Europe Surgical Sealants and Adhesives Market Research Report By Product, Application & Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic & Rest of Europe) - Industry Size, Share, Trends, Growth, Forecast | 2026 to 2034

Market Size, 2025

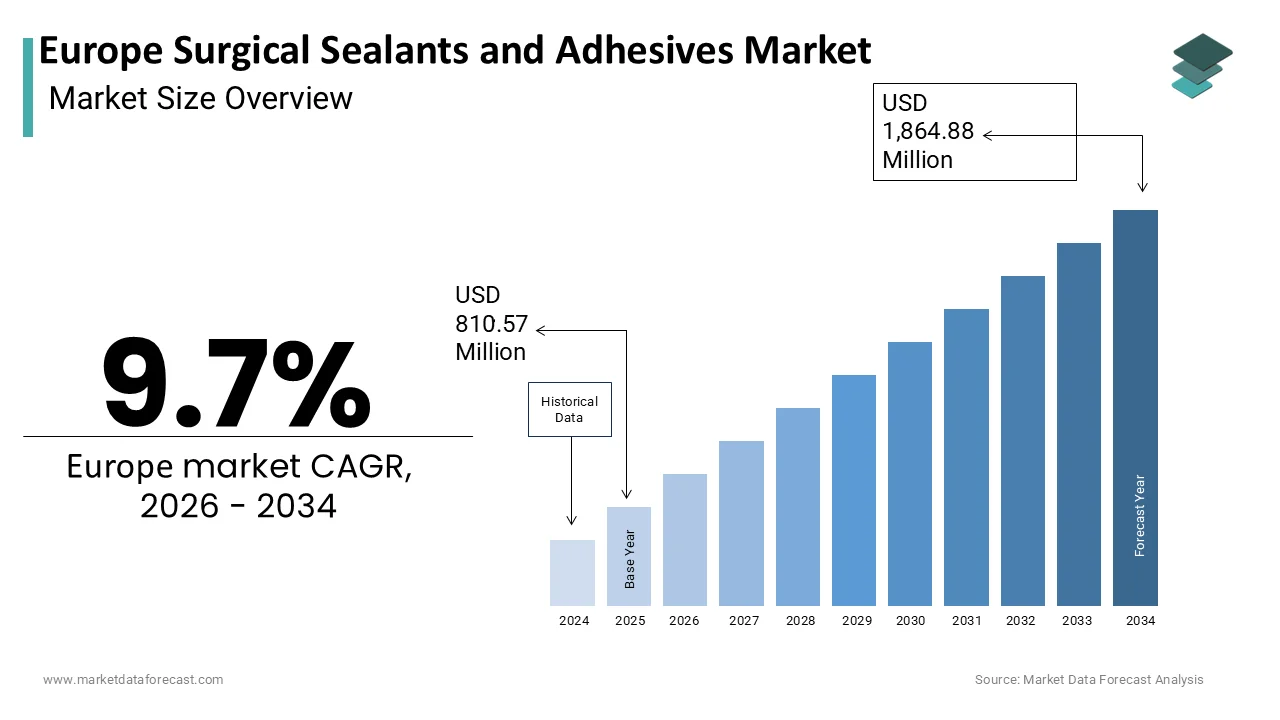

$810.57 MnMarket Estimate, 2026

$889.20 MnMarket Forecast, 2034

$1,864.88 MnCAGR, 2026–2034

9.7%Europe Surgical Sealants & Adhesives Market Executive Summary

The Europe Surgical Sealants & Adhesives Market was valued at USD 738.90 million in 2024, is expected to reach USD 810.57 million in 2025, and is projected to grow significantly to USD 1,699.99 million by 2033, registering a strong CAGR of 9.7% (2025–2033). Growth is supported by rising adoption of minimally invasive surgeries, increasing robotic-assisted procedures, and rising demand for effective hemostasis and tissue sealing solutions across high-volume specialties.

Market Highlights

- Market Size in 2024: USD 738.90 million

- Market Size in 2025: USD 810.57 million

- Market Forecast for 2033: USD 1,699.99 million

- Growth Rate (2025–2033): 9.7% CAGR

Europe Surgical Sealants & Adhesives Market Data Book

- 2024 Market Size — USD 738.90 million

2025 Market Size — USD 810.57 million

2033 Market Forecast — USD 1,699.99 million

CAGR (2025–2033) — 7% - Largest Product (2024) — Natural / Biological Sealants

Fastest-Growing Product — Synthetic & Semisynthetic Sealants — 9.8% CAGR - Largest Indication (2024) — Tissue Sealing & Hemostasis

Fastest-Growing Indication — Tissue Engineering — 12.3% CAGR - Largest Application (2024) — General Surgeries — 28.3%

Fastest-Growing Application — Pulmonary Surgeries — 10.7% CAGR - Largest Country (2024) — Germany — 26.3%

Country-Level Insights

- Germany leads with 26.3% market share, driven by high surgical volumes, robust reimbursement, and strong hospital infrastructure.

- France, the UK, Italy, and Spain show strong uptake supported by national guidelines, robotic surgery expansion, and increasing adoption of synthetic sealants.

Major Market Participants in Europe

CryoLife, Johnson & Johnson (Ethicon), Baxter International, C.R. Bard, Cohera Medical, Ocular Therapeutix, Vivostat A/S, Sealantis Ltd., Medtronic plc, Sanofi, B. Braun Melsungen AG.

Europe Surgical Sealants and Adhesives Market Size

The Europe Surgical Sealants and Adhesives Market is projected to grow from USD 810.57 million in 2025 to USD 889.20 million in 2026 and reach USD 1,864.88 million by 2034, registering a CAGR of 9.7% during the forecast period from 2026 to 2034.

Surgical sealants and adhesives are advanced biomaterials applied during operative procedures to achieve hemostasis, seal tissue interface, prevent fluid leakage, and approximate wound edges without traditional sutures or staples. In Europe, these products range from fibrin and collagen-based sealants to synthetic polyethylene glycol and cyanoacrylate formulations, which are integral to minimally invasive surgery, enhanced recovery protocols, and complex reconstructions in cardiothoracic, cardiac neurosurgery, and general surgery disciplines. As per the European Society of Anaesthesiology and Intensive Care, postoperative complications related to bleeding or anastomotic leakage contribute to 18% of surgical readmissions annually, where the clinical value of effective sealing technologies. The European Commission’s Medical Device Regulation classifies most surgical sealants as Class III devices requiring robust clinical evidence and stringent biocompatibility testing prior to market access.

MARKET DRIVERS

Rising Volume of Minimally Invasive and Robotic Surgeries

The rapid adoption of laparoscopic and robotic surgical techniques across Europe is a primary driver of demand for advanced surgical sealants and adhesives. These approaches limit tactile feedback and access to traditional suturing, tools, making liquid or sprayable sealants essential for managing bleeding and sealing pulmonary or hepatic parenchyma. National health systems increasingly reimburse sealant use in specific high-risk laparoscopic procedures, where Germany’s DRG catalog includes supplemental payments for fibrin sealants in liver resections, while France’s National Authority for Health recommends polyethylene glycol-based adhesives for lung volume reduction surgery. This procedural shift, coupled with institutional endorsement, ensures consistent and growing clinical adoption.

High Burden of Surgical Complications Driving Preventive Adoption

The postoperative complications, such as bleeding, cerebrospinal fluid leakage, and anastomotic dehiscence, impose significant clinical and economic burdens, prompting proactive use of sealants as preventive measures is additionally elevating the growth of the European surgical sealants and adhesives market. According to the European Board of Surgical Qualification, postoperative hemorrhage occurs in 4 to 6% of major abdominal surgeries, leading to extended hospital stays and increased transfusion needs. These evidence-based recommendations transform sealants from optional adjuncts into essential components of complication prevention strategies.

MARKET RESTRAINTS

Stringent Regulatory Hurdles Under the EU Medical Device Regulation

The European Union Medical Device Regulation has significantly increased the time and cost of bringing new surgical sealants is a major attribute limiting the growth of the European surgical sealants and adhesives market. Unlike the previous Medical Devices Directive, the MDR requires comprehensive clinical investigation data, biocompatibility testing under ISO 10993, and post-market surveillance plans for all Class III devices, including most sealants. Additionally, only 14 notified bodies are currently designated for Class III devices as per the European Commission’s NANDO database, creating severe bottlenecks. Small and medium-sized enterprises face particular challenges in developing a full technical dossier can cost over 500,000 euros and require multi-center trials across three EU countries. This regulatory complexity delays access to next-generation bioresorbable and antimicrobial sealants and disproportionately favors large multinationals with established quality systems, stifling competition and limiting clinical choice.

Limited Reimbursement for Advanced Sealant Technologies

Many advanced surgical sealants face inconsistent or absent reimbursement across healthcare systems, limiting their routine use, which is additionally to degrade growth. According to the European Health Management Association, only 11 of the 27 EU member states provide specific procedure-based reimbursement for synthetic sealants, with most relying on lump-sum diagnosis-related group payments that do not cover high-cost adjuncts. In Italy and Spain, hospitals must absorb the full cost of sealant, which can range from 350 to 800 euros per unit, as reported by the Italian Society of Surgical Technology. Consequently, adoption remains confined to tertiary centers or high-risk cases even when clinical guidelines support broader use. Germany offers supplementary payments for fibrin sealants in liver surgery but excludes synthetic alternatives, creating a market distortion that discourages innovation.

MARKET OPPORTUNITIES

Integration with Antimicrobial and Drug Delivery Platforms

The development of surgical sealants embedded with antimicrobial agents or therapeutic payloads presents a transformative opportunity to address infection and enhance healing. According to the European Centre for Disease Prevention and Control, surgical site infections affect 2 to 5% of patients annually, with deep organ space infections increasing mortality by 30%. In response, companies are engineering sealants that release antibiotics, antiseptics, or growth factors directly at the surgical site. Similarly, the European Commission’s Horizon Europe program funded the “SmartSeal” project to develop fibrin matrices that release VEGF to accelerate vascularization in reconstructive flaps. These multifunctional platforms align with the EU’s priority on antimicrobial stewardship and personalized medicine, offering surgeons tools that go beyond mechanical sealing to actively modulate the wound environment and improve outcomes.

Expansion into Regenerative and Soft Tissue Reconstruction Surgery

The growing demand for complex soft tissue repairs in trauma, oncology, and reconstructive surgery is creating new opportunities for the growth of the European surgical sealants and adhesives market. According to the study, over 1.2 million reconstructive procedures were performed in the EU in 2023, often involving fragile tissues where sutures cause tearing. Sealants based on fibrin or synthetic hydrogels provide gentle yet secure adhesion for skin grafts, nerve coaptation, and dural closure without mechanical trauma. In craniofacial reconstruction, surgeons increasingly use light-activated adhesives to fix bone fragments in pediatric patients, avoiding metal hardware. The European Tissue Engineering and Regenerative Medicine Society endorses sealant use in scaffold-based therapies to secure biologics at the defect site. As regenerative approaches gain traction, sealants evolve from passive barriers to active enablers of tissue integration and functional recovery, opening high-value niches beyond traditional hemostasis and sealing.

MARKET CHALLENGES

Lack of Standardized Clinical Protocols and Surgeon Training

The inconsistent use of surgical sealants due to the absence of universal clinical protocols and formalized surgeon training programs is degrading the growth of the European surgical sealants and adhesives market. According to a 2023 survey, only 38% of general surgery residency programs include structured modules on sealant selection application techniques or indications. This knowledge gap leads to wide practice variation, while 72% of cardiothoracic surgeons in Germany routinely use sealants for lung resections, less than 25% of general surgeons in Eastern Europe do so for similar procedures. Moreover, national guidelines often lack specificity on product types or dosing, leaving decisions to individual preference. This inconsistency undermines cost-effectiveness analyses and hampers health technology assessment.

Biocompatibility and Long-Term Safety Concerns with Synthetic Formulations

Persistent concerns about inflammatory responses, foreign body reaction, and degradation byproducts of synthetic sealants pose a significant challenge to their acceptance in sensitive anatomical sites. The bio-compatibility and long-term safety concerns with synthetic formulations are another attribute to acts as a barrier for the growth of the European surgical sealants and adhesives market. According to some reports, 42 cases of granuloma formation are linked to polyethylene glycol-based sealants used in spinal and cranial procedures. Although rare, these events trigger heightened scrutiny from regulatory bodies and surgical societies. In France, the National Agency for Medicines and Health Products Safety issued a 2022 safety alert recommending caution with cyanoacrylate adhesives in pediatric neurosurgery due to exothermic polymerization risks.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Product, Indication, Application, and Region. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, Rest of Europe |

| Market Leaders Profiled | CryoLife, Inc., Johnson & Johnson, Ethicon, Inc., Baxter International, Inc., C.R. Bard, Inc., Cohera Medical, Inc., Ocular Therapeutix, Inc., Vivostat A/S, Sealantis Ltd, Medtronic plc, Sanofi Group, B. Braun Melsungen AG |

SEGMENTAL ANALYSIS

By Product Insights

The Natural/Biological segment accounted in holding a dominant share of the European surgical sealants and adhesives market in 2025. Natural sealants are primarily fibrin and collagen-based formulations, an have decades of clinicuse in n high-risk surgeries where biocompatibility is non-negotiable. In neurosurgery, the European Association of Neurosurgical Societies endorses dural sealants derived from human fibrinogen for cerebrospinal fluid leak prevention due to their seamless integration with native tissue. This safety advantage is critical in cranial, spinal, and pediatric applications where even minor inflammation can compromise outcomes. National health technology assessments in Germany and Sweden consistently rate fibrin sealants as “high value” for specific indications, reinforcing institutional procurement and surgeon trust.

The Synthetic & Semisynthetic Sealants and Adhesives segment is projected to grow at a CAGR of 9.8% throughout the forecast period. Synthetic sealants based on polyethylene glycol poloxamers or cyanoacrylates offer rapid curing, strong adhesion, and resistance to fluid shear forces, hhigh-pressuree or dynamic tissues. In robotic lung surgery, where tactile feedback is limited, surgeons rely on light-activated or sprayable synthetics that set in seconds without manual compression. Next-generation synthetic sealants integrate antimicrobial agents, growth factors, or hemostatic nanoparticles, expanding their therapeutic role. Similarly, a Dutch consortium launched a resorbable PEG hydrogel that releases VEGF to enhance tissue integration in breast reconstruction. These platforms align with the EU’s priority on antimicrobial stewardship and regenerative medicine.

By Indication Insights

The tissue sealing & hemostasis segment was the largest by accounting for a prominent share of the European surgical sealants and adhesives market in 2025. Bleeding remains one of the most common and costly surgical complications in Europe. Sealants and adhesives are routinely used to supplement sutures in parenchymal organs, where traditional methods are insufficient. National guidelines in Sweden and Germany mandate hemostatic agent use in partial nephrectomies to preserve renal function. Blood transfusions and reoperations for bleeding significantly inflate hospital costs. According to the study, managing a single postoperative hemorrhage episode adds 8,200 to 12,500 euros to the episode cost. Hospitals under diagnosis-related group payment systems increasingly adopt sealants as cost avoidance tools. In the UK, the National Health Service estimates that routine use of fibrin sealants in liver surgery reduces transfusion needs by 35% translating to 1,200 euros saved per case. Similarly, the French National Authority for Health includes sealant efficacy in its medico-economic evaluations for procedure reimbursement.

The Tissue Engineering segment is expected to register the fastest CAGR of 12.3% throughout the forecast period. Surgical sealants serve as delivery vehicles and fixation matrices in tissue engineering applications. In maxillofacial reconstruction, surgeons apply sealants to anchor 3D printed bioceramic implants,s, ensuring stability during vascularization. Cancer resections and trauma injuries often require large tissue replacement, where sealants enable secure integration of grafts and flaps. In breast reconstruction after mastectomy, surgeons use uselight-activated adhesives to secure acellular dermal matrices without sutures, reducing seroma formation. National cancer plans in Germany and the Netherlands now include regenerative reconstruction as standard care, driving sealant adoption in oncology pathways.

By Application Insights

The general surgeries segment was the largest by accounting for 28.3% of the European surgical sealants and adhesives market in 2025. As per recent survey reports, 74% of laparoscopic liver resections now use hemostatic sealants to control parenchymal bleeding. These standardized protocols across high-volume procedures create massive, consistent demand across public and private hospitals. The rise of laparoscopic and robotic general surgery has increased reliance on sealants for staple line reinforcement.

The Pulmonary Surgeries segment is likely to grow at a CAGR of 10.7% from 2025 to 2033.Eurorolloutt of low-dose lung cancer screening is dramatically increasing early-stage resection volumes. According to the study, 14 member states launched population-based screening in 2023, with Germany alone detecting over 8,000 early-stage nodules requiring sublobar resection. These parenchymal sparing procedures have high air leak rates up to 40% in segmentectomies by making sealants clinically indispensable. These approaches limit manual tissue handling, making staple line reinforcement with synthetic sealants critical. Hospitals invest in integrated delivery systems that apply sealants through a 5 millimeter port, enabling precise application without instrument exchange.

COUNTRY LEVEL ANALYSIS

Germany Surgical Sealants And Adhesives Market Analysis

Germany was the top performer of the European surgical sealants and adhesives market by capturing 26.3% of the share in 2025, with its high surgical volume ad advanced healthcare infrastructure, and stringent quality standards. Germany’s DRG system includes specific supplementary payments for sealant use in li, ver lung, and neurosurgery, ensuring consistent hospital procurement. The Federal Joint Committee regularly updates its benefit assessments to include new sealant indications based on HTA evaluations. Leading university hospitals in Berlin, Munich, and Heidelberg serve as European reference centers for robotic and minimally invasive surgery, where sealant adoption is near universal. This combination of volume policy and clinical leadership solidifies Germany’s dominant position.

France Surgical Sealants And Adhesives Market Analysis

The French surgical sealants and adhesives market was positioned second by holding 15.2% of share in 2025 due to centralized health technology assessment and strong uptake in public hospitals. The National Authority for Health conducts rigorous medico-economic evaluations and has issued positive opinions for over 15 sealant products since 2020. France’s public hospital system performs 78% of complex surgeries, driving bulk procurement through group purchasing organizations like UNAH. The country is a pioneer in robotic thoracic and colorectal surgery, with centers in Lyon and Paris routinely using synthetic sealants for staple reinforcement. Additionally, France’s National Cancer Institute mandates sealant use in lung and liver resections as part of its standardized care pathways.

United Kingdom Surgical Sealants And Adhesives Market Analysis

The United Kingdom surgical sealants and adhesives market growth is likely to be driven by the cost-effectiveness and complication prevention under the National Health Service. NICE guidelines endorse sealants for air leak management after lung resection and dural sealing in neurosurgery, creating national standards of care. Teaching hospitals in London, Oxford, and Edinburgh lead in complex reconstructions and transplant surgery, where biological sealants are standard.

Italy Surgical Sealants And Adhesives Market Analysis

Italy's surgical sealants and adhesives market growth is likely to grow with the high volume of general and oncologic surgery and regional healthcare autonomy. Italy’s National Cancer Plan includes specific funding for advanced surgical technologies, including sealants in hepatic and pulmonary resections. Regional health agencies in Lombardy and Emilia Romagna have implemented local formularies that approve premium sealants for high-risk procedures. Additionally, Italy is a hub for reconstructive surgery with plastic surgery units in Florence and Bologna using adhesives for complex flap fixation.

COMPETITIVE LANDSCAPE

The European surgical sealants and adhesives market is characterized by intense but differentiated competition among global medtech leaders and specialized biologics companies. Unlike commodity medical device segments, competition here is defined by clinical validation, regulatory compliance, and integration into surgical pathways rather than price. Established players leverage decades of real-world evidence and plasma supply chains to dominate the biological segment while innovators advance synthetic platforms with superior mechanical properties. The EU Medical Device Regulation has raised entry barriers favoring firms with mature quality systems and notified body relationships. Competition is further segmented by application, cardiothoracic, and neurosurgery favor biologicals for biocompatibility, while general and robotic surgery increasingly adopt synthetic across high-volume. Reimbursement heterogeneity across member states creates market fragmentation, requiring localized health economics strategies.

KEY MARKET PLAYERS

Prominent Companies dominating the europe surgical sealants and adhesives market profiled in the report are

- CryoLife, Inc

- Johnson & Johnson

- Ethicon, Inc.

- Baxter International, Inc

- C.R. Bard, Inc

- Cohera Medical, Inc

- Ocular Therapuetix, Inc

- Vivostat A/S

- Sealantis Ltd

- Medtronic plc

- Sanofi Group

- B. Braun Melsungen AG.

TOP LEADING PLAYERS IN THE MARKET

- Baxter International.c is a global leader in biological surgical sealants with a strong presence in Europe through its Tisseel and Evicel fibrin sealant portfolios. The company leverages plasma fractionation expertise and decades of clinical validation to serve cardiothoracic, neurosurgical, and general surgery markets. In recent years, Baxter has expanded manufacturing capacity at its facilities in Germany and Austria to meet growing European demand and ensure supply resilience under the EU Medical Device Regulation. It actively collaborates with surgical societies such as the European Association for Cardio-Thoracic Surgery to develop evidence-based application guidelines. Through continuous investment in ipost-marketet registries and real-world outcomes studies, Baxter reinforces the clinical and economic value of its biological sealants acrohigh-volumeume European procedures.

- Ethicon Inc. plays a pivotal role in the European surgical sealants and adhesives market through its advanced synthetic and hemostatic platform, including SurgiSeal and Evarrest. The company integrates sealant technologies into its broader portfolio of energy devices and sutures, enabling bundled solutions for minimally invasive and robotic surgery. It also expanded its training programs with the European Academy of Robotic Surgery to educate surgeons on optimal sealant use in robotic workflows.

- Takeda Pharmaceutical Company Limited contributes to the European market through its Nycomed legacy fibrin sealant product, including Beriplast and TachoSil which are widely used in hepatic neurosurgical and oncologic procedures. The company maintains plasma collection and manufacturing infrastructure compliant with EU blood safety directives, ensuring consistent quality and viral safety. In recent years, Takeda has deepened engagement with national health technology assessment bodies in Germany, France, and the UK to demonstrate the cost-effectiveness of sealants in reducing transfusions and reoperations. It also participates in EU-funded clinical registries tracking sealant performance in real-world settings.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Key players in the European surgical sealants and adhesives market focus on generating robust clinical and health economic evidence to support reimbursement and guideline inclusion. They align product development with minimally invasive and robotic surgical workflows by designing delivery systems compatible with narrow trocars and endoscopic instruments. Companies invest in plasma fractionation and synthetic polymer manufacturing within the EU to ensure supply chain compliance with the Medical Device Regulation and blood safety directives. Strategic collaborations with surgical societies and academic centers drive adoption through training programs and real-world data collection. Additionally, firms pursue indication expansion into regenerative and reconstructive surgery by integrating sealants with tissue engineering scaffolds and drug delivery platforms to create multifunctional therapeutic solutions.

MARKET SEGMENTATION

This research report on the europe surgical sealants and adhesives market has been segmented and sub-segmented into the following categories.

By Product

-

Natural/Biological Surgical Sealants & Adhesives

- Polypeptide/Protein-based Sealants & Adhesives

- Polysaccharide-based Sealants & Adhesives

- Synthetic & Semisynthetic Sealants and Adhesives

- Cyanoacrylates

- Polyethylene Glycol-based Hydrogel

- Urethane-based Adhesives

By Indication

- Tissue Sealing & Hemostasis

- Tissue Engineering

By Application

- Central Nervous System Surgeries

- General Surgeries

- Cardiovascular Surgeries

- Orthopedic Surgeries

- Cosmetic Surgeries

- Ophthalmic Surgeries

- Urological Surgeries

- Pulmonary Surgeries

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

1. How does the aging population impact the Europe Surgical Sealants and Adhesives Market?

An increasing geriatric population in Europe leads to higher incidences of chronic diseases requiring surgeries, which significantly fuels the Europe Surgical Sealants and Adhesives Market expansion.

2. Which countries are leading in the Europe Surgical Sealants and Adhesives Market?

Germany, the UK, France, and Italy are the leading contributors to the Europe Surgical Sealants and Adhesives Market due to advanced healthcare infrastructure and investments.

3. What are the main types of products in the Europe Surgical Sealants and Adhesives Market?

The Europe Surgical Sealants and Adhesives Market includes natural or biological types like fibrin and collagen sealants and synthetic options like cyanoacrylates and hydrogels.

4. How are technological advancements influencing the Europe Surgical Sealants and Adhesives Market?

Innovations such as PEG-based sealants and bio-based adhesives with improved biocompatibility and biodegradability are expanding the Europe Surgical Sealants and Adhesives Market.

5. What role does minimally invasive surgery play in the Europe Surgical Sealants and Adhesives Market?

Minimally invasive surgeries increase the demand for efficient wound closure materials, driving faster adoption in the Europe Surgical Sealants and Adhesives Market.

6. How are government policies affecting the Europe Surgical Sealants and Adhesives Market?

Supportive healthcare policies, reimbursement mechanisms, and investments in hospital infrastructure in Europe are positively influencing growth in the Europe Surgical Sealants and Adhesives Market.

7. What surgical specialties contribute the most to the Europe Surgical Sealants and Adhesives Market?

Key specialties include cardiovascular, orthopedic, neurological, and general surgery, which account for major shares in the Europe Surgical Sealants and Adhesives Market.

8. How is the Europe Surgical Sealants and Adhesives Market segmented by application?

Applications in the Europe Surgical Sealants and Adhesives Market span tissue sealing, hemostasis, tissue engineering, and specialty surgeries like ophthalmology and urology.

9. What challenges does the Europe Surgical Sealants and Adhesives Market face?

Challenges include stringent regulatory approvals, high product costs, and competition from traditional wound closure methods in the Europe Surgical Sealants and Adhesives Market.

10. How important is biocompatibility in the Europe Surgical Sealants and Adhesives Market?

Biocompatibility is crucial, as products must be safely absorbed or integrated by tissues, minimizing inflammation and accelerating healing in the Europe Surgical Sealants and Adhesives Market.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com