Europe Taxi Market Size, Share, Trends, COVID-19 Impact & Growth Forecast Research Report, Segmented By Service Type, Booking Type, Vehicle Type and Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic and Rest of Europe), Industry Analysis From (2026 to 2034)

Market Size, 2025

$83.68 BnMarket Estimate, 2026

$90.47 BnMarket Forecast, 2034

$168.82 BnCAGR, 2026–2034

8.11%Europe Taxi Market Size

The European taxi market size was valued at USD 83.68 billion in 2025 and is anticipated to reach USD 90.47 billion in 2026 and USD 168.82 billion by 2034. growing at a CAGR of 8.11% during the forecast period from 2026 to 2034.

Unlike ride-hailing services, conventional taxis are typically regulated at municipal levels, requiring specific permits, vehicle markings, and fare structures. As per the International Road Transport Union, there are approximately 400,000 taxis operating across the European Union, which represents a critical component of public mobility, particularly for tourists, elderly populations, and individuals in areas with limited ride-hailing penetration. In cities like Vienna, Lisbon, and Helsinki, taxis are integrated into multimodal transit networks, with designated ranks at airports, train stations, and hospitals. As per the European Commission, taxis and private hire vehicles are essential for urban mobility, providing flexible door-to-door transport that complements public transit systems, underscoring their role in last-mile connectivity and non-private vehicle mobility.

High Urbanization and Congestion-Driven Demand for Point-to-Point Mobility

Europe dense urban centers, where private car ownership is increasingly impractical due to traffic congestion and parking constraints have amplified reliance on taxis for efficient point-to-point travel, which is one of the major factors propelling the European taxi market expansion. According to Eurostat, 75% of Europeans live in urban areas, with cities like Paris, Rome, and London facing significant traffic challenges that discourage private vehicle use. This congestion discourages private vehicle use, prompting commuters and visitors to opt for taxis that can navigate dedicated lanes and access restricted zones. As per Transport for London, licensed taxis remain a vital part of the city transport network, providing accessible and reliable services that account for a meaningful portion of central zone travel despite representing a small fraction of total vehicles. The predictability of metered fares and availability at transit hubs further solidify taxis as a preferred alternative to driving in high-density environments.

MARKET DRIVERS

Tourism Recovery and Airport Passenger Volume Surge

The resurgence of international travel has significantly boosted demand for airport taxi services, which is a core segment of the European taxi market and is further contributing to the regional market growth. As per Eurostat, 1.1 billion people in the European Union traveled by air in 2024, representing an 8.3% increase compared with the previous year and surpassing pre-pandemic levels. Airports remain primary access points for taxi usage, particularly among tourists unfamiliar with local public transit or carrying luggage. According to the International Air Transport Association, air travel demand has shown a robust recovery across European hubs, with major airports recording full capacity on intra-European routes. Additionally, regulated taxi ranks at terminals ensure safety and transparency, reinforcing consumer confidence in comparison to unlicensed operators.

MARKET RESTRAINT

Regulatory Fragmentation and Licensing Barriers Across Municipalities

The lack of harmonized regulations with licensing, pricing and operational rules determined at city or regional levels is a significant impediment to the European taxi market growth. According to the European Commission, taxi and private hire vehicle regulations vary significantly across member states, often creating administrative complexity for fleet operators. In cities like Berlin and Paris, obtaining a taxi license can involve high costs and lengthy waiting periods, which may discourage new entrants and limit supply. As per the European Transport Workers Federation, the workforce in the taxi sector is facing challenges as traditional licensing barriers and high operational costs make the profession less attractive to new drivers. This fragmentation stifles innovation, reduces service availability, and weakens the sector ability to compete with centralized digital platforms.

Competition from Ride-Hailing Platforms with Dynamic Pricing and App-Based Convenience

The proliferation of ride-hailing services such as Uber, Bolt, and Free Now has significantly eroded the market share of traditional taxis, particularly among younger and tech-savvy users, which is further impeding the regional market expansion. According to a consumer mobility survey, 68% of urban Europeans aged 18 to 35 prefer app-based ride-hailing due to real-time tracking, cashless payments, and price transparency. In contrast, only 29% reported using traditional taxis in the past month. As per industry assessments, ride-hailing platforms now account for over 40% of on-demand urban trips in several major metropolitan areas where digital adoption is high. While taxis operate under fixed tariffs, ride-hailing services leverage dynamic pricing and surge algorithms, often offering lower off-peak rates. This technological and experiential gap has diminished taxi ridership, especially in metropolitan areas where digital adoption is high.

MARKET OPPORTUNITY

Integration of Taxis into Multimodal Mobility Platforms

The incorporation of licensed taxis into unified digital mobility ecosystems that combine public transit, bike-sharing, and ride services is a promising opportunity for the European taxi market. As part of the EU Mobility as a Service initiative, cities like Helsinki and Vienna have integrated taxi services into apps such as Whim and WienMobil, allowing users to plan, book, and pay for end-to-end journeys seamlessly. According to recent mobility data, usage of multimodal trip planning apps has increased significantly as commuters seek more flexible travel options. As per the European Commission, integrating taxis into these platforms could increase their utilization rate by 30% in underserved areas. This shift not only modernizes the sector but also aligns with sustainability goals by reducing reliance on private vehicles.

Electrification and Green Incentive Programs for Urban Fleets

The transition to low-emission urban transport presents a strategic opportunity for taxi operators to adopt electric vehicles supported by national and municipal incentives. According to the European Environment Agency, several major European cities have introduced subsidies or tax exemptions for electric taxi conversions to reduce urban pollution. In Paris, taxi drivers receive significant financial support to replace older vehicles with electric models, contributing to a notable rise in green taxi registrations. As per the Île-de-France Mobility Authority, the number of electric taxis in the region increased by 40% between 2021 and 2023. Additionally, zero-emission zones in cities like Oslo and Brussels grant electric taxis unrestricted access, improving operational efficiency. With high annual mileage, electrification offers substantial fuel and maintenance savings, positioning the sector as a key beneficiary of Europe’s green mobility transition.

MARKET CHALLENGES

Aging Driver Demographics and Workforce Shortages

The critical labor shortage due to an aging workforce and declining interest among younger generations is primarily challenging the European taxi market growth. According to the European Transport Workers Federation, the average age of licensed taxi drivers in several major European countries exceeds 57 years, with recruitment rates insufficient to offset retirements. As per a study by the German Federal Ministry of Transport, 43% of taxi licenses in Berlin were held by drivers over 65, while only 8% of new applicants were under 40. This demographic imbalance threatens service continuity, particularly in rural and peri-urban areas. The demanding nature of the job, irregular hours, and perceived lack of social recognition further deter new entrants. Without targeted training programs and improved working conditions, the sector risks systemic capacity decline, undermining urban mobility resilience.

Technological Lag in Booking and Payment Infrastructure

Many traditional taxi operators remain technologically outdated that rely on radio dispatch and cash payments, which diminishes competitiveness against digital-first platforms is also challenging the regional market expansion. According to digital maturity assessments, only 39% of taxis in Southern and Eastern Europe offer app-based booking or contactless payment options, whereas the vast majority of ride-hailing trips are fully digital. This gap alienates tech-dependent users and reduces operational efficiency. As per the European Payments Council, cash transactions still account for 52% of taxi fares in countries like Greece and Poland, increasing security risks and transaction time. While initiatives like the EU-funded Taxi2030 project aim to modernize fleets with integrated digital terminals, widespread adoption is hindered by cost and fragmented ownership structures, leaving many operators unable to bridge the digital divide.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 7.9% |

| Segments Covered | By Service, Type, Booking Type, Vehicle Type, and Country. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Market Leaders Profiled | Uber, FreeNow, Hopp, Ola, Gett, Addison Lee, London Lady Chauffeurs, Bolt, iTaxi, Helbiz, YandexTaxi, Taxi Polska, MiniTaxi, MOIA (a subsidiary of Volkswagen), BerlKönig, and Others. |

SEGMENTAL ANALYSIS

By Service Insights

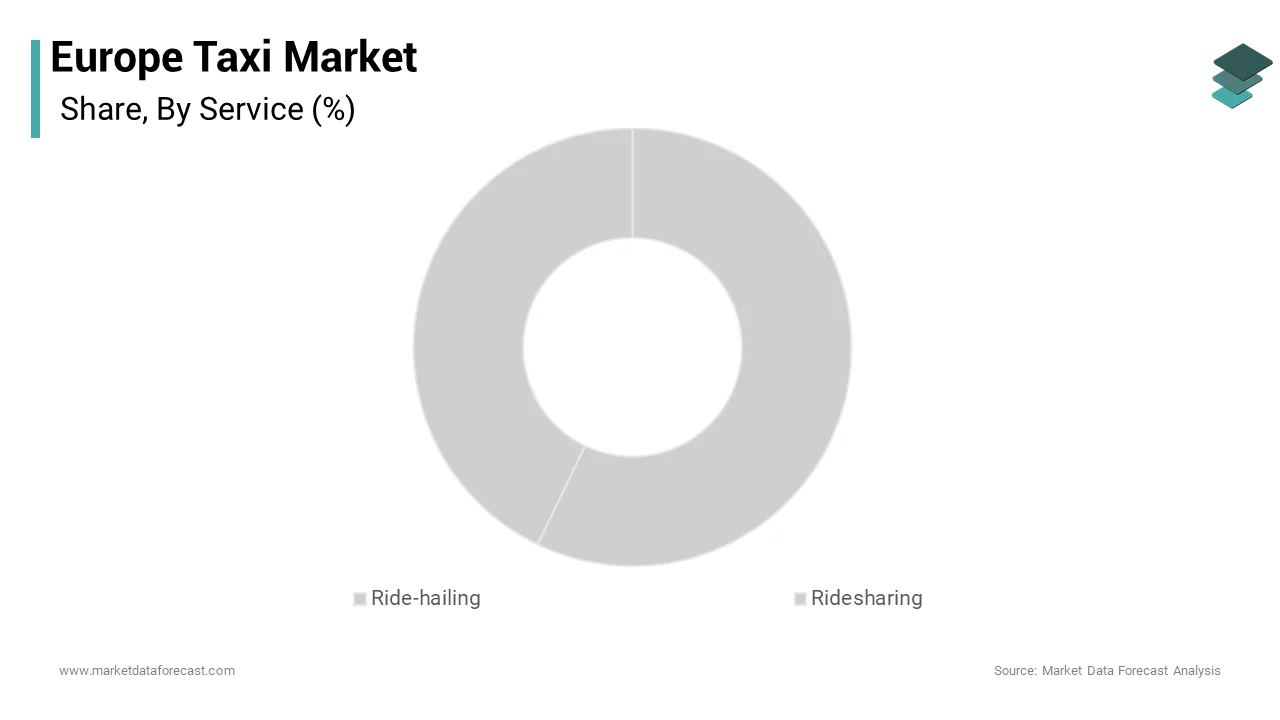

The ride-hailing segment dominated the Europe taxi market by capturing 63.6% of European market share in 2025. The dominance of ride-hailing segment in the European market is primarily driven by the widespread adoption of app-based platforms like Uber, Bolt, and Free Now. According to a consumer survey, 71% of urban users in cities like Amsterdam, Lisbon, and Vienna prefer ride-hailing due to its reliability and integration with digital payment systems. The model scalability is further reinforced by its ability to operate across regulatory boundaries with relative agility compared to traditional taxi licensing regimes. Additionally, partnerships with corporate mobility programs and integration into corporate travel platforms have expanded business-use adoption, particularly in financial and tech hubs such as Frankfurt and Dublin, where on-demand mobility is essential for professional efficiency.

On the other end, the ride sharing segment is estimated to grow at the fastest CAGR of 15.4% during the forecast period in the European market owing to the rising environmental awareness and the demand for cost-efficient, socially connected urban mobility. Unlike ride-hailing, which offers private trips, ridesharing involves shared journeys with dynamically matched passengers traveling in similar directions, reducing per-capita emissions and congestion. As per the European Environment Agency, shared mobility services can reduce carbon emissions by up to 30% per passenger-kilometer compared to single-occupancy vehicles. According to BlaBlaCar, the platform carried 80 million passengers in 2023, an annual increase of 23%, with intercity routes showing high growth. The European Commission Urban Mobility Framework has also incentivized shared transport through funding for integrated platforms. Moreover, younger demographics, particularly students and remote workers, are embracing ridesharing for long-distance travel due to affordability and social interaction, positioning it as a sustainable alternative to private car ownership.

By Booking Insights

The online booking segment had the largest share of the European taxi market in 2025. The growth of the online booking segment in the European market is attributed to the ubiquity of smartphones and high-speed mobile internet. As per the European Commission, over 85% of Europeans use the internet regularly, with a vast majority utilizing mobile devices for daily services. Platforms like Uber, Free Now, and Bolt have streamlined the booking process with GPS integration, fare estimation, and driver tracking, significantly enhancing user confidence and convenience. According to the European Payments Council, contactless and digital payments now account for 76% of online taxi transactions, reducing friction and improving security. The shift is further accelerated by post-pandemic hygiene concerns, with consumers avoiding cash and physical dispatch points in favor of touchless digital interactions.

The offline booking segment is predicted to expand at a CAGR of 5.4% during the forecast period in the European market, defying digital dominance in specific contexts where reliability and accessibility outweigh app-based convenience. This resurgence is particularly evident among elderly populations, tourists unfamiliar with local apps, and in areas with poor digital connectivity. According to a study on elderly mobility, 58% of adults over 65 still prefer hailing taxis or calling dispatch centers due to digital literacy barriers. Similarly, in historic city centers like Prague, Dubrovnik, and Florence, where narrow streets limit app-based navigation, traditional taxi ranks remain primary access points. As per Transport for London, black cabs at Heathrow and Victoria Station serve over 1.2 million offline passengers monthly. Municipal efforts to modernize radio dispatch systems and introduce hybrid digital terminals in conventional fleets are enhancing service quality, ensuring offline booking remains a viable, trusted option.

By Vehicle Insights

The cars segment accounted for the highest share of 90.9% of the European market in 2025. Cars represent the dominant vehicle type in the Europe taxi market, accounting for 91% of all service vehicles in operation as of 2023, which is rooted in universal passenger expectations for comfort, luggage capacity, and weather-protected travel. In major hubs like Frankfurt and Paris, over 85% of arriving passengers opt for car taxis due to space and safety considerations. According to the European Automobile Manufacturers Association, purpose-built taxi models are engineered for durability and high-mileage urban operations, offering durability and accessibility. Additionally, regulatory frameworks in countries like the UK and Germany mandate minimum vehicle standards for licensed taxis, reinforcing the preference for four-wheel sedans and MPVs over smaller alternatives, especially for families and business travelers.

However, the motorcycle taxis segment is on the rise and is predicted to record a CAGR of 12.2% during the forecast period in the European market owing to their agility in congested urban environments and lower operational costs. In cities like Rome, Athens, and Lisbon, where traffic congestion reduces average speeds to below 15 km/h, motorcycle taxis offer faster last-mile delivery and passenger transit. According to the INRIX Global Traffic Scorecard, motorized two-wheelers can bypass traffic delays by up to 40% compared to cars during peak hours. Companies like MOTOVOX in Italy and RapidRide in Spain have expanded fleets of licensed motorcycle taxis equipped with passenger seating and weather protection. As per mobility reports, there has been a notable increase in licensed motorcycle taxi registrations in Southern Europe. Additionally, their lower emissions and reduced parking footprint align with urban sustainability goals, making them an attractive solution for eco-conscious municipalities aiming to decongest city centers.

COUNTRY-LEVEL ANALYSIS

Germany Taxi Market Analysis

Germany held the dominating position in the European taxi market in 2025 and is likely to solidify its position as the largest taxi market in the region over the next few years as it continues to modernize its Passenger Transport Act to integrate digital platforms with traditional services. Germany holds the largest share of the Europe taxi market, accounting for approximately 22% in 2023, which is a result of its highly regulated yet technologically progressive framework. With over 75,000 licensed taxis, Germany emphasizes safety, vehicle standards, and driver training, ensuring high service quality. The introduction of the Passenger Transport Act modernized fare structures and allowed app-based dispatch, enabling integration with Free Now and Uber. According to the German Taxi Association, over 30% of new taxi registrations in 2023 were electric, reflecting a strategic shift toward sustainable urban mobility within a disciplined regulatory environment.

UK Taxi Market Analysis

The UK is likely to see a rapid full electrification of its urban taxi fleet over the next few years as London and other major cities enforce strict zero-emission requirements for all newly licensed vehicles. The UK commands a 19% share of the European taxi market, distinguished by its iconic black cab and advanced digital integration. London Public Carriage Office licenses over 21,000 Knowledge-trained drivers, a unique system requiring mastery of 25,000 streets, ensuring unmatched navigational reliability. As per Transport for London, black cabs complete over 300,000 trips weekly, with high usage at Heathrow and central business districts. According to the Office for Zero Emission Vehicles, there was a 55% increase in electric taxi registrations in 2023, as the country shifts toward sustainable transport. This duality of heritage and innovation positions the UK as a leader in regulated, sustainable urban transport.

France Taxi Market Analysis

France is likely to achieve a higher degree of market harmony over the next few years as traditional taxi cooperatives and ride-hailing platforms increasingly collaborate through unified booking apps. France holds a 17% share of the regional market, characterized by a complex interplay between traditional taxi operators and disruptive digital platforms. According to the Ministry of Ecological Transition, over 60,000 licensed taxis operate nationwide, with high concentration in Paris where G7 taxis dominate airport and hotel transfers. In response to digital disruption, traditional operators have adopted apps like Taxis G7 and Heetch, enabling real-time booking and payment. As per Île-de-France Mobilités, over 12% of Parisian taxis were electric in 2023, supported by low-emission zones and government incentives. Despite labor unrest and regulatory challenges, the market is gradually modernizing, balancing consumer demand for convenience with driver protection.

Italy Taxi Market Analysis

Italy is likely to see a steady increase in taxi digitalization over the next few years as major tourist cities like Rome and Milan adopt municipal apps to streamline service and pricing. Italy accounts for 14% of the European taxi market, marked by fragmented regulation and emerging technological adoption. With over 50,000 licensed vehicles, the sector is highly localized, with each municipality setting its own fare and licensing rules. In tourist-heavy cities like Venice and Rome, demand peaks seasonally, driving reliance on both street hails and app-based services. As per the Italian Taxi Confederation, there has been a 28% increase in app-based bookings since 2021, signaling a steady shift toward digitalization. Additionally, motorcycle taxis are gaining traction in historic centers where cars face access restrictions, indicating a move toward more agile urban solutions.

Spain Taxi Market Analysis

Spain is likely to emerge as a regional leader in sustainable taxi services over the next few years as the country utilizes its massive tourism revenue to fund the electrification of city fleets. Spain holds a 12% share of the Europe taxi market, driven by its robust tourism industry and progressive urban mobility policies. According to the Ministry of Transport, over 85 million international visitors in 2023 generated substantial demand for reliable, language-accessible transport, particularly in Barcelona, Madrid, and Malaga. The country has embraced digital transformation, with Free Now and Uber widely operational, while traditional taxi cooperatives like Radio Taxi Barcelona have launched their own apps. As per national registrations, over 18% of new taxi registrations in 2023 were electric, supported by national and regional subsidies. The integration of taxis into multimodal platforms further enhances accessibility, positioning Spain as a forward-looking player in sustainable urban mobility.

COMPETITIVE LANDSCAPE

The competition in the European taxi market is defined by a complex interplay between legacy taxi operators, global ride-hailing giants, and regional mobility platforms navigating divergent regulatory environments. While traditional taxis retain trust through licensing and safety standards, digital platforms dominate through superior user experience and scalability. The market is highly fragmented, with national and municipal regulations shaping service models, pricing, and vehicle standards. Incumbents are modernizing through app integration, while tech-driven entrants face pushback over labor practices and market disruption. Electrification and multimodal integration are emerging as key differentiators. Success increasingly depends on balancing innovation with compliance, sustainability, and equitable treatment of drivers, creating a dynamic, high-stakes environment where adaptability determines long-term viability across diverse urban ecosystems.

KEY MARKET PLAYERS

A few of the market players in the European taxi market include

- Uber

- FreeNow

- Hopp

- Bolt Technology OÜ

- Ola

- Gett,

- Addison Lee

- London Lady Chauffeurs

- Bolt

- iTaxi

- Helbiz

- YandexTaxi

- Taxi Polska

- MiniTaxi

- MOIA (a subsidiary of Volkswagen)

- BerlKönig

Top Players In The Market

- Uber has redefined urban mobility across Europe by establishing a dominant digital infrastructure that connects millions of riders with drivers through its real-time app-based platform. The company operates in over 150 cities across the region, offering services ranging from standard ride-hailing (UberX) to premium (Uber Comfort) and shared options (Uber Pool). In recent years, Uber has strengthened its integration with public transit by incorporating metro and bus schedules into its app in cities like Berlin and Madrid, enhancing multimodal journey planning. It has also accelerated its transition to zero-emission transport, committing to make 100% of rides on its platform in European cities electric by 2030. To support this, Uber launched the Green Future initiative, partnering with leasing firms to offer discounted EVs to drivers. Additionally, the acquisition of micromobility provider Lime’s European operations in select markets has expanded its urban mobility ecosystem, reinforcing its position as a comprehensive mobility platform.

- Bolt has emerged as a major competitor in the European taxi and ride-hailing market by focusing on affordability, driver-centric policies, and localized market penetration. Originating in Estonia, the company has expanded into over 45 European cities, including Paris, Rome, and Istanbul, offering competitive commission rates that attract independent drivers. Bolt has differentiated itself by introducing flat-fee pricing models in several markets, reducing fare volatility during peak hours and increasing rider predictability. The company launched Bolt Drive, a car rental service for drivers, in partnership with Europcar and Alphabet, improving fleet accessibility. In 2023, Bolt introduced Bolt Food and Bolt Courier, creating a diversified urban logistics ecosystem that increases driver utilization between rides. Furthermore, Bolt has invested in data privacy and local compliance, hosting its European user data within the EU to align with GDPR standards, thereby building trust among both drivers and passengers in a highly regulated environment.

- Free Now, a joint venture between BMW and SIXT, operates as a leading multimodal mobility platform across Europe, integrating licensed taxis with ride-hailing and micro-mobility services. Active in over 100 cities, including Hamburg, Lisbon, and Warsaw, Free Now enables users to book traditional taxis via app, bridging the gap between regulated operators and digital convenience. The platform has strengthened relationships with licensed taxi drivers by offering transparent pricing and lower commission rates compared to global platforms. In 2022, Free Now expanded its service portfolio by integrating e-scooters and e-bikes from providers like TIER and Lime in select cities, positioning itself as a full-spectrum urban mobility solution. The company has also partnered with municipal transport authorities in Munich and Barcelona to embed taxi services into official public transit apps. By emphasizing compliance, driver support, and sustainability, Free Now has become a trusted intermediary between traditional taxi networks and modern digital expectations.

Top Strategies Used By Key Market Participants

Key players in the Europe Taxi Market are leveraging strategies such as platform digitization, integration with multimodal transport ecosystems, electrification of fleets, competitive pricing models, and strategic partnerships with municipal authorities and vehicle leasing companies. Companies are enhancing user experience through real-time tracking, cashless payments, and dynamic routing algorithms. Emphasis is placed on driver retention via reduced commission structures and access to affordable electric vehicles. Expansion into adjacent services like food delivery and micromobility increases driver utilization and revenue streams. Additionally, compliance with local regulations and data protection laws strengthens market legitimacy, while sustainability commitments align with EU environmental directives, ensuring long-term operational resilience and consumer trust in an evolving regulatory landscape.

MARKET SEGMENTATION

This research report on the European taxi market has been segmented and sub-segmented into the following categories.

By Service Type

- Ride-hailing

- Ridesharing

By Booking Type

- Online

- Offline

By Vehicle Type

- Motorcycles

- Cars

- Others

By Country

- UK

- Russia

- Germany

- Italy

- France

- Spain

- Sweden

- Denmark

- Poland

- Switzerland

- Netherlands

- Rest of Europe

Frequently Asked Questions

What is the Europe taxi market?

The Europe taxi market includes traditional taxi services, ride-hailing apps, and private hire vehicles operating across major European cities to provide paid passenger transport services.

Why is the Europe taxi market important?

The market supports urban mobility, tourism, commuters, airport transfers, and last-mile transportation, contributing to public transport ecosystems and economic activity in cities.

What are the key segments of the taxi market in Europe?

Key segments include traditional taxi services, app-based ride-hailing, premium/black-car services, and wheelchair-accessible or special-needs taxis.

What drives growth in the Europe taxi market?

Growth is driven by urbanization, digital ride-hailing adoption, tourism recovery, integration with public transport, and demand for flexible mobility options.

How do ride-hailing apps impact the Europe taxi market?

Ride-hailing platforms improve booking convenience, pricing transparency, cashless payments, route optimization, and customer experience, increasing overall market usage.

What challenges does the Europe taxi market face?

Challenges include regulatory compliance differences, competition from ride-hailing and micromobility, fuel cost volatility, driver shortages, and sustainability pressures.

How do regulations influence the taxi market?

EU and national regulations govern driver licensing, safety standards, fare controls, digital dispatching rules, and emissions limits, shaping how services operate in each country.

What trends are shaping the Europe taxi market?

Key trends include electrification of fleets, app-based dispatching, contactless payments, dynamic pricing, shared rides, and integration with smart city mobility platforms.

What role does sustainability play in the taxi market?

Sustainability initiatives push for electric and hybrid taxis, lower emissions zones, green certifications, and subsidies for cleaner vehicles, aligning with climate goals.

Who are major players in the Europe taxi and ride-hailing space?

Major players include local taxi operators, global ride-hailing apps, and regional mobility platforms that offer booking, payment, and fleet management solutions.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com