Europe Tombstone Market Size, Share, Trends, and Growth Analysis Report, Segmented by Application, Distribution / Sales Channel, and Country – Industry Forecast From 2026 to 2034

Europe Tombstone Market Report Summary

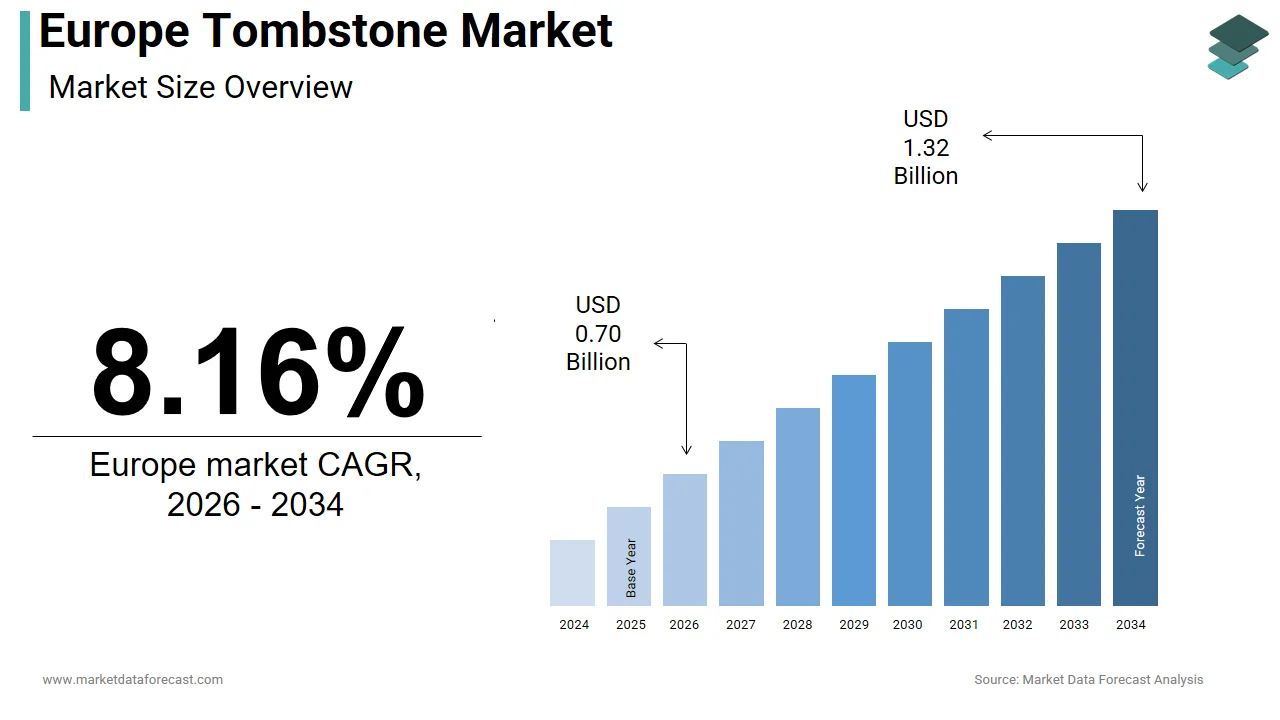

The Europe tombstone market was valued at USD 0.65 billion in 2025, is estimated to reach USD 0.70 billion in 2026, and is projected to reach USD 1.32 billion by 2034, growing at a CAGR of 8.16% from 2026 to 2034. Market growth is driven by increasing demand for personalized memorials, the cultural significance of burial practices, and the expansion of commercial cemeteries and memorial parks. Tombstones play a vital role in honoring the deceased, with growing emphasis on customization, craftsmanship, and premium materials. The rising aging population, evolving funeral traditions, and advancements in stone processing technologies are further supporting market growth across Europe.

Key Market Trends

- Increasing demand for personalized and customized memorials.

- Growing use of premium materials such as granite and marble.

- Expansion of commercial cemeteries and memorial parks.

- Rising influence of artistic and heritage-based monument designs.

- Advancements in stone engraving and fabrication technologies.

Segmental Insights

- Based on material type, the granite segment dominated the Europe tombstone market by capturing 65.8% share in 2025, driven by its durability, aesthetic appeal, and long lifespan.

- Based on design and style, the traditional monuments segment held the largest share of 62.9% in 2025, supported by strong cultural preferences and historical continuity.

- Based on application, the commercial cemeteries and memorial parks segment led the market in 2025, driven by organized burial infrastructure and increasing urbanization.

Regional Insights

The Europe tombstone market is witnessing steady growth across major countries due to cultural traditions and evolving memorial preferences.

- Germany led the regional market in 2025 with 22.7% share, supported by structured cemetery systems and strong demand for high-quality memorials.

- The United Kingdom followed with 18.4% share in 2025, driven by established funeral services and increasing demand for customized designs.

- Italy holds a significant position due to low cremation rates and strong cultural emphasis on elaborate and artistic memorials.

Competitive Landscape

The Europe tombstone market is moderately fragmented, with the presence of regional stone manufacturers and global suppliers. Market players are focusing on customization, high-quality materials, and expanding product portfolios. Technological advancements in stone processing and design innovation are shaping competitive dynamics across the market.

Prominent companies operating in the Europe tombstone market include ZhaoYang Stone, Antolini Luigi & Figli Spa, Shanghai Tianshou, Tombstones For Africa, Fujian Huian Haobo Stone Company, Ceabis, Bataung Memorial Tombstones, Kushalbagh Marbles, Levantina Group, Xiamen Stone Co., Ltd, Hebei Yiheng Stone Co., Ltd, Fujian Quanzhou Stone Group, Shandong Yujie Stone Co., Ltd, Cosentino S.A., Fujian Xiamen Ming Stone, Quanzhou Jomoo Stone, Fujian Stone Industry Co., Ltd, Xiamen Huasen Stone Co., Ltd, Shandong Yulong Stone, Xiamen City Yitong Stone Co., Ltd, Fujian Yongkang Stone Co., Ltd, Shandong Yitian Stone Co., Ltd, and Xiamen Stone Home Co., Ltd.

Europe Tombstone Market Size

The Europe tombstone market was valued at USD 0.65 billion in 2025, is estimated to reach USD 0.70 billion in 2026, and is projected to reach USD 1.32 billion by 2034, growing at a CAGR of 8.16% from 2026 to 2034.

A tombstone (or gravestone/monument) is a durable memorial marker, typically made of stone, granite, or marble, used in cemeteries to mark a grave and reflect religious, cultural, and personal identity. This market operates within a complex cultural and regulatory framework where traditional burial practices intersect with evolving demographic realities. As per Eurostat data, the European Union recorded 4.81 million deaths in 2024, significantly outnumbering live births and establishing a consistent baseline demand for permanent memorialization solutions. The median age of the EU population reached 44.7 years in 2024, reflecting a profound societal shift toward an older demographic structure that inherently drives the need for end-of-life services. Italy and Portugal reported record proportions of citizens aged over 65 in 2024, reaching 24.3% and 24.5% respectively, which underscores the intensifying pressure on funeral infrastructure. Despite the rising popularity of alternative farewell methods, assessments indicate that traditional cemeteries still encompass a vast expanse of land across Europe, serving as the essential physical foundation for the sector. The market is characterized by a strong preference for durable materials like gray and blue granite, particularly in Western and Northern regions where classical designs remain prevalent. Unlike transient consumer goods, tombstones represent a permanent cultural artifact, deeply rooted in European heritage and religious traditions that prioritize physical remembrance. The interplay between high mortality rates in an aging society and the finite nature of burial space creates a unique dynamic where the value of each memorial unit increases due to spatial constraints and material longevity requirements.

MARKET DRIVERS

Rising Geriatric Population Driving Sustained Demand

The accelerating expansion of the elderly demographic is a key force behind the volume growth within the Europe tombstone market. As life expectancy extends and birth rates decline, the absolute number of deaths annually continues to rise, creating a structural necessity for memorial products. According to Eurostat, life expectancy at birth in the EU reached 81.7 years in 2024, indicating that individuals are living longer but eventually contributing to the mortality statistics that fuel this sector. The proportion of people aged over 65 increased in 26 of the 27 EU countries in 2024, with nations like Italy and Portugal seeing nearly a quarter of their total population in this age bracket. This demographic bulge ensures a steady stream of potential customers as this large cohort naturally progresses through the end-of-life stage. Projections indicate that the EU population will peak around 2026 before beginning a gradual decline, meaning the current period represents a high-water mark for absolute death numbers driven by previous baby boomer generations. In 2025, twenty-two of the twenty-five countries with the highest senior populations globally are located in Europe, highlighting the region's unique concentration of aging citizens. The median age has climbed by 5.4 years since 2004 to reach 44.7 years, signaling a long-term trend that secures demand for decades to come. The European Union has seen its annual number of deaths consistently exceed live births for over a decade. This natural population decrease provides a predictable and robust pipeline for the funeral services and memorial monuments industry. This statistical reality means that manufacturers and retailers of tombstones face a reliable demand curve that is less susceptible to economic fluctuations and more dependent on inevitable biological outcomes. The sheer scale of the aging population ensures that even if cremation rates rise, the absolute number of traditional burials requiring headstones remains substantial in culturally conservative regions.

Cultural Preference for Traditional Burial in Specific Regions

Deeply entrenched cultural and religious traditions in Southern and Eastern Europe maintain a robust demand for physical tombstones, despite global shifts toward cremation, which fuels the growth of the Europe tombstone market. Northern European nations have widely embraced flame-based final dispositions. In contrast, countries with strong Catholic and Orthodox influences continue to favour interment and the erection of permanent stone markers. As per multiple studies, Greece maintained a cremation rate below 5% in recent years, standing in stark contrast to the over 80% rate observed in the United Kingdom. This resistance to cremation in specific locales ensures that the market for granite and marble monuments remains vibrant and essential. In Romania and Bulgaria, cremation rates have historically remained in the single digits, preserving the necessity for traditional cemetery plots and headstones. The cultural imperative to visit a physical gravesite for prayer and remembrance drives families to invest in high-quality, durable memorials that can withstand decades of exposure. Even in countries with moderate cremation rates, a significant portion of the population opts for burial to honor familial customs and religious doctrines. The enduring popularity of traditional burials in many European regions ensures that the continent remains a critical driver for the global tombstone and monument market, even as other regions like the Asia-Pacific begin to command a larger total volume of the global sector. The extensive network of established cemeteries distributed across the European continent provides the essential physical infrastructure required to sustain the long-standing cultural preference for ground-based interments. Families in these regions often view the tombstone not merely as a marker but as a sacred object integral to the mourning process, leading to higher expenditure per unit. This cultural steadfastness acts as a buffer against the rapid adoption of alternative memorialization methods seen in other parts of the world, securing a dedicated customer base for traditional stonemasons and monument suppliers.

MARKET RESTRAINTS

Severe Shortage of Available Burial Space

The critical scarcity of land designated for new cemeteries is a significant restraint on the expansion of the Europe tombstone market. Urbanization and strict zoning laws have severely limited the ability to open new burial grounds, forcing many municipalities to restrict the sale of new plots or mandate the reuse of existing ones. As per research, England is facing an acute shortage of burial space due to the inability to reuse grave sites, a practice that is more common in Continental Europe but still insufficient to meet demand. In major metropolitan areas, the cost of a burial plot has skyrocketed, sometimes exceeding the price of the tombstone itself, which discourages families from opting for traditional interment. Municipalities across Europe are attempting to secure more land for burial grounds, though these expansion projects frequently encounter significant resistance from local communities and complex regulatory requirements. The total area covered by European cemeteries is approximately 200,000 hectares, a finite resource that cannot easily be expanded in densely populated zones. This spatial constraint forces local authorities to impose stricter regulations on the size and type of monuments allowed, often limiting the market to smaller, less expensive markers. In some cases, cities have stopped selling new graves entirely, pushing consumers toward cremation or alternative burial methods that do not require a traditional headstone. The lack of available land effectively caps the volume of new tombstones that can be installed, regardless of the demand generated by mortality rates. Consequently, manufacturers face a shrinking addressable market in key urban centers where the majority of the population resides. This land crisis compels the industry to adapt by offering compact memorials or focusing on renovation services for existing graves rather than new installations.

Escalating Costs of Raw Materials and Production

Surging prices for natural stone and energy-intensive processing have emerged as a major barrier to the Europe tombstone market. As a result, these costs are hindering market growth and profitability. The tombstone industry relies heavily on granite and marble, commodities that have seen significant price inflation due to global supply chain disruptions and increased extraction costs. According to various sources, rising costs of raw materials, including granite, marble, and bronze, are driven by heightened global demand and logistical challenges. Energy prices in Europe have remained volatile, impacting the cost of cutting, polishing, and transporting heavy stone materials, which are energy-intensive processes. Funeral costs in the Netherlands jumped by roughly 40% over seven years, reaching approximately €10,000 in 2025, with monument costs being a significant component of this increase. In the United Kingdom, the average cost of a basic funeral rose to £4,285 in 2024, placing financial strain on families who may then opt for cheaper memorial alternatives. These escalating expenses force consumers to downsize their purchases, choosing smaller markers or synthetic materials instead of premium natural stone. Suppliers face squeezed margins as they struggle to pass the full extent of cost increases onto price-sensitive customers. The volatility in the global stone market makes long-term pricing strategies difficult for manufacturers, leading to uncertainty in investment and production planning. Additionally, transportation costs for importing stone from non-European quarries have risen due to fuel price fluctuations and trade tariffs. This economic pressure threatens to reduce the overall value of the market even if the volume of units sold remains stable. Families facing financial hardship may delay the purchase of a headstone or choose temporary markers, further dampening immediate market revenue.

MARKET OPPORTUNITIES

Integration of Digital Memorialization Technologies

The convergence of physical memorials with digital technology is a transformative opportunity for the Europe tombstone market. This paves the way to expand its value proposition. Modern consumers increasingly seek interactive and multimedia experiences that extend beyond the static inscription of traditional headstones. As per the CNIL 10th Innovation and Foresight Report, specific technologies are now being designed explicitly for the digital afterlife, dealing directly with death and mourning through post-mortem data management. Manufacturers can integrate QR codes, NFC chips, or augmented reality markers into tombstones, allowing visitors to access photo galleries, video tributes, and biographical stories via smartphones. The European Memory Data Space initiative emphasizes a growing pan-European focus on digitizing historical and personal records, which aligns perfectly with the concept of smart memorials. This hybrid approach appeals to younger generations who are accustomed to digital interaction and wish to preserve memories in a dynamic format. Companies that offer these tech-enabled solutions can command higher price points and differentiate themselves in a crowded marketplace. Based on the State of the Digital Decade findings, European authorities are prioritising universal access to high-speed mobile and fixed networks, ensuring that the necessary infrastructure is becoming available for visitors to engage with digital content in public and private spaces across the continent. By bridging the gap between the physical stone and the digital cloud, the industry can create recurring revenue streams through hosting services and content management subscriptions. This innovation transforms the tombstone from a one-time purchase into an ongoing service relationship with the bereaved family. It also allows for the preservation of history in a way that physical stone alone cannot achieve, adding a layer of emotional and practical value. Embracing this digital shift enables traditional stonemasons to modernize their offerings and remain relevant in a rapidly evolving technological landscape.

Growing Demand for Eco-Friendly and Sustainable Monuments

The increasing consumer consciousness regarding environmental sustainability offers a significant avenue for growth through the development of green memorial solutions and the expansion of the European tombstone market. As environmental regulations tighten and public awareness grows, there is a rising preference for tombstones made from locally sourced, ethically quarried, or recycled materials. The EU Nature Restoration Law, which came into effect in August 2024, places new emphasis on biodiversity and land restoration, influencing how quarrying operations and cemetery expansions are managed. Manufacturers who adopt sustainable quarrying practices and obtain certifications like ISO 14001 can appeal to eco-conscious buyers who want to minimize their carbon footprint. There is a burgeoning market for biodegradable urns and natural stone markers that blend seamlessly into the landscape without disrupting local ecosystems. The push for sustainable stone quarrying practices in 2025 has transformed the industry, with modern operators focusing on pollution prevention and area restoration. Families are increasingly willing to pay a premium for products that align with their values of environmental stewardship and responsible consumption. This trend also encourages the use of alternative materials such as reclaimed stone or composite materials that require less energy to produce. By positioning their products as environmentally responsible, companies can tap into a demographic that prioritizes sustainability in all purchasing decisions. Furthermore, cemeteries themselves are looking to become greener spaces, creating demand for monuments that support rather than hinder ecological goals. This shift towards sustainability not only opens new product categories but also enhances brand reputation and loyalty among forward-thinking consumers. It represents a strategic pivot that aligns the traditional tombstone industry with the broader green economy movement sweeping across Europe.

MARKET CHALLENGES

Stringent Environmental Regulations on Quarrying

The implementation of rigorous environmental laws governing stone extraction and processing acts as a major challenge for the supply chain of the Europe tombstone market. New regulations aim to protect biodiversity and reduce the ecological impact of mining activities, often resulting in reduced output and higher compliance costs. The EU Nature Restoration Law requires operators to restore disturbed areas and prevent pollution, adding layers of complexity and expense to quarrying operations. While the EU plans to loosen some rules to encourage mining, the overall regulatory environment remains strict regarding water usage, chemical handling, and land rehabilitation. Compliance with these standards necessitates significant investment in technology and processes, which smaller quarrying firms may struggle to afford. The Health and Safety Executive in the UK has noted that regulation of small stone-processing firms remains intense, limiting their ability to scale production efficiently. These constraints can lead to shortages of raw materials, causing delays in production and fulfillment of orders for tombstones. Additionally, the permitting process for new quarries or the expansion of existing ones has become lengthier and more uncertain, stifling supply growth. Operators must navigate a complex web of local, national, and EU-level regulations that can vary significantly across member states. The cost of adhering to these environmental mandates is often passed down the supply chain, inflating the final price of the monument for the consumer. This regulatory burden creates a barrier to entry for new players and limits the flexibility of established manufacturers to respond to market spikes in demand. Consequently, the industry faces a constant tension between meeting the need for natural stone and adhering to the continent's ambitious environmental goals.

High Financial Burden on Bereaved Families

The escalating total cost of funerals and memorialization imposes a severe financial strain on families, which inhibits the expansion of the Europe tombstone market. This leads to deferred purchases or the selection of inferior products. As the economic landscape in Europe remains challenging, many households find themselves unable to afford traditional high-quality tombstones amidst rising living costs. In the Netherlands, the average funeral cost surged to over €10,000 in 2025, a 40% increase from seven years prior, making comprehensive memorialization unattainable for many. Similarly, in the United Kingdom, the average basic funeral cost reached £4,285 in 2024, with additional expenses for monuments pushing the total well beyond the budget of average earners. This financial pressure forces families to make difficult choices, often opting for simpler, less durable markers or delaying the installation of a headstone indefinitely. The disparity in costs across Europe is stark, with funerals in Norway and Spain being relatively affordable while those in Belgium and Germany remain prohibitively expensive for some demographics. Economic uncertainty and inflation erode disposable income, reducing the willingness of consumers to spend on premium memorial products. Insurers and funeral planners note that cost is becoming the primary deciding factor for families, overshadowing preferences for material quality or design intricacy. This trend threatens to commoditize the market, driving a race to the bottom in terms of price and quality. Manufacturers face the challenge of maintaining profitability while offering products that fit within the tightening budgets of their clientele. The high financial barrier not only reduces the volume of sales but also shifts the market mix toward lower-margin items, impacting the overall health and innovation capacity of the industry.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Application, Distribution / Sales Channel, and Country. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, and the Rest of Europe. |

| Market Leaders Profiled | ZhaoYang Stone, Antolini Luigi & Figli Spa, Shanghai Tianshou, Tombstones For Africa, Fujian Huian Haobo Stone Company, Ceabis, Bataung Memorial Tombstones, Kushalbagh Marbles, Levantina Group, Xiamen Stone Co., Ltd., Hebei Yiheng Stone Co., Ltd., Fujian Quanzhou Stone Group, Shandong Yujie Stone Co., Ltd., Cosentino S.A., Fujian Xiamen Ming Stone, Quanzhou Jomoo Stone, Fujian Stone Industry Co., Ltd., Xiamen Huasen Stone Co., Ltd., Shandong Yulong Stone, Xiamen City Yitong Stone Co., Ltd., Fujian Yongkang Stone Co., Ltd., Shandong Yitian Stone Co., Ltd., Xiamen Stone Home Co., Ltd., and Others. |

SEGMENTAL ANALYSIS

By Material Type Insights

The granite segment was the largest in the Europe tombstone market and occupied a 65.8% share in 2025. This dominance of the segment is primarily driven by the material's superior durability and resistance to harsh European weather conditions, which range from the freezing winters of Scandinavia to the humid climates of Southern Europe. Apart from these, a major factor propelling granite to the forefront of the market is its exceptional ability to withstand environmental degradation over centuries. Unlike softer stones, granite possesses a high density and low porosity, making it impervious to acid rain and freeze-thaw cycles that frequently damage other materials. In regions like the United Kingdom and Germany, where rainfall is abundant and temperatures fluctuate widely, families prioritize longevity, leading to a preference for gray and blue granite varieties. The long-term value proposition resonates deeply with consumers who view tombstones as permanent legacy markers. Furthermore, the availability of granite quarries within Europe, particularly in Portugal and Spain, reduces transportation costs and carbon footprints, aligning with local sourcing trends. The material's versatility in polishing allows for a wide array of finishes, from matte to high gloss, catering to diverse aesthetic preferences while maintaining structural integrity against the elements. A further key driver for the dominance of granite is its relative cost-effectiveness compared to premium marble and bronze, coupled with a robust and stable supply chain. While high-end marble can be prohibitively expensive due to scarcity and difficult extraction processes, granite remains abundantly available across the European continent and through established import routes from India and China. In economically uncertain times, families often seek dignified yet affordable memorial solutions, and granite offers the best balance between quality and price. The processing technology for granite has also advanced significantly, with automated cutting and polishing machines reducing labor costs and production time. This efficiency allows suppliers to offer customized designs at price points accessible to the middle class. Additionally, the consistent supply of granite prevents the market volatility seen in rarer stone types, providing stability for funeral directors and monument retailers when planning inventory. The widespread acceptance of granite in both religious and secular cemeteries further solidifies its market position, as it meets the regulatory requirements of nearly all European municipalities regarding material standards for public burial grounds.

The marble segment is predicted to witness the highest CAGR of 5.8% during the forecast period due to a resurgence in appreciation for classical aesthetics and the increasing demand for personalized, high-end memorial art in affluent European regions. In addition, the rapid expansion of this segment is largely attributed to a renewed cultural interest in classical artistry and the timeless elegance that only marble can provide. Historically associated with Renaissance sculpture and ancient monuments, marble carries a prestige that appeals to families seeking to honor their loved ones with a piece of art rather than a simple marker. Wealthy demographics in these regions are increasingly commissioning bespoke statues and intricate relief carvings that showcase the translucency and veining unique to marble. The material's softness allows stonemasons to execute highly detailed designs that are impossible to achieve with harder granite, catering to a niche but growing market for customization. The trend is further supported by the restoration of historic cemeteries, where matching new markers to existing marble structures is often a regulatory or aesthetic requirement. As the population of high-net-worth individuals in Europe continues to grow, the desire for distinctive and artistically significant memorials drives the preferential selection of marble despite its higher maintenance needs. An additional factor enabling the faster growth of the marble segment is the development of advanced protective coatings and maintenance technologies that mitigate the material's traditional vulnerabilities. Historically, the susceptibility of marble to acid rain and staining limited its use in outdoor environments, but recent innovations have dramatically extended its lifespan. These advancements have reassured consumers and cemetery authorities that marble monuments can endure modern environmental challenges without rapid deterioration. The availability of specialized cleaning services that use laser technology to remove grime without damaging the stone has also made marble a more practical choice for long-term memorials. Furthermore, the integration of these maintenance protocols into warranty packages offered by monument suppliers provides additional peace of mind to buyers. This technological evolution transforms marble from a high-maintenance liability into a viable, durable option, unlocking its potential in markets previously dominated solely by granite and driving its accelerated adoption across the continent.

By Design and Style Insights

In 2025, the traditional monuments segment held the majority share of 62.9% of the Europe tombstone market. This prevalence of these monuments is driven by deep-seated religious traditions and the conservative nature of burial practices in many European communities. The overwhelming command of traditional designs is fundamentally rooted in the strong influence of Christianity, particularly Catholicism and Orthodoxy, across large parts of Europe. These faiths often prescribe specific symbolic forms for memorials, such as the cross for Christians or specific iconography for Orthodox believers, which dictate the design choices of the bereaved. The cultural expectation to conform to established norms of remembrance ensures that families opt for familiar and respectful designs that honor their ancestors in a recognized manner. In rural areas and smaller towns, where community ties and traditional values are strongest, deviation from standard monument styles is often discouraged. Furthermore, many historic cemeteries have strict guidelines mandating that new markers blend seamlessly with the existing architectural style, effectively enforcing the use of traditional designs. This regulatory and social pressure creates a stable and massive market for classic monuments, as families prioritize conformity and respect for tradition over individual expression in the context of death and mourning. Beyond religious mandates, the preference for traditional monuments is driven by a widespread perception that classic designs convey a greater sense of dignity, solemnity, and timelessness. Families often view upright headstones and elaborate traditional structures as a more respectful tribute to the deceased compared to flat markers or abstract modern art. The enduring popularity of materials like polished granite in traditional cuts reinforces this perception of permanence and seriousness. In many European cultures, the tombstone serves as a focal point for family gatherings and religious observances, and the familiar form of a traditional monument facilitates these rituals. Sources reveal that even among younger generations who might otherwise prefer modern aesthetics, there is a tendency to revert to traditional styles when purchasing for parents or grandparents to honor their wishes and societal expectations. This intergenerational dynamic ensures a continuous demand for classic designs. Additionally, the resale value and acceptance of traditional monuments in cemetery plots are generally higher, as they are less likely to face objections from cemetery boards or neighbors, making them a safer and more pragmatic choice for consumers seeking a lasting and dignified memorial.

The Modern and Custom designs segment is estimated to register the fastest CAGR of 6.5% between 2026 and 2034, owing to shifting societal attitudes toward personalization and the desire of younger generations to celebrate the unique life and personality of the deceased. Also, the swift ascent of modern and custom designs is mainly fueled by a paradigm shift in how society approaches death, moving from a focus on uniform mourning to the celebration of individual life stories. Younger demographics, including Millennials and Gen X, are increasingly rejecting standardized templates in favor of unique memorials that reflect the hobbies, passions, and personalities of their loved ones. The trend is evident in the rising popularity of monuments shaped like musical instruments, sports equipment, or abstract art pieces that tell a specific narrative. The decline of rigid religious adherence in Northern and Western Europe has further liberated families to explore creative expressions of grief. Social media also plays a role, as families share images of unique memorials, inspiring others to seek distinctive tributes. This desire for differentiation drives the demand for custom work, pushing the market away from mass-produced traditional stones toward artisan-crafted modern pieces that serve as personalized legacies rather than generic markers. The acceleration of the modern design segment is heavily supported by the widespread adoption of advanced manufacturing technologies that make complex customization affordable and accessible. Innovations such as computer numerical control (CNC) carving, high-resolution laser etching, and 3D printing have revolutionized the stonemasonry industry, allowing for the precise execution of intricate designs that were previously too costly or technically difficult to produce. These technologies have reduced production lead times, making it feasible for manufacturers to handle a high volume of unique orders without compromising efficiency. The ability to etch high-quality photographs and detailed portraits onto stone surfaces has become a standard offering, appealing to those who wish to keep the visual memory of the deceased alive. Furthermore, the precision of modern machinery allows for the creation of sleek, minimalist designs that align with contemporary architectural trends in urban cemeteries. This technological empowerment lowers the barrier to entry for custom designs, enabling a broader segment of the population to afford personalized memorials and driving the rapid expansion of this market sector.

By Application Insights

The commercial cemeteries and memorial parks segment dominated the Europe tombstone market and accounted for a substantial share in 2025. Factors such as the centralized management of burial grounds and the high volume of interments occurring in public and private municipal facilities are attributed to the supremacy of this segment. The prominence of commercial cemeteries is also supported by the centralized administration of burial spaces, which enforces strict regulations on monument types, sizes, and materials to ensure uniformity and safety. Municipalities and private cemetery operators maintain comprehensive lists of approved vendors and design standards that families must adhere to, channeling the vast majority of tombstone purchases through these official channels. These institutions often have exclusive contracts with specific monument suppliers or maintain in-house stonemasonry services, consolidating market share within the commercial sector. The need for long-term maintenance and the preservation of the cemetery's aesthetic integrity necessitates rigorous oversight, which naturally favors the commercial model over scattered private graves. In densely populated countries like the Netherlands and Germany, land scarcity has led to the development of large-scale memorial parks that maximize space efficiency, further concentrating demand. Regulatory frameworks also mandate that monuments in commercial cemeteries meet specific stability and safety criteria to prevent accidents, a requirement that professional commercial operators are best equipped to manage. This structured environment ensures a steady and predictable flow of business for suppliers operating within the commercial cemetery network, solidifying its position as the dominant application segment. The sheer volume of annual interments handled by commercial cemeteries and memorial parks is the primary quantitative driver of their market dominance. With Europe recording millions of deaths annually, the infrastructure of public and private cemeteries is the only capable system to manage this scale of final disposition. These facilities possess the necessary land, logistical support, and administrative capacity to handle thousands of burials each year, a feat that private landowners cannot match. The concentration of population in urban areas means that most families rely on local municipal cemeteries or large private memorial parks for burial services, as private land suitable for graves is scarce or legally restricted. The development of "garden cemeteries" and large-scale memorial parks in major cities has further increased the capacity and appeal of commercial applications, attracting families with their serene environments and professional upkeep. Additionally, the trend toward pre-planning funerals often involves purchasing plots and monuments directly through cemetery administrations, locking in future sales for the commercial segment. The economies of scale achieved by these large operations allow them to offer competitive pricing and comprehensive service packages, reinforcing their status as the primary destination for tombstone procurement across the continent.

The home use and private graves segment is anticipated to witness the fastest CAGR of 4.2% over the forecast period. A niche but expanding desire for intimate and family-managed memorials on private property, particularly in rural and semi-rural regions, is the factor behind the rapid expansion of this segment. The accelerating growth in private graves is propelled by a growing desire among certain demographics for intimate, family-controlled memorialization that avoids the formal and sometimes impersonal atmosphere of public cemeteries. Families in rural areas or those with substantial private land holdings increasingly prefer to bury their loved ones on their own property to maintain a constant physical connection and oversee the care of the grave personally. According to research, the concept of the "family plot" is seeing a revival as people seek to reclaim agency over the death care process and create a secluded sanctuary for remembrance. This trend is particularly noticeable in countries with extensive rural landscapes like Sweden, Finland, and parts of France, where land ownership laws permit private burials under specific conditions. The emotional benefit of having a loved one resting in a familiar, private setting appeals to those who find commercial cemeteries too crowded or restrictive. Furthermore, the privacy afforded by home graves allows for more flexible and personalized mourning practices, free from the visiting hours and rules imposed by public institutions. This longing for closeness and autonomy drives the demand for high-quality tombstones suitable for private landscapes, spurring growth in this specialized segment. A further key factor enabling the rapid expansion of the private graves segment is the gradual relaxation of regulations regarding home burials in several European jurisdictions, coupled with the availability of suitable rural land. While strict laws historically confined burials to public cemeteries, some regions have amended legislation to allow private interments provided that environmental and health standards are met. The abundance of private agricultural and residential land in less densely populated areas provides the physical space necessary for this practice to flourish. Environmental impact assessments have shown that small-scale private burials, when managed correctly, pose minimal risk to groundwater or public health, reassuring regulators and facilitating policy changes. This regulatory shift opens up a new market for monument suppliers who can cater to the specific needs of private landowners, such as designing markers that blend with natural surroundings or meet specific zoning aesthetic codes. The lower cost associated with avoiding cemetery plot fees also makes private graves an attractive financial alternative for some families, further stimulating demand. As awareness of these legal possibilities spreads, more families are exploring the option of private memorialization, driving the segment's faster growth rate relative to the saturated commercial market.

COUNTRY LEVEL ANALYSIS

Germany Tombstone Market Analysis

Germany led the Europe tombstones market and captured a 22.7% share in 2025. The demand for tombstones in Germany is driven by its large population and the legal requirement for grave upkeep. Its market shows a highly regulated industry and a strong culture of grave maintenance. In Germany, the concept of "Grabpflege" or grave care is deeply embedded in the culture, with families legally obligated to maintain the appearance of the grave site for a specific lease period, usually ranging from 20 to 30 years. This regulation ensures a consistent demand for high-quality, durable tombstones and regular landscaping services. The German market is distinguished by its preference for polished granite and strict aesthetic guidelines enforced by local cemetery administrations, which often dictate the color, size, and font of inscriptions to maintain uniformity. The presence of a well-established network of stonemasons, known as "Steinmetz," who undergo rigorous apprenticeship training, guarantees a high standard of craftsmanship. Furthermore, the aging population in Germany, with a median age exceeding 45 years, provides a steady pipeline of demand. The market is also seeing a shift toward eco-friendly materials and simpler designs as environmental consciousness grows, but the core demand remains anchored in tradition and regulatory compliance, making Germany a stable and dominant force in the regional landscape.

United Kingdom Tombstone Market Analysis

The United Kingdom was the second-largest market in the Europe tombstone market and accounted for a 18.4% share in 2025. However, it faces unique challenges due to severe space constraints and the highest cremation rate on the continent. Despite a notable portion of deaths resulting in cremation, the demand for memorial markers remains significant, particularly for cremation gardens and niche memorials within churchyards and municipal cemeteries. According to sources, the UK faces a critical shortage of burial space, with some London cemeteries projected to run out of room within the next decade, driving up the cost of plots and influencing the size and type of monuments installed. This scarcity has led to a trend toward smaller, flat markers or plaques rather than large upright headstones to maximize space efficiency. The market is also influenced by the Church of England's regulations, which govern a vast number of burial grounds and enforce strict rules on design and material. However, there is a growing segment for personalized and artistic memorials, especially in secular memorial parks where regulations are more flexible. Despite these pressures, the cultural importance of remembrance ensures a steady market, with a notable increase in the installation of memorial benches and tree plaques as alternatives to traditional stone, reflecting a pragmatic adaptation to spatial limitations.

Italy Tombstone Market Analysis

Italy is another major player in the European tombstone market due to an exceptionally low cremation rate and a profound cultural devotion to elaborate, artistic memorials. Unlike its Northern European counterparts, Italy maintains a cremation rate of below 30%, meaning the vast majority of the population still opts for traditional burial, sustaining high demand for full-sized tombstones. The Italian market is unique in its appreciation for sculpture and artistic detail, with many families viewing the tombstone as a masterpiece of stone carving rather than a mere marker. This cultural nuance supports a thriving local industry of skilled artisans, particularly in regions like Tuscany and Carrara, famous for their marble quarries. The All Saints' Day tradition, where families gather to clean and decorate graves with flowers and candles, reinforces the ongoing investment in grave maintenance and monument quality. Although economic fluctuations have impacted discretionary spending, the cultural imperative to honor the dead with dignity and beauty remains a powerful driver. The market is also seeing a modernization trend in urban areas, with sleeker designs gaining traction, but the core demand remains firmly rooted in traditional, high-craftsmanship marble and granite structures that reflect Italy's rich artistic heritage.

France Tombstone Market Analysis

France grew steadily in the Europe tombstone market owing to a balanced mix of traditional burial practices and a growing acceptance of cremation, alongside strict secular regulations. The French market is heavily influenced by the concept of "concessions," where families purchase the right to use a burial plot for a renewable period, typically 30, 50, or 99 years, which dictates the longevity and quality of the tombstone required. The French government enforces rigorous standards on cemetery management and monument safety, ensuring that all tombstones meet specific structural integrity criteria to prevent accidents in public spaces. There is a distinct regional variation in preferences, with the south of France showing a penchant for lighter colored stones and more ornate designs, while the north favors darker granites and sober styles. The market is also driven by the "Toussaint" holiday, similar to Italy, which sees a nationwide surge in grave visits and maintenance activities. Recent trends indicate a growing interest in eco-friendly burials and natural stone options that blend with the landscape, aligning with France's strong environmental policies. The presence of numerous small, independent stonemasons across the countryside ensures a decentralized but resilient supply chain that caters to local tastes and traditions, keeping the market vibrant and diverse.

Spain Tombstone Market Analysis

Spain is likely to expand significantly in the European market from 2026 to 2034 due to deep-rooted Catholic traditions, a rapidly aging population, and a cultural emphasis on family pantheons and communal graves. The Spanish market is unique in its prevalence of "panteones familiares" or large family mausoleums often elaborate structures housing multiple generations, thereby driving demand for significant quantities of stone and high-value custom work. While cremation is gaining ground, particularly in urban centers like Madrid and Barcelona, traditional burial remains dominant in many regions, supported by the strong influence of the Catholic Church. The Spanish culture places a high value on the visual presentation of graves, with families frequently investing in fresh flowers, cleaning, and monument upgrades, creating a recurring revenue stream for the industry. The market is also characterized by a preference for light-colored granites and marbles that reflect the Mediterranean sunlight and aesthetic. Economic recovery in Spain has bolstered consumer confidence, allowing families to spend more on premium memorial options after years of austerity. Furthermore, the tourism-driven economy in coastal regions has led to the development of modern, park-like cemeteries that cater to both locals and expatriates, introducing new design trends and expanding the market scope beyond traditional norms.

COMPETITIVE LANDSCAPE

The competition in the Europe tombstone market is characterized by a fragmented landscape comprising numerous small local stonemasons alongside a few large multinational corporations. This mix creates a dynamic environment where traditional craftsmanship competes directly with industrial-scale production efficiency. Local artisans often dominate specific regions by leveraging deep community ties and offering bespoke services that large firms cannot easily replicate. Conversely, major players utilize their extensive distribution networks and economies of scale to offer competitive pricing and standardized quality across multiple countries. The rivalry intensifies as companies strive to differentiate themselves through unique design offerings, superior material durability, and exceptional customer service. Price competition remains fierce, particularly in economically sensitive segments, prompting many firms to innovate with cost-effective materials or flexible payment plans. Additionally, the push toward digitalization and eco-friendly practices has become a new battleground where companies vie for leadership in sustainability and technological adoption. This multifaceted competitive pressure drives continuous improvement in product quality and operational efficiency throughout the sector.

KEY MARKET PLAYERS

The leading companies operating in the Europe tombstone market include:

- ZhaoYang Stone

- Antolini Luigi & Figli S.P.A.

- Shanghai Tianshou

- Tombstones For Africa

- Fujian Huian Haobo Stone Company

- Ceabis

- Bataung Memorial Tombstones

- Kushalbagh Marbles

- Levantina Group

- Xiamen Stone Co., Ltd

- Hebei Yiheng Stone Co., Ltd

- Fujian Quanzhou Stone Group

- Shandong Yujie Stone Co., Ltd

- Cosentino S.A.

- Fujian Xiamen Ming Stone

- Quanzhou Jomoo Stone

- Fujian Stone Industry Co., Ltd

- Xiamen Huasen Stone Co., Ltd

- Shandong Yulong Stone

- Xiamen City Yitong Stone Co., Ltd

- Fujian Yongkang Stone Co., Ltd

- Shandong Yitian Stone Co., Ltd

- Xiamen Stone Home Co., Ltd

TOP PLAYERS IN THE MARKET

- Antolini Luigi & Figli Spa stands as a preeminent force in the European natural stone sector with a profound impact on the global tombstone industry. Headquartered in Italy, this company leverages centuries of artisanal heritage to produce high-end marble and granite monuments that define luxury memorialization worldwide. Their contribution to the global market involves exporting exquisite Italian stone designs to over fifty countries while setting benchmarks for quality and artistic craftsmanship. Recently, the company has intensified its focus on digital integration by implementing advanced computer numerical control cutting technologies to enhance precision in custom monument production. They have also expanded their sustainable quarrying initiatives to align with stringent European environmental regulations, ensuring long-term resource availability. By participating in major international trade fairs and collaborating with renowned architects, Antolini continues to reinforce its reputation as a leader in premium memorial solutions. Their strategic investments in logistics infrastructure have further streamlined global distribution, allowing them to maintain a dominant presence in both traditional and emerging markets.

- Levantina Group operates as a colossal entity in the natural stone industry originating from Spain and exerting significant influence over the Europe tombstone market through its vast quarry holdings and processing capabilities. The company contributes extensively to the global landscape by supplying diverse granite and marble varieties that serve as primary materials for monuments across continents. Their recent actions to strengthen market position include the acquisition of strategic quarry assets in key regions to secure raw material supply chains against global volatility. Levantina has also launched innovative eco-friendly product lines that utilize recycled stone materials, appealing to the growing segment of environmentally conscious consumers in Europe. They have invested heavily in automated polishing facilities to increase production efficiency and reduce labor costs while maintaining superior finish quality. Furthermore, the group has developed proprietary digital platforms that allow customers to visualize custom tombstone designs in real time, enhancing the buyer experience. These technological and operational advancements ensure Levantina remains at the forefront of industry innovation and competitive strength.

- Cosentino S.A. is a distinguished Spanish multinational known globally for its high-value composite and natural stone surfaces, including those utilized in the memorial sector. While famous for kitchen countertops, their division dedicated to architectural and memorial stone plays a crucial role in the Europe tombstone market by offering durable and aesthetically versatile materials. Their global contribution lies in pioneering the development of engineered stone products that mimic natural granite and marble while offering enhanced resistance to weathering and staining. Recent strategic moves involve expanding their production capacity in Europe to meet the rising demand for personalized and modern memorial designs. Cosentino has also forged partnerships with leading funeral service providers to integrate their materials into exclusive memorial collections. The company actively promotes sustainability through water recycling systems in its manufacturing plants and carbon-neutral logistics initiatives. Cosentino strengthens its market position by continuously innovating in material science and design aesthetics. They provide next-generation memorial solutions that blend tradition with modern technology.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in the Europe tombstone market primarily employ vertical integration strategies to control the entire supply chain from quarry extraction to final installation. This approach allows companies to minimize costs and ensure consistent quality control over raw materials. Another prevalent strategy is the adoption of advanced digital technologies such as three-dimensional modeling and laser etching to offer highly customized memorial designs that cater to individual preferences. Companies are also increasingly focusing on sustainability by obtaining environmental certifications and utilizing eco-friendly quarrying practices to appeal to conscientious consumers. Strategic partnerships with funeral homes and cemetery management firms enable manufacturers to secure direct sales channels and enhance brand visibility. Furthermore, market participants are expanding their geographic footprint through acquisitions of local stonemasonry businesses to penetrate regional markets more effectively. These combined efforts allow industry leaders to maintain competitive advantages and adapt to evolving consumer demands.

MARKET SEGMENTATION

This research report on the Europe tombstone market has been segmented and sub-segmented into the following categories.

By Material Type

- Granite

- Marble

- Others

By Design / Style

- Traditional Monuments

- Modern / Custom Designs

By Application

- Home-use / Private Graves

- Commercial Cemeteries / Memorial Parks

By Distribution / Sales Channel

- Direct

- Retail

- Online

By Country

- United Kingdom

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Rest of Europe

Frequently Asked Questions

What is the Europe tombstone market?

The Europe tombstone market provides granite/marble memorials for traditional burials. UK leads personalization; Germany dominates precision granite fabrication.

How does the Europe tombstone market function?

The Europe tombstone market operates through quarries, artisan workshops, and cemetery suppliers using CNC/laser tech for custom inscriptions and designs.

What drives growth in the Europe tombstone market?

Aging populations, memorial personalization, and restoration demand propel the Europe tombstone market. Cremation shifts favor smaller plaques.

Which countries lead the Europe tombstone market?

UK commands the Europe tombstone market via bespoke memorials. Germany, France follow with granite expertise and regulatory harmonization.

What materials define the Europe tombstone market?

Granite and marble define the Europe tombstone market for durability/weather resistance. Bronze plaques serve modern cremation preferences.

What applications shape the Europe tombstone market?

Traditional cemeteries and private estates shape the Europe tombstone market, alongside columbarium niches and pet memorials.

How does regulation influence the Europe tombstone market?

EU quarrying standards and cemetery height limits govern the Europe tombstone market, promoting sustainable sourcing and design compliance.

What trends affect the Europe tombstone market?

Digital sculpting, eco-materials, and QR-code memorials transform the Europe tombstone market. Cremation niches gain popularity.

What challenges face the Europe tombstone market?

Cremation rise, skilled artisan shortages, and green regulations challenge the Europe tombstone market. Import competition pressures locals.

How has cremation impacted the Europe tombstone market?

Cremation reduced large tombstone demand in the Europe tombstone market, boosting compact plaques, urn vaults, and garden memorials.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com