Europe Tinned Fruits Market Size, Share, Trends & Growth Forecast Report By Product (yellow peaches, tangerine, grape), Packaging, End-User, and Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic & Rest of Europe), Industry Analysis From 2025 to 2033

Europe Tinned Fruits Market Size

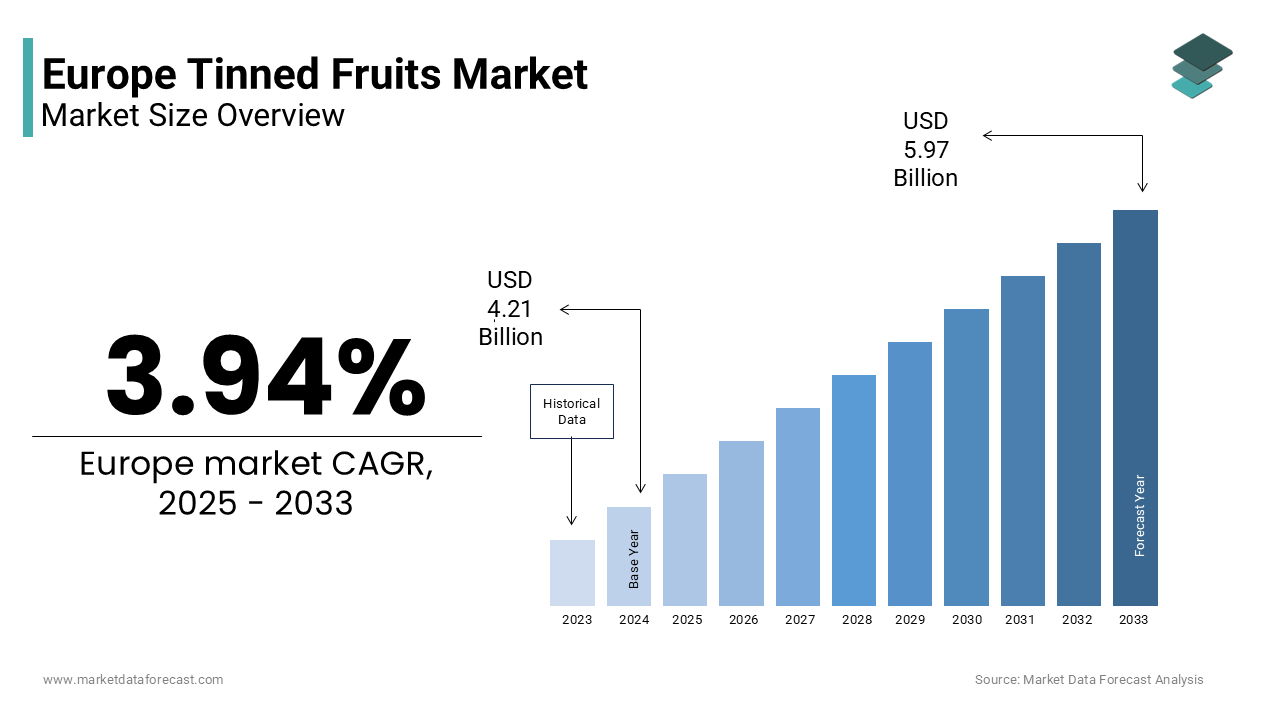

The Europe tinned fruits market size was valued at USD 4.21 billion in 2024. The European market size is estimated to be worth USD 5.97 billion by 2033 from USD 4.38 billion in 2025, growing at a CAGR of 3.94% from 2025 to 2033.

The Europe Tinned Fruits Market refers to the commercial trade and consumption of preserved fruit products that are processed, sealed in airtight metal containers, and sterilized for extended shelf life. These fruits include peaches, pears, pineapples, apricots, cherries, and mixed fruit combinations, typically packed in syrup or juice. Tinned fruits cater to both retail consumers and foodservice industries, offering convenience, nutritional value, and long-term storage benefits without refrigeration.

This market has evolved significantly due to shifting consumer preferences toward ready-to-use ingredients and growing demand from the baking, confectionery, and beverage sectors.

The UK and Germany remain dominant players in tinned fruit consumption within Western Europe, while Eastern European countries such as Poland and Romania show rising domestic production capabilities.

MARKET DRIVERS

Rising Demand for Convenience Foods Across Urban Populations

Urbanization and fast-paced lifestyles have significantly influenced dietary habits across Europe, leading to a surge in demand for ready-to-consume and easy-to-prepare food items.

Also, approximately 75% of Europe's population resides in urban areas, where time constraints and work pressures drive reliance on convenience foods. Tinned fruits, known for their long shelf life and ease of use in desserts, smoothies, and snacks, align well with this evolving consumer behavior.

In particular, younger demographics—Millennials and Gen Z—are increasingly opting for pre-processed food options that save preparation time without compromising on nutrition.

Apart from these, the rise of meal kits and online grocery platforms has further facilitated the accessibility of tinned fruits, boosting sales across the region.

Moreover, the hospitality and food service sector remains a key consumer of tinned fruits, especially in bakery and catering operations. This steady institutional demand is reinforcing growth in the Europe Tinned Fruits Market.

Expansion of Private Label Brands in Supermarkets and Discount Retailers

Private label brands have gained significant traction in the European retail landscape, particularly among budget-conscious consumers seeking quality products at competitive prices.

Supermarket chains such as Lidl, Aldi, Carrefour, and Tesco have aggressively expanded their own-brand portfolios to capture market share and improve profit margins. These retailers often source directly from manufacturers, allowing them to offer tinned fruits at lower prices compared to branded alternatives. This pricing advantage is particularly appealing in economically sensitive regions like Eastern Europe, where affordability plays a crucial role in purchase decisions.

The combination of cost efficiency, improved packaging, and consistent availability has made private label tinned fruits a preferred choice among price-sensitive shoppers, thereby fueling overall market expansion.

MARKET RESTRAINTS

Increasing Health Awareness and Shift Toward Fresh Produce Consumption

Growing health consciousness among European consumers has led to a noticeable shift away from processed foods, including tinned fruits, which are often perceived as high in added sugars and preservatives. According to a 2023 report by the European Food Safety Authority (EFSA), sugar intake among adults in the EU remains above the recommended 10% of daily caloric intake, prompting regulatory actions and public campaigns promoting fresh fruit consumption.

Also, governments in countries like France, Denmark, and Sweden have implemented front-of-pack nutrition labeling systems such as Nutri-Score, which tend to rate tinned fruits lower than fresh alternatives. This has discouraged certain consumer segments from purchasing canned fruit products regularly.

Additionally, as per the FAO, per capita fresh fruit consumption in the EU rose by 4.2% between 2020 and 2023, outpacing the growth of canned fruit consumption during the same period. The increasing popularity of organic produce and cold-pressed juices has further diverted attention from traditional tinned fruit offerings, posing a significant challenge to market growth.

Supply Chain Disruptions and Raw Material Price Volatility

The Europe Tinned Fruits Market has been significantly impacted by ongoing supply chain disruptions and fluctuating raw material costs, especially for imported fruits. Many European processors rely on external sources, particularly from South America, Africa, and Asia, for fruits such as pineapple and mango. These rising input costs have compressed profit margins for manufacturers and led to increased retail prices, dampening consumer demand.

Moreover, the war in Ukraine and sanctions against Russia disrupted trade routes and caused shortages of essential packaging materials such as tinplate and aluminum. These cumulative factors have hindered the market’s ability to maintain stable pricing and ensure continuous product availability across the region.

MARKET CHALLENGES

Growth of Plant-Based Diets and Clean Label Trends

The rising adoption of plant-based diets and clean label trends across Europe presents a compelling opportunity for the tinned fruits market. Consumers are increasingly seeking natural, minimally processed foods with transparent ingredient lists. According to a 2023 study by ProVeg International, approximately 10% of Europeans identify as vegetarian or vegan, while another 30% actively reduce animal-based food consumption. This shift has spurred demand for plant-forward ingredients, including unsweetened or naturally sweetened tinned fruits used in vegan desserts, yogurts, and protein shakes.

To meet this demand, manufacturers are reformulating products to exclude artificial additives and high-fructose corn syrup. Similarly, premium private labels from retailers like Waitrose and Marks & Spencer now highlight “clean label” certifications and reduced sugar content on packaging.

So, with growing awareness and willingness to pay a premium for healthier options, the tinned fruits market can capitalize on this trend by emphasizing transparency, sustainability, and minimal processing techniques to attract a new wave of conscious consumers.

Expansion into E-commerce and Direct-to-Consumer Sales Channels

The rapid expansion of e-commerce platforms and direct-to-consumer (D2C) models offers a promising avenue for growth in the Europe Tinned Fruits Market. This digital transformation has enabled niche and regional tinned fruit producers to reach wider audiences beyond traditional retail networks.

E-commerce allows brands to showcase product attributes such as organic certification, ethical sourcing, and exotic flavors more effectively through detailed descriptions and customer reviews. Amazon Pantry, Ocado, and Picnic have all reported increased traffic for pantry staples, including canned fruits, particularly among younger and tech-savvy consumers.

Additionally, D2C strategies enable companies to gather valuable consumer insights and tailor promotions accordingly. As per McKinsey, a significant portion of European consumers now prefer hybrid shopping models combining online and offline purchases, indicating sustained potential for digital-first approaches in the tinned fruits sector.

MARKET CHALLENGES

Regulatory Pressure and Labeling Requirements Across EU Member States

One of the most pressing challenges facing the Europe Tinned Fruits Market is the complex and varying regulatory environment across EU member states. While the European Food Safety Authority (EFSA) sets overarching food safety standards, individual countries impose additional labelling, nutritional claims, and packaging requirements that create compliance complexities for manufacturers.

For example, France mandates the Nutri-Score system, Sweden enforces strict advertising restrictions on sugary foods, and Germany requires precise origin labelling for fruits. According to a report by the European Consumer Organisation (BEUC), inconsistent labelling policies have led to confusion among consumers and increased operational costs for food processors trying to standardize packaging across borders.

Besides, the European Parliament’s push for stricter regulations on added sugars and preservatives has prompted some manufacturers to reformulate products, incurring additional R&D and production expenses. As per the Confederation of Food and Drink Industries of the EU (FoodDrinkEurope), compliance costs for small and medium-sized enterprises (SMEs) in the canned food sector rose by 14% in 2023 compared to the previous year. These regulatory hurdles pose a significant barrier to market agility and competitiveness, especially for smaller players lacking the resources to adapt swiftly.

Climate Change Impact on Domestic Fruit Production and Sourcing

Climate change is increasingly affecting fruit cultivation patterns across Europe, disrupting both domestic production and sourcing strategies for the tinned fruits market. Extreme weather events such as unseasonal frosts, prolonged droughts, and heatwaves have led to declining yields of key fruits like peaches, apricots, and cherries, which are commonly tinned. This has severely impacted orchards in Southern Europe, particularly in Italy and Spain, where peach and apricot harvests declined by 18% and 12%, respectively, as per data from the International Association for Mediterranean and Temperate Horticulture (CIHEAM).

Consequently, processors are forced to rely more heavily on imports, which increases costs and exposes the market to international trade risks. Moreover, unpredictable harvest cycles make it difficult for manufacturers to plan production schedules and maintain consistent inventory levels.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| CAGR | 3.94% |

| Segments Covered | By Product, Packaging, End-User, and Region |

| Various Analyses Covered | Global, Regional, & Country Level Analysis; Segment-Level Analysis; DROC; PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, Rest of Europe |

| Market Leaders Profiled | Coca Cola Amatil Limited, H.J. Heinz Company, ConAgra Foods Inc., Rhodes Food Group, Pinnacle Foods Inc., Del Monte, Dole Food Company, Inc., and Seneca Foods Corporation, and others |

REGIONAL ANALYSIS

Spain Tinned Fruits Market Analysis

Spain held a prominent position in the Europe Tinned Fruits Market, both as a leading producer and exporter, particularly of peaches and apricots. The country's favorable Mediterranean climate supports high-yield orchard farming, especially in regions like Extremadura and Murcia.

The Spanish tinned fruits industry benefits from well-established agro-processing clusters and strong export linkages, primarily to France, Germany, and the UK. The sector is also supported by government-backed cooperatives and EU agricultural subsidies that help maintain competitive pricing.

Domestic consumption has remained stable due to rising demand from the foodservice and bakery industries. With increasing investments in sustainable packaging and organic certifications, Spain is poised to further consolidate its leadership role in the regional tinned fruits market.

Germany Tinned Fruits Market Analysis

Germany stood as one of the largest consumers and distribution centers for tinned fruits in Europe, driven by its robust retail infrastructure and diverse culinary applications. Its central geographical location and advanced logistics network make it a key transit point for imports and exports across the continent.

The German market is characterized by high retail penetration, with major supermarket chains such as Schwarz Group (which includes Lidl and Kaufland) and Edeka offering a wide range of private label and branded tinned fruits. Moreover, the country’s thriving bakery and confectionery sectors, rely heavily on tinned fruits for ingredient supply. Rising health consciousness has also led to a shift toward low-sugar and organic variants, prompting manufacturers to reformulate products accordingly. These factors collectively reinforce Germany’s dominant position in the Europe Tinned Fruits Market.

France Tinned Fruits Market Analysis

France maintains a significant presence in the Europe Tinned Fruits Market, driven by deep-rooted culinary traditions and a preference for preserved ingredients in both household and professional kitchens. Also, French cuisine frequently incorporates tinned fruits into desserts, pastries, and sauces, fostering consistent demand across both retail and foodservice channels. Additionally, France serves as a key export destination for Spanish and Portuguese canned fruits. The country’s Nutri-Score labeling system has prompted several brands to reduce sugar content in canned offerings, aligning with evolving consumer preferences. With a mature retail landscape and growing emphasis on sustainability, France continues to play a crucial role in shaping product innovation trends within the broader European tinned fruits sector.

United Kingdom Tinned Fruits Market Analysis

The United Kingdom remains a vital player in the Europe Tinned Fruits Market, maintaining a notably market share in 2024 despite ongoing post-Brexit trade adjustments and economic pressures. Also, the convenience factor, coupled with extended shelf life, makes tinned fruits a preferred option among budget-conscious consumers. Inflationary pressures led to anincrease in private label canned fruit sales, with retailers such as Tesco, Sainsbury’s, and Asda expanding their own-brand ranges.

The hospitality sector, including cafes, pubs, and bakeries, also contributes significantly to demand. Moreover, the rise of plant-based diets and ready-to-eat meal kits has introduced new consumption avenues. Despite Brexit-related disruptions in supply chains, the UK market has demonstrated resilience, adapting through local sourcing initiatives and digital retail expansion, ensuring sustained relevance in the European context.

Italy Tinned Fruits Market Analysis

Italy plays a notable role in the Europe Tinned Fruits Market, particularly in domestic processing and niche exports. The country's strong agro-industrial base enables efficient transformation of locally grown stone fruits into canned formats.

While Italy’s domestic consumption remains moderate compared to other Western European countries, internal demand has been gradually rising. This growth is attributed to increased availability in hypermarkets and rising interest in long-lasting pantry staples.

Italy is also expanding its export footprint. With technological upgrades and strategic export diversification, Italy is positioning itself as a growing force in the regional tinned fruits landscape.

KEY MARKET PLAYERS AND COMPETITIVE LANDSCAPE

Major players in this market are Coca Cola Amatil Limited, H.J. Heinz Company, ConAgra Foods Inc., Rhodes Food Group, Pinnacle Foods Inc., Del Monte, Dole Food Company, Inc., and Seneca Foods Corporation.

The Europe Tinned Fruits Market is characterized by a mix of well-established multinational brands and strong regional players, all competing on product quality, pricing, and sustainability. Consumer preferences for convenience, health-conscious options, and environmental responsibility are shaping the competitive dynamics across the region. Major companies are continuously adapting their strategies to cater to evolving dietary habits and regulatory landscapes. Brand loyalty remains significant, but private label products offered by large supermarket chains are gaining traction due to their cost-effectiveness and accessibility. Innovation in product formulation and packaging has become a key differentiator among competitors aiming to capture market share. Additionally, digital transformation and e-commerce expansion are enabling companies to strengthen their distribution networks and engage directly with consumers. As competition intensifies, firms are also investing in sustainable sourcing and transparent labeling to align with European values and regulatory expectations. The overall market environment remains dynamic, with companies striving to balance affordability, nutrition, and environmental impact to maintain relevance and competitiveness.

TOP PLAYERS IN THE EUROPE TINNED FRUITS MARKET

One of the leading players in the Europe Tinned Fruits Market is Del Monte Foods , known for its extensive portfolio of preserved fruits and strong brand recognition across multiple European markets. The company has a long-standing presence in the region, offering a variety of tinned fruit products tailored to local tastes while maintaining high quality standards. Del Monte leverages its global supply chain and regional sourcing partnerships to ensure product consistency and availability.

Another major player is Dole Food Company , which plays a crucial role in supplying tinned tropical fruits such as pineapple and mango to European consumers. Dole's commitment to sustainable farming and food safety has positioned it as a trusted brand in both retail and foodservice channels. The company’s strategic collaborations with European retailers have enabled it to maintain a steady market presence and adapt to evolving consumer preferences.

Princes Limited , a UK-based food and beverage company, is also a key participant in the market. Known for its private label and branded canned fruit offerings, Princes serves major supermarket chains across Europe. The company focuses on innovation in packaging and nutritional transparency, aligning with regional trends toward healthier and more environmentally responsible products.

TOP STRATEGIES USED BY KEY MARKET PLAYERS

A major strategy employed by key players in the Europe Tinned Fruits Market is product innovation and reformulation to meet changing consumer health preferences. Companies are increasingly launching low-sugar, organic, and clean-label variants to align with rising demand for natural and minimally processed foods. This approach helps brands stay relevant amid growing scrutiny over sugar content in preserved fruits.

Another prominent strategy is expansion into e-commerce and direct-to-consumer platforms . Leading manufacturers are strengthening their digital presence through online retail partnerships and subscription models, allowing them to reach younger, tech-savvy consumers who prefer convenience and transparency in purchasing decisions.

Lastly, companies are focusing on sustainable sourcing and eco-friendly packaging solutions to enhance brand reputation and comply with stringent environmental regulations in Europe. By adopting recyclable materials and promoting ethical supply chains, market participants aim to differentiate themselves and build long-term consumer trust.

RECENT HAPPENINGS IN THE MARKET

- In March 2024, Del Monte Foods launched a new line of organic tinned fruits across several European markets, targeting health-conscious consumers and reinforcing its brand image as a provider of premium-quality preserved produce.

- In June 2024, Dole Food Company partnered with a major German discount retailer to introduce exclusive private label canned fruit packs, enhancing its shelf presence and expanding access to budget-oriented shoppers.

- In September 2024, Princes Limited introduced recyclable steel packaging for its entire range of tinned fruits sold in the UK and Ireland, aligning with corporate sustainability goals and responding to consumer demand for greener alternatives.

- In November 2024, a leading Spanish tinned fruit processor expanded its export operations to Eastern Europe by establishing a new logistics hub in Poland, improving supply chain efficiency and market access.

- In February 2025, an Italian agro-processing firm acquired a small organic canning facility in Sicily to vertically integrate its production capabilities and meet growing demand for certified organic tinned fruits in domestic and international markets.

MARKET SEGMENTATION

This research report on the Europe tinned fruits market is segmented and sub-segmented into the following categories.

By Product

- Introduction

- Yellow Peaches

- Tangerine

- Grape

By Packaging

- Introduction

- Glass Packaging

- Metal Packing

- Others

By End-User

- Introduction

- Supermarket

- Convenience Stores

- Online Retailing

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

1. What is the projected size and growth rate of the Europe tinned fruits market?

The market is expected to grow from USD 4.38 billion in 2025 to USD 5.97 billion by 2033, at a CAGR of 3.94%.

2. What factors are driving the growth of the tinned fruits market in Europe?

Busy lifestyles, longer shelf life, and rising demand for convenient and ready-to-eat foods are driving growth.

3. Which countries are key contributors to the European tinned fruits market?

Germany, the UK, France, Italy, and Spain are among the leading markets in the region.

4. What types of fruits are commonly available in tinned form in Europe?

Yellow peaches, tangerines, pineapples, cherries, and pears are some of the most popular tinned fruits.

5. What trends are shaping consumer preferences in this market?

Consumers are leaning toward low-sugar, organic, and preservative-free tinned fruit options.

6. What are the main distribution channels for tinned fruits in Europe?

Supermarkets, convenience stores, and online retailing are the primary distribution channels.

7. What challenges does the tinned fruits market face in Europe?

Rising competition from fresh and frozen alternatives, sustainability concerns, and packaging regulations.

8. How is sustainability influencing packaging choices in this market?

There’s a growing shift toward recyclable and BPA-free metal or glass packaging to meet eco-conscious consumer demand.

9. Are there any notable innovations in the European tinned fruit industry?

Yes, innovations include resealable lids, mixed-fruit blends, and healthier syrup alternatives like fruit juice concentrates.

10. What opportunities exist for new entrants in this market?

Opportunities lie in premium offerings, organic variants, and targeting health-conscious and vegan consumer segments.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com