Europe Transfection Reagents And Equipment Market Research Report By Product, Method, Application, End User & Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic & Rest of Europe) - Industry Analysis (2026 to 2034)

Market Size, 2025

$279.63 MnMarket Estimate, 2026

$301.44 MnMarket Forecast, 2034

$549.74 MnCAGR, 2026–2034

7.8%Europe Transfection Reagents and Equipment Market Size

The Europe transfection reagents and equipment market was valued at USD 279.63 million in 2025 and increased to USD 301.44 million in 2026. The market is projected to reach USD 549.74 million by 2034, growing at a CAGR of 7.8% from 2026 to 2034.

Transfection, a critical technique in molecular biology, involves introducing nucleic acids into eukaryotic cells for gene expression studies, functional genomics, and therapeutic development. The Europe transfection reagents and equipment market is Europe Transfection Reagents and Equipment Market witnessing robust growth due to expanding applications in life sciences research, biopharmaceutical production, and advanced therapy development.

According to the European Molecular Biology Organization (EMBO), academic and industrial research institutions across Germany, France, and the UK are increasingly adopting transfection technologies to support CRISPR-based genome editing, RNA interference, and vaccine development.

Universities and contract research organizations (CROs) are also investing in automated transfection platforms to improve reproducibility and scalability. With rising funding for biomedical research and strong regulatory support for innovative therapies, Europe remains a pivotal hub for transfection-related advancements.

MARKET DRIVERS

Expansion of Biopharmaceutical R&D Activities

One of the primary drivers of the Europe transfection reagents and equipment market is the rapid expansion of biopharmaceutical research and development. There has been a significant increase in the number of gene and cell therapy applications submitted for clinical trials across the region. In particular, companies involved in monoclonal antibody production, mRNA vaccine development, and CAR-T cell therapies rely heavily on transfection techniques for transient and stable gene expression. Germany, France, and the United Kingdom have emerged as key centers for such R&D, supported by government grants and private investments.

The growing reliance on mammalian cell lines like CHO and HEK293 for therapeutic protein manufacturing further amplifies the need for efficient transfection reagents and electroporation systems, reinforcing market growth.

Rising Investments in Genomic Research and Gene Editing Technologies

Another major driver fueling the Europe transfection reagents and equipment market is the surge in genomic research and the adoption of gene-editing tools such as CRISPR-Cas9.

Transfection plays a crucial role in delivering plasmids, siRNA, and CRISPR components into target cells, making it an indispensable tool in functional genomics and target validation studies. In Sweden and Switzerland, academic institutions are integrating high-throughput transfection platforms with automated screening workflows to accelerate drug discovery. Furthermore, Horizon Europe, the EU’s flagship research program, has allocated substantial funding toward genetic disease research, encouraging widespread use of transfection methodologies.

MARKET RESTRAINTS

High Cost of Advanced Transfection Systems

A significant restraint affecting the Europe transfection reagents and equipment market is the high cost associated with advanced transfection technologies. According to the European Observatory on Health Systems and Policies, many publicly funded research institutions struggle with budget constraints that limit their ability to procure cutting-edge transfection systems. Automated electroporation devices, lipid-based reagent kits, and microinjection platforms often require substantial initial investment and ongoing maintenance costs. These financial limitations create a barrier to the widespread adoption of next-generation transfection solutions, especially among smaller academic and contract research organizations.

Complexity and Variability in Transfection Efficiency Across Cell Types

The variability in transfection efficiency across different cell types poses another challenge to the Europe transfection reagents and equipment market.

According to the University of Heidelberg’s Department of Molecular Biology, achieving consistent transfection outcomes remains difficult when working with primary cells, stem cells, or hard-to-transfect immune cells. This inconsistency necessitates extensive protocol optimization, increasing both time and resource expenditure.

Moreover, differences in cellular uptake mechanisms and cytotoxic responses to transfection agents further complicate standardization efforts. While manufacturers are developing cell-specific reagent formulations, the lack of universal compatibility continues to hinder seamless integration into high-throughput research pipelines. This technical complexity limits the scalability of transfection-based assays and affects overall research productivity across the region.

MARKET OPPORTUNITIES

Integration of AI and Automation in Transfection Workflows

A promising opportunity for growth in the Europe transfection reagents and equipment market lies in the integration of artificial intelligence (AI) and automation into transfection workflows.

Automated liquid handling systems and robotic transfection platforms are being deployed in high-content screening facilities to enhance throughput and reduce human error.

These technological advancements are enabling faster development cycles in drug discovery and personalized medicine. As AI-assisted transfection platforms become more accessible, they are expected to drive efficiency gains and expand the application scope of transfection technologies across Europe.

Growth of Academic-Industry Collaborations in Gene Therapy Development

The strengthening collaboration between academic institutions and industry players in gene therapy development presents a major growth opportunity for the Europe transfection reagents and equipment market.

According to the European Society of Gene and Cell Therapy (ESGCT), numerous joint ventures have emerged between universities and biotech firms focused on advancing gene-based treatments for inherited disorders and oncology indications. These partnerships rely heavily on transfection techniques for vector production, target validation, and in vitro modeling.

Also, collaborative programs with pharmaceutical companies have led to increased procurement of high-performance transfection kits and scalable electroporation systems. In addition, Horizon Europe has facilitated cross-border research networks that promote standardized transfection practices and shared infrastructure. These developments are not only accelerating translational research but also creating sustained demand for innovative transfection solutions tailored to complex therapeutic applications.

MARKET CHALLENGES

Regulatory Hurdles in Clinical Translation of Transfection-Based Therapies

One of the most pressing challenges facing the Europe transfection reagents and equipment market is the stringent regulatory landscape governing the clinical translation of transfection-based therapies.

According to the European Medicines Agency (EMA), the approval process for gene transfer vectors and related delivery systems involves rigorous safety and efficacy evaluations, which significantly delay commercialization timelines. As per the European Commission’s guidelines on advanced therapy medicinal products (ATMPs), transfection-derived therapeutics must undergo extensive preclinical testing before entering clinical trials. In France and Belgium, regulatory authorities have imposed additional requirements for Good Manufacturing Practice (GMP) compliance in transfection-based product development, increasing operational complexity for manufacturers. Consequently, while scientific progress is robust, the slow pace of regulatory approvals hampers the broader adoption of transfection technologies in clinical settings.

Limited Standardization Across Transfection Protocols and Reporting Methods

Another significant challenge in the Europe transfection reagents and equipment market is the lack of standardized protocols and reporting frameworks across research institutions.

According to the European Molecular Biology Laboratory (EMBL), inconsistencies in transfection methodology ranging from reagent concentrations to post-transfection analysis lead to difficulties in comparing results across studies.

As per a review published in Nucleic Acids Research , discrepancies in transfection efficiency measurements make it challenging to benchmark performance between different reagents and instruments. In multi-center collaborations, particularly those under Horizon Europe initiatives, variations in laboratory practices hinder data interoperability and reproducibility.

Industry stakeholders are calling for consensus guidelines to harmonize transfection reporting standards, which could streamline research workflows and enhance confidence in experimental outcomes across the European market.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2026 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Product, Method, Application, End User and Country. |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis; DROC, PESTLE Analysis, Porter's Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Country Covered | UK ,France ,Spain ,Germany ,Italy ,Russia ,Sweden ,Denmark ,Switzerland ,Netherlands ,Turkey ,Czech Republic, Rest of Europe. |

| Market Leader Profiled | Thermo Fisher Scientific Inc., Promega Corporation, Hoffmann-La Roche Ltd. |

SEGMENTAL ANALYSIS

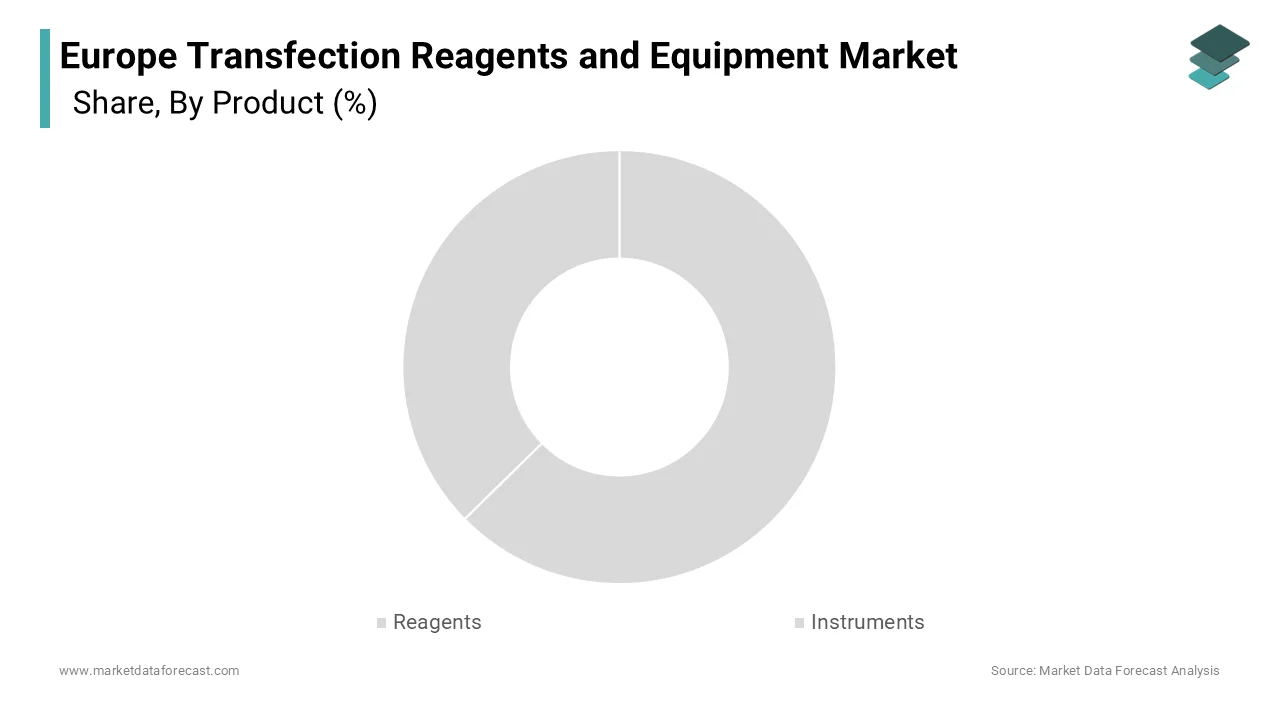

By Product Insights

The reagents segment spearheaded with 65.5% in the Europe transfection reagents and equipment market in 2025. This dominance is primarily attributed to the high consumption rate of transfection reagents across academic research, biopharma production, and gene-editing applications.

Moreover, the recurring nature of reagent purchases unlike instruments that are typically one-time investments ensures sustained demand. With ongoing advancements in nucleic acid delivery methods, this segment remains at the forefront of market growth.

The instruments segment is experiencing the highest growth rate, projected to expand at a CAGR of nearly 8.2%. This surge is driven by increasing adoption of automated and high-throughput transfection systems in both academic and industrial settings. As per the Fraunhofer Institute for Biomedical Engineering, German pharmaceutical companies are integrating robotic liquid handling platforms with real-time monitoring capabilities to enhance reproducibility and efficiency in gene delivery. In France and Switzerland, advanced electroporation devices and microinjection systems are being adopted for stem cell engineering and regenerative medicine applications.

In addition, the integration of AI-assisted transfection analytics into next-generation instruments is further boosting demand. With growing emphasis on precision and automation, the instruments segment is poised for rapid expansion across the European market.

By Method Insights

Biochemical transfection methods accounted for the majority of the European market, capturing 55.4% of total adoption. These methods include lipid-mediated transfection, polymer-based delivery, and other non-viral chemical approaches that facilitate efficient gene transfer into eukaryotic cells.

Besides, biochemical techniques are widely preferred due to their ease of use, scalability, and compatibility with a broad range of cell types.

Apart from these, pharmaceutical firms in Germany and Austria are utilizing polyethyleneimine (PEI)-based formulations for transient transfection in CHO cell lines used for therapeutic protein production. Biochemical transfection is particularly favored in high-throughput screening environments where viral vector safety concerns and cost constraints limit widespread application.

Physical transfection methods are witnessing the fastest growth, expanding at a CAGR of around 9.5%. This increase is primarily driven by advancements in electroporation, microinjection, and gene gun technologies that offer higher transfection efficiencies, especially for hard-to-transfect cell types.

In addition, physical methods are gaining traction in stem cell and primary cell research due to their ability to bypass endosomal entrapment issues associated with biochemical approaches. In Switzerland and Sweden, biomedical research institutions are increasingly adopting microfluidic-based electroporation systems for improved cell viability and transfection consistency. These innovations are enabling more precise genome editing and synthetic biology applications. In addition, rising investments in personalized medicine and ex vivo gene therapies are further accelerating the adoption of physical transfection techniques across Europe.

By Application Insights

Biomedical research constituted the largest application area, representing 60.5% of the Europe transfection reagents and equipment market. This is due to the extensive use of transfection techniques in fundamental biological studies, including gene function analysis, pathway elucidation, and disease modeling.

In Germany and France, major universities and research hospitals employ transfection methodologies for CRISPR-Cas9 gene editing, RNA interference, and reporter assays.

Also, Horizon Europe-funded initiatives have expanded collaborative research efforts, reinforcing the role of transfection in advancing life sciences knowledge. With continued government and private funding, biomedical research remains the cornerstone of market demand.

Therapeutic delivery is emerging as the fastest-growing application segment, expanding at a CAGR 10.7%. This growth is fueled by the rising development of gene and cell therapies, mRNA vaccines, and CAR-T treatments across Europe.

According to the European Medicines Agency (EMA), the number of advanced therapy medicinal product (ATMP) applications has surged in recent years, many of which rely on transfection for vector production and cell modification.

In Belgium and the Netherlands, contract manufacturing organizations (CMOs) are scaling up transfection-based processes to support GMP-grade viral vector production for clinical trials.

Transfection plays a critical role in the rapid development of next-generation vaccines, including self-amplifying RNA constructs. Furthermore, Horizon Europe has prioritized regenerative medicine and immunotherapy, driving investment in scalable transfection solutions tailored for therapeutic applications.

By End User Insights

Academic and research institutes dominated the Europe transfection reagents and equipment market in 2025, accounting for over 55.5% of total end-user demand. This lead position is underpinned by the heavy reliance of universities, medical schools, and public research centers on transfection technologies for basic science investigations and training programs.

As per the European Molecular Biology Laboratory (EMBL), academic institutions across Germany, the UK, and Sweden are conducting large-scale functional genomics studies that require robust transfection protocols. In addition, Horizon Europe supports numerous collaborative research networks that leverage transfection for CRISPR screening, proteomics, and disease modeling. With continuous government funding and institutional procurement cycles, academic entities remain the largest consumer group in the regional market.

Pharmaceutical and biotechnology companies represent the fastest-growing end-user segment, expanding at a CAGR of 9.7%. This growth is driven by the increasing reliance on transfection for biologics production, gene therapy development, and high-throughput drug screening.

According to Roche Innovation Labs, transfection efficiency directly impacts process yield and quality in cell-based therapeutics. Apart from these, contract development and manufacturing organizations (CDMOs) are expanding their transfection infrastructure to meet growing demand for ATMPs. As biopharma innovation intensifies, this segment is expected to drive substantial market expansion.

COUNTRY LEVEL ANALYSIS

Germany led the largest market share in Europe, contributing over 22.4% of total revenue in 2025. The country's dominant position is driven by its world-class research institutions, strong biopharma industry, and government support for life sciences innovation. Universities like the Max Planck Institute and Charité Berlin are at the forefront of CRISPR-based research and stem cell engineering. Moreover, pharmaceutical giants such as Merck KGaA and Boehringer Ingelheim are leveraging transfection for therapeutic protein production and vaccine development. With a robust ecosystem of academic-industry collaborations and regulatory alignment with EMA standards, Germany continues to lead the European transfection market.

The UK is hub for genomic and biotech innovation. The country’s strong presence in genomic research, bolstered by institutions like the Wellcome Sanger Institute and Francis Crick Institute, drives consistent demand for transfection tools. Despite Brexit-related uncertainties, the country maintains a leading role in biotech innovation through partnerships between academia and global pharma players, ensuring sustained growth in transfection technology adoption.

France is seeing growing demand for the European transfection market. The country benefits from a well-established network of public research institutions, including INSERM and CNRS, which actively engage in transfection-based studies related to oncology, neurodegenerative disorders, and infectious diseases.

In addition, French biotech firms like Transgene and DBV Technologies are integrating transfection into their therapeutic development pipelines. With Horizon Europe funding and national research grants supporting innovation, France is strengthening its foothold in the transfection market.

Switzerland is known for its dense concentration of pharmaceutical multinationals including Roche and Novartis and elite research institutions like ETH Zurich, the country has a high adoption rate of advanced transfection systems. Additionally, Switzerland’s favorable regulatory environment and strong intellectual property protections attract global investment in gene and cell therapy development.

Sweden is an emerging leader in functional genomics. The country has become an emerging leader in functional genomics and RNA-based research, largely driven by institutions such as the Karolinska Institute and SciLifeLab. Government-backed initiatives like Vinnova’s life sciences program have supported the development of novel transfection reagents optimized for difficult cell types. With growing interest in precision medicine and regenerative therapies, Sweden is positioning itself as a key player in the European transfection landscape.

KEY MARKET PLAYERS AND COMPETITIVE LANDSCAPE

Thermo Fisher Scientific Inc., Promega Corporation, Hoffmann-La Roche Ltd. (Switzerland), QIAGEN N.V. (Netherlands), Bio-Rad Laboratories, Lonza Group (Switzerland), Sigma-Aldrich Corporation, Mirus Bio LLC and MaxCyte Inc. are some of the major companies in the European transfection reagents and equipment market.

The competition in the Europe transfection reagents and equipment market is marked by a dynamic mix of established multinational corporations and innovative regional players striving to capture a larger share of this rapidly advancing sector. Global leaders such as Thermo Fisher Scientific, Merck KGaA, and Lonza dominate due to their comprehensive product portfolios, strong R&D capabilities, and well-established distribution networks. These companies set the pace in innovation, frequently launching advanced transfection reagents and high-throughput instrumentation tailored to the evolving demands of life sciences research and biopharma production. However, mid-sized and niche-focused firms are gaining traction by offering specialized solutions that cater to specific research areas or hard-to-transfect cell types. The market is also witnessing increased competition from local biotech firms leveraging agile business models and cost-effective offerings to penetrate academic and small-scale research labs. As demand for precision medicine, gene editing, and biologics continues to rise, vendors must continuously innovate while ensuring regulatory compliance and scalability. This evolving competitive landscape fosters both collaboration and rivalry, ultimately driving technological advancements and broader accessibility of transfection tools across Europe.

Top Players in the Market

Thermo Fisher Scientific is a global leader in life sciences research tools, including transfection reagents and equipment. The company offers a broad portfolio of lipid-based transfection agents, electroporation systems, and viral vector solutions tailored for academic and industrial applications. In Europe, it plays a crucial role in supporting gene-editing research, vaccine development, and biopharmaceutical production. Its contributions to the global market include continuous innovation, extensive technical support, and partnerships with leading research institutions, ensuring high-performance transfection workflows across diverse experimental settings.

Merck KGaA is a key player known for its high-quality transfection reagents, particularly through its Sigma-Aldrich brand. The company provides advanced non-viral gene delivery solutions, including proprietary lipid formulations and polymer-based systems. In Europe, Merck supports academic and biotech sectors by offering scalable and efficient transfection technologies. Its commitment to developing cell-specific reagents and automation-compatible kits enhances reproducibility and throughput in both basic and applied research, making it a preferred supplier across major research hubs in Germany, France, and the UK.

Lonza is a prominent provider of transfection solutions for large-scale therapeutic applications, particularly in gene and cell therapy manufacturing. With specialized electroporation platforms and GMP-grade reagents, the company serves contract development and manufacturing organizations (CDMOs) and pharmaceutical firms across Europe. Lonza contributes significantly to the global market by enabling scalable, high-efficiency transfection processes essential for producing next-generation biotherapeutics, reinforcing its position as a trusted partner in translational and clinical research.

Top Strategies Used by Key Market Participants

- Key players in the Europe transfection reagents and equipment market are employing strategic collaborations and academic-industry partnerships to align with evolving research trends and expand their market reach. By engaging with universities, research institutes, and biotech startups, companies ensure early adoption of their products and gain insights into emerging application needs.

- Another major strategy involves product innovation and differentiation , where manufacturers focus on developing novel reagent formulations, automated transfection systems, and cell-specific delivery platforms. These advancements help address challenges related to efficiency, cytotoxicity, and scalability, setting industry benchmarks and enhancing customer loyalty.

- Lastly, companies are investing in technical support, training programs, and digital integration to improve user experience and streamline workflows. By offering customized protocols, online resources, and AI-assisted optimization tools, they ensure seamless adoption of transfection technologies across diverse research environments, strengthening their foothold in the competitive European landscape.

RECENT HAPPENINGS IN THE MARKET

- In February 2023, Thermo Fisher Scientific launched a new line of high-efficiency lipid-based transfection reagents specifically designed for CRISPR-Cas9 applications, targeting academic and biotech researchers across Germany and the UK.

- In September 2023, Merck KGaA expanded its collaboration with a French gene therapy institute to co-develop optimized transfection protocols for induced pluripotent stem cells, aiming to enhance reproducibility and reduce cytotoxic effects in regenerative medicine studies.

- In April 2025, Lonza introduced an upgraded electroporation system tailored for GMP-compliant cell and gene therapy manufacturing, addressing growing demand from CDMOs and pharma firms in Switzerland and the Netherlands.

- In November 2025, PromoCell , a European biotech firm, partnered with a German university hospital to develop transfection reagents suited for primary immune cells, expanding its footprint in immunotherapy research applications.

- In March 2025, Bio-Rad Laboratories acquired a Swedish startup specializing in microfluidic-based transfection technology, aiming to integrate novel methods into its existing portfolio and strengthen its presence in high-content screening markets.

MARKET SEGMENTATION

This research report on the europe transfection reagents and equipment market has been segmented and sub-segmented into the following categories.

By Product

- Reagents

- Instruments

By Method

- Biochemical Transfection Method

- Physical Transfection Methods

By Application

- Biomedical Research

- Therapeutic Delivery

By End User

- Academic & Research Institutes

- Pharmaceutical & Biotechnology Companies

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

What are the factors driving the growth of the Europe Surgical Equipment Market?

Factors driving the growth of the Europe Surgical Equipment Market include the increasing number of surgical procedures, advancements in surgical technology, growing geriatric population, and rising prevalence of chronic diseases requiring surgical interventions.

Which countries in Europe have a significant presence in the surgical equipment market?

Several countries in Europe have a significant presence in the surgical equipment market, including Germany, France, the United Kingdom, Italy, and Spain.

What are the major challenges faced by the Europe Surgical Equipment Market?

Major challenges faced by the Europe Surgical Equipment Market include the high cost of surgical equipment, stringent regulatory requirements, concerns regarding the safety and efficacy of certain devices, and limited healthcare budgets in some countries.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com