Europe Termite Control Market Size, Share, Growth, Trends, And Forecast Research Report, Segmented By Type, Control Method, Application And By Region (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic & Rest of EU), Industry Analysis Forecast From (2025 to 2033)

Europe Termite Control Market Size

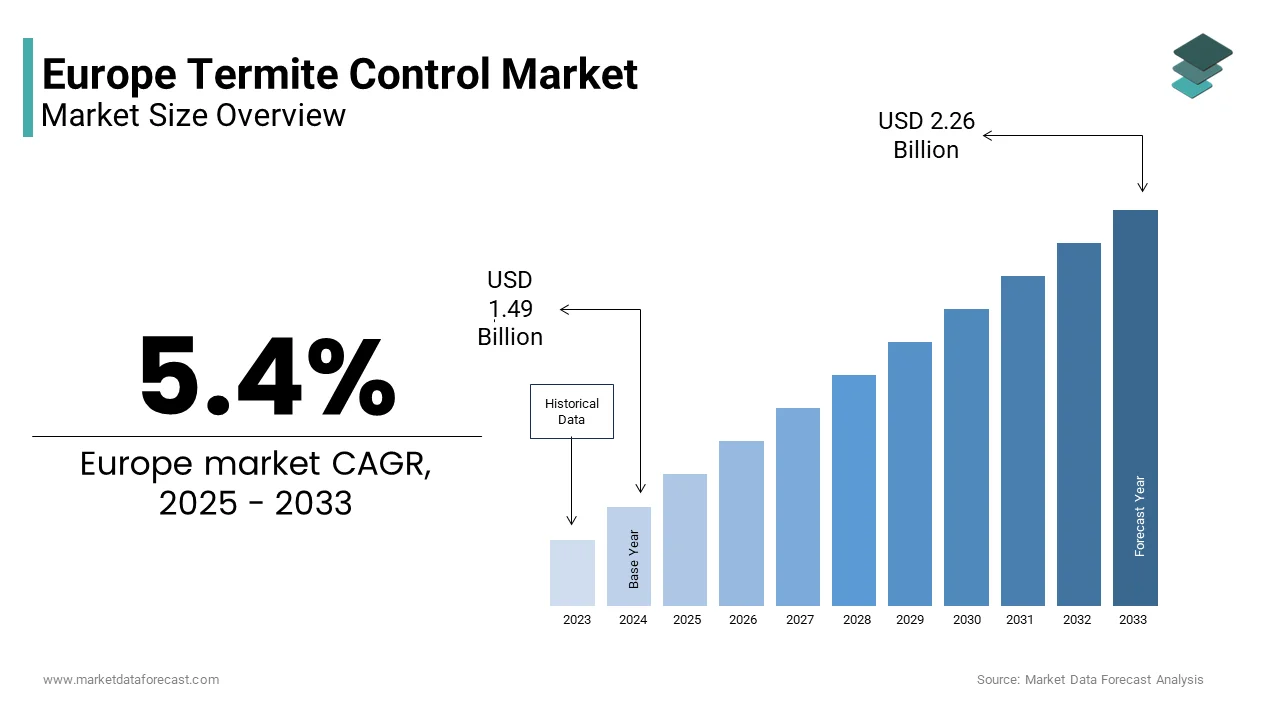

Europe termite control market was valued at USD 1.41 billion in 2024 and is anticipated to reach USD 1.49 billion in 2025 from USD 2.26 billion by 2033, growing at a CAGR of 5.4%from 2025 to 2033. Termites are damaging to humans, livestock, and the environment. Hence, various preventive and control measures to control the proliferation of termites have been driving the growth of this market globally.

The termite control is a range of preventive and remedial strategies designed to detect, manage, and eradicate subterranean and drywood termite infestations in residential, commercial, and heritage structures. Termite control methods include chemical soil treatment, ts baiting systems, physical barriers, and non-chemical interventions like heat or microwave treatments. According to the Joint Research Centre of the European Commission, many buildings across the EU are estimated to be at moderate to high risk of termite infestation, with urban centers in Mediterranean countries showing the highest vulnerability. As per the European Environment Agency, average annual temperatures in southern Europe have risen since 1990, creating more hospitable conditions for termite colony establishment and survival.

MARKET DRIVERS

Expansion of Termite Habitats Due to Climate Change and Urbanization

The rising temperatures and changing precipitation patterns linked to climate change are enabling termites to establish colonies in regions previously considered inhospitable. The expansion of termite habitats due to climate change and urbanization is are major factor propelling the growth of the Europe termite control market. According to the European Environment Agency, the number of days per year with temperatures above 25 degrees Celsius in southern Europe increased by 28% between 1990 and 2023, significantly extending the active foraging season for subterranean termites, such as Reticulitermes lucifugus. Urban expansion into peri-urban green zones further exacerbates risk by bringing structures into closer contact with natural termite reservoirs. Similarly, in Italy, the Institute for Environmental Protection and Research documented a northward shift in termite activity over the past decade. National building codes are responding slowly. These ecological and regulatory shifts create urgent demand for proactive termite control solutions in both new builds and existing infrastructure.

Stringent Heritage Conservation Requirements in Historic Urban Centers

Europe’s dense inventory of historic buildings, where manwere y were constructed with timber frames or wooden structural elements, is highly vulnerable to termite damage, yet subject to strict conservation protocols that limit invasive chemical treatments. This factor is substantially elevating the growth of the Europe termite control market. According to Europa Nostra, many protected heritage sites across the EU contain significant wooden components at risk of biological degradation. In response, the national heritage agencies increasingly mandate non-destructive monitoring and eco-friendly remediation. The French Ministry of Culture requires integrated pest management plans for all classified monuments, with preference for baiting systems and thermal treatments that avoid structural alteration. Similarly, Italy’s Central Institute for Restoration established a national termite surveillance network in 2023 covering 250 high-value sites, including Venice and Florence, where drywood termites threaten centuries-old wooden ceilings and furnishings. The European Commission’s Horizon Europe program is to develop non-chemical termite control technologies compatible with heritage preservation standards. This regulatory and cultural imperative drives innovation in low-impact detection and eradication methods tailored to sensitive architectural contexts.

MARKET RESTRAINTS

Stringent EU Regulations on Biocidal Products Under BPR Regulation 528 2012

The European Union’s Biocidal Products Regulation imposes rigorous approval requirements for chemical termite control agents, significantly limiting the availability of active substances. According to the European Chemicals Agency, few active ingredients are currently approved for use in termite control products under Product Type 18 as of early 202,5, down from 24 in 20,15 due to environmental and toxicological concerns. The re-approval process for substances like fipronil and imidacloprid has been suspended pending further endocrine disruption assessments, creating supply uncertainties. As per the European Professional Pest Management Association, the average cost of dossier submission for a new biocide exceeds 1.5 million euros, with approval timelines often exceeding four years. These barriers disproportionately affect small pest control firms that rely on cost-effective chemical solutions. In Germany, the Federal Institute for Occupational Safety and Health reported in 2024 that pest management companies faced treatment delays due to restricted chemical access. This regulatory tightening forces a shift toward non-chemical alternatives that are often more expensive and labor-intensive, thereby constraining market responsiveness despite growing infestation risks.

Low Public Awareness and Absence of Mandatory Termite Inspection Protocols

The lack of widespread public awareness and standardized termite inspection requirements in real estate transactions or construction permitting is another attribute degrading the growth of the Europe termite control market. According to the European Confederation of Woodworking Industries, some of the EU member states mandate pre-sale termite inspections even in high-risk zones. In Spain, a 2024 survey by the National Association of Property Registrars found that few homebuyers in termite-prone regions requested pest assessments during property transfers. Similarly, in Italy, regional authorities in Lombardy and Tuscany only introduced voluntary termite monitoring programs in 2023 with limited uptake. This knowledge gap leads to delayed detection and extensive structural damage before intervention occurs. The Joint Research Centre estimates that the average time between initial infestation and detection in Europe exceeds 3.5 years compared to 12 months in countries with mandatory screening.

MARKET OPPORTUNITIES

Integration of Smart Monitoring Technologies and IoT-Based Detection Systems

The adoption of connected sensor networks and AI-powered monitoring platforms for proactive termite management is creating new opportunities for the growth of the Europe termite control market. Wireless moisture, temperature, and acoustic sensors can now detect early termite activity through subtle changes in wood integrity or microclimate conditions long before visible damage appears. According to the European Innovation Council, over 30 startups received Horizon Europe funding between 2022 and 2024 for smart pest detection technologies, including subterranean termite monitoring systems. In the Netherlands, a pilot project led by the Delft University of Technology deployed IoT-enabled bait stations in Rotterdam’s historic port district, reducing detection time from 18 months to under 6 weeks. These digital solutions align with EU priorities for smart cities and preventive building maintenance, offering scalable non-invasive alternatives that overcome chemical restrictions and support early intervention.

Development of Bio-Based and Non-Toxic Termite Control Solutions

The growing demand for environmentally sustainable pest management is accelerating R&D into bio-based termite control agents derived from fungi, bacteria, or plant extracts, which is additionally fuelling the growth othe f the Europe termite control market. According to the European Bioeconomy Forum, many research projects funded under Horizon Europe 2023 focused on microbial biopesticides targeting termite gut microbiomes or nest ecosystems. In Italy, the National Research Council successfully field tested a Metarhizium anisopliae-based formulation in 2024 that achieved 92% colony suppression in Reticulitermes nests without harming non-target organisms. Switzerland’s Agroscope Institute developed a lignin-based bait matrix that enhances fungal spore delivery, while degrading naturally in soil. These innovations respond to tightening biocide regulations and consumer preference for green building practices. The European Committee for Standardization is also drafting new certification criteria for “eco pest control” services, which will create differentiation for providers using bio-based protocols. This scientific and policy alignment opens premium service channels in both residential and heritage sectors seeking chemical-free solutions.

MARKET CHALLENGES

Fragmented Regulatory Frameworks Across EU Member States

The policies remain highly fragmented across member states, creating compliance complexity, which is one of the major challenging factors for the Europe termite control market players. While France mandates termite risk mapping and building declarations in 52 departments, Spain only requires action in 15 provinces, and Germany has no national termite legislation despite documented infestations in Baden-Württemberg and Bavaria. According to the European Professional Pest Management Association, companies operating in three or more EU countries must navigate 8 to 12 distinct regulatory regimes for product registration application protocols and service certification. In 2024, as per the European Court of Auditors, inconsistent enforcement of BPR at the national level leads to “regulatory arbitrage”, where restricted chemicals remain available in some countries. This patchwork undermines harmonized pest management strategies and complicates cross-border service delivery for multinational firms.

Limited Technical Expertise and Training in Termite Biology and Management

The shortage of pest management professionals with specialized knowledge in termite identification behavior and control, particularly outside traditional infestation zones, is also limiting the growth of the Europe termite control market. According to the European Confederation of Pest Management Associations, some certified termite specialists operate across the entire EU, with over 70% concentrated in southern France and northern Italy. In countries like the Czech Republic and Poland, where emerging infestations are now reported, local pest controllers often misidentify termite damage as fungal decay, ay delaying appropriate intervention. Training programs remain scarce and unstandardized. The European Skills Agenda for Pest Management has yet to include termite modules in its vocational curriculum.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| CAGR | 5.4% |

| Segments Covered | By Species Type, Control Method, Application & Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

| Regions Covered | U.K., Italy, Germany, France, and Spain |

| Market Leaders Profiled | BASF SE (Germany), The Dow Chemical Company (U.S.), Bayer CropScience AG (Germany), Syngenta AG (Switzerland), Sumitomo Chemical Co. (Japan), FMC Corporation (U.S.), Nufarm Limited (Australia) |

SEGMENTAL ANALYSIS

By Species Insights

The subterranean segment was the largest by accounting for a significant share of the Europe termite control market in 2024 due to their aggressive foraging behavior, widespread distribution in Mediterranean and Atlantic coastal regions, and capacity to cause rapid structural damage. These termites require contact with soil moisture and build extensive underground networks that can infiltrate buildings through foundation cracks. As per the French Ministry of Ecological Transition, reported in 2024, termite interventions in high-risk departments targeted subterranean colonies due to their colony size, es, many individuals, and ability to consume up to 5 grams of wood per day per colony. National regulations reinforce this focus. France’s 1999 Termite Law mandates soil treatment and perimeter baiting for all new constructions in infested zones. Similarly, Spain’s Technical Building Code requires continuous chemical barriers in subterranean termite areas. These ecological and regulatory factors ensure sustained demand for deep soil injection and bait station systems tailored to subterranean behavior.

The drywood termites segment is expected to witness the fastest CAGR of 9.4% from 2025 to 2033, with their silent infestation patterns expanding geographic range and threat to high-value heritage and furniture assets. Unlike subterranean species, they do not require soil contact and can establish colonies directly within structural timbers or antique wooden objects, making detection difficult until severe damage occurs. According to the European Committee for Standardization, drywood termite reports have increased by 42% across southern Europe since 2020, with new colonies documented in historic buildings in Venice, Lisbon, and Marseille. The Institute for Environmental Protection and Research in Italy confirmed in 2024 that Kalotermes flavicollis has adapted to urban microclimates with indoor humidity by enabling survival in modern apartments. Heritage institutions are responding urgently.

By Control Method Insights

The chemical control methods segment held a dominant share of the Europe termite control market due to their immediate efficacy, reliability, and integration into national building codes. Soil termiticides and bait systems containing active ingredients such as chlorantraniliprole or hexaflumuron remain the backbone of preventive and remedial programs in high-risk zones. According to the European Professional Pest Management Association, termite management plans in France, Italy, and Spain still rely on chemical soil barriers for new constructions as mandated by local regulations. The French National Agency for Housing reported in 2024 that approved termite prevention certificates for property transactions included chemical perimeter treatments. These methods persist because non-chemical alternatives often lack scalability for large structures or require repeated applications. Chemical baits also offer the advantage of colony elimination through trophallaxis, a feature unmatched by physical barriers.

The biological control methods segment is likely to witness the fastest CAGR of 11.2% during the forecast period, by tightening biocide regulations, ns, rising demand for eco-friendly solutions, and advances in microbial technology. These methods utilize entomopathogenic fungi, such as Metarhizium anisopliae or Beauveria bassiana, that infect and kill termites through natural pathways without harming non-target organisms. In 2024, the Italian National Research Council demonstrated some colony mortality in Reticulitermes nests using a Metarhizium spore formulation applied via bait stations with no adverse effects on soil microbiota. Switzerland’s Agroscope Institute developed a lignin-encapsulated fungal product that remains viable for some months in field conditions. Furthermore, the European Committee for Standardization is finalizing certification criteria for “bio pest control services”, which will enable premium pricing and public procurement preference. These scientific and policy developments position biological methods as the high-growth-growth growth sustainable alternative in sensitive environments, including school heritage sites, and organic farms.

By Application Insights

The residential segment was the largest by accounting for 58.3% of the Europe termite control market share in 2024, with the high property value,,s aging housing stock, and increasing termite activity in urban and peri-urban zones. Many residential buildings in southern Europe were constructed before modern anti-termite standards and contain vulnerable wooden beams, floors, and window frames. According to Eurostat, the EU’s residential buildings were built before 1970, with this figure in Italy and Spain. In France, the National Notaries Council reported in 2024 that termite inspection disclosures affected some of the estate transactions in high-risk departments with average remediation costs. Homeowners are increasingly proactive due to mandatory disclosure laws and insurance requirements. Spain’s General Directorate for Housing introduced a national registry in 2023 requiring all termite treatments in residential buildings to be documented and reported. These legal and financial incentives ensure consistent demand for both preventive and curative services in the residential sector.

The commercial and industrial segment is growing at the fastest CAGR of 10.1% from 2025 to 2033, driven by stringent building compliance requirements, its rising asset protection needs, and the concentration of high-value infrastructure infrastructuretermite-prone urban centers. Warehouses, shopping malls, hotels, and data centers with expansive ground contact surfaces are particularly vulnerable to subterranean termite incursions. According to the European Construction Industry Federation, new commercial projects in Mediterranean EU countries now include integrated termite management systems as part of sustainability certifications, such as BREEAM. In Italy, the Civil Protection Department mandated in 2024 that all logistics hubs in coastal regions implement continuous monitoring and baiting programs following termite damage to pharmaceutical storage facilities in Genoa. Similarly, France’s Ministry of Economy requires termite risk assessments for all public infrastructure in high-risk zones. These institutional mandates, coupled with business interruption risks, create robust demand for scalable professional termite control solutions in the commercial domain.

COUNTRY ANALYSIS

France Termite Control Market Analysis

France was the largest contributor of the Europe termite control market by capturing 28.3% of the share in 2024 due to its comprehensive legal framework long long-standing infestation history, and proactive public policy. The country enacted the pioneering 1999 Termite Law, aw which mandates municipal risk mapping, compulsory seller disclosure, and preventive treatments in designated zones. According to the French Ministry of Ecological Transition, 52 departments are officially classified as termite-infested-infested infested of the national territory, with many buildings declared infested as of 2024. The National Agency for Housing maintains a public registry of interventions and requires certified operators for all treatments. Additionally, France hosts the European Union’s reference laboratory for termite identification at the National Museum of Natural History, ensuring scientific oversight. These structures, legal and institutional mechanisms, create a mature, regulated market that sets the standard for termite management across Europe.

Spain Termite Control Market Analysis

Spain was positioned second by holding 22.3% of the Europe termite control market share in 2024, with its warm climate, extensive coastal development, and high concentration of historic urban centers vulnerable to both subterranean and drywood species. According to the Spanish Ministry of Transport, many autonomous communities have reported active termite colonies with the highest densities in Valencia, Andalusia, and Catalonia. The 2023 update to the Technical Building Code now requires continuous chemical barriers or physical termite shields in all new constructions within designated high-risk municipalities. The General Directorate for Housing also launched a national termite registry in 2023, linking treatment records to property titles to enhance real estate transparency. Furthermore, Spain’s tourism infrastructure, comprising over 200000 hotels and historic sites, is increasingly investing in preventive termite programs to protect wooden heritage assets. These regulatory and economic drivers sustain Spain’s highly active market with growing professionalization.

Italy Termite Control Market Analysis

The Italian termite control market is likely to grow steadily in the coming years, with its dense inventory of historic buildings, rising urban infestations, and recent policy advancements. According to the Italian Institute for Environmental Protection and Research, termite activity has expanded northward, with confirmed colonies now in Emilia Romagna and Tuscany beyond traditional southern hotspots. Additionally, regional governments in Lombardy and Sicily introduced mandatory pre-sale inspections for properties over 50 years old. These cultural preservation imperatives, combined with innate-driven infestation eexpaexpansionre robust and sustained demand across residential and heritage sectors.

Germany Termite Control Market Analysis

Germany's termite control market growth is likely to grow with the emerging infestations in southern states and strict chemical regulation that favors non-invasive methods. According to the German Pest Control Association, confirmed termite colonies have been documented in Baden-Württemberg, Bavaria, and Hesse, primarily linked to imported timber. The Federal Institute for Risk Assessment restricts most soil termiticides under the Biocidal Products Regulation, forcing reliance on baiting, heat treatment, and monitoring systems. In 2024, the Bavarian State Office for Health and Food Safety launched a pilot program using IoT-enabled bait stations in historic towns, such as Rothenburg ob der Tauber, to enable early detection without chemical use. Furthermore, Germany’s dense network of timber frame houses built between 1850 and 1930 creates latent vulnerability. These regulatory and architectural factors position Germany as a high-compliance market with a growing demand for innovative low-impact solutions.

The United Kingdom Termite Control Market Analysis

The United Kingdom termite control market growth is likely to be driven by its isolated but intensifying infestations and strong emphasis on building integrity in historic districts. Although termites are not native to the UK,, have many colonies, since 1994 primarily in London, Portsmouth, and Edinburgh, linked to imported tropical hardwoods. According to the UK’s Animal and Plant Health Agency, all confirmed sites are under statutory control orders requiring professional eradication and monitoring. The Royal Institution of Chartered Surveyors mandates termite risk assessment for Grade II listed buildings in affected postcodes. Additionally, the British Pest Control Association launched a national certification program for termite specialists in 2023 to address technical gaps. These targeted institutional responses ensure that, despite a limited geographic spread, the UK maintains a specialized, high-value market segment focused on precision eradication and heritage protection.

COMPETITIVE LANDSCAPE

The Europe termite control market features a competitive landscape shaped by a mix of multinational pest management corporations, specialized heritage conservation service providers, and regional operators adapting to localized infestation patterns. Competition is not primarily price-driven but centers on regulatory compliance, technical expertise, and the integration of sustainable methods that align with EU environmental standards. Leading companies differentiate through certified baiting systems, digital monitoring platforms, and non-chemical eradication techniques such as heat or microwave treatments, particularly in sensitive contexts like historic buildings. The enforcement of the Biocidal Products Regulation has reduced the availability of traditional termiticides, favoring firms with robust R&D capabilities in bio-based alternatives. Market fragmentation across member states with varying legal mandates for inspections and treatments requires tailored strategies and localized service networks. Additionally, the rising threat of drywood termites in cultural assets is driving demand for precision interventions that preserve structural integrity. This environment rewards scientific rigor, regulatory agility, ty, and deep collaboration with public and heritage stakeholders.

KEY MARKET PLAYERS

These are the market players that are dominating the Europe termite control market.

- BASF SE (Germany)

- Anticimex Group

- The Dow Chemical Company (U.S.)

- Bayer CropScience AG (Germany)

- Syngenta AG (Switzerland)

- Sumitomo Chemical Co. (Japan)

- FMC Corporation (U.S.)

- Nufarm Limited (Australia)

- United Phosphorus Limited (India)

- Rentokil Initial plc. (U.K.)

- ADAMA Agricultural Solutions Ltd. (Israel)

- Nippon Soda (Japan)

- ControlSolution plc. (U.S.)

- Ensystex (U.S.)

Top Players In The Market

- BASF SE is a global leader in pest control solutions with a significant presence in the Europe termite control market through its advanced baiting and soil treatment technologies. The company contributes to the global market by developing next-generation active ingredients that comply with stringent EU biocide regulations while maintaining high efficacy. Recently, BASF expanded its Sentricon Always Active baiting system across France, Spa, in, and Italy, integrating digital monitoring capabilities to enable remote colony tracking. It also partnered with national heritage agencies in southern Europe to deploy non-invasive termite control protocols for historic buildings. These initiatives demonstrate their strategic alignment with European regulatory standards and cultural preservation priorities while reinforcing their role as an innovator in sustainable termite management.

- Rentokil Initial is a UK-headquartered global pest control specialist with deep operational roots across Europe, offering integrated termite detection and eradication, n monitoring services. The company contributes to the global market by combining digital innovation with field expertise to deliver customized termite management plans for residential, commercial, and heritage clients. , 2024, Rentokil launched its TermiteScan AI platform in Germany and Italy, which uses thermal imaging and moisture sensors to detect early infestations without structural intrusion. It also collaborated with French municipal authorities to implement city-wide termite surveillance in high-risk departments. These actions reflect its focus on technology-enabled preventive care and public sector partnerships to address Europe’s evolving urban pest challenges.

- Anticimex Group is a Sweden-based international pest control provider with a strong footprint in southern Europe, specializing in eco-friendly and non-chemical termite solutions. The company contributes globally by advancing heat microwave and baiting technologies that align with European green building standards. Anticimex introduced its Smart Digital Monitoring System across Spain and PortPortugalfeaturing wireless bait stations and real-time alerts for termite activity. It also trained over 300 technicians in drywood termite identification and treatment in collaboration with heritage conservation bodies in Italy. These efforts underscore its commitment to sustainable innovation and capacity building in regions facing emerging infestation threats.

Top Strategies Used by the Key Market Participants

Key players in the Europe termite control market primarily focus on developing non-chemical and low-impact control solutions, achieving compliance with EU bioregulations in monitoring and AI-powered detection systems, establishing partnerships with public authorities and heritinstitutionstin,,s, and expanding technician training programs to address regional expertise gaps in termite biology and management across diverse European climates and building typologies.

MARKET SEGMENTATION

This research report on the market is segmented and sub-segmented into the following categories.

By Species Type

- Subterranean termites

- Dry wood termites

- Damp wood termites

- Others

By Control Method

- Chemical control methods

- physical and mechanical control methods

- biological control methods

- botanicals and other control methods

By Application

- commercial and industrial

- residential

- agriculture and livestock farms

- other applications

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

What is driving growth in the Europe termite control market?

Rising structural damage risks, climate change–driven termite expansion, and stricter building protection standards.

Which termite species are most common in Europe?

Subterranean termites dominate, especially in Southern and Western Europe, with increasing spread to Central regions.

Which industries use termite control services the most?

Residential housing, commercial buildings, construction, and property management firms.

What treatments are commonly used for termite control in Europe?

Soil treatments, baiting systems, wood preservatives, and integrated pest management (IPM) programs.

Why is termite activity increasing in Europe?

Warmer temperatures and higher humidity levels are expanding termite habitats northward.

Which European countries are heavily affected?

Spain, Italy, France, and Portugal show the highest infestation levels, with growing concerns in Germany and the UK.

What challenges does the termite control market face?

Strict EU chemical regulations, limited availability of approved pesticides, and high service costs.

Are eco-friendly termite solutions gaining popularity?

Yes, non-toxic baiting systems, biological controls, and green-certified products are seeing rising demand.

How do construction companies benefit from termite control?

Pre-construction treatments help prevent structural damage and reduce long-term maintenance costs.

What is the future outlook for Europe’s termite control market?

Steady growth is expected as urban development expands and climate trends increase termite risks across new regions.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com