Europe Warehouse Automation Market Size, Share, Trends, & Growth Forecast Report By Component (Hardware, Software, Services), End-User Industry, Technology and Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic and Rest of Europe), Industry Analysis From 2025 to 2033

Europe Warehouse Automation Market Report Summary

The Europe warehouse automation market was valued at USD 5.92 billion in 2024, is estimated to reach USD 7.02 billion in 2025, and is projected to reach USD 27.41 billion by 2033, growing at a CAGR of 18.56% during the forecast period from 2025 to 2033. The growth of the Europe warehouse automation market is driven by persistent labor shortages, rising e-commerce penetration, increasing demand for same-day delivery, and the rapid digital transformation of logistics infrastructure across the region. The adoption of robotics, automated storage and retrieval systems, and intelligent warehouse software is accelerating as logistics operators seek higher throughput, improved accuracy, and lower operational dependency on manual labor. Additionally, strong institutional support through EU digitalization initiatives and Industry 4.0 programs is reinforcing the shift toward automated fulfillment environments.

Key Market Trends

- Increasing deployment of autonomous mobile robots and goods-to-person systems to address workforce shortages.

- Rising adoption of AI-enabled warehouse management and execution software for real-time orchestration.

- Growing investment in urban micro-fulfillment centers to support same-day and hyperlocal delivery models.

- Expansion of modular and retrofit-friendly automation solutions for existing warehouse infrastructure.

- Strong focus on energy efficiency and sustainability through electric robotics and optimized material flow systems.

Segmental Insights

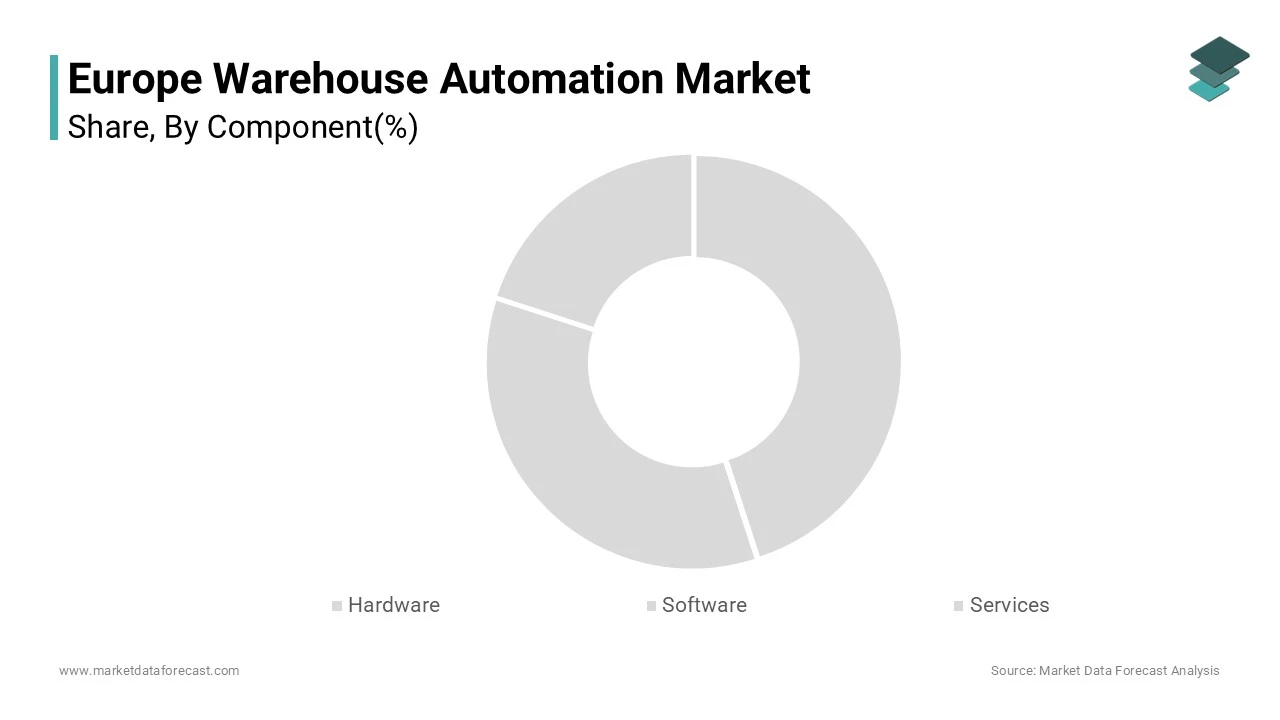

- Based on component, the hardware segment held the largest share of the Europe warehouse automation market in 2024. The dominance of this segment is attributed to the essential role of physical equipment such as conveyors, automated guided vehicles, robotic picking systems, and sortation units in enabling warehouse automation. Most automation projects across Europe begin with large-scale hardware installations before integrating advanced software layers.

- Based on end-user industry, the post and parcel segment accounted for the largest share of the Europe warehouse automation market in 2024. This segment’s leadership is driven by rapidly growing parcel volumes, cross-border e-commerce activity, and regulatory delivery-time requirements that necessitate high-speed automated sortation and handling systems.

- Based on technology type, the automated guided vehicles (AGV) segment held a significant market share in 2024 due to their long-established use in structured industrial environments such as automotive and manufacturing logistics. However, the autonomous mobile robots (AMR) segment is expected to grow at the fastest rate during the forecast period, supported by its flexibility, faster deployment, and suitability for dynamic e-commerce fulfillment operations.

Regional Insights

- Germany was the largest contributor to the Europe warehouse automation market in 2024, supported by strong manufacturing activity, high labor costs, and extensive adoption of Industry 4.0 technologies. The country’s advanced engineering ecosystem and public-private collaboration continue to accelerate automation adoption.

- The United Kingdom holds a prominent position in the European market, driven by high e-commerce penetration, advanced grocery fulfillment models, and strong investments in automated distribution centers, particularly in pharmaceutical and retail logistics.

- France is witnessing steady growth due to state-led digital transformation programs, increasing urban logistics demand, and automation adoption across postal, retail, and food distribution networks.

- The Netherlands plays a strategic role as a logistics gateway for Europe, with automation driven by port operations, sustainable logistics initiatives, and advanced fulfillment hubs supporting cross-border trade.

- Italy is emerging as a high-growth market, supported by fashion e-commerce, food exports, and government funding programs aimed at modernizing small and medium-sized logistics operators.

Competitive Landscape

The Europe warehouse automation market is characterized by intense competition among global system integrators, established European engineering firms, and rapidly growing robotics startups. Market participants are focusing on delivering end-to-end automation solutions that combine hardware, intelligent software, and lifecycle services. Strategic acquisitions, partnerships with e-commerce and logistics providers, and investments in AI-driven orchestration platforms are strengthening competitive positioning. Compliance with EU safety, machinery, and cybersecurity regulations has become a critical differentiator, while demand for scalable and interoperable solutions continues to shape vendor strategies. Prominent players operating in the Europe warehouse automation market include Swisslog Holding AG (KUKA AG), SSI Schaefer AG, TGW Logistics Group GmbH, KNAPP AG, Vanderlande Industries B.V., Dematic GmbH (KION Group AG), WITRON Logistik + Informatik GmbH, AutoStore Holdings Ltd., Ocado Group plc, Exotec SAS, Mecalux S.A., Körber Supply Chain GmbH, Geekplus Technology Co. Ltd., Locus Robotics Inc., GreyOrange Pte. Ltd., and Jungheinrich AG.

Europe Warehouse Automation Market Size

The europe warehouse automation market size was valued at USD 5.92 billion in 2024 and is anticipated to reach USD 7.02 billion in 2025 from USD 27.41 billion by 2033, growing at a CAGR of 18.56% during the forecast period from 2025 to 2033.

Warehouse automation includes technologies and integrated systems designed to streamline storage retrieval sorting and inventory management processes within logistics facilities through robotics software and data driven control mechanisms. Unlike traditional warehousing, automation in this context reduces manual intervention while enhancing throughput accuracy and energy efficiency. As of 2025, as per the European Materials Handling Federation, a majority of large logistics operators in Western Europe have deployed some form of automation, ranging from conveyor systems to autonomous mobile robots. The urgency to adopt such solutions stems from structural labour shortages and rising consumer expectations for delivery speed. According to the Fraunhofer Institute for Material Flow and Logistics, automated European fulfillment centers achieve significantly faster order processing times compared to manual facilities, which indicates the efficiency gains of automation. Furthermore, the European Union’s Digital Europe Programme has allocated billions of euros since 2021 to support the integration of smart logistics technologies in small and medium enterprises (SMEs), which is signalling institutional commitment to operational modernization across the supply chain.

MARKET DRIVERS

Persistent Labor Shortages Accelerate Adoption of Robotic Fulfillment Systems

Europe’s logistics sector faces a critical deficit in available and reliable manual labor, which is directly compelling warehouse operators to turn to automation as a structural solution rather than a performance enhancer and driving the warehouse automation market growth in Europe. According to the European Labour Authority’s 2024 Labour Shortages Report, transport and storage consistently rank among the top five sectors facing acute vacancies across the EU, with Germany highlighted as one of the most affected countries. This gap has widened due to demographic aging, with workers over 55 now representing as per Eurostat (2024) nearly one‑third of the sector’s workforce. In response, companies are deploying goods‑to‑person robotics and automated storage and retrieval systems to maintain operational continuity. For example, a typical automated fulfillment center in the Netherlands reduces direct labor requirements by 40 to 60% while increasing picking accuracy to 99.9% according to the Dutch Logistics Association. The trend is particularly acute in Southern Europe, where seasonal labor turnover exceeds 30% annually, making consistent service levels nearly impossible without technological intervention. Automation thus serves not merely as a cost optimization tool but as a necessity for baseline functionality in an increasingly constrained labor environment.

Rising Consumer Expectations for Same‑Day and Hyperlocal Delivery

European consumers now expect faster and more precise delivery windows, which is fundamentally reshaping warehouse throughput requirements and driving investment in high‑speed automation and fuelling the regional market expansion. According to a 2024 ECB Consumer Expectations Survey, euro area households increasingly demand shorter delivery times, with delays beyond 24 hours cited as a key factor in switching retailers. This shift has intensified pressure on fulfillment centers to process orders in under 30 minutes from receipt to dispatch. Automated sortation systems and robotic pick walls now enable facilities in cities like Berlin and Copenhagen to handle according to the International Federation of Robotics (2024) more than 10,000 orders per hour during peak periods, a volume unattainable with manual labor alone. Moreover, retailers such as Zalando and Ocado have embedded AI‑driven demand forecasting with real‑time robotic task allocation, reducing average dispatch latency by more than 50%. These performance benchmarks have redefined competitive viability, making automation indispensable for any player targeting urban e‑commerce dominance.

MARKET RESTRAINTS

High Initial Capital Expenditure Deters Small and Medium Enterprises

The substantial upfront investment required for comprehensive warehouse automation is majorly hindering the European warehouse automation market growth. For instance, full‑scale automation projects in Europe can cost between €8 million and €15 million for a mid‑sized facility, excluding recurring expenses for maintenance and retraining. For context, as per Eurostat (2024), more than 90% of logistics firms in the EU employ fewer than 50 people and operate on annual revenues below €10 million. These entities lack access to the capital markets enjoyed by large real estate investment trusts or multinational retailers, rendering full automation economically unfeasible. While modular and pay‑per‑use automation models are emerging, they remain limited in scale and functionality. Consequently, many SMEs continue to rely on semi‑automated solutions like conveyors or voice picking, which deliver incremental rather than transformative gains, thereby perpetuating a two‑tier market structure that entrenches competitive disparity.

Interoperability Gaps Between Legacy Systems and Modern Automation Platforms

Many existing warehouses across Europe were constructed before 2010 and operate on legacy warehouse management systems that lack the application programming interfaces necessary to integrate with contemporary robotic or AI‑driven automation platforms, which is further impedes the regional market expansion. According to Gartner’s 2024 Magic Quadrant for Warehouse Management Systems, a significant share of European warehouses still relies on ERP systems developed prior to 2012, limiting real‑time data exchange with modern orchestration engines. This technological misalignment forces operators to choose between costly full system overhauls or maintaining siloed operations where automated and manual processes run in parallel, reducing overall efficiency. For instance, a logistics provider in Italy reported a 20% increase in mis-shipments after partially automating picking without upgrading its core inventory database as documented in a case study by the Politecnico di Milano. Until standardized middleware solutions gain wider adoption, interoperability constraints will continue to delay or dilute automation benefits for a significant portion of the European logistics base.

MARKET OPPORTUNITIES

Repurposing Underutilized Industrial Buildings with Modular Automation

Europe’s vast inventory of vacant or underused industrial structures is a strategic opportunity to the European warehouse automation market. According to BNP Paribas Real Estate’s European Logistics Market Report (2024), more than 8.8 million square meters of warehouse space was taken up in the first half of 2024, highlighting both demand and the potential of repurposed industrial assets. These sites often feature high ceiling clearances, robust floor load capacities, and existing utility infrastructure, making them ideal for modular automation systems such as mobile robot fleets and plug‑and‑play sortation lines. In 2024, the city of Turin approved a fast‑track permitting process for logistics retrofits that include automation, reducing approval timelines from 14 months to under five as per the Turin Metropolitan Development Authority. Companies like AutoStore and Geek+ have capitalized on this trend by offering containerized automation pods that can be installed within eight weeks. This approach not only accelerates time to market but also aligns with circular economy principles by extending the life cycle of existing buildings while meeting modern fulfillment demands.

Integration of Artificial Intelligence for Predictive Warehouse Operations

The convergence of artificial intelligence with warehouse automation is another potential opportunity for the European warehouse automation market. According to DHL Supply Chain (2025), AI‑driven workload forecasting in its Leipzig facility reduced idle robotic time by 30% and cut energy consumption by nearly 20%. Similarly, as per Ocado Intelligent Automation (2024), reinforcement learning and dynamic task allocation boosted throughput during peak hours by more than 25%. These capabilities transform automation from a static efficiency tool into a responsive nervous system for the warehouse. As cloud‑based AI services become more accessible through partnerships with firms like SAP and Microsoft, even mid‑sized operators can adopt predictive intelligence without building in‑house data science teams, democratizing next‑generation automation.

MARKET CHALLENGES

Cybersecurity Vulnerabilities in Connected Automation Ecosystems

As warehouse automation systems become increasingly interconnected through Internet of Things sensors, cloud‑based control platforms, and real‑time data feeds and they present expanded attack surfaces for cyber threats, which is a notable challenge to the warehouse automation market expansion in Europe. According to ENISA’s 2024 Report on the State of Cybersecurity in the Union, attempted intrusions targeting industrial control systems rose significantly, with ransomware incidents disrupting logistics operations across multiple EU member states. Unlike isolated machinery, modern automated warehouses rely on continuous communication between robots, warehouse management software, and external enterprise systems, meaning a single compromised node can halt entire operations. A cyberattack on a Swedish e‑commerce fulfillment center in late 2024 encrypted robotic fleet coordinates and inventory data, causing a five‑day shutdown and estimated losses of €12 million as reported by the Swedish Civil Contingencies Agency. Most small logistics operators lack dedicated cybersecurity personnel, and standard automation vendors rarely include enterprise‑grade security protocols by default. Until cybersecurity becomes a mandatory component of automation procurement and certification, the digitalization of warehousing will remain inherently exposed to operational and financial disruption.

Regulatory Uncertainty Around Autonomous Mobile Robots in Shared Workspaces

The deployment of autonomous mobile robots alongside human workers in European warehouses is hindered by inconsistent and evolving occupational safety regulations across member states, which is further challenging the warehouse automation market growth in Europe. While the European Machinery Regulation sets baseline safety requirements, national labor inspectorates interpret human‑robot interaction rules differently, creating compliance ambiguity for pan‑European operators. According to VTT Technical Research Centre of Finland (2024), the updated Machinery Regulation (EU 2023/1230) introduced baseline requirements for autonomous mobile machines, but detailed national guidelines vary widely. For example, France mandates physical separation barriers for all mobile robots operating at speeds above 0.5 meters per second, whereas Germany permits collaborative operation under dynamic geofencing as long as risk assessments are updated quarterly according to the Federal Institute for Occupational Safety and Health. This fragmentation complicates standardization of automation rollouts and increases legal risk. In 2024, a logistics provider halted robot deployment in four Southern European countries after conflicting rulings on emergency stop requirements delayed facility certifications. Moreover, the absence of EU‑wide standards for robot behavior in emergency scenarios—such as fire evacuations or power failures further deters investment. Until harmonized safety frameworks for human‑robot collaboration are codified, adoption of flexible mobile automation will remain uneven and legally precarious

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| Segments Analysed | By Component, End-User Industry, Technology Type, Warehouse Size and Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter's Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Analysed | United Kingdom, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, the Netherlands, Turkey, and the Czech Republic. |

| Market Leaders Profiled | Swisslog Holding AG (KUKA AG), SSI Schaefer AG, TGW Logistics Group GmbH, KNAPP AG, Vanderlande Industries B.V., Dematic GmbH (KION Group AG), WITRON Logistik + Informatik GmbH, AutoStore Holdings Ltd., Ocado Group plc, Exotec SAS, Mecalux S.A., Körber Supply Chain GmbH, Geekplus Technology Co. Ltd., Locus Robotics Inc., GreyOrange Pte. Ltd., and Jungheinrich AG. |

SEGMENTAL ANALYSIS

By Component Insights

The hardware segment occupied 57.5% of the European warehouse automation market share in 2024. This dominance of hardware segment in the European market can be credited to the foundational role of physical automation equipment, such as conveyors, robotic arms, automated guided vehicles and sortation systems in enabling core operational transformation. Automation in European warehouses begins with the installation of tangible machinery, as software and services cannot function without compatible hardware platforms. According to the German Engineering Federation (VDMA), more than 70% of new automation projects in Western Europe in 2024 began with procurement of robotic picking arms or mobile transport systems. For instance, a typical e‑commerce fulfillment center requires hundreds of autonomous mobile robots to achieve baseline throughput targets, representing multimillion‑euro hardware investments before software integration. Additionally, legacy facilities undergoing retrofitting prioritize hardware upgrades first, such as installing high‑density shuttle racking before layering on digital control systems. This sequential adoption pattern reinforces hardware’s continued market leadership.

The software segment is on the rise and is estimated to witness the fastest CAGR of 13.1% over the forecast period owing to the Shift toward intelligent orchestration over mechanical execution. European operators are increasingly prioritizing software that enables intelligent coordination of diverse hardware assets rather than merely acquiring more robots. According to the German Engineering Federation, nearly 68% of new automation deployments in Germany and the Netherlands in 2024 included AI‑powered warehouse control software as the central orchestration layer. For example, Ocado’s proprietary OS manages thousands of robots simultaneously while minimizing congestion through predictive pathing, reducing average travel time by more than 20%. This intelligence layer transforms fixed hardware into adaptive systems, which is delivering exponential value from the same physical assets. As a result, software budget allocation is rising faster than hardware spend.

By End User Industry Insights

The post and parcel segment led the European warehouse automation market in 2024 by holding 33.9% of the regional market share in 2024. The dominance of post and parcel segment in the European market is attributed to the sector’s extreme volume volatility and regulatory pressure to modernize last mile networks. According to the Universal Postal Union, cross‑border parcel volumes within the European Union reached more than 6 billion units in 2024, which is marking a near 20% increase compared to 2022. National postal operators and private couriers like DHL and La Poste face unprecedented sorting demands that manual labor cannot meet. Automated cross‑belt sorters now process tens of thousands of parcels per hour in major hubs such as Leipzig and Roissy, achieving sortation accuracy above 99%. Without such throughput, compliance with EU delivery time mandates, such as 48‑hour domestic and 72‑hour intra‑EU standards would be impossible. This regulatory and volume pressure has made automation non‑optional for all major postal networks.

The food and beverage segment is the fastest growing end user segment in the Europe warehouse automation market and is expected to record a CAGR of 13.08% over the forecast period owing to the stringent cold chain integrity requirements drive specialized automation. According to the European Cold Chain Federation, more than half of frozen food distribution centers in Germany and Scandinavia in 2024 deployed robotic palletizing and shuttle‑based AS/RS systems to minimize door openings and human presence in cold zones. These systems reduce temperature deviation incidents by up to 70% compared to manual handling. Furthermore, EU Regulation 852/2004 mandates traceability and hygiene compliance, which automated barcode and vision systems enforce more reliably than manual logs. Companies like Nestlé and Danone now require certified automated handling for all chilled logistics partners, which is creating vendor pull.

By Technology Type Insights

The automated guided vehicles segment held the largest technology segment share in the Europe warehouse automation market at 29.5% in 2024. The leading position of automated guided vehicles segment in the European market is attributed to the decades of industrial integration and proven reliability in structured environments. Automation Monitor, more than 60% of AGV deployments in 2024 occurred in facilities built before 2010. Automotive and heavy industrial sectors, which is still reliant on linear material flow prefer AGVs for their deterministic paths and minimal software complexity. For example, Volkswagen’s logistics center in Wolfsburg uses over 300 AGVs on magnetic tracks to move engine blocks with zero deviation, a reliability unattainable with newer autonomous systems in such high precision contexts. This compatibility ensures AGVs remain the default choice for industries prioritizing stability over flexibility.

The autonomous mobile robots segment the fastest growing technology segment in the Europe warehouse automation market and is predicted to grow at a CAGR of 22.8% over the forecast period. According to the European E‑Commerce Logistics Council, nearly three‑quarters of new automation projects in urban fulfillment centers in 2024 selected AMRs over AGVs. For instance, Zalando’s Berlin micro hub deployed 120 AMRs in three weeks to handle seasonal spikes, reconfiguring workflows weekly based on demand, which is something impossible with fixed path AGVs. This agility is critical in high churn retail environments where layout changes are frequent.

REGIONAL ANALYSIS

Germany Warehouse Automation Market Analysis

Germany occupied the leading position in the Europe warehouse automation market in 2024 due to the advanced manufacturing, engineering excellence, and strong public‑private collaboration on Industry 4.0. According to the Federal Ministry for Economic Affairs, the Plattform Industrie 4.0 program has supported hundreds of logistics digitization projects since 2020. As per the International Federation of Robotics, Germany hosts Europe’s highest density of robotic installations, with over 250,000 industrial robots in operation in 2023. Automotive and machinery sectors require ultra‑precise automated material handling, which is driving demand for high‑end AGVs and AS/RS systems. According to Eurostat, Germany’s average hourly labor costs were among the highest in Europe in 2024, incentivizing automation investment. Major logistics hubs in the Rhine‑Ruhr and Munich regions now feature fully automated cross‑docking facilities, setting continental benchmarks for efficiency.

United Kingdom Warehouse Automation Market Analysis

The United Kingdom holds a prominent position in the Europe warehouse automation market, with strength in e‑commerce innovation, pharmaceutical logistics, and agile technology adoption despite post‑Brexit trade complexities. According to the Office for National Statistics, online retail penetration in the UK was the highest in Europe in 2024, driving automation in fulfillment centers. Ocado’s Andover Customer Fulfilment Centre operates thousands of robots in a grid‑based AS/RS system, achieving tens of thousands of orders per week with near‑perfect accuracy. As per the Association of the British Pharmaceutical Industry, UK pharmaceutical exports exceeded £40 billion in 2023, with automated storage systems critical for compliance with MHRA regulations. According to the UK government’s Made Smarter program, more than 2,000 SMEs have received support for automation adoption since 2021.

France Warehouse Automation Market Analysis

France commands a strong share of the Europe warehouse automation market. The growth of France in the European warehouse automation market is driven by the state‑led digital transformation, urban logistics demands, and retail automation. According to the Ministry of the Economy, the France 2030 investment plan allocated €1.5 billion to smart logistics infrastructure, including automated urban micro‑hubs in Paris, Lyon, and Marseille. As per La Poste’s 2024 sustainability report, its automated parcel facility in Roissy processes hundreds of thousands of parcels daily using robotic sorters, reducing manual handling significantly. France’s leadership in luxury goods and fresh food exports necessitates high‑integrity automated handling, with companies such as LVMH and Carrefour mandating automated case picking for premium product distribution. According to French labor regulations, restrictions on night shifts further accelerate automation, as robots operate continuously without compliance constraints.

Netherlands Warehouse Automation Market Analysis

The Netherlands plays a pivotal role in the Europe warehouse automation market. The Port of Rotterdam’s logistics gateway status and national leadership in sustainable automation are propelling the market growth in Netherlands. According to the Port of Rotterdam Authority, automated container terminals use fleets of automated guided vehicles and stacking cranes, enabling 24/7 operations with reduced energy consumption. Inland, logistics parks such as Rotterdam The Hague Airport Logistics Zone require automation readiness certifications for new warehouses. Companies like ASML and Philips drive demand for clean‑room compatible robotic systems that handle high‑value semiconductors and medical devices. As per TenneT, the Netherlands’ electricity grid is overwhelmingly renewable, making electric AMRs and automated systems more carbon‑efficient than in fossil‑fuel dependent regions.

Italy Warehouse Automation Market Analysis

Italy ranks among the top five European warehouse automation markets, with growth driven by fashion e‑commerce, food export logistics, and regional development funds targeting SME modernization. According to the Italian Fashion Chamber, leading fashion brands such as Benetton and Prada have automated regional distribution centers to manage high SKU complexity and seasonal volatility. As per ISTAT, Italy exported more than €50 billion worth of processed food in 2023, necessitating automated cold‑chain fulfillment. According to the National Recovery and Resilience Plan, hundreds of millions of euros have been allocated to subsidize automation for small logistics firms, with more than 1,000 projects approved by mid‑2024. These initiatives are transforming Italy from a manual logistics economy into an agile automated hub serving Southern Europe and North Africa.

COMPETITIVE LANDSCAPE

Competition in the Europe warehouse automation market is characterized by intense innovation rivalry between global integrators European engineering specialists and agile robotics startups. Leading firms differentiate through end to end system integration combining proprietary hardware with intelligent software while niche players focus on vertical specific solutions such as cold chain robotics or pharma compliant automation. The market is witnessing consolidation as larger players acquire AI and machine vision startups to enhance cognitive capabilities. Simultaneously open architecture trends are pressuring vendors to ensure interoperability rather than lock in. Regulatory alignment with EU Machinery Regulation and cybersecurity directives has become a critical competitive parameter. Talent acquisition in robotics software and systems engineering is another key battleground as demand outpaces supply. This dynamic environment fosters rapid technological advancement but also raises barriers for new entrants lacking domain expertise or service infrastructure.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the Europe Warehouse Automation Market include

- wisslog Holding AG (KUKA AG)

- SSI Schaefer AG

- TGW Logistics Group GmbH

- KNAPP AG

- Vanderlande Industries B.V.

- Dematic GmbH (KION Group AG)

- WITRON Logistik + Informatik GmbH

- AutoStore Holdings Ltd.

- Ocado Group plc

- Exotec SAS

- Mecalux S.A.

- Körber Supply Chain GmbH

- Geekplus Technology Co. Ltd.

- Locus Robotics Inc.

- GreyOrange Pte. Ltd.

- Jungheinrich AG

- Honeywell Intelligrated

Top Players in the Market

Dematic

Dematic is a global leader in intelligent warehouse automation solutions with deep integration across Europe’s e commerce retail and logistics sectors. The company designs and deploys advanced systems including automated storage and retrieval solutions robotic sortation and warehouse execution software. Dematic has significantly contributed to global automation standards through its modular and scalable technologies adopted by major retailers and third party logistics providers. In 2024 the company launched its next generation iQ software platform enhancing real time orchestration of mixed robotic fleets across temperature controlled and ambient environments. This innovation strengthens its position by enabling seamless interoperability and predictive task allocation in complex European fulfillment networks.

KION Group

KION Group is a prominent European provider of intralogistics solutions with a comprehensive portfolio spanning automated guided vehicles autonomous mobile robots and warehouse management software under its Dematic and Linde Material Handling brands. The company plays a pivotal role in advancing material flow automation across automotive food and beverage and e commerce industries globally. Recently KION accelerated its software driven strategy by enhancing its WMS and fleet management systems with cloud native architecture and AI powered analytics. These upgrades allow customers to dynamically scale automation in response to demand volatility while maintaining operational resilience across multi site European operations.

Schenck Process Group

Schenck Process Group has emerged as a specialized force in warehouse automation through its focus on intelligent material handling and bulk logistics solutions tailored for food pharmaceutical and chemical industries. While globally recognized for precision feeding and conveying systems the company has expanded its automation footprint in Europe by integrating robotic palletizing and automated guided cart systems into end to end warehouse workflows. In 2024 Schenck launched its LogiCare digital twin platform enabling predictive maintenance and performance simulation for automated material flow systems. This digital layer enhances system uptime and lifecycle value reinforcing its relevance in highly regulated European industrial supply chains.

Top Strategies Used by the Key Market Participants

Key players in the Europe warehouse automation market are prioritizing software centric solutions that unify diverse robotic hardware under intelligent orchestration platforms. They are investing in cloud based and modular architectures to enable scalable deployment for small and medium enterprises. Strategic partnerships with e commerce retailers and logistics service providers ensure co developed automation tailored to real world operational demands. Companies are also embedding sustainability into system design by optimizing energy consumption and supporting circular economy principles through retrofit compatible technologies. Finally they are expanding local engineering and support teams across Europe to ensure rapid implementation compliance with regional safety standards and post deployment service excellence.

MARKET SEGMENTATION

This research report on the europe warehouse automation market has been segmented and sub–segmented into the following categories.

By Component

- Hardware

- Software

- Services

By End-User Industry

- Food and Beverage

- Post and Parcel

- E-commerce and Groceries

- General Merchandise and 3PL

- Apparel and Footwear

- Manufacturing (Durable/Non-Durable)

- Other End-User Industries

By Technology Type

- Autonomous Mobile Robots (AMR)

- Automated Guided Vehicles (AGV)

- Cube-Based AS/RS (e.g., AutoStore)

- Shuttle-Based AS/RS

- Mixed-Case Palletizing Robotics

- Warehouse Software Suites (WMS/WES/WCS)

By Warehouse Size

- Small-Scale

- Mid-Scale

- Large-Scale

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

What is the Europe warehouse automation market?

The Europe warehouse automation market includes technologies and solutions such as robotics, automated storage systems, conveyors, and software used to automate warehouse operations across the region.

What factors are driving the growth of the Europe warehouse automation market?

Key drivers include the rapid growth of e-commerce, rising labor shortages, increasing demand for faster order fulfillment, and the need to reduce operational costs.

What types of solutions are included in warehouse automation?

Solutions include automated storage and retrieval systems (AS/RS), mobile robots (AGVs and AMRs), conveyors and sortation systems, palletizing systems, and warehouse management software.

Which industries are the major adopters of warehouse automation in Europe?

Major adopters include e-commerce and retail, food and beverage, post and parcel, manufacturing, third-party logistics (3PL), and apparel and footwear industries.

What role do robotics play in warehouse automation?

Robotics improves picking, packing, sorting, and material transport efficiency while reducing human error and dependency on manual labor.

How does warehouse automation support e-commerce growth in Europe?

Automation enables faster order processing, higher accuracy, same-day delivery capabilities, and efficient handling of high order volumes.

What challenges does the Europe warehouse automation market face?

High initial investment costs, system integration complexity, cybersecurity risks, and lack of skilled workforce are key challenges.

What is the difference between AGVs and AMRs?

AGVs follow fixed paths using guides or markers, while AMRs use sensors and AI to navigate dynamically, offering greater flexibility.

Which countries are leading the Europe warehouse automation market?

Germany, the United Kingdom, France, Italy, and the Netherlands are leading countries due to strong industrial and logistics infrastructure.

What is the future outlook for the Europe warehouse automation market?

The market is expected to grow steadily during the forecast period due to technological advancements and expanding logistics and retail sectors.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com