Europe Trifluralin Market Size, Share, Trends & Growth Forecast Report, Segmented By Crop, Type, Application, And By Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic and Rest of Europe), Industry Analysis From 2024 to 2033

Europe Trifluralin Market Size

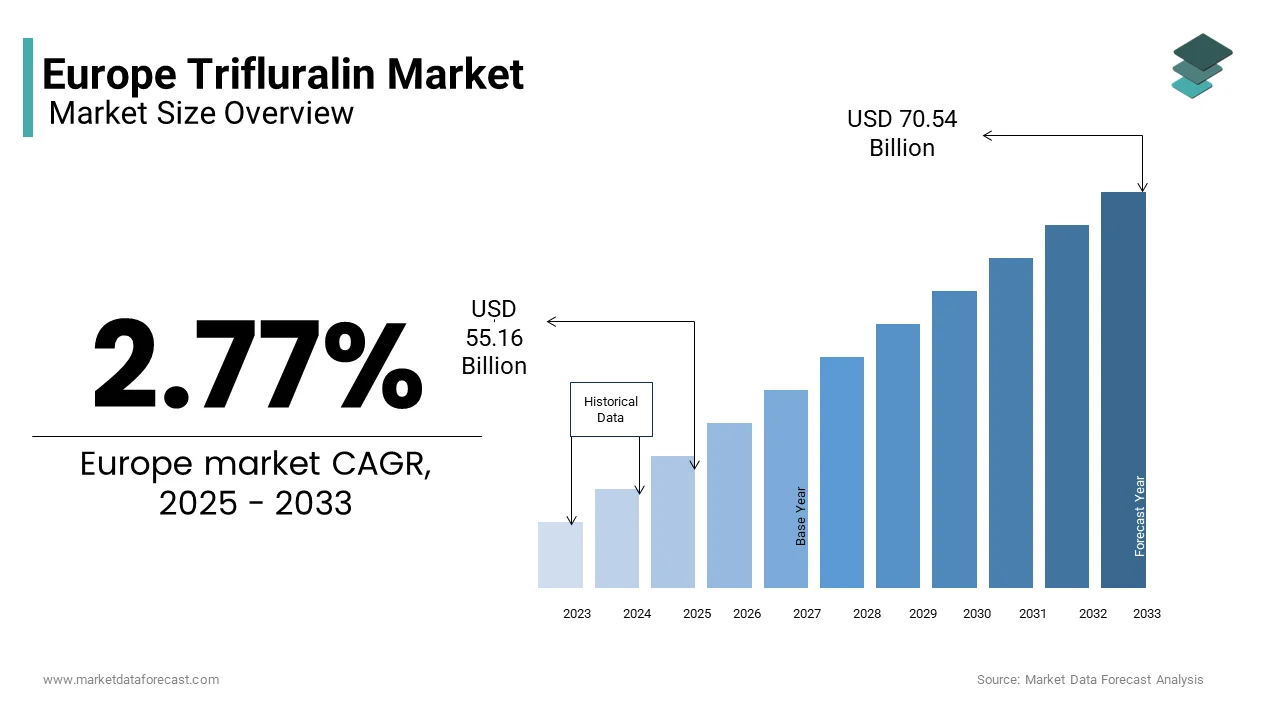

In 2024, the Europe trifluralin market is projected to grow from USD 55.16 billion to USD 70.54 billion by 2033, growing at a CAGR of 2.77%.

Trifluralin is a pre-emergence herbicide widely used in agriculture to control annual grasses and broadleaf weeds. It belongs to the dinitroaniline chemical family and functions by inhibiting root cell division in germinating weed seeds, thereby preventing their establishment. In the European market, trifluralin has been historically applied across a range of crops, including cereals, oilseeds, and vegetables, particularly in countries with extensive arable farming such as France, Germany, Poland, and Ukraine.

Despite its efficacy, the usage of trifluralin in Europe has seen regulatory scrutiny due to environmental concerns, particularly regarding its persistence in soil and potential groundwater contamination. Several EU member states have imposed restrictions or withdrawn product registrations altogether. However, it remains in limited use under strict compliance conditions where alternatives are either less effective or economically unviable.

As per the European Crop Protection Association, herbicide demand in Western Europe grew by 2.1% year-on-year in 2023, driven by integrated weed management strategies that sometimes include residual herbicides like trifluralin. While synthetic herbicide usage trends are shifting toward more environmentally benign compounds, trifluralin continues to play a niche role in specific agronomic systems across Eastern and Central Europe.

MARKET DRIVERS

Expansion of Organic Farming and Integrated Weed Management Practices

One of the key drivers of the Europe trifluralin market lies within the framework of integrated weed management (IWM) practices adopted in semi-organic and transitional farms. Although trifluralin is not approved for certified organic production, its residual effect and cost-efficiency make it an attractive option for farmers transitioning from conventional to low-input systems, especially in Eastern Europe, where farm economics are tighter.

In countries like Romania and Bulgaria, where the adoption of IWM techniques is growing, trifluralin is increasingly being used alongside mechanical weeding and cover cropping to reduce reliance on post-emergence herbicides. Within this context, transitional farms often rely on selective herbicides like trifluralin to manage weed pressure without immediate full withdrawal from synthetic chemicals.

Apart from these, as per the European Innovation Partnership (EIP-AGRI) in 2023, 43% of surveyed farms in Central and Eastern Europe were integrating reduced-chemical input strategies, many of which included short-term applications of residual herbicides such as trifluralin. This trend is further supported by national agricultural advisory services in Poland and Hungary, which recommend its use in rotation with other herbicides to delay resistance development and maintain crop yields during transition phases.

The continued relevance of trifluralin in these evolving farming systems underscores its utility beyond purely conventional applications, providing a temporary yet significant boost to its market presence in select regions of Europe.

Increasing Demand for High-Yield Crops Amidst Shrinking Arable Land

An additional critical driver of the Europe trifluralin market is the persistent need to maximize yield per hectare amid diminishing available arable land and rising population pressures. With urbanization and land degradation reducing cultivable areas, farmers are increasingly turning to efficient and cost-effective weed control solutions to optimize productivity.

Like, according to the Food and Agriculture Organization (FAO), the average arable land per capita in Europe declined by 8.4% between 2010 and 2022. Simultaneously, cereal demand in the region rose by 6.3%, driven by both domestic consumption and export needs. In response, farmers—particularly in countries like Germany, France, and Poland—are relying on herbicides such as trifluralin to ensure early-season weed suppression and protect yield potential in crops like wheat, barley, and rapeseed.

As per data from the European Environment Agency, in 2023, approximately 4.1 million hectares of farmland in the EU were affected by moderate to severe weed infestations, leading to an estimated 10–15% loss in grain yield if left untreated. Trifluralin’s pre-emergence activity provides a long-lasting solution to this challenge, especially in no-till and conservation agriculture systems that are gaining traction across the continent.

Moreover, the ability of trifluralin to offer season-long weed control with a single application makes it a preferred choice in high-pressure environments, reinforcing its continued use despite tightening regulations in certain markets.

MARKET RESTRAINTS

Regulatory Restrictions and Environmental Concerns Across the EU

One of the most significant restraints affecting the Europe trifluralin market is the tightening of regulatory frameworks across the European Union, driven by increasing environmental and health-related concerns. The European Chemicals Agency (ECHA) and the European Food Safety Authority (EFSA) have classified trifluralin as a substance of very high concern (SVHC) due to its potential endocrine-disrupting properties and environmental persistence.

In 2022, the European Commission revoked the approval of trifluralin under Regulation (EC) No 1107/2009, effectively banning its use in all EU member states starting January 2023. This decision followed a multi-year evaluation process that found insufficient evidence to confirm the compound's safety for groundwater and aquatic ecosystems. Countries such as Denmark, Sweden, and Austria had already implemented national bans before the EU-wide phase-out.

According to the Pesticide Action Network (PAN) Europe, over 20 active pesticide substances were removed from the EU market between 2018 and 2023 due to similar risk assessments, with trifluralin being among the most recent. The ban has significantly curtailed its availability, especially in Western Europe, where regulatory enforcement is strongest.

While some Eastern European countries initially resisted the phase-out, citing economic implications, they eventually complied with EU directives. As a result, the overall market volume for trifluralin in Europe has contracted sharply.

Availability and Adoption of Safer Alternatives and Bioherbicides

Another major constraint on the Europe trifluralin market is the rapid development and adoption of alternative herbicidal products that are perceived as safer and more environmentally sustainable. The European agrochemical industry has been witnessing a strong shift towards bio-based herbicides and synthetic compounds with lower ecological footprints, reducing the relevance of older chemistries like trifluralin.

Companies such as BASF, Syngenta, and UPL have invested heavily in developing non-residual, biodegradable options that align with the EU’s Green Deal and Farm to Fork Strategy targets.

For instance, pelargonic acid-based herbicides and microbial formulations derived from Bacillus species have gained traction in both conventional and transitional farming systems. These alternatives offer faster breakdown times, minimal soil residue, and compatibility with integrated pest management (IPM) protocols.

Furthermore, as per Wageningen University’s research in 2023, newer synthetic herbicides such as pyroxasulfone provided equivalent or superior weed control to trifluralin without the associated environmental risks. These findings have encouraged policymakers and extension agencies to promote substitution programs, accelerating the displacement of legacy products like trifluralin from mainstream agricultural use across Europe.

MARKET OPPORTUNITY

Growth in Conservation Agriculture and Reduced-Tillage Farming Systems

An emerging opportunity for the Europe trifluralin market lies in the expansion of conservation agriculture and reduced-tillage farming systems, particularly in Central and Eastern Europe. These practices aim to minimize soil disturbance, enhance carbon sequestration, and improve water retention—objectives that align closely with the EU’s broader sustainability goals outlined in the Common Agricultural Policy (CAP) reform and the European Green Deal.

Trifluralin, as a pre-emergence herbicide, plays a crucial role in such systems by offering effective weed control without the need for frequent plowing or mechanical interventions. Its residual action helps suppress weeds during the early growth stages of crops, which is especially beneficial in no-till systems where post-emergence spraying can be logistically challenging.

In countries like Hungary, Romania, and Bulgaria, where adoption rates are growing rapidly, government subsidies and technical support from the European Innovation Partnership (EIP-AGRI) are encouraging farmers to adopt no-till methods.

In these contexts, trifluralin remains a favored option due to its affordability and proven efficacy in controlling grassy weeds, a common issue in conservation tillage systems. Despite the EU-wide ban on new registrations, existing stockpiles and grandfather clauses in some member states have allowed limited use in alignment with conservation farming protocols, presenting a niche yet strategic opportunity for sustained application in specific agronomic settings.

Use in Non-Agricultural Applications and Specialized Horticulture

A further growing avenue for trifluralin utilization in Europe is its application in non-agricultural sectors, particularly in specialized horticulture, landscaping, and industrial site maintenance. While agricultural use has faced regulatory headwinds, these alternative applications remain relatively less scrutinized and continue to offer viable market opportunities.

Trifluralin is commonly used as a soil sterilant in railway embankments, industrial zones, and ornamental plant nurseries to prevent unwanted vegetation growth. In these scenarios, its long residual effect is an advantage rather than a liability, making it preferable to short-acting herbicides that require frequent reapplication.

Among these, trifluralin-based formulations were noted for their effectiveness in maintaining weed-free zones around infrastructure sites. Moreover, in controlled-environment horticulture, trifluralin is sometimes used in potting mixes and greenhouse beds to inhibit weed germination without affecting the primary crop. Though niche, this segment benefits from the lack of suitable alternatives that offer comparable performance and cost efficiency.

With urban green space initiatives expanding across Europe, the demand for durable vegetation control solutions like trifluralin is expected to persist, albeit in a more regulated and targeted manner.

MARKET CHALLENGES

Development of Herbicide-Resistant Weeds and Diminished Efficacy

One of the foremost challenges facing the Europe trifluralin market is the emergence of herbicide-resistant weed populations, which undermines the compound’s effectiveness and diminishes farmer confidence in its long-term viability. Resistance develops when weeds adapt to repeated exposure to the same mode of action—in this case, microtubule inhibition—which is characteristic of the dinitroaniline herbicide group to which trifluralin belongs.

Also, there were many documented cases of trifluralin-resistant weed species globally, with some confirmed in Europe, including Alopecurus myosuroides (blackgrass) and Lolium rigidum (annual ryegrass). These species are prevalent in major cereal-growing regions such as France, Germany, and the UK, where intensive herbicide use has accelerated resistance development.

In field trials, trifluralin demonstrated a reduction in efficacy against resistant blackgrass populations compared to susceptible strains. This diminished performance necessitates higher application rates or supplementary treatments, increasing costs and potentially exacerbating environmental concerns.

Farmers are increasingly seeking diversified weed management approaches, including tank mixes and rotational herbicides, to mitigate resistance risks. However, given the regulatory constraints on many alternative chemistries in Europe, this challenge becomes even more pronounced. Consequently, the declining reliability of trifluralin poses a serious obstacle to its sustained market relevance, especially in regions where resistant weed populations have become widespread.

Economic Pressures on Small and Medium-Sized Farms Limiting Herbicide Investments

Another pressing challenge impacting the Europe trifluralin market is the financial strain on small and medium-sized agricultural enterprises (SMEs), which constitute the majority of European farms and are key consumers of herbicidal products. Rising input costs, fluctuating commodity prices, and reduced direct payments under the reformed Common Agricultural Policy (CAP) have constrained investment capacity, particularly in Eastern and Southern Europe.

In countries like Poland, Romania, and Greece, where trifluralin was previously more affordable and widely used, farmers have been forced to cut back on agrochemical purchases due to liquidity issues.

This economic pressure is compounded by the phasing out of subsidized access to older-generation herbicides and the increasing cost of compliant alternatives. Trifluralin, though cheaper than newer chemistries, has become less accessible due to supply chain disruptions following the EU-wide regulatory restrictions.

As a result, many SMEs are reverting to manual weeding or reduced herbicide applications, which negatively impacts weed control efficacy and crop yields. This trend threatens not only the commercial viability of trifluralin but also the broader herbicide market, as budgetary limitations drive farmers toward less effective or outdated management practices, limiting the sector’s modernization prospects.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| CAGR | 2.77% |

| Segments Covered | By Crop, Type, Application, and By Country |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

| Regions Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republi,c and Rest of Europe |

| Market Leaders Profiled | Shandong Qiaochang Chemical Co., Ltd., Chongqing Shurong, Shenzhen Sunrising Industry Co., Ltd., Chemical Co., Ltd., BASF, Jiangsu Fengshan Group Co., Ltd., and Dow Chemical Company |

SEGMENTAL ANALYSIS

By Crop Insights

Field Crops

Field crops dominated the Europe trifluralin market, accounting for a substantial share of total herbicide application volume in 2024. This segment includes major crops such as wheat, barley, maize, rapeseed, and sunflowers, which are extensively cultivated across Western and Eastern Europe.

The dominance of field crops is primarily driven by their vast acreage and the high susceptibility of these crops to early-season weed infestations. Effective weed control during the critical germination phase is essential to maintaining yield stability, particularly in no-till and reduced-tillage systems where mechanical weeding is limited.

Another key driver is the economic efficiency of trifluralin in large-scale farming operations. Despite regulatory constraints in certain regions, countries such as Poland, Romania, and Ukraine have continued using trifluralin under grandfather clauses or through existing stockpiles, especially in less intensively monitored agricultural zones. The compound's compatibility with integrated weed management strategies—particularly in transitional farms aiming to reduce synthetic chemical dependency gradually—further supports its sustained presence in the field crops segment.

Fruit & Vegetable Crops

The fruit and vegetable crops segment is emerging as the fastest-growing within the Europe trifluralin market, projected to grow at a CAGR of 6.1% during the forecast period. While currently smaller than field crops, this segment is gaining momentum due to evolving agronomic practices and increasing demand for high-value produce.

One of the primary drivers is the expansion of protected and semi-protected horticulture, particularly in Southern and Central Europe. Countries like Spain, Italy, and the Netherlands have seen significant investment in greenhouse-based vegetable production, where effective weed control without damaging root systems is crucial. Like, the area under greenhouse cultivation in the EU increased, with increasing use of herbicides in managing weeds in container-grown and raised-bed systems.

Also, the use of trifluralin in orchards—especially apple, pear, and stone fruit plantations—has gained traction as an alternative to labor-intensive manual weeding. Despite tighter regulations on pesticide usage in fresh produce, the ability of trifluralin to offer season-long weed suppression with minimal phytotoxicity makes it a preferred choice in niche horticultural applications, supporting its accelerated adoption in this segment.

By Type Insights

Miscible Oil (Emulsifying Concentrate)

The miscible oil or emulsifying concentrate (EC) formulation accounts for 68.4% of the Europe trifluralin market by product type in 2024. This dominance stems from its superior solubility, ease of application, and compatibility with various spray equipment used in modern agriculture. Their liquid nature allows for uniform dispersion when mixed with water, ensuring consistent soil coverage and enhanced efficacy against germinating weed seeds.

Moreover, the EC form is particularly suited for integration into precision agriculture technologies, including GPS-guided sprayers and drone-based application systems. In Eastern Europe, where access to advanced granular application machinery is more limited, EC formulations remain the preferred option due to their adaptability to traditional tractor-mounted sprayers.

Granular (GR) Formulation

The granular (GR) formulation of trifluralin is experiencing the fastest growth in the Europe market, anticipated to expand at a CAGR of 7.3% between 2025 and 2033, outpacing the EC segment due to its unique advantages in specific agricultural and non-agricultural settings.

This growth is largely attributed to the rising adoption of GR formulations in conservation agriculture and industrial vegetation management. Unlike liquid formulations, granular trifluralin can be applied directly into the soil profile during planting, reducing drift risk and enhancing environmental safety—a factor increasingly emphasized by policymakers and agri-environmental programs.

In countries like Hungary and Romania, where no-till adoption has surged, granular trifluralin is often incorporated into seed drills, providing targeted pre-emergence control without requiring additional spraying passes. Furthermore, GR formulations are gaining popularity in urban landscaping and infrastructure maintenance, where minimizing spray drift near residential areas is crucial.

By Application Insights

Annual Grasses

Controlling annual grasses remained the largest application segment for trifluralin in Europe, representing 58.2% of total herbicide usage in 2024. This dominance is attributable to the widespread prevalence of grassy weeds such as blackgrass (Alopecurus myosuroides ), wild oat (Avena fatua ), and ryegrass (Lolium spp. ), which pose significant threats to cereal and oilseed crop yields across the continent. These weeds are particularly problematic due to their rapid germination cycle and increasing resistance to post-emergence herbicides, necessitating effective residual control measures.

Moreover, the shift toward conservation tillage practices—especially in Germany, Poland, and the UK—has amplified the need for reliable pre-emergence solutions. Despite regulatory restrictions in some regions, the continued presence of trifluralin in this segment is supported by its proven efficacy in integrated weed management systems, where it is often used in rotation with other herbicides to delay resistance development and maintain optimal crop productivity.

Wireweed

The wireweed (Polygonum aviculare) control segment is witnessing the fastest growth in the Europe trifluralin market, projected to expand at a CAGR of 8.2%, driven by its increasing infestation rates in both agricultural and industrial settings. Wireweed is a highly adaptable broadleaf weed known for its resilience to multiple herbicide modes of action and its rapid colonization of disturbed soils. It has become a growing concern in rotational crops such as potatoes, sugar beets, and legumes, particularly in Northern and Central Europe. Trifluralin’s mode of action—targeting cell division in germinating weed roots—makes it uniquely effective against wireweed, which is less responsive to post-emergence glyphosate-based treatments. Also, its utility in industrial vegetation management—such as along railways, storage yards, and construction sites—where wireweed frequently establishes, has contributed to increased demand.

KEY MARKET PLAYERS

Shandong Qiaochang Chemical Co., Ltd., Chongqing Shurong, Shenzhen Sunrising Industry Co., Ltd., Chemical Co., Ltd., BASF, Jiangsu Fengshan Group Co., Ltd., and Dow Chemical Company are the leaders in the Europe Trifluralin market.

COUNTRY-LEVEL ANALYSIS

Germany

Germany held the leading position in the Europe trifluralin market, accounting for 14.4% of total regional consumption in 2024. Despite stringent pesticide regulations, the country continues to utilize trifluralin under grandfather provisions, particularly in specialized horticulture and industrial vegetation management.

A key driver is the country’s extensive adoption of conservation agriculture and precision farming techniques. In addition, Germany's robust landscape maintenance sector, including railway embankments and green infrastructure, relies on trifluralin for long-term vegetation control. Moreover, the country’s strong research framework supports continued application in controlled environments. Institutions like the Julius Kühn Institute have conducted trials confirming trifluralin’s efficacy against resistant weeds like Amaranthus retroflexus and Chenopodium album, reinforcing its relevance despite declining overall pesticide usage. However, regulatory pressure is expected to limit future expansion, pushing industry players toward alternative chemistries.

France

France remains a key player in the Europe trifluralin market, primarily driven by its large cereal and oilseed sectors. The country's extensive farmland creates persistent demand for effective pre-emergence weed control solutions. One of the key factors sustaining trifluralin use is its role in combating herbicide-resistant blackgrass (Alopecurus myosuroides ), which has become a major agronomic challenge. In addition, farmers have turned to residual herbicides like trifluralin as part of integrated weed management strategies.

Despite the EU-wide ban on new registrations, France allows limited use of existing stocks, particularly in transitional farms adopting lower-input systems. However, increasing adoption of bioherbicides and stricter enforcement of chemical reduction policies are expected to constrain its long-term market presence.

Poland

Poland holds a significant position in the Europe trifluralin, supported by its status as one of the continent’s top agricultural producers. With large hectares of arable land—second only to France—Poland’s extensive cereal and potato cultivation drives steady demand for effective pre-emergence herbicides. Another contributing factor is the slower pace of regulatory enforcement in Eastern Europe compared to Western counterparts. Although the EU revoked approval for trifluralin in 2023, Poland permitted the continued use of existing stocks, allowing for a gradual transition to alternative herbicides.

Spain

Spain contributes notably to the Europe trifluralin market, driven by its expanding horticultural and specialty crop sectors. The country’s Mediterranean climate supports year-round cultivation of fruits, vegetables, and olives, where effective weed control is essential to maintaining yield quality and minimizing labor costs. Trifluralin’s ability to provide season-long control with a single application makes it a preferred option in orchard and vineyard management. Also, Spain’s growing use of drip irrigation and mulching systems aligns well with trifluralin’s application methods, allowing for targeted weed suppression without interfering with irrigation infrastructure.

Italy

Italy also occupies a key position in the Europe trifluralin market, fueled by its diverse agricultural landscape and strong focus on specialty crops. The country’s extensive rice, maize, and vineyard cultivation creates a consistent need for selective pre-emergence herbicides. Trifluralin’s effectiveness in flooded and semi-flooded conditions makes it particularly valuable in rice paddies, where mechanical weeding is impractical. Moreover, the country’s viticulture sector relies on residual herbicides to maintain clean vine rows and improve harvest efficiency. Despite ongoing regulatory scrutiny and efforts to promote biological alternatives, Italy’s complex agricultural structure and regional variations in enforcement allow for continued trifluralin use in select applications, supporting its stable market position.

Top Players in the Europe Trifluralin Market

One of the leading players in the Europe trifluralin market is BASF SE. As a global leader in the agrochemical industry, BASF has played a significant role in the formulation and distribution of herbicidal products, including those containing trifluralin. The company's strong research and development capabilities have enabled it to optimize application methods and enhance product efficiency. Although shifting focus toward more sustainable alternatives, BASF continues to support existing formulations through its extensive supply chain network across Europe.

Another major player is Syngenta AG, a Switzerland-based multinational agrochemical and seed company. Syngenta has historically contributed to the growth of the trifluralin market through its portfolio of broad-spectrum herbicides used in cereal and oilseed cultivation. The company has been instrumental in educating farmers on integrated weed management practices that include residual herbicides like trifluralin. Despite regulatory pressures, Syngenta remains active in advisory services and product stewardship related to older chemistries.

The third key participant is UPL Limited, an Indian multinational agrochemical company with a growing presence in the European market. UPL has maintained relevance by offering cost-effective formulations and supporting transitional farming systems where synthetic herbicides are still necessary. Through strategic partnerships and localized distribution networks, the company ensures continued availability of trifluralin-based products in Eastern Europe, where regulatory enforcement is less stringent than in Western regions.

Top Strategies Used By Key Market Participants

A primary strategy employed by key players in the Europe trifluralin market is product differentiation and formulation optimization. Companies are focusing on enhancing the solubility, application efficiency, and environmental compatibility of trifluralin-based products to meet evolving agricultural needs while adhering to regulatory constraints. This includes developing granular and emulsifiable concentrate forms tailored for precision agriculture techniques.

Another critical approach is strategic partnerships and collaboration. Major agrochemical firms are forming alliances with local distributors, farm cooperatives, and agronomic consultants to maintain market access, especially in regions where direct sales may be restricted. These collaborations also facilitate knowledge transfer and better adoption of best practices among farmers.

Lastly, companies are investing in educational outreach and technical advisory services. By engaging directly with growers through field trials, demonstration programs, and extension services, they ensure continued use of trifluralin within permitted guidelines. These efforts help maintain product relevance even as the industry transitions toward alternative weed control solutions.

COMPETITION OVERVIEW

The competitive landscape of the Europe trifluralin market is shaped by a combination of regulatory pressures, shifting agricultural practices, and the influence of major agrochemical companies. While the overall market is declining due to restrictions imposed by EU pesticide regulations, competition persists primarily in niche applications and regional pockets where usage remains permissible under grandfather clauses or transitional frameworks. Large multinational corporations dominate the space, leveraging their extensive distribution networks, technical expertise, and long-standing relationships with agricultural stakeholders. These firms continue to offer trifluralin-based formulations while simultaneously promoting alternative herbicides that align with sustainability goals. Smaller regional suppliers also play a role, particularly in Eastern Europe, where economic constraints and slower regulatory enforcement allow for continued reliance on cost-effective pre-emergence herbicides. The market dynamic is further influenced by the increasing emphasis on integrated weed management strategies, which encourage rotational use of herbicides to delay resistance development. As a result, competition is not only about product availability but also about providing comprehensive agronomic support to sustain crop productivity under evolving environmental and policy conditions.

RECENT HAPPENINGS IN THE MARKET

- In February 2023, BASF SE launched an updated technical advisory program aimed at assisting European farmers in optimizing the use of residual herbicides, including trifluralin, within integrated weed management systems. This initiative was designed to extend product usability under tightening regulatory conditions.

- In May 2023, Syngenta AG partnered with several national agricultural advisory bodies across Central and Eastern Europe to promote responsible application practices for legacy herbicides like trifluralin, ensuring compliance with evolving EU standards while maintaining efficacy.

- In September 2023, UPL Limited expanded its distribution network in Poland and Romania to reinforce the availability of trifluralin-based formulations in regions where regulatory enforcement remains lenient compared to Western Europe.

- In January 2024, Nufarm Limited introduced a new granular formulation of trifluralin specifically adapted for conservation tillage systems, responding to the growing demand for soil-friendly application methods in sustainable agriculture.

- In June 2024, ADAMA Agricultural Solutions initiated a series of farmer training workshops across the Balkans, emphasizing the strategic integration of trifluralin into rotational herbicide programs to manage resistant weed populations effectively.

MARKET SEGMENTATION

This research report on the Europe trifluralin market is segmented and sub-segmented into the following categories:

By Crop

- Field crops

- Fruit & vegetable crops

By Type

- Miscible Oil (emulsifying concentrate) and granular (GR)

By Application

- Annual grasses

- Wireweed

- Spurrey

- Father

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

What is Trifluralin and how is it used in European agriculture?

Trifluralin is a selective pre-emergence herbicide primarily used to control annual grasses and broadleaf weeds in crops such as soybeans, sunflowers, maize, and sugar beets. In Europe, it’s applied during soil preparation before crop emergence to prevent weed competition, which helps improve yield efficiency and reduce manual weeding costs.

Is Trifluralin still approved for use in the European Union?

The regulatory status of Trifluralin in the EU has evolved over time due to environmental and health concerns. While it was previously authorized in several member states, recent assessments by the European Food Safety Authority (EFSA) and the European Chemicals Agency (ECHA) have raised concerns regarding its persistence in soil and potential groundwater contamination. As a result, some countries have restricted or phased out its use, while others continue limited application under strict guidelines.

Which countries in Europe are the main users of Trifluralin?

Historically, countries like France, Germany, Romania, and Poland were among the top users of Trifluralin-based herbicides due to their large-scale production of row crops where the herbicide was effective. However, due to tightening regulations and growing preference for alternative herbicides with lower environmental impact, usage has declined significantly in recent years, especially in Western Europe.

Why is there increasing scrutiny around Trifluralin in Europe?

Trifluralin has come under increased scrutiny because of its potential environmental risks. It is known to persist in soil and can leach into groundwater, posing risks to aquatic ecosystems. Additionally, some studies suggest possible endocrine-disrupting effects, which has led to calls for stricter regulation under the EU’s Sustainable Use Directive and the REACH Regulation framework.

Are there alternatives to Trifluralin being adopted in European farming?

Yes, farmers and agrochemical companies across Europe are increasingly turning to alternative herbicides and integrated weed management practices. Products based on active ingredients like pendimethalin, S-metolachlor, and flufenacet are gaining popularity. There's also a growing interest in non-chemical methods such as cover cropping, mechanical weeding, and precision agriculture tools to reduce reliance on synthetic herbicides.

How does the EU’s pesticide policy affect the future of Trifluralin in Europe?

The EU’s Farm to Fork Strategy, part of the broader Green Deal, aims to reduce the use and risk of chemical pesticides by 50% by 2030. This initiative has intensified pressure on regulators to reassess older compounds like Trifluralin. While not outright banned yet, its long-term viability in the European market depends on compliance with new safety standards and the development of formulations that minimize environmental impact.

What impact do consumer preferences have on the use of Trifluralin in Europe?

Consumer demand for organic produce and sustainable farming practices is influencing the decline in Trifluralin use. Farmers aiming for organic certification must avoid synthetic herbicides entirely. Even conventional producers are shifting toward safer alternatives to meet retailer and consumer expectations for reduced chemical residues in food and the environment.

Are there ongoing research efforts related to Trifluralin in Europe?

Several European research institutions and agricultural universities are studying the long-term effects of Trifluralin on soil microbiota, water systems, and biodiversity. Some projects are exploring biodegradation techniques to neutralize residual herbicide in contaminated soils. Others are focused on developing bioherbicides or microbial solutions that could replace synthetic herbicides like Trifluralin.

What challenges do farmers face in transitioning away from Trifluralin?

Farmers often cite higher costs of alternative herbicides, lack of awareness about integrated weed management, and the need for specialized equipment as key challenges. In Eastern Europe, where adoption of modern agronomic practices is slower, there is still some reliance on older, cost-effective herbicides. Education and government subsidies are helping ease the transition, but progress varies by region.

What is the future outlook for the Trifluralin market in Europe?

The future outlook for Trifluralin in Europe is cautious. With tightening regulations, rising environmental awareness, and availability of safer alternatives, its market share is expected to shrink further. However, niche applications in certain crops or regions may sustain limited use for a few more years. Long-term survival will depend on reformulation efforts, improved safety profiles, and alignment with EU sustainability goals.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com