Analysis

The Netherlands witnessed a consistent growth in the Europe sulfuric acid market by serving as a important logistics and processing node due to its strategic port infrastructure and integrated industrial clusters. Rotterdam and Moerdijk host major chemical parks where companies like OCI Nitrogen and Yara utilize sulfuric acid for fertilizer synthesis and industrial reagent production. The Netherlands imports significant quantities of molten sulfur, primarily sourced internationally, for use in domestic acid production facilities, highlighting its function as a central location for importing and distributing this material. Large volumes of sulfuric acid move through Dutch ports, destined for nearby countries. The nation demonstrates strong engagement in circular chemistry principles, with a high percentage of spent acid from industrial processes being regenerated and returned to use. Furthermore, an industrial park in Geleen is actively involved in testing innovative, more sustainable methods for producing sulfuric acid, leveraging regional initiatives and support. This convergence of maritime advantage, circular policy, and chemical innovation reinforces the Netherlands’ outsized influence in the regional sulfuric acid supply chain.

Sweden Sulfuric Acid Market Analysis

Sweden is likely to expand notably in the Europe sulfuric acid market from 2025 to 2033 due to its leadership in sustainable metallurgy and battery recycling. The country’s acid demand is primarily driven by Boliden’s smelting operations in Rönnskär and Harjavalta, which produce high grade copper, nickel, and zinc while generating notable metric tons of sulfuric acid annually as a byproduct. Swedish industrial processes effectively manage sulfur dioxide emissions, converting nearly all of them into a usable acid product. This approach aligns with broader national efforts aimed at minimizing waste generation. One recycling facility utilizes this type of acid to recover significant amounts of materials, including nickel, cobalt, and lithium, from older batteries. The amount of material recovered exceeds 95 percent of the total. A notable increase is expected in the country's capacity to recycle batteries in the coming years, which in turn will necessitate more acid. The electrical grid used for operations is predominantly fossil free, ensuring that any external energy used for acid production maintains a low carbon footprint. This unique integration of clean energy, advanced recycling, and byproduct valorization positions Sweden as a model for sustainable sulfuric acid utilization in Europe.

COMPETITIVE LANDSCAPE

The Europe sulfuric acid market features moderate competition characterized by a blend of integrated chemical producers metal refiners and specialized acid suppliers. Competition is not primarily price driven but instead centers on reliability of supply logistical efficiency regulatory compliance and sustainability credentials. Large players leverage byproduct acid from smelting operations to gain cost advantages while fertilizer manufacturers prioritize secure feedstock access. Smaller independent producers focus on niche applications such as high purity grades for electronics or battery recycling. The market exhibits high entry barriers due to capital intensity stringent safety regulations and complex permitting requirements. Strategic differentiation arises through circular economy initiatives such as acid regeneration and closed loop systems. Geographical proximity to end users particularly in industrial clusters like the Rhine corridor enhances competitive positioning. Overall competition is shaped more by operational excellence and integration depth than by aggressive pricing or market share battles.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the Europe Sulfuric Acid Market include

- BASF SE

- LANXESS AG

- Akzo Nobel N.V.

- Nouryon

- Arkema S.A

- Solvay S.A.

- INEOS Group

- Grupa Azoty S.A.

- Aurubis AG

Top Players in the Europe Sulfuric Acid Market

BASF SE

BASF SE is a leading German chemical company with extensive involvement in the Europe sulfuric acid market through its integrated production facilities and downstream chemical operations. The company utilizes sulfuric acid as a critical reagent in manufacturing fertilizers, detergents, and performance chemicals. In recent years BASF has reinforced its position by modernizing acid handling infrastructure at its Ludwigshafen site and advancing closed loop regeneration systems to align with EU circular economy mandates. The company also collaborates with metallurgical partners to optimize byproduct acid integration, reducing external procurement needs. These initiatives underscore BASF’s commitment to operational efficiency and environmental compliance while supporting stable sulfuric acid availability across its European value chain.

Aurubis AG

Aurubis AG is a major European copper producer headquartered in Germany and a significant generator of sulfuric acid as a byproduct of non ferrous metal smelting. The company operates large scale smelters in Hamburg Germany and Lünen Germany as well as in Olen Belgium producing high purity sulfuric acid that serves both internal refining processes and external chemical customers. Aurubis has recently invested in advanced gas cleaning and acid concentration technologies to enhance product quality and reduce emissions. The company also expanded its logistics capabilities for acid distribution via rail and barge to better serve customers across Central and Northern Europe. These strategic upgrades position Aurubis as a reliable and sustainable supplier within the regional sulfuric acid ecosystem.

Yara International ASA

Yara International ASA is a Norwegian based global leader in mineral fertilizers with substantial sulfuric acid consumption across its European production network. The company operates multiple phosphate fertilizer plants in the Netherlands Germany and France where sulfuric acid is essential for converting rock phosphate into plant available nutrients. Yara has strengthened its market role by securing long term sulfur supply agreements and implementing energy efficient acidulation processes that lower carbon intensity. Recently the company integrated digital monitoring systems at its Sluiskil Netherlands facility to optimize acid usage and minimize waste. Yara’s focus on decarbonizing fertilizer production while ensuring supply continuity reinforces its strategic importance in the Europe sulfuric acid value chain

Top Strategies Used by the Key Market Participants

Key players in the Europe sulfuric acid market primarily adopt strategies centered on vertical integration byproduct valorization and regulatory compliance. Companies operating in metallurgy generate sulfuric acid internally to reduce procurement dependence and stabilize costs. Chemical and fertilizer producers secure long term sulfur feedstock contracts to mitigate price volatility. Investments in acid regeneration and waste acid recycling systems align with EU circular economy directives and reduce environmental liability. Additionally firms enhance logistics through multimodal transport networks to navigate cross border regulatory complexities. Digital process optimization and real time monitoring improve efficiency and safety in acid handling. Collaborations with battery recyclers and green hydrogen projects open new demand channels. These strategies collectively bolster supply resilience competitiveness and sustainability across the European sulfuric acid landscape.

MARKET SEGMENTATION

This research report on the europe sulfuric acid market has been segmented and sub–segmented into the following categories.

By Application

- Fertilizers

- Chemical Manufacturing

- Metal Processing

- Textile

- Paper & Pulp

- Automotive

- Others

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

What is sulfuric acid used for in Europe?

Sulfuric acid is primarily used in fertilizer production, chemical manufacturing, petroleum refining, metal processing, and wastewater treatment across Europe.

What is driving the growth of the Europe sulfuric acid market?

Market growth is driven by increasing demand from fertilizer manufacturing, expanding chemical industries, and rising metal processing activities.

Which industry consumes the most sulfuric acid in Europe?

The fertilizer industry is the largest consumer, using sulfuric acid mainly for phosphate fertilizer production.

Which European countries lead the sulfuric acid market?

Germany, France, the United Kingdom, Italy, and Spain are major contributors due to strong industrial and agricultural sectors.

What impact does import and export activity have on the market?

Trade balances help stabilize supply in regions with limited production capacity.

How is the market segmented by application?

The market is segmented into fertilizers, chemicals, metal processing, petroleum refining, and others.

What technological advancements are shaping the market?

Advances in emission control systems and energy-efficient production processes are improving operational efficiency.

How does industrial growth affect sulfuric acid demand in Europe?

Expansion of industrial manufacturing directly increases sulfuric acid consumption.

What is the forecast outlook for the Europe sulfuric acid market?

The market is expected to grow steadily due to sustained industrial and agricultural demand.

What opportunities exist in the Europe sulfuric acid market?

Opportunities include growth in green chemicals, recycling-based sulfur recovery, and advanced industrial applications.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com